Is Australia headed for an economic boom? Or economic nirvana? - CommSec

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economics | May 10, 2021

Is Australia headed for an economic boom?

Or economic nirvana?

Economic Issues

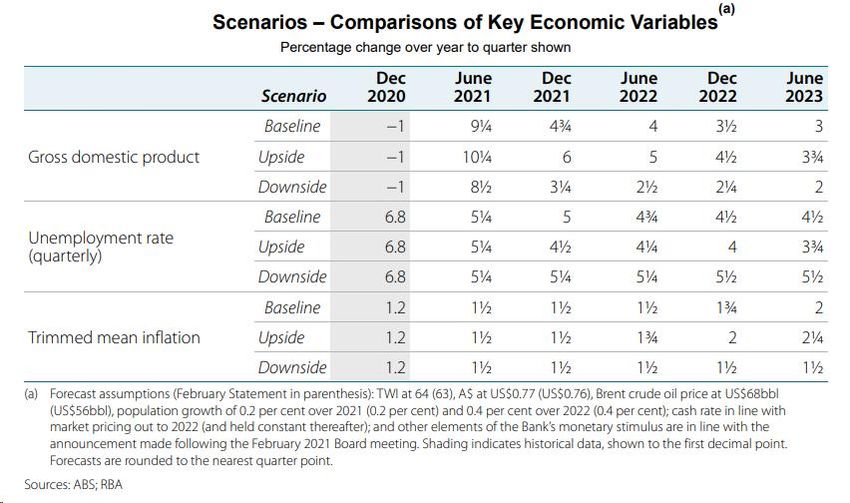

Economic forecast: The Reserve Bank has lifted its 2021 calendar year economic growth forecast from

4.00 per cent to 5.25 per cent. If realised, economic growth would be the strongest for over 30 years. But

notably the 2.5 per cent contraction in 2020 was the biggest in quarterly records going back to 1959.

Implications: Strong economic growth, lower unemployment, benign inflation and record low interest rates

is a powerful combination. Investors must be alert to the risks of boom-like conditions. But investors must

always be alert to the opportunities for investments in consumer discretionary, construction, construction

materials and information technology.

The economic environment is fundamentally important for investors – especially the sectoral winners and losers

What does it all mean?

The word ‘boom’ is used cautiously, principally because booms never end quietly. In other words, booms tend to

be followed by busts. The case in point was the boom of the late 1980s that preceded the recession of 1991.

On Friday the Reserve Bank lifted its economic growth forecasts. The Reserve Bank now expects growth of 5.25

per cent on average over the 2021 calendar year. The growth forecast for the 2021/22 year is now 5.00 per cent,

up from the 3.75 per cent forecast made in February. And growth in calendar 2022 is now tipped at 4.00 per cent,

up from 3.25 per cent.

The jobless rate is now seen at 5 per cent at the end of 2021 before hitting the “full employment” level of 4.5 per

Craig James, Chief Economist

Twitter: @CommSec

IMPORTANT INFORMATION AND DISCLAIMER FOR RETAIL CLIENTS

The Economic Insights Series provides general market-related commentary on Australian macroeconomic themes that have been selected for coverage by the Commonwealth Securities Limited (CommSec) Chief

Economist. Economic Insights are not intended to be investment research reports.

This report has been prepared without taking into account your objectives, financial situation or needs. It is not to be construed as a solicitation or an offer to buy or sell any securities or financial instruments, or as a

recommendation and/or investment advice. Before acting on the information in this report, you should consider the appropriateness and suitability of the information, having regard to your own objectives, financial

situation and needs and, if necessary, seek appropriate professional of financial advice.

CommSec believes that the information in this report is correct and any opinions, conclusions or recommendations are reasonably held or made based on information available at the time of its compilation, but no

representation or warranty is made as to the accuracy, reliability or completeness of any statements made in this report. Any opinions, conclusions or recommendations set forth in this report are subject to change

without notice and may differ or be contrary to the opinions, conclusions or recommendations expressed by any other member of the Commonwealth Bank of Australia group of companies.

CommSec is under no obligation to, and does not, update or keep current the information contained in this report. Neither Commonwealth Bank of Australia nor any of its affiliates or subsidiaries accepts liability for

loss or damage arising out of the use of all or any part of this report. All material presented in this report, unless specifically indicated otherwise, is under copyright of CommSec.

This report is approved and distributed in Australia by Commonwealth Securities Limited ABN 60 067 254 399, a wholly owned but not guaranteed subsidiary of Commonwealth Bank of Australia ABN 48 123 123 124.

This report is not directed to, nor intended for distribution to or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution,

publication, availability or use would be contrary to law or regulation or that would subject any entity within the Commonwealth Bank group of companies to any registration or licensing requirement within such

jurisdiction.

Economic Insights: Is Australia headed for an economic boom?

cent at the end of 2022.

But over the next 18 months, underlying inflation is

not expected to hit 2 per cent (1.75 per cent in late

2022).

Economic nirvana? Perhaps. But it is also important

to remember that growth and unemployment have

bettered even the most optimistic Reserve Bank

forecasts over the past year.

So it’s worth considering the latest ‘upside’ targets

from the Reserve Bank. On the Reserve Bank’s most

optimistic assumptions, annual economic growth

would hit 10.25 per cent in June and 6 per cent in

December (admittedly from a low base). The jobless

rate would hit the “full employment” threshold late this

year but inflation still wouldn’t exceed 1.5 per cent.

The Reserve Bank won’t consider lifting rates until

inflation is sustainably within the 2-3 per cent target

band. So conceivably unemployment could hit 4.5 per

cent by end year with the cash rate still locked at a

record low of 10 basis points.

Too good to be true?

It’s important to remember that these forecasts are

from the Reserve Bank, one of the most cautious and

conservative central banks.

But there appears a growing appreciation for the fact

that inflation – not just here but across the globe –

has been low for a number of years. And a key

reason for that is technology – consumers can buy

goods whenever they want from wherever they want.

Also, organisations like Airtasker, Uber and Menulog

have boosted completion and kept downward

pressure on prices. In addition, businesses in white

collar industries can also get work done offshore – and this is largely unaffected by Covid-19. While wage growth

– a key component of inflation – hit record low levels in Australia at the end of 2020 – with the pace of pay rises

easing since the height of the mining construction boom.

But what happened in 1988?

Cash rates had been falling ahead of the October 1987 sharemarket crash. The cash rate was around 18.8 per

cent in August 1986 and had fallen to 11.3 per cent in October 1987. Rates hit lows of 10.65 per cent in February

1988.

But after the sharemarket crash, the feared economic downturn didn’t arrive. Investors instead switched affections

May 10, 2021 2

Economic Insights: Is Australia headed for an economic boom?

from shares to property, underpinned by lower interest rates. According to CoreLogic, home prices rose by 2.8

per cent in October 1987, lifting the annual rate from 5 per cent to 9 per cent. By late 1988, home prices were

running at a 30-32 per cent annual rate – far higher than we are witnessing today.

To quell the ‘irrational exuberance’ in housing and general ‘conspicuous consumption’, the Reserve Bank lifted

cash rates over 1988 and 1989, with rates hitting highs of 18.2 per cent in November 1989.

Under the pressure of high interest rates, the economy contracted in December quarter 1989 and September

quarter 1990 ahead of the recession in the first half of 1991. Interest rates were progressively cut from 1990 and

didn’t stop falling until 1994.

What are the implications for investors?

No two periods are alike. The environment in 1988 was starkly different to current times. But in all times, investors

need to be aware of the risks and opportunities.

The Covid-19 pandemic shocked economies across the globe in 2020 and the response to the pandemic has

varied. Those shocks are still reverberating. Australia has done well in suppressing the virus, and all levels of

government and the Reserve Bank acted quickly in supporting businesses and families.

As a result, the economic recovery has been strong, but it is important not to be complacent. Risks lie to the

upside and downside. For instance an extended closure of foreign borders may make it difficult for firms to fill

open positions. Further, the longer that foreign borders are closed, the greater the risk that demand for homes will

reduce, affecting the home building sector. Policymakers must be agile in continuing to watch for the threats to

the economic recovery.

But if Australia continues on its current course, strong economic growth will boost employment and give increased

security to those in work. A tighter job market should bring higher wage growth. Businesses are well placed to

embrace low interest rates to lift investment. Low rates and government grants are boosting home construction

and the buoyant house building should continue over 2021.

Note that the Reserve Bank won’t be lifting interest rates until wage growth is closer to 3 per cent. At present

wages are “expected to pick up to a little under 2 per cent over 2021, before gradually increasing to around 2¼

per cent by mid 2023.” Even on the “upside” scenario, wage growth won’t hit 3 per cent before 2024, tempering

“boom” expectations.

But whether you call it a ‘boom’, economic nirvana or just a strong economic recovery, the economic outlook

seems bright.

The current investment environment is positive for consumer discretionary, construction, construction materials

and information technology sectors of the Australian sharemarket. Financials will benefit from the expectation of

firmer borrowing, but super-low interest rates will cap margins and revenue.

Based on traditional valuations, the sharemarket may seem expensive on the current share price to earnings ratio

(PE ratio) of 20.97 (the long-term average is 15.5). But valuations are more difficult to make in an environment of

near-zero interest rates. Continued strong economic growth would serve to boost corporate earnings and justify

current share prices.

The All Ordinaries index has hit record highs on numerous occasions over the past month. The benchmark ASX

200 is also expected to make new highs in coming weeks. The ASX 200 index is tipped to end the calendar year

at 7,200 points.

Craig James, Chief Economist, CommSec

Twitter: @CommSec

May 10, 2021 3You can also read