NEW ERA RISE OF A IN DIGITAL PAYMENTS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RISE OF A NEW ERA IN DIGITAL PAYMENTS

2

I dream of a Digital India where the world

looks to India for the next Big Idea

Hon’ble Prime Minister Shri Narendra Modi

inaugurated the 'Digital India Week' at the

Indira Gandhi Indoor Stadium, New Delhi

1st July 2015

3 CONTENTS Ushering in a Digital India 04 Continued Innovation 07 Seamless Customer Experience 08 leads to Explosive Growth Benefits Accrue Across the 09 Payments Ecosystem UPI at the Forefront of Innovation 10 Benefits of UPI for Merchants 11 and Customers Customer Speaks 12 Benefits of UPI to the Banks & FinTech 14 Growth story of UPI 15 UPI Goes Global 17

4 Ushering in a Digital India

5

November 2010 November 2010 March 2012

December 2012 August 2014 August 2016

NCMC

December 2016 October 2017 March 2019

6

Introduction

• India’s digital payments system -has evolved pushing India towards becoming a cashless

rapidly over the last few years. This has economy.

been encouraged by various developments • Firstly, Promotion of digital payments has

in information and communication technol- been accorded highest priority by the Gov-

ogy and by forward looking Regulatory and ernment of India to bring each and every

Government policies. The trinity of near segment of our country under the formal

universal account penetration, increasing fold of digital payment services. The vi-

smartphones penetration and low cost pay- sion is to provide facility of seamless dig-

ments rails has led to a never-before boom ital payment to all citizens of India in a

in digital transactions. For instance, since convenient, easy, affordable, quick and

April 2016, UPI has become synonymous to secured manner.

a rapid digital payment which has seen an

• Secondly, Government is also working on

exponential growth trajectory to cross over

incentivizing digital transactions by provid-

200cr transactions a month. This is further

ing various tax and non-tax benefits to cus-

expected to grow 10x over the next 3 years.

tomers and merchants.

Digital India and Demonetization Drive

• Thirdly, Citizens have been provided multi-

• During the inauguration of the ple options to make digital transactions. A

‘DigiDhan Mela’ on 31stDecember 2016, dedicated ‘Digidhan Mission’ has been set

Honorable Prime Minister, Shri Narendra up for building strategies and approaches

Modi launched BHIM UPI App and urged in collaboration with all stakeholders to

people to make digital payments a habit promote digital payments and create

to transform the country into a cashless awareness.

economy.

• Some of the reforms undertaken in digital

• The Mela resulted in the ‘Digital India’ pro- payments are:-

gramme, which is a flagship programme of

Banking from anywhere, expanding the

the Government of India with a vision to

base of financial inclusion

transform the nation into a digitally em-

powered society and a knowledge econo- Subsidy to end beneficiary’s account

my. To achieve “Faceless, Paperless, Cash- Use of next-gen technologies

less” status is the goal of Digital India. Scaling-up the merchant acceptance

• The ambitious drive to shift from a cash- infrastructure

based to a digital economy saw a strong Incentive schemes for customers and

push in the form of demonetization in merchants

2016, which accelerated this transition by UPI referral and cashback schemes

2-3 years. Since then, the Government of Digital literacy and awareness

India has undertaken several initiatives for

7

Continued Innovation

Early Products Bharat Bill Payment System (BBPS) in

2017

• There has been a continuum of innovation

National Common Mobility Card (NCMC)

in the digital payments space since 1980’s.

– One Nation One Card in 2019

Some of the important milestones attained

in this overall process of development of the NPCI Driving Digital Adoption

payments system include the introduction • To consolidate the innovation in the pay-

of:- ments industry, the Government estab-

MICR clearing in the early 1980s lished the National Payments Corporation

Electronic Clearing Service (ECS) and Elec- of India (NPCI), a not-for-profit umbrella

tronic Funds Transfer (EFT) in the 1990s organization was founded in 2009 to man-

age India’s retail payment systems. NPCI has

Issuance of credit and debit cards by banks

sharply focussed on bringing innovations in

in the 1990s

retail payment systems through the use of

ATMs, Mobile and Internet Banking in

technology for achieving greater efficien-

early 2000s

cy in operations and widening the reach of

The National Financial Switch (NFS) in payment systems.

2003

• NPCI has now been recognized internation-

RTGS and NEFT in 2004

ally for it’s significant impact on retail pay-

The Cheque Truncation System (CTS) in ment systems in India. Many international

2008 organizations and government’s are in ac-

Next Generation Payment Platforms tive consultations with NPCI to translate

• The Government of India has played a pivot- the success of NPCI’s payments systems

al role in driving the adoption of digital pay- in their context. Moreover, the NPCI has

ments by taking a number of steps towards evolved into a strong collaborative platform,

creating a cashless society. Post 2014, this providing opportunities for not only banks,

drive has accelerated as can be witnessed in but also for FinTech players to participate in

the significant initiatives taken to develop in- real- time payments system.

novative next generation payment products • The Government’s ambitious drive to shift

and platforms including introduction of:- from a cash-based to a digital economy

National Unified USSD Platform saw a push in the form of demonetiza-

(NUUP*99#) in 2014 tion in 2016. Since then, the Government

National Electronic Toll Collection (NETC) of India has under taken several initia-

in 2016 tives for pushing India towards becoming a

Unified Payments Interface (UPI) and cashless economy.

BHIM App in 2016

8

Seamless Customer Experience

leads to Explosive Growth

Accelerating Growth required

• It is noteworthy that total digital transac- Interoperability – Customers can trans-

tions which were 1,004 crores in FY 2016- fer money on a real-time basis (available

17 have seen exponential growth post the 24×7) and across multiple bank accounts

launch of UPI. During FY 2017-18, 106% using any UPI App

growth was witnessed taking the tally to Affordable merchant acceptance infra-

2,071 crore transactions. structure both static UPI QR and dynam-

ic UPI QR at the merchant locations

• In FY 2018-19, UPI accounted for 17% of

the total 31 billion digital transactions in the Cost-effective way of making/accepting

country. The next fiscal year saw UPI’s share payments

rising to more than 27% as it processed 12.5 Enhanced security

billion transactions of the total 46 billion UPI is a completely open and interopera-

digital transactions. In FY 2020-21, UPI ble: Transaction can be initiated from any

accounted for 40% of the total 55 billion bank’s UPI app

digital transactions Works on Immediate Payment Service

To put these numbers in context, the value (IMPS) platform

of transactions on BHIM UPI amounted to Both payment and collection transactions

15% of India’s GDP in FY 2019-20. are possible

• With UPI, customers can make payments No need of pre-addition/approval of ben-

instantly via their mobile devices. It has eficiary

become a popular digital payment option • As a result, as of June 2021, UPI

owing to its unparalleled benefits superior has 21+ crore users who did 2.8

customer experience features like :- billion financial transactions in June,

Simple to use functionality: Requires totalling to a settlement value of

only Virtual Payment Address (VPA), `5.47 lakh crore.

i.e.: account no., IFSC code, etc. are not

9

Benefits Accrue Across the

Payments Ecosystem

• UPI’s rapid growth has once again demon- quire any brick and mortar branch visits

strated India’s ability to build a world-class • Low cost QR code based physical accept-

payments infrastructure from scratch. The ance aided by in–app, web and intent based

UPI system has created a national open payments

standard which has been adopted by more

• Fully compliant with international security

than 200 Indian banks.

standards and certifications

• The open systems has enabled global

• Payments are UPI ID based, providing high-

players like Google, WhatsApp, Walmart,

er security and confidentiality to theUsers

True Caller, Amazon, Uber to provide

UPI services. • Enables contactless payments across all chan-

nels like mobile, ATM, internet and Mobile

• Further, benefits of UPI accrue across the

Banking

payments ecosystem:-

• In short, UPI’s large number of benefits

• Person to Person (P2P) and Person to Mer-

has truly transformed the country from a

chant (P2M) payments give customers 100%

cash-dependent economy to a nation known

coverage of payment transactions

for its digital payments landscape.

• Truly interoperable payment system running

round the clock with participation from both

banks and non-bank entities

• UPI also allows for multiple methods for in-

tegrating merchants - QR based payments

being the most popular. In just 5 years, over

100 million UPI QRs have been deployed

in the market for accepting merchant pay-

ments, from only 2.5 million devices that

were accepting merchant payments prior

to this.

• Support for all sources of funds viz. Bank Ac-

count, Pre-paid Wallets, Overdraft Account

etc.

• Fully digital on-boarding which does not re-

10

UPI at the Forefront of Innovation

Enhancing Trust for Customers and small businesses collect payments from

Businesses their customers, which used to be manual,

mostly cash-based. Using UPI, merchants

• The benefits of UPI was observed in full

can now remind customers to pay and even

glory during the COVID-19 pandemic when

set up specific dates for the customer to pay

UPI served as critical lifeline especially for

by, simplifying the collection process.

small and micro merchants. In FY 2020-21,

UPI processed over 9 billion contactless Tapping Use Cases

merchant transactions with total value • UPI has also helped Banks to reduce cash

over `6 lakh crores. requirements on channels like ATMs

• UPI has made buying and selling through and Branches resulting in reduction in

fintech app solutions, easier for both e-com- operational costs and improving custom-

merce providers as well as consumers. This er experience. It can also anchor a broader

has created a huge demand in the FinTech suite of fintech applications like micro-pen-

industry. There is no lag which helps in the sions, digital insurance products, and flexible

smooth flow of business. loans. These are custom solutions created by

Indian technology companies, on the public

• Moreover, UPI has opened a host of oppor-

infrastructure of UPI.

tunities for start-ups and e-Commerce play-

ers to come up with innovative solutions that • Tech companies are increasingly leveraging

elevate the customer experience. the power of UPI to expand the digital eco-

system and this has led to a great accelera-

• UPI also changed the way merchants and

tion in the pace of financial inclusion.11

Benefits of UPI for Merchants

and Customers

For Merchants:- For Customers:-

• Secure and convenient way to • Round-the-clock availability

receive payment directly in bank • No sharing of sensitive data

account.

• Simple user interface including ease of raising

• Low cost infrastructure for receiv- complaints

ing payment – QR Code

• Convenience and affordability (no cost/ very low

• No need to handle cash cost)

• Zero MDR • Availability of apps with simpler interfaces

• No risk of storing sensitive data • Suitable for payments without exposing account

• Collect functionality details

• Suitable for both online and offline • Convenient for high frequency low value merchant

merchants payments

• Integration into real-time pay- • Multiple options (Apps) available for to the

ments customer. Customers can choose from BHIM,

• Access to large database of cus- individual bank as well as non-bank Apps

tomers using UPI payment mode • Financial inclusion due to low cost and ease of

• No need of storing customers operation

bank or financial details • Creates Digital financial footprint for users which

enables access to credit and other financial services12

Customer

Speaks13 Customer Speaks

14

Benefits of UPI to the Banks &

FinTech

For Banks:- For Payment Service Providers & FinTech:-

• Low cost alternative to cash • Open architecture fosters innovation and

transactions development of unique products

• Low merchant onboarding cost • Promotes partnerships with banks & FIs for

• Data on transactions enables development of customer centric solutions

targeting customers for other • Opportunity to target UPI customers for

financial services credit and other financial services

“

The UPI Platform has been build on a

open source stack which is one of the most

advanced open source stacks which means

that UPI is capable of scaling up to billions of

“

With many customers opting for contactless payments, UPI

has become their preferred mode in the digital payments

innovation in the country giving customers a truly world-class

transaction at very low cost. experience.

Shri Nandan Nilekani, Co-Founder, and Non- Mr. Harshil Mathur, Razorpay

Executive Chairman, Infosys

“

Ever since UPI launched is 2016, we have

wintnessed UPI’s rapid adoption amongst

the public. The success story of UPI has been

acknowledged across the world with other

“

UPI AUTOPAY gives customers and business the

complete control of their payments. The feature helps

businesses automate billing, improve cash flows, and offers

better pricing.

countries trying to emulate siiler solutions.

Shri Rajnish Kumar (Formar Chairman, State Mr. Sudhir Sehgal - PayU

Bank of India

“

UPI is a big step forward in customer convenience which

offers significant customer of registering recurring

payments one time without the fear of forgeting monthly

payments.

Mr. Parag Rao, HDFC Bank15

Growth of UPI Ecosystem

Number of Banks in UPI Number of Unique Customers in UPI (Cr)

25

250 224 21

216 20

20

200

142 148 15

14

150

91 10 8

100

44 5 3

50

0

0 0

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Jun-21 Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Jun-21

UPI - Merchant Payments

10,000 6,00,000

UPI Apps

9,291

5,00,000

8,000 6,22,061 cr

16 Fintech

4,00,000 20 Fintech

6,000 Apps

4,458

Apps

3,00,000

4,000

2,17,479 2,00,000

80+ total UPI Apps

2,000 1,131 1,00,000

2 104 49,512

- 79 4,130 -

FY 16-17 FY 17-18 FY 18-19 FY 19-20 FY 20-21

Vol (mn) Val (cr)16

Growth in UPI transactions

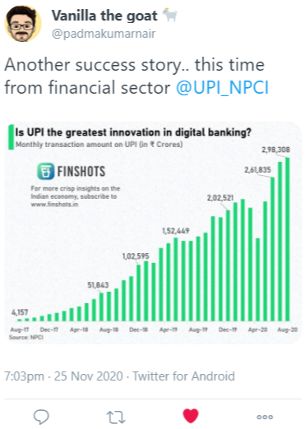

UPI has gained significant traction in the domestic market, and also recognition in

international markets in a short span of time.

F.Y-2016-17 F.Y-2017-18 F.Y-2018-19 F.Y-2019-20 F.Y-2020-21

Volume Value Volume Value Volume Value Volume Value Volume Value

Platform (in Lakh) ( Cr) (in Lakh) ( Cr) (in Lakh) ( Cr) (in Lakh) ( Cr) (in Lakh) ( Cr)

UPI 179 6,947 9,152 1,09,832 53,534 8,76,970 1,25,186 21,31,730 2,23,307 41,03,653

CONTRIBUTION OF UPI TRANSACTIONS IN TOTAL DIGITAL TRANSACTION

(IN CR)

6000 90%

5554

80%

5000

4572 70%

4000 60%

3134 50%

3000

40% 40%

2070

2000 30%

27%

20%

1000 17% 2233

1251 10%

4%

92 535

0 0%

17-18 18-19 19-20 20-21 (Provisional)

Total Fin. Txn. Vol UPI Fin. Txn Vol % UPI Share17

UPI Goes Global

• Reserve Bank of India (RBI), in close collab- • For instance, UPI is now live in Singapore and

oration with the Government and National in the UAE, work is under progress. NPCI is in

Payments Corporation of India (NPCI), is discussions with more than 30 countries for

working to expand the reach of Unified Pay- enabling acceptance of remittances through

ments Interface (UPI) globally. In this con- the adoption of UPI.

nection, RBI has approached other central • Further, many other institutions across dif-

banks highlighting the features of UPI as an ferent countries have reportedly been ex-

efficient and secure system. ploring setting up UPI like platforms.

• To streamline the foray of UPI into inter- • At global forums like the World Bank and

national markets, National Payments Cor- Bank for International Settlements (BIS),

poration of India (NPCI) has launched its there have been discussions around the

dedicated international subsidiary ‘NPCI need and importance of domestic real-time

International’. low-cost payment systems and also on the

• NPCI has achieved the pinnacle of success at possibility of connecting payment systems

developing an exemplary robust payments of different countries to facilitate real-time,

system that is cost effective, secure, conven- low cost cross border remittances.

ient and instantaneous. Several nations have • UPI has immense potential to provide the

displayed an inclination towards establishing basis for a stronger bilateral business and

a ‘real time payment system’ or ‘domestic economic partnership with other jurisdic-

card scheme’ inspired by the exemplary in- tions, and helps buttress India’s soft power.

novations by NPCI in the country.

“

With UPI, India has created something

‘truly special’ and is opening up a world of

opportunities for micro and small businesses

that are the backbone of the Indian economy.

“

UPI was thoughtfully planned and critical aspects of its

design led to its success. It is an open system on which

technology companies can build apps that help users

to directly manage transfers into and out of their bank

accounts.

Mark Zuckerberg, CEO-Facebook

Sundar Pichai, CEO-Alphabet

“India has built an ambitious platform for digital

payments, including a system for sending

rupees between any bank or smartphone app.

“

India’s Unified Payments Interface allows both domestic

and global players to develop mobile payment applications.

As such, it lowers the barriers to entry, especially for smaller

firms, thus levelling the playing field.

Bill Gates, Co-Founder-Microsoft Agustin Carstens, GM-BIS

“

Google has been a successful market participant in India’s use of UPI,

and Google Pay provides one of the three leading mobile applications

that use UPI, as measured by transaction volume. Google wants the

US government to follow a similar model of open-payments to build

FedNow, a new interbank real-time gross settlement service (RTGS) for

faster digital payments in the country.

Mark Isakowitz, VP-Google11

18

UPI Chalega

GHAR SE

BILL PAYMENT

KE LIYE

UPI CHALEGA

chalega

Easy Safe Instant

Easy. Safe. Instant.

upichalega.comMinistry of Information and Broadcasting Government of India

You can also read