"Disciplined Liquids Development in Four Prolific Core Areas" - Investor Presentation - Advantage Oil & Gas LTD.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

“Disciplined Liquids Development in Four Prolific Core Areas” Investor Presentation TSX: AAV November 2019

ADVANTAGE AT A GLANCE

TSX 52-week trading range $1.35 - $3.46

Shares Outstanding (basic) 187 million

Market Capitalization $0.4 billion

Enterprise Value $0.7 billion

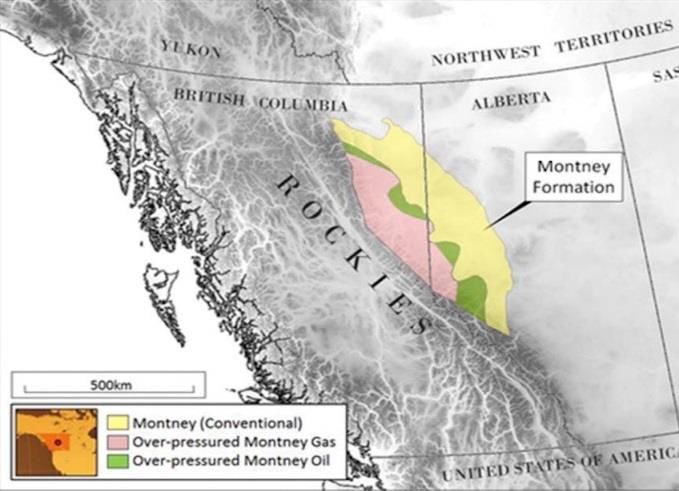

Advantage Montney Assets

2019 Guidance (1)

Total Production 43,500 to 46,500 boe/d

Liquids Production (~100% Increase vs 2018) 2,900 to 3,200 bbls/d

Progress

Glacier

Q3 2019 Production Valhalla

Total Production 42,080 boe/d

BC AB

Liquids Production 3,142 bbls/d Pipestone/

Wembley

6 Miles

Notes:

(1) Forward-looking information. Refer to three year development plan (November 1, 2018 and Advantage holds 134,400 net acres (210 net

July 8, 2019 news releases) and Advisory for material assumptions and risk factors. sections) in the condensate/light oil-rich

Montney Glacier/Pipestone fairway

2

BUILDING ON FOUNDATIONAL ASSETS, TRANSITIONING TO TOP-TIER LIQUIDS

Solid Today Solid Tomorrow

Reinvest in Our High Return

Free Cash Generating Asset

Liquids Assets

Retain Competitive Edge with

Ultra-Low Costs Commanding Infrastructure

Minimal Commitments and Self-

Financial Strength & Flexibility Funding Program

Revenue Diversification to

Exposure to AECO < 20%(1) Continue by Increasing Liquids

(1) Forward-looking information. Percent of forecast revenue expected to be exposed to AECO in 2019 & beyond. Refer to three year

development plan (November 1, 2018 and July 8, 2019 news releases) and Advisory for material assumptions and risk factors.

3

COMMITMENT TO ENVIRONMENTAL LEADERSHIP AND SUSTAINABILITY

“A Proud Clean Energy Producer – The World Needs More of Our Energy”

CO2 Sequestration Plant Flared Volumes as Percent of

(tonnes CO2e accredited) Production

90,367 Improved operating efficiencies and

0.34%

90,000 tonnes CO2e equates to 0.30% lower emission equipment design

approx. 20,000 vehicles (1)

0.22%

57,410 56,999 0.14%

47,393

40,853

2014 2015 2016 2017 2018 2015 2016 2017 2018

Non-Producing Wells vs LMR • Natural gas is the fastest way to reduce

Non-Producing Net Wells (AIF 2018)

5,000 CO2 emissions – by displacing coal

Ultra-low liability

4,000 exposure • Created 650 full-time jobs/year over the

last 5 years

3,000

• Contributed >$1 million to community

Advantage

2,000 programs since inception

1,000 • Fully reclaimed equivalent of 60% of

legacy Advantage field sites to date

0

0 10 20 30 40 • See Sustainability Report on AAV website

LMR (Jan 2019) (1) Based on estimates per Environmental Protection Agency emissions per vehicle 4

(2) LMR – Liability Management Ratio as determined by Alberta Energy Regulator

LIQUIDS DEVELOPMENT PROGRAM OBJECTIVES

Total Revenue Diversification Value Enhancement (1)

>50% Liquids by 2021

• Transition to >50% liquids revenue

(condensate/light oil)

20% Liquids

39% Midwest US • Double digit Adjusted Funds Flow

9% 53% (“AFF”) per share growth

Dawn

12% Fixed Price • Double digit return on capital

Empress employed

17%

AECO

39% 16% • Generates significant free cash &

Well Diversified

19% maintains Total Debt to AFF ~2.0x

Natural Gas

Portfolio

16%

8% • Preserves low cost structure

2%

20%

15% 11% • Develops significant AFF from

4% Wembley, Progress & Valhalla in

2019E 2020E 2021E addition to Glacier

Notes: (1) Forward-looking information. Refer to three year development plan (November 1, 2018 and

July 8, 2019 news releases) and Advisory for material assumptions and risk factors. 5

LIQUIDS DEVELOPMENT UNDERPINNED BY TOP TIER ASSETS (1)

Condensate & Light Oil Focused

6 miles • Glacier asset generating free cash

Progress

• Significant oil pool discovery at

Progress

Glacier • Liquids development underway

‘The Foundation’ in all land blocks

Valhalla

• Utilize 3rd party gas processing for

initial Pipestone/Wembley wells

BC AB • Two 5,000 bbls/d liquids hubs at

Multi-zone Pipestone/Wembley and

Pipestone/ Progress to be constructed (100%

Premium Liquids Wembley

Development working interest)

Throughout the

Fairway • Existing spare processing capacity

at Glacier Plant to accommodate

growth at Progress and Valhalla

(1) Forward-looking information. Refer to three year development plan (November 1, 2018 6

and July 8, 2019 news releases) and Advisory for material assumptions and risk factors.

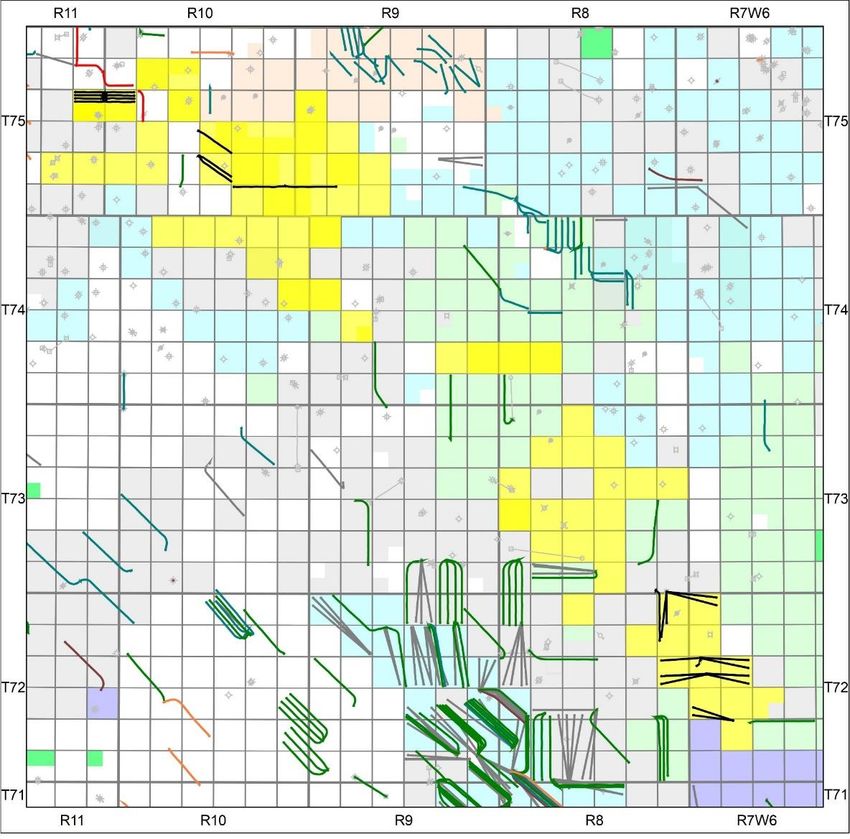

OPERATIONS OVERVIEW – SHIFTING TO MIDDLE MONTNEY LIQUIDS

Deep Liquids-Rich Inventory (1)(2)(3)

Booked Undeveloped Unbooked Upside

Progress

TOTAL future

location inventory

Glacier ~1,400 to 1,500

697

Valhalla

70

Pipestone/ 216 244

129 11

Wembley

100 bbls/mmcf

• Total of ~210 net sections (134,400 net acres)

• Middle Montney is liquids-rich throughout (25 to 280

bbls/mmcf)

• Only 75 liquids-rich wells drilled to date – 6% of inventory

Liquids-rich

• 100% Ownership of Glacier Gas Plant

Middle Montney

• 400 mmcf/d raw gas capacity, 6,800 bbls/d liquids

handling

(1) Management Estimates. Refer to Advisory.

(2) Based on Sproule December 31, 2018 Reserves Report.

(3) C + shallow cut recoveries. 7

3

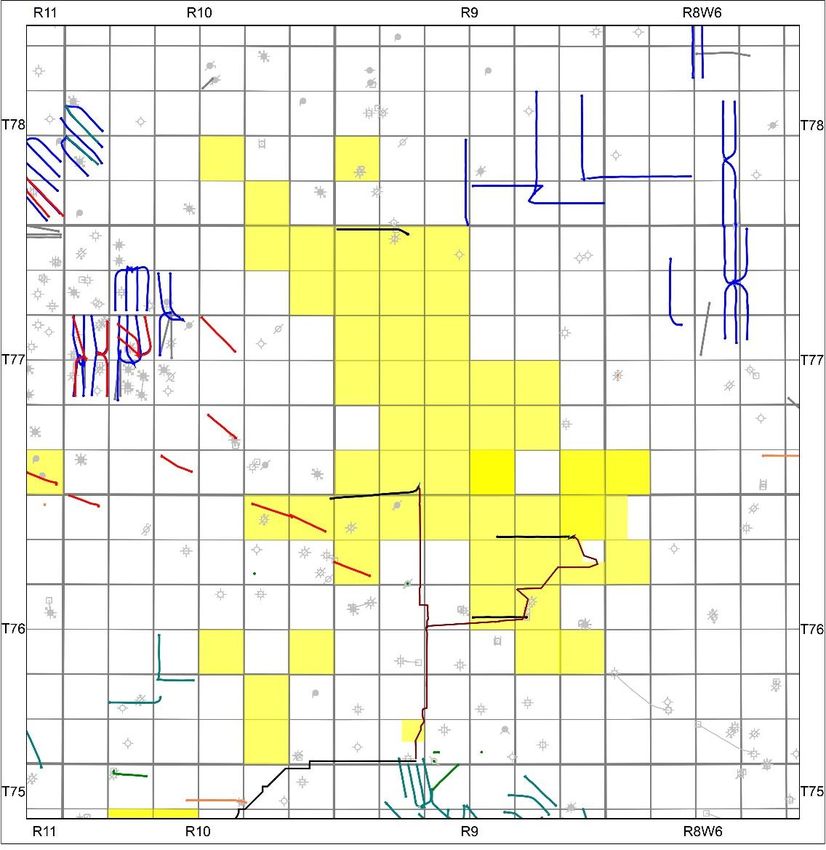

ADVANTAGE MONTNEY – MULTIZONE DEVELOPMENT THROUGHOUT

Wembley

primary target

Valhalla liquids

appraisal targets

Glacier liquids

zones New oil pool discovery

Advantage Operated HZ

Offset Operator HZ

8

WEMBLEY/VALHALLA (PIPESTONE) LIQUIDS RICH DEVELOPMENT

• 71 net sections in the premium, multi-

Recently completed D3 Well

layer, liquids fairway

30% liquids (IP30)

• Valhalla wells are tied into AAV Glacier

Plant to the West

Valhalla • Wembley wells will flow South to

New 5 well pad Tidewater and Keyera plants

7,117 boe/d

(22% liquids)(1)

Competitor well • Seven Wembley wells planned for Q3/Q4

Confidential competitor well IP30 1,422 boe/d

(~41% oil, NGL not available) (67% liquids) (4)

2019, plus one water disposal

Confidential competitor well

(~44% oil, NGL not available) AAV 12-25 • Wembley area continues to show

(62% liquids) predictable, top tier results across the

fairway (150-300 bbls/mmcf)

Pipestone/Wembley

4 well pad

drilling • Valhalla showing similar results, though

earlier in development

Half-cycle Economics(2)(3)

(AECO Cdn $2.00/mcf & $US 60/bbl WTI)

Rate of Return % Payout Years Breakeven(3)

>90% 1.3 - 1.4

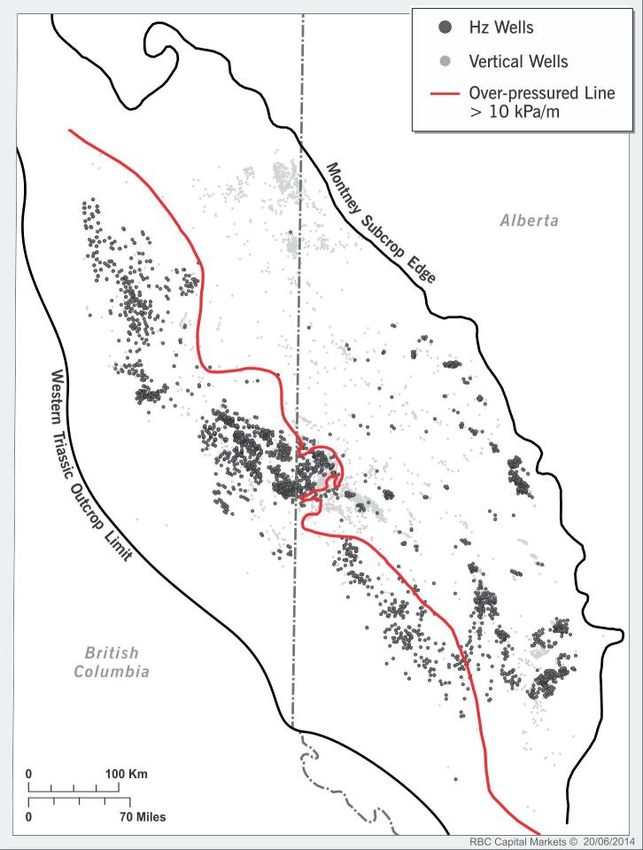

SIGNIFICANT LIGHT OIL POOL DISCOVERY AT PROGRESS

Kelt Oil Wells Tourmaline Oil Wells

Up to 153,000 bbls CTD Up to 152,000 bbls CTD

13-31 Montney D1 (2017)

• 50 net sections assembled at low cost

over 5 years

• Appraisal drilling began in 2017

• 4 Advantage wells drilled to date

• Recent advancement in frac design at

16-36 Montney D3 (1) 16-36 resulted in >1,000 bbls/d oil rate(1)

1,038 bbls/d oil

290 bbls/d NGL

• Recent pressure data indicates majority

4.9 mmcf/d gas

02/2-34 Montney D3 (2018)

of lands are over-pressured

• Pipeline to AAV Glacier Plant to be

constructed November 2019

Progress oil wells are expected to

5-22 Montney D3 (2018)

be competitive with

Tie in to AAV

Glacier Plant

Wembley/Pipestone

(1) Average rate at 5,168 kPa over 72 hours at end of frac flowback and production test. Entrained NGLs calculated using composition

from 02/2-34 well and shallow-cut recoveries. Production rates were continuing to increase prior to the well being shut in due to

flare limitations. Preliminary results are not necessarily indicative of long-term performance or of ultimate recovery. 10LIQUIDS-RICH MIDDLE MONTNEY AT GLACIER STEPPING UP

• Early development was in Upper and Lower

Q1 2019 10 Well

Middle Montney Pad – Montney (lean gas)

Average Final Rate 422

bbls/d (73 bbls/mmcf) • Recent focus on Middle Montney, where liquids

range from 25 to 80 bbls/mmcf

• 89 net sections

• 750 well inventory (4), including 480 liquids-rich

• Low costs = resilient netbacks

• IP30 well liquids rates up to 400 bbls/d

Half-cycle Economics(1)(2)

(AECO Cdn $2.00/mcf & $US 60/bbl WTI)

Q4 2018 5 Well Middle

Montney Pad – Average

Breakeven(3)

Final Rate 428 bbls/d per Rate of Return % Payout Years (AECO Cdn $)

Well (85 bbls/mmcf)

40% - 90% 1.4 – 2.2STRATEGIC INFRASTRUCTURE CONTROL, FLEXIBLE PIPELINE ACCESS

100% Owned Glacier Gas Plant –

400 mmcf/d Raw Gas + 6,800 bbls/d C3+ Liquids Extraction

TCPL Groundbirch

Lateral

BC AB Advantage Glacier

Gas Plant

Future AAV Progress

Liquids Hub

AAV Liquids Handling Hub Keyera

2,000 bbls/d Pipestone Plant

• NGTL sales gas firm transportation service in-place.

6 miles

Connection to Alliance pipeline completed.

Company Land

• >100 mmcf/d surplus capacity available at Glacier Plant Company Gas Plant

3rd Party Gas Plants

TransCanada Pipeline

• Pipeline to tie Progress in to AAV Glacier Plant to be Pembina Pipeline

Advantage Pipeline Tidewater AAV Wembley Liquids Hub

constructed by November 2019 Alliance Pipeline Pipestone Plant 5,000 bbls/d Q2-2020

Tidewater Pipeline

• 3rd Party processing secured to match early

Pipestone/Wembley growth profile

122019 GUIDANCE AND ESTIMATES (1)(2)

Average production (boe/day) 43,500 - 46,500

Gas production (mmcf/d) 244 to 260

Liquids production (bbls/d) 2,900 to 3,200

% Liquids / % Condensate/light oil 7% / 76%

Royalties ($/boe) and Royalty Rate (%) $0.40 (3%)

Operating Cost ($/boe) $2.00

Transportation Cost ($/boe) $3.40

G&A/Finance Cost ($/boe) $1.50

Cash Used in Investing Activities (4) (millions) $180 to $200

Net Capital Expenditures (3)(4) (millions) $180 to $200

Notes:

(1) Forward-looking information. Refer to Advisory for cautionary statements regarding Advantage’s budget and three-year development plan including

material assumptions and risk factors.

(2) Refer to Three Year Plan news release dated November 1, 2018 and 2019 capital expenditure guidance in news release dated July 8, 2019.

(3) Non-GAAP Measure which may not be comparable to similar non-GAAP measures used by other entities. Refer to Advisory.

(4) Net Capital Expenditures is the same as Cash Used in Investing Activities as no change in non-cash working capital is assumed between years and

other differences are immaterial.

13THREE YEAR DEVELOPMENT PLAN – LIQUIDS TRANSITION(1)

Total Production (boe/d) Liquids Production and 14,000 bbls/d

Exit

Composition (bbls/d) 10,500 to

48,500 to

46,000 to 52,500 11,500

43,500 to 48,000

46,500

22% 6,500 to

7% 15%

7,500

2,900 to

C5+ /

78% light oil

3,200

76%

76%

2019G 2020E 2021E 2019G 2020E 2021E

Gas Liquids % of Total

Costs ($/boe) Three Year Development Plan

$1.55 • Capital program calibrated to maintain

$1.60

G&A and

$1.50 strong balance sheet

Finance $3.65

$3.55 • Flexibility exists to manage gas production

Transport $3.40 with minimal impact on adjusted funds

$2.95 flow

$2.60

Operating $2.00

$0.40 $0.75 $1.20

Royalties

2019G 2020E 2021E

Notes:

(1) Forward-looking information. Refer to three year development plan (November 1, 2018 and July 8, 2019 news releases) 14

and Advisory for material assumptions and risk factors. G – Guidance, E - EstimatesDEVELOPMENT PLAN PRICE SENSITIVITY(1)

Gas Price Sensitivity Oil Price Sensitivity

Total Debt to Adjusted Funds Flow (2) Total Debt to Adjusted Funds Flow (2)

AECO $1.30/mcf AECO $1.70/mcf WTI US$50.00/bbl WTI US$70.00/bbl

(@ WTI US$58/bbl Flat) (@ AECO Cdn$1.65/mcf Flat)

2.0

1.8 1.8 1.9

1.6

1.6 1.6

1.3

1.4 1.2

1.0

0.6

2019 2020 2021 2019 2020 2021

Notes:

(1) Forward-looking information. Refer to three year development plan (November 1, 2018 and July 8, 2019 news releases) and

Advisory for material assumptions and risk factors.

(2) Non-GAAP measure which may not be comparable to similar non-GAAP measures used by other entities. Refer to Advisory.

(3) Estimated average three-year C5+/Light Oil differential to WTI of US$7.50/bbl and FX $0.755 Cdn/US. Other market 15

diversification based on future prices as of April 2, 2019.STRONG HEDGES AND TRANSPORTATION IN-PLACE (1)

Current Hedging Transactions (MMcf/d) Hedging Strategy

140 90% • Summer 2019 AECO hedges mitigate

AECO ($Cdn/Mcf) volatility

80%

120 $2.87 $2.87

Dawn ($US/Mmbtu) • Expect to hedge both liquids and natural

70% gas in future periods

100 $3.01 % of AECO Exposure

Hedged 60%

% of Dawn Exposure

80 $3.01 Hedged 50% Transportation

60 40% • Sufficient current and future

transportation capacity available to meet

$3.16

30% requirements of 2019-2021 development

40 $2.83 $1.84 $1.84 $2.12

20% plan

$2.26 $1.36 $1.36

20 • Actively manage contracted

10%

$1.36 transportation capacity to optimize

0 0% portfolio

Q1-19 Q2-19 Q3-19 Q4-19 Q1-20 Q2-20 Q3-20 Q4-20

Notes:

(1) Forward-looking information. Refer to three year development plan (November 1, 2018 and July 8, 2019 news releases)

and Advisory for material assumptions and risk factors.

16Financial Discipline Operationally Nimble Returns Focus

APPENDIX

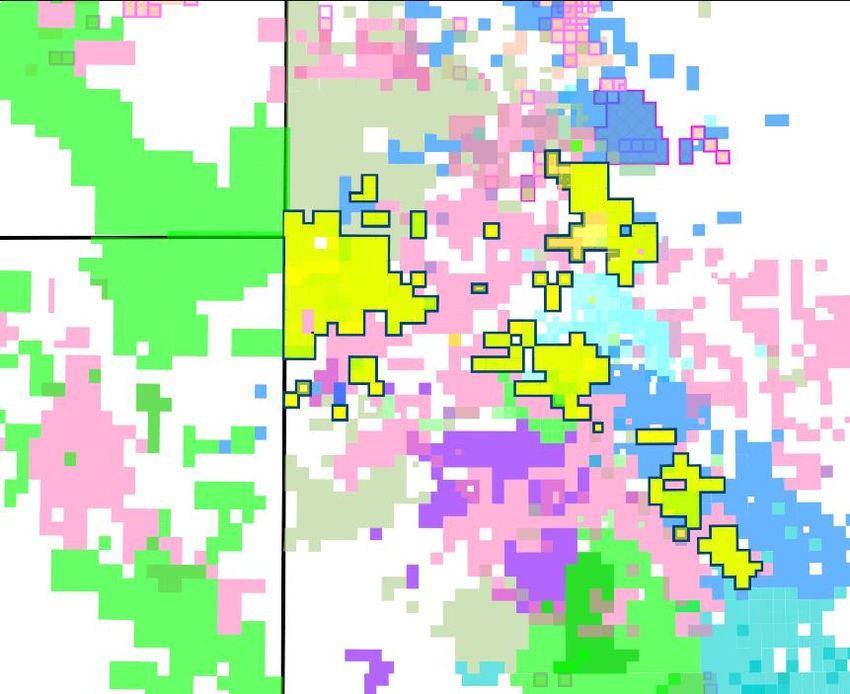

18GLACIER – LOCATED IN THE HEART OF THE MONTNEY RESOURCE PLAY

BC AB

Glacier

Pipestone Liquids Fairway

Source: Geoscout, Corporate Presentations

Montney Siltstone Comparison:

• 700 times more permeability

• 4x more formation thickness

• Very low clay content

• Liquids & Improved well efficiencies strong economics

Up to 83 bbls/MMcf

19CONTINUOUS IMPROVEMENT HAS LED TO EXCEPTIONAL EFFICIENCIES

20MIDDLE MONTNEY PRODUCTION CONTINUES TO INCREASE

2018/19 11 wells

Gen 6: Slickwater, OH Packers, Stage

• 2017+ Middle Montney wells with frac design changes

completions Avg 33 frac stages including >30 frac stages & numerous mechanical

systems evaluated

2016/17 6 Wells

• 39 total Middle Montney wells on-production across

Gen 5: Slickwater, OH Packers, Cased

hole & Stage completions Glacier land block.

Avg 27 frac stages

2015 13 wells

Gen 4: Slickwater, OH Packers

Avg 19 frac stages

2014 3 wells

Gen 3: Slickwater, OH Packers

Avg 15 frac stages

2013 4 wells

Gen 2: Poly CO2, & Slickwater Plug and Perf

Avg 13 frac stages

2012 2 wells

Gen 1: Poly CO2, Sand Plugs,

Avg 15 frac stages

Middle Montney Budget Type Curve (IP30 5.0 mmcf/d & 5.0 Bcf)

21GLACIER MONTNEY ASSIGNED 2P EUR PER WELL & INTERVAL

Glacier - 2P Recoveries per Interval(1)

# of Gross HZ Wells 2P Recovery [bcf/well]

Developed Undeveloped Total Developed Undeveloped Total

Interval

YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE

2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018

1 UM 103 111 115 141 133 130 244 244 245 4.9 5.1 5.2 5.9 5.8 5.8 5.4 5.5 5.5

2 MM 12 15 22 52 65 61 64 80 83 5.8 5.6 6.4 5.2 5.6 5.4 5.3 5.6 5.7

3 MM 8 10 13 25 35 40 33 45 53 4.5 4.4 4.6 4.1 4.4 4.4 4.2 4.4 4.5

4 MM 2 3 4 5 11 14 7 14 18 6.1 7.4 7.7 5.9 6.6 6.6 6.0 6.7 6.8

5 LM 43 51 54 84 81 86 127 132 140 7.1 7.7 7.8 6.4 6.5 6.4 6.6 6.9 6.9

Total 168 190 208 307 325 331 475 515 539

Valhalla - 2P Recoveries per Interval(1)

# of Gross HZ Wells 2P Recovery [bcf/well]

Developed Undeveloped Total Developed Undeveloped Total

Interval

YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE YE

2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018

1 UM 2 4 4 5 5 2 9 9 2.9 6.6 6.8 7.9 7.5 2.9 7.3 7.2

2 MM 1 2 2 5 7 1 7 9 4.4 4.3 5.0 4.1 4.2 4.4 4.2 4.4

4 MM 1 1 2 2 0 3 3 2.1 3.8 2.1 3.4 2.1 3.5

Total 3 7 7 0 12 14 3 19 21

(1) Based

on Sproule 2016 - 2018 year-end reserve reports. Indicated raw gas volumes per well. Refer to Statement of Reserves Data and

Other Oil and Gas Information in the Corporation’s Annual Information Forms which are available at www.sedar.com and 22

www.advantageog.com.WEMBLEY MONTNEY ASSIGNED 2P EUR PER WELL & INTERVAL

Wembley Montney Assigned 2P EUR Per Well & Interval(1)

# of Gross HZ Wells 2P Gas & Free Liquids Recovery [bcf/well mstb/well]

Interval Developed Undeveloped Total Developed Undeveloped Total

YE YE YE YE YE YE YE YE YE YE YE YE

2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018

4 MM 1 11 0 12 2.3 358 2.3 358 2.3 358

Total 0 1 0 11 0 12

(1) Based on Sproule 2017 and 2018 year-end reserve reports. Indicated raw gas volumes per well. Refer to Statement of Reserves Data and

Other Oil and Gas Information in the Corporation’s Annual Information Forms which are available at www.sedar.com and 23

www.advantageog.com.ADVISORY

Forward-Looking Information and Statements

The information in this presentation contains certain forward-looking information and forward-looking statements (collectively, "forward-looking statements")

within the meaning of applicable securities laws relating to the Corporation's plans and other aspects of its anticipated future operations, management focus,

strategies, financial, operating and production results and business opportunities. These statements relate to future events or our future intentions or performance.

All statements other than statements of historical fact may be forward-looking statements. The statements have been prepared by management to provide an

outlook of the Corporation's activities and results and may not be appropriate for other purposes. Forward-looking statements are often, but not always, identified

by the use of words such as “seek”, “anticipate”, “plan”, “continue”, “estimate”, “guidance”, “demonstrate”, “expect”, “may”, “can”, “will”, “project”, “predict”,

“potential”, “target”, “intend”, “could”, “might”, “should”, “believe”, “would” and similar expressions and include statements relating to, among other things, the

Corporation's 2019 to 2021 Development Plan (the "Plan"), the Plan's development focus and the timing thereof, the expected sources of funding for the Plan;

expected results and benefits to be derived from the Plan include, but are not limited to, increasing the anticipated amount of annual average liquids production,

increasing C5+/light oil production mix and the expected amount of C5+/light oil production mix, diversifying the Corporation's revenue sources including the

composition of natural gas and liquids, developing additional operational and infrastructure optionality and how this will be achieved; annual production average

and the expected amount by which total annual average production will be increased by in 2019 to 2021; expected net capital expenditures for 2019 to 2021,

including the expected focus and allocation of such expenditures; the expected cumulative capital investment over the Plan's three years; resource development

potential beyond the Plan and the Corporation's future drilling inventory; the benefits derived from third party processing arrangements the Corporation entered

into with two midstream firms; and other matters. Advantage’s actual decisions, activities, results, performance or achievement could differ materially from those

expressed in, or implied by, such forward-looking statements and accordingly, no assurances can be given that any of the events anticipated by the forward-looking

statements will transpire or occur or, if any of them do, what benefits that Advantage will derive from them.

With respect to the forward-looking statements contained in this presentation, Advantage has made a number of material assumptions regarding, but not limited

to: current and future commodity prices; the Corporation's current and future hedging program; future exchange rates; future production and composition

including natural gas and liquids; royalty regimes and future royalty rates; future operating costs; future transportation costs and availability of product

transportation capacity; future general and administrative costs; the estimated well costs including frac stages and lateral lengths per well; the number of new

wells required to achieve the objectives of the Plan; that the Corporation will be able to complete its infrastructure projects on a timely basis; the timing for the

construction to be completed on third party mid-stream facilities; timing and amount of net capital expenditures; and that the Corporation will have sufficient

financial resources required to fund its capital and operating expenditures and requirements as needed.

24ADVISORY

Management has included the summary of assumptions and risks related to forward-looking information in order to provide shareholders with a more

complete perspective on Advantage's future operations and such information may not be appropriate for other purposes. Advantage’s actual results,

performance or achievement could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no

assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits

that Advantage will derive there from. Management does not have firm commitments for all the costs, expenditures, prices or other financial assumptions

used to prepare the forward-looking information or assurance that such operating results will be achieved and, accordingly, the complete financial effects of

all of those costs, expenditures, prices and operating results are not objectively determinable. Readers are cautioned that the foregoing lists of factors are

not exhaustive. The Corporation and management believe that the statements have been prepared on a reasonable basis, reflecting management's best

estimates and judgments. However, because this information is highly subjective and subject to numerous risks including the risks discussed above, it should

not be relied on as necessarily indicative of future results. These forward-looking statements are made as of the date of this presentation and Advantage

disclaims any intent or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or results or

otherwise, other than as required by applicable securities laws.

These statements involve substantial known and unknown risks and uncertainties, certain of which are beyond Advantage’s control, including, but not

limited to: changes in general economic, market and business conditions; industry conditions; impact of significant declines in market prices for oil and

natural gas; actions by governmental or regulatory authorities including increasing taxes and changes in investment or other regulations; changes in tax

laws, royalty regimes and incentive programs relating to the oil and gas industry; the effect of acquisitions; Advantage's success at acquisition, exploitation

and development of reserves; failure to achieve production targets on timelines anticipated or at all; unexpected drilling results; changes in commodity

prices, currency exchange rates, net capital expenditures, reserves or reserves estimates and debt service requirements; the occurrence of unexpected

events involved in the exploration for, and the operation and development of, oil and gas properties, including hazards such as fire, explosion, blowouts,

cratering, and spills, each of which could result in substantial damage to wells, production facilities, other property and the environment or in personal

injury; changes or fluctuations in production levels; individual well productivity; lack of available capacity on pipelines; delays in anticipated timing of drilling

and completion of wells; delays in completion of infrastructure; lack of available capacity on pipelines; individual well productivity; competition from other

producers; the lack of availability of qualified personnel or management; credit risk; changes in laws and regulations including the adoption of new

environmental laws and regulations and changes in how they are interpreted and enforced; our ability to comply with current and future environmental or

other laws; stock market volatility and market valuations; liabilities inherent in oil and natural gas operations; uncertainties associated with estimating oil

and natural gas reserves; competition for, among other things, capital, acquisitions of reserves, undeveloped lands and skilled personnel; incorrect

assessments of the value of acquisitions; geological, technical, drilling and processing problems and other difficulties in producing petroleum reserves; ability

to obtain required approvals of regulatory authorities; and ability to access sufficient capital from internal and external sources. Many of these risks and

uncertainties and additional risk factors are described in the Corporation’s Annual Information Form dated February 28, 2019 which is available at

www.Sedar.com and www.advantageog.com. Readers are also referred to risk factors described in other documents Advantage files with Canadian

securities authorities.

25ADVISORY

Oil and Gas Information

Barrels of oil equivalent ("boe") and thousand cubic feet of natural gas equivalent ("mcfe") may be misleading, particularly if used in isolation. Boe and mcfe

conversion ratios have been calculated using a conversion rate of six thousand cubic feet of natural gas equivalent to one barrel of oil. A boe and mcfe

conversion ratio of 6 mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value

equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the

energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

This presentation discloses drilling inventory in the Glacier, Valhalla, Progress and Pipestone/Wembley areas in three categories: (i) proved locations; (ii)

probable locations; and (iii) unbooked locations. Proved locations and probable locations are derived from Sproule Associates Limited reserves evaluation

effective December 31, 2018 and account for drilling locations that have associated proved and/or probable reserves, as applicable. Unbooked locations are

internal estimates based on our prospective acreage and an assumption as to the number of wells that can be drilled per section based on industry practice

and internal review. Unbooked locations do not have attributed reserves or resources. Of the 1,400 to 1,500 total drilling locations identified herein, 327 are

proved locations, 29 are probable locations and 1,044 to 1,144 are unbooked locations. Unbooked locations have been identified by management as an

estimation of our multi-year drilling activities based on evaluation of applicable geologic, seismic, engineering, production and reserves information. There is

no certainty that the Corporation will drill all unbooked drilling locations and if drilled there is no certainty that such locations will result in additional oil and

gas reserves, resources or production. The drilling locations on which we actually drill wells will ultimately depend upon the availability of capital, regulatory

approvals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results, additional reservoir information that is obtained and other factors.

While certain of the unbooked drilling locations have been de-risked by drilling existing wells in relative close proximity to such unbooked drilling locations,

other unbooked drilling locations are farther away from existing wells where management has less information about the characteristics of the reservoir

and therefore there is more uncertainty whether wells will be drilled in such locations and if drilled there is more uncertainty that such wells will result in

additional oil and gas reserves, resources or production.

References in this presentation to production test rates, initial production rates, IP30 rates, flow rates, yields and other short-term production rates are

useful in confirming the presence of hydrocarbons, however such rates are not determinative of the rates at which such wells will commence production and

decline thereafter and are not indicative of long term performance or of ultimate recovery. Additionally, such rates may also include recovered "load oil"

fluids used in well completion stimulation. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate

production of Advantage. Advantage cautions that the test results should be considered to be preliminary.

26ADVISORY

Advantage has presented certain type curves and well economics for its Montney areas. The type curves presented are based on Advantage's historical

production. Such type curves and well economics are useful in understanding management's assumptions of well performance in making investment

decisions in relation to development drilling in the Montney area and for determining the success of the performance of development wells; however, such

type curves and well economics are not necessarily determinative of the production rates and performance of existing and future wells and such type curves

do not reflect the type curves used by our independent qualified reserves evaluator in estimating our reserves volumes. The type curves differ as a result of

varying horizontal well length, stage count and stage spacing. The type curves represent the average type curves expected. In this presentation, estimated

ultimate recovery represents the estimated ultimate recovery associated with the type curves presented; however, there is no certainty that Advantage will

ultimately recover such volumes from the wells it drills.

In presenting such type curves, inputs and economics information and in this presentation generally, Advantage has used a number of oil and gas metrics

which do not have standardized meanings and therefore may be calculated differently from the metrics presented by other oil and gas companies. Such

metrics include DCE+T, "EUR", "NPV10", "payout", "rate of return" (or "ROR"), "half cycle ROR", and “operating netback". EUR represents the estimated

ultimate recovery of resources associated with the type curves presented. NPV10 represents the anticipated net present value of the future net revenue

discounted at a rate of 10% associated with the type curves presented. Payout means the anticipated years of production from a well required to fully pay

for the DCE+T of such well. ROR means the rate of return of a well or the discount rate required to arrive at a NPV equal to zero. Half cycle ROR means the

rate of return of a well or the discount rate required to arrive at a NPV equal to zero when taking into account "half cycle" costs, which include drilling,

completion, equip and tie-in capital expenditures.

Production estimates contained herein are expressed as anticipated average production over the calendar year. In determining anticipated production for

the years ended 2019 to 2021 Advantage considered historical drilling, completion and production results for prior years and took into account the

estimated impact on production of the Corporation’s 2019 to 2021 expected drilling and completion activities.

27ADVISORY

Non-GAAP Measures

The Corporation discloses several financial and performance measures that do not have any standardized meaning prescribed under International Financial

Reporting Standards ("IFRS" or “GAAP”). These financial and performance measures include “net capital expenditures”, “adjusted funds flow”, “total debt”,

and “total debt to adjusted funds flow”. Such financial and performance measures should not be considered as alternatives to, or more meaningful than

measures determined in accordance with GAAP including “net income”, “comprehensive income”, “cash provided by operating activities”, or “cash used in

investing activities”. Management believes that these measures provide an indication of the results generated by the Corporation’s principal business

activities and provide useful supplemental information for analysis of the Corporation’s operating performance and liquidity. Advantage’s method of

calculating these measures may differ from other companies, and accordingly, they may not be comparable to similar measures used by other companies.

“Net capital expenditures” include total capital expenditures related to property, plant and equipment and exploration and evaluation assets incurred during

the period. Management considers this measure reflective of actual capital activity for the period as it excludes changes in working capital related to other

periods. The Corporation considers “adjusted funds flow” to be a useful measure of Advantage’s ability to generate cash from the production of natural gas

and liquids, which may be used to settle outstanding debt and obligations, and to support future capital expenditures plans. Changes in non-cash working

capital are excluded from adjusted funds flow as they may vary significantly between periods and are not considered to be indicative of the Corporation’s

operating performance as they are a function of the timeliness of collecting receivables or paying payables. Expenditures on decommissioning liabilities are

excluded from the calculation as the amount and timing of these expenditures are unrelated to current production, highly variable and discretionary. “Total

debt” is the total of bank indebtedness and working capital deficit. “Total debt to adjusted funds flow” is a ratio calculated as total debt divided by adjusted

funds flow for the previous four quarters. Total debt to adjusted funds flow is considered by management to be a useful measure as it is commonly used to

evaluate the leverage of a company and the ability to settle outstanding debt and obligations with cash generated from operations. Refer to the

Corporation’s most recent Management’s Discussion and Analysis, which is available at www.sedar.com and www.advantageog.com, for additional

information about certain financial measures, including reconciliations to the nearest GAAP measures, as applicable.

28ADVISORY

Abbreviations

The following abbreviations used in this presentation have the meanings set forth below.

bbl barrel

bbl/d barrel per day

bbls/d barrels per day

bbls/mmcf barrels per million cubic feet

boe barrels of oil equivalent of natural gas, on the basis of one barrel of oil or natural gas liquids for six thousand cubic feet of natural gas

boe/d barrels of oil equivalent per day

GJ Gigajoule

mcf thousand cubic feet

Mcfe thousand cubic feet equivalent on the basis of six thousand cubic feet of natural gas for one barrel of oil or natural gas liquids

mmcf/d million cubic feet per day

mmcfe/d million cubic feet equivalent per day

NGL natural gas liquids

DCE+T drill, complete, equip and tie-in

C3+ propane plus

C5+ pentanes plus

29ADVANTAGE CONTACT INFORMATION

Investor Relations

1.866.393.0393

ir@advantageog.com

www.advantageog.com

Listed on TSX: AAV

Advantage Oil & Gas Ltd.

Suite 2200, 440 – 2nd Avenue SW

Calgary, Alberta T2P 5E9

Main: 403.718.8000

Facsimile: 403.718.8332

Advantage 100% W.I. Glacier Gas Plant

Andy Mah, P.Eng. Director, President & Chief Executive Officer

Mike Belenkie, P.Eng. Chief Operating Officer

Craig Blackwood, C.A. Chief Financial OfficerYou can also read