Market Commentary August 2020 - Capital Tower Ltd

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market

Commentary

August 2020

The Right Advice At The Right Time

Capital Tower Ltd, 85 Yarmouth Road, Norwich, Norfolk, NR7 0HF

Capital Tower Ltd Registered in England and Wales No. 03411161

Authorised and regulated by the Financial Conduct Authority

Pressure: pushing down on me, Pressing down on you, no man ask for. Under pressure that burns a building down, Splits a family in two, Puts people on streets. That’s OK. That’s the terror of knowing What this world is about. Watching some good friends screaming, “Let me out!” Tomorrow gets me higher. Pressure on people, people on streets. OK. Chippin’ around, kick my brains ‘round the floor. These are the days: it never rains but it pours. People on streets. People on streets. It’s the terror of knowing What this world is about. Watching some good friends screaming, “Let me out!” Tomorrow gets me higher, higher, high! Pressure on people, people on streets. Turned away from it all like a blind man. Sat on a fence, but it don’t work. Keep coming up with love, but it’s so slashed and torn. Why, why, why!? Love, love, love, love, love. Insanity laughs under pressure. We’re breaking. Can’t we give ourselves one more chance? Why can’t we give love that one more chance? Why can’t we give love, give love, give love, give love, give love, give love, give love, give love, give love? ‘Cause love’s such an old-fashioned word, And love dares you to care for the people on the edge of the night, And love dares you to change our way of caring about ourselves. This is our last dance. This is our last dance. This is ourselves. Under pressure. Pressure. Queen and David Bowie – “Under Pressure” 02

market commentary

“No Pressure – No Diamonds.”

Thomas Carlyle – 19C Scottish Historian

In the 1985 film Brewster’s Millions, Richard Pryor, our Investment Process, and which we follow, is

as Monty Brewster, is “under pressure” to spend $30 Royal London Asset Management. They attribute

million in 30 days so that he can inherit $300 million. the success of a range of their global multi asset

Of course, the 1980s is over 30 years ago, and so funds to the way they align fund management to the

allowing for inflation, today’s required expenditure Corporate Life Cycle of companies. One of the fund

would be much higher. Our new Chancellor, Rishi managers explains it like this:

Sunak, didn’t seem under much pressure when

he spent £30 billion in 30 minutes in his Summer “Thinking like a CEO: using the Life Cycle to navigate the

Statement. This pushes the deficit to £300 billion crisis.

– but who will pay for it? We may all come under

pressure in the future. However, Britain is not alone as “Our investment universe comprises around 6,000 stocks.

it ramps up spending. The world over, central banks We are fundamental, bottom-up investors, so we need a

are printing money to bankroll governments during way to understand the world and categorise companies

the Covid crisis. When this stops, perhaps in the that isn’t rooted in top-down macroeconomics. The broad

autumn, then it will be a test of countries’ creativity to economic environment will have an effect, of course, but

deal with it. We have covered some alternative ways we believe that good companies perform well across the

in previous commentaries. economic cycle. What matters more is how the company is

using its capital.

One of the consequences of this is that National

Savings products have become much more attractive. “Through a proprietary algorithm, our Corporate Life Cycle

The NS&I’s increased funding target is partly an model categorises companies according to their stage of

acknowledgement of reality – in the first three development. Quantitative analysis helps us to identify

months of 2020/21, NS&I raised a net £14.5bn. NS&I potential opportunities by scoring stocks across a range

is currently offering table-topping interest rates (for of detailed financial factors. We then apply our scoring

example, 1.16% AER for Income Bonds, and a 1.40% system to rank characteristics to identify which companies

prize rate on Premium Bonds). NS&I looks set to be to conduct further fundamental research into for possible

dominant in the savings market in a way that it has inclusion in the portfolio.

not been for some years. The decision to allow this is

probably more political than financial. “As figure 1 shows, the Corporate Life Cycle plots

economic returns against required returns (that is to

“A man out walking with his dog is like the economy say, cost of capital) and describes a typical corporate

and the stockmarket. The man walks in a fairly journey. It describes five distinct phases: Accelerating,

straight line. The dog on the other hand runs off Compounding, Slowing & Maturing, Mature,

madly in random directions every minute. When the and Turnaround. These elp us to understand where

man reaches his destination, he will have travelled companies are in their journey and how to analyse them

say 1 kilometre. The dog will have travelled say to pick the real winners – and, perhaps more importantly,

4 times that (if not more) but reaches the same avoid the potential losers.

destination. The man is the economy. The dog is the

stockmarket” “One of the advantages of our Life Cycle framework is that

Andre Kostolany, legendary Hungarian-born investor it helps us to think like a CEO: where to deploy capital,

1906–1999 what the returns are on that capital and should we be

shrinking, or growing capital deployed to certain divisions?

One of the select fund managers that currently meets Depending on where businesses are in the Life Cycle,

03

market commentary

they should approach the crisis differently. Companies grocery delivery platform, the company is a global

in the ‘Accelerating’ stage have the opportunity to grow leader and has licenced the technology to supermarket

quickly and should take advantage of the opportunities chains internationally. The current environment has

presented. They are often innovators and are culturally favoured the business versus its competitors, accelerating

more flexible and able to embrace change. This can be a its development and customer demand. Ocado has

huge advantage in uncertain times and that innovation raised capital to take advantage of these additional

can disrupt other markets, some of them large. Amazon is opportunities.

a poster child for this, both on the home delivery shopping

side, where it was rolling out additional capacity to move “Companies in the ‘Slowing & Maturing’ category of the

towards next day delivery in the US. Its cloud business Life Cycle frequently have a mix of business operations or

Amazon Web Services (AWS) has also been a major divisions. The current environment is an opportunity to re-

beneficiary of the lockdown as it enables businesses to evaluate their core competencies and areas of competitive

scale up computing power in a very short time. Most advantage. The crisis provides an opportunity for greater

people working from home will be using remote desktop discipline around where to reinvest capital, considering

systems, many of which will be hosted on AWS. the returns available. The lockdown has a different

footprint around the world with many Asian countries

“Furthermore, Netflix hosts its online streaming content on far less impacted relative to Europe or the US. This might

the AWS platform, despite being a competitor of Amazon be an opportunity to shrink underperforming divisions

Prime Video. In lockdown, many customers will have used and allocate that capital to areas of higher return. As

both of these services more and Amazon has increased the an example, Tesco has sold some of its international

competitive advantage that it enjoyed going into crisis. operations to focus on its core business.

“Ocado, the UK grocery delivery service and technology Potential losers?

platform provider, is another beneficiary of the crisis. “‘Turnarounds’ are some of the businesses that are under

Having spent almost 20 years developing its online most threat from the crisis. These are companies that

04

market commentary

“Optimism is unfashionable today, particularly

among intellectuals. Everyone makes fun of

it. Someone said, ‘Pessimists got that way

financing optimists.’ But I’m not pessimistic and

I advise you not to be. As the fellow said, ‘I’d be

a pessimist, but it would never work.’”

John Gardner, author who took over the

mantle of writing the James Bond books in

the 1980s.

already have low returns on capital and to create wealth companies (high returns and strong balance sheets)

for shareholders, need to turn around and improve those getting stronger as they are better able to take advantage

returns. The lockdown makes this even more challenging. of opportunities, whether through new areas of demand

or having better balance sheets to navigate through lower

“The reward for management teams that are prepared to levels of cash generation in most industries. No single

take the initiative and have a balance sheet that matches model or analysis is a magic bullet for investing; but seeing

the operational volatility side of their business should the world as a company’s management sees it helps to

be positive. There will be opportunities as competitors identify those that are actively responding to the crisis.

struggle, go bankrupt or have to raise capital at punitive Owning companies that merely survive the pandemic

rates. Cost cutting should be easier as the business won’t deliver outperformance. We are looking for the

rationale is easily understood and, in many cases, there are ‘Accelerators’ that are increasing investment to take full

government schemes to help. advantage of the current environment, and ‘Slowing &

Maturing’ or ‘Turnaround’ companies that are doubling

“Having an appropriate balance sheet will help some down on restructuring.”

businesses prosper over others that have taken on too

much leverage. Those that can survive should enjoy higher The best fund managers have a process behind them that

returns in the next cycle as capital will exit some industries. helps focus their minds, avoids complacency, and typically

While this is a challenging area to invest in, it is also where delivers results.

valuations are most attractive. The data shows that it is

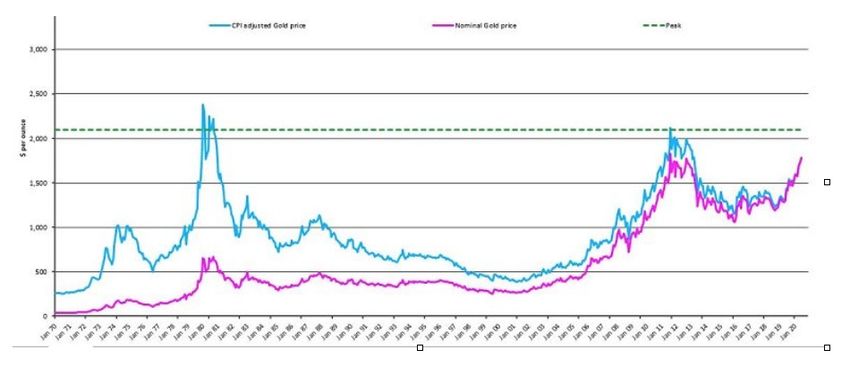

less well covered by analysts, so there are likely to be more Gold Rush

opportunities. The gold price has been rising steadily and recently

hit an all-time high, beating its previous record high of

Identifying alpha $1,922 in 2011.

“Overall, we believe that the crisis will result in strong

Chart 1: The gold price since 1970 ($/oz)

Source: Bloomberg, Schroders, July 2020

05

market commentary

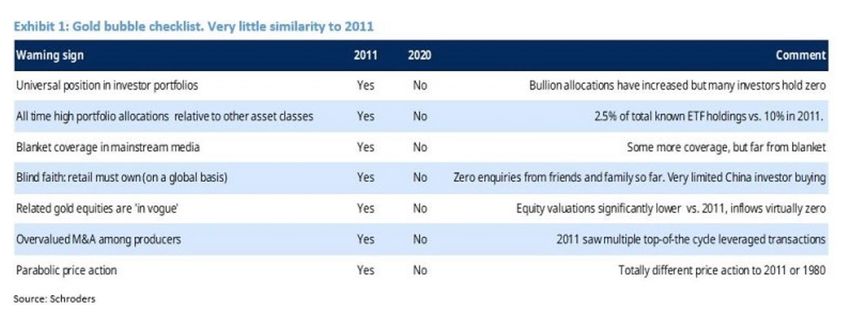

Such heights have led some investors to rue missing of dangerous bubble phase. The result is that there are

out on gold’s recent moves, viewing it now as expensive very obvious differences between now and 2011.

or even in a bubble. After a year-to-date rise of more

than 20%, following a similar rise in 2019, this is an One area where momentum has been clearly

understandable reaction. But taking a long-term aggressive is in ETF buying of physical gold. It has been

view (of years, not weeks), this may not be the correct the standout (in fact, the only) area of demand growth

reaction. And gold equities in particular are signalling in the 2020 gold market. The numbers themselves are

that this cycle has a lot further to run. Here’s why. indeed very striking. According to published data, 643

tonnes have been added to physical gold ETFs so far

Looking at history, it’s worth pointing out that gold bull this year, comparing to 372 tonnes added in all of 2019.

markets tend to end in sharp moves upwards, virtually In 2009, we saw a record annual increase of 665 tonnes.

in a straight line. In 2011, for example, gold surged

around 15% in the month before the peak and only For comparison, 656 tonnes equate to almost 40%

ever traded above $1,800 for 19 days. of global gold production. Since the Federal Reserve

effectively declared in April that it would do “whatever

The peak average annual price was actually in 2012 at it takes” to keep the economy from collapsing, ETF

$1,669, well below current levels. In 1981, gold prices holdings of gold have risen 72 out of 79 days. Surely the

moved 80% between December 1979 and January scale of total ETF holdings (3200 metric tonnes in total,

1980, an even more aggressive parabolic move. Below or 104 million ounces) represents an unsustainable

is a checklist of warning signs to help us and other bubble? Again, we really don’t think so. In an era of

investors gauge whether gold is already in some kind truly gargantuan global liquidity creation and highly

06

market commentary

elevated financial asset valuations, what really matters

is how large these holdings are on a relative basis.

Looked at this way, gold holdings are not particularly

high at all. In 2011, gold ETF holdings represented “It is a capital mistake to

c.10% of all ETF holdings globally. Today that number is

closer to 2.5%. Looked at on a more aggregate measure, theorise before one has data.

we estimate above-ground gold stocks represent just Insensibly one begins to twist

over 2.7% of total global financial assets, a vastly lower

number than either 2011, 1980 or 1974.

the facts to suit theories, instead

of theories to suit facts.”

Against a backdrop of record-high global debt, we

believe we are moving through a major epoch-

Sherlock Holmes in The Sign of Four

change in global macro policy towards a much greater by Sir Arthur Conan Doyle

acceptance of inflationary outcomes. The result is

likely to be more deeply negative real interest rates

and greater risk of broad currency debasement. In this

environment, continued increases in gold allocations

could have extraordinary impacts on aggregate private

gold holdings.

There is no obvious reason why gold prices should leading to both record operating margins and record-

be capped at current levels in such an environment. forecast free cash flow generation, which is likely in

For gold producers, current operating conditions are turn to trigger material increases in distributions to

exceptionally good and again stand in stark contrast shareholders. Despite this, gold equities have only just

to 2011. On the revenue side, gold prices are being begun to outperform the price of bullion itself, another

driven by understandably strong demand for gold as a sign this cycle has further to run, as shown below.

monetary hedge. Meanwhile, operating costs remain

broadly under control and management attitudes to

large scale capital spending remain conservative. This is

Chart 3: Gold producer equities have barely begun to outperform the underlying gold price

FTSE Gold miners index divided by gold price (shown as a ratio)

07

market commentary

SUMMARY statistical evidence from other experts to support

his views. Most often from the excellent site https://

We have largely avoided comment on the virus itself coronavstats.co.uk/uk.

in these issues, but the quote above summarises the

main reason for the massive impact of Covid-19. It is The graph below is taken from their website on 27th

an unknown with the potential to kill, and we are all July 2020.

fearful. It is fear that makes us sell shares – even though

logic may say otherwise. Sadly, this fear is just the fuel There has been an increase recently in the number of

the media needs to keep us in panic and retain our lurid identified cases in the UK, but that is most likely down

interest in them. to the massive amount of testing being carried out –

which is now the most in Europe. We also now need to

Yet behind the apocalyptic headlines, you will find little question the actual cause of deaths as it has transpired

snippets of pragmatism that tell us the reality. American that Public Health England were counting deaths where

finance writer Morgan Housel wrote in late July that in individuals may have recovered some months ago but

the US, from a health point of view, life is as safe as it’s subsequently died from unconnected causes (even

ever been. In 1918, roughly 1000 deaths per 100,000 a car crash) as Covid deaths. This will not be unusual

were from infectious diseases. Now it’s down to 46 per to us – in Texas and Florida, the definition of a “case”

100,000. And he goes on to say that, because local news was changed by local health authorities on 18th May,

over the years has finally given way to non-stop global from one where a positive test equalled one case, to a

news, this makes the world feel perpetually broken “probable case”. That’s where, if you have a cough or

because there’s always a tragedy somewhere and you temperature, you become a “case” without being tested.

are guaranteed to hear about it. Pessimism sounds Furthermore, up to 15 more “probable cases” are added.

more seductive than optimism to the media. That’s people you may have been in contact with, in

theory. Ludicrous exaggeration.

One of the experts we have been following for some

time is renowned oncologist Professor Karol Sikora (@ Add to that the many very clever scientists both in the

ProfKarolSikora). His Twitter account is an amazing UK and around the world who have provided better

site of calm reflection and guidance. Promoting the ways to treat the virus and offer potential for a vaccine

08

market commentary

just around the corner, and maybe the situation isn’t

anywhere near as bad as might be portrayed.

That is not to say Covid-19 is not a serious condition

nor that we should ignore government guidelines.

“The oldest and strongest

Indeed, by following these it is more likely the virus emotion of mankind is fear and

will be beaten, and we can return to (hopefully an the oldest and strongest fear is

improved) normality.

fear of the unknown.”

So, whilst there may appear to be many reasons to Horror fiction writer Howard P

be fearful, we still believe there are more reasons to

remain Cautiously Optimistic…

Lovecraft (1890–1937)

09

Capital Tower Ltd, 85 Yarmouth Road, Norwich, Norfolk, NR7 0HF Capital Tower Ltd Registered in England and Wales No. 03411161 Authorised and regulated by the Financial Conduct Authority This commentary is compiled internally by Capital Tower Ltd and reflects our views based on the extensive industry research we receive each month. It does not however constitute advice or a recommendation to invest. You should always seek our professional advice before proceeding with any investment.

You can also read