From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

From Traditional Floor Trading to Electronic High Frequency

Trading (HFT) ‐ Market Implications and Regulatory Aspects

Prof. Dr. Hans‐Peter Burghof

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen

HFT has fundamentally changed financial markets…

Traditional floor trading Modern high frequency trading (HFT)

Amazon: More than 100,000 quotes per second in Amazon on June 7, 2013

BATS IPO ‐ from $15 to 0 in 1.5 seconds: Stock begins trading at $15.25. Within 900 milliseconds from opening

the stock price had fallen to $0.29. Within 1.5 seconds the price dropped to $0.0002. 567 trades were

executed before trading halt.

May 6 2010 , Flash Crash: DJIA plunges by around 1,000 points (9%) and recovers the losses within minutes

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 2

… in the sense that

Today’s market environment

Human are removed from the direct decision‐making process of security transactions and substituted by

computer software

Speed has become the single most important factor in security trading

Fundamentals do not play any role for most high frequency traders

Holding periods are often limited to milliseconds (10−3) or even nanoseconds (10−9)

The competitive advantage has shifted from those…

with superior capabilities in determining the “true” value of an asset

to those…

who can trade faster than others!

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 3

What is HFT?

HFT is a subset of algorithmic trading Definition of algorithmic trading in Mifid II:

Trading in financial instruments where a computer algorithm

Algorithmic High Frequency automatically determines individual parameters of orders such

Trading Trading as whether to initiate the order, the timing, price or quantity of

the order or how to manage the order after its submission, with

limited or no human intervention

Market making Statistical arbitrage

Typical features of HFT:

Spread Capturing Market Neutral

Proprietary trading Rebate Driven Arbitrage

Strategies Cross Arbitrage

Large number of orders with small size Not only (Asset, Market, ETF)

Rapid cancellation of orders one type of

No overnight positions HFT but a variety Strategies

of different

Very short holding periods Liquidity detection Others

strategies Pinging Momentum

Use of colocation and proximity Sniping Latency Arbitrage

services Quote Matching Manipulation (e.g.

Quote Stuffing,

Focus on highly liquid securities Spoofing)

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 4

HFT activity

HFT activity at regulated markets and MTFs in Europe in 5/2013 Falling market shares of HFT (39% in

40%

Europe in 2012 according to TABB

35%

30% Group)

25%

Value traded

20%

Generally higher market shares of

15%

HFT in the U.S. (51% in in 2012

10%

5% according to TABB Group)

0%

NYSE Euronext Amsterdam

All Venues

NYSE Euronext Paris

Borsa Italiana

London Stock Exchange

Irish Stock Exchange

CHI‐X

Turquoise

NYSE Euronext Lisbon

NYSE Euronext Brussels

BATS

Higher market shares at less

regulated trading venues

HFT activity has plateaued on

established markets, continues to

HFT Activity expand globally (e.g. Asia)

Source: European Securities and Markets Authority (2014): Report on Trends, Risks and Vulnerabilities

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 5

Market implications – Market quality

Price

Authors Sample period Market Method Liquidity Volatility

discovery

NASDAQ OMX

Brogaard et al. (2014) 08 – 10/ 2012 Empirical

Stockholm

Martinez, Rosu (2013) ‐ ‐ Theoretical

Hasbrouck, Saar (2013) 10/ 2007 & 06/ 2008 NASDAQ Empirical

Brogaard et al. (2012) End of year 2009 NASDAQ, BATS Empirical ‐

Bias et al. (2011) ‐ ‐ Theoretical ‐ ‐

06/ 2010

Kirilenko et al. (2011) E mini S&P 500 Empirical

(Flash Crash)

Civitanic, Krilenko (2010) ‐ ‐ Theoretical

Brogaard (2010) 2008,2009 & 02/ 2010 NASDAQ Empirical

Overall, the literature tends to find that HFT improves market quality!

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 6

Market implications – Market quality

Influence of HFT on market quality

Liquidity Volatility Price discovery

• Based on traditional liquidity • HFT traders tend to reduce • HFT traders act as market

measures HFT tends to volatility due to smaller price makers and hence can

increase liquidity on the differences depending on positively affect price discovery

market market conditions. • But: Depending on market

• But: The duration of liquidity • But: This effect seems to affect situation and strategy HFT

provision is often short predominantly short term traders can also strongly

volatility deviate from that role

The proponents of HFT argue that HFT plays an important role in the price discovery

process, leading to an increase in price efficiency => improved market quality

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 7

Market implications – Negative externalities

The downside of HFT

The “need for speed” harms “real” investments, market stability & fairness

Speed has become the single most important factor in security trading

Fundamentals do not play any role for most high frequency traders

Operational risk: Systemic risk

• Quote stuffing • Flash crashes

• Sunshine liquidity

• Sunshine market‐

making

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 8

Market implications – Operational risk

The strong growth of HFT activity during the past decade lead to a sharp increase in the amount of quotes

Why is this a problem?

The placement of bids and asks via HFT can be compared with sending spam Emails

In relation to sending and receiving it is practically free of charge for the sender but not for the recipient

Forwarding and processing continuously increasing amounts of data generates increasingly problems and

costs for trading venues and market participants and may lead to a breakdown of the trading system of

individual trading venues.

HFT abuse the restricted capacity of trading venues and other market participants to handle continuously

increasing data volumes:

Speed wars aka quote stuffing aka fake liquidity

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 9

Market implications – Operational risk

Quote stuffing / fake liquidity

War between HFT algorithms

HFT place a large amount of quotes within a single

second (e.g. 15.000 and more) and cancels it

immediately

Other market participants and trading venues

have to process these quotes which takes time

The HFT originator knows that his quotes are “fake”

and neglects their processing. Yet, he analyses the

reaction of the other market participants and waits for arbitrage opportunities when prices differ

Quote stuffing is a main driver for system outages at trading venues

Pure market manipulation!

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 10Market implications – Operational risk

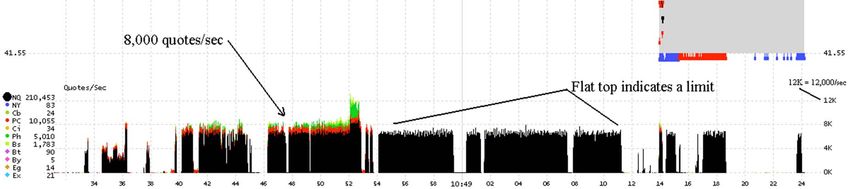

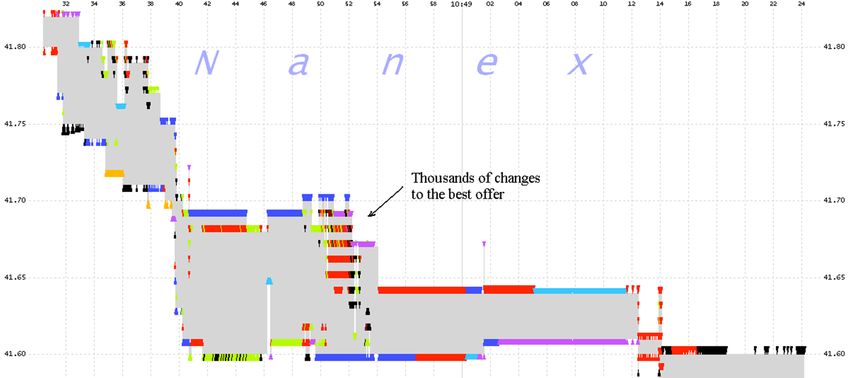

Quote stuffing in

Michal Kors Inc. (KORS)

on Feb. 14, 2012

KORS is stuffed with

quotes from multiple

exchanges exceeding

18.000 quotes/sec

The picture shows

about 40 seconds

divided into 50

millisecond intervals

Before KORS hand only

a few hundred trades in

the same time span

Source: Nanex

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 11Market implications – Operational risk

Sunshine liquidity / Sunshine market‐making

Burghof/Spankowski/Wagener (2014) find

that trading activity on Multilateral

Trading Facilities (MTFs) – where HFT are

preferably active – reduces significantly in

times of increased market distress.

Also when market‐making becomes

difficult, market participants on MTFs –

presumably HFT – seem to reduce their

liquidity provision.

Hence, HFT is no big help for a sustainable

efficiency in financial markets

Source: Burghof/Spankowski/Wagener (2014): Back to the roots – Market fragmentation and order routing

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 12Market implications – Systemic risk

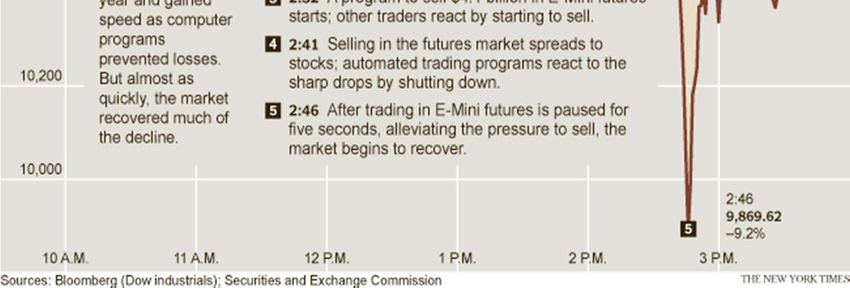

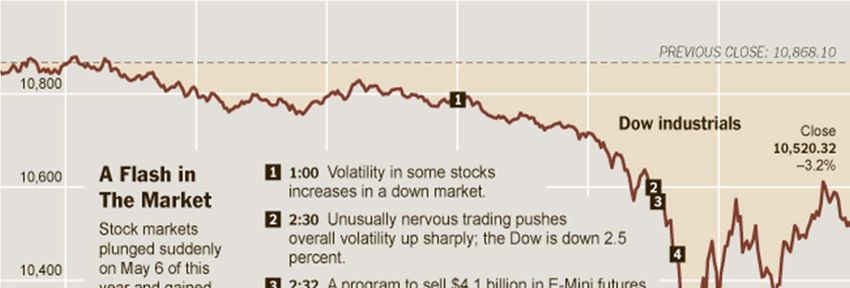

Flash crash on May 6, 2010

in the DOW

Trigger: Negative news of

Europe/Greek ‐> new

riots

At 14:42:44:075 was an

immediate sale of ~ $125

million worth of June

2010 eMini futures and a

sale of nearly $100

million ETFs

HFT did not trigger the flash crash, but their responses to the selling pressure on that day increased volatility

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 13Market implications – Summary

No real No fair market

Critical in very volatile

investments conditions for non‐HFT

Quote stuffing can reduce the

market situations

quality of quotes and affect

market quality negatively

Positive influence on

No clear cut result can

market quality Improves price discovery

be drawn

Regulation?

HFT HFT strategies

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 14Regulatory aspects

In general, European (MiFID) and German aspects on German details:

HFT regulation seem to be compatible, both foresee: Stock Exchange Supervisory Authorities and BaFin

Trading venue capacities have to be sufficient for HFT receive increased enforcement powers (information

Excessive usage fees to be charged on all trading requests, prohibition of Algo trading strategies)

venues High Frequency Traders are now subject to licensing

Order flagging to control HFT strategies (‐> Trader ID) obligation under German Banking Act

Order‐to‐Trade ratios published by all trading venues Regulation and supervision of HFT as financial

Installment of circuit breakers at all trading venues services institutions by BaFin (‐> Prop traders now

Appropriate minimum tick sizes on all trading venues also have to register)

Regulation on the basis of taxes has been seen critical by several scholarly papers. Deterioration of market quality in

France and Italy where this regulatory practice has been used (e.g., Meyer et al., 2013; Gomber et al., 2014)

Universität Hohenheim Institut für Financial Management Lehrstuhl für Bankwirtschaft & Finanzdienstleistungen 15You can also read