FY2019 AGM PRESENTATION CORPORATE - KIMLY LIMITED - SGX

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

KIMLY LIMITED FY2019 AGM CORPORATE PRESENTATION 21 January 2020

CONTENTS Corporate Profile Strategy Recalibration Financial Highlights Outlook

CORPORATE PROFILE

Listed on 20th March 2017 on the SGX Catalist

Board, Kimly Limited is a leading and established

operator of coffeeshops, food courts and other

food outlets across Singapore, with a proven track

KIMLY LIMITED

record of nearly 30 years.

Kimly operates a total of 70 food outlets under its

Outlet Management Division and 135 food stalls

under its Food Retail Division as at 26th November

2019. Outlet Management Food Retail

Division Division

EXPANDING OUR FOOTPRINT

Mixed Vegetable Seafood Zi Char

Location Type Drink Stall Dim Sum Stall Kanaaji

Rice Stall Stall

Blk 691, Woodlands Awarded

Drive 73 under HDB

PQM

Blk 365, Sembawang Awarded

Crescent under HDB

PQM

Blk 322, Sumang Awarded

Walk under HDB

PQM

Blk 143, Teck Whye Acquisition

Lane

Blk 106, Bidadari Managing Under 3rd party

Park Drive Agent brand

Flavors @ U-Town Awarded

new lease

STRATEGY RECALIBRATION

Asset Ownership

Asset

ownership

• Direct ownership to enlarge revenue

streams.

• Maximizing Central Kitchen’s

capabilities with Food Retail expansion.

• Stability of Food Retail businesses

through long term leases.

STRATEGY RECALIBRATION Rationale of Asset Ownership • To further expand the Group’s network of food outlets • To establish new food outlets and food stalls as and when strategic locations become available • Enable the Group to mitigate uncertainty surrounding its private leases, which can be influenced by market competition

STRATEGY RECALIBRATION

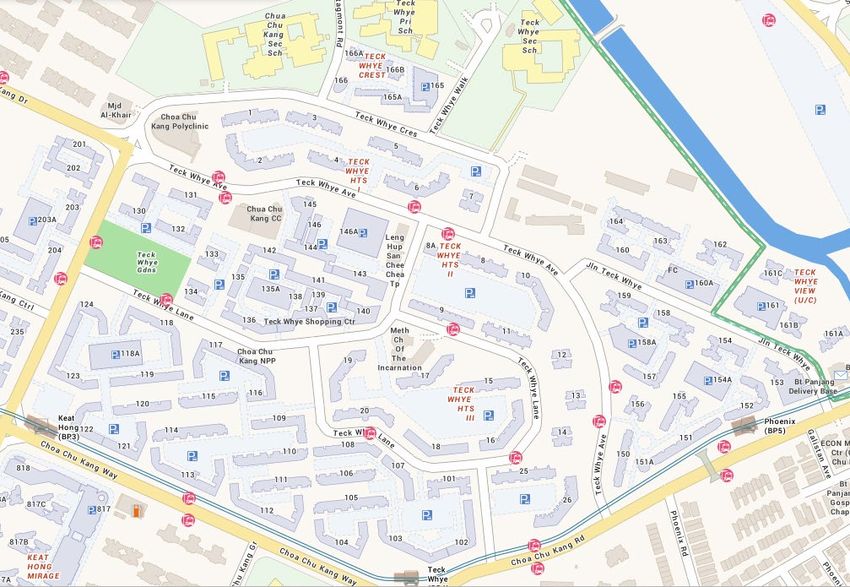

Newly-acquired coffeeshop: Blk 143, Teck Whye Lane

Acquisition

S$14.0 million

Consideration

Teck Whye Neighborhood Centre

Net Floor Area 224 sqm

Opening Date In Operations

Food Retail Dim Sum Stall and Mixed Vegetable

Blk 143 Teck Whye Lane

Division Rice Stall

Densely Populated Matured Housing

Estate, Schools and Private

Characteristics residential clusters. Served by 3 LRT

stations. Teck Whye LRT Station

Keat Hong LRT Station

Phoenix LRT Station

STRATEGY RECALIBRATION Newly-acquired coffeeshop: Blk 143, Teck Whye Lane

STRATEGY RECALIBRATION

Further enlarging our footprints

* Non-binding term sheet between Jin Wei Holdings Pte. Ltd. and several

vendors for the acquisition of a portfolio of coffeeshop leases,

coffeeshop units and industrial canteen units

Target Properties comprises:

•Four long term leasehold coffeeshop properties units, which are HDB commercial

units located within mature HDB estates;

•Three freehold industrial canteen units, which are located in mature and populated

industrial areas in close proximity to residential areas; and

•Three short term coffeeshop leases, which are HDB direct leases, located within

mature and populated HDB residential areas (The acquisition by the Group of

interests in the entities holding the HDB leases for the three coffeeshop properties

does not constitute an assignment of tenancy).

*Please refer to the Group’s announcement released on 22 October 2019 for more information.

OUTLET MANAGEMENT DIVISION

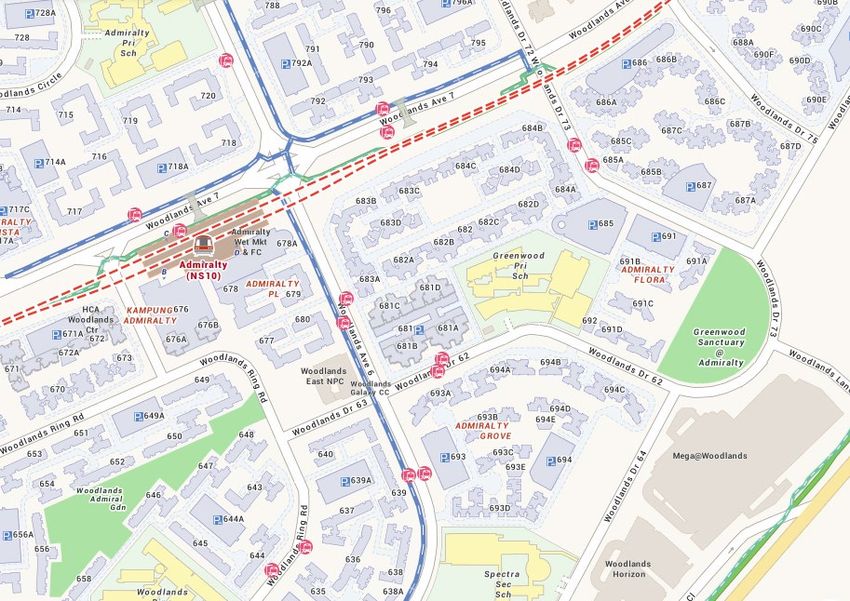

AWARDED UNDER HDB PQM: Blk 691, Woodlands Drive 73

Opening Date In Operations

Seafood Zi Char Stall and Mixed

Food Retail Division Vegetable Rice stall.

Blk 691,

Woodlands Dr 73

Matured Housing Estate, established

footfall, close proximity to industrial

Characteristics parks. More new housing estates are

being constructed in close proximity.OUTLET MANAGEMENT DIVISION AWARDED UNDER HDB PQM: Blk 691, Woodlands Drive 73

OUTLET MANAGEMENT DIVISION

AWARDED UNDER HDB PQM: Blk 365, Sembawang Crescent

Opening Date In Operations

Dim Sum stall and Mixed Vegetable

Food Retail Division Rice stall.

Combination of a new and matured

Characteristics Housing Estate, near schools, close

proximity to industrial parks.

Blk 365, Sembawang CrescentOUTLET MANAGEMENT DIVISION AWARDED UNDER HDB PQM: Blk 365, Sembawang Crescent

OUTLET MANAGEMENT DIVISION

AWARDED UNDER HDB PQM: Blk 322, Sumang Walk

Opening Date In Operations

Food Retail Dim Sum stall and Mixed Vegetable

Division Rice stall.

Blk 322, Sumang Walk

Right beside park connector, highly

populated Schools and

Condominiums. Served by 2 LRT

Characteristics and 1 MRT stations. Limited F&B

establishments in Sumang, Punggol

estates.OUTLET MANAGEMENT DIVISION

Progressing with time

Enhancing Tray Return Reward System

Customers will return used cutlery and crockery to collection

device located at a convenient area within the food outlet

Reward: QR code for discount at food stall (synchronised with

POS system to allow monitoring)

Workload for cleaners and food outlet staff is reduced

Cashless Payment at Bukit Batok Blk 292, U-Town, Jurong

West Blk 651

Convenient alternative cashless payment methods, staying

relevant to our younger customers who are more familiar with

such cashless payment methods

More than 50% of transactions are made through cashless

payment options at Flavors@U-Town’s drinks stall.OUTLET MANAGEMENT DIVISION

Progressing with time

Launch of New Improved Taste of our Traditional Kopi &

Teh Peng!

Cater to consumers’ preference

Traditional Kopi

and Teh Peng

Can DrinksOUTLET MANAGEMENT DIVISION

Progressing with time: Flavours @ University Town, NUS

IN OPERATIONS

Estimated

(Asset enhancement done in

Opening Date 2019)

Drinks stall, Kanaagi Japanese

Food Retail

food stall, Mixed Vegetable Rice

Division stall

Serves a large captive population F l a v o r s @ U- T ow n

in University Town. Close

proximity to student

Characteristics accommodation. Anchored by

heritage hawker, Tian Tian

Chicken Rice from Maxwell.OUTLET MANAGEMENT DIVISION Progressing with time: Flavours @ University Town, NUS

FOOD RETAIL DIVISION

Seafood “Zi Char” Stalls

Harnessing the strengths of our Central Kitchen and IT capabilities

to improve productivity

Increase number Reduced

of semi- Better Tablet ordering workload for Central Kitchen

finished food consistency in + Food pager stall workers, increase in

items prepared food quality system + POS reduce reliance productivity

at central system + HQ ERP on highly- with machinery

kitchen skilled chefsFOOD RETAIL DIVISION Mixed Vegetable Rice Stalls Harnessing the strengths of our Central Kitchen and IT capabilities to improve productivity Replacing manual repetitive low value work with the help of food processing machines. Increased productivity Improved quality and consistency control Improve revenue per worker contribution Cost savings through bulk purchase

FOOD RETAIL DIVISION

Mixed Vegetable Rice Stalls

Harnessing the strengths of our Central Kitchen and IT capabilities to improve

productivity

Implementation of Combi-Oven

Automation of several cooking processes Automation of several

cooking processes

Freeing up precious time so our frontline staff

can do more higher value work, eg: improving

customer service and hygiene management Reduced man-hour

requirements for food

Reduced man-hour requirements for food preparation

preparation

Energy-saving and heat reduction capabilities

to make work environment more conducive to Implementation of

attract more seniors to join our industry Combi-OvenFOOD RETAIL DIVISION

Dim Sum Stalls

Harnessing the strengths of our Central Kitchen and IT

capabilities to improve productivity

• The Group continues to devise new attractive products catering to changing consumer preferences.

Target

Incentive

Program to

Increased improve

Strong

reach of sales

response

online

from

Newest delivery

customers

product in footprint

Dim Sum

menu

Bak Kwa

PauFINANCIAL HIGHLIGHTS

FY2019 Revenue

S$208.3 m

REVENUE BY BUSINESS SEGMENT (S$’M)

3.0% / S$6.1 m y-o-y

202.2

208.3 Outlet Management

80.9

192.1 88.6

97.2

S$111.1 m

172.2

74.6

2.2% / S$2.5 m y-o-y

46.7%

43.8% - Due mainly to cessation of

42.1%

43.4% operation of a coffeeshop

113.6

97.6

111.2 111.1

Food Retail

S$97.2 m

56.2% 53.3%

56.6% 57.9% 8.8% / S$8.6 m y-o-y

- Due mainly to revenue

contribution from new

FY2016 FY2017 FY2018 FY2019 businesses (Tonkichi and

Outlet Management Division Food Retail Division Rive Gauche) and

delivery salesFINANCIAL HIGHLIGHTS

PROFITABILITY

Gross Profit (S$’m) & EBITDA (S$’M) & EBITDA MARGIN (%)

Gross Profit Margin (%) 27.5 27.1 27.4 20.00%

45

27.0 26.0

40.2 40.7 16.0%

40 37.2 38.4 14.1% 16.00%

21.6% 20.0%

23.0

13.6%

19.9%

35

19.5% 12.5%

12.00%

19.0

30

25 15.0 8.00%

20

11.0 4.00%

15

10 7.0 0.00%

FY2016 FY2017 FY2018 FY2019 FY2016 FY2017 FY2018 FY2019

Gross Profit Gross Profit Margin EBITDA EBITDA MarginFINANCIAL HIGHLIGHTS

NET PROFIT AFTER TAX (S$’M)

30 16.0% NPAT

25 24.2

14.1% 14.0% S$20.1 m

21.4 21.9 12.0% 8.4% / S$1.8 m y-o-y

20.1

20

10.0%

- The increase in gross profit of

11.2%

10.8% $0.5 mil was affected by higher

15 9.6%8.0%

6.0%

selling and distribution expense,

administrative expense and

10

4.0%

5 income tax expense.

2.0%

0 0.0%

FY2016 FY2017 FY2018 FY2019

NPAT Net Profit MarginFINANCIAL HIGHLIGHTS

PBT (S$’M) & PROFIT MARGIN (%) BY BUSINESS SEGMENT

11.8

12

10.9

11.5 Outlet Management

10.4

11.2% 10.6%

S$10.4 m

10.2%

8

9.4% 11.0% / S$1.1 m y-o-y

8.00% - Due mainly to

continued pressure

4

on rents and payroll

costs

gestation period for

0 0.00%

new outlets located

FY2016 FY2017 FY2018 FY2019 in new precincts.

Profit Before Tax Profit MarginFINANCIAL HIGHLIGHTS

PBT (S$’M) & PROFIT MARGIN (%) BY BUSINESS SEGMENT

21.2% 19.7%

22.2% 19.2

19.0

18.8

18.0

20.7% Food Retail

15.5

21.00%

S$19.2 m

15.0 2.2% / S$0.4 m y-o-y

Lower profit margin due to:

13.00% Continued pressure on

11.0 ingredients and payroll costs

restaurant and confectionery

business have a lower profit

7.0 5.00% margin

FY2016 FY2017 FY2018 FY2019

Profit Before Tax Net Profit MarginFINANCIAL HIGHLIGHTS

Sep 2019 Cash and cash equivalents

CASH GENERATIVE BUSINESS LEADING TO S$87.2 m

STRONG OPERATING CASH FLOW

Net Cash Generated From Operating Activities (S$’M) Sep 2019 Net cash

36.0

36.4 S$53.9 m

32.0

28.4 29.0 FY2019 net cash generated from operating

28.0

activities

24.0

S$36.4 m

20.0

16.0

12.0

7.2 Lower net cash generated from operating activities in

8.0

FY2018 due to consideration receivable of $16.0 m

4.0 pursuant to the Rescission.

0.0

FY2016 FY2017 FY2018 FY2019FINANCIAL HIGHLIGHTS

DIVIDENDS DIVIDENDS

FY2018 FY2019 Total of 1.40 SG cents per

Total of 0.96 SG cent ordinary share

per ordinary share

Interim

Interim

Dividend

50.7% payout ratio Dividend 80.2% payout ratio

0.28 4.36% dividend yield 0.56 6.0% dividend yield

Singapore cent Singapore cent

per share, paid per share,

in May 2018 paid in July

2019

Final Dividend Final Dividend

0.68

(subject to approval)

Singapore cent

per share, paid in

February 2018

0.84

Singapore cent per share,

payment date TBAOUTLOOK

Expansion of footprint in mature

Recalibration of corporate

and populated estates with Barring unforeseen

strategy and leveraging on

established footfalls, growing of circumstances, the Group expects

improved central kitchen and

market presence and standing as to continue to be profitable in the

supply chain functions to pursue

one of the leading F&B operators financial year ahead

asset ownership

in SingaporeYou can also read