Horizons et Tendances - EPAS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Horizons et Tendances, 9 janvier 2019 1

Formation continue

Horizons et Tendances

Mercredi 15 janvier 2020, Lausanne

www.epas.ch

Horizons et Tendances, 9 janvier 2019 2

Horizons et Tendances, 15 janvier 2020

Perspectives économiques /

investissements 2020

Vincent Juvyns

www.epas.ch

Global growth GTM – Europe |4

Real GDP growth Contribution to global real GDP growth

% change year on year % change year on year

6 5

4 4

Global economy

2 3

0 2

-2 1

-4 0

2020

consensus forecast Global

-6 -1 China

US 1,8%

EM ex-China

UK 1,1%

-8 -2 DM ex-US

Eurozone 1,0%

US

Japan 0,3%

-10 -3

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20 '85 '88 '91 '94 '97 '00 '03 '06 '09 '12 '15 '18

Source: (Left) BEA, Bloomberg, Eurostat, Japan Cabinet Office, ONS, Refinitiv Datastream, J.P. Morgan Asset Management. Forecasts are from Bloomberg contributor composite. (Right) Refinitiv Datastream, World Bank,

J.P. Morgan Asset Management. EM is emerging markets. DM is developed markets.

Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

3

Global Purchasing Managers’ Index (PMI) for manufacturing GTM – Europe | 5

2019

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Nov Dec

Global 50,3 50,1

Developed 49,5 49,1

Emerging 51,0 51,0

Global economy

Eurozone 46,9 46,3

France 51,7 50,4

Germany 44,1 43,7

Eurozone

Italy 47,6 46,2

Spain 47,5 47,4

Greece 54,1 53,9

Ireland 49,7 49,5

Sweden 45,7 47,1

Developed

Switzerland 48,8 50,2

UK 48,9 47,5

US 52,6 52,4

Japan 48,9 48,8

China 51,8 51,5

Indonesia 48,2 49,5

Korea 49,4 50,1

Emerging

Taiwan 49,8 50,8

India 51,2 52,7

Brazil 52,9 50,2

Mexico 48,0 47,1

Russia 45,6 47,5

Source: Markit, J.P. Morgan Asset Management. The Global Purchasing Managers’ Index (PMI) for manufacturing assesses the economic health of the sector by

surveying manufacturing businesses regarding output, new orders, stocks of purchases, supplier delivery times and employment. A score of 50 indicates that economic

activity is neither expanding nor contracting, above 50 indicates expansion. The colours range from red to yellow to green, where red is below 50, yellow is at 50 and

green is above 50. Quarterly averages are shown, except the two most recent monthly data points. Past performance is not a reliable indicator of current and future

results. Guide to the Markets - Europe. Data as of 31 December 2019.

4

Global core inflation and inflation expectations GTM – Europe |8

Core inflation Market-based inflation expectations

% change year on year %, 5y5y inflation swap

5 5

4 4 UK

Global economy

Headline inflation

target

3 3

US

2 2

1 1 Eurozone

Japan

0 0

US

-1 UK -1

Eurozone

Japan

-2 -2

'07 '09 '11 '13 '15 '17 '19 '07 '09 '11 '13 '15 '17 '19

Source: (Left) Bank of Japan, BLS, Eurostat, ONS, Refinitiv Datastream, J.P. Morgan Asset Management. CPI is the Consumer Price Index. Core inflation for the US is defined as CPI excluding food and energy. Core

inflation for Japan is defined as CPI excluding fresh food and energy. Core inflation for the UK and the eurozone is defined as CPI less energy, food, alcohol and tobacco. Japan core CPI has been adjusted down by 2% from

April 2014 to March 2015 to remove the estimated impact of the consumption tax hike over this period. (Right) Bloomberg, J.P. Morgan Asset Management. 5y5y inflation swap represents the market’s expectation of five-year

average inflation, starting in five years’ time. Data for Japan starts in March 2007 due to data availability. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31

December 2019.

5

Global central bank policy GTM – Europe |9

Market expectations for policy rate Central bank balance sheets

% USD trillions

12-month change Global central bank

2.0 3.0 18

in balance sheet balance sheet

Forecast*

2.5 16

1.6

Global economy

US

14

2.0

1.2

12

1.5

0.8 10

UK

1.0

0.4 8

0.5

6

Japan

0.0

0.0

4

Eurozone

-0.4

Switzerland -0.5 2

-0.8 -1.0 0

Dec ’19 Dec ’20 Dec ’21 Dec ’22 Dec ’23 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Source: (Left) Bloomberg, J.P. Morgan Asset Management. Expectations are calculated using OIS forwards. (Right) Bank of England (BoE), Bank of Japan (BoJ), European Central Bank (ECB), Refinitiv Datastream, Swiss

National Bank (SNB), US Federal Reserve (Fed), J.P. Morgan Asset Management. Global central bank balance sheet is the sum of the balance sheets of the BoE, BoJ, ECB, Fed and SNB. *Balance sheet forecast

assumptions: BoE to have zero net asset purchases over the forecast period; BoJ to have an annualised net asset purchase pace of 20 trillion yen over the forecast period; ECB to have net asset purchases of 20 billion

euros per month over the forecast period; SNB to have zero net asset purchases over the forecast period; Fed to increase assets by USD 60 billion per month through to June 2020, after which it is assumed that the balance

sheet will remain steady. Past performance is not a reliable indicator of current and future results.

Guide to the Markets - Europe. Data as of 31 December 2019.

6

Global income GTM – Europe | 48

Asset yield comparison

% yield

Equity

10 9.4

Fixed income

8 Average Europe inflation: 1,5% Alternatives

(12 months to November 2019) 5.5

6 4.8 4.8

4.1 4.2

4 3.4

2.3 2.6

2

0.0 0.5

0

-0.2

-2

German Cash Euro IG DM equity EM equity MSCI Global Global REITs Global EM debt DM high yield Global

Equities

Bunds Europe convertibles infrastructure transport

Equity index yields

% yield Buyback yield

6 Dividend yield

5

4

3

2

1

0

FTSE All-Share S&P 500 MSCI World MSCI Europe ex-UK MSCI Japan MSCI EM

Source: (Top) Bloomberg Barclays, BofA/Merrill Lynch, Clarkson, Drewry Maritime Consultants, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management. Additional yield often comes with

associated capital and/or liquidity risk. Global infrastructure and global transport yields are as of March 2019 and June 2019, respectively. Yields for the bond indices are yield to worst and dividend

yields for the equity indices. Global transport levered yield is rental income minus operating expenses, debt amortisation and interest expenses, expressed as a percentage of equity value. Global

convertibles: Bloomberg Barclays Global Convertibles; DM equity: MSCI World; EM equity: MSCI EM; German bunds: Germany 10-year yield; Euro IG: Bloomberg Barclays Euro Agg. –

Corporates; Global REITs: FTSE NAREIT Index; DM high yield: BofA/Merrill Lynch Developed Markets High Yield Constrained; EM debt: J.P. Morgan EMBI Global; Global infrastructure: MSCI

Global Infrastructure Asset Index – Low risk. (Bottom) Bloomberg, FTSE, MSCI, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management. Buyback yield is last twelve months

buybacks divided by the market cap of the index. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2019.

7

Horizons et Tendances, 9 janvier 2019 9

Horizons et Tendances, 15 janvier 2020

Quels placements et asset classes

favoriser pour 2020?

Eric Rosset

www.epas.ch

2019 WITHIN THE TOP 3 VINTAGE YEARS

Pictet LPP 40 Index – Annual Returns (Rebased)

Source: Pictet Asset Management, Refinitiv, December 2019

Perspectives d'investissement 2020

10 Pictet Asset Management

A l'attention des investisseurs professionnels

LOOKING INTO 2020

› ‘Slowdown part 2’ › Last missing piece to global easing

jigsaw

› US lags global slowdown

› Odds tilted towards more Fed easing

Global China’s › Clear need of easing

Desynchronised Defensive Easing

Slowdown

› Multiple constraints (including

‘stagflation’)

› ‘Initial recovery part 1’ › Diversifying away from negative

Paradigm Shift Constructing yielding debt

› Test cases: India, Korea, EMU, UK

in Policy Mix Robust Portfolios

› US election: the next big step forward

› Using optionality to capture growth

surprises

in this shift?

› Keeping credit risk at bay

Source: Pictet Asset Management, December 2019

Perspectives d'investissement 2020

11 Pictet Asset Management

A l'attention des investisseurs professionnels

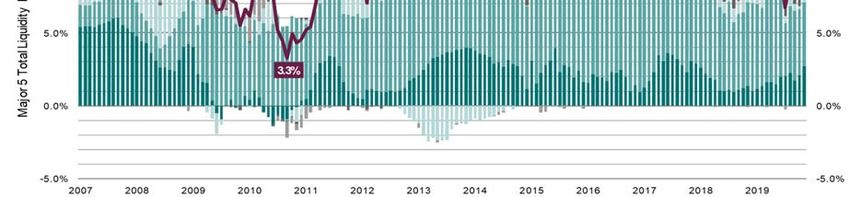

FROM TIGHTENING TO PIVOT AND MODEST EASING

Major 5 – Total (Policy & Private) Liquidity Flow by Major Bloc (6-Month Rolling, % GDP)

Double tightening

Pivot

2007 Peak 2017 Peak

50% US 20% US

20% China 50% China

Note: Total Liquidity flow calculated as Policy plus Private Liquidity flows, as % of nominal GDP, using current-USD GDP weights (US: 36.9%, China: 26.1%, EMU: 23.5%, Japan: 8.7%, UK: 4.9%)

Source: Refinitiv Datastream, Pictet Asset Management

Perspectives d'investissement 2020

12 Pictet Asset Management

A l'attention des investisseurs professionnels

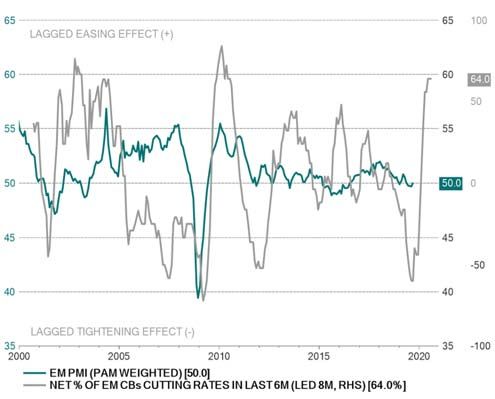

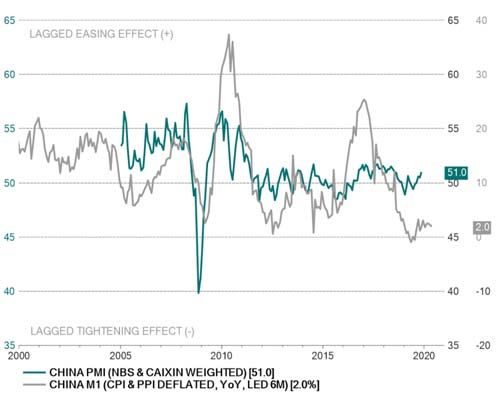

ONE MISSING PIECE TO GLOBAL EASING PUZZLE? CHINA

EM – Activity & Central Bank Breadth China – Activity & Policy Easing

Source: Pictet Asset Management, Refinitiv, December 2019 Source: Pictet Asset Management, Refinitiv, December 2019

Perspectives d'investissement 2020

13 Pictet Asset Management

A l'attention des investisseurs professionnels

ANGLO-SAXON BONDS TO PROVIDE PORTFOLIO BALANCE

US – 10Yr Yield & 10% Return Implied Target Swiss – 10Yr Yield & 10% Return Implied Target

Source: Pictet Asset Management, Refinitiv, December 2019 Source: Pictet Asset Management, Refinitiv, December 2019

Perspectives d'investissement 2020

14 Pictet Asset Management

A l'attention des investisseurs professionnels

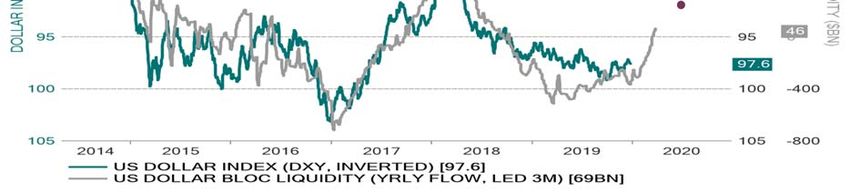

USD LIQUIDITY TIGHTNESS TO FADE AWAY

US Dollar Index (DXY) v. US Dollar Bloc Liquidity ($bn)

Source: Pictet Asset Management, Refinitiv, December 2019

Perspectives d'investissement 2020

15 Pictet Asset Management

A l'attention des investisseurs professionnels

GROWTH INCREASINGLY VULNERABLE, INCREMENTAL SHIFT TO VALUE

Global IT – Price v. Earnings Global Financials – Price v. Earnings

Source: Pictet Asset Management, Refinitiv, December 2019 Source: Pictet Asset Management, Refinitiv, December 2019

Perspectives d'investissement 2020

16 Pictet Asset Management

A l'attention des investisseurs professionnels

CORE VIEWS FOR 2020

› Risk budget allocation: market weight in equities, using optionality where possible, keep

duration long

› US slowdown part 2: keep defensive equities (staples, utilities, REITs, healthcare), shave

cyclical growth equities

› Initial recoveries part 1: dedicate a risk budget to corners of Europe (domestic oriented) and

GEM (India, Korea) equities

› Portfolio balance: rotate into Anglo-Saxon core bonds (US, UK, Canada, Australia)

› Weaker US dollar: favour US TIPS & EM LC debt, keep gold

› Beware credit: more companies falling into BBB and out of BBB into High Yield

Perspectives d'investissement 2020

17 Pictet Asset Management

A l'attention des investisseurs professionnels

For more information

This marketing material is for distribution to financial situation, or to obtain specific advice names of all MSCI indexes and products) are

PICTET ASSET MANAGEMENT professional investors only. This marketing from an industry professional. trademarks of MSCI or its subsidiaries.

document is issued by Pictet Asset Management

Rte des Acacias 60 S.A.. It is neither directed to, nor intended for The value and income of any of the securities or For active equities funds, please note that the

financial instruments mentioned in this strategy is benchmark agnostic; the MSCI World

1211 Geneva 73 distribution or use by any person or entity who

is a citizen or resident of, or domiciled or document may fall as well as rise and, as a is not a benchmark but a reference index which

consequence, investors may receive back less serves as a proxy for Global Equities (other

www.group.pictet located in, any locality, state, country or

jurisdiction where such distribution, publication, than originally invested. Risk factors are listed proxies such as MSCI ACWI are equally

availability or use would be contrary to law or in the fund’s prospectus and are not intended to appropriate). The strategy’s investment

regulation. Only the latest version of the fund’s be reproduced in full in this document. universe is more concentrated than global

indices as it is limited to the theme, but it

@PictetAM prospectus, the KIID (Key Investor Information Past performance is not a guarantee or a contains stocks not included in those indices as

Document), regulations, annual and semi-annual reliable indicator of future performance.

reports may be relied upon as the basis for it is unconstrained in sizes and regions.

Performance data does not include the Reference indices do not influence the portfolio

investment decisions. These documents are commissions and fees charged at the time of construction process.

Pictet Asset Management Switzerland available on www.assetmanagement.pictet or at subscribing for or redeeming shares. This

Pictet Asset Management S.A. , 60 Route des marketing material is not intended to be a

Acacias – 1211 Geneva 73. substitute for the fund’s full documentation or

The information and data presented in this for any information which investors should

assetmanagement.pictet document are not to be considered as an offer obtain from their financial intermediaries acting

or solicitation to buy, sell or subscribe to any in relation to their investment in the fund or

securities or financial instruments. funds mentioned in this document.

mega.online Information, opinions and estimates contained in Pictet Asset Management SA has not acquired

this document reflect a judgment at the original any rights or license to reproduce the

date of publication and are subject to change trademarks, logos or images set out in this

without notice. Pictet Asset Management S.A. document except that it holds the rights to use

has not taken any steps to ensure that the any entity of the Pictet group trademarks. The

securities referred to in this document are trademarks, logos and images set out in this

suitable for any particular investor and this document are used only for the purpose of this

document is not to be relied upon in substitution presentation.

for the exercise of independent judgment. Tax This document is for information purposes only.

treatment depends on the individual They should not be considered by the recipient

circumstances of each investor and may be as an offer, an invitation or a personal

subject to change in the future. Before making recommendation to acquire or sell any product

any investment decision, investors are or fund or subscribe to any asset management

recommended to ascertain if this investment is service.

suitable for them in light of their financial

knowledge and experience, investment goals and MSCI marks used in this paper (including the

Perspectives d'investissement 2020

18 Pictet Asset Management

A l'attention des investisseurs professionnels

Horizons et Tendances, 9 janvier 2019 19

Horizons et Tendances, 15 janvier 2020

Perspectives pour le marché

immobilier

Damian Künzi

www.epas.ch

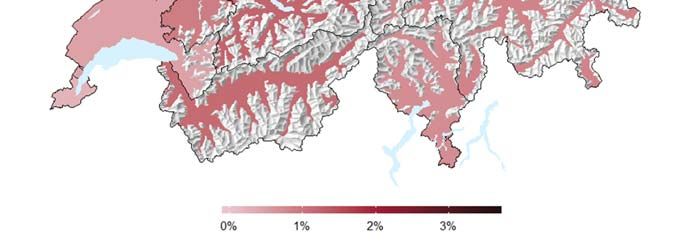

Un cycle immobilier long et mature en Suisse

22 ans

14 ans x 2.4

x 2.6

16 ans

x 2.4

Prix des maisons à

plusieurs logements,

indice TRX de Wüest

Partner

Source: Wüest Partner

20 | Horizons et tendances | 15.01.2020Comment investir dans une période de

répression financière prolongée?

%

21 | Horizons et tendances | 15.01.2020

Prime de risque sur l’immobilier Suisse :

attrayante et sans alternative

%

%

22 | Horizons et tendances | 15.01.2020Défi 1 : ralentissement de l’économie suisse

et du solde migratoire

2

90000

70000 1

points de %

personnes

50000

0

30000

-1

10000

-10000 -2

1995 2000 2005 2010 2015 2020

Solde migratoire, échelle gauche

Différence de croissance Suisse/zone euro, échelle droite

23 | Horizons et tendances | 15.01.2020

Défi 2 : écart croissant entre offre et

demande, hausse des taux de vacance

Source : Office fédéral de la statistique, Swiss Life

Taux de vacance

24 | Horizons et tendances | 15.01.2020Défi 3 : augmentation de la pression politique

Problèmes d’accessibilité des prix

Genève : Initiative populaire «Construisons des logements pour toutes et tous»

approuvée le 24 novembre 2019

Berlin: introduction d’un gel temporaire des loyers

Bâle: plusieurs initiatives en attente de mise en œuvre :

En période de pénurie, les investisseurs doivent demander des autorisations

de projets de rénovation ou de démolition pour les «logements abordables»

Suisse : initiative populaire fédérale «davantage de logements abordables»,

mise en votation le 9 février 2020

Nouvelles règles en matière d’efficacité énergétique

25 | Horizons et tendances | 15.01.2020

Notre réponse : gestion active innovante et

préférence donnée aux emplacements centraux

Projet «Cornaredo

Park» à Lugano

Source : Archilyse, Swiss Life Asset Managers

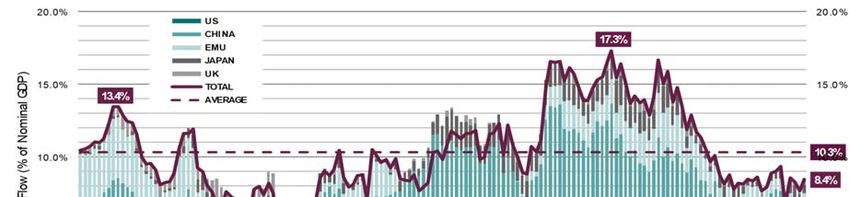

26 | Horizons et tendances | 15.01.2020Prime de risque plus élevée à l’étranger

Rendements de bureaux «prime» au T3 2019

5%

4.50%

4.2% 4.00% 3.95%

4%

3.40% 3.30% 3.23% 3.25% 3.25%

2.43% 3.12% 3.09%

3% 2.70%

2.60%

2.30%

2.00% 3.52% 2.12%

3.67%

2% 4.02%

3.64% 3.57% 3.56% 3.49% 3.38% 3.27% 3.08%

3.00%

2.70%

2.40%

1% 2.07%

1.13%

0.48% 0.28%

0% 0.17%

-0.02% -0.24% -0.27% -0.26% -0.29%

-0.40% -0.40% -0.40% -0.44% -0.57%

-1%

Rendements des obligations Prime de risque immobiliers Rendements de

d'Etat à 10 ans vs. rendements des obligations d'Etat bureaux «prime»

Source : PMA, Wüest Partner, Cushman & Wakefield Macrobond ¦ Rendement des obligations d’Etat en moyenne trimestrielle; *T2 2019

27 | Horizons et tendances | 15.01.2020

Disclaimer

• Publié et approuvé par le Département économique

Swiss Life Asset Managers, Zurich

• Swiss Life Asset Managers est susceptible d’avoir suivi ou utilisé les recommandations présentées plus haut avant leur publication. Bien

que nos prévisions soient basées sur des sources considérées comme fiables, aucune garantie ne saurait être donnée quant à

l’exactitude et à l’exhaustivité des informations utilisées. Le présent document contient des prévisions portant sur des évolutions futures.

Nous ne nous engageons ni à les réviser, ni à les actualiser. Les évolutions effectives peuvent fortement différer de celles anticipées dans

nos prévisions.

28 | Horizons et tendances | 15.01.2020You can also read