Managing global assets: keeping faith in low discount rates Alex Lyle, Head of Managed Funds

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Managing global assets: keeping faith in low discount rates Alex Lyle, Head of Managed Funds For professional investors only May 2021

Discount rates to remain low

Inflation risk? To us, inflation appears transitory

◼ Short-term risks Eurozone, UK and US Core Inflation:

◼ Capacity loss Range bound since 2000

◼ Bottlenecks

◼ Increased costs from COVID

◼ Less globalisation

◼ Environmental/regulatory costs

◼ Raw material prices

◼ We do not expect a material increase over the

medium term

◼ Capacity restored

◼ Long-term deflationary forces return

◼ Productivity improvements in the pipeline

Source: Macrobond, as at 11 May 2021.

2

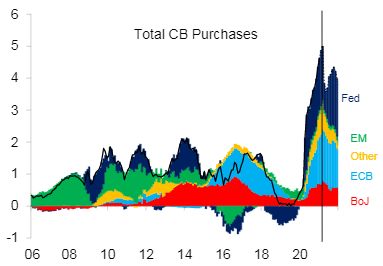

Discount rates to remain low

Reasons to be cheerful: Authorities have their feet on the floor

Rolling 12m global central bank purchases Fed Funds Futures curve

($trn)

Source: Citibank, as at 31 December 2020. Source: Macrobond, as at 13 May 2021

3

Bond outlook

We remain cautious on fixed income overall

10yr government bond yields Reasonable backdrop but little value

14% ◼ We expect yields to stay low in light of low

US Germany UK Japan

inflation and ongoing Quantitative Easing

12%

◼ Most attractive opportunities in: US Treasuries

10% and European periphery

8% ◼ Yet overall value is limited here, despite

increase in yields

6%

◼ Credit spreads remain fairly attractive

4%

2%

0%

-2%

1990 1995 2000 2005 2010 2015 2020

Source: Bloomberg, as at 10 May 2021.

4

The economic recovery

Governments also stoking the fire

Developed government gross debt and fiscal balances 20201 (% of GDP)

130 125,5

Gross public debt

125

120

115 +20.8%

110

104,7

105

100

Jan '20 Nov '20

0 WEO

-5 -3,0

-11.4%

-10

-15

-14,4

-20 Fiscal balance

Jan '20 Nov '20

WEO

Source: IMF, World Economic Outlook database; and IMF staff estimates, 2020 forecasts as at November 2020.

5The economic recovery

The ‘V-shape’

US Retail Sales and manufacturing PMIs US GDP: 2021 expectations upgraded

8%

6%

4%

2%

0%

-2%

-4%

2018 2019 2020 2021 2021

(Jan est.) (May est.)

Source: Macrobond, as at 11 May 2021. Source: Bloomberg, estimates are 1 January and 10 May 2021 consensus forecasts.

6The economic recovery

Excellent vaccine news

Daily new confirmed cases per million people All Americans offered a vaccine by August

1 000

800

600

400

200

0

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21

UK US

All intellectual property rights in the brands and logos set out in this slide are reserved by

respective owners. The mention of any specific shares or bonds should not be taken as a

Source: John Hopkins University CSSE COVID-19 Data, as at 8 May 2021. recommendation to deal.

7Equity prospects: Companies are surprising on the upside

And the ‘COVID winners’ are thriving

S&P500 EPS ahead of estimates by 22% US companies beating Q1 earnings estimates

100%

Beaten Reported

25% 50%

22,1%

86%

20%

0%

EPS Surprise

Q1 21

15% Amazon, Apple, Facebook, Microsoft &

Alphabet: Combined results: Q1-21 versus Q1-20

10% 100%

5% 50% +105%

+41%

0%

0% Revenue Profit

Q1 '16 Q1 '17 Q1 '18 Q1 '19 Q1 '20 Q1 '21 Source: Macrobond and S&P500, as at 5 May 2021. The mention of any specific shares or bonds

Source: Macrobond and S&P500, as at 11 May 2021. should not be taken as a recommendation to deal.

8Areas of interest in equities

Secular trends to continue and even accelerate

De-carbonisation Payments:

Digitisation Demographic change

Cloud computing But shorter-term, play the economic bounce

Re-opening/cyclicality

Medical tech

Source: Columbia Threadneedle Investments. All intellectual property rights in the brands and logos set out in this slide are reserved by respective owners. The mention of any specific shares or bonds should not

be taken as a recommendation to deal.

9Global property (REITs)

Near-term economic headwinds. Supportive structural trends

Neutral overall view Seeking a sustainable competitive advantage

+ Low funding costs Industrial Towers & data centres

+ Growth sectors of interest

- Retail format rapidly changing

- Future office requirements in question

Barriers

to entry

Seeking a Residential Self-storage

Pricing Low

power sustainable capex,

through competitive high

scale margin

advantage

Secular

demand

Source: Columbia Threadneedle and Stanlib, as at 31 March 2021. The mention of any specific shares or bonds should not be taken as a recommendation to deal. All intellectual property rights in the brands and

logos set out in this slide are reserved by respective owners

10Preferred asset classes for the medium term

Strongly Strongly

Dislike Neutral Favour

dislike favour

Fixed Income

Property

Some Equities

Positives and

opportunities in Focus on strong

negatives: leave

US Treasuries, economies of US

us net neutral

European & Asia and

with focus on

periphery and attractive growth

growth themes

credit companies

Columbia Threadneedle, as at May 2021.

11Important information

For use by Professional and/or Qualified Investors only (not to be used with or passed on to retail clients)

Past performance is not a guide to future performance. Your capital is at risk.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested.

Performance figures and other data relating to a fund or a representative account are provided for illustrative purpose only and may differ from that of other separately managed accounts due to such differences

as cash flows, charges, applicable taxes, and differences in investment strategy and restrictions.

Where references are made to portfolio guidelines and features, these are at the discretion of the portfolio manager and may be subject to change over time and prevailing market conditions. Actual investment

parameters will be agreed and set out in the prospectus or formal investment management agreement. An actual proposal will be subject to negotiations and the content of this document are not binding and

remain subject to contract.

Please note that the performance target may not be attained.

The analysis included in this document has been produced by Columbia Threadneedle Investments for its own investment management activities, may have been acted upon prior to publication and is made

available here incidentally. Any opinions expressed are made as at the date of publication but are subject to change without notice and should not be seen as investment advice. Information obtained from external

sources is believed to be reliable, but its accuracy or completeness cannot be guaranteed.

The mention of any specific shares or bonds should not be taken as a recommendation to deal.

This presentation and its contents are confidential and proprietary. The information provided in this presentation is for the sole use of those attending the presentation. It may not be reproduced in any form or

passed on to any third party without the express written permission of Columbia Threadneedle Investments. This presentation is the property of Threadneedle Investments and must be returned upon request.

This presentation is not investment, legal, tax, or accounting advice. Investors should consult with their own professional advisors for advice on any investment, legal, tax, or accounting issues relating an

investment with Columbia Threadneedle Investments.

Issued by Threadneedle Asset Management Limited. Registered in England and Wales, Registered No. 573204, Cannon Place, 78 Cannon Street, London EC4N 6AG, United Kingdom. Authorised and regulated in

the UK by the Financial Conduct Authority

Columbia Threadneedle Investments is the global brand name of the Columbia and Threadneedle group of companies.

12You can also read