GABO German American Business Outlook 2019 - January 29, 2019 6:00pm to 9:00pm

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GABO

2019 German American

Business Outlook 2019

January 29, 2019

6:00pm to 9:00pm

Deutsche Bank, 60 Wall Street, 47th Floor, New York

Hosted by:

#GABO2019

PROGRAM

GERMAN AMERICAN

BUSINESS OUTLOOK 2019

6:00 p.m. Registration

6:30 p.m. Welcome Remarks

Michaela Ludbrook

Head of Global Transaction Banking, Americas, Deutsche Bank

Rainer Bender

Global Chairman of Corporate Banking Coverage, Deutsche Bank AG

6:35 p.m. Introductory Remarks

Caroll H. Neubauer

Chairman & CEO, B. Braun Medical Inc. / Chairman, GACC New York

Peter Riehle

President & CEO, WITTENSTEIN Holding Corp. /

Chairman, German American Chambers of Commerce

6:45 p.m. Economic Update by Torsten Slok

Chief International Economist, Deutsche Bank

7:05 p.m. Presentation of Business Outlook Survey Results by Mark Tomkins

President & CEO, GACC Midwest

7:40 p.m. Transatlantic Panel Discussion

Caroll H. Neubauer

Chairman & CEO, B. Braun Medical Inc. / Chairman, GACC New York

Daniel Andrich

President & CEO, Representative of German Industry + Trade (RGIT)

Peter Riehle

President & CEO, WITTENSTEIN Holding Corp. /

Chairman, German American Chambers of Commerce

Vincent Halma

President & CEO, KION North America

Moderator: Dr. Volker Treier

Chief Executive of Foreign Trade, Member of the Executive Board, DIHK

8:25 p.m. Networking Reception

Hosted by Deutsche Bank

#GABO2019 #GERMANBUSINESS

#GACCNY #GACCMIDWEST #GACCSOUTH #GACCWEST

GREETING

Dear Reader,

It is evident that many of the pivotal economic developments in the last year continue to evolve on a

daily basis. So far, the economies of the US and Germany remain on a path of sustained growth and low

unemployment, though concerns are rising on both sides of the Atlantic.

Our German American Business Outlook (GABO) this year again provides insight into how German

subsidiaries in the US view this country as a business location and their expectations for the coming year.

The overwhelming majority anticipate moderate growth of up to 3%, though when asked about their own

sales, a post-recession high of 9% foresee a contraction in their business. Among the more key topics are

a move to diversification and M&A, while also addressing workforce and visa challenges, as well as the

importance of open markets on their supply chains. Nonetheless, the overall outlook remains optimistic.

We at the GACC and Representative of German Industry + Trade (RGIT) are committed to fostering

positive economic ties between the US and Germany. That includes highlighting the interests of our

members to ensure that their businesses thrive. And we, of course, greatly appreciate their continued

support of our organization.

Respectfully yours,

DANIEL ANDRICH DIETMAR RIEG

President & CEO, RGIT President & CEO, GACC New York

MARK TOMKINS KRISTIAN WOLF

President & CEO, GACC Midwest CEO, GACC West

STEFANIE ZISKA

President & CEO, GACC South

SURVEY

#GABO2019

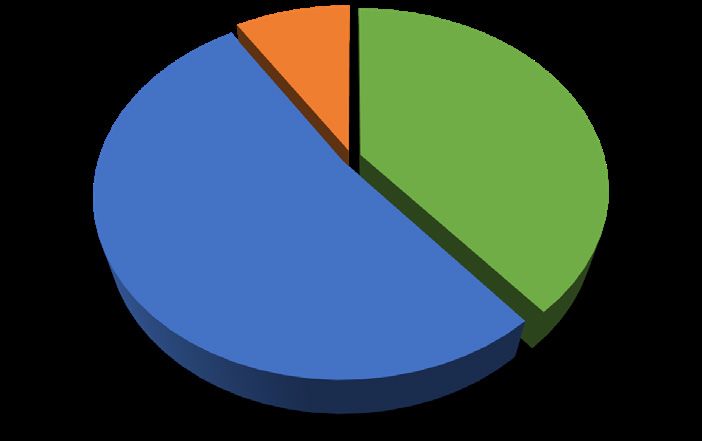

GROWTH EXPECTATION FOR YOUR BUSINESS IN 2019

Growth expectation for your business in 2019

9%

9%

39% 39% Expectations for individual

businesses are still positive

Expectations for individual businesses are still

52% but 9% expect a

positive but 9% expect a contraction for their own

52%

contraction for their own

business in 2019, the highest since emerging from

business in 2019, the

the recession.

highest since emerging

from the recession.

Stronggrowth

Strong growth > 3%

> 3% Flat to

Flat tomoderate

moderategrowth

growth

0%0%

- 3%- 3%

Contraction

Contraction < <

0%0% growth

growth

#GABO2019

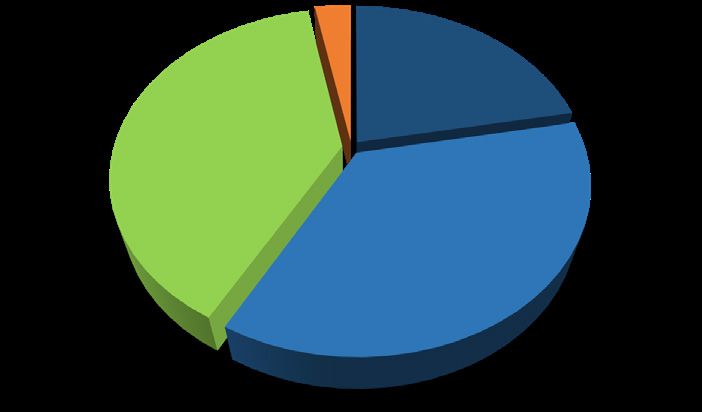

GROWTH EXPECTATION FOR THE US ECONOMY IN 2019

Growth expectation for the US economy in 2019

3% 10%

3%

10%

While the general

outlook for the overall

economy is still very

While thepositive, 3% of

general outlook for the overall

economycompanies expect

is still very positive, a companies

3% of

87%

contraction of the US in 2019.

expect a contraction of the US economy

economy in 2019.

87%

Strong

Stronggrowth

growth> 3%

> 3% Flat

Flat to

tomoderate

moderategrowth 0%0%

growth - 3%- 3%

Contraction < <

Contraction 0%0%

growth

growth

#GABO2019

#GABO2019

STRATEGIC ACTIONS: M&A AND DIVERSIFICATION

Strategic

Strategic Actions:

Actions: M&A

M&A and

and Diversification

Diversification

M&A

M&Aexecuted

M&A executedin

executed inin201

2018

2018

8 M&A

M&Aplanned

M&A plannedin

inin201

2019

2019

9 Diversification

Diversification executed

executed

Diversification executed ininin2018

2018 Diversification

2018 Diversification planned

plannedfor

Diversification planned for

for2019

2019

2019

20%20%

20%

50%50%

50%

9%9%9% 37%

37%

37%

0%

0% 5%

5% 10%

10% 15%

15% 20%

20% 25%

25% 0%

0% 10%

10% 20%

20% 30%

30% 40%

40% 50%

50% 60%

60%

#GABO2019

TOP REASONS FOR FUTURE INVESTMENT IN THE US

Top reasons for future investment in the US

Customer demand for

Customer demand for goods / services

goods / services 80%

80%

The US market’s

attractiveness for German

The US market’s attractiveness for German

subsidiaries for future

subsidiaries for future investment is based on

Proximitytotocustomer

Proximity customer base

base 71%

71%

investment is based on

customer demand, proximity to the customer base

customer

and the relative marketdemand,

stability. proximity

to the customer base and the

Relativemarket

Relative market stability

stability

35%

35% relative market stability.

#GABO2019

WORKFORCE AND VISA CHALLENGES PART 1

Workforce and Visa challenges

Degree of difficulty in attracting

skilled labor 87% of German subsidiaries

still have difficulties

13%

13%

22%

22%

attracting

87% of German skilled

subsidiaries stilllabor.

have difficulties

24%

24% This

attracting highlights

skilled the needthefor

labor. This highlights need for

pipelinespipelines

of qualifiedof qualified

employees, for example

throughemployees,

apprenticeship for example

programs.

41%

through apprenticeship

41%

programs.

Always

Always Veryoften

Very often Sometimes

Sometimes Rarely

Rarely

#GABO2019

#GABO2019

WORKFORCE AND VISA CHALLENGES PART 2

Workforce

Workforce and

and Visa

Visa challenges

challenges

Ease

Easeof

ofreceiving

receivingwork

workvisas

visas2017

2017 Ease

Easeof

ofreceiving

receivingwork

workvisas

visas2018

2018

3%

3% 3%

3%

3% 22%

22% 3%

22%

19%

19%

19% 41%

41%

39%

39%

39%

41%

36%36%

36% 37%

37%

37%

Strongly

Strongly worsened

Stronglyworsened

worsened Slightly

Slightly worsened

Slightlyworsened

worsened No

No change

Nochange

change Positive

Positive Strongly

Strongly worsened

Stronglyworsened

worsened Slightly

Slightly worsened

Slightlyworsened

worsened No

No

No change Positive

change

change Positive

SURVEY CONTINUED

#GABO2019

Importance

IMPORTANCE OF of open

OPEN markets

MARKETS

72% of surveyed companies

state open markets as very

2018

2018 72%

72% important, an increase of

19% over

72% of surveyed last year.

companies state open markets as

very important, an increase of 19% over last year.

An overwhelming

An overwhelming 90% stated that90%

open markets

are ratherstated that open

or very important markets

to their business.

2017

2017

53%

53%

are rather or very important

to their business.

#GABO2019

IMPACT OF NEW TARIFFS AND TRADE CONFLICTS PART 1

Impact of new tariffs and trade conflicts

Impact of tariffs imposed by the US

on China

While only 39% of German

4%

4%

subsidiaries in the US

13%

13%

29%

29% While only 39% of German subsidiaries in the US

reported sourcing products

reported sourcing products from China, a

from China, a staggering

staggering 83% of these companies are negatively

impacted83%

by theof these

tariffs companies

imposed areChina.

by the US on

54% 54% negatively impacted by the

tariffs imposed by the US on

Very negative

Very negative Negative

Negative No impact

No impact Positive

Positive

China.

#GABO2019

IMPACT OF NEW TARIFFS AND TRADE CONFLICTS PART 2

Impact of new tariffs and trade conflicts

Impact on business by

steel/aluminium tariffs

19% of the surveyed

14%

14%

German subsidiaries

31%

19% of the surveyed German subsidiaries

31% process steel and/or

23% process steel and/or aluminium. Of these, 64%

23% aluminium. Of these, 64%

are negatively impacted by the new tariffs on steel

are negatively impacted by

and aluminium.

32%

32%

the new tariffs on steel and

aluminium.

Very negative

Very negative Negative

Negative No impact

No impact Positive

Positive

EXECUTIVE SUMMARY Only 3% of surveyed companies predict a contraction of the US economy, however, 9% see a contraction for their own business, which is the highest since the recession. A large increase of German subsidiaries are planning diversification of their business and M&A as strategic actions in 2019. One major challenge continues to be finding skilled labor, and difficulties in obtaining work visas have increased to 78% of surveyed companies. 90% of respondents say open markets are rather or very important to their business.

WELCOME REMARKS

MICHAELA LUDBROOK

Head of Global Transaction Banking, Americas, Deutsche Bank

Ms. Ludbrook is the Head of Global Transaction Banking, Americas. She joined

GTB in April 2018 as the Global Head of Strategic Execution. Prior to that, Ms.

Ludbrook has held a number of executive positions at Deutsche Bank. Before

joining Deutsche Bank, Ms. Ludbrook worked at Goldman Sachs for seven

years in the US and at JP Morgan for 15 years with assignments in London,

Tokyo and New York in a variety of functions.

RAINER BENDER

Global Chairman of Corporate Banking Coverage, Deutsche Bank AG

Mr. Bender became Global Chairman of Corporate Banking Coverage in

September 2018. He has banking experience since more than 45 years and

his focus was mainly the client coverage of multinational corporate clients.

He started with an apprenticeship in 1970, thereafter worked as branch

manager, credit officer and relationship manager. In 1990 he built a team

for multinational corporates and since then has held had various leading

positions. Prior to his global chairman role Mr. Bender has headed the

corporate banking Germany, Austria and Switzerland franchise.

INTRODUCTORY REMARKS

CAROLL H. NEUBAUER

Chairman & CEO, B. Braun Medical Inc.

Located in Bethlehem, Pennsylvania, the company is a global leader in infusion therapy

and pain management, and a pioneer in passive safety devices and PVC-free and DEHP

free products. Mr. Neubauer oversees the company's North American operations. He

also serves on the B. Braun Global Board in Germany and as Chairman of the German

American Chamber of Commerce, New York.

PETER RIEHLE

President & CEO, WITTENSTEIN Holding Corp.

As President and CEO of WITTENSTEIN Holding Corp., Mr. Riehle is responsible

for all aspects of leading the North American Headquarters of WITTENSTEIN

SE. An award-winning manufacturer of motion control and mechatronics

systems, WITTENSTEIN is renowned in the industry for the quality of its

products and for its innovations in mechatronic drive technology, servo

systems and mechanical components. Prior to his current position, Mr. Riehle

held notable leadership roles in North America spanning 20 years, including

positions as CEO and President at DMG America (DMG/Mori) in Chicago, IL,

and Vice President Sales and Marketing at Trumpf Inc. in Farmington, CT.

ECONOMIC UPDATE

TORSTEN SLOK

Chief International Economist, Deutsche Bank

Mr. Slok’s Economics team has been top-ranked by Institutional Investor in

fixed income and equities since 2010. Prior to joining Deutsche Bank in 2005,

Mr. Slok worked at the OECD in Paris and at the IMF in the Division responsible

for writing the World Economic Outlook and the Division responsible for

China, Hong Kong, and Mongolia. He has published numerous journal articles

in Journal of International Economics, Journal of International Money and

Finance, and The Econometric Journal.

SURVEY PRESENTATION

MARK TOMKINS

President & CEO, GACC Midwest

Mr. Tomkins is the President & CEO of the German American Chamber of

Commerce of the Midwest. He joined the GACC Midwest in March 2006. Prior

to this, Mr. Tomkins spent over 10 years in business development consulting,

working with businesses throughout the world in developing strategic alliances

and long-term cooperations. Prior to this, Mr. Tomkins worked in the automotive

and IT industry in Germany and the US. Within the Chamber, Mr. Tomkins has

been responsible for building the consulting services department and for assisting

German companies in their US market development and has been responsible for

numerous initiatives including the Chamber’s skilled workforce initiative, multiple

conferences, business delegations and pilot projects.

INDUSTRY PANEL MODERATOR: DR. VOLKER TREIER Chief Executive of Foreign Trade, Member of the Executive Board, DIHK Dr. Treier is Member of the Executive Board. As the Chief Executive of Foreign Trade he is responsible for International and European Economic Affairs, the network of bi-national German Chambers, Delegations and Representations of German Industry and Commerce (AHKs) in 92 countries worldwide. CAROLL H. NEUBAUER Chairman & CEO, B. Braun Medical Inc. Located in Bethlehem, Pennsylvania, the company is a global leader in infusion therapy and pain management, and a pioneer in passive safety devices and PVC-free and DEHP free products. Mr. Neubauer oversees the company's North American operations. He also serves on the B. Braun Global Board in Germany and as Chairman of the German American Chamber of Commerce, New York. DANIEL ANDRICH President & CEO, Representative of German Industry + Trade (RGIT) Mr. Andrich is President and CEO, Representative of German Industry and Trade. Prior to this appointment, Mr. Andrich worked for the Federation of German Industries (BDI), one of RGIT’s principals in Berlin, from 2008 to 2016. At BDI, he was Senior Policy Advisor for Global Governance and Trade Promotion and most recently Executive Assistant to BDI President Ulrich Grillo. In 2012, Mr. Andrich worked at RGIT as a visiting fellow and Senior Policy Advisor. PETER RIEHLE President & CEO, WITTENSTEIN Holding Corp. As President and CEO of WITTENSTEIN Holding Corp., Mr. Riehle is responsible for all aspects of leading the North American Headquarters of WITTENSTEIN SE. An award-winning manufacturer of motion control and mechatronics systems, WITTENSTEIN is renowned in the industry for the quality of its products and for its innovations in mechatronic drive technology, servo systems and mechanical components. Prior to his current position, Mr. Riehle held notable leadership roles in North America spanning 20 years, including positions as CEO and President at DMG America (DMG/Mori) in Chicago, IL, and Vice President Sales and Marketing at Trumpf Inc. in Farmington, CT. VINCENT HALMA President & CEO, KION North America Mr. Halma is the President and CEO of KION North America Corporation - a member of the KION Group, one of the world’s two leading manufacturers of industrial trucks and supply chain solutions. His prior experience includes roles as Vice President of the Western European subsidiaries and managing director for STILL Netherlands—one of KION Group’s brand companies. Prior to the KION Group, he served in a variety of capacities at Cargotec Corporation—the leading provider of cargo handling solutions.

ABOUT US GACCs The German-American Chambers of Commerce (GACCs) in Atlanta, Chicago, Detroit, Houston, New York, Philadelphia, Pittsburgh and San Francisco all work together under the network of the GACCs. With approximately 2,500 members and an extensive national and international business network, the GACCs offer a broad spectrum of activities and services. Other German-American organizations and chapters are affiliated with the GACCs. The German Chamber Network (AHKs) is closely connected to the Chambers of Industry and Commerce (IHKs) in Germany. The umbrella organization of the IHKs is the German Association of Chambers of Industry and Commerce (DIHK), which speaks for 3.6 million business enterprises in Germany, coordinating and supporting the AHKs. GLOBALLY CONNECTED AHKs provide experience, connections, and services worldwide through 140 locations in 92 countries. The service portfolio of the AHKs is unified worldwide under the brand name DEinternational. The AHKs cooperate closely with the foreign trade and inward investment agency of the Federal Republic of Germany—Germany Trade & Invest (GTAI). www.ahk-usa.com RGIT The Representative of German Industry and Trade (RGIT) communicates the interests of German business on behalf of its principals, the Federation of German Industries (BDI) and the Association of German Chambers of Commerce and Industry (DIHK) in Washington, DC. Through its actions, RGIT highlights the importance of German business in the U.S. and encourages the further deepening of the U.S. and Germany’s already close economic ties. This material is distributed by the Representative of German Industry and Trade (RGIT) on behalf of the Federation of German Industries (BDI) and the Association of German Chambers of Commerce and Industry (DIHK). Additional information is available at the Department of Justice, Washington, DC. www.rgit-usa.com

CONTACT GACC MIDWEST GACC NEW YORK GACC SOUTH Mark Tomkins Dietmar Rieg Stefanie Ziska President & CEO President & CEO President & CEO T +1 312 494-2172 T +1 212 974-8848 T +1 404 586-6815 tomkins@gaccmidwest.org drieg@gaccny.com sziska@gaccsouth.com www.gaccmidwest.org www.gaccny.com www.gaccsouth.com GACC WEST RGIT WASHINGTON Kristian Wolf DANIEL ANDRICH President & CEO President & CEO T +1 415 248-1241 T +1 202 659-4777 kwolf@gaccwest.com dandrich@rgit-usa.com www.gaccwest.com www.rgit-usa.com

You can also read