Howard Hughes Enjoys Solid Growth Due to Strong Land Sales Performance

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SAIBUS

RESEARCH November 19, 2012

Howard Hughes Enjoys Solid Growth Due to

Strong Land Sales Performance

Our firm owns The Howard Hughes Corporation (HHC) and we have owned it since November

2010, when it was spun-off from General Growth Properties (GGP). We are pleased that our

investment has nearly doubled in this time. We are more pleased with the fact that Howard

Hughes is no longer buried under GGP’s ownership and now is its own independent company.

Howard Hughes saw its revenues bottom out in 2009 at $136.3M, which included $34.6M in

Master Planned Community land sales. We expect HHC’s total revenue to potentially reach

$350M in 2012 and MPC land sales to potentially top $160M. Our expectations are based upon

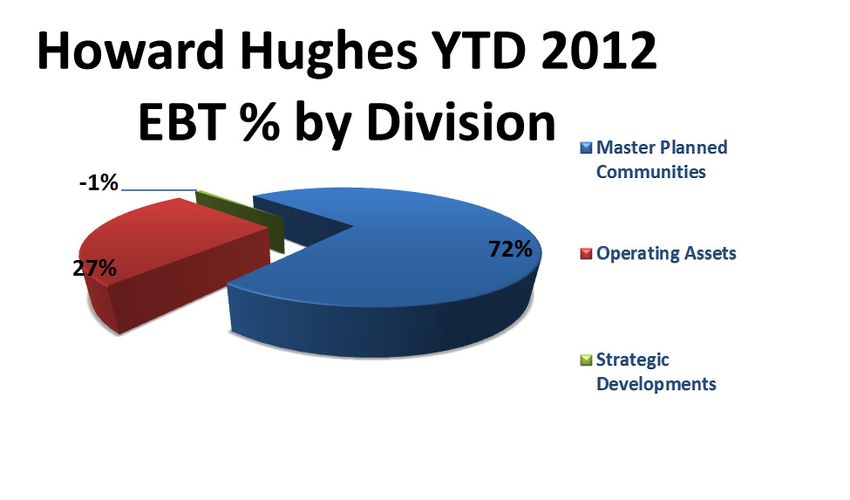

HHC’s solid YTD 2012 performance in which the company generated $268.5M in total

revenues, and the key driver continues to be its MPC land sales, which contributed $120M, or

nearly half of its revenue.

Source: Howard Hughes 2010-2011 Annual Reports and Saibus Research estimates

Howard Hughes enjoyed continued solid performance in the second quarter of 2012. While

seeing a $215M year-over-year decline in a quarter’s profits versus the prior year’s comparable

period is never pleasant, we have taken note of the following non-operating factors that are

influencing this negative shift:

$234.2M decline in its warrant liability gain versus the prior year’s period. In our first

report on Howard Hughes, we elaborated on how declines in the company’s stock price

during a quarter result in a non-cash non-operating gain on the warrant liabilities it

issued to its management sponsors and gains in the stock price result in a non-cash

non-operating loss

$2.9M non-cash loss on the remeasurement of its tax indemnity receivables related to its

Tax Matters (Spin-off) Agreement with GGP. GGP indemnified HHC against 93.75% of

all losses, claims, damages, liabilities and reasonable expenses to which it is subjected,

in each case solely to the extent directly attributable to certain taxes related to sales of

certain assets in its MPC segment prior to March 31, 2010, in an amount up to $303.8

million, plus interest and penalties related to these amounts so long as GGP controls the

1

www.saibusresearch.com

SAIBUS

RESEARCH November 19, 2012

action in the Tax Court related to the dispute with the IRS as described below.

Excluding these non-operating, non-cash headwinds, the company’s adjusted Q3 2012

operating income increased by nearly 700% versus Q3 2011 levels and 227% for YTD

2012 versus YTD 2011 levels.

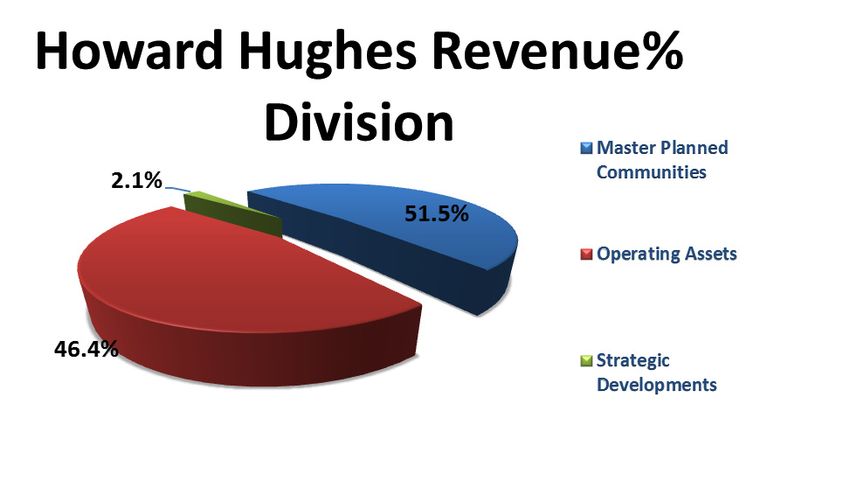

Howard Hughes saw significant year-over-year reported revenue growth, like in H1 2012.

However, H1 2012 reported revenue growth was driven by its acquisition of the minority interest

in The Woodlands that it did not previously own. Q3 2012 revenues are comparable to Q3 2011

revenues because the acquisition of the minority interest in The Woodlands was early in the Q3

2011 period. The company also saw growth from its conference center and resort properties,

minimum guaranteed rents from operating properties and other land and rental property

revenues, which more than offset a sharp decline in condominium unit sales revenues and other

related strategic developments revenues.

Source: Howard Hughes Q3 2012 10-Q

Master Planned Communities: Because Howard Hughes is now owns The Woodlands

outright, we believe that this will provide the company with the control it needs to maximize the

value of its assets. On a pro forma basis assuming The Woodlands minority interest was

acquired on January 1, 2011 instead of July 2011, revenues from the Master Planned

Communities segment of $48.6M in Q3 2012 showed strong growth relative to the $41.1M

achieved in Q3 2011. Master Planned Communities EBT of $20.8M was strong relative to the

$7.4M achieved in Q3 2011. This was incredible even though the company was facing a

softening macroeconomic environment. For the three and nine months ended September 30,

2012, HHC MPC sold 96.3 and 292.5 residential acres as compared to 77.1 and 269.1 acres for

the three and nine months ended September 30, 2011. The majority of the residential acres

sold during the first nine months of 2012 were from The Woodlands (151 acres), Summerlin

(71.6 acres) and Bridgeland (63.9 acres) communities. Variances in price per acre are largely

attributable to selling certain product types in different locations.

Operating Assets: HHC’s best performing division this year has been the Operating Assets.

These assets are what attracted our firm to Howard Hughes in the first place and why we have

2

www.saibusresearch.com

SAIBUS

RESEARCH November 19, 2012

maintained our holding in it. On a pro forma basis, this division saw its Q3 2012 revenue

increase by 14.44% versus Q3 2011 levels. YTD 2012 revenue reached $124.6M and

increased by 12% versus YTD 2011 levels. All three service lines within the Operating Assets

division saw 10% revenue growth or more. This healthy revenue increase for HHC Operating

Assets was primarily related to higher occupancy at the Resort and Conference Center,

stabilization of two office properties located in The Woodlands, specialty lease programs at

South Street Seaport and Riverwalk Marketplace and new leases at Ward Centers. The

division also benefitted from positive operating leverage keeping Q3 2012 expenses of $37M

flat with adjusted Q4 2011 levels. This enabled the division to generate a solid 10% EBT

margin for the quarter and 16% YTD levels, up from less than 0.5% in Q3 2011 and less than

10% for YTD 2011.

Strategic Developments are HHC’s smallest operating segment. It’s a good thing that it is the

smallest segment because these assets generally require substantial future development to

achieve their highest and best use. Other than the residential condominium project located in

Nouvelle at Natick (Boston, Massachusetts), which is now sold out, the remaining properties in

this segment generate little to no revenues. Expenses relating to these assets are primarily

related to carrying costs, such as property taxes and insurance, and other ongoing costs related

to maintaining the assets in their current condition. Revenue declined on a year-over-year basis

because Condominium unit sales decreased as it only sold zero and two condominium units at

Nouvelle at Natick for the three and nine months ended June 30, 2012, respectively, and have

no remaining units at September 30, 2012. These 2012 sales were units designated for low-

income housing.

Source: Howard Hughes Q3 2012 10-Q

We like the fact that the majority of Howard Hughes’s stock is backed by four leading

institutional investors, which includes Bill Ackman (Pershing Square) and Brookfield Asset

Management’s (BAM) Brookfield Retail Holdings subsidiary. We like that Howard Hughes is now

an independent company, no longer subject to the bureaucracy and capital needs of the highly

leveraged General Growth Properties and we like Howard Hughes’s portfolio of high-end

properties. While GGP is a highly leveraged company that must pay out 90% of its pro-forma

taxable income as ordinary dividends to shareholders in order to qualify as a tax-exempt Real

3

www.saibusresearch.comSAIBUS

RESEARCH November 19, 2012

Estate investment trust, Howard Hughes utilizes shareholders’ equity in order to finance 65% of

its assets. Mortgages and stock warrant liabilities only account for ~25% of asset financing and

the rest is financed by operating working capital liabilities, which are more than offset by cash

and operating working capital assets.

In conclusion, we’re satisfied with our holding in The Howard Hughes Corporation. We believe

that investors who want to invest in the real estate industry should consider The Howard

Hughes Corporation. We like that Howard Hughes enjoyed an unexpected positive free cash

flow of $47M in 2011 and $39M in the year-to-date period. We like that Howard Hughes has

had strong growth from its Master Planned Communities and Operating Assets profits and these

divisions have powerful operating leverage that results in the conversion of sales growth to a

high level of incremental operating income growth. Finally, we are long Howard Hughes

because we find that very few companies can even hope to replicate Howard Hughes’s portfolio

of high-end master planned communities, retail properties, office buildings and strategic land

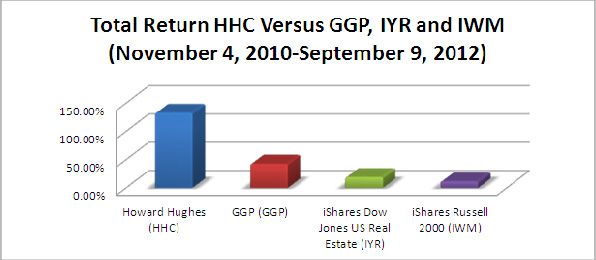

development. Since Howard Hughes has gone public, it has outperformed its former parent as

well as the iShares Dow Jones US Real Estate ETF (IYR) and the iShares Russell 2000 (Small

Cap) Index ETF (IWM). Despite HHC’s strong performance relative to other real estate

companies, it is only trading at a 24.77% premium to book value.

Source: Morningstar Direct

4

www.saibusresearch.comSAIBUS

RESEARCH November 19, 2012

DISCLAIMER

Past performance is not necessarily indicative of future results. All investments involve risk

including the loss of principal. This report is confidential and may not be distributed without the

express written consent of the original author and does not constitute a recommendation, an

offer to sell or a solicitation of an offer to purchase any security or investment product. Any such

offer or solicitation may only be made by means of delivery of an approved confidential private

offering memorandum.

Investments may currently or in the future buy, sell, cover or otherwise change the form of its

investment in the companies discussed in this letter for any reason. The author hereby

disclaims any duty to provide any updates or changes to the information contained here

including, without limitation, the manner or type of any of the investments.

All of the views expressed in this research report accurately reflect the research analysts’

personal views regarding any and all of the subject securities or issuers. The research analyst is

not registered with FINRA, and may not be subject to FINRA rule 2711 restrictions on:

communicating with the subject company, public appearances, and trading securities held in the

research analysts’ account. No part of the analysts’ compensation was, is, or will be, directly or

indirectly, related to the specific recommendations or views expressed in this research report.

The analyst responsible for the production of this report certifies that the views expressed herein

reflect his or her accurate personal and technical judgment at the moment of publication.

Under no circumstances must this document be considered an offer to buy, sell,

subscribe for or trade securities or other instruments.

Disclosure: Our firm is long HHC

Copyright 2011-2012 Saibus Research. All rights reserved. This report or any portion hereof may not be

reprinted, sold or redistributed without the written consent of Saibus Research.

5

www.saibusresearch.comYou can also read