Multi-asset market outlook - For professional investors January 2020 - Robeco

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Multi-asset market outlook

For professional investors

January 2020

1

General overview

December: oil was the top performer in 2019 > Clearly, markets have ended 2019 on an optimistic note. Global equities

returned 30% unhedged in euros. In fact, it is quite difficult to find a

major asset class that did not generate a positive return in 2019.

> The strong momentum could well extend into the new year, as the

main the drivers remain in play. These are improving economic growth,

supportive central banks and easing geopolitical concerns on Brexit and

the US-China trade dispute. All of this fits nicely with our base case that

equity markets still haven’t reached their highs for this cycle.

> While we are confident about our base case, 2020 brings some risks.

Some of these are well known, such as the delayed recovery in

earnings, now expected to come in the second quarter. But some of

them are new, like the increase in tension in the Middle East after the

Source: Bloomberg, Robeco

US killed an Iranian general. The short-term impact of this has already

Positions: we are still bullish, only a bit more careful

been felt as risk markets wobbled. The longer-term risk of a further

Portfolio BM Active destabilized Middle East have the potential to change the market

Equities Developed Markets 27.000% 25.0% 2.0%

Equities Emerging Markets 5.000% 5.0% dynamic more profoundly through sustained higher oil prices and, with

Real Estate Equities 5.0% 5.0%

it, higher inflation.

Commodities 5.0% 5.0%

Core Gov Bonds 1-10 20.0% 20.0%

Core Gov Bonds 10+ 7.5% 7.5%

Investment Grade Corp Bonds 20.0% 20.0% > Our overweight in equities is now smaller than it has been over the past

High Yield Corp Bonds 0.0% 5.0% -5.0% 12 months. We intend to increase the equity weighting at better price

Emerging Market Bonds LC 5.0% 5.0%

Cash 5.50% 2.5% 3.0% levels. We continue to hold onto our long-term underweight in high

EUR/USD 1.0% 0.0% 1.0%

EUR/JPY 0.0% 0.0%

yield bonds. Overall, the combination of these positions leaves us

EUR/GBP 0.0% 0.0% somewhat neutral on risky assets. We have also tilted the portfolio

EUR CASH -1.0% 0.0% -1.0%

toward an overweight in euros at the expense of the US dollar.

Source: Robeco

2

Special Topic Economy Equities Fixed Income Commodities & FX

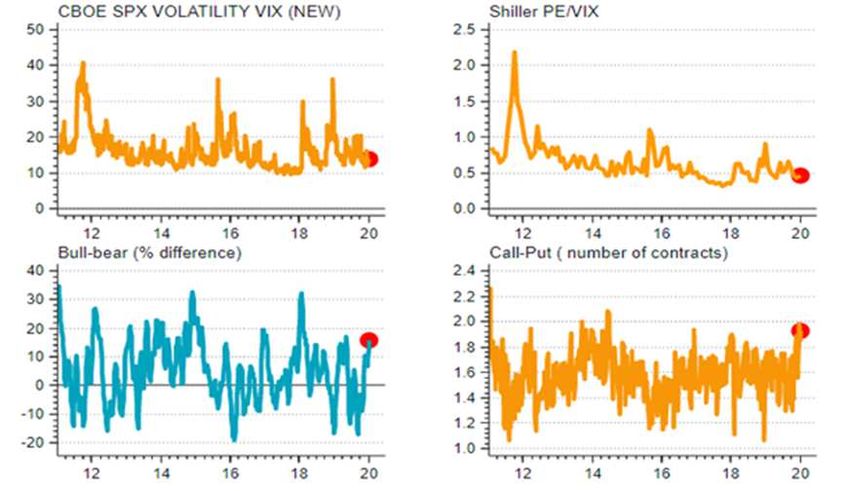

> Theme of the month: Mind the skew – stocks may not yet have peaked (I)

Global equity returns’ historical frequency distribution 1900-2019

> Geopolitical uncertainty has been given new impetus with the killing of

Iranian General Qasem Soleimani, while the prospects of a Phase One

trade deal between the US and China, and a subsequent recovery in the

global manufacturing sector, look fully priced in. But our base case

remains that we haven’t yet seen the highs in the equity market for this

bull run. As we have argued in recent months, we expect a recovery in

earnings around Q2 2020. In the meantime, dovish central banks are

providing support to compensate for a delayed recovery in

fundamentals.

> Another line of reasoning underpins our base case for potential further

Source: Dimson, Marsh and Staunton Database (2017) , Robeco upside for stocks – ‘the skew’. Since 1900, global equities have on

average posted returns of 8%, but the historical return distribution is

Regional ERP is still above long-term averages highly skewed, and large positive return realizations are quite common.

In fact, global equity returns of more than 20% in a calendar year have

occurred 20% of the time since 1900.

> Interestingly, lopsided positive returns tend to cluster. Of those 24 years

with returns in excess of 20%, high returns were generated in

subsequent years. For instance, 1921 (a 27.5% return) was followed by a

27.7% return in 1922, and the 36.1% return seen in 1985 was followed

by a 38.2% return in 1986. Moreover, the years with clustered equity

returns of above 20% had a common feature; the year preceding the

cluster was typically negative for the stock market, with 1927 being the

only exception. For instance, 1920 saw a loss of 26.8%, while 1984 was

a flattish year, falling 0.1%.

Source: Refinitiv Datastream , Robeco

3

Special Topic Economy Equities Fixed Income Commodities & FX

> Theme of the month: Mind the skew – stocks may not yet have peaked (II)

One of the laggards in 2019: the value factor

> Looking at all those periods that had a year with returns below the

historical average followed by a stellar +20% year, we had an average

return in the second year of 14.5%. Given that stocks rose >20% in

2019, and this was preceded by a below historical average return year

in 2018, the 30.0% return for the MSCI World was not exceptional; it is

close to the average recorded since 1900. Moreover, it can’t be ruled

out that 2020 could be another year of returns above the historical

average

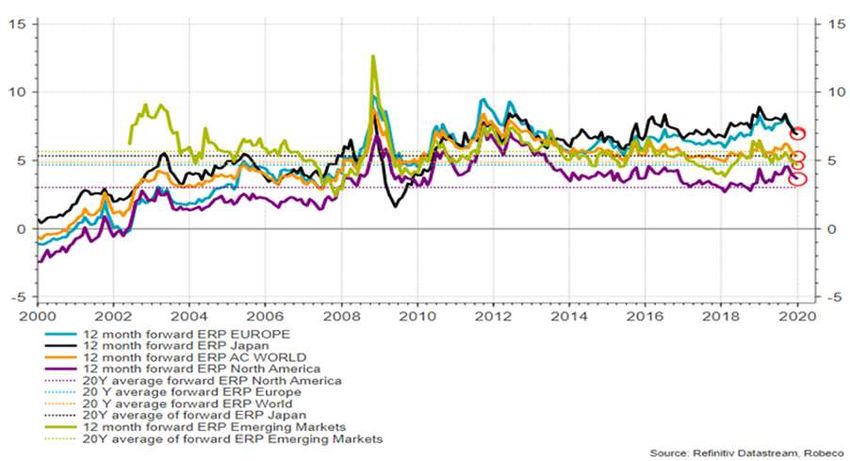

> Also, judging from valuation, fundamentals and sentiment indicators,

equities do have upside risk left. From a relative valuation perspective,

the global equity risk premium is still above historical averages, and the

Source: Refinitiv Datastream , Robeco

case for European and Japanese equities from an equity risk premium

Past capex intentions lead productivity growth perspective is even stronger. From a sentiment angle, US retail investors

and hedge funds have become less bearish, and further capitulation by

the bears could propel equities higher. In addition, there were sectors,

factors and regions that were clearly lagged the global benchmark in

2019, notably equities with a value tilt.

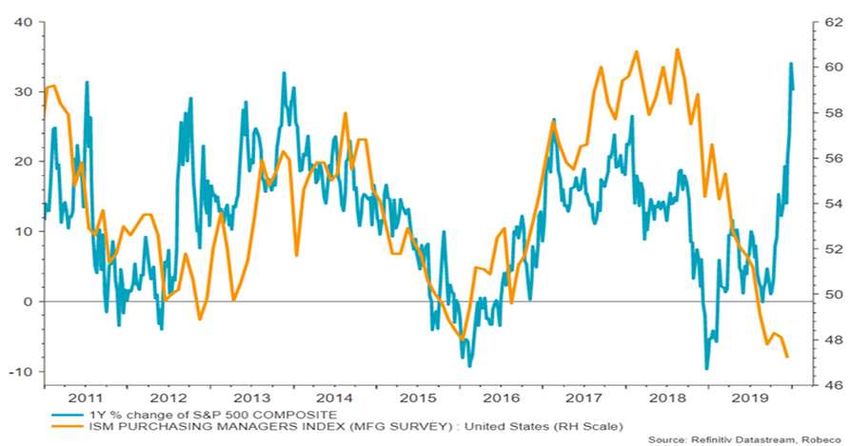

> Risks to our bullish base case scenario are the fact that US equity

markets look richly priced, and geopolitical risk is potentially no longer

ebbing, as we had expected going into 2020. Year-on-year S&P 500

Index returns suggest that the market is priced for a full recovery in the

ISM Manufacturing index to a level of 60. The recent negative surprise

in the index, which dropped back to 47.2, indicating contraction,

already hints that reflation into 2020 is unlikely to be smooth.

Source: Refinitiv Datastream , Robeco

4

Special Topic Economy Equities Fixed Income Commodities & FX

> United States

ISM Manufacturing the tentative recovery is already being challenged > We think that the Fed is on hold for the foreseeable future. The rate cuts

in July, September and October were ‘insurance cuts’, and their impact

will be monitored carefully in the coming period. The current policy

setting can be seen as accommodative, but as concerns remain about

inflation and inflation expectations, this is seen as the correct path

given the economic environment. For the Fed to change its view would

require a “material reassessment” of economic conditions.

> The ISM manufacturing index remains below 50, so it is still

contracting, while the latest number slipped below the previous

reading. Another daunting fact is that the monthly reading hasn’t been

this low since 2009, so the stabilization of manufacturing that had just

Source: Bloomberg, Robeco started to set in is already being challenged. The bright spot continues

The National Home Price Index is bottoming out to be the consumer. Employment growth and steady gains in average

hourly earning should support disposable income. High net worth, low

debt service costs and a relatively high level of saving all paint a picture

of a healthy consumer. We expect the housing market to remain firm as

the consumer’s balance sheet remain in good shape, and affordability is

maintained due to low mortgages rates.

> The bipartisan budget act of 2019 also ensures that government

spending and investment will remain at a healthy clip, and be

supportive for growth. All in all, we expect the US to grow by around 2%

this year – not spectacular, but still a decent growth rate.

Source: Bloomberg, Robeco

5

Special Topic Economy Equities Fixed Income Commodities & FX

> Europe

Eurozone growth likely to weaken somewhat in Q1 2020 > Although some leading indicators such as M1 money growth (8% y-o-y)

and the German IFO suggest that the downturn in Eurozone economic

growth may be bottoming out, the pace of growth remains slow and

fragile, as the preliminary November PMI surveys show. Moreover,

underlying Eurozone inflation still lingers at around 1%, well below the

ECB’s current medium-term inflation target of “below but close to 2%”.

Nevertheless, Eurozone core inflation has rebounded to 1.3% for the

first time since April 2017.

> New ECB President Christine Lagarde has been stressing the need for a

prolonged phase of highly accommodative monetary policy, while

underlining that the ECB stands “ready to adjust all of its instruments,

Source: Refinitiv Datastream , Robeco as appropriate” – hence retaining an easing bias. While acknowledging

Tight Eurozone labor market suggests further wage growth into 2020 there were “some signs of economic stabilization”, she affirmed that

the Governing Council continues to expect that it will keep policy rates

at “present or lower levels” until it sees the inflation outlook

convincingly converge to the target.

> In other words: the ECB could still cut rates further, even as concerns

about the negative side effects of the negative rate policy – of which the

central bank was “very aware”, according to Lagarde –prompted

Sweden’s Riksbank to hike rates back to zero on 19 December.

Meanwhile, net asset purchases, which restarted on 1 November and

amount to EUR 20 bln per month, are still expected to run “for as long

as necessary, and to end shortly before” the ECB starts raising rates.

Source: Refinitiv Datastream , Robeco

6

Special Topic Economy Equities Fixed Income Commodities & FX

> Japan

Japanese industrial production: no recovery yet > Our view is that the Bank of Japan (BoJ) is firmly on hold. This contrasts

with the market consensus, which expects further easing. These

expectations are legitimate, as they are in line with the BoJ’s long-

standing position that pre-emptive moves are necessary as long as the

inflation target is not met. However, there have been some indications

by the central bank lately that monetary policy may have reached the

end of its effectiveness, as positives are outweighed by negative effects.

This means fiscal policy seems to be a better instrument for reaching

growth and inflation targets. Not that we think the door is completely

closed for further monetary policy support; it is just that the barrier for

this is much higher. A trigger to prompt the BoJ into action could be

external risks, such as a massive appreciation of the yen.

Source: Bloomberg, Robeco

Inflation remains far below target > The damage by the VAT hike to consumer disposable income and

growth will only slowly be undone. A main driver for the recovery will be

fiscal stimulus. The JPY 26 trn economic package should start to have

an impact in the second quarter. This package, the first in three years,

aims to spark consumer spending and bolster infrastructure. It is

coming at a time that manufacturing is starting to show signs of

stabilization. This, in combination with the upcoming Tokyo Olympic

Games, should temporarily boost growth towards potential in 2020.

> The inflation index excluding both energy and fresh food – the gauge

preferred by the BoJ –came in at 0.8% y-o-y and remains far below the

target of 2.0%.

Source: Bloomberg, Robeco

7

Special Topic Economy Equities Fixed Income Commodities & FX

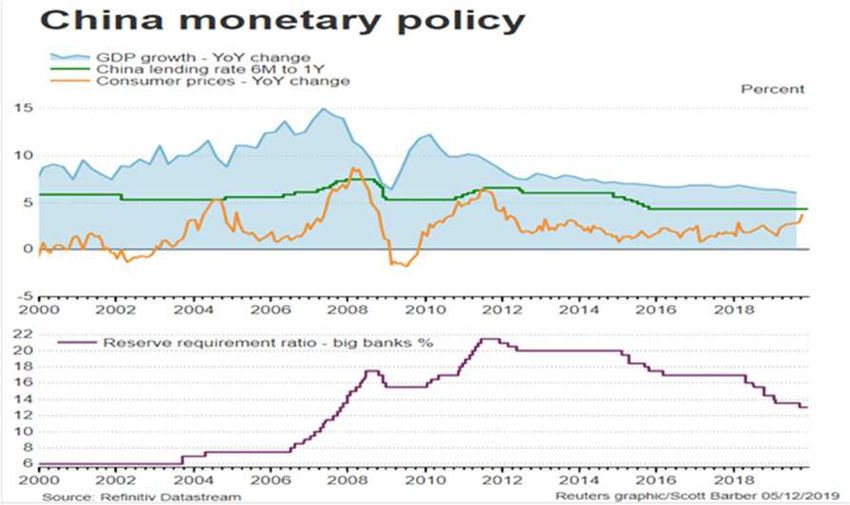

> China

Manufacturing profit slump portrays weak corporate pricing power > China is grappling with weaker domestic and global economic demand,

as trade tensions with the US remain unresolved. This is reflected in

weak corporate profitability and weakening pricing power. China’s

National Bureau of Statistics revealed that industrial profits declined

9.9% (y-o-y). However, the services sector, which accounts for more

than half of China’s output, is showing recovery and expanding. The

Caixin services PMI increased to 53.3 in November, up from 51.1 .

> Negotiations between China and the US to achieve a ‘Phase 1 deal’ are

ongoing, but are cumbersome. President Trump tweeted that the highly

anticipated trade deal could be delayed “until after the election” due to

take place in November 2020. New US legislation on the pro-

democracy protests in Hong Kong and the detention of Moslem Uighurs

No RRR cuts last month, but a MLF cut in Xinjiang province have further ruffled the ongoing negotiations.

> China’s monetary stimulus to counter domestic weakness has been

rather piecemeal. The central bank delivered its first policy rate cut since

2016 by reducing the 1-year MLF and 7-day reverse repo rate by 5 bps

last month. Obviously, the pace of rate easing has lagged that of many

other central banks. Chinese authorities seem to now have a higher

tolerance for slower economic growth than in the past, given the focus

on deleveraging and de-risking of their financial system, especially in

the context of the pork price-induced rise in consumer price inflation to

3.8% in October (note that core CPI inflation remains subdued at 1.5%).

8

Special Topic Economy Equities Fixed Income Commodities & FX

> Equities (I)

Global developed equities: 2019 performance > 2019 was a year that delivered stellar returns for long-only equity

investors. The MSCI World index delivered a total return of 28.4%, at

the top of the range of the past 10 years. It has been a bull market in

everything, as even lagging segments of the market generated returns

in excess of 20%. The MSCI World Value Index, for example, still

returned 21.7%. With global earnings growth flattish on an annual

basis, investors focused on companies that were able to maintain

earnings momentum and largely escape margin compression,

especially corporates with high and stable cashflows represented by the

quality factor. The MSCI Quality Index (in USD) generated 36.1%.

> Trailing EPS decelerated from 17% in early 2019 to become slightly

negative by the end of December (-0.6%). With earnings on a

Trailing EPS for US stocks have been trending down in 2019 downtrend, led by margin compression, multiple expansion delivered

the bulk of returns. A steady downtrend in global margin compression,

notably in the US, is a phenomenon often observed in late cycle, pre-

recession environments. This has been caused by rising unit labor costs.

US wage growth has been accelerating above 3%, while productivity

growth has remained below trend at 1.5%. The latest NFIB surveys

suggest that small and medium-sized US corporates are expecting a

softening of wage pressures in the near term. However, given the

historical tight labor markets around the world, rising wage pressures

are challenging for margins going into 2020. As household financial

balances are healthy, given strong deleveraging over the past decade

(especially in the US), real income rises and house price appreciation,

sales growth is expected to bottom out and contribute to a rebound in

earnings growth as early as Q2 2020.

9

Special Topic Economy Equities Fixed Income Commodities & FX

> Equities (II)

Sales growth: tentative signs of stabilization from ISM new orders > Our base case remains that we haven’t yet seen the highs in the equity

market for this bull run. As we have argued in recent months, we expect

a recovery in earnings around Q2 2020. In the meantime, dovish

central banks are providing support to compensate for a delayed

recovery in fundamentals. Bull markets typically die because of

euphoria that is eventually stymied by central bank overtightening.

While we see pockets of exuberance, central banks appear unwilling to

take the proverbial punchbowl away. Only a few participants in the

recent Fed meetings showed concern that keeping rates low over too

long a period might encourage excessive risk-taking.

> Moreover, the appetite to hike policy rates in advanced economies

Source: Refinitiv Datastream , Robeco seems low, given still subdued levels of inflation and concerns about

Sentiment has turned more bullish, is not flashing a contrarian signal yet weakness abroad. The risk for equity markets is that higher wage

pressures and de-globalization cause inflation in the second half of

2020, leaving markets guessing whether central banks will be forced to

make a hawkish shift in monetary policy. However, inflation risk is not

likely to reverse the rising tide for risky assets just yet.

> There are a couple of near-term risks; Iran-US relations and the

observation that the expected rebound in manufacturing already seems

to be fully priced in. Nevertheless, relative equity valuations (especially

in Japan and Europe) and potential bear capitulation after a stellar

2019 that has seen consistent retail outflows are factors that keep us

overweight equities in the near term. Equity segments that have lagged

in the bull run so far could be favored if global activity accelerates.

Source: Refinitiv Datastream , Robeco

10Special Topic Economy Equities Fixed Income Commodities & FX

> Developed Market Equities

Developed equity momentum remained in positive territory > 2019 proved to be a stellar year for developed market equities, with

returns well in excess of 20%. Markets ended the year on a high note,

as synchronized central bank easing and an agreement between US and

China on trade allowed them to shift into a higher gear.

> Developed equity short momentum remained positive in December.

Monthly momentum of equity returns in local currency showed that

S&P 500 stocks gained another 3.7%. European Stoxx600 equities

generated 3.7% in local currency. Returns in Japan retraced a bit

towards the end of the year, with the Nikkei 225 equity index up 0.5%

in December. The long momentum signal (12M-1M) in local currency of

the Eurostoxx has been very positive, now at 18.7%, while the signal for

Source: Refinitiv Datastream , Robeco the US market is even stronger at 24.2%. Japanese equities’ long

Equity multiples have risen over the year momentum is still lagging other developed regions, but has been

improving, generating a +17.5% return on the 12M-1M metric.

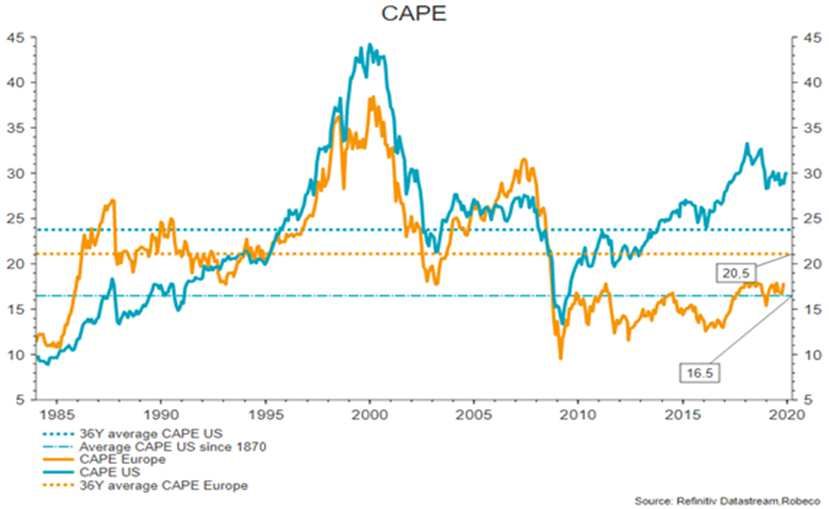

> Equity valuations on a CAPE basis have been trending up after the

market rout of Q4 2018. Multiple expansion accounted for a solid chunk

of total equity returns last year. While markets priced in a truce

between the US and China and reflation in early 2020, trailing earnings

have became more flattish. The US Shiller CAPE at December 2019 was

30.0, which is 40% above the 40-year moving average. Multiple

expansion in Europe on a CAPE basis has been somewhat stronger,

albeit from lower absolute levels. We continue to favor Europe (and

Japan) over the US in our regional equity allocation.

Source: Refinitiv Datastream , Robeco

11Special Topic Economy Equities Fixed Income Commodities & FX

> Equities: Emerging vs. Developed

Emerging market equities: 2019 performance

> Emerging market equities (in euros) realized a return of 20.6% in 2019.

While this is significantly higher than the average annual return during

the last 10 years, emerging equities trailed developed market equities

by almost 10%. Slower GDP growth in China, the US-China trade war

and relatively poor earnings quality contributed to the

underperformance. This is what made us hesitant to implement a truly

outspoken overweight in emerging markets throughout the year.

> However, if our base case scenario of no US recession and gradual

improvement in global GDP growth pans out, the outlook for emerging

equities looks relatively attractive. A turning point in growth

momentum has historically benefited EM stocks. We expect this to be

Source: Bloomberg & Robeco

the same this time, especially since emerging economies themselves

Emerging versus developed markets: Valuation are the main cause of the turning point. Earnings revisions will likely

improve, quickly unlocking some of the relatively attractive valuation.

> This reasoning is mainly focused on emerging market equities versus US

stocks. Compared to other regions, which also profit from faster global

growth, we expect the differences to be small in the near term. It’s

mainly the shift from the US to the rest of the world where we see the

divergence in performance happening.

> We start 2020 with a small overweight in emerging market equities.

Source: Refinitiv Datastream, Robeco

12Special Topic Economy Equities Fixed Income Commodities & FX

> AAA Bonds (I)

10-year German yields: 2019 performance > When one looks at the meandering of German 10-year rates in 2019, it

Basis points is pretty clear that the pattern is generally in line with the 10-year

average, but that the basis point moves were much larger. Up until the

third quarter, the 10-year moved lower in line with the average.

However, in the fourth quarter, German 10-year rates started to diverge

and start rising again. This ascent regained more then half of the

ground that was lost during the first quarters of the year.

> While the increase in the fourth quarter might be seen as atypical when

compared to the average, it lines up perfectly with the way economic

data developed through out the year. For a great part of 2019, the

patience of market participants was tested, as economic numbers came

Source: Bloomberg & Robeco

in softer globally, and particularly in the Eurozone. Given the increase in

Economic surprises: slowly coming to grips with reality geopolitical uncertainty, and the eroding benefits of the 2018 tax cuts in

the US, some softening was to be expected. However, the persistency of

the slowdown was a surprise.

> The economic surprise index conveys a picture of continued adjustment

of economic expectations throughout the first quarters of the year. In

the third quarter, expectations finally seem to have caught up with

reality and started to overshoot downwards. This created an

environment of improving surprises, and triggered the turnaround in

German 10-years. While almost all G-10 rates followed the pattern of

weakening in the first quarters of the year, and than a stabilization in

the third quarter, the gyrations in German 10-years were exceptional

Source : Bloomberg & Robeco compared to their peers.

13Special Topic Economy Equities Fixed Income Commodities & FX

> AAA Bonds (II)

Global Economic Polity Uncertainty Index remained high during 2019 > This illustrates the sensitivity of Europe, and Germany in particular, to

disturbances caused by the US-China trade dispute. So, what do we

expect for 2020? Over the past months we have been consistent in our

view that the economic weakness we witnessed was excessive. Just

like everyone else, however, we were surprised at how long the

softness – particularly in manufacturing – remained in place. Our

expectation is that the tentative signs of stabilization that we are

finally starting to witness will take hold further.

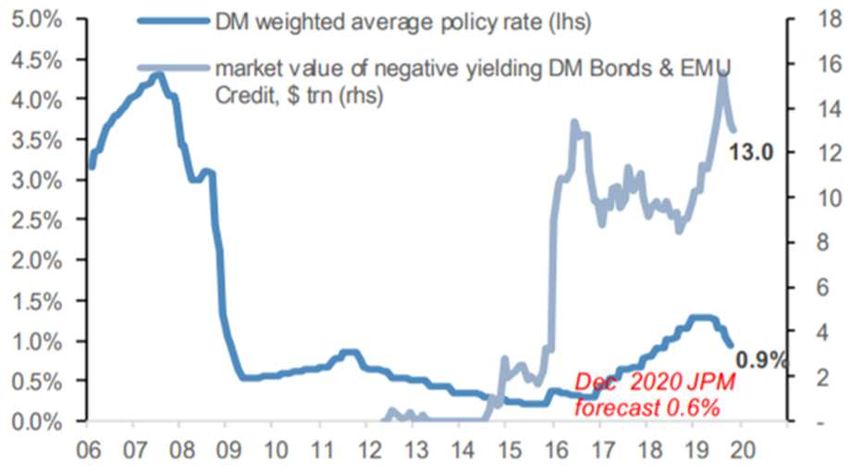

> While we are optimistic about economic prospects, we are aware that

in the near future, this will probably have no impact on central bank

policy. The soft patches we witnessed over the past period has led the

Source: Bloomberg & Robeco

majority of central banks down a path they will not deviate from easily.

Developed market central banks are back in easing mode So, we expect the current easy financial conditions to remain in place

for the coming year. Only an exceptional flare-up of inflation might

change this view, but this is highly unlikely.

> With the barrier for central banks to raise rates higher than it is for

them to ease, our assumption is that it will be difficult for yields to fully

withstand this gravitational pull lower. We do, however, think it is

highly unlikely that yields will move to new lows, and we have a bias

for rates to move higher.

> We continue to prefer a neutral to slightly underweight position in

government bonds.

Source: Source: J.P.Morgan

14Special Topic Economy Equities Fixed Income Commodities & FX

> Investment Grade Credits

Euro investment grade credits: 2019 performance > Euro investment grade credits realized a generous return of 6.2% during

the whole of 2019. As the chart on the top left shows, this was

considerably higher than the average return of the last 10 years.

Contributors to returns included the global fall in bond yields as a result

of a strong accommodative turn in central bank policy, combined with

continuous low spreads due to slowing but positive and stable growth.

> Low yields and low spreads. This characterizes the starting point for

investment grade credits into 2020. Yet, we are neutral. In our base

case scenario of gradual improvement in global growth, credit spreads

can stay tight for longer and default risk remains low. In this scenario,

investors will likely look past the rise in company leverage.

Source: Bloomberg, Robeco

Spread: no big regional divergence > In case of any adverse market circumstances, bond yields have room to

fall in the US, the biggest part of the investment grade universe. In

Europe, the ECB remains a strong tailwind for credits. From this

perspective, investment grade credits look significantly more attractive

than global high yield bonds.

> We are neutral on investment grade credits, with a small preference for

Eurozone credits relative to US credits, because of hedging costs (still

relatively high) and the ECB maintaining its role as a marginal buyer for

the foreseeable future.

Source: Bloomberg, Robeco

15Special Topic Economy Equities Fixed Income Commodities & FX

> High Yield

> Global high yield bonds (hedged to euros) realized an impressive result

Global high yield: 2019 performance

of almost 10% in 2019. This is 3.5% above the average annual return

over the last 10 years. On average, the global high yield spread fell by

120 basis points, and most of the spread compression was realized in

the first quarter of this year. The significant drop in global bond yields

combined with the fact that defaults were low on average (even though

they rose in the US in the latter part of the year) resulted in a a very

solid return for the asset class. We held a overweight in equities against

our underweight in high yield almost throughout the year, and equities

realized a return triple the size that of high yield, so the underweight

contributed positively to the overall portfolio result.

Source: Robeco & Bloomberg

> We remain uninspired by the outlook for global high yield bonds in a

High yield: defaults are low in Europe, higher in the US multi-asset portfolio. With the recent mini-rally, valuations look even

more stretched. Yields as well as spreads are low. The dispersion

between cheaper CCCs but very rich BBs is a negative. If the market

cycle turns, there is virtually no place to hide, except for those bonds

that have the highest default risk. Given that the rise in company

leverage could qualify as the sole bubble of this economic expansion,

we expect that cracks should appear in lower-graded bonds first.

> For European high yield bonds, we expect some protection via the ECB,

which will buy investment grade credits for the foreseeable future. This

is pushing some investors higher up the risk scale as returns are likely to

be low. We retain a significant underweight in global high yield bonds.

Source: BofA Merrill Lynch & Bloomberg

16Special Topic Economy Equities Fixed Income Commodities & FX

> Emerging Market Debt

Emerging market debt in local currency: 2019 performance > Local currency emerging market bonds realized a stellar return of 11.7%

in 2019. As the chart on the top left shows, this was significantly higher

that the average emerging market debt return during the last 10 years.

The asset class also beat high yield bonds. Lower bond yields around the

globe as a result of renewed central bank easing, combined with low

emerging market inflation, the continuous search for yield and bullish

sentiment towards risky assets, all contributed to the return. The returns

do though mask a number of idiosyncratic events surrounding countries

such as Argentina, South Africa and Turkey.

> Compared to other fixed income asset classes, the outlook for local

currency emerging market debt is relatively upbeat. Contrary to

Source: Bloomberg, Robeco

developed market government bonds, yields have room to drop further

Emerging market currencies against the euro in the near term, as inflation levels in emerging economies fall as well.

> In addition, we see some value in emerging market currencies, which

should be a small tailwind going forward. This is especially the case in

the event of a durable trade deal between the US and China, which

reduces the pressure on the Chinese yuan.

> Idiosyncratic risk will impact the performance of the overall asset class

from to time, but apart from some smaller usual suspects, we believe

an improvement in the global economic cycle will continue to make

investors more forgiving in their search for yield.

Source: Thomson Reuters Datastream, Robeco

> We have a neutral weight in emerging debt in the multi-asset portfolio.

17Special Topic Economy Equities Fixed Income Commodities & FX

> FX (I)

EUR/USD: 2019 performance > 2019 was a relatively low-volatility year for currency markets. The

EUR/USD remained within the relatively tight 1.09 and 1.1550 range.

The pair reached its high in the first month of the year, and from

thereon, it was a continued slide lower. An inflection point was reached

in the third quarter, when the Fed had sufficient room to continue to cut

rates while the ECB had few-to-no options left to provide further easing.

This divergence in policy flexibility put a floor under the euro.

> 2019 was a tough year for the single currency. Within G-10, it only

managed to appreciate against the Swedish currency, which is known

for its cyclical characteristics. Given the weakness we have seen in

manufacturing and exports, it is no surprise that the krona was under

Source: Bloomberg, Robeco

pressure.

It was a tough year for the EUR

> If a currency loses ground against such a wide range of currencies, then

it is pretty clear that the weakness is most probably driven by local

characteristics. So, why did the euro do so badly? First of all, it

continued to be the currency with the lowest yield within G-10. And

when compared to other low-yielding currencies like the Swiss franc and

the Japanese yen, it lacks their safe haven credentials. The euro also

isn’t a commodity currency and doesn’t benefit from rising oil prices like

the Norwegian krona and the Canadian dollar. On top of that, the two

main geopolitical risks of 2019 affected the Eurozone disproportionally.

Source :NWM, IMF, Haver

18Special Topic Economy Equities Fixed Income Commodities & FX

> FX (II)

Manufacturing ISM: the manufacturing recovery remains fragile > So, in 2019 the odds were stacked pretty heavily against the euro. For

2020, however, things are starting to look a bit better. Firstly, the two

major geopolitical risks that weighed on the euro have eased, at least in

the near term. Secondly, we don’t see the Fed hiking rates anytime

soon, and the ECB has already shown its hand, somewhat neutralizing

the rate disadvantage. We also expect the recovery of the global

economy to continue, and think that this will be beneficial for the euro.

> Sterling was one of the strongest currency within the G-10 in 2019. The

British pound took a hit shortly after Boris Johnson was elected to lead

the UK’s ruling Conservative Party, but pressure on sterling abated as it

became clear that new elections were to be held. The Conservatives’

Source: NWM, IMF, Haver

eventual victory in those elections gives them a clear mandate. The

Sterling: one of the strongest currencies in the G-10 market sees this as positive, as they expect Johnson will move more

towards the center. It currently feels that the market has fully priced in

this optimistic scenario. So far, however, there is no clear indication

that Johnson is indeed stepping away from a hard Brexit. We think that

this will ultimately start to weigh on sterling.

> We continue to think that the US dollar will weaken in 2020, as it will

have to do without any rate support this year. If we are correct that the

global economy will indeed strengthen further, we think other

currencies like the euro will start to catch up. A risk to this view is an

increase in geopolitical tension in the Middle East. We currently have a

small EUR overweight against the USD.

Source: Bloomberg, Robeco

19Important information

Robeco Institutional Asset Management B.V. has a license as manager of Undertakings for Collective Investment in Transferable Securities (UCITS) and Alternative Investment Funds (AIFs) (“Fund(s)”)

from The Netherlands Authority for the Financial Markets in Amsterdam. This document is solely intended for professional investors, defined as investors qualifying as professional clients, have

requested to be treated as professional clients or are authorized to receive such information under any applicable laws. Robeco Institutional Asset Management B.V and/or its related, affiliated and

subsidiary companies, (“Robeco”), will not be liable for any damages arising out of the use of this document. Users of this information who provide investment services in the European Union have

their own responsibility to assess whether they are allowed to receive the information in accordance with MiFID II regulations. To the extent this information qualifies as a reasonable and appropriate

minor non-monetary benefit under MiFID II, users that provide investment services in the European Union are responsible to comply with applicable recordkeeping and disclosure requirements. The

content of this document is based upon sources of information believed to be reliable and comes without warranties of any kind. Without further explanation this document cannot be considered

complete. Any opinions, estimates or forecasts may be changed at any time without prior warning. If in doubt, please seek independent advice. It is intended to provide the professional investor with

general information on Robeco’s specific capabilities, but has not been prepared by Robeco as investment research and does not constitute an investment recommendation or advice to buy or sell

certain securities or investment products and/or to adopt any investment strategy and/or legal, accounting or tax advice. All rights relating to the information in this document are and will remain the

property of Robeco. This material may not be copied or used with the public. No part of this document may be reproduced, or published in any form or by any means without Robeco's prior written

permission. Investment involves risks. Before investing, please note the initial capital is not guaranteed. Investors should ensure that they fully understand the risk associated with any Robeco product

or service offered in their country of domicile (“Funds”). Investors should also consider their own investment objective and risk tolerance level. Historical returns are provided for illustrative purposes

only. The price of units may go down as well as up and the past performance is not indicative of future performance. If the currency in which the past performance is displayed differs from the currency

of the country in which you reside, then you should be aware that due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local currency. The

performance data do not take account of the commissions and costs incurred on trading securities in client portfolios or on the issue and redemption of units. Unless otherwise stated, the prices used

for the performance figures of the Luxembourg-based Funds are the end-of-month transaction prices net of fees up to 4 August 2010. From 4 August 2010, the transaction prices net of fees will be

those of the first business day of the month. Return figures versus the benchmark show the investment management result before management and/or performance fees; the Fund returns are with

dividends reinvested and based on net asset values with prices and exchange rates of the valuation moment of the benchmark. Please refer to the prospectus of the Funds for further details.

Performance is quoted net of investment management fees. The ongoing charges mentioned in this document are the ones stated in the Fund's latest annual report at closing date of the last calendar

year. This document is not directed to, or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such

distribution, document, availability or use would be contrary to law or regulation or which would subject any Fund or Robeco Institutional Asset Management B.V. to any registration or licensing

requirement within such jurisdiction. Any decision to subscribe for interests in a Fund offered in a particular jurisdiction must be made solely on the basis of information contained in the prospectus,

which information may be different from the information contained in this document. Prospective applicants for shares should inform themselves as to legal requirements also applying and any

applicable exchange control regulations and applicable taxes in the countries of their respective citizenship, residence or domicile. The Fund information, if any, contained in this document is qualified

in its entirety by reference to the prospectus, and this document should, at all times, be read in conjunction with the prospectus. Detailed information on the Fund and associated risks is contained in

the prospectus. The prospectus and the Key Investor Information Document for the Robeco Funds can all be obtained free of charge at www.robeco.com.

Additional Information for US investors

Neither Robeco Institutional Asset Management B.V. nor the Robeco Capital Growth Funds have been registered under the United States Federal Securities Laws, including the Investment Company Act

of 1940, as amended, the United States Securities Act of 1933, as amended, or the Investment Advisers Act of 1940. No Fund shares may be offered or sold, directly or indirectly, in the United States or

to any US Person. A US Person is defined as (a) any individual who is a citizen or resident of the United States for federal income tax purposes; (b) a corporation, partnership or other entity created or

organized under the laws of or existing in the United States; (c) an estate or trust the income of which is subject to United States federal income tax regardless of whether such income is effectively

connected with a United States trade or business. Robeco Institutional Asset Management US Inc. (“RIAM US”), an Investment Adviser registered with the Securities and Exchange Commission under

the Investment Advisers Act of 1940, is a wholly owned subsidiary of ORIX Corporation Europe N.V. and offers investment advisory services to institutional clients in the US. In connection with these

advisory services, RIAM US will utilize shared personnel of its affiliates, Robeco Nederland B.V. and Robeco Institutional Asset Management B.V., for the provision of investment, research, operational

and administrative services.

Additional Information for investors with residence or seat in Australia and New Zealand

This document is distributed in Australia by Robeco Hong Kong Limited (ARBN 156 512 659) (“Robeco”), which is exempt from the requirement to hold an Australian financial services license under the

Corporations Act 2001 (Cth) pursuant to ASIC Class Order 03/1103. Robeco is regulated by the Securities and Futures Commission under the laws of Hong Kong and those laws may differ from

Australian laws. This document is distributed only to “wholesale clients” as that term is defined under the Corporations Act 2001 (Cth). This document is not for distribution or dissemination, directly or

indirectly, to any other class of persons. In New Zealand, this document is only available to wholesale investors within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act

2013 (‘FMCA’). This document is not for public distribution in Australia and New Zealand.

Additional Information for investors with residence or seat in Austria

This information is solely intended for professional investors or eligible counterparties in the meaning of the Austrian Securities Oversight Act.

20Additional Information for investors with residence or seat in Brazil

The Fund may not be offered or sold to the public in Brazil. Accordingly, the Fund has not been nor will be registered with the Brazilian Securities Commission – CVM, nor has it been submitted to the

foregoing agency for approval. Documents relating to the Fund, as well as the information contained therein, may not be supplied to the public in Brazil, as the offering of the Fund is not a public

offering of securities in Brazil, nor may they be used in connection with any offer for subscription or sale of securities to the public in Brazil.

Additional Information for investors with residence or seat in Canada

No securities commission or similar authority in Canada has reviewed or in any way passed upon this document or the merits of the securities described herein, and any representation to the contrary is

an offence. Robeco Institutional Asset Management B.V. is relying on the international dealer and international adviser exemption in Quebec and has appointed McCarthy Tétrault LLP as its agent for

service in Quebec.

Additional Information for investors with residence or seat in Colombia

This document does not constitute a public offer in the Republic of Colombia. The offer of the Fund is addressed to less than one hundred specifically identified investors. The Fund may not be promoted

or marketed in Colombia or to Colombian residents, unless such promotion and marketing is made in compliance with Decree 2555 of 2010 and other applicable rules and regulations related to the

promotion of foreign Funds in Colombia.

Additional Information for investors with residence or seat in the Dubai International Financial Centre (DIFC), United Arab Emirates

This material is being distributed by Robeco Institutional Asset Management B.V. (Dubai Office) located at Office 209, Level 2, Gate Village Building 7, Dubai International Financial Centre, Dubai, PO

Box 482060, UAE. Robeco Institutional Asset Management B.V. (Dubai office) is regulated by the Dubai Financial Services Authority (“DFSA”) and only deals with Professional Clients or Market

Counterparties and does not deal with Retail Clients as defined by the DFSA.

Additional Information for investors with residence or seat in France

Robeco is at liberty to provide services in France. Robeco France (only authorized to offer investment advice service to professional investors) has been approved under registry number 10683 by the

French prudential control and resolution authority (formerly ACP, now the ACPR) as an investment firm since 28 September 2012.

Additional Information for investors with residence or seat in Germany

This information is solely intended for professional investors or eligible counterparties in the meaning of the German Securities Trading Act.

Additional Information for investors with residence or seat in Hong Kong

The contents of this document have not been reviewed by the Securities and Futures Commission (“SFC”) in Hong Kong. If you are in any doubt about any of the contents of this document, you should

obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (“Robeco”). Robeco is regulated by the SFC in Hong Kong.

Additional Information for investors with residence or seat in Italy

This document is considered for use solely by qualified investors and private professional clients (as defined in Article 26 (1) (b) and (d) of Consob Regulation No. 16190 dated 29 October 2007). If made

available to Distributors and individuals authorized by Distributors to conduct promotion and marketing activity, it may only be used for the purpose for which it was conceived. The data and

information contained in this document may not be used for communications with Supervisory Authorities. This document does not include any information to determine, in concrete terms, the

investment inclination and, therefore, this document cannot and should not be the basis for making any investment decisions.

Additional Information for investors with residence or seat in Shanghai

This material is prepared by Robeco Investment Management Advisory (Shanghai) Limited Company (“Robeco Shanghai”) and is only provided to the specific objects under the premise of

confidentiality. Robeco Shanghai has not yet been registered as a private fund manager with the Asset Management Association of China. Robeco Shanghai is a wholly foreign-owned enterprise

established in accordance with the PRC laws, which enjoys independent civil rights and civil obligations. The statements of the shareholders or affiliates in the material shall not be deemed to a promise

or guarantee of the shareholders or affiliates of Robeco Shanghai, or be deemed to any obligations or liabilities imposed to the shareholders or affiliates of Robeco Shanghai.

Additional Information for investors with residence or seat in Peru

The Fund has not been registered with the Superintendencia del Mercado de Valores (SMV) and is being placed by means of a private offer. SMV has not reviewed the information provided to the

investor. This document is only for the exclusive use of institutional investors in Peru and is not for public distribution.

21Additional Information for investors with residence or seat in Singapore

This document has not been registered with the Monetary Authority of Singapore (“MAS”). Accordingly, this document may not be circulated or distributed directly or indirectly to persons in Singapore

other than (i) to an institutional investor under Section 304 of the SFA, (ii) to a relevant person pursuant to Section 305(1), or any person pursuant to Section 305(2), and in accordance with the

conditions specified in Section 305, of the SFA, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. The contents of this document have not

been reviewed by the MAS. Any decision to participate in the Fund should be made only after reviewing the sections regarding investment considerations, conflicts of interest, risk factors and the

relevant Singapore selling restrictions (as described in the section entitled “Important Information for Singapore Investors”) contained in the prospectus. You should consult your professional adviser if

you are in doubt about the stringent restrictions applicable to the use of this document, regulatory status of the Fund, applicable regulatory protection, associated risks and suitability of the Fund to

your objectives. Investors should note that only the sub-funds listed in the appendix to the section entitled “Important Information for Singapore Investors” of the prospectus (“Sub-Funds”) are

available to Singapore investors. The Sub-Funds are notified as restricted foreign schemes under the Securities and Futures Act, Chapter 289 of Singapore (“SFA”) and are invoking the exemptions from

compliance with prospectus registration requirements pursuant to the exemptions under Section 304 and Section 305 of the SFA. The Sub-Funds are not authorized or recognized by the MAS and

shares in the Sub-Funds are not allowed to be offered to the retail public in Singapore. The prospectus of the Fund is not a prospectus as defined in the SFA. Accordingly, statutory liability under the SFA

in relation to the content of prospectuses would not apply. The Sub-Funds may only be promoted exclusively to persons who are sufficiently experienced and sophisticated to understand the risks

involved in investing in such schemes, and who satisfy certain other criteria provided under Section 304, Section 305 or any other applicable provision of the SFA and the subsidiary legislation enacted

thereunder. You should consider carefully whether the investment is suitable for you. Robeco Singapore Private Limited holds a capital markets services license for fund management issued by the MAS

and is subject to certain clientele restrictions under such license.

Additional Information for investors with residence or seat in Spain

The Spanish branch Robeco Institutional Asset Management B.V., Sucursal en España, having its registered office at Paseo de la Castellana 42, 28046 Madrid, is registered with the Spanish Authority

for the Financial Markets (CNMV) in Spain under registry number 24.

Additional Information for investors with residence or seat in Switzerland

This document is exclusively distributed in Switzerland to qualified investors as defined in the Swiss Collective Investment Schemes Act (CISA) by Robeco Switzerland AG which is authorized by the Swiss

Financial Market Supervisory Authority FINMA as Swiss representative of foreign collective investment schemes, and UBS Switzerland AG, Bahnhofstrasse 45, 8001 Zurich, postal address: Europastrasse

2, P.O. Box, CH-8152 Opfikon, as Swiss paying agent. The prospectus, the Key Investor Information Documents (KIIDs), the articles of association, the annual and semi-annual reports of the Fund(s), as

well as the list of the purchases and sales which the Fund(s) has undertaken during the financial year, may be obtained, on simple request and free of charge, at the office of the Swiss representative

Robeco Switzerland AG, Josefstrasse 218, CH-8005 Zurich. The prospectuses are also available via the website www.robeco.ch.

Additional Information for investors with residence or seat in the United Arab Emirates

Some Funds referred to in this marketing material have been registered with the UAE Securities and Commodities Authority (the Authority). Details of all Registered Funds can be found on the

Authority’s website. The Authority assumes no liability for the accuracy of the information set out in this material/document, nor for the failure of any persons engaged in the investment Fund in

performing their duties and responsibilities.

Additional Information for investors with residence or seat in the United Kingdom

Robeco is subject to limited regulation in the UK by the Financial Conduct Authority. Details about the extent of our regulation by the Financial Conduct Authority are available from us on request.

Additional Information for investors with residence or seat in Uruguay

The sale of the Fund qualifies as a private placement pursuant to section 2 of Uruguayan law 18,627. The Fund must not be offered or sold to the public in Uruguay, except in circumstances which do

not constitute a public offering or distribution under Uruguayan laws and regulations. The Fund is not and will not be registered with the Financial Services Superintendency of the Central Bank of

Uruguay. The Fund corresponds to investment funds that are not investment funds regulated by Uruguayan law 16,774 dated September 27, 1996, as amended.

Additional Information concerning RobecoSAM Collective Investment Schemes

The RobecoSAM collective investment schemes (“RobecoSAM Funds”) in scope are sub funds under the Undertakings for Collective Investment in Transferable Securities (UCITS) of MULTIPARTNER

SICAV, managed by GAM (Luxembourg) S.A., (“Multipartner”). Multipartner SICAV is incorporated as a Société d'Investissement à Capital Variable which is governed by Luxembourg law. The custodian

is State Street Bank Luxembourg S.C.A., 49, Avenue J. F. Kennedy, L-1855 Luxembourg. The prospectus, the Key Investor Information Documents (KIIDs), the articles of association, the annual and semi-

annual reports of the RobecoSAM Funds, as well as the list of the purchases and sales which the RobecoSAM Fund(s) has undertaken during the financial year, may be obtained, on simple request and

free of charge, via the website www.robecosam.com or www.funds.gam.com.

22You can also read