MNI RBNZ Preview - April 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MNI RBNZ Preview – April 2021

Meeting Date: Wednesday, 14 April

Statement Release Time: 14:00 NZST/03:00 BST

Link To Statement: https://www.rbnz.govt.nz/monetary-policy/official-cash-rate-decisions

CONTENTS

• Page 2-3: MNI POV (Point of View)

• Page 4-6: RBNZ February Monetary Policy Review

• Page 7: RBNZ February Monetary Policy Statement – Key Variables Under The Baseline Scenario

Page 8-11: Sell-Side Analyst Views

• Page 12: MNI Policy Team Insights

1|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB

MNI POV (Point Of View): Bubble, Bubble, Housing Trouble

While the Monetary Policy Committee have a lot to digest, policymakers are set to take a breather and leave

monetary policy settings unchanged. Recent developments have muddied the waters rather than provided any

clear guidance for the RBNZ, which makes the Reserve Bank’s hitherto preferred strategy of keeping all options

open a reasonable choice. There will be no press conference and no updates on economic forecasts, so the most

we can realistically expect on Wednesday are subtle tweaks to the MPC’s language, reflecting the latest housing

market dynamics, mixed economic data, and the launch of the trans-Tasman travel bubble.

New Zealand’s economy unexpectedly contracted in

the final quarter of 2020, missing both market

expectations of a slight uptick and the RBNZ’s forecast

of a flat reading. And high-frequency confidence

gauges have been flashing red light. Both ANZ

Business Confidence and ANZ Consumer Confidence

declined in March (the former extended its fall in April,

per the flash reading), even as NZIER Quarterly

Survey of Business Opinion and quarterly Westpac

Consumer Confidence improved a tad. Meanwhile,

survey data suggested that price pressures are

building up. This mixed bag of data signals is not

enough to nudge the MPC in any specific direction.

Renewed outbreaks of Covid-19 in the community pushed

Auckland into lockdown two times in February alone. Let

this serve as another reminder that the risk of infections

penetrating strict border controls remains. On the bright

side, New Zealand and Australia finally managed to reach

an accord on quarantine-free, two-way travel. The much

awaited trans-Tasman travel bubble will take effect next

week. This is a welcome development, which had not

entered the RBNZ’s equation before – their baseline

scenario assumed that there will be no travel bubbles prior

to 2022.

The NZ dollar pulled back from multi-year highs in the

wake of February MPS. Last month, RBNZ Deputy

Governor Bascand told MNI that continued currency

appreciation could be “challenging in terms of our

objectives,” but the TWI eased off and stabilised just

shy of the RBNZ’s forecast levels. Given the broader

reflationary narrative, the NZD may still rebound toward

and past recent highs, but this is not the most pressing

concern for the RBNZ, especially that commodity

markets remain buoyant.

All eyes are now on the property market after the

government declared war on surging house prices.

Wednesday’s is the first meeting since the government

tweaked the RBNZ’s remit, asking the MPC to take the

housing market into consideration while setting monetary

policy. Subsequently, the government poured another

bucket of cold water on the blazing property market, as PM

Ardern unveiled a suite of measures aimed at curbing

speculation and increasing housing supply.

2|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBAnalysts have warned that measures announced by the government may negatively affect the economic recovery.

Sharon Zollner, a former senior economist with the RBNZ, told MNI last month that they resembled an effective

interest rate hike and may discourage the MPC from changing its dovish monetary policy outlook. Indeed, money

markets reacted by re-pricing the odds of an OCR hike, as wagers on pre-2023 policy normalisation were pared

back. The impact of the government’s new housing policies are yet to be seen. In fact, some economists have

pointed out that steps targeting property investors may lead to rent increases – a suggestion which PM Ardern

promptly brushed away as speculative. Higher rents, in turn, could accelerate inflation, thus bringing rate hikes

closer. When prompted, Finance Minister Robertson pledged to monitor rents and “take action if necessary,” but it

is unclear how far is the government ready to go with intervening in the housing market.

The bottom line is that from the RBNZ’s perspective it might be better to wait and watch the housing market drama

unfold, rather than firmly articulate any prejudgements about the potential consequences of measures delivered to

date. In addition, the economic data have been mixed and while the trans-Tasman travel bubble is encouraging,

snap lockdowns remain a sword of Damocles handing over smooth economic recovery. This MPC are known for

their reluctance to deliver bold policy measures at non-MPS meetings and the most we can expect today are

rhetorical tweaks. No doubt policymakers will debate the mixed bag of latest data signals and the ramifications of

the government’s campaign against surging house prices, but at the end of the day they will likely limit themselves

to reaffirming their commitment to the “least regrets” approach and pledging readiness to use the full policy arsenal

if needed.

3|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBRBNZ February Monetary Policy Review Announcement

The Monetary Policy Committee agreed to maintain the current stimulatory level of monetary settings in order to

meet its consumer price inflation and employment remit. The Committee will keep the Official Cash Rate (OCR) at

0.25 percent, and the Large Scale Asset Purchase (LSAP) Programme of up to $100 billion and the Funding for

Lending Programme (FLP) operation unchanged.

Global economic activity has increased since the November Monetary Policy Statement. However, this lift in activity

has been uneven both between and within countries.

The initiation of global COVID-19 vaccination programmes is positive for future health and economic activity. The

Committee agreed, however, that there remains a significant period before widespread immunity is achieved. In the

meantime, economic uncertainty will remain heightened as international border restrictions continue.

Economic activity in New Zealand picked up over recent months, in line with the easing of health-related social

restrictions. Households and businesses also benefitted from significant fiscal and monetary policy support,

bolstering their cash-flow and spending. International prices for New Zealand’s exports also supported export

incomes, although the New Zealand dollar exchange rate has offset some of this support.

Some temporary factors were currently supporting consumer price inflation and employment. These one-off factors

include higher oil prices, supply disruptions due to trade constraints, the recent suite of supportive fiscal stimulus,

and a spending catch-up following the easing of social restrictions.

The economic outlook ahead remains highly uncertain, determined in large part by any future health-related social

restrictions. This ongoing uncertainty is expected to constrain business investment and household spending

growth. The Committee agreed that inflation and employment would likely remain below its remit targets over the

medium term in the absence of prolonged monetary stimulus.

The Committee agreed to maintain its current stimulatory monetary settings until it is confident that consumer price

inflation will be sustained at the 2 percent per annum target midpoint, and that employment is at or above its

maximum sustainable level. Meeting these requirements will necessitate considerable time and patience.

The Committee agreed that it remains prepared to provide additional monetary stimulus if necessary and noted that

the operational work to enable the OCR to be taken negative if required is now completed.

Summary Record of Meeting

The Committee reviewed recent international and domestic economic developments, and their implications for the

outlook for inflation and employment. Members noted the lift in domestic economic activity, as evident across a

range of indicators including inflation, employment, household spending, GDP, and asset prices.

The Committee discussed the key factors supporting the pickup in economic activity. Household and business

balance sheets have fared considerably better than was anticipated at the start of the pandemic. This is in part due

to the responses of monetary and fiscal policy, but also due to a number of other factors, in particular the

containment of COVID-19 that has enabled ongoing domestic economic activity. People who arrived in New

Zealand during the early stages of the pandemic and subsequently stayed on, are contributing to both housing and

broader demand pressures. New Zealand’s commodity export prices and volumes have also remained robust

despite the global economic slowdown.

The Committee agreed that several of the factors supporting economic activity are likely to prove temporary. Fiscal

policy will continue to support the economy, but its impulse is unlikely to be as strong as last year. In addition,

economic uncertainty persists due to the sustained closure of international borders and the manifestation of new

strains of the virus. These factors continue to weigh on business confidence and investment intentions.

Several members noted the projected increase in headline inflation can also in part be explained by one-off factors,

particularly oil price increases. The Committee agreed that the interaction between the headline, core, and wage

4|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBinflation, and inflation expectations, will be important in determining the sustainability of inflation pressures in the

medium-term.

The Committee noted the labour market has proved more resilient than anticipated at the outset of the pandemic,

although unemployment has risen. The Wage Subsidy scheme played an important role in helping businesses

maintain employment. However, labour market conditions remain uneven across sectors and regions. Those

sectors most reliant on tourism-related business activities continue to lag behind on job opportunities, with this

likely to persist as long as international borders remain closed. Some members noted that labour effort is being

reallocated to other activities and saw the potential for construction activity to remain strong. The Committee

expects to see an ongoing gradual recovery in employment towards its maximum sustainable level.

The Committee noted that although the recovery in economic activity was uneven across countries, the

performance of some of New Zealand’s main trading partners, in particular China, has been more resilient than

expected. The stronger performance of economies geared more towards global goods demand, which has

provided continued support to New Zealand’s commodity exports. However, the gains from higher export

commodity prices have been somewhat offset by the stronger New Zealand dollar.

The Committee noted that the spread of more virulent strains of COVID-19 presents an ongoing risk to global

economic activity. However, the development of effective COVID-19 vaccines has improved the medium-term

economic outlook, helping to reduce uncertainty and boost confidence. Members noted the global economic

recovery remains dependent on health outcomes and the success of the COVID-19 vaccine programmes.

The Committee noted that global financial asset prices have been inflated by both fiscal and monetary policy

stimulus, and the expectations of the success of the vaccine programmes. Members also noted that long-term

sovereign bond yields had increased, in part reflecting greater expected growth and inflation.

The Committee noted that domestic financial conditions remain highly stimulatory, that is, promoting spending and

investing. Since the November Statement, international and domestic long-term interest rates have risen, driven by

an improved growth and inflation outlook.

However, domestic borrowing rates faced by households and businesses have declined marginally. Members

agreed that domestic borrowing costs would need to remain low to achieve the Committee’s objectives.

The Committee discussed the effectiveness of monetary policy settings in delivering the necessary monetary

stimulus. The level of Official Cash Rate (OCR) and forward guidance had helped anchor short-term interest rates.

The Funding for Lending (FLP) programme had helped keep downward pressure on retail interest rates. The

Committee noted that the Large Scale Asset Purchase (LSAP) programme had continued to apply a downward

influence on long-term interest rates and provide bond market liquidity.

Members noted the FLP will continue to lower bank funding costs, even if international wholesale borrowing costs

rise. The Committee noted that the decline in bank funding costs provides banks with scope to further reduce

interest rates for household and businesses. The Committee agreed it expects to see the full pass-through of lower

funding costs to borrowing rates, and it will closely monitor progress.

The Committee discussed how monetary policy settings were affecting financial stability. Members noted that

monetary policy actions had supported financial stability as they have improved the cashflow positions of

households and businesses. The Committee noted that the recent changes to the Bank’s Loan-to-Value Ratio

(LVR) requirements occurred to ensure that financial system soundness is maintained.

Overall, the Committee agreed that the risks to the economic outlook are balanced, in large part due to the

anticipated prolonged period of monetary stimulus. The Committee reflected on the international experience of

central banks following the Global Financial Crisis. The Committee agreed that it was important to be confident

about the sustainability of an economic recovery before reducing monetary stimulus. Some members also reflected

on the extended period of below-target inflation in many countries, including New Zealand, prior to the pandemic.

The Committee agreed that, in line with its least regrets framework, it would not change the stance of monetary

policy until it had confidence that it is sustainably achieving the consumer price inflation and employment

objectives. The Committee expects that gaining this confidence will take considerable time and patience. While

5|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBdoing so, the Committee agreed to look through any temporary factors driving prices as required by the Remit, and

noted that there will be periods during which inflation will be above the 2 percent target midpoint.

The Committee discussed the range and settings of its monetary policy tools. Members noted that the banking

system is operationally ready for negative interest rates. The Committee assessed a negative OCR and the LSAP

programme against its Principles for Alternative Monetary Policy. The Committee agreed that it was prepared to

lower the OCR to provide additional stimulus if required.

The Committee discussed the LSAP programme and noted that many factors influence domestic long-term bond

yields, including expectations for monetary policy, global bond yields, and the economic outlook. The Committee

noted staff advice that reduced government bond issuance was placing less upward pressure on New Zealand

government bond yields, and that domestic bond markets had continued to function well. Members noted that staff

had adjusted purchase volumes since the November Statement, in light of these conditions.

The Committee agreed to continue with the LSAP programme with purchases of up to $100 billion by June 2022.

The Committee also endorsed staff continuing to adjust weekly bond purchases as appropriate, taking into account

market functioning. The Committee agreed that weekly changes in the LSAP do not represent a change in

monetary policy stance.

The Committee agreed that current monetary policy settings were appropriate to achieve its inflation and

employment remit. The Committee agreed it would maintain monetary stimulus until it is confident that consumer

price inflation will be sustained around the 2 percent target midpoint and employment is at or above its maximum

sustainable level. The Committee expects a prolonged period of time to pass before these conditions are met.

On Wednesday 24 February, the Committee reached a consensus to:

• hold the OCR at 0.25 percent;

• maintain the existing LSAP programme of a maximum of $100 billion by June 2022; and

• maintain the existing FLP conditions.

6|Page

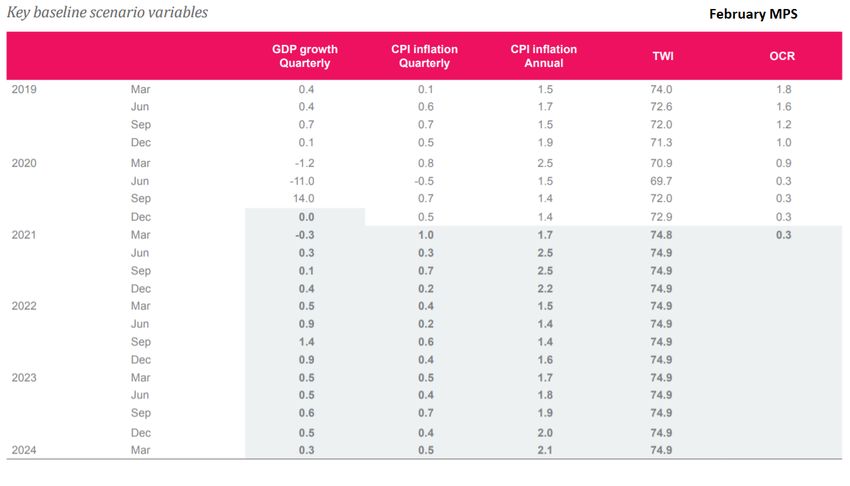

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBRBNZ February Monetary Policy Statement – Key Variables

Under The Baseline Scenario

7|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBSell-Side Analyst Views

ANZ

• The Reserve Bank has its next opportunity to comment on the state of the world on Wednesday next week,

at its OCR Review. There will be no supporting forecasts nor press conference. We expect the RBNZ to

leave the OCR at 0.25% and do not expect any changes to the overall size, duration and general terms of

the FLP and LSAP programmes. The RBNZ is likely to play with a straight bat, reiterating its “wait and see”

and “least regrets” approaches to policy.

• Economic data has started to soften in recent weeks, such as the gentle rolling over in business sentiment,

consumer confidence, retail sales, and a drop in February building consents. The biggest disappointment

was GDP falling 1.0% q/q in Q4, versus RBNZ expectations of 0.0%. But coming off such a huge Q3

bounce, this miss is of less import than normal, and the ‘news’ value of the general data-flow for the RBNZ

is limited, given that its forecasts, like ours, have already built in a softening as unsustainable spending

overshoots fade, fiscal stimulus wanes, and the pain from the closed border mounts. On the other hand,

though, pricing pressures have continued to build both here and overseas. And, inflation expectations in

the ANZ Business Outlook have rebounded to 2.0%, from a low of 1.3% in May 2020.

• The pace (and duration) of LSAP purchases continues to fall as the pace of issuance has slowed, and this

trend is likely to continue. With global yields rising and the worst of the crisis behind us, there is less work

for the LSAP to do from a macroeconomic perspective, and we expect it to have less of an influence on

bond yields and the slope of the yield curve going forward. That speaks to a further gradual reduction in the

pace of purchases, especially if the pace of issuance slows further, which is the risk. However, exiting QE

elegantly isn’t easy. Reducing the pace of LSAP purchases too quickly could slow the pace of growth in

settlement cash (or possibly even drive it lower), which may in turn tighten bank funding conditions and

drive up short-term interest rates, both of which would be unwelcome at this time.

ASB

• It’s been a mixed bag of developments since the RBNZ materially upgraded its economic outlook back in

February. Vaccine roll-outs continue apace in the US and UK, to the point that the global growth outlook is

being uprated. Some of NZ’s key commodity exports are seeing strong price support. NZ is now bubbling

up with Australia, which will enable foreign tourists to enter NZ and inject some cash into those regions that

have borne the brunt of the border closure. NZ has started its vaccination programme, although it is too

early to say when the population will have been vaccinated sufficiently to achieve herd immunity and

enable border controls to be more fully relaxed.

• Some events have created potential headwinds. The Government’s housing policies aimed at reducing

investor housing demand are likely to cool off the housing market – one of the key supports of economic

rebound to date – at a much swifter pace. Although we don’t expect the wider economic impacts to be

large, the changes come with a risk that consumer spending and construction activity will be softer than

otherwise this year. Global long-term interest rates have jumped in recent months in response to a brighter

global outlook, although so far NZ’s key mortgage rates remain unaffected. And, as a reminder that not

everything goes quite as forecast, Q4 GDP was weaker than virtually everyone expected, highlighting that

even our relatively quick economic rebound has its challenges.

• All up, we expect the RBNZ to continue emphasising the economic outlook remains in a muddle, with

plenty of chances still for twists and turns. As per usual, the RBNZ will emphasise that highly

accommodative monetary policy settings will be needed for some time, and that it stands ready to add

support if needed.

• For now, we still expect the RBNZ to remain on hold until August 2022, with the RBNZ to trim the LSAP

programme and to halt purchases altogether before that. Factoring in our estimates of the housing policy

impacts implies a combination of marginally slower economic growth yet marginally faster inflation. But the

housing changes could mean the RBNZ waits longer, particularly if the demand impacts prove to be

stronger than we allow for.

Barclays

• With the RBNZ effectively closing the door to further easing at its February meeting, we expect no change

to policy settings. The bank will likely reiterate that policy will remain accommodative given continuing

uncertainties. However, we think the bank will also emphasise that it is not looking to normalise policy

settings anytime soon. Notably, this will be the first meeting in which the RBNZ will be required to outline

the impact of its decisions on house prices.

8|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBBNZ

• Interest rate markets are not pricing in a full rate hike for New Zealand until 2023. We still think mid-2022 is

more likely and the market currently gives a nod to this with a 50/50 chance of such priced. From our

perspective, we see no reason why the RBNZ would want to shift current market expectations.

Consequently, we think the message it delivered in February, will be largely unchanged when the bank

releases its Monetary Policy Review (MPR) on April 14.

• Some would argue plenty has happened for the RBNZ to adopt a more dovish stance than it did in

February. At the top of the list are the recent housing policy announcements from Government which, it is

judged by many, will dampen house prices. Additionally, Q4 GDP came in miles below the RBNZ’s

February forecast assumption. The RBNZ was at zero change for the quarter but the actual reading was a

much more ugly -1.0%.

• But there is, potentially, just as much to ponder on the flip side of the equation. And, even the housing

announcements can be seen through a different lens. While the announced policy mix might moderate

house price inflation it might also push up rents. Rents are more directly observable in the CPI and could,

in the first instance, result in annual CPI inflation pushing even higher than the 2.5% we are already

forecasting by midyear. In the broader housing component of the CPI, local government rates are also

expected to rise significantly, as are construction costs.

• It should also be noted the upcoming MPR is probably of less interest than the May 5 Financial Stability

Report. That report is likely to enlighten us as to how bothered the RBNZ is about the current level of

house prices in New Zealand and the implications of such for prudential policy. While the Reserve Bank will

not use monetary policy to correct what it will see as essentially a prudential policy issue, the impact that

prudential policy measures have on house prices could well affect future monetary policy decisions. In

short, the more house prices are clobbered by prudential actions, the lesser will be household spending

and GDP which, in turn, will take pressure off the RBNZ to tighten monetary policy.

Citi

• The overall message is likely to be mixed, and we do not expect major direct impact on the markets.

NZDUSD fell below its 100d MA last month, but has declined little further since then. We see near-term

downside to the 100d MA minus 2σ band (around 0.695). A near-term rebound will also be limited at the

100d MA (around 0.715). Even so, this month’s meeting will be the first since the change in the Remit, so

the view of the RBNZ regarding the housing market as outlined in the statement will be important.

ING

• The Reserve Bank of New Zealand's meeting on 14 April should be a rather uneventful one. The policy

message will likely be very similar to the February meeting. Back then, the central bank stressed how the

improvement in global and domestic conditions was not changing the fact that prolonged monetary

stimulus was necessary to sustainably reach inflation (1-3%) and employment goals.

• Since then, the Bank has received only one important data input, which probably endorsed the need to

maintain a dovish tone: GDP unexpectedly dropped 0.9% year-on-year (-1.0% QoQ) in 4Q20, falling short

of central bank expectations of 0.3% YoY growth as was specified in February forecasts.

• However, that isn't enough to suggest that the Bank will step in with even more stimulus than it is currently

providing. Negative rates appear out of the question (if nothing else, because of housing-bubble concerns),

and more quantitative easing seems unlikely considering that total purchases under the Large Scale Asset

Purchase Programme’s (LSAP) are still far from reaching the NZD 100bn ceiling.

• Despite the central bank fiercely defending its independence and its inflation-and-employment remit after

the government asked to consider house prices when setting policy, the size of the housing bubble in New

Zealand has become too large to believe it won't impact monetary policy. Some tax-related government

measures announced at the end of March aimed at curbing surging housing prices are expected to take

some burden off the central bank, and the market has subsequently reacted by scaling back expectations

for policy normalisation in 2021-2022.

Kiwibank

• The RBNZ will almost certainly maintain their on-hold stance and keep policy settings unchanged. There's

simply no need to move the cash rate at this stage. There's no need to cut and it's far too early to hike. The

conditions around the LSAP programme too are unlikely to change. The April MPR is merely a stepping

stone to the more important statement in May.

9|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB• In May, the RBNZ will formally upgrade their forecasts after a soft finish to 2020. The Kiwi economy

contracted by 1% in the final quarter of 2020, compared to the RBNZ's forecast of flat (0%). Since the

RBNZ's February statement, the stream of local data has weakened. Momentum in household spending is

starting to slow, as lockdown savings are bottoming out. Although households are in a far better shape

than we thought possible this time last year. The spending sugar rush that kept the economy afloat is

starting to wane. And the pressures on locked out tourism and education were amplified over the peak

holiday season. The Kiwi economy will likely contract further in Q1, meaning a technical recession. Some

volatility is to be expected. But the Kiwi economy is ultimately on a recovery path.

• In contrast, the global growth outlook has improved markedly. We've gone from counting Covid cases to

counting Covid vaccines. In time, we will move from locking down to opening up. The light at the end of the

tunnel is widening by the day. Stronger global growth is supporting Kiwi export prices, and there's good

news for non-farm sectors. The trans-Tasman travel bubble and an improving US economy are positive

developments. The much-awaited travel bubble will provide much needed foreign cash injection. And

President Biden's stimulus package and speedy vaccine rollout is helping the world's largest economy

recover.

• Already released surveys from ANZ suggested that business sentiment faded a touch over the period. The

impact of our closed border was thrown into sharp relief as many tourist operators struggled, and Auckland

experienced two snap lockdowns. Also weighing on confidence is likely to be weakening profitability. Cost

pressures intensified at the start of the year following rising oil prices, ongoing supply-chain disruption and

snarl-ups at our major ports. Margin pressure is increasing the chance of accelerating inflation. The RBNZ

will be interested to see how pricing intentions respond. And if intentions actually turn into price hikes.

NZIER

• There remains a wide range of views amongst the Shadow Board members on what the Reserve Bank

should do with monetary policy. The focus on the housing market has become more intense in recent

months, and the recent announcements of policy measures to address house price sustainability has

reduced the appetite for tighter monetary policy over the coming year.

• For the upcoming April RBNZ meeting, Shadow Board members are in favour of leaving the monetary

policy stance unchanged. Given the recent announcement of measures such as extending the bright-line

test to 10 years and the removal of interest deductibility for investment properties, Shadow Board members

felt a wait and see approach was appropriate to assess the effects on the New Zealand economy. Beyond

the April meeting, board members were divided over whether to tighten monetary policy, with some

members highlighting the winding down of the Large Scale Asset Purchase Programme (LSAP) and

Funding for Lending Programme (FLP) as the primary means of commencing the tightening of monetary

policy. Some members also considered higher interest rates as appropriate for the coming year.

TD Securities

• Expect all policy settings to be left unchanged with no reason for the Bank to deviate from its message that

"considerable time and patience" will be required to meet its objectives. The Bank will highlight the pick in

global activity/Trans-Tasman bubble reopening, but note the unsteady global vaccine roll out, weaker

domestic data and Government changes to NZ housing policy.

Westpac

• We expect no significant change in the Reserve Bank’s stance at its Monetary Policy Review (MPR) on

Wednesday. (Formerly known as the OCR Review – the name change reflects the fact that the Official

Cash Rate is no longer the only policy tool in play.) The recent news on the domestic economy has been

softer than expected, but this is offset to some degree by a rapidly improving global outlook and growing

concerns about cost and price pressures.

• The confirmation of the trans-Tasman travel bubble is a clear ‘surprise’ for the RBNZ, which had assumed

no border reopening of any kind until 2022. That said, it may not end up having much impact on GDP –

prior to the border closure, net tourism spending between New Zealand and Australia was closer to

balanced. As Kiwis start to head to Australia again, that will come at the expense of those areas that

benefited from diverted spending in 2020, such as home furnishings and renovations.

• The Government’s recent housing policy changes – specifically the removal of interest deductibility for

property investors – are a big deal for the housing market, and will have implications for the outlook for

consumer spending, activity and inflation. The impact is probably less significant for the RBNZ than for us –

10 | P a g e

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBits forecast of house prices in the February MPS was already on the more conservative side, with house

price inflation expected to cool rapidly from the second half of this year.

• In its February Monetary Policy Statement, the RBNZ concluded that “meeting [its inflation and

employment] requirements will necessitate considerable time and patience”. While it didn’t publish a

forward projection for the OCR (and won’t at next week’s review either), the implication was that the OCR

is unlikely to rise from its current level of 0.25% for a long time. And it could go lower – even negative – if

conditions warrant it.

• We expect that message to be more or less repeated this week. This would be broadly neutral for financial

markets – which wouldn’t have been the case prior to the Government’s housing policy announcement last

month, when the local market had started to join the recent global trend towards pricing in rate hikes.

• The RBNZ will also reiterate that it’s prepared to provide additional monetary stimulus if necessary. Any

further easing would most likely be in the form of a negative OCR, and the RBNZ will again emphasise that

it is both willing, and now able, to do so after last year’s preparation work. We see no real scope to expand

the Large-Scale Asset Purchase (LSAP) programme further, and indeed at the current pace of purchases

it’s likely to wind up well short of the $100bn cap.

11 | P a g e

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBMNI Policy Team Insights

MNI STATE OF PLAY: RBNZ Eyes On "Patchy" Recovery

By Lachlan Colquhoun

The Reserve Bank of New Zealand's monetary policy committee meets Wednesday with the economy in a better

place than previously feared and the strength of the housing market a looming concern for policymakers and

legislators alike as house prices rack up year-on-year gains of more than 20%.

Despite the improved outlook for the economy, no change expected to the main policy settings, with the official

cash rate unchanged at the historic low of 0.25% -- where it has sat since March last year. Last month, RBNZ

deputy governor Geoff Bascand told MNI it was too early to remove the accomodative punchbowl.

The bank has previously said it was prepared to cut the OCR to zero or even into negative territory, asking the

banking system to be ready for a possible move. However, the RBNZ recently signaled a potential change of

outlook with an announcement easing the dividend payment restrictions placed on commercial banks at the height

of the COVID-19 disruptions.

Banks are now able to pay 50% of normal dividends to shareholders with restrictions coming off in July.

"The New Zealand economy has rebounded to a stronger position than anticipated at the outset of the Covid-19

pandemic and as such, the complete restriction on dividends is no longer needed," Bascand said recently in

announcing the move.

"Economic activity in New Zealand has picked up over recent months," he added.

At the same time, the RBNZ has also reintroduced loan to value ratios (LVRs) for mortgages in an attempt to de-

risk the booming housing market, which has seen median prices spike 23% over the last 12 months.

--PATCHY

Bascand described the NZ economic recovery as "patchy," suggesting that the central bank will take a cautious

approach before moving away from its dovish approach.

The most recent Monetary Policy Statement, released in February, said that "significant monetary stimulus remains

necessary" to meet the bank's targets of full employment and an inflation rate of between 1% and 3%. Inflation is

currently at 1.4%.

The RBNZ is also mindful that changing policy before any of the other larger central banks will put upward pressure

on the NZD, which has appreciated by just over 15% in the last year to USD70 cents. Some pressure has come off

in the last month after the NZD hit USD74 cents in late February, a trend which the RBNZ will welcome.

The RBNZ also has a program of Quantitative Easing in place, and has said it will buy up to NZD100 billion of NZ

Government bonds and some local government bonds on the secondary market by June 2022.

12 | P a g e

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBYou can also read