How banks can use AI to transform the customer experience - May 2020 - In collaboration with - Efma

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

REPORT How banks can use AI to transform the customer experience May 2020 In collaboration with

The expert’s point of view

Over the last 12 months, Efma’s senior advisor Rudradeb Mitra had the opportunity to interact with

bankers (C-level executives as well as department heads) from over 20 countries, from Africa, Asia,

Europe, and South America, and the most common question he encountered was – ‘Is AI all hype’?

Let me answer this question through the story of Segway Inc. Segway Inc. was founded by Dean Kamen with a

dream of making a zero-emission transportation vehicle. Right from the beginning, it got a lot of interest, and it

was speculated “to be the fastest company to reach $1 billion in sales” and “to become more important than

the internet”. It was backed by people like Amazon’s Jeff Bezos and Apple’s Steve Jobs. The rest is well-known

history. Segway never even came close to its promises and can be considered a failure.

There were many reasons for the failure of Segway but the most important reason, as mentioned by Ron Bills,

CEO of Segway in 2004, was a lack of focus on the value creation. What problems does a Segway solve? And

at what costs (a Segway is not affordable for the majority of people)? Where could it be integrated into traffic?

Where could it be charged? Most of these questions remained unanswered, and consequently, the Segway could

not live up to the initial hype.

Great technology does not necessarily make a successful product. Success is always based on the

value created. So keep it simple stupid and focus on creating value.

Artificial intelligence has all the right ingredients to be a disruptive technology. However, now it is time to lay the

foundation for the future. It can either become another over-hyped technology or the next internet or something

even more significant.

One of the key places where banks can create a lot of value is improving customer experience.

‘‘

I think the most important thing is to have empathy and really listen to your

customers. I cannotThe full content ofenough

emphasize this report

howisimportant

exclusively it isreserved for talk as if

to not simply

you are customer Efmacentric.

memberYou institutions. If you

need to live andwish to know

breathe this more

everyabout

day.

gaining full access to

Ben Chisell, product director at Starling Bank.exclusive content, as well as other

benefits, go to www.efma.com/joinefma or contact

membership@efma.com

In the past, the banking customer experience was mostly restricted to in-branch, from the point a customer enters

a bank branch to the point she leaves it. In such a scenario, it was easier to listen to each individual customer

and build relations. These days, however, most customers interact with their banks via devices, which is both

an opportunity and a threat. Opportunities such as this give direct, 24/7 access to customers with a lot of

personalized data but can also be a threat if banks decide to keep on using old models of customer experience

and engagement.

3

In today’s digital era, banks need to build new customer-centric models to comfort actual

psychology of decision making and offer personalized communications, interactions, and

acquisitions. Such models will ensure that banks can bring every individual customer back

to the forefront of their operations.

Using machine learning to learn patterns in customer experience

‘‘

The future of business is consumer to business, not business to consumer.

Businesses must customize for consumers.

Jack Ma, executive chairman at Alibaba.

Let us look at a couple of ways how businesses can customize to customers and see how AI can help create new

customer centric models. Figure 1 shows the focus areas of banks in terms of achieving operational excellence,

and the corresponding column represents the relevance of artificial intelligence in achieving the goal.

Figure 1: Focus areas for operational excellence and artificial intelligence [1]

Focus area Operational Artificial

excellence intelligence

Increase transparency and frequency

in communication

Refocus on client risk/return profile

Focus on easy-to-access and easy-to-deal with

private bankers and simplify process

The full

Enhance pro-activeness andcontent of this

anticipation of report is exclusively reserved for

client needs Efma member institutions. If you wish to know more about

gaining full access to exclusive content, as well as other

Simplify certain products

benefits, go to www.efma.com/joinefma or contact

membership@efma.com

Reduce # of relationships per relationship

manager

Enhance array of products

Enhance technical and product skill set of

private bankers

Produce more reliable, timely management

information and comprehensive external

reporting

Relevance High Medium Low

4 How banks can use AI to transform the customer experience

We will take two use cases from the focus areas and show how artificial intelligence can be used.

Case I: Predicting customer needs and creating customized communications

Imagine that you are a customer who is thinking of buying a car and around the same time, you receive a

communication from your bank informing you that you are entitled to excellent loan terms if you take out a car

loan in the next five days. Bingo! Won’t that make you feel like your bank values and cares for you?

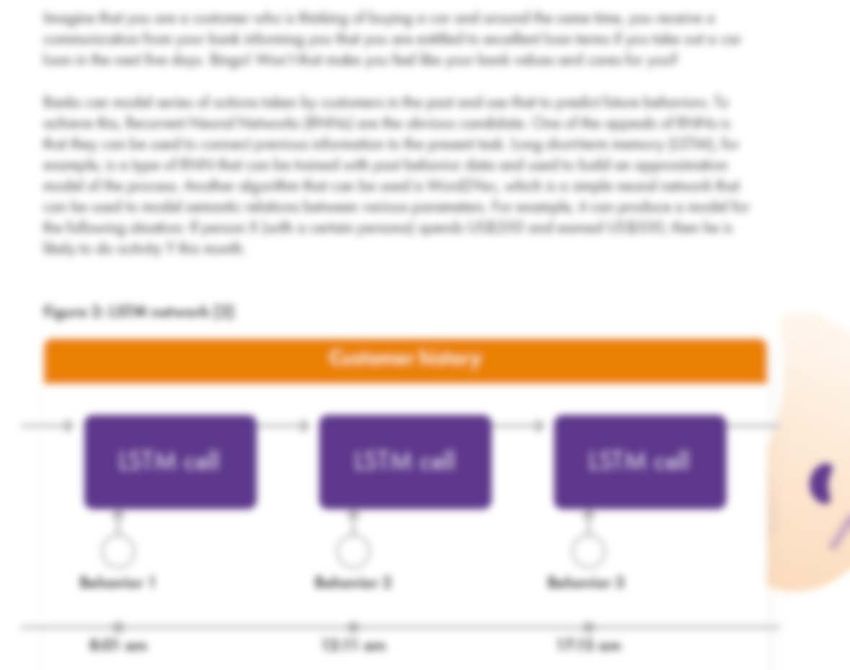

Banks can model series of actions taken by customers in the past and use that to predict future behaviors. To

achieve this, Recurrent Neural Networks (RNNs) are the obvious candidate. One of the appeals of RNNs is

that they can be used to connect previous information to the present task. Long short-term memory (LSTM), for

example, is a type of RNN that can be trained with past behavior data and used to build an approximation

model of the process. Another algorithm that can be used is Word2Vec, which is a simple neural network that

can be used to model semantic relations between various parameters. For example, it can produce a model for

the following situation: If person X (with a certain persona) spends US$200 and earned US$500, then he is

likely to do activity Y this month.

The full content of this report is exclusively reserved for

Efma member institutions. If you wish to know more about

gaining

Figure 2: LSTM network [2] full access to exclusive content, as well as other

benefits, go to www.efma.com/joinefma or contact

membership@efma.com

Customer history

LSTM cell LSTM cell LSTM cell

Behavior 1 Behavior 2 Behavior 3

8:01 am 12:11 am 17:15 am

5

You can also read