Energy transition: towards electricity without CO 2 - Kenergia.it

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

34th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy System

Giovanni Simoni

CEO Kenergia

Energy transition: towards electricity without CO2

30th June 2021

30/06/2021 Kenergia srl - All rights reserved 1

Kenergia Srl

Rain Water Storage Solution Solar Breeder

Grid Parity 2 Srl

Recovery Srl Provider Srl Marocco Sarl

30/06/2021 Kenergia srl - All rights reserved 2

INDEX 1. THE ORIGINS OF PV 2. THE CLIMATE CHANGES 3. THE DEVELOPMENT OF PV 4. THE PV TO OPTIMISE THE LAND USE EFFICIENCY: AGRIVOLTAICS 5. THE PROBLEMS OF “PV PERMITTING” IN ITALY 6. CONCLUSION 30/06/2021 Kenergia srl - All rights reserved 3

1. THE ORIGINS OF PV

PV is now the most important technology

for the green revolution of the electricity

production in the world.

It took 40 years to

achieve this goal! In 1980 c-Si solar cell thickness was 600 µm,

with silver micro-grid.

30/06/2021 Kenergia srl - All rights reserved 4

1. THE ORIGINS OF PV

In Italy, the first commercial PV cells entered the «market» in

1980-1981.

Pragma SpA (an ENI company) was the first PV factory in

Europe.

PV factory Number of PV factory

In 1987 production: workers:

1 MW/year 100

PV factory Number of PV factory

In 2021 production: workers:

3000 MW/year 100

«Fiera di Genova» in 1980 was the first international solar

energy exhibition.

Productivity increased by 3000 times!

Source: Kenergia - http://www.kenergia.it/storia-fotovoltaico/

30/06/2021 Kenergia srl - All rights reserved 5

1. THE ORIGINS OF PV

In 1981 commercial PV module efficiency was

[2]

8÷10% while the price was 12$/Wp (for a

minimum production at least of 26kWp). The 2018

record lab cell efficiency was > 22%[1].

Today, the average PV module efficiency is

about 20% (the same value of lab cell

efficiency in 1981).

Sources: [1] Ing. Simoni – Conferenza Nazionale sull’Energia 1987 – «Prospettive di sviluppo per il settore fotovoltaico, proposta per un programma

decennale».

[2] Fraunhofer ISE – «Photovoltaics report» 2020.

30/06/2021 Kenergia srl - All rights reserved 6

1. THE ORIGINS OF PV

[3] Thanks to the simplification of the PV

module industrial production process,

material usage for silicon cells has

been reduced significantly during the

last 13 years from around 16 g/Wp to

less than 4 g/Wp due to increased

efficiencies, thinner wafers and wires

as well as larger ingots.

This played a central role in the

decrease PV solar cells price,

together with other factors as

“economy of scale” and increase of

the efficiency.

Sources: [3] Fraunhofer ISE – «Photovoltaics report» 2020.

30/06/2021 Kenergia srl - All rights reserved 7

1. THE ORINGINS OF PV

[4]

While the cost of solar module has

declined significantly over the years, in

2005 the cost of PV electricity was at

least 10 times higher than the market

price.

The Italian Governement adopted an

aggressive incentives policy (initially

more than $550/MWh!). This lead to a

world wide installation record in the

2011 of 9,5GW!

EU Directive 2001/77/EC

(«RES Directive»)

Source: [4] BloombergNEF – «Global Solar Investment Report State of solar markets and role of concessional finance in ISA member countries” 2020.

30/06/2021 Kenergia srl - All rights reserved 8

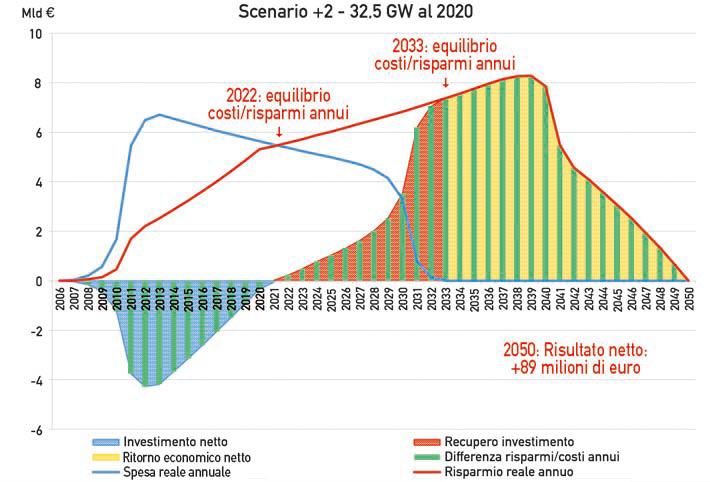

1. THE ORIGINS OF PV

COMPARISON BETWEEN INCENTIVES AND GAS SAVINGS IN

B€ “SCENARIO +2” [5] Scenario +2 was chosen as the "base scenario"

2033: cumulative savings > that resulting from the SEN, in the most

PV total incentives

2013 cautious assumption for the increment of the

2022: equilibrium annual gas price.

costs/savings

The graph represents a synthesis of results of

the comparison between the real cost of the

incentives paid in the bill and the actual savings

obtained in terms of natural gas imports.

2050: Net result

+ € 89 bilion • In 2022 the annual savings in fossil fuel

imports exceed the annual cost of

Net investment Return on investment

incentives.

Net economic return Difference between annual savings/costs

Real annual cost Real annual cost saving

• In 2033 the cumulative savings exceeds the

Source: [5] Ing. Giovanni Simoni – QualEnergia - «Il sole che fa bene al Paese» 2013. total PV incentives.

30/06/2021 Kenergia srl - All rights reserved 9

2. THE CLIMATE CHANGES

GREENHOUSE GLOBAL GAS EMISSIONS

2021

Total: 33.0 Gt CO2

2021

Total: 33.0 Gt CO2

Global energy-related CO2 emissions by sector [8] Global energy-related CO2 emissions, 1990-2021 [9]

Source: [8] International Energy Agency (IEA), Global energy-related CO2 emissions by Source: [9] International Energy Agency (IEA), Global energy-related CO2 emissions,

sector, Paris https://www.iea.org/data-and-statistics/charts/global-energy-related-co2- 1990-2021, Paris https://www.iea.org/data-and-statistics/charts/global-energy-related-co2-

emissions-by-sector emissions-1990-2021

30/06/2021 Kenergia srl - All rights reserved 102. THE CLIMATE CHANGES

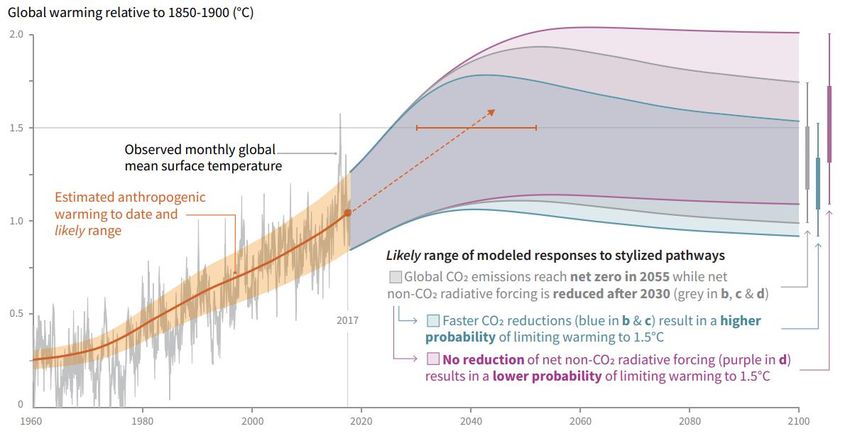

[10] Human activities

are estimated to

have caused

approximately

1.0°C of global

warming above

pre-industrial

levels, with a likely

range of 0.8°C to

a) It Represents the ΔT of global warming in the hypothesis both to reach 1.2°C.

CO2 global emissions net-zero in 2055 and to begin the decrease of other Global warming is

greenhouse gas emissions (non- CO2) in 2030.

likely to reach

b) best-case scenario: it represents ΔT of global warming in hypotesis to

reach CO2 global emissions net-zero in 2040, limiting global warming to

1.5°C between

1,5°C. 2030 and 2052 if it

c) worst-case scenario: it represents ΔT of global warming in hypotesis to continues to

not begin the decrease of greenhouse gas emissions (non- CO2) in 2030. increase at the

current rate.

Estimated anthropogenic global warming is currently increasing at 0.2°C per decade due to past and

ongoing emissions.

Source: [10] International Panel on Climate Change (IPCC) – «Global Warming of 1,5°C» 2018.

30/06/2021 Kenergia srl - All rights reserved 11[11] 2. THE CLIMATE CHANGES

GLOBAL CONTEST: THE 2050 NET-ZERO STRATEGY

Many countries have already fixed at 2050 the

date to net-zero the use of fossil fuels as

primary sources for the production of energy

both in electrical and thermal form.

The EU aims to be climate-neutral by 2050 –

an economy with net-zero greenhouse gas

emissions. This objective is at the heart of

the European Green Deal and in line with the

EU’s commitment to global climate action

under the Paris Agreement.

Source: [11] International Energy Agency (IEA) – «Net-zero by 2050» 2021.

30/06/2021 Kenergia srl - All rights reserved 122. THE CLIMATE CHANGES

Ever‐cheaper renewable energy

[12]

technologies give electricity the edge in

the race to zero.

Our pathway calls for scaling up solar

and wind rapidly this decade, reaching

annual additions of:

+ 630 GW PV

By 2030

+ 390 GW WIND

By 2030

Source: [12] International Energy Agency (IEA) – «Net-zero by 2050» 2021.

30/06/2021 Kenergia srl - All rights reserved 132. THE CLIMATE CHANGES

EUROPEAN GREEN NEW DEAL

As part of the European Green Deal, the Commission proposed in September 2020 to raise the 2030 greenhouse

gas emission reduction target, including emissions and removals, to at least 55% compared to 1990.

Key targets for 2030 [13]:

At least 40% cuts

in greenhouse gas

emissions (from 1990 levels)

At least 32% share

for renewable energy

At least 32.5% improvement

in energy efficiency

Source: [13] European Commission website - https://ec.europa.eu/clima/policies/strategies/2030_en

30/06/2021 Kenergia srl - All rights reserved 142. THE CLIMATE CHANGES

ITALIAN GREENHOUSE GAS EMISSIONS [15]

Green Deal

Per sector

Primary balance

Electrical sector

Waste

Agriculture Transport Heating and transport sector

and Breeding

Chemical Processes

Heating

Other sectors

Electrical Energy

Total emissions

73% of emissions are producted by the energy

sector.

Source: [15] Elettricità Futura – «Audizione Commissione X – Attività produttive, commercio e turismo» 2021

30/06/2021 Kenergia srl - All rights reserved 152. THE CLIMATE CHANGES

ITALIAN PNIEC TARGETS [16]

To achieve Green Deal targets Italy will have to: Evolution of renewable capacity by 2030

• Update the PNIEC (Piano Nazionale Integrato per Bio and Geothermal Innovative RES

Energy (PNRR)

l’Energia e il Clima) according to European Green Deal

targets.

Bio and Geothermal

Energy

• To install new 65 GW of renewable energy by 2030

(70GW including PNRR), increasing highly the rate of Hydro

annual installations.

Hydro PV PV

• To fix new regional targets of renewable energy

Wind

development (burden sharing).

Wind

• Regional permitting managers will have to be more

responsible to achive new targets.

Preliminary balance 2020

Source: [16] Elettricità Futura – «Audizione Commissione X – Attività produttive, commercio e turismo» 2021.

30/06/2021 Kenergia srl - All rights reserved 162. THE CLIMATE CHANGES

ITALIAN ELECTRICAL PENETRATION [16]

Comparison between the percentages of the penetration Electrical demand (annual variation, left axis, %)

of the electric carrier in 2017 between the various EU-28 Index 2005=100 and share of final consuption (avarage

countries. [17] 3 years, right axis) [18]

Sources: [17] Elettricità Futura – «Vettore Elettrico: lo scenario attuale e le prospettive future» 2019.

[18] Agenzia Nazionale per le nuove tecnologie, l’energia e lo sviluppo economico sostenibile (ENEA) – «Analisi trimestrale del sistema

energetico italiano 01/2021».

30/06/2021 Kenergia srl - All rights reserved 172. THE CLIMATE CHANGES

ITALIAN GREEN NEW DEAL TARGETS [19]

With the current trend the «2030 targets» will be reached in 2085

+ 7 GW/year

are the annual installation of renewable

plants to reach the 2030 Green Deal

target.

+ 0,8 GW/year

Is renewable capacity of 2020 of which 120

MW PV utility scale (-50% of 2019) and 85

MW wind (-80% of 2019).

INITIAL TREND

Source: [19] Elettricità Futura – «Audizione Commissione X –

Attività produttive, commercio e turismo» 2021.

30/06/2021 Kenergia srl - All rights reserved 183. THE DEVELOPMENT OF PV

PV

PV POWER EVOLUTION AND PV

P installed

PLANTS NUMBER IN ITALY [6] YEAR

[MW]

2019 757

2018 426

2017 399 «Conto Energia»

2016 382 I Conto Energia D.M. 28th

2015 307 july 2005 and D.M. 6th

february 2006;

2014 409 II Conto Energia D.M. 19th

2013 1.400 february 2007;

2012 3.654 III Conto Energia D.M. 6th

august 2010;

2011 9.539

IV Conto Energia D.M. 5th

2010 2.328 may 2011;

2009 781 V Conto Energia D.M. 5th

2008 344 july 2012.

Source: [6] Gestore dei Servizi Energetici (GSE) – «Rapporto statistico solare fotovoltaico 2020».

30/06/2021 Kenergia srl - All rights reserved 193. THE DEVELOPMENT OF PV

LOW RENEWABLE COSTS ALLOW TO POWER PAST

COAL [7]

2021 Renewable electricity costs have fallen sharply over

the past decade, driven by improving technologies,

economies of scale, increasingly competitive supply

chains and growing developer experience.

Since 2010, utility-scale solar PV power has

shown the sharpest cost decline at 82%.

Source: [7] International Renewable Energy Agency IRENA 2021 - https://www.irena.org/newsroom/articles/2021/Jun/Low-Renewable-Costs-Allow-To-Power-Past-Coal

2021. 30/06/2021 Kenergia srl - All rights reserved 204. THE PV TO OPTIMISE THE LAND USE EFFICIENCY: AGRIVOLTAICS

ITALIAN CONTEST: PV LAND USE

During the years the ratio between

PV land use and power installed

[ha/MW] decreased thanks to the

increase in the PV module ratio

between power and area [W/m2]:

➢ In 2008 P= 250 W 2 m2

➢ Today P= 500 W 2 m2

Target of Total PV

new PV land for

1,43 50.000

+35 GW power on PV Land the target

ha/MW ha

the of new 35

ground GW

[20]

Source: [20] Elettricità Futura – «Audizione Commissione X – Attività produttive, commercio e turismo» 2021.

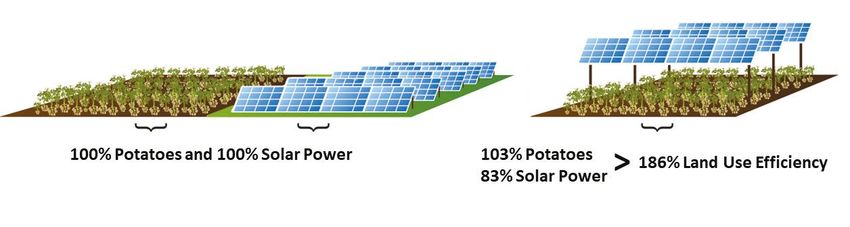

30/06/2021 Kenergia srl - All rights reserved 214. THE PV TO OPTIMISE THE LAND USE EFFICIENCY: AGRIVOLTAICS

To reach the 2030 target in Italy we need to built 35GW of PV on land (PVL). A global investment of around €25

billions in less than 10 years! A large part of PVL should use agricoltural land: the so called Agrivoltaics (AGV).

The AGV plant, to be accepted by local Authorities, must consider a strong priority to agricoltural production..

AGV can [21]:

1. Contribute to a responsible use of natural resources such as land and water;

2. Promote sustainable agricultural practices;

3. Increase the EU’s agriculture resilience to climate change and other shocks and stresses;

4. Enable sustainable development in rural areas through higher yields and new business opportunities.

Source: [21] SolarPower Europe – «Agrisolar Best Practise Guidelines» Version 1.0, 2021.

30/06/2021 Kenergia srl - All rights reserved 225. THE PROBLEMS OF “PV PERMITTING” IN ITALY

PV “Autorizzazioni Uniche” requested in Italy PV “Autorizzazioni Uniche” issued in Italy

20 GW of PV “Autorizzazioni Uniche” requested in Italy in 1,4 GW of PV “Autorizzazioni Uniche” issued in Italy from

the last 3 years [22] 2016 to 2020 [22]

Source: [22] Energy & Strategy Group, Politecnico di Milano School of Management – «Renewable energy Report 2021».

30/06/2021 Kenergia srl - All rights reserved 236. CONCLUSION

- In Italy, like in many other countries, PVL and AGV are playing the basic role in the energy transition.

- A correct combination of agricultural production and electricity generation on the same land is a basic

condition to reach the 2030 enviromental target.

- This is not an easy task for the different conditions to be satisfied:

a) no soil food consumption;

b) acceptance by farmers to work on the same land with electrical operators;

c) financial and economic agreements;

d) Landscape integration of the PVL.

- Kenergia is investing in a new approach to the projects, and we are very confident on our Hybrid

Methodology that will demonstrate the economic convenience for all the involved stakeholders.

30/06/2021 Kenergia srl - All rights reserved 24Contact

Giovanni Simoni

g.simoni@kenergia.com

www.kenergia.com

30/06/2021 Kenergia srl - All rights reserved 25You can also read