EMEA Structured Finance Chart Book - UPDATE - S&P Global

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

EMEA Structured Finance Andrew South

Casper Andersen

Antonio Farina

Mathias Herzog

Chart Book

Alastair Bigley Volker Laeger

Sandeep Chana

July 2021

UPDATE

Highlights—News

– Issuance. Investor-placed securitization issuance was up 60% year-to-date at the end of June, to €52 billion. While 2020 may be a

flattering basis for comparison, issuance this year is also almost on a par with the same point in 2018, when volumes eventually hit a

post-2008 record by year-end. Strong growth in CLO refinancing and reset activity has added a further €35 billion to volumes. By contrast,

European benchmark covered bond issuance was down by 38% in the first half of the year, at €40 billion. Continued high growth in bank

deposits and ample availability of cheap central bank funding has reduced covered bond issuers’ wholesale funding needs.

– Rating actions. In June 2021, we only lowered one rating on a European structured finance security, while there were 17 upgrades spread

among eight ABS and RMBS transactions. In the year to mid-2021, we have lowered only about 3% of our European structured finance

ratings.

– Regulation. The European Banking Authority (EBA) has launched a consultation on sustainable securitizations. The regulator’s mandate

resulted from recent updates to the Securitization Regulation. The EBA is looking for insights on current market practices and potential

challenges to developing a sustainable securitization market; the business need, relevance, and potential content of an EU framework for

the sector; and the potential risk profile of sustainable securitizations compared with similar “non-sustainable” transactions.

– Dutch buy-to-let RMBS. Recent issuance included the first Dutch buy-to-let (BTL) RMBS transaction to carry the EU’s “simple,

transparent, and standardized” label: Domi 2021-1 B.V. The senior notes priced at the joint-tightest spread for a European BTL RMBS

since 2008: +63 basis points. However, Dutch BTL lending faces increasing political risk, with some municipalities looking to prevent

investors purchasing newly completed properties. This comes on top of a recent hike in stamp duty for BTL investors, who must now pay

an 8% levy on purchases. Although private residential renting is not new in the Netherlands, the relatively high population density

combined with low rates and increased demand from property investors has pushed property prices up 11.5% since June 2020, according

to the Dutch Central Bank. This has put home ownership out of reach for some and turned BTL into a political issue. Measures announced

so far would have a limited effect on existing BTL RMBS but signify growing political risk in the sector that will be worth monitoring.

2Highlights—Green Mortgages And Green RMBS: What Are The

Challenges?

Sustainable Finance Timelines

– As policymakers legislate toward long-term

climate-neutrality targets, more economic

activities are being viewed through a

sustainability lens, including residential

property ownership and financing.

– Green mortgages can take two forms: a

traditional loan financing the purchase of an

energy-efficient property, or a further

advance to fund energy-related home

improvements, such as solar panels,

insulation, or boiler upgrades.

– So far, there have several approaches to

green RMBS, including securitizations where

the collateral comprises green properties

exclusively or transactions where the

collateral is not green, but there is a

commitment to use the proceeds to originate

green mortgages over time.

Source: S&P Global Ratings. For more details, see “Credit FAQ: Green Mortgages And Green RMBS – What Are The Challenges?,” published June 28, 2021.

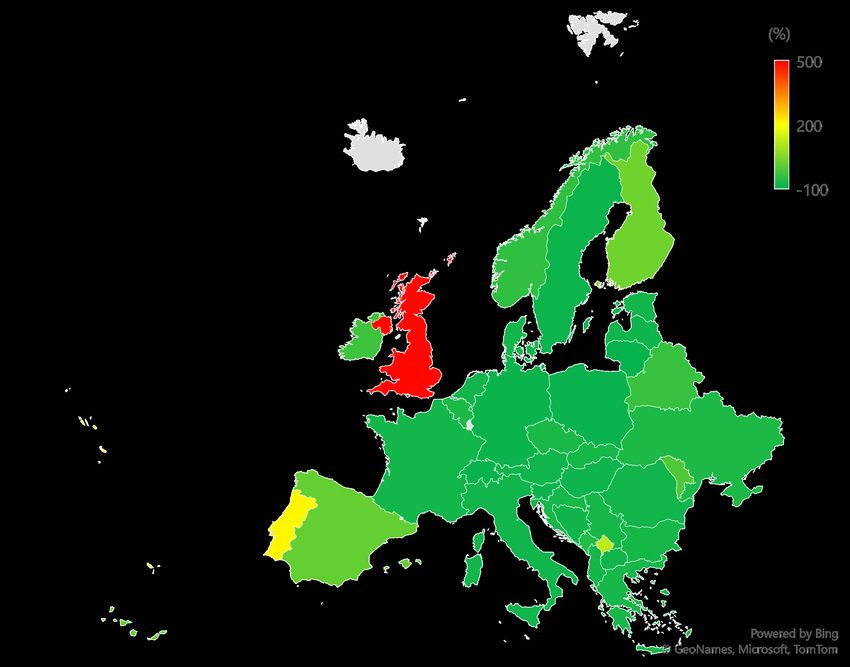

3Highlights—European RMBS Update

British Pound Sterling Five-Year Swap Rate Evolution

– High excess spread levels in recent U.K.

1.0

RMBS issuances may have peaked, as swap

0.9 rates increase and asset margins decline

due to increased competition.

0.8

– Loan-level analysis of U.K. mortgage lending

0.7

shows that origination standards were

0.6 generally maintained in 2020, with no

0.5 significant increase in risk layering.

%

0.4

– The Dutch BTL market is facing political

pressure, with sharp increases in stamp duty

0.3

for newly purchased investment properties.

0.2 – Generally, the European payment holiday and

0.1 government salary support schemes will

continue to mid-2021 and we do not expect

0.0

material RMBS collateral performance

Mar-20

Jul-20

Nov-20

Feb-20

Apr-20

Dec-20

May-20

Feb-21

Jun-20

Jan-20

Sep-20

Oct-20

Jan-21

Aug-20

movements in the short term.

Source: S&P Global Ratings. For more details, see “European RMBS Market Update Q1 2021,” published May 11, 2021.

4Highlights—U.K. Buy-To-Let Market Primer

Key Figures

– The U.K. BTL market, which turns 25 years

old this year, has developed significantly

since its inception, particularly relating to the

products on offer.

– In recent years, the performance of BTL

collateral has been positive, with total

arrears at less than 1% (with the majority of

delinquent loans in the early stages of

arrears).

– BTL RMBS transactions are more likely to

contain nuanced property types, such as

houses in multiple occupations (HMOs) or

multi-unit freehold blocks.

– As well as the usual methods of servicing

defaulted loans, BTL servicers can also use

the concept of "receiver of rent".

Source: S&P Global Ratings. For more details, see “S&P Global Ratings’ U.K. Buy-To-Let Market Primer,” published June 1, 2021.

5Highlights—Period Of Maximum Liquidity Stress May Have Passed

For U.K. Pub Corporate Securitizations

Available Sources Of Liquidity

Liquidity facility/reserve funds Cash accounts* – Following a third national lockdown in

350

England, the U.K. government allowed pubs

to re-open for indoor service from May 17.

300

– Over the next 12 to 24 months, we expect

250 earnings visibility to remain low as the sector

Available amount (Mil. £)

grapples with several issues, with full-year

200 revenue recovering to 2019 levels only by

2022.

150 – Our break-even analysis points to ratings

stability in the face of positive developments

100 that reduce the likelihood of future

nationwide lockdowns in England and put

50 the U.K. government in a position to take

further, non-regressive, steps toward easing

0 restrictions over the coming months.

Mitchells & Butlers Greene King Finance Unique Pub Finance Marston's Issuer PLC Spirit Issuer PLC

Finance PLC PLC Co PLC

Source: S&P Global Ratings. For more details, see “Period Of Maximum Liquidity Stress May Have Passed For U.K. Pub Corporate Securitizations,” published May 24, 2021.

6Highlights—Property In Transition: Zooming In On The Global Office

Reboot

Office Space Demand In Europe Is Below The Five-Year Average In All Major Markets

Paris London Berlin Madrid Barcelona – Given the growth in remote working, office

3000

landlords will face higher vacancy rates,

demands for greater environmental quality,

Total office take-up (000 square meters)

2500 and more flexible lease terms.

– Still, for key office markets globally, we

2000 expect recovery to a new normal.

– These trends are reflected in recovering

1500 investor appetite for office-related assets

including CMBS and REIT debt and equity,

while bank exposure to CRE debt remains

1000

broadly manageable.

– A prolonged recovery in office real estate

500

could hurt local government revenues, both

directly through lower property-related tax

0 income and more broadly through, for

2015 2016 2017 2018 2019 2020 5-year average

example, lower income from related

transportation sector income.

Source: S&P Global Ratings. For more details, see “Property In Transition: Zooming In On The Global Office Reboot,” published May 6, 2021.

7Contents

– Issuance 9

– Credit Performance 11

– Fundamentals 13

– RMBS 15

– ABS 18

– Structured Credit 21

– CMBS 24

– Covered Bonds 27

– Recent Research 30

8Issuance—Securitizations

1. Investor-Placed Securitization Issuance 2. 2021 YTD Investor-Placed Securitization Issuance, By Sector

(Bil. €) Year to date Rest of year YTD deal count (right scale) (Bil. €) 2.1

U.K. RMBS

120 120 15.3 Dutch RMBS

100 100 Securitization 13.8

Other RMBS

80 80 issuance in H1 2021

German ABS

was up by 60% on

60 60 the previous year U.K. ABS

40 40 Other ABS

20 20 3.7

CLO

0 0 6.7

3.7 CMBS

2013 2014 2015 2016 2017 2018 2019 2020 2021 1.8 4.7

3. Cumulative Investor-Placed Securitization Issuance 4. CLO Refinancing And Reset Issuance

(Bil. €) 2019 2020 2021 (Bil. €) New issue Refi/reset

120 40

100

30

80

60 20

40

10

20

0 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2013 2014 2015 2016 2017 2018 2019 2020 2021 YTD

1-3. Year-to-date (YTD) figures as of end-June each year. Excludes CLO refinancings and resets. Source: S&P Global Ratings. 4. Source: S&P Global Ratings, S&P LCD.

9Issuance—Covered Bonds

1. Benchmark Covered Bond Issuance 2. 2021 YTD Benchmark Covered Bond Issuance, By Country

(Bil. €) Year to date Rest of year YTD deal count (right scale) (Bil. €) 5.3 France

150 150 1.0 12.3 Germany

Covered bond 1.5 Norway

issuance in H1 2021

100 100 2.0 U.K.

was down by 38%

on the previous year 2.2 Italy

50 50 Netherlands

5.5 Sweden

0 0

10.3 Other

2013 2014 2015 2016 2017 2018 2019 2020 2021

3. Cumulative Benchmark Covered Bond Issuance 4. Change In YTD Issuance, 2021 Vs. 2020, By Country

(Bil. €) 2019 2020 2021 Norway

140 Sweden

120 Italy

100 Netherlands

Germany

80

Spain

60

Other

40

U.K.

20

France

0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec (Bil. €) (12) (10) (8) (6) (4) (2) 0 2 4

1-4. Year-to-date (YTD) figures as of end-June each year. Source: S&P Global Ratings.

10Credit Performance—Long-Term Ratings Drift

Rating Action Count, 12-Month Rolling 12-Month Trailing Average Change In Credit Quality

(000) Upgrade Downgrade* Default (Notches) ABS CMBS RMBS SC Overall

2 1

1

0

0

1 (1)

2 Recent downward

ratings migration has

(2)

mostly been confined

3 to the CMBS sector

4 (3)

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

* Excluding defaults. Excludes covered bonds. Source: S&P Global Ratings. As of end-March 2021. SC--Structured credit. Securities whose ratings migrated to 'NR' over the period

are classified based on their rating prior to 'NR'. Source: S&P Global Ratings.

11Credit Performance—Ratings Heatmaps

Distribution Of Ratings And 12-Month Transitions CreditWatch Placements And Resolutions, Last 12 Months

Upgrades Downgrades CCC/CC B BB BBB A AA AAA Downgraded Affirmed Remain on CreditWatch negative

100%

RMBS Structured Credit ABS CLO

Other SC

75% Buy-to-let RMBS

Other ABS

50% Corp. Sec.

Repack

Prime RMBS

25%

Auto

CMBS

0% Nonconforming RMBS

CLO

Other SC

conforming

Other RMBS

Repack

Prime

Auto

Other ABS

BTL

Corp. Sec.

CMBS

Non-

Other RMBS

0 5 10 15

BTL--Buy-to-let. SC--Structured credit. Based on rating transitions over the previous 12 months as of SC--Structured credit. Classified CreditWatch negative actions over the 12 months to end-June 2021

end-June 2021. Excludes confidential ratings and covered bonds. Source: S&P Global Ratings. based on subsequent resolution. Source: S&P Global Ratings.

12Fundamentals—Issuance Drivers

12-Month Lending & Deposit Growth, Eurozone Real Economy Eurozone Credit Institutions’ Use Of Central Bank Funding

Loans Deposits LTRO MRO

12 2.5

Rates of both deposit and loan Eurozone financial institutions’

10 book growth are beginning to use of term funding from central

normalize for eurozone banks, 2.0 banks has ticked higher once

although the gap still suggests again

8 limited wholesale funding needs

1.5

6

(Tril. €)

(%)

4

1.0

2

0.5

0

(2) 0.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Real economy includes households and nonfinancial corporates. Source: European Central Bank. LTRO—Long-term refinancing operations. MRO—Main refinancing operations. Source: European Central

Bank.

13Fundamentals—COVID-19 And Related Restrictions

1. Monthly Growth/(Decline) In New Cases, June 2021 2. Daily New Cases Vs. Vaccine Rollout

U.S. U.K. European Union South America Asia

New cases per million

1,000

800

600

400

The U.K. and Portugal are 200

currently outliers in Europe, 0

seeing renewed growth in 0 10 20 30 40 50 60 70

COVID-19 case numbers

Share of population that received at least one vaccine dose (%)

Traffic to recreational sites is

3. Retail And Recreation Mobility almost back to pre-pandemic levels

U.K. Germany France Italy Spain

20

0

(20)

(40)

%

(60)

(80)

(100)

Mar-20

Jul-20

Nov-20

Apr-20

Dec-20

Mar-21

Jul-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-20

Oct-20

Jan-21

Aug-20

1. Based on seven-day new case counts. Source: Our World In Data. 2. Latest data as of July 6, 2021. Source: Our World In Data, S&P Global Ratings. 3. Change in seven-day trailing average vs. Feb. 2020 benchmark. Latest

data as of July 3, 2021. Source: Google LLC “Google COVID-19 Community Mobility Reports”.

14RMBS Alastair Bigley Senior Director +44 20 7176 3245 alastair.bigley@spglobal.com

RMBS—Issuance

Investor-Placed RMBS Issuance 2021 YTD Investor-Placed RMBS Issuance, By Subsector

(Bil. €) Year to date Rest of year (Bil. €) 0.6 0.4

2.7

40

U.K.

30 Netherlands

3.7 Ireland

20

26.3 France

10 22.2 23.6 22.8

15.2 18.6 17.6 15.3 Spain

12.6 12.6 12.8

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Cumulative Investor-Placed RMBS Issuance RMBS Issuance Mix, By Originator Type

(Bil. €) 2019 2020 2021 Non-bank Bank

40 100%

30 80%

60%

20

40%

10 20%

0 0%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Year to date (YTD) figures as of end-June each year. Source: S&P Global Ratings.

16RMBS—Rating Actions & Performance Metrics

1. Monthly Rating Actions Count, Last 24 Months 2. Cumulative Rating Actions Count, Last 12 Months

Default Downgrade CreditWatch negative Upgrade Prime Nonconforming BTL Other RMBS

100

80

Upgrade 191 12 2 4

60

40

20 CreditWatch Neg. 1 0 5 0

0

20 Downgrade 7 3 1 1

Jul-19

Nov-19

Dec-19

Mar-20

Jul-20

Nov-20

Feb-20

Apr-20

Dec-20

Mar-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-19

Oct-19

Jan-20

Sep-20

Oct-20

Jan-21

Aug-19

Aug-20

Default 1 0 0 0

3. Average Total Arrears Rate 4. Latest Annualized House Price Growth

U.K. prime U.K. BTL Italy

(%) Netherlands

Netherlands Spain U.K. nonconforming

8 14 U.K.

6 13 Ireland

4 12

Italy

2 11

Spain

0 10

Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20 Dec-20 (%) 0 2 4 6 8 10 12 14

1. Excludes confidential ratings. Source: S&P Global Ratings. 2. BTL--Buy-to-let. Excludes confidential ratings. Source: S&P Global Ratings. 3. Source: S&P Global Ratings. 4. To May 2021. Source: National statistical

offices, Nationwide (U.K.).

17ABS

Volker Laeger

Senior Director

+49 69 3399 9302

volker.laeger@spglobal.comABS—Issuance

Investor-Placed ABS Issuance 2021 YTD Investor-Placed ABS Issuance, By Subsector

(€ bil.) Year to date Rest of year (€ bil.)

40 3.7 German auto

4.1

French auto

30

U.K. auto

20 Other auto

0.4

10 U.K. cards

14.6 16.1 12.5 16.4 13.2

8.1 9.6 8.6 7.4 8.3 1.3 Other

0

2.7

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 1.1

Cumulative Investor-Placed ABS Issuance ABS Issuance Mix, By Tranche Rating Category Count

(€ bil.) 2019 2020 2021 B and below BB BBB A AA AAA

30 100%

25 80%

20

60%

15

40%

10

5 20%

0 0%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Year to date (YTD) figures as of end-June each year. Source: S&P Global Ratings.

19ABS—Rating Actions & Performance Metrics

1. Monthly Rating Actions Count, Last 24 Months 2. Cumulative Rating Actions Count, Last 12 Months

Default Downgrade CreditWatch negative Upgrade Auto/

Credit cards Corp. sec. Other ABS

consumer

20

10

Upgrade 24 5 3 9

0

10

20 CreditWatch Neg. 4 0 2 0

30

40 Downgrade 0 0 6 0

Jul-19

Nov-19

Nov-20

Dec-19

Mar-20

Jul-20

Feb-20

Apr-20

Dec-20

Mar-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-19

Oct-19

Jan-20

Sep-20

Oct-20

Jan-21

Aug-19

Aug-20

Default 0 0 0 0

3. ABS 30+ Day Arrears Rate Indices 4. Used Car Price Index

German auto U.K. auto All auto U.K. Spain Italy Germany France

2.5 110

2.0 108

1.5 106

104

%

1.0 102

0.5 100

0.0 98

Jul-17

Nov-17

Mar-18

Jul-18

Nov-18

Mar-19

Jul-19

Nov-19

Mar-20

Jul-20

Nov-20

Mar-21

Mar-20

Jul-20

Nov-20

Dec-20

Mar-21

May-18

May-19

May-20

May-21

Feb-20

Apr-20

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-17

Jan-18

Sep-18

Jan-19

Sep-19

Jan-20

Sep-20

Jan-21

Sep-20

Oct-20

Jan-21

Aug-20

1. Excludes confidential ratings. Source: S&P Global Ratings. 2. Excludes confidential ratings. Source: S&P Global Ratings. 3. Source: S&P Global Ratings. 4. Source: Residual Value Intelligence, Autovista Group.

20Structured Credit

Sandeep Chana

Director

+44 20 7176 3923

sandeep.chana@spglobal.comCLO—Issuance

1. Investor-Placed CLO New Issuance 2. Investor-Placed CLO Refi/Reset Issuance

(Bil. €) Year to date Rest of year (Bil. €) Year to date Rest of year

35 40

30

25 30

20

20

15 34.5

10 10

13.3 14.7 13.8 14.2

5 6.9 7.6 7.2 8.4 10.1 9.9

0 0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

3. Cumulative Investor-Placed CLO New Issuance 4. Monthly European Leveraged Finance Origination Volumes

(Bil. €) 2019 2020 2021 (Bil. €) Bonds Loans

35 30

30 25

25 20

20

15

15

10

10

5 5

0 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2019 2020 2021

1. Year-to-date (YTD) figures as of end-June each year. Source: S&P Global Ratings. 2. Source: S&P LCD. 3. Source: S&P Global Ratings. 4. Three-month rolling average. Loan figures are institutional only. Source: S&P LCD,

S&P Global Ratings.

22CLO & Structured Credit—Rating Actions & Performance Metrics

1. Monthly Rating Actions Count, Last 24 Months 2. Cumulative Rating Actions Count, Last 12 Months

Default Downgrade CreditWatch negative Upgrade CLO SME Repack Other SC

20

10 Upgrade 8 1 15 0

0

10 CreditWatch Neg. 14 5 2 0

20

30 Downgrade 27 4 5 1

Jul-19

Nov-19

Nov-20

Dec-19

Mar-20

Jul-20

Feb-20

Apr-20

Dec-20

Mar-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-19

Oct-19

Jan-20

Sep-20

Oct-20

Jan-21

Aug-19

Aug-20

Default 0 0 0 3

3. European CLO Exposure To ‘CCC’ Category Corporate Obligors 4. Speculative-Grade Corporate Default Rate

16 U.S. Europe

14

12 14

10 12

8 10

%

6 8

%

4 6

2 4

0 2

0

Mar-20

Jul-20

Nov-20

Apr-20

Dec-20

Mar-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Sep-20

Oct-20

Jan-21

Aug-20

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

1. Excludes confidential ratings. Source: S&P Global Ratings. 2. SC—Structured Credit. Excludes confidential ratings. Source: S&P Global Ratings. 3. Solid line is the median, with each band representing a decile, from 10th

to 90th percentiles. Estimates based on portfolios from latest available trustee reports, with ratings updated. Source: S&P Global Ratings. 4. Dashed lines represent forecasts. Source: S&P Global Ratings.

23CMBS Mathias Herzog Director +49 69 3399 9112 mathias.herzog@spglobal.com

CMBS—Issuance

Investor-Placed CMBS Issuance 2021 YTD Investor-Placed CMBS Issuance, By Country

(Bil. €) Year to date Rest of year (Bil. €) 0.1

10 0.3

0.6

U.K.

8

Netherlands

6 Germany

4 Pan-European

5.5 0.5

2 Spain

1.3 2.3 2.0 2.0 2.1

0 1.1

0.6

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Cumulative Investor-Placed CMBS Issuance Primary Spreads On European CMBS Issuance

(Bil. €) 2019 2020 2021 (bps) GBP - AAA EUR - AAA GBP - BBB EUR - BBB

5 500

4 400

3 300

2 200

1 100

0 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan-19 Apr-19 Jul-19 Oct-19 Feb-20 May-20 Aug-20 Nov-20 Mar-21 Jun-21

Year-to-date (YTD) figures as of end-June each year. Sterling spreads are over three-month LIBOR prior to 2020 and subsequently over SONIA. Source: S&P Global Ratings.

25CMBS—Rating Actions

1. Monthly Rating Actions Count, Last 24 Months 2. Cumulative Rating Actions Count, Last 12 Months

Default Downgrade CreditWatch negative Upgrade Hotel Retail Mixed Other CMBS

10

Upgrade 0 4 0 0

5 CreditWatch Neg. 0 0 0 0

Downgrade 6 24 14 4

0

Default 0 3 0 0

5

3. European CMBS Loans In Special Servicing

Overall loan count % in special servicing (right scale) %

10

140 70

120 60

100 50

15 80 40

60 30

40 20

20 10

20 0 0

Jul-19

Nov-19

Nov-20

Dec-19

Mar-20

Jul-20

Feb-20

Apr-20

Dec-20

Mar-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-19

Oct-19

Jan-20

Sep-20

Oct-20

Jan-21

Aug-19

Aug-20

Mar-17

Dec-17

Mar-18

Dec-18

Mar-19

Dec-19

Mar-20

Dec-20

Mar-21

Jun-17

Jun-18

Jun-19

Jun-20

Sep-17

Sep-18

Sep-19

Sep-20

1. Excludes confidential ratings. Source: S&P Global Ratings. 2. Excludes confidential ratings. Source: S&P Global Ratings. 3. Based on loans backing European CMBS rated by S&P Global Ratings. Source: S&P Global

Ratings.

26Covered Bonds

Antonio Farina Casper Andersen

Senior Director Senior Director

+34 91 788 7226 +49 69 3399 9208

antonio.farina@spglobal.com casper.andersen@spglobal.comIssuance—Covered Bonds

Benchmark Covered Bond Issuance 2021 YTD Benchmark Covered Bond Issuance, By Country

(Bil. €) Year to date Rest of year YTD deal count (right scale) (Bil. €) 5.3 France

150 150 1.0 12.3 Germany

1.5 Norway

100 100 2.0 U.K.

2.2 Italy

50 50 Netherlands

5.5 Sweden

0 0

10.3 Other

2013 2014 2015 2016 2017 2018 2019 2020 2021

Cumulative Benchmark Covered Bond Issuance Change In YTD Issuance, 2021 Vs. 2020, By Country

(Bil. €) 2019 2020 2021 Norway

140 Sweden

120 Italy

100 Netherlands

Germany

80

Spain

60

Other

40

U.K.

20

France

0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec (Bil. €) (12) (10) (8) (6) (4) (2) 0 2 4

Year-to-date (YTD) figures as of end-June each year. Source: S&P Global Ratings.

28Covered Bonds—Rating Actions & Performance Metrics

1. Monthly Rating Actions Count, Last 24 Months 2. Cumulative Rating Actions Count, Last 12 Months

Downgrade Outlook negative Outlook positive Upgrade Central &

Northern Southern

Eastern Other CB

Europe Europe

8 Europe

6

4 Upgrade 0 2 1 0

2

0

2 Outlook Positive 0 0 0 0

4

6 Outlook Negative 0 4 0 0

Jul-19

Nov-19

Nov-20

Dec-19

Mar-20

Jul-20

Feb-20

Apr-20

Dec-20

Mar-21

May-20

Feb-21

Apr-21

May-21

Jun-20

Jun-21

Sep-19

Oct-19

Jan-20

Sep-20

Oct-20

Jan-21

Aug-19

Aug-20

Downgrade 0 0 0 0

3. Average Notches Of Uplift 4. Average Overcollateralization

Notches uplift Unused notches uplift Available Required for current rating

10 100

8 80

6 60

%

4 40

2 20

0 0

Nether-

Sweden

Ireland

Norway

Belgium

Spain

Austria

France

Italy

U.K.

Finland

Denmark

Germany

Nether-

Sweden

Ireland

Norway

Belgium

Spain

Austria

France

Italy

U.K.

Finland

Denmark

Germany

lands

lands

1. & 2. Based on count of issuers with covered bond rating actions in the time period. Excludes confidential ratings. CB—Covered Bonds. Source: S&P Global Ratings. 3. As of Q2 2021. Source: S&P Global Ratings. 4. As of Q2

2021. The scale is capped at 100%. Programs in Spain have an average available overcollateralization exceeding 250%. Source: S&P Global Ratings.

29Recent Research (1)

For similar information on North American Structured Finance, please download the most recent edition of our U.S. And Canada Structured

Finance Surveillance Chart Book.

– Covered Bonds Must Adjust To A New Reality After COVID-19, June 30, 2021

– Global Covered Bond Insights Q2 2021, June 30, 2021

– Credit FAQ: Green Mortgages And Green RMBS – What Are The Challenges?, June 28, 2021

– European Auto ABS Index Report Q1 2021, June 22, 2021

– European And U.K. Credit Card ABS Index Report Q1 2021, June 22, 2021

– European RMBS Index Report Q1 2021, June 16, 2021

– Data Requirements And Criteria Application For EMEA Nonperforming And Reperforming Structured Finance Transactions, June 15, 2021

– Global Structured Finance: Charting The Recovery From COVID-19, June 14, 2021

– Austrian Covered Bonds Harmonization Proposal Merges Three Laws Into One, June 10, 2021

– S&P Global Ratings’ U.K. Buy-To-Let Market Primer, June 1, 2021

– Period Of Maximum Liquidity Stress May Have Passed For U.K. Pub Corporate Securitizations, May 24, 2021

– LIBOR Transition: Laws Won’t Eliminate All Uncertainty, May 14, 2021

Source: S&P Global Ratings.

30Recent Research (2)

– European RMBS Market Update Q1 2021, May 11, 2021

– European CMBS Monitor Q1 2021, April 29, 2021

– The ESG Pulse: A Spotlight on Structured Finance, April 28 ,2021

– European RMBS Index Report Q4 2020, April 14, 2021

– U.K. Pubs, Shaken And Stirred, Look To Recover After A Cocktail Of Headwinds, April 8, 2021

– Global Covered Bond Insights Q1 2021, April 8, 2021

– Global Covered Bond Characteristics And Rating Summary Q1 2021, April 8, 2021

– ESG Industry Report Cards For Structured Finance Published, March 31, 2021

– European And U.K. Credit Card ABS Index Report Q4 2020, March 11, 2021

– European Auto ABS Index Report Q4 2020, March 11, 2021

– Covered Bonds In New Markets: Expect Only A Gradual Recovery, March 8, 2021

– As European Hotels Grapple With Prolonged Restrictions, Are Operators And Landlords Sharing The Pain?, Feb. 24, 2021

– How The Geographic Footprints Of U.K. Pub Corporate Securitizations May Influence Their Performance, Feb. 8, 2021

– European RMBS Outlook 2021, Jan. 25, 2021

– European Structured Finance Outlook 2021: In Short Supply, Jan. 20, 2021

Source: S&P Global Ratings.

31Copyright © 2021 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any

means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P

and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible

for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P

PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS

OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct,

indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in

connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions

(described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in

any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P

does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or

independent verification of any information it receives. Rating-related publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limited to, the publication of a

periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement

at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account

thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to

other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made

available on its Web sites, www.standardandpoors.com (free of charge), and www.spcapitaliq.com (subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

Australia: S&P Global Ratings Australia Pty Ltd holds Australian financial services license number 337565 under the Corporations Act 2001. S&P Global Ratings' credit ratings and related research are not intended for and must not be distributed to

any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).

STANDARD & POOR'S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor's Financial Services LLC.

spglobal.com/ratings

32You can also read