Market survey - 2019/Q1 Hamburg - German Property Partners

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market survey Commercial | Investment 2019/Q1 Hamburg Hamburg | Sylt | Berlin

Commercial | Investment

Hamburg 2019/Q1

Key Facts Investment

€0.5bn | -65% year-on-year change

18% | -9 pp year-on-year change

Office: 47% | -4pp year-on-year change

Office: 2.8% | -0.1 pp year-on-year change

Commercial: 2.7% | -0.2 pp year-on-year change

Logistics: 4.5% | +0.3 pp year-on-year change

pp = percentage point

Transaction volume Share of foreign investors Strongest asset class (Net) Prime yield

“The rather slow start to 2019 is the consequence of last Six properties, traded at between €25m and €50m, made up

year’s record result. A large number of big-ticket sales were the largest share of the market, taking some 44% of the total

made in 2018, leaving a much-reduced choice of properties volume. Only one property, the “Arne-Jacobsen-Haus” (Überse-

and depressing the volume traded in the first quarter.” ” ering 12) in City North, sold by Vattenfall Europe to Matrix Im-

Axel Steinbrinker | Managing director mobilien, commanded a price over €50m. Vattenfall sold the

building it has so far occupied itself for around €60m. When

Transaction volume Vattenfall has moved out of the building, which is under a pres-

A rather slow start to 2019 ervation order, the new owners plan to refurbish the property

and erect a new building on the part of the site available for re-

Investment trading in commercial properties in Hamburg was development. Vattenfall will be moving into the “EDGE Elbside”

rather sluggish at the beginning of 2019. Whereas the volume a development project located on Amerigo-Vespucci-Platz,

traded during the same quarter of 2018 was €1.3bn (28 trans- HafenCity, in 2023.

actions), the totals at the end of the 1st quarter of 2019 stood

at €460m and 21 transactions. Year on year, therefore, the

volume traded fell by around 65%. Whereas numerous trades

with price tags of more than €100m were characteristic of the Transaction volume

prior year’s market, such transactions were in short supply in 2015-2019/Q1 | in € bn

the first three months of 2019. Only one trade in this price cat-

egory was initiated in the 1st quarter.

10-year average (2009–2018):

ca. €3.2bn

The biggest single known transaction was the sale of the building

site at Großer Burstah 3, for which Gator paid Commerz Real Forecast

over €100m. At the end of 2018 it was already apparent that

the owner of the development site, a Commerzbank subsidiary,

was planning to sell it to the Hamburg property firm Gator. Al-

though this trade alone accounted for more than a fifth of the

total volume, the bulk of the overall result for the 1st quarter of

2019 was comprised of transactions costing up to €50m. The Q1

4,0 4,5 3,6 6,0 0.5

majority of transactions, eleven, were priced at €10m or less,

but they contributed only 13% or some €59m to the total result. 2015 2016 2017 2018 2019/Q1

Source: Grossmann & Berger GmbH

www.grossmann-berger.de | Page 2

Commercial | Investment

Hamburg 2019/Q1

Selected transactions

2019/Q1

Redevelopment site Großer Burstah | Großer Burstah 3 | City

Plot | Investor: Gator | Purchase price: over €100m

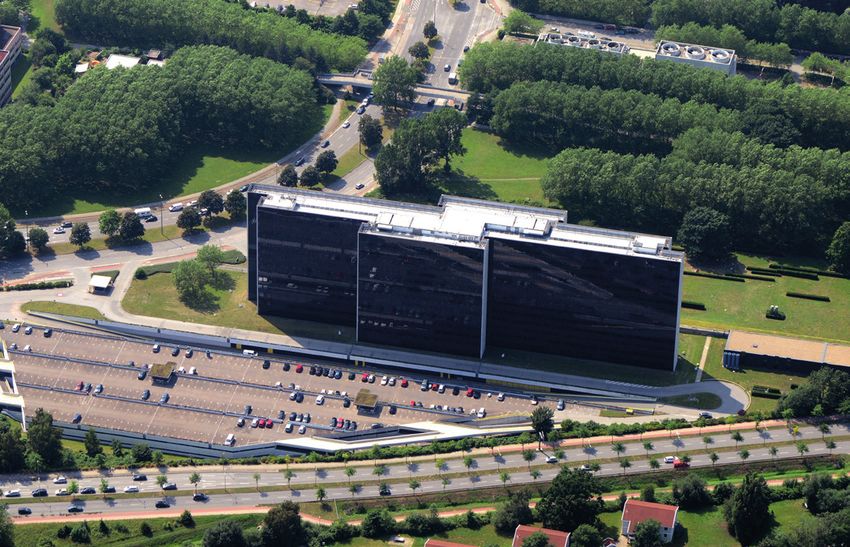

Arne-Jacobsen-Haus | Überseering 12 | City North

Office | Investor: Matrix Immobilien |Purchase price: ca. €60m

Redevelopment site City-Hochhäuser | Klosterwall 6-8 | City

Plot | Investor: Aug. Prien | Purchase price: ca. €60m

Lindner Hotel Am Michel | Neanderstraße 20 | City

Hotel | Investor: Institutional investors | Purchase price: ca. €34m

Office building | Süderstraße 63 | City South

Office | Investor: DEKA Immobilien | Purchase price: over €30m

Arne-Jacobsen-Haus | Office | Überseering 12 | City North

Transaction volume As in previous years, office properties were the biggest-selling

2019/Q1 | in € millions | by size category, accounting for 47% of the volume traded (€219m).

About half of the properties sold in the 1st quarter of 2019

Transaction volume

were office blocks. In addition to the sale of the “Arne-Jacob-

No. of transactions

sen-Haus” that was already mentioned, an especially note-

worthy transaction in this asset class was the office block at

Süderstrasse 63, City South, which Warburg HIH sold to Deka

Immobilien. Completed in 1999, this property changed hands for

over €30m.

As was to be expected, considering the 1st-quarter sales of

the Großer Burstah and Klosterwall development sites, the

second most popular asset class was building land (31% and

11 2 6 1 1 €143m). Comprising 10% of the market, hotels were the third-

13% 8% 44% 13% 22% most-popular asset class. Apart from the sale of the “Lindner

59 38 203 60 100 Hotel Am Michel” (Neanderstrasse 20), which institutional in-

up to up to up to up to over vestors acquired from Lloyd Funds, this result owed much to

10 25 50 100 100 the sale of the “Hotel Heimhude” (Heimhuder Strasse 16) and

Source: Grossmann & Berger GmbH the “Berghotel Hamburg Blick” (Wulmsberg 12). The two last-

named were bought by designer store Stilwerk in order to

further the company’s hospitality business plans. A mixed use

property sold in the Billstedt district lifted this asset class to

Transaction volume fourth place in the asset ranking (6%). Logistics properties,

2019/Q1 | by asset class which accounted for a share of 4% (€18m) came behind in fifth

place. Unlike the prior year retail properties played only a minor

Other 2% role on the market in the first three months of 2019.

Industrial/

logistics 4%

Once more, the City proved to be the busiest sub-market. Some

Mixed use 6% 45% (€205m) of the total volume traded was transacted in this

top-ranking inner city district, followed by City South with a

Hotel 10% share of 16% (€75m) and City North with 13% (€60m). Unchar-

47% Office acteristically, the usually strong HafenCity sub-market posted

no transactions in the 1st quarter of 2019. Several trades took

place in subordinate locations, reflecting the changing strategies

of investors. Buyers are increasingly turning their attention to

Undeveloped

sites 31% non-core locations with development potential. Accounting for

12% of the volume traded (three transactions totalling €54m),

Hamburg East was close behind in fourth place.

Source:

Quelle: Grossmann & Berger GmbH

www.grossmann-berger.de | Page 3

Commercial | Investment

Hamburg 2019/Q1

Prime yields Yields

2015-2019/Q1 | (Net) initial yield | in % Prime yields low but stable

Compared with the prior quarter, prime yields on commercial

5.40 Industrial/logistics properties in Hamburg have stabilized at their low rate, thus

4.90 halting the decline of the previous months. Year on year the

4.60 4.50 4.50 prime yield on logistics properties has recovered from the low

Office point seen in that quarter and is now 4.50%. At the end of the

3.70

first three months of the year, returns on both office properties

3.30

and commercial buildings stood at 2.80%.

3.60 2.90 2.80 2.80

3.30

Commercial buildings 2.90

2.70 2.70 Investors and vendors

2015 2016 2017 2018 2019/Q1 National buyers dominated the market

Source: Grossmann & Berger GmbH National players were especially active on both the buying and

selling sides of the market. Accounting for 85% of vendors and

82% of buyers, German investors were almost alone on the

Transaction volume market for commercial real estate investment in Hamburg.

2019/Q1 | by investor groups Year on year the share of foreign investors in the market fell

a further 9 percentage points to 18%. Developers were the

Other 6% biggest buyers in the 1st quarter; their spend of €265m rep-

Corporates/

resented more than half (58%) of the total volume of trans-

owner-occupiers 3% actions. Fund managers comprised the next biggest group of

Private equity/ buyers (13%) followed by open end property investment funds

opportunity

funds 8% (12%).

Open-end

retail funds 12% Open end property investment funds were behind 24% of the

sales volume (€110m), and thus the biggest group of vendors.

Project

58% developers This result stemmed primarily from the sale of the site at

Großer Burstah, which Commerz Real sold for its Hausinvest

Fondsmanager 13% fund. Owner-occupiers accounted for 21% of the volume traded

(second place), followed in third place by non-listed property

companies with a share of 10%.

Source: Grossmann & Berger GmbH Outlook

Positive mood but shortage of supply

Transaction volume There will still be demand for suitable investment properties in

2019/Q1 | by vendor groups Hamburg in 2019. The favourable market environment, ongoing

low interest rates and the stability of the German economy

are likely to ensure that business remains brisk in the year just

started. However, the year 2019 is not expected to repeat the

exceptional performance of 2018 and experts reckon with a

Open-end

24% retail funds total transaction volume of between €4.0bn and €4.5bn. Prime

Other 28% yields probably bottomed out at the end of 2018. It is to be ex-

pected that yields will now consolidate.

Public

sector 8% Corporates/

owner-

21% occupiers

Project developers 9% Non-listed

10% property

companies

Source: Grossmann & Berger GmbH

www.grossmann-berger.de | Page 4Commercial | Investment

Hamburg 2019/Q1

Skilled consultancy

Services und contacts

From left to right: Sonja Ebert | Anna Martens | Stephan Eckert

What can we do for you? Sonja Ebert | MBA Real Estate Management

An analysis of the property markets is an important part of the Phone: +49 (0)40 / 350 80 2 - 641

wide-ranging consultancy services offered by Grossmann & Mail: s.ebert@grossmann-berger.de

Berger. We would be pleased to be of assistance in your deci-

sion-making process and can draft an offer that is tailored to Stephan Eckert | Urban and Regional Development M. Sc.

your specific requirements. Phone: +49 (0)40 / 350 80 2 - 231

Mail: s.eckert@grossmann-berger.de

Anna Martens | Diplom-Ingenieur Master of Urban Planning

Phone: +49 (0)40 / 350 80 2 - 615

Mail: a.martens@grossmann-berger.de

Glossary

Definitions, investment market

Transaction volume: The transaction volume is the sum of the purchase prices of Photo credits:

Cover: Titel: “Kallmorgen-Tower“, Willy-Brandt-Straße, Page 2: Colonnaden 72 © Jenner Eg-

all commercial property sold in Hamburg during the period under review. The date berts Fotografie, Page 3:“Arne-Jacobsen-Haus“, Überseering 12 © Friedel Luftbilder.

of signing determines when a transaction is included in the statistics. Buy to let

We draw your attention to the fact that all statements made here are non-binding. Most of

investments in residential properties are not included in the transaction volume. the information is based on third-party reports. The sole intention of this market survey is to

Asset class: A property is allocated to an asset class according to the predominant provide general infomation for our clients.

way in which space is used (at least 75%) when the contract is signed. Grossmann & Berger GmbH | Bleichenbrücke 9 (Stadthöfe) | D - 20354 Hamburg

Individual properties and portfolio transactions: An individual property trans- Phone: +49 (0)40 / 350 80 2 - 0 | Fax: +49 (0)40 / 350 80 2 - 36

info@grossmann-berger.de | www.grossmann-berger.de

action means the purchase of a building used for commercial purposes or of a

piece of land for development. Portfolio transactions involve the purchase of at Managing directors: Andreas Rehberg, Holger Michaelis, Lars Seidel, Axel Steinbrinker

Chairman of the supervisory board: Frank Brockmann

least two separate properties in different locations. Registered office Hamburg • Registered at Hamburg no. B 25866

Prime yield: The prime yield is the initial return attainable on a property that has

been let on normal market terms (tenants with good credit ratings), has top quality

structure and fit-out and stands in one of the very best locations. It is stated as the

net initial yield in per cent, i.e. the ratio between the annual rental income less non-

apportionable ancillary costs and the gross purchase price (net purchase price plus

land acquisition tax, notary’s fees and agency commission.)

www.grossmann-berger.de | Page 5You can also read