Information booklet launceston retail audit and activity centres strategy: RENAISSANCE - Stable ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

launceston retail audit

and activity centres strategy:

information booklet

RENAISSANCE

planning

4 - 5 july 2011

understand | envision | plan | sustain

©Copyright, Renaissance Planning Pty Ltd, July 2011

This work is copyright. Apart from any use as permitted

under Copyright Act 1963, no part may be reproduced

without written permission of Renaissance Planning Pty Ltd

Disclaimer: Neither Renaissance Planning Pty Ltd nor any

member of employee of Renaissance Planning Pty Ltd takes

responsibility in any way whatsoever to any person or organisation

(other than that for which this report has been prepared) in

respect of the information set out in this report, including any

errors or omissions herein. Renaissance Planning is not liable

for errors in plans, specifications, documentation or other

advice not prepared or designed by Renaissance Planning.

RENAISSANCE Planning Pty Ltd ABN 91 796 676 210 ACN 094 933 972

Suite 307/91 Murphy Street Richmond Victoria 3121

strategic planners | urban designers | economists | landscape architects

table of contents

1. Purpose of the Presentation 2

2. Background to the Study 2

3. Study Purpose 2

4. Key Outcome Requirements 3

5. Study Process 3

6. Reference Areas 4

Greater Launceston Urban Area 4

North Tasmania Region 4

Launceston Central Area 7

Launceston Central Business District 8

Retail Core District 9

Kmart Plaza Precinct 9

7. Key Findings 9

Launceston: The Regional City 9

Current State of the Retail Commercial System 10

Forecast Population Growth (2011 - 2021 - 2036) 18

Forecast Retail Expenditure Growth in the Greater Urban Area 18

(2011 - 2021 - 2036)

Effects of Online Retailing 18

Forecast Retail Sales in the Greater Urban Area (2011 - 2021 - 2036) 19

Retail Floorspace Requirements for the Greater Urban Area 20

(2011 - 2021 - 2036)

Scale of Potential Developments 20

8. Recommended Strategy 21

Strategic Principles 21

Key Issues in the Review of the Activity Centre Hierarchy 21

Activity Centre Hierarchy and Recommended Policy Framework 22

Introduction of Master Planning Requirements 23

Application of Indicative Floorspace Requirements 23

Recommended Impact Assessment Framework 23

Review of Woolworths Proposal 26

Market Development Initiatives 28

Recommended Principles to Streamline the Launceston Planning Scheme 28

Recommended Process of Monitoring and Review 28

9. Next Steps 29

Launceston Retail Audit & Activity Centres Strategy: 1

Information Booklet

purpose of the presentation

Key objectives for the Presentation:

• briefly outline the background and purpose of the Study;

1

• provide a broad overview of the study process;

• outline the key findings and their significance for the Strategy;

• present the major elements of the Strategy, and in this context;

• explain the review of the Woolworths proposal and the recommendation to Council;

• indicate the next steps in the process.

background to the study

•

•

Contacts by Woolworths Limited (late 2010);

Submission for rezoning at Connector Park for a Marketplace shopping centre;

2

• Council seeking strategic response;

• Requirements for a clear strategic direction that is strongly evidenced based;

• Study commissioned on 1 March 2011.

study purpose

• Comprehensive review of the 2004 Launceston Retail Strategy;

3

• a requirement for a detailed empirically based review of the structure and function of the retail-

commercial system;

• review of online retailing and implications for future activity centre provision;

• an assessment of retail floorspace requirements over the next 20 years and beyond;

• an activity centres strategy to guide Launceston’s retail-commercial system over the next 20 years

and beyond;

• detailed functional assessments of Launceston CBD and key centres for master planning;

• assessment of the proposed Woolworths Marketplace shopping centre development at Connector

Park with clear recommendations for Council.

2

key outcome requirements

In the broadest of terms, Council has sought from the Study, three major outputs:

•

4

guidance for a clear strategic development direction that is consistent with recent visioning for the

City and that is firmly based on a strong empirical foundation;

• a forward looking Strategy that is directed to facilitating new major investment in the City and the

Greater urban area that is seen by the business community as being proactive;

• a Strategy that takes full account of access and sustainability considerations, and particularly of the

significant investment represented in the existing retail commercial hierarchy in Launceston and its

suburbs; and that long-term directions indicated by the Strategy will seek to maximise public benefit

for current and future residents of Launceston and its regional community.

study process

•

•

The study process encompassed the following steps:

ongoing liaison and regular reporting to a Steering Group;

5

• reviews of regional and municipal policies and strategies;

• review of the population forecasts for Launceston and the region;

• commissioning of extensive surveys for the study:

- land use and floorspace;

- In-Centre Surveys;

- In-Home Telephone Surveys.

• analysis of the surveys and supporting research;

• assessment of structural and functional characteristics of the retail-commercial system;

- forecasting of expenditure and the assessment of retail and office floorspace requirements;

• finalisation of the Retail Audit;

• drafting of the Activity Centres Strategy;

• presentations to Council, regional and business stakeholders.

• review by Council of the draft documents;

• revised draft final reports to Council;

• Council formally receives the reports and commences consultation process;

• finalisation of activity centres policy by Council.

Launceston Retail Audit & Activity Centres Strategy: 3

Information Booklet

reference areas

Greater Launceston urban area

6

In this study the principal reference area is the greater Launceston urban area. It is the area used for all

the key demand and supply assessments including:

• an inventory of retail, bulky goods and office floorspace;

• population analysis and forecasting;

• retail expenditure assessments and projections;

• assessments of current and future retail sales;

• analyses of future floorspace requirements.

The area encompasses urban areas of the City of Launceston together with the contiguous suburbs that

extend into parts of West Tamar and Meander Valley municipalities , together with urban localities in

George Town and Northern Midlands municipalities.

The area is defined by the Australian Bureau of Statistics (ABS) as the Launceston statistical sub-division

(SSD), and comprises (refer Figure 1):

• City of Launceston (Inner and Part B),

• George Town (Part A),

• Meander Valley (Part A),

• Northern Midlands (Part A),

• West Tamar (Part A).

At June 2010, the estimated resident population (ERP) of the greater Launceston urban area was ap-

proximately 106,150 persons (refer Table 1).

North Tasmania Region

A supporting reference area was also defined for the study. This is a broader surrounding area encom-

passing the municipalities and districts that together with the Launceston urban area make up the North

Tasmania region. A map of the region and its relationship with the greater Launceston urban area is

shown in Figure 1. The area of the North Tasmania region outside the greater Launceston urban area

comprises the following SLAs:

• City of Launceston (Part C),

• George Town (Part B),

• Meander Valley (Part B),

• Northern Midlands (Part B),

4

• West Tamar (Part B),

• Break O’Day,

• Dorset,

• Flinders.

At June 2010, the ERP of the balance of the North Tasmania region outside the greater Launceston ur-

ban area was approximately 36,160 persons, and the total population of the North Tasmania region was

approximately 142,310 persons.

Figure 1: Greater Launceston Urban Area and North Tasmania Region

George Town GREATER

Part A

LAUNCESTON

URBAN AREA

Flinders

West Tamar

Part A

West Tamar

Part A City of

Launceston

Inner

and

Meander Part B

Valley

Part A Northern

Midlands

Part A

George

Town Dorset

Part B

50 km

West

Tamar Launceston

Part B Part C

(outside

GLUA) Break O’Day

Meander

Valley

Part B

Northern

Midlands

Part B

LEGEND

Greater Launceston

Urban Area

North Tasmanian

Region: Balance

Launceston Retail Audit & Activity Centres Strategy: 5

Information Booklet

Table 1: North Tasmania Region: Historic and Forecast Estimated Resident Population, 2006 – 2021 – 2036

Estimated Resident Population (ERP)

Tasmanian North Region Historic (ABS ERP) Forecast ERP*

2006 2010 2011 2016 2021 2026 2031 2036**

Greater Launceston

City of Launceston (Inner & Part B) 61,670 62,980 63,370 65,220 67,030 68,760 70,480 72,240

George Town (Part A) 5,680 5,830 5,850 5,880 5,870 5,830 5,800 5,770

Meander Valley (Part A) 8,510 8,920 9,050 9,580 10,110 10,610 11,100 11,620

Northern Midlands (Part A) 7,860 8,010 8,080 8,350 8,580 8,750 8,890 9,030

West Tamar (Part A) 19,650 20,410 20,620 21,480 22,280 22,980 23,660 24,360

Total Greater Launceston Urban Area 103,370 106,150 106,970 110,510 113,870 116,930 119,930 123,020

North Region Balance

City of Launceston (Balance) 2,860 2,840 2,840 2,790 2,710 2,610 2,560 2,440

George Town (Balance) 1,050 1,060 1,060 1,060 1,060 1,060 1,070 1,070

Meander Valley (Balance) 10,460 10,770 10,790 10,880 10,890 10,820 10,720 10,620

Northern Midlands (Balance) 4,650 4,650 4,640 4,550 4,420 4,270 4,160 3,960

West Tamar (Balance) 1,960 2,070 2,120 2,330 2,540 2,750 2,890 3,230

Break O'Day 6,250 6,510 6,590 6,880 7,150 7,390 7,550 7,880

Dorset 7,210 7,360 7,350 7,240 7,110 6,930 6,860 6,600

Flinders 890 900 910 920 920 930 930 940

Total North Region Balance 35,330 36,160 36,300 36,650 36,800 36,760 36,740 36,740

Total Tasmanian North Region 138,700 142,310 143,270 147,160 150,670 153,690 156,670 159,760

* Estimates based on Department of Health and Aging and Demographic Change Advisory Council medium projections

** Renaissance Planning estimate based on average annual rate of growth between 2026-2031,'

6

Launceston Central Area (LCA)

The Launceston Central Area (LCA) is a reference area for detailed analysis of retail-commercial floor-

space. The boundaries are consistent with the Launceston Central Activities District as defined in the

Launceston Planning Scheme. It encompasses the Launceston Central Business District (CBD) and ad-

jacent areas and generally extends between 400 – 900 metres from the intersection of Brisbane and St

John Streets (refer Figure 2).

Figure 2: Launceston Central Area Precincts

orth

t-N

r Eas

ute

:O

LCA

ct

cin

Pre

a nk

thb

Sou

sk rth

rt hE No

: No B D:

LCA in gC

ort

pp

Su

t

es

thw Ea

st

or

N D:

D: B

ct CB ingC

cin tin

g ort

Pre or pp

p ort p Su

: Sea Sup

LCA Cornwall Square

Transit Centre

chment

Cat :

ble re

Co st

Centreway Arcade

lka D hea

th

B

C ort

ou

a

Olde Brisbane Mall

W

N -S

m

st

:

Ea

200

re

Co ast

er

:

re

ut

D e

Co st CB outh

O

D we

A:

B

C r th S

LC

No

CB

Su

pp

D

Quadrant Plaza

:

Co

or

re Shopping Centre

Co est

tin

re

:C

g

D w

CB uth

CB

ha

Powells Arcade

So

D:

rle

ent

W

sS

City Plaza/

e:

es

Ludbrooks Arcade

tre

hm

r

t

Co st st

e

D ea ea

tW

CB orth th

atc

Su

ou

es

:S

p

N

t

D

po

CB

C

ing

rti

:

ble

re ort

ng

re

: rth Co ast pp

CB

Su

ka

Co est - No C BD the

D:

t u

al

D w

CB rth es So

W

So

rW

No ute

CB

u

m

th

D

O

we

A:

0

:

Co

re 50

LC uth

st

Co est ct

re

So cin

:C

D

CB uth

w st-

e Pre

ha

So rW ar

e

ute

rle

u

:O Sq

sS

LC

A es

tre

nc

Pri

et

LCA: A:

W

LC

es

Jimmy’s

t

LCA: Coles

Wellington

Street

IGA

Legend

Core CBD

Supporting CBD

Launceston Central Area Balance 300m

0 150

Green Space / Parks

Waterways

Launceston Retail Audit & Activity Centres Strategy: 7

Information Booklet

Launceston Central Business District (CBD)

The Launceston CBD is the principal retail and commercial centre of Launceston and the North Tasma-

nia region. For the purposes of the Strategy, it is defined as the area within approximately 330 – 450 me-

tres of the intersection of Brisbane and St John Streets (refer Figure 2). It is generally bounded as follows:

• to the north by William Street,

• to the east by Tamar Street,

• to the south by York, George and Elizabeth Streets,

• to the west by Wellington Street.

Figure 3: Suburb of Launceston

Ravenswood

nswood

Invermay Ravenswood

Invermay

East

Trevallyn Launceston

East Legend

Launceston

Launceston Central Area

Core CBD

Newstead

Supporting CBD

Launceston Launceston Central Area Balance

Ravenswood

Outside of Launceston Central Area

Launceston (Kmart) Plaza Precinct

West Launceston (suburb) Other

Launceston Newstead

Launceston Waterways

Invermay South Green Space

Cadastre

0 500 1000m Launceston Suburb Boundary

West

Launceston

South

Launceston

8Retail Core District

The Launceston retail core district is the region’s pre-eminent shopping destination. The retail core dis-

trict is defined as the area within approximately 200 metres of the intersection of Brisbane and St John

Streets. It is comprised of five city blocks and parts of the sixth city block west of Charles Street (refer

Figure 2).

Kmart Plaza Precinct

The Kmart Plaza precinct comprises the shopping centre at Racecourse Road together with adjacent

bulky goods activities centred on Boland Street (refer Figure 3).

key findings

launceston: the regional city

7

Launceston is an important regional services city. It has a modern airport and the city is part of the main

air route network that links that nation’s eastern seaboard cities. It is a major gateway for tourism to

Tasmania.

In common with other regional cities Launceston serves an extensive area beyond the municipality and

urban district. The city’s economy and future prosperity is in large part underpinned by its regional ser-

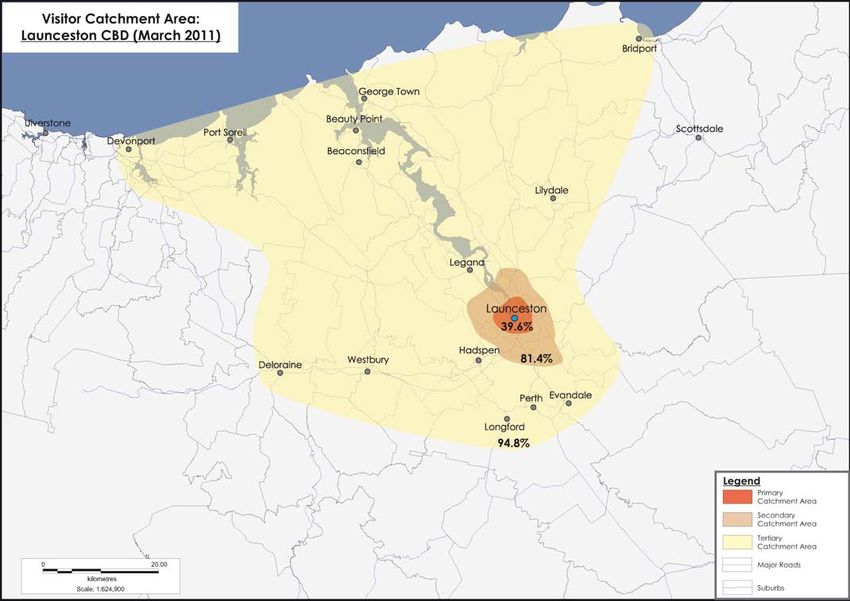

vices role. Its regional catchment area (RCA) identified in the In-Centre Surveys (refer Figure 4) defines

a broad area of influence that applies to a wide range of services that encompasses:

• retailing (including bulky goods and automotive retailing);

• commercial services;

• professional services;

• government and administration;

• legal services and justice;

• health and community services;

• entertainment and the arts;

• higher education;

• regional sporting facilities;

• hospitality and tourism;

• transport and distribution.

Launceston Retail Audit & Activity Centres Strategy: 9

Information Bookletcurrent state of the retail-commercial system

Overall provision of retail-commercial floorspace

• occupied retail goods and services floorspace (non bulky goods): approximately 1.97 square me-

tres Gross Leasable Area (GLA) per capita (average for regional cities approximately 1.83 square

metres per capita),

• occupied bulky goods floorspace: approximately 0.61 square metres GLA per capita (average for

regional cities approximately 0.63 square metres per capita),

• total occupied retail floorspace: approximately 2.58 square metres GLA per capita (average for

regional cities approximately 2.46 square metres per capita),

• occupied office floorspace: approximately 1.7 square metres GLA per capita (average for regional

cities approximately 1.12 square metres per capita),

• overall level of provision for retail and bulky goods floorspace is similar to that of other regional cities,

• level of occupied office floorspace provision is relatively high but this is a positive finding. It reflects

the wider and more comprehensive commercial services role played by Launceston than is the

case in other regional cities of the same size in eastern Australia (e.g. Ballarat and Bendigo). Com-

mercial services in regional cities in Victoria and New South Wales are overshadowed by the service

roles played by Melbourne and Sydney and by the relative ease of access to regional cities from

the metropolitan areas.)

Importance of the LCA

• significant concentration of retail-commercial floorspace in central Launceston,

• approximately 45 per cent of occupied retail goods and services floorspace in the greater urban

area is concentrated in the LCA,

• some 40 per cent of occupied bulky goods floorspace is in the LCA,

• approximately 67 per cent of occupied office floorspace is located in the LCA,

• the prime retail focus is the retail core precinct:

- the premier shopping destination in North Tasmania,

- unique concentration of department and discount department stores, national chain fashion stores

and a number of Launceston and Tasmanian stores that have developed as major attractors in

the region,

- network of pedestrian spaces and places,

- iconic heart of the city: significant heritage streetscapes,

- extensive street based and arcaded shopfront environment,

- highest concentrations of pedestrian activity in the region,

- public transport focus for the city and region,

- regional catchment area that extends well beyond the greater urban area (refer Figure 4).

10• Supporting CBD precincts: The retail core precinct is encompassed by several CBD precincts that

extend up to 500 metres from the intersection of Brisbane and St John Streets:

- major concentrations of government and commercial offices, retailing and bulky goods stores,

tourism and accommodation facilities, retail services, cafes and restaurants,

- the diversity and concentration of activities in the supporting CBD is a great strength of central

Launceston. Most significant concentrations of commercial activities in the region (refer Figures 5

and 6).

- the proximity and interaction between the retail core and supporting CBD precincts is a powerful

support for the retail core. The wider CBD underpins the prosperity of significant services industries

which reinforce the regional attraction of central Launceston.

Figure 4: Launceston CBD Regional Catchment Area

Launceston Retail Audit & Activity Centres Strategy: 11

Information BookletFigure 5: Launceston Retail, Bulky Goods and Office and Floorspace Distribution by Centre Type 2011

250,000

200,000

Vacant Shop / Office

Floorspace (sq. metres GLA)

Other Services

150,000 Professional and Medical Services

Bulky Goods

Retail Services

Specialty Non-Food Stores

100,000

Department and General Stores

Other Food Stores / Cafes

Supermarkets

50 000

50,000

0

Figure 6: Launceston Retail, Bulky Goods and Office Tenancies Distribution by Centre Type 2011

700

600

500 Vacant Shop / Office

Other Services

Number of Tenancies

Professional and Medical Services

400

Bulky Goods

Retail Services

300 Specialty Non-Food Stores

Department and General Stores

Other Food Stores / Cafes

200

Supermarkets

100

0

12LCA Precincts beyond the CBD

• Significance of education activities, cafes, restaurants, hospitality, recreation, and entertainment ac-

tivities,

• Important bulky goods precincts in the south of the LCA.

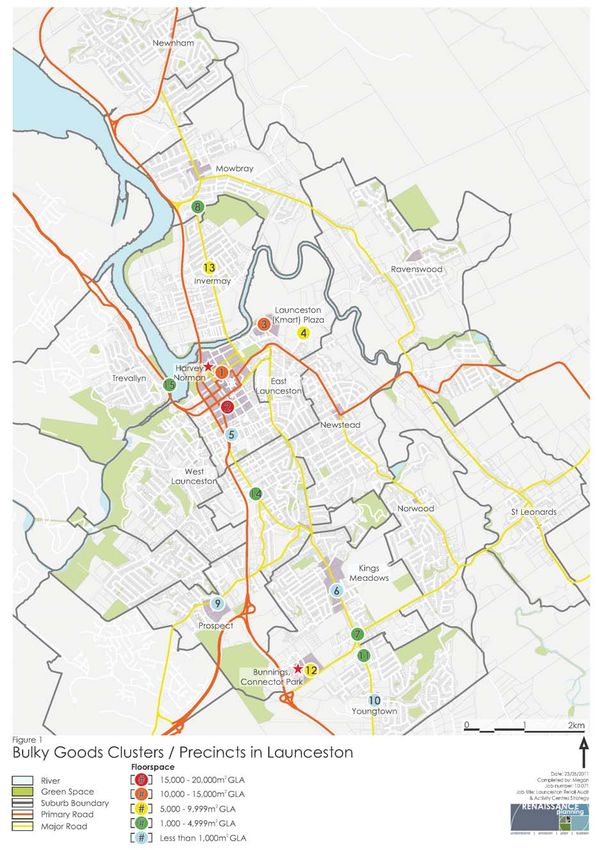

Bulky Goods Floorspace

The spatial distribution of bulky goods floorspace in Launceston reflects the strong influence of the central

city and highway routes as key determinants in the locational pattern of development. Approximately 75

per cent of occupied bulky goods floorspace in the greater urban area is concentrated in several clusters

and precincts (refer Figure 7). These comprise:

• two extensive clusters of bulky goods activities in the LCA form the largest concentrations of this activity

in the greater urban area:

- a northern CBD cluster that includes Harvey Norman and Spotlight (refer Figure 7, area 1),

- a southern area which includes a cluster in the CBD (Kingsway area) and an area of development

extending to the southern area of the LCA (area 2, Figure 7),

• an area of bulky goods development in the Kmart Plaza precinct (area 3, Figure 7),

• an important bulky goods and mixed use precinct located at Invermay (area 13, Figure 7),

• the Bunnings development at Connector Park (area 12, Figure 7).

The District Centres

• strategically located activity centres north and south of the Launceston CBD (refer Figure 8),

• recognition in the Launceston Planning Scheme of the higher order activity role for the District Centres

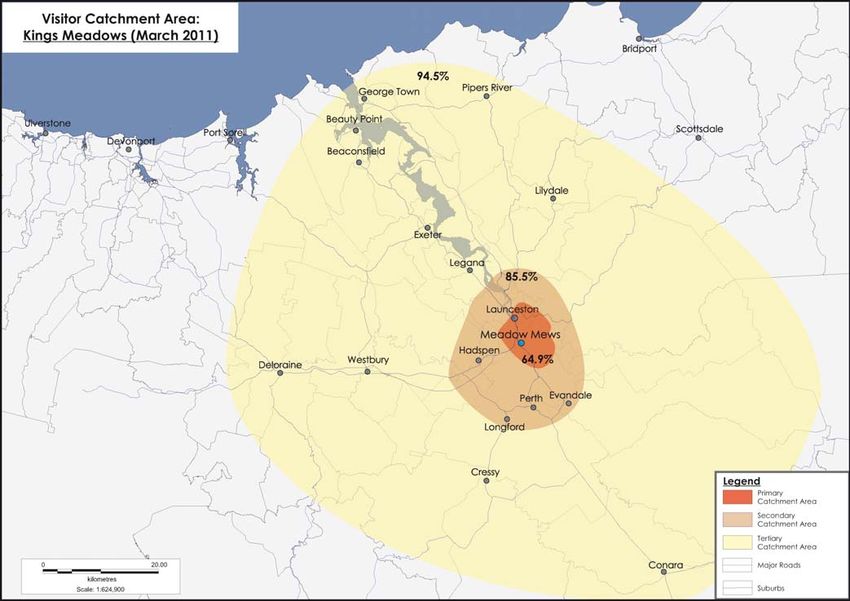

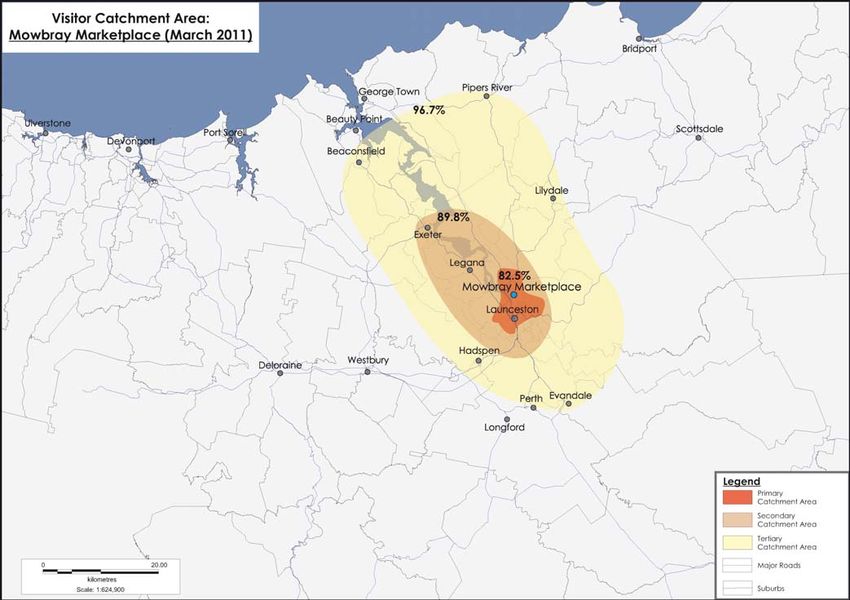

of Kings Meadows and Mowbray,

• the District Centres have approximately 15 per cent of retail goods and services floorspace in the

greater urban area and very minor proportions of offices and bulky goods floorspace (approximately 3

per cent and 1 per cent respectively);

• both centres have street based retail services and commercial activities together with internal shop-

ping malls,

• the only supermarkets in excess of 3,000 square metres GLA in the City of Launceston are located in the

District Centres and a fourth is being completed, to be opened in Mowbray,

• catchment analysis indicates extensive district and regional catchments extending over the Launces-

ton suburban area and the surrounding localities (refer Figures 9 and 10),

• the two District Centres have significant potential to provide a wider range of discretionary retail goods

together with retail and commercial services that extends far beyond the provision of food and gro-

cery shopping. This direction is recommended by the Strategy.

Kmart Plaza Precinct

• sub regional shopping centre located at Racecourse Road, approximately 1.2 kilometres east of the

Launceston CBD,

• has approximately 5 per cent of the occupied retail goods and services floorspace in the greater ur-

ban area,

• significant clustering of bulky goods floorspace in the precinct (some 14 per cent of the bulky goods

floorspace in the greater urban area);

• opportunities for amenity improvements.

Launceston Retail Audit & Activity Centres Strategy: 13

Information BookletFigure 7: Bulky Goods Clusters and Precincts in Launceston 14

Figure 8: Existing Launceston Activity Centre Hierarchy

g ( )

Newnham

To

Le

ga

na

Mowbray

North

Riverside

Riverside

Ravenswood

Invermay

Launceston

(Kmart) Plaza

Launceston CBD

Harvey

Trevallyn Norman

East

Launceston

Newstead

Wellington

Street Coles

West

Launceston

Norwood

Five Ways

St Leonards

Kings

Meadows

Prospect

p Vale

Prospect

Prospect

Marketplace Bunnings,

Connector Park

Youngtown

0 1 2km

Launceston CBD Neighbourhood Stores / Clusters Primary Road

Major Road

Commercial / Bulky Goods Precincts

District Centres Residential

Date: 23/05/2011

River Reserved Residential Completed by: Megan

Launceston (Kmart) Plaza Precinct Job number: 10-071

Green Space Future Urban Job title: Launceston Retail Audit

& Activity Centres Strategy

Business

Neighbourhood Centres

Commercial/Industrial

Launceston Retail Audit & Activity Centres Strategy: 15

Information BookletFigure 9: Kings Meadows Regional Catchment Area Figure 10: Mowbray Marketplace Regional Catchment Area 16

Neighbourhood Centres and Clusters in the City of Launceston

• locally based activity centres anchored by a supermarket function,

• provide approximately 7 per cent of the greater urban area’s stock of retail goods and services

floorspace;

• provide for the comprehensive daily needs and a range of weekly requirements of local residents,

• Launceston’s retail pattern is characterised by small neighbourhood centres and clusters in the City

of Launceston and the development of larger neighbourhood activity centres in the suburbs and

localities outside the City within the greater urban area,

• neighbourhood activity centres in the City of Launceston which provide both a supermarket and a

range of supporting retail stores and services comprise:

- Prospect,

- Newstead,

- Ravenswood,

- Trevallyn,

- Lilydale.

• a characteristic of the City of Launceston’s retail pattern is the development of a number of neigh-

bourhood clusters. These are individual free standing supermarkets or supermarkets with limited or

no supporting retail stores and services and comprise the following:

- Charles Street (Jimmy’s Coles) in the LCA,

- Wellington Street IGA in the LCA,

- Wellington Street Coles,

- Newnham,

- Norwood,

- West Launceston,

- Youngtown.

• In the suburbs and localities outside the City of Launceston, there are a number of neighbourhood

centres collectively these make up about 16 per cent of retail goods and services floorspace in the

greater urban area and about 5 per cent of the region’s bulky goods floorspace and some 4 per

cent of office floorspace. The neighbourhood centres include:

- George Town,

- Beaconsfield,

- Legana Shopping Centre,

- Prospect Vale Marketplace,

- Longford,

- Riverside,

- Exeter.

• Legana and Prospect Vale are mall type shopping centres anchored by full line supermarkets in

excess of 3,000 square metres GLA,

• Riverside is an older mall based shopping centre anchored by a 2,700 square metre GLA supermar-

ket,

• George Town and Longford are historic town centres serving extensive rural catchments.

Launceston Retail Audit & Activity Centres Strategy: 17

Information Bookletforecast population growth (2011 - 2021 - 2036)

Greater Urban Area (refer Table 1)

• projected ERP at 2011: 106,970 persons,

• forecast average growth rate: 2011 – 2021 (medium series): 0.63 per cent per annum,

• forecast population at 2021: 113,870 persons,

• forecast average growth rate: 2021 – 2036 (medium series): 0.52 per cent per annum,

• forecast population at 2036: 123,020 persons.

North Tasmania Region Balance (refer Table 1)

• projected ERP at 2011: 36,300 persons,

• negligible overall growth or decline over the forecast periods 2011 – 2021 and 2021 – 2036, (me-

dium series),

• forecast population at 2021: 36,800 persons,

• forecast population at 2036: 36,740 persons.

North Tasmania Region

• projected ERP at 2011: 143,270 persons,

• forecast population at 2021: 150,670 persons,

• forecast population at 2036: 159,760 persons.

forecast retail expenditure growth in the greater urban area

(2011 - 2021 - 2036)

• forecasts prepared for the major retail expenditure categories,

• forecasts take account of underlying long term trends in real expenditure growth in Tasmania and

current cyclical patterns,

• for food, groceries and liquor and food catering: average real growth per capita for 2011 – 2021

in the range 0.7 – 0.9 per cent per annum; long term estimates for 2021 – 2036 in the range 0.8 – 1.2

per cent per annum,

• for non food retail goods: average real growth per capita for 2011 – 2021 in the range approxi-

mately 0.9 per cent per annum; long term estimates for 2021 -2036 in the range 1.0 – 1.5 per cent

per annum.

effects of online retailing

• Information from In-Home Telephone Surveys in the Launceston region (March 2011) indicates that

online currently constitute 4 – 10 per cent for particular categories of household goods and 2 – 7 per

cent for specific categories of bulky goods,

18• conservative approach taken for online expenditures,

• for the purposes of forecasts for the Strategy it was assumed that all online expenditures would be

“out-of-region”; that is, no component would be attributable to retail stores in the greater Launces-

ton urban area;

• further assumed that significant differential real growth rates would be maintained for online retail-

ing for the foreseeable future at a rate of 4.0:1.0 for the entire period 2011 – 2021 and at a rate of

3.5:1.0 for the entire period 2021 – 2036,

• the assumptions taken together are likely to overstate the net regional outflows of resident retail

expenditures attributable to online retailing,

• cumulative effects of online estimates: reductions in potential retail sales in the greater urban area

over the forecast period:

9 – 12 per cent for household goods (online and other escape expenditures),

8 – 12 per cent for bulky goods (online and other escape expenditures).

forecast retail sales in the greater urban area (2011 - 2021 - 2036)

• for year ended 30 June 2011, currently estimated at approximately $1.4 billion at 2010/11 constant

prices (refer Table 2),

• 2021 forecast sales approximately $1.61 billion at 2010/11 constant prices,

• 2036 forecast sales approximately $2.0 billion at 2010/11 constant prices

Table 2: Greater Launceston Urban Area: Estimated Current and Forecast Retail Sales

(2011 - 2021 - 2036)*

Current and Forecast Annual Retail Sales at 2010/11

constant prices

Commodity Group

2011 2021 2036

($ million)

Food, groceries & liquor 555.9 636.7 769.0

Food catering (cafes and restaurants) 200.0 233.3 300.0

Household goods 369.7 426.3 545.2

Bulky goods 218.8 252.9 328.7

Selected services 48.5 56.5 71.2

Total 1,392.9 1,605.7 2,014.0

* Excludes online sales for household goods and bulky goods

Launceston Retail Audit & Activity Centres Strategy: 19

Information Bookletretail floorspace requirements for the greater urban area

(2011 - 2021 - 2036)

• on the basis of the forecast sales and assessments of current and future levels of retail turnover per

square metre, forecasts were prepared of retail floorspace requirements for the greater urban area

by major time period;

• for the period 2011 – 2021, forecast net additional retail floorspace requirements for the greater ur-

ban area are approximately 40,000 square metres GLA (refer Table 3);

• for the period 2021 – 2036, forecast net additional retail floorspace requirements for the greater ur-

ban area are approximately 63,000 square metres GLA.

Table 3: Greater Launceston Urban Area: Forecast Net Additional Retail Floorspace Requirements

(2011 - 2021 - 2036)

Forecast Net Additional Retail Floorspace Requirements by

Major Commodity Group / Service Group Time Period (m² GLA)

2011 - 2021 2021 - 2036 2011 - 2036

Food, groceries & liquor 8,120 10,670 18,790

Food catering (cafes and restaurants) 3,720 5,710 9,430

Household goods 11,100 17,600 28,700

Bulky goods 9,740 18,410 28,150

Retail services (all) 4,960 6,760 11,720

Total Occupied Shopfront Floorspace 37,640 59,150 96,790

Vacant Retail Floorspace Allowance 2,410 3,770 6,180

Total Retail Floorspace 40,050 62,920 102,970

scale of potential developments

• research undertaken for the Strategy indicates that there are a number of proposals that have ei-

ther been received or are likely to be made for retail and bulky goods developments in the greater

urban area,

• for retail goods and services developments (excluding bulky goods) the scale of potential proposals

exceed 50,000 square metres GLA including:

- proposals totaling approximately 37,000 square metres GLA in the City of Launceston,

- proposals totaling approximately 14,000 square metres GLA in the municipalities of West Tamar and

Meander Valley.

• potential bulky goods developments proposals are likely to exceed 20,000 square metres GLA (all in

the City of Launceston),

• it will be noted that the cumulative scale of all of the potential proposals exceeds the total retail

floorspace requirements of the greater urban area well beyond 2021.

20recommended strategy

strategic principles

8

The recommended policy framework comprises a set of principles that set out the underlying rationale

and directions for the Strategy. These principles encompass the following:

• Principle 1: Maximise Launceston’s regional service role;

• Principle 2: Maintain and consolidate a network of sustainable centres and precincts;

• Principle 3: Support and facilitate place making, activity diversity and design amenity;

• Principle 4: Support integrated planning to accommodate future investment, growth and change;

• Principle 5: Recognise that the activity centre system and a broad range of other activities have

evolved and will continue to develop in a market based system;

• Principle 6: Optimise sustainable access to the existing and future network of activity centres;

• Principle 7: Ensure that the planning and development of activity centres maximises net community

benefit to current and future communities of Launceston and its regional catchment area

key issues in the review of the activity centre hierarchy

Spatial Patterns of Urban Growth: Implications for New Activity Centres

• fractionated growth in the greater urban area;

• no single development front;

• no new major centres justified on the basis of new significant population areas;

• identified growth patterns will support small neighbourhood centres/neighbourhood clusters at (sub-

ject to master planning):

- Waverley;

- Hadspen;

- Prospect Vale/Blackstone Heights (vicinity Casino Rise/Country Club Avenue);

• potentials to consolidate existing neighbourhood activity centres/clusters at (subject to master plan-

ning):

- Newnham;

- Prospect Vale Marketplace;

- Legana;

Overall spatial structure of the existing activity centre network;

• strategic relationship of the LCA and the District Centres of Kings Meadows and Mowbray as the

Launceston Retail Audit & Activity Centres Strategy: 21

Information Bookletsupporting higher order centres provides a linear network system. Well suited to meet prospective

needs for the foreseeable future (subject to master planning):

• the CBD and LCA have excellent potentials for further retail consolidation particularly in relation to

bulky goods;

• critical high quality improvement opportunities need to be identified for the retail core and adja-

cent precincts in the CBD;

• both Kings Meadows and Mowbray have significant opportunities for higher order expansion and

consolidation;

• the overall higher order network delivers a linear system that is highly accessible to the wider urban

area. Well suited to improved public transport access and residential development consolidation,

improvements to pedestrian access etc;

• bulky goods developments in Launceston are uniquely centrally concentrated and there is mar-

ket support to further consolidate this pattern. A great opportunity that needs to be supported by

policy. Further reinforcement of a linear activity centre system;

• broader based consolidation of the LCA. The LCA is a very extensive area. There are significant op-

portunities to identify and facilitate new medium density residential and mixed use precincts within

this area. This will powerfully reinforce the core precinct and adjacent CBD precincts;

• broader based consolidation of the District Centres. Need to identify potentials and facilitate medi-

um density residential and mixed use development opportunities as part of the future development

and consolidation of the District Centres.

activity centre hierarchy and recommended policy framework

The recommended activity centre hierarchy and accompanying policy framework comprise a central

element of the Strategy. This is set out in Section 5.3 of the Summary Report. The Strategy recommends:

• a revised hierarchy structure comprised of six complementary tiers to ensure the ongoing sustain-

able provision and the dynamic development of retail stores and services as part of a broader di-

versity of activities to address the current and future needs of residents and visitors;

• the Strategy defines key roles for each centre/precinct type. These provide for:

- the central place and primacy role of the Launceston CBD;

- consolidated higher order role for the District Centres of Kings Meadows and Mowbray;

- affirmation of the regional role of bulky goods precincts;

- recognition of the existing district and regional role of Kmart Plaza precinct;

- the important neighbourhood and local service roles of neighbourhood centres;

- the supporting local service role of neighbourhood stores and clusters.

• a set of recommended policies have been provided for the activity centre hierarchy. These provide

guidance in relation to:

- recommended role for each centre type;

22- public transport and pedestrian access;

- retail stores and services;

- place making and heritage;

- activity centre environment and amenity;

- activity diversity;

- community focus and access;

- recommended priority initiatives for each activity centre type.

introduction of master planning requirements

• the Strategy recommends the need for coordinated physical master planning in the LCA, District

Centres and in precincts and activity centres where significant development is to be undertaken;

• the Strategy sets out planning and design requirements and guidelines for master planning;

application of indicative floorspace requirements

• the Strategy recommends that the identified floorspace requirements be considered as indicative

and advisory;

• it is not intended that the identified floorspace requirements should form the basis of any formal al-

location system;

• the purpose of the identified floorspace requirements is to indicate the likely order of floorspace

and land that the activity centre network may need to accommodate over the next 20 years and

beyond and to ensure that master planning takes full account of likely future demands and require-

ments.

recommended impact assessment framework

The Strategy recommends the adoption of an impact assessment framework for the evaluation of retail

development proposals that may require rezoning of land or where development is of a scale likely to

have significant effects on existing activity centres.

The impact assessment framework is placed within the overall consideration of net community benefit

and takes account of a number of criteria encompassing:

• Strategic location and context of the proposed development. Extent to which the proposal:

- is consistent with existing policy and the zoned and planned use of the land as envisaged in the

Launceston Planning Scheme;

- contributes to the consolidation of the activity centre network consistent with Council policy and

the recommendations of the Strategy;

Launceston Retail Audit & Activity Centres Strategy: 23

Information Booklet- impacts on the strategic basis for which major infrastructure has been planned and provided.

• Sustainable access. Extent to which the proposal:

- contributes to improved pedestrian and cycle access;

- contributes to improved access, amenity or safety for travel to the development by public trans-

port;

- can be accommodated to ensure safe and effective access utilising the existing main road net-

work.

• Opportunity for choice. Extent to which the proposal:

- broadens retail and commercial choices for residents;

- contributes to a wider diversity of activities in the existing and designated activities centres net-

work;

- minimises the need for a multiplicity of trips;

- contributes to community, health and professional services activities.

• Places for people. Extent to which the proposal:

- improves the attraction, spaces, amenity and environment for people of all ages at the subject

development and/or of any centre in the existing and designated activities centres network;

- contributes to street-based or externally focused pedestrian environments;

- contributes to the development of gathering spaces and places;

- contributes to the improved urban design, landscape and architecture of the subject development

and/or of any centre in the existing and designated activities centres network;

- contributes to improved safety and amenity at the subject location and/or at any centre in the

existing and designated activities centres network.

• Economic viability. Extent to which the proposal:

- contributes to the generation of a diversity of employment opportunities during the construction

and operational phases of the development;

- impacts on the trade, employment and viability of activity centres in the existing and designated

activity centres network;

- contributes to the long term viability of the existing and designated network of activity centres,

consistent with Council policy and the recommendations of the Strategy;

- could cause planning blight or loss of amenity through vacancies and disinvestment at any centre

in the existing and designated network of activity centres;

- may cause significant losses and services in relevant impact centres;

- may contribute to a loss of investment, capitalised value and future development opportunities in

relevant impact centres;

- may contribute to a loss of confidence for investment in existing activity centre network and in the

24certainty that the Planning Scheme can ensure a coherent and secure pattern of investment in the

future;

- may contribute to externality costs in public infrastructure and/or services that would be generated

as a direct consequence of its development and operation.

• Environmental sustainability. Extent to which the proposal:

- contributes to the use of renewable energy sources and minimises its carbon footprint through de

sign, layout and construction;

- utilises solar design and orientation to contribute an energy efficient development that minimises

energy requirements;

- applies water sensitive urban design (WSUD) practices in the design, layout and construction of the

development;

- contributes to environmental sustainability through maximising opportunities for public transport and

walk trips and maximising opportunities for multi purpose trips.

• Amenity and safety. Extent to which the proposal:

- ensures safety for visitors and workers through its design and layout and the treatment of the public

realm, pedestrian spaces and access routes;

- demonstrably minimises negative impact effects on the subject site and the general surrounds.

Launceston Retail Audit & Activity Centres Strategy: 25

Information Bookletreview of woolworths proposal

In December 2010 Council received a request to rezone land located at Connector Park to facilitate

the development of a marketplace shopping centre. The proposed development would be a free-

standing regional shopping centre. The proposed development would comprise:

• a Big W discount department store of approximately 8,310 square metres GLA;

• a Woolworths full line supermarket of approximately 3,800 square metres GLA;

• mini majors: 1,000 square metres GLA;

• other specialty stores and services: 2,500 square metres GLA.

The total proposal at full development is approximately 15,610 square metres GLA.

The Strategy was required to undertake a strategic and economic impact assessment of the proposal,

and to provide a considered response and advice to Council on the outcomes of the assessment.

There were several important considerations in developing a response to the proposal. These encom-

passed:

• detailed consideration of existing Council policy;

• evidenced based comprehensive analysis of the structure and function of the existing retail-com-

mercial system;

• modifications to existing policy recommended by the Strategy;

• application of a recommended impact assessment framework;

• provision of a strategic view of the proposal and implications for the activity centres system, in terms

of the intent of Council policy and the recommendations of the Strategy.

Background to the Evaluation: Key Initiatives Undertaken at the Kings Meadows District Centre

• under existing Council policy the proposed development could only locate in the Launceston CBD;

• under the recommendations of the Strategy the scope of potential locations has been broadened

to encompass the District Centres of Kings Meadows and Mowbray;

• as part of the Strategy process an initial retail master planning assessment was undertaken for the

Kings Meadows District Centre. The objective of this work was to assess:

- whether a modern marketplace development could be located in the Kings Meadows District

Centre;

- whether this type of development could be effectively integrated within the centre and to provide

realistic opportunities for significant further investment and improvements to the amenity and

environment of the centre;

• the outcomes of the assessment indicate that a modern marketplace development of the scale

envisaged at Connector Park is a realistic potential outcome at Kings Meadows and would make a

26material contribution to the long-term improvement of the shopping environment and public realm

of the activity centre;

• the retail master planning process has involved a number of stakeholders including senior represen-

tation from Council and Woolworths Limited;

• at the present time (4-5 July 2011) this is an ongoing process.

The Evaluation: Key Points

• the subject land for the proposal is not supported by structure or strategic planning, nor by the

Launceston Planning Scheme or by Council’s existing activity centre policies or by the recommen-

dations and intent of the Strategy;

• the isolated location of the subject site will likely result in a range of negative effects generated

by a freestanding regional shopping centre, with no relationship to the existing network of activity

centres;

• the retail master planning work undertaken at Kings Meadows indicates that a modern market-

place development could be realistically accommodated at the District Centre;

• the proposed development will have significant economic trade effects on several activity centres

but significant trade effects would also be likely if a similar development to that proposed was to be

located at the Kings Meadows District Centre;

• the key difference is the medium and long-term outcome of a marketplace development at Con-

nector Park compared to a similar type of development at Kings Meadows. In the latter situation,

the role of the District Centre will be significantly upgraded. This would in turn be likely to attract

other investment to the District Centre and provide a sustainable basis for significant design and

safety improvements at the centre. Other benefits would arise from better utilisation of the existing

public transport network, other commercial and recreational activities at the centre etc.

• in the event that the Connector Park development was to proceed, there would likely be long-term

disinvestment effects at Kings Meadows. A key element in existing Council policy would be under-

mined. It would also likely reduce confidence in the capacity of the Planning Scheme to provide a

reasonable degree of assurance for long-term decision making and investment.

Conclusions and Recommendations

• on the basis of the above assessments and considerations, the Strategy does not support the pro-

posed development at Connector Park.

• it is recommended that Council not proceed with progressing the Connector Park proposal given

that it cannot meet fundamental policy requirements, either of Council’s activity centres policy, or

of the requirements of the Launceston Planning Scheme, or of the recommendations and intent of

the Strategy.

• it is recommended that Council support a marketplace development at the Kings Meadows District

Centre and work to achieve this outcome.

Launceston Retail Audit & Activity Centres Strategy: 27

Information Bookletmarket development initiatives

The Strategy recommends Council coordinate the development of a set of market support and market

development initiatives in cooperation with the Tasmanian government and business and community

stakeholders. Key initiatives encompass:

• A new online initiative for Launceston: recommended establishment of a joint website with the busi-

ness community to market the city and key events and to provide a shared high profile address for

businesses to market products and services;

• proactive tenancy liaison and recruitment;

• city events program;

• cooperative support for business training and development;

• joint hosting of a regional business and investment forum.

recommended principles to streamline the launceston planning

scheme

Research undertaken for the Strategy included a review of statutory provisions of the Launceston Plan-

ning Scheme in relation to retail developments. The Strategy provides principles to facilitate the stream-

lining of the Launceston Planning Scheme. It recommends that the Planning Scheme specify a dual

requirement for future development approvals for use and development:

• the use requirements would focus only on the strategic and policy requirements of the zone;

• the development requirements would focus on the specific design and development objectives of

the zone consistent with the directions of the Strategy.

recommended process of monitoring and review

It is recommended that Council adopt a monitoring program to assess progress in implementing the

Strategy or to identify areas where modifications to the Strategy may be required.

It is recommended that Council undertake cyclical reviews to update the information base and de-

mand forecasts. It is recommended that these be undertaken on a five year basis, following each

Census. The first review should be undertaken in 2018 following the 2016 Census and public release of

the outcomes of the Census.

289 next steps • review by Council of the draft documents, • revised draft final reports to Council, • formal receipt of reports and commencement of consultation process by Council, • finalisation of activity centres policy by Council. Launceston Retail Audit & Activity Centres Strategy: 29 Information Booklet

Launceston Retail Audit & Activity Centres Strategy

Prepared by

RENAISSANCE

planning

understand | envision | plan | sustain

forYou can also read