MARA Project Asset Overview - January 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MARA

Project

Agua Rica – Alumbrera

Asset Overview

January 2021

669790

Cautionary Note

Regarding Forward-Looking Statements

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This presentation contains or incorporates by reference “forward-looking statements” and “forward-looking information” under applicable

Canadian securities legislation and within the meaning of the United States Private Securities Litigation Reform Act of 1995. Forward-looking information includes, but is not limited to leverage ratios,

information with respect to the Company’s strategy, plans, guidance and production outlook, or future financial or operating performance, continued advancements at Minera Agua Rica Alumbrera (MARA),

expected production and costs, and the general economics of the MARA project, mine plan optimization, simplified permitting process as a result of relying on Alumbrera processing facilities, expected higher

throughput rates without significant capital expenditure increases, plans and objectives for future exploration, future feasibility studies and environmental impact assessment in 2022, and the potential for

future additions to mineral resources and mineral reserves and mine life extensions. Forward-looking statements are characterized by words such as “plan,” “expect”, “budget”, “target”, “project”,

“intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are based on the opinions,

assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors

that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include the impact of general domestic and foreign business, economic and

political conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating metal prices (such as gold, copper,

silver and zinc), currency exchange rates (such as the Brazilian real, the Chilean peso, the Argentine peso, and the Canadian dollar versus the United States dollar), interest rates, possible variations in ore

grade or recovery rates, changes in the Company’s hedging program, changes in accounting policies, changes in Mineral Reserves (as defined herein) and Mineral Resources (as defined herein), and risks related

to acquisitions and/or dispositions, changes in project parameters as plans continue to be refined, changes in project development, construction, production and commissioning time frames, risks associated

with infectious diseases, including COVID-19, nature and climatic condition risks, risks related to joint venture operations, the possibility of project cost overruns or unanticipated costs and expenses, potential

impairment charges, higher prices for fuel, steel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, including but not limited to, failure of plant,

equipment or processes to operate as anticipated, unexpected changes in mine life, final pricing for concentrate sales, unanticipated results of future studies, seasonality and unanticipated weather changes,

costs and timing of the development of new deposits, success of exploration activities, permitting timelines, environmental and government regulation and the risk of government expropriation or

nationalization of mining operations, risks related to relying on local advisors and consultants in foreign jurisdictions, environmental risks, unanticipated reclamation expenses, title disputes or claims,

limitations on insurance coverage, timing and possible outcome of pending and outstanding litigation and labour disputes, risks related to enforcing legal rights in foreign jurisdictions, vulnerability of

information systems and risks related to global financial conditions, as well as those risk factors discussed or referred to herein and in the Company's Annual Information Form filed with the securities

regulatory authorities in all provinces of Canada and available at www.sedar.com, and the Company’s Annual Report on Form 40-F filed with the United States Securities and Exchange Commission. Although

the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors

that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events

could differ materially from those anticipated in such statements. The Company undertakes no obligation to update forward-looking statements if circumstances or management’s estimates, assumptions or

opinions should change, except as required by applicable law. The reader is cautioned not to place undue reliance on forward-looking statements. The forward-looking information contained herein is

presented for the purpose of assisting investors in understanding the Company’s expectations in connection with the upside potential of the MARA project, including production, financial and operational

performance and results at the MARA project and may not be appropriate for other purposes.

Non-GAAP Measures:

The Company has included certain non-GAAP financial measures and additional line items or subtotals, which the Company believes that together with measures determined in accordance with IFRS, provide

investors with an improved ability to evaluate the underlying performance of the Company. Non-GAAP financial measures do not have any standardized meaning prescribed under IFRS, and therefore they may

not be comparable to similar measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of

performance prepared in accordance with IFRS. The non-GAAP financial measures included in this presentation include: Free cash flow, cash costs per copper equivalent pound, EBITDA, all-in sustaining costs

per copper equivalent pound. Please refer to section 11 of the Company’s current third quarter Management’s Discussion and Analysis, and associated press release which is filed on SEDAR and includes a

detailed discussion of the usefulness of the non-GAAP measures. The Company believes that in addition to conventional measures prepared in accordance with IFRS, the Company and certain investors and

analysts use this information to evaluate the Company’s performance. In particular, management uses these measures for internal valuation for the period and to assist with planning and forecasting of future

operations.

Qualified Persons

Unless otherwise indicated, scientific and technical information contained in this presentation related to metallurgy and capital expenditure estimates has been reviewed and approved by Anthony Maycock, P.

Eng, of MM Consultores Limitada and scientific and technical information related to mining has been reviewed and approved by Rodrigo Nunes, MAusIMM CP (Min), Vice President (Mining), Optimize Group Inc.

All other scientific and technical information contained in this presentation has been reviewed and approved by Sébastien Bernier, P.Geo, an employee of Yamana Gold Inc. (Senior Director, Geology and

Mineral Resources). All of the individuals named above are "Qualified Person“s as defined by Canadian Securities Administrators' National Instrument 43-101 - Standards of Disclosure for Mineral Projects.

The information presented herein was approved by management of Yamana Gold on January 28, 2020.

All amounts are expressed in United States dollars unless otherwise indicated.

This presentation includes market and industry data which was obtained from various publicly available sources and other sources believed by the Company to be true. Although the Company believes it to be

reliable, the Company has not independently verified any of the data from third party sources referred to in this presentation, or analyzed or verified the underlying reports relied upon or referred to by such

sources, or ascertained the underlying assumptions relied upon by such sources. The Company does not make any representation as to the accuracy of such information

Confidential

Key MARA Project Highlights1,4

Globally competitive, de-risked copper development project with highly

attractive economics

• 27 year mine life based on mineral reserves and supported by 86km of drilling

High-grade, • High-grade open pit deposit with mineral reserve and mineral resource (“R&R”) growth over the past year

long-life orebody • Top 25 global copper producer when operational with potential for higher annual production rates

• Attractive NPV8 of $1.9bn and IRR of 21%

Attractive project 2

• Low AISC (US$1.49/lb) provides both gross margin and leverage to the copper price

economics and ramp- • Expected to commence production just as the copper supply gap is expected to materialize

up timing • Total LOM Capital of $3.9bn with initial capital of $2.8bn after reclassifying mining fleet costs from sustaining

• Conventional open-pit, truck and shovel mining operation and concentrator

• Higher certainty of capital costs due to minimum processing plant investment requirements

De-risked profile

• Use of existing Alumbrera facilities offers a deep real life understanding of the flowsheet performance, productivities

driven by Agua Rica - and cost profiles not typically available for greenfield projects and is expected to simplify the permitting process

Alumbrera integration • Historical operations at Alumbrera and local representation in Agua Rica provide intimate environmental and social

knowledge and existing open relationships with critical stakeholders, as well as qualified local workforce and services

• Forecast to produce over 900ktpa of concentrate over its first 5 years; copper smelters increasingly demanding

quality concentrate to blend and backfill excess supply

Attractive copper • MARA is currently forecast to produce a “custom clean”3 concentrate (LOM average arsenic level of 0.4%) during a

concentrate time when the global copper concentrate supply is expected to show an increase in arsenic content

• Low impurities beyond arsenic

• Significant by-product credits (19% of LOM revenue)

• Further Mine plan optimization ongoing; resequencing has showed and optimized grade profile and reduced re-handle

costs, and further improving base LOM economics

• Softer Agua Rica ore allows for full utilization of installed capacity; recent studies show that higher throughput rates

Potential for (up to 120ktpd+) could also be achievable without significant capex increases

upside/expansion • Potential resource expansions available at Agua Rica due to reclassification of inferred mineral resources within the

pit shell (mine plan based only on mineral reserves) and Alumbrera open pit remaining mineral resources

• Located within one of the most prolific copper producing region in the world with further exploration upside

• Opportunity to monetize rhenium in molybdenum concentrate (not included in PFS)

Notes non-GAAP measure can be found at www.yamana.com/Q32020

1 Information based on internal Agua Rica Prefeasibility Study B (the “PFS(B)”) 3. Defined as

Location and Project Overview

Proximally located to some of the largest and most successful mines in the

world

Asset landscape1 Project summary2`

Location Catamarca, Argentina

La Granja Pre-feasibility

Feasibility Post-integration ownership Yamana 56.25% / Glencore 25.00% / Newmont Goldcorp 18.75%

Construction Mineralization Cu-Mo-Au-Ag

Antamina

Operating

Mineral Reserves (30-Jun-19) 1,105Mt @ 0.49% Cu, 0.03% Mo, 0.21g/t Au, 2.8g/t Ag

Expansion

Mineral Resources (M&I)3 (30-

260Mt @ 0.28% Cu, 0.03% Mo, 0.11g/t Au, 1.8g/t Ag

Jun-19)

Cerro Verde Quellaveco PFS(A) complete (2019) - PFS(B) complete (2020)

Status

FS ongoing, expected 2022, EIA ongoing expected to be filed 2022

Toquepala

Collahuasi Study PFS(A) – July 19, 2019 PFS(B) Update - 2020

Quebrada Blanca

El Abra

Radomiro Tomic Ministro Hales Nameplate throughput 40Mtpa 42 Mtpa

Toqui Cluster Chuquicamata

Average annual CuEq 533 Mlbs (F10Y) 556 Mlbs (F10Y)

Spence Centinela Sulfide 4

Taca Taca production 452 Mlbs (LOM) 469 Mlbs (LOM)

Escondida

5

Salvador AISC per pound (LOM) $1.54 $1.49

MARA

Estimated mine life 28 years 27 years

NuevaUnion

Los Azules

Initial capital costs $2.39bn6 $2.78bn6

Los Pelambres El Pachon Sustaining capital costs $1.5bn6 $1.1bn6

Andina Division Los Bronces

LOM Strip Ratio (Operating) 1.66x 1.66x

El Teniente

NPV (8%): $3 Cu, $1300 Au $1,935mn $2,101mn

NPV (8%): $3 Cu, $1300 Au 7

300 km N/A $1,906 mn

(with progressive export tax)

Notes

1 Asset location data from S&P Global Market Intelligence IRR 19.3% 21.2%

2 Shown on a 100% basis. “PFS(A)” refers to press release dated July 19, 2019 on www.sedar.com

3 Mineral resources shown exclusive of mineral reserves. Mineral resources which are not mineral reserves do not have demonstrated economic viability. Further details including assumptions and reporting notes are presented in the full mineral

reserves and mineral resources estimates commencing on slide 17. Full table of Mineral Reserves and Mineral Resources available on slide 7.

4 Copper equivalent metal includes copper with gold, molybdenum, and silver converted to copper-equivalent metal based on the following metal price assumptions: $3/lb Cu, $1,300/oz Au, $$11/lb Mo, and $18.00/oz Ag.

5 A non-GAAP measure, additional line item or subtotal. A reconciliation of the IFRS measure to the non-GAAP measure can be found at www.yamana.com/Q32020. See “Cautionary Note Regarding Forward-Looking Statements”.

6 Initial capital reduced to US$2.4bn if first year of owner mine fleet purchases are reclassified as sustaining capital (as per PFS(A), details in press release dated July 19, 2019). Total LOM Capex remained the same.

7 Internal PFS(B) refers to the Case 7 model and it reflects the inclusion of progressive Argentina export tax, which was set to expire by 2021 at the time of PFS(A). Limited elements of the mine optimization developed for PFS(B) contain conceptual 4

estimates that will be detailed in the FS Confidential

Project Footprint

Conventional, low-risk operation that will leverage existing infrastructure

MARA Project location Project overview1

Bajo de la Alumbrera • Conventional high tonnage truck and shovel open pit mining, with crusher located at the

Mine / processing mine site

Agua Rica • Crushed ore will be conveyed 35km to the existing Alumbrera process plant via overland

and tunnel (6km) conveyor system

Power line

• The existing infrastructure of Alumbrera will be used for the processing of Agua Rica ore

Tucumán

Filter plant / rail loading

with minimal modifications expected to be required. The following existing Alumbrera

facilities will be utilized:

Belén Concentrate pipeline

o Concentrator plant, including grinding and flotation circuits, moly plant, and tailings

Catamarca system producing copper and molybdenum concentrates

o Agua Rica’s softer ore allows for the full utilization of the installed capacity

NVA rail o Tailings dam (which has capacity for processing the first 7 years of Agua Rica ore,

after which point the exhausted Alumbrera open pit is planned to be used as TSF)

El Pachón Córdoba o Concentrate transportation system (pipeline, filter plant, train and port shipping

facilities)

Rosario o Federal and provincial roads, all of which are in good condition, provide access to all

Port facility2 facilities in Catamarca and Tucumán provinces as well as the Alumbrera port

• Electrical power will be supplied from Alumbrera’s existing 220 kV powerline

Buenos Aires

• Concentrate will be pumped approximately 180km to the Tucuman filter plant, where it

will be filtered and loaded onto trains

o Filtered concentrate will then be railed 830km to the Rosario port, where it will be

shipped to customers; the Rosario Port has a 40,000 tonne concentrate storage

facility and requires minimum modification (increase of concentrate storage and

Projects handling capacity)

Operations • Integration with Alumbrera’s existing facilities is expected to simplify the permitting

300 km Cities and towns process as the MARA project possesses a smaller environmental footprint and enhances

Fluor, August 2013

the understanding of critical environmental, social and stakeholder issues

Notes

1 Information is based on PFS(A) unless otherwise noted, details in Yamana’s press release dated July 19, 2019 available at www.sedar.com. See “Cautionary Note Regarding Forward-Looking Statements”.

2 Rosario Port facility is on the western shore of the Paraná River

5

ConfidentialCapital Cost Build

3

Capital cost profile with adequate level of contingency

Initial capital cost breakdown 100% Initial Capex Breakdown

Plant, Process & Facilities Initial Capex

Item

Agua Rica Materials Handling (conveyor)

(US$m)

437

(% of total)

15.7%

5% 4%

Agua Rica Infrastructure 341 12.3%

Alumbrera Facilities 142 5.1%

Ore & Waste Rock Conveyance Tunnel 84 3.0%

Agua Rica Mine Site Facilities 95 3.4%

Indirect Costs

Contingency Costs

302

290

10.8%

10.4%

40%

Reclassification to Sustaining Capex (133) (4.8%)

Total 1,559 56.1%

Mine Initial Capital 51%

Item (US$m) (% of total)

Mine Contractor 601 21.6%

Other Mining 128 4.6%

Contingency 106 3.8%

Mine Equipment 281 10.1%

Total 1,116 40.1% Mine Capex Agua Rica Infrastructure

Owners' Cost Initial Capital 1 Plant Upgrades Owners' Cost

Item (US$m) (% of total)

Owners’ Project team 22 0.8%

General Expenses 17 0.6%

Pre-Opex and First Fills 10 0.4% • Update from PFS 2019 considers the reclassification of mining fleet

Agua Rica Services 11 0.4% from sustaining to construction, effectively reducing the LOM AISC

Other 45 1.6% from $1.52/lb to $1.49/lb

Total 106 3.8%

Total Initial Capital Costs

Item (US$m) (% of total)

• Processing Plant upgrades represent only 5% of the total initial

Plant, Process & Facilities 1,559 65.3% capex, significantly reducing the project complexity and execution

Mine 1,116 46.7% risk

Owners' Cost 106 4.4%

Total 2,781 100.0%

Total contingency 2 396 16.6%

Notes

1 11% contingency built into Owners’ cost estimate

2 Contingency percentage based on total initial capex exclusive of contingency cost 6

3 See “Cautionary Note Regarding Forward-Looking Statements”. Information from Internal PFS(B) Study

ConfidentialMineral Reserves and Mineral Resources

Significant and growing mineral reserve and mineral resource base

Reserves and Resources – Agua Rica (June 30, 2019)1,2

Tonnage Grade Contained

Cu Mo Au Ag Cu Mo Au Ag

(mt)

( %) ( %) ( g/ t ) ( g/ t ) (kt) (kt) ( m o z) ( m o z)

Proven 587 0.57% 0.03% 0.25 3.0 3,347 176 4.72 57.0

Probable 518 0.39% 0.03% 0.16 2.6 2,018 155 2.66 43.8

Total Reserves 1,105 0.49% 0.03% 0.21 2.8 5,366 331 7.38 100.8

Measured 54 0.22% 0.02% 0.13 1.6 118 11 0.22 2.7

Indicated 206 0.30% 0.03% 0.11 1.9 619 62 0.73 12.3

M&I (exc lusive) 260 0.28% 0.03% 0.11 1.8 737 73 0.95 15.0

Inferred 743 0.23% 0.03% 0.09 1.6 1,709 223 2.15 38.7

Medium Term Opportunities Agua Rica Mineral Resource

tonnage growth (Mt)

• Reclassification of Inferred material within the current pit

shell through infill drilling

• Potential to mine part of the remaining mineral resources in

Alumbrera as a starter project

1,105

743

260

Total Reserves M&I (exclusive) Inferred

Notes

December 31, 2018 June 30, 2019

1. 100% Basis. R&R for Agua Rica only, does not include R&R data for Alumbrera.

2. Mineral resources shown exclusive of mineral reserves. Mineral resources which are not mineral reserves do not have demonstrated economic viability. See slide 17 for Mineral Reserve and Mineral Resource

Reporting notes

7

ConfidentialCopper Concentrate Specification

Substantial copper concentrate production with LOM average copper

grade of 25%

Copper concentrate production (kt) and concentrate grade (%)1 Key metrics

Parameter Value

1,044 First 5 year

average

977 900ktpa

concentrate

production:

864 862 851

LOM average

788 concentrate 673ktpa

754 738 production:

716 728

688 695

675

640 625 LOM average Cu in

632 615 615

611 concentrate 25%

550 535 568 564 562 568 grade:

474

34%

31% 29% 28% 27%

28% 27%

26% 25% 26% 23% 23% 27% 24% 25% 26% 27% 25% 243

23% 23%

20% 20% 20% 20% 20%

26% 25%

'26E '27E '28E '29E '30E '31E '32E '33E '34E '35E '36E '37E '38E '39E '40E '41E '42E '43E '44E '45E '46E '47E '48E '49E '50E '51E '52E

Cu concentrate (kt) Cu concentrate grade (%)

Notes

1 Mine plan from Internal PFS(B) study. See “Cautionary Note Regarding Forward-Looking Statements”

8

ConfidentialCopper Concentrate Specification (Cont’d)

Significant by-products in concentrate, while the blending strategy allows

for the effective management of arsenic levels in concentrate

Metal production (kt Cu eq.) and grade (% Cu)1,2 LOM revenue split

Ag:

356 Copper By-products Copper grade Mo: 2%

7%

319

302 Au:

276 276 10%

235 244 245

222 223 215

193 195 201 208 205 191

187 180 177 182 183

176 168 165

160

0.9% Cu:

0.8% 0.8%

0.7% 81%

0.5% 0.6% 0.5% 78

0.4% 0.4% 0.4% 0.4% 0.3% 0.5% 0.4% 0.4% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4% 0.3% 0.4% 0.5% 0.4%

0.3%

0.6%

'26E '27E '28E '29E '30E '31E '32E '33E '34E '35E '36E '37E '38E '39E '40E '41E '42E '43E '44E '45E '46E '47E '48E '49E '50E '51E '52E

Arsenic level throughout LOM (%)3,4

0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.9%

0.4%

0.2% 0.2% 0.3%

0.1% 0.5%

As penalty threshold: 0.2%

'26E '27E '28E '29E '30E '31E '32E '33E '34E '35E '36E '37E '38E '39E '40E '41E '42E '43E '44E '45E '46E '47E '48E '49E '50E '51E '52E

As level (%)

Bismuth, antimony, mercury, lead, fluorine, chlorine, selenium, alumina, cadmium, and zinc are expected to be

below penalty levels3

Notes 3 Minor cadmium and zinc penalties may be present in select few years

1 Assumes metal prices of $3.06/lb Cu, $1,608/oz Au, $9.10/lb Mo, $20.54/oz Ag 4 Years added to the mine plan based on inferred tonnes are assumed to be 0.5% arsenic.

2 Shown on a pre-stream basis. Mine plan from Internal PFS(B) study. See “Cautionary Note

9

Regarding Forward-Looking Statements” ConfidentialMARA in Context

MARA is forecast to be a top copper producer when compared to today’s

largest copper mines

Copper production by mine (kt Cu)(1,3)

Escondida 1,185

Collahuasi 565

Morenci 460

El Teniente 460

Cerro Verde 455

Antamina 449

Buenavista 438

KGHM Polska Miedz 399

Chuquicamata 385

Las Bambas 383

Los Pelambres

If MARA was in production in 2020 it

363

Polar Division 356

Los Bronces 335 would rank among the top copper

producers in the world

Quellaveco 300

Grasberg 275

QB2 272

Kamoto 269

Radomiro Tomic 266 First 10 full years of production2

Toquepala 258

MARA 252

Taca Taca 242

Kansanshi 232

Producing

Mt Isa Copper 221

Development - First 10 years average production

Trident - Sentinel 220

Notes

1. Based on CY2019 production except Escondida, which is based on FY2020 production (year ended 6/30/2020).

2. Based on Internal PFS(B) study. See “Cautionary Note Regarding Forward-Looking Statements” 10

3. Source: Public company filings and press releases. ConfidentialMARA in Context (Cont’d)

(2)

MARA has one of the highest grades amongst comparable copper

development projects(3) …

0.90% Bubble size legend

(M&I CuEq Contained)

1Mt

0.80%

5Mt

Magistral

0.70% MARA

CuEq grade (%)

10Mt

Cotabambas

Galeno

0.60% El Pachon Quellaveco

Los Azules

Taca Taca

0.50% QB2

Canariaco Norte

Josemaria

0.40%

Zafranal

0.30%

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Ore Tonnage (Mt)(1)

Notes

1. Tonnage and M&I size shown on 100% ownership basis.

2. CuEq calculated using contained metal; Price assumptions are based on spot prices as at January 22, 2021 ($7,782/t Cu, $1,853/oz Au, $25.32/oz Ag, $10.18/lb Mo). 11

3. Source: Public company filings and press releases. ConfidentialMARA in Context (Cont’d)

… and MARA has one of the lowest capital intensity compared to other

significant copper development projects

Capital intensity

(US$m/kt Cu eq. M&I)(1,3)

Cotabambas 2.09

Zafranal 0.60

Josemaria 0.58

Los Azules 0.45

Quellaveco 0.44

El Pachon 0.43

Magistral 0.39

Canariaco Norte 0.36 Average(2): 0.56

QB2 0.32

Taca Taca 0.31

MARA 0.25 - 0.293

Galeno 0.19

MARA’s low capital intensity is driven by the ability to utilize Alumbrera’s existing infrastructure

Notes

1. Price assumptions are based on spot prices as at 1/22/2021 ($7,782/t Cu, $1,853/oz Au, $25.32/oz Ag, $10.18/lb Mo).

2. Excluding MARA. Source: Public company filings and press releases.

3. Calculated based on development capital expenditures and CuEq calculated using contained metal. Low end of MARA range reflects initial capex from PFS(A) and high end of MARA range reflects initial capex 12

from Internal PFS(B) study. See “Cautionary Note Regarding Forward-Looking Statements”. ConfidentialSummary Project Metrics

Forecast to consistently generate significant cash flow

Unlevered free cash flow profile1,2,3,4

1,068 1,028

979

802

586

501 522 509 514

465 474 461

396 400 367 384

355

313 308 307 302

177 209

136 106

209 (47) (72)

'26E '27E '28E '29E '30E '31E '32E '33E '34E '35E '36E '37E '38E '39E '40E '41E '42E '43E '44E '45E '46E '47E '48E '49E '50E '51E '52E '53E

EBITDA profile (US$m)1,4

1,404

1,252

1,179

1,101

746 764

665 629 619

954 562 560

498 535 515

424 438 472 455 438

400

307 325 608 689

503

(45)

'26E '27E '28E '29E '30E '31E '32E '33E '34E '35E '36E '37E '38E '39E '40E '41E '42E '43E '44E '45E '46E '47E '48E '49E '50E '51E '52E

Notes

1 Cost data based on Internal PFS(B); assumes metal prices of $3.06/lb Cu, $1,608/oz Au, $9.10/lb Mo, $20.54/oz Ag. “See Cautionary Note Regarding Forward-Looking Statements”

2 Shown on a post capex, post-tax, post-stream basis

3 Subject to tax optimization

4 A non-GAAP measure, additional line item or subtotal. A reconciliation of the IFRS measure to the non-GAAP measure can be found at www.yamana.com/Q32020

13

ConfidentialLeveraged to Metal Prices

MARA Leverage to Copper Price and Precious Metals

Metal Prices Sensitivity Summary1

Downside Downside PFS(B) Update Upside Upside

Scenario 2 Scenario 1 2020 Scenario 1 Scenario 2

Metal Prices

Copper $/lb 2.50 2.75 3.00 3.25 3.50

Gold $/oz 900 1,100 1,300 1,500 1,800

Molybdenum $/lb 7.0 9.0 11.0 13.0 15.0

Silver Price $oz 14.0 16.0 18.0 20.0 22.0

Production CuEq Mlbs

First 10-years 537 547 556 563 572

LOM 451 461 469 475 484

2

AISC

First 10-years $1.48 $1.46 $1.44 $1.42 $1.40

LOM $1.54 $1.51 $1.49 $1.47 $1.44

NPV (8%) $48 $986 $1,906 $2,710 $3,490

IRR after tax 8.4% 15.4% 21.2% 26.2% 30.8%

EBITDA (10-year

2 $502 $646 $791 $935 $1,090

Average) US$ M

Notes

1 Information is based on Internal PFS(B). “See Cautionary Note Regarding Forward-Looking Statements”. 14

2 A non-GAAP measure, additional line item or subtotal. A reconciliation of the IFRS measure to the non-GAAP measure can be found at www.yamana.com/Q32020

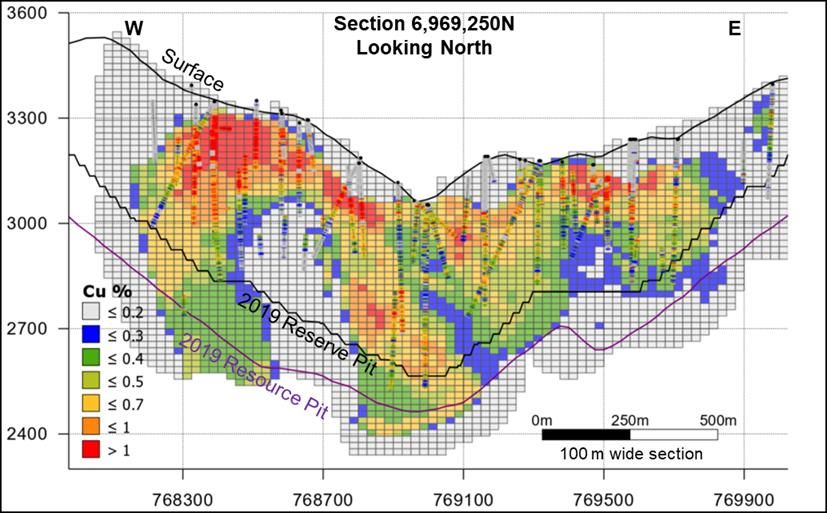

ConfidentialUpside Potential1

MARA possesses both concrete short term initiatives and longer term potential

enhancements that could materially improve the value of the project

• Throughput increase Agua Rica cross section

o Recent studies indicate a throughput rate of up to 120ktpd

High grade copper

is achievable and would require no significant process in first phases

plant modifications. This opportunity is being developed

as part of the Feasibility Study

• Further mine plan optimization under review; with new

sequencing expected to optimize production profile and

reduce re-handle costs

• Agua Rica mine life extension

o Existing Inferred mineral resource within the pit and the Inferred Resources with

deposit open at depth offer significant opportunity for potential to define

additional pushback Open at Depth

mine life extensions RPA, August 2013

o Mineral Resource below the Alumbrera open pit presents

an alternative for operators to supplement the Agua Rica Alumbrera processing facilities

ore or start production earlier, particularly in an

attractive copper price environment

• Regional exploration

o MARA is located in one of the most prolific copper

producing regions in the world, providing substantial

exploration upside

• Opportunity to monetize rhenium in molybdenum

concentrate

Notes 15

1 See “Cautionary Note Regarding Forward-Looking Statements”.

ConfidentialIntegration Agreement

MARA JV formally established in 2020

• On 7 March 2019, Yamana, Glencore and Goldcorp (now Newmont) (the “Owners”), recognizing the significant

economic benefits of using Alumbrera facilities for processing Agua Rica ore, entered into an integration agreement

(the “Integration Agreement”)

• The purpose of the Integration Agreement was:

o The establishment of the split of relative economic interests of the Owners in the combined integrated operation –

which are 56.25% Yamana, 25% Glencore and 18.75% Newmont Goldcorp and the creation of a Technical Committee

to advance the PFS and FS studies along with other project matters

o The facilitation of the interim period following which the Owners could complete an Integration Transaction,

entering into a joint venture agreement and associated documents which will govern future development and

operations of the integrated project

• On December 18, 2020, the Owners announced the completion of the formal Integration thereby entering into a JV:

o Yamana is the Manager of the JV and responsible of advancing the project to a construction decision

o A series of committees were formed to provide guidance and oversight on the project, as well as compliance and

HSEC matters

o The Alumbrera cash balances of US$220 M as of December 31st, 2020 became part of the MARA project

• The project expenses are financed pro-rata to the ownership percentages

• The product is available to the Owners for purchase pro-rata to their ownership percentages

16

ConfidentialAgua Rica Mineral Reserve and Mineral Resource

Reporting Notes – June 30, 2019

Mineral Reserves Mineral Resources

Mineral Reserves are estimated using a variable Mineral Resources are estimated using a variable

metallurgical recovery. metallurgical recovery.

Average metallurgical recoveries of 86% Cu, 35% Au, 43% LOM average metallurgical recoveries of 86% Cu, 35% Au,

Ag, and 44% Mo were considered. 43% Ag, and 44% Mo were considered.

Open pit Mineral Reserves are reported at a variable cut- Mineral Resources are constrained by an optimized pit

off value averaging $8.42/t, based on metal price shell based on metal price assumptions of $4.00/lb Cu,

assumptions of US$3.00/lb Cu, $1,250/oz Au, $18/oz Ag, $1,600/oz Au, $24/oz Ag, and $11/lb Mo. Open pit

and $11/lb Mo. A LOM average open pit costs of $1.72/t Mineral Resources are reported at a variable cut-off value

moved, processing and G&A cost of $6.70/t of run of which averages $8.42/t milled with overall slope angles

mine processed. The strip ratio of the mineral reserves is varying from 39° to 45° depending on the geotechnical

1.7 with overall slope angles varying from 39° to 45° sector.

depending on the geotechnical sector.

1. CIM (2014) definitions were followed for mineral reserves and mineral resources.

2. All mineral resources are reported exclusive of mineral reserves.

3. Mineral resources which are not mineral reserves do not have demonstrated economic viability.

4. Mineral reserves and mineral resources are reported as of June 30, 2019.

5. Mineral reserves QP, Giorgio de Tomi, MIMMM CEng. Member of the Institute of Minerals, Materials and Mining (UK), and Chartered Engineers

(UK) of Deswick Brazil, consultants to Yamana. Mineral resources QP, Matthew Hastings, MAusIMM(CP) and Berkley Tracy, PG, CPG, PGeo,

SRK Consulting (U.S.) Inc.

17

ConfidentialYou can also read