ONEWORLDMESSENGER POSITIVELY DISRUPTING GLOBAL REMITTANCE 2019 - ONEWORLDMESSENGER LTD, A WYOMING REGISTERED COMPANY WWW.ONEWORLDMESSENGER.IO ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

OneWorldMessenger

POSITIVELY DISRUPTING GLOBAL REMITTANCE

2019

OneWorldMessenger Ltd, a Wyoming Registered Company

www.oneworldmessenger.io

This document is confidential and the right to use it is limited to OneWorldMessenger ltd.

1

“This revolutionizes the way the world moves money.” 2

OneWorldMessenger

04 Main Summary

06 Why Invest in MBIT

07 Executive Summary

11 Company Overview

13 Our Technology

15 Market Potential

25 Profit Potential

28 Process & System

29 Regulation and Auditing Control

30 Disclaimer and Investment Risks

31 List of Countries in Territory

3

Main Summary A. Competitive Advantage OneWorldMessenger offers secure advanced banking, utilizing the latest in banking technology. Our advanced blockchain technology allows us to have some of the fastest and most secure banking transactions and remittance. We expect to have a presence in every country and offer services to the unbanked, reaching an estimated 250 million users by 2025. We have a real bank card that can be used to make purchases at any POS as well as at over 4.5 million ATM machines around the globe. Earn cash back (in crypto) on every purchase using our bank card. We will offer 180,000 loading points within the USA and about 1.5 million worldwide. Our fees are a fraction of others. While the average remittance fees are anywhere between 5% to 7%, our system allows users to send money to anyone around the globe for free (using card to card technology) or as little as $0.75 (using one of 4.5 million ATM machines). B. Our Strategic Partners Wallmart CVS 7 Eleven Walgreens IBM Trescon Depo C. Proprietary Technology Our blockchain technology is one of the fastest and arguably the safest in the industry. Messenger Fintech is FINMA registered and utilizes the latest in financial technology. 4

D. Security/Consumer Protection

We designed our crypto wallets with security in mind. All data is encrypted and stored using

military-grade security and encrypted with AES-256. We employ two-factor authentication

as an added extra layer of security, ensuring the safety of your account and wallet. For an

additional step of security, we are not only relying on 2FA—Two Factor Authentication – but

mixing it up with fingerprint Biometrics.

Get real time notification of the use of bank card with an option to instantly lock and unlock

of bank card via phone.

Advanced KYC/AML authentication and verification system.

E. Fees

Card cost: Midnight Black card $200; Cobalt Blue card $50

Loading and top-off fees $4.95

ATM withdrawal fees $0.75 at any ATM

Can send money to anyone around the globe for free (using card to card technology) or as

little as $0.75 (using ATM machines).

F. Client Services

High tech banking services available on any smart phone.

Best money remittance fees in the industry.

Bank cards with the latest in functionality, technology, and security that can be used at over

4.5 million ATM’s and 44 million POS locations around the globe.

G. Global Expansion

The goal of our global expansion strategy is to reach an unprecedented level of market

penetration by having an estimated 250 million users and 1.5 million loading point by 2025. A

considerable 30% of our revenue is designated for marketing, promotion and growth.

H. Changing the World /Bettering the World

OneWorldMessenger’s goal is to have an impact on humanity by empowering a considerable

segment of the world’s unbanked and underbanked population-an estimated 2.6 billion.

We envision a world where anyone with a smart phone can have a bank account and where

anyone can send or receive money at a fraction of the current costs. Our objective is to

harness the power of the blockchain and fintech to level the world’s financial playing field.

5

Why Invest in MBIT The MBIT token is a game changer. It is the next big thing in the world of cryptocurrency, maybe only rivaled by the likes of Bitcoin and Etherium. Without going deep into the technical aspects of how crypto or the MBIT works, our blockchain is one of the fastest and most secure in the industry. Over the past few years, as cryptocurrencies have grown in popularity, their price has risen dramatically. The trend has fluctuated but has maintained an upward trend and will continue to go up as more and more people continue to buy crypto. Cryptocurrency is becoming mainstream as more governments are adapting it, and states are creating legislation in favor of it. Even banks are taking the approach that they need to get involved in crypto in order to survive. They see the tremendous investment opportunity presented during the relatively early stages of cryptocurrency. Experts, including Tim Draper of Draper Investments on CNBC predict that in 5 years, most stores won’t even accept cash anymore. Just crypto or other forms of electronic payments. The MBIT token is poised to dominate the world of crypto. Unlike all other cryptocurrencies, the MBIT is not just a speculative security token but is part of a tangible, real service. For starters, MessengerBank provides MBIT token holders with 40% profit sharing, distributed among all token holders. Revenue will be generated from millions of users-an estimated 250 million users and $690 million annually by 2025. Members will be using OneWorldMessenger for online banking, money remittance, bill payment, etc. Our strategy includes over 1.5 million loading points worldwide, starting with 180,000 loading points in the continental USA. We will furnish users with permanent bank cards accepted at millions of retail locations and at more than 4.5 million ATM locations worldwide. In addition, the value of the MBIT token will go up exponentially as it becomes one of the most sought after tokens in the crypto space. MessengerBank, OneWorldMessenger, and MBIT will become household names. Can you imagine the smile on your face if you purchased the MBIT for pennies today and in two or three years it is valued for $10 maybe $40 dollars? Now is the perfect opportunity, don’t miss out like you may have missed out on Bitcoin, Apple, Microsoft. Google, Amazon, etc…. 6

Executive Summary

MessengerBank’s mission is to bridge the gap between digital and fiat currencies by providing

a decentralized, Blockchain-enabled mobile banking solution that is easy to use, accessible,

nondiscriminatory and inclusive of all demographics. Unlike other Blockchain-based services,

MessengerBank is enabling the mass adoption of cryptocurrencies so that anyone can use

cryptocurrencies as they would use fiat currencies. We achieve this by providing seamless

exchange between crypto and fiat, by providing quick enrollment, safe and compliant on-

boarding and easy-to-use features on our banking platform while offering all the traditional

banking services people are used to.

MessengerBank’s digital and transparent services are not only attractive for the banked

population, but they can also deliver financial inclusion solutions to the 2.6 billion unbanked and 1

billion underbanked globally, thereby creating a unique cross-border platform to serve everyone,

everywhere.

It may be hard to believe, but about 2.6 billion people in the world do not have a bank account.

The majority of them live in low and middle-income emerging markets, but even in high-income

countries, large numbers of people are unable to use banks to meet their day to day financial

needs. While banking is fairly accessible in the western world, most countries have very high

barriers to open bank accounts. Over 2.6 billion people can’t even qualify to open a bank account

because they do not meet local banking financial qualifications or there are no banks close to

where they live.

With this said, OneWorldMessenger was created with the simple objective of leveling the

financial playing field by banking the unbanked and providing rapid, low cost remittance

anywhere on the globe. There is a huge market potential in banking the unbanked and in the

global remittance business, and it is fully sustainable. We have formed an exclusive strategic

partnership with industry-leading Messenger Fintech, based in Zug Switzerland.

OneWorldMessenger is poised to take full advantage of these booming market opportunities.

We are on track to provide secured, high tech, high speed online banking services to about 250

million of the world’s unbanked by 2025. We will offer the latest in banking services, including

an advanced bank card, the ability for bill pay and many other services. Our services will be done

at a fraction of the cost of traditional banking. We will tap into this underserved portion of this

population and provide services that would simply have been impossible to many of the world’s

unbanked to receive otherwise. Not only would we be changing the world of banking, we will also

empower and improve the lives of hundreds of millions of people worldwide.

7

Worldwide flow of remittance has more than doubled in the last decade and is currently at about $700 billion dollars (2018). This only accounts for transfers via official channels. It is estimated that there is about an additional 50% of the amount transferred via informal channels, pushing the number to over one trillion dollars. OneWorldMessenger is a high-tech payment and financial services company registered in Wyoming. We operate under the umbrella of MessengerBank and will build MessengerBank’s POS (Point of Sale) and loading point network for remittance and online banking. Messenger Fintech has some of the most advanced fintech and blockchain technology and has partnerships with IBM and other tech companies. Thanks to our high tech banking system and partnerships, OneWorldMesseneger is a game changer that will positively disrupt the banking and remittance market. This strategy will establish us as a major player in the world of remittance and banking while allowing us to achieve significant financial profits. OneWorldMessenger traces its roots back to 1999, to ClubWorldConnect (CWC). CWC redefined the remittance industry and went on to become arguably the world’s most successful remittance company before being sold for $863 million in 2008. CWC was a true pioneer in the field of money remittance. The company created a system that utilized mobile Visa sim cards and SMS cards over its own mobile network to allow immigrants to send money home while providing the highest security and speed at the cheapest rates. Keep in mind, this was all done in 2008, before the age of smartphones and other technology that have come to shape our everyday life. The CWC team went back to the drawing board, relying on years of experience and the latest advancement in fintech as well as blockchain technology, to bring us OneWorldMessenger. OneWorldMessenger is scheduled to start operations in the United States on July 4th, 2019 by launching in about 180,000 loading points at locations such as Walmart, CVS Pharmacy, 7-Eleven, Walgreen’s and many more. The US territory is the launching phase to a global expansion that will have us in over 220 countries. We will have loading points in the respective country’s major big box and grocery store locations as well as community centers, banks and other digital payment services. “Our clients will be able to instantaneously withdraw funds, for as little as $0.75, anywhere on the globe using one of the more than 4.5 million ATM’s.” 8

OneWorldMessenger has a winning formula utilizing the latest in banking and financial

technology, fraud detection, KYC/AML and blockchain technology. Our clients will not only be

able to load and reload their accounts in hundred of thousands of loading point in over 220

countries but also instantaneously withdraw funds, for as little as $0.75, anywhere on the globe

using one of the more than 4.5 million ATM’s.

We have an aggressive, well-funded, and sophisticated multi-faceted marketing and advertising

campaign that will turn MessengerBank and OneWorldMessenger into a household name and

leader in the world of online banking and global remittance.

Based on conservative industry estimates, we expect exponential growth, fueled by customer

loyalty, brand recognition and massive availability of ground-breaking banking and remittance

services.

Phase 1: US Market Launch.

We are launching our banking and remittance services in the US market on the 4th of July

2019. We should have our 180,000 loading locations at places such as Walmart, CVS, 7-Eleven,

Walgreen’s. Our bank cards will allow our clients to withdraw money at any of over 4.5 million

ATM machines, anywhere in the world. This rollout will be heavily marketed and advertised by us

and our business partners.

Phase 2: Latin America, and most of Asia

This expansion will add at least 200,000 additional loading points by partnering up with the

leading retailers in that region, such as Carrefour, Tesco, Walmart, and China Union Pay. By

this phase, our services will be available to most of the world’s population as well as its biggest

economies. This phase will also have a considerable marketing budget.

Phase 3: Rest of World Implementation, Including Europe, Africa, and India

This phase will complete our global expansion by making our loading points available in Europe,

Africa, and India. This will allow anyone, in any country to be able to open an online bank account,

send and receive money around the world or around the corner within seconds. Thanks to our

technology, our customers will only pay a fraction of current banking and remittance fees.

OneWorldMessenger has a solid development strategy to launch in the USA and quickly be

available in all countries. We expect to generate substantial profits by not only becoming the

world leader in remittance but also by introducing online banking to anyone, including the

world’s unbanked. Our remittance service and banking fees will be our two main parallel sources

of revenue.

9

Expected Transactions Amount: OneWorldMessenger expects approximately 15 million users in the first year, we project to have a total of approximately 250 million users by 2025. That will translate to about $54 billion in forecasted transaction volume in our first year and about $900 billion by 2025. Forecasted Net Profit: Due to our efficient technology, we expect low operational expense and high net yearly profit of about $216 million by the end of the first year. That should steadily increase to about $1.1 billion for the year 2025. By 2025 we conservatively estimate to have about 250 million users in our ecosystem and expect continued exponential growth year after year. OneWorldMessenger is looking to raise funds through sales of the MBIT coin. This token is a great opportunity with unlimited returns. Forty percent of Messenger Fintech’s profits will be passed on to token holders in the form of revenue sharing. Another 30% will be put right back into growing and improving the OneWorldMessenger network in the form of marketing, advertising and continuously improving technology. The remaining 30% will go to Messenger Fintech. Buyers of this coin are not just buying another cryptocurrency but are joining forces with OneWorldMessenger and getting under the MessengerBank umbrella, poised to become one of the largest online banks and remittance companies. Our token truly has no equal in the crypto space and may very well become one of the most sought after crypto currencies. This is your opportunity to get in with us at such relatively early stage. PROFIT DISTRIBUTION 40% PROFIT SHARING TO MBIT TOKEN HOLDERS 30% DESIGNATED FOR MARKETING & GROWTH 30% TO MESSENGER FINTECH 10

Company Overview

Worldwide flow of remittance has more than doubled in the last decade and is currently at about

$700 billion dollars (2018). This only accounts for transfers via official channels. It is estimated that

there is about an additional 50% of the amount transferred via informal channels, pushing the

number to over one trillion dollars. OneWorldMessenger is a high-tech payment and financial

services company registered in Wyoming. We operate under the umbrella of MessengerBank

and will build MessengerBank’s POS (Point of Sale) and loading point network for remittance and

online banking.

Messenger Fintech has some of the most advanced fintech and blockchain technology and has

partnerships with IBM and other tech companies. Thanks to our high tech banking system and

partnerships, OneWorldMesseneger is a game changer that will positively disrupt the banking

and remittance market. This strategy will establish us as a major player in the world of remittance

and banking while allowing us to achieve significant financial profits.

OneWorldMessenger traces its roots back to 1999, to ClubWorldConnect (CWC). CWC redefined

the remittance industry and went on to become arguably the world’s most successful remittance

company before being sold for $863 million in 2008. CWC was a true pioneer in the field of

money remittance. The company created a system that utilized mobile Visa sim cards and SMS

cards over its own mobile network to allow immigrants to send money home while providing

the highest security and speed at the cheapest rates. Keep in mind, this was all done in 2008,

before the age of smartphones and other technology that have come to shape our everyday life.

The CWC team went back to the drawing board, relying on years of experience and the latest

advancement in fintech as well as blockchain technology, to bring us OneWorldMessenger.

OneWorldMessenger is scheduled to start operations in the United States on July 4th, 2019 by

launching in about 180,000 loading points at locations such as Walmart, CVS Pharmacy, 7-Eleven,

Walgreen’s and many more. The US territory is the launching phase to a global expansion that will

have us in over 220 countries. We will have loading points in the respective country’s major big

box and grocery store locations as well as community centers, banks and other digital payment

services.

“Our clients will be able to instantaneously withdraw

funds, for as little as $0.75, anywhere on the globe

using one of the more than 4.5 million ATM’s.”

11We are really proud of our history. We are here today, not only thanks to our groundbreaking technology but also thanks to our previous experience and achievements with ClubWorldConnect. We are confident that our CWC experience and know-how is going to be instrumental in allowing us to harness the latest achievements in fintech and blockchain on our way to achieving tremendous success with OneWorldMessenger. We would like to share with you just a few of the many recognitions we had with ClubWorldConnect: 12

Our Technology

What is Fintech:

Have you used any form of online banking? Have you bought coffee using your smartphone?

Have you made any online bill payment or online check deposit? If you answered yes to any of

the above, then you have used fintech. Thanks to the advances in smartphones, tablets, and

social media, fintech is becoming a ubiquitous part of everyday financial transactions. Fintech,

a combination of “financial technology”, now handles all banking and financial transactions,

from A to Z. Consider fintech as the industry that will replace analog and traditional banking and

financial transactions.

Fintech is used for:

• Cryptocurrency and digital cash

• Blockchain technology

• Smart contracts

• Compliance such as AML and KYC

• Banking the unbanked and underbanked

• Cybersecurity and encryption

• Online Banking

Fintech seeks to improve and automate the delivery and use of financial services. Fintech uses

specialized software and algorithms to help companies, business owners and consumers better

manage their financial operations.

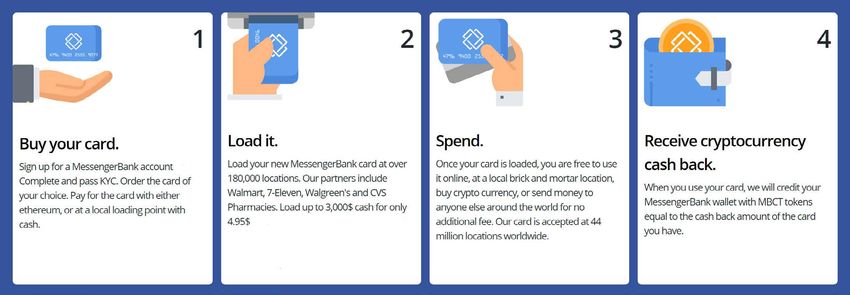

A person wishes to send money The blockchain is used as a rail Her relative uses his bank

to her relative in another to securely and efficiently send card that is linked to the same

country. She looks up on her money in an instant. MessengerBank account at

phone the closest loading point any ATM around the world to

and adds money to her account. withdraw those funds and pays

only $0.75

13When fintech emerged in the 21st Century, the term was initially applied to the technology behind the scene, as the back-end systems of established financial institutions. Now the shift is more towards consumer-oriented services and therefore a more consumer-oriented purpose. Fintech now includes most technological innovation and automation in the financial world and has come to include financial literacy, education, streamlining of wealth management services, lending and borrowing, retail banking, fundraising, money transfers/payments, investment management and more. Fintech also includes the development and use of crypto-currencies that run on blockchain technology. We will offer the world’s most secure, convenient, and advanced bank card with features such as card lock and unlock to minimize fraud and lost cards, real-time notification, as well as card to card free money transfer. We will use our proprietary blockchain as the rail for all our transactions allowing for lightning speed transactions, anywhere on the globe. Each account holder will have an online wallet that is unrivaled in technology and security. We designed our crypto wallets with security in mind. All data is encrypted and stored using military- grade technology and encrypted with AES-256. We will employ two-factor authentication as an added extra layer of security, ensuring the safety of your account and wallet. For an additional step of security, we are not only relying on 2FA—Two Factor Authentication – but mixing it up with fingerprint Biometrics. Why Invest in MBIT? Through our cutting-edge technology, we are disrupting the financial world of banking. We will be offering anyone with a cell phone access to full banking services such as debit cards accepted at any ATM and retail POS that accepts cards, bill pay, as well as a nationwide prepaid debit card platform with over 180,000 loading points. 14

Market Potential

A strong global economy fueled a record 2018 remittance flow approaching, $700 billion.

Remittances to low and middle-income countries are projected to jump by almost 11 percent this

year to a record of $528 billion, according to the latest edition of the World Bank’s Migration and

Development Brief. This increase is on top of a 7.8 percent gain last year. Due to our pioneering

technology, we are positioned to become a major player in global remittance.

When high-income countries are included, 2018 total global remittances are approaching

$700 billion this year and are expected to grow 3.7 percent to $715 billion next year. To put this

in perspective, in just 13 short years, between 2006 and 2019, the global remittance market

ballooned from $276 billion to well over $700 billion; close to a 250% growth! These statistics only

include numbers in “official channels”. Unofficial channels also account for a huge flow of global

movement of money. Thanks to outstanding advances in hi-tech solutions, we do not expect the

remittance industry to level off as the world is becoming a much smaller place.

Thanks to the mass adoption of smartphones and other technology, the digital volume portion

is expected to account for about half of all global remittance. To put this in perspective, digital

remittance accounted for merely 10% of total remittance in 2014, this translates into about 500%

increase. While traditional remittance services are struggling to adapt to this shifting trend that

represents by far the fastest growing, OneWorldMessenger is positioned to capture and control

a considerable market share in remittance that could translate into very lucrative financial returns.

“A strong global economy fueled a record 2018

remittance flow approaching, $700 billion...we are

positioned to become a major player in global

remittance.”

15North American Region The United States has by far the largest volume of outbound remittance. A large portion is by migrant workers and immigrants sending money; a considerable number of those funds are sent to Latin American nations. According to the Central Bank of Mexico, Mexicans sent home $26.1 billion in 2017. The vast majority came from those living in the United States. Remittances are one of Mexico’s top sources of foreign income, outpacing oil exports, which totaled $18.5 billion between January and October. Remittance was second to manufacturing exports as top source of foreign income for Mexico. Mexico accounts for one-third of all remittance from the USA to Latin America and the Caribbean. Experts add that the devastating earthquake in and around Mexico City in September likely caused Mexicans to send extra assistance to loved one to help in the recovery process. Some of Mexico’s poorest states tend to receive the most in remittances, making the extra cash a key source of income for millions of Mexicans living in poverty. At least $30-billion a year is transferred in and out of Canada citing data supplied by the World Bank. More than 6.7 million people in Canada, or more than 20 percent of the entire Canadian population, were born elsewhere-a very high proportion among any population vs nationals. Obviously, this leads to mostly outbound remittance, where people send money to friends and relatives in their native lands. “The United States has by far the largest volume of outbound remittance. A large portion is by migrant workers and immigrants sending money; a considerable number of those funds are sent to Latin American nations.” 16

Central & South America

The strong U.S. economy and labor market, is expected to lead to significant flows of remittance

by migrant workers back home to Latin America and the Caribbean that will reach over $90

billion in 2019. Mexico and Central American countries are the main beneficiaries. During 2018,

family remittances to Central American countries totaled $28.67 million, that is an 11% growth

from the previous year.

From January to March of this year Honduras received $1.2 billion in family remittances, an

amount 10.1% higher than that reported in the first quarter of 2018. In the first two months of

2019, the country received $776 million in family remittances, an amount 12% higher than that

reported in the same period of the previous year. In the first month of 2019, the country received

$402 million in family remittances, 17% more than in January of the previous year.

In the first three months of 2019 Guatemala’s income from family remittances in the country

will total $2.2 billion, 9% more than in the same period last year. The latest figures from the Bank

of Guatemala show that in March 2019 the country received $826 million in remittances, 10%

more than the $754 million recorded in the same month in 2018. In the first two months of 2019,

income from family remittances in the country totaled $1.38 million, 9% more than in the same

period last year.

Last year, family remittances sent to Nicaragua totaled $1.5 million, 7.9% more than the $1.39

million reported in 2017. In 2018 the country received $1.5 billion in family remittances, 8% more

than that recorded in 2017. In terms of year-on-year growth, Nicaragua ranks fifth as a recipient of

family remittances at the regional level. Remittances to Honduras registered the highest growth

in the region, 14%, followed by Guatemala (13.4%) and the Dominican Republic (10.4%), according

to a report by the Central Bank of Nicaragua (BCN).

17Asia Asia accounts for over 60% of the world’s population and also accounts for the world’s fastest economies and labor force. Many foreign laborers from countries like the Philippines, Pakistan, India, Bangladesh work in places like the Middle East and send money on a monthly basis back home. Due to trade and a large population, remittance in and out of Asia is robust and is consistently trending upwards. Remittance recipients were led by India with a total of$80 billion this year, followed by China’s $67 billion, the Philippines with $34 billion. Remittance flows to East Asia and the Pacific region are expected to grow by 6.6% in 2018 to $142 billion, 1.5 percentage points higher than the growth rate in 2017. Remittances to the region reached $148 billion in 2018. Remittances to South Asia increased by a staggering 13.5% to $132 billion in 2018. This increase is driven by stronger economic conditions, export to western trading partners, and emigrants sending money back home. India accounts for about $80 billion in total remittance, $70 billion in incoming remittance. The majority of India’s outbound remittance, about $4 billion is to Bangladesh. This number reflects the number of migrant workers in India sending money back to family members, those are prime candidates for our banking services. Also, there is about $13 billion sent from the UAE India, $5.5 billion to Pakistan and, $4 billion to the Philippines. These clients can also greatly benefit from OneWorldMessenger’s online banking and remittance services. Indonesia has about $9 billion in inbound remittance mostly from immigrant workers in Saudi Arabia, the USA, and China. And presents another very promising market for our services. “Asia accounts to over 60% of the world’s population... Top remittance recipients were led by India with a total of $80 billion this year, followed by China’s $67 billion, the Philippines with $34 billion.” 18

Africa

Remittances to low- and middle-income countries, a category that describes most African

countries, grew rapidly and are projected to reach a new record in 2019 according to the latest

edition of the World Bank’s Migration and Development Brief.

Remittance flows rose in Sub-Saharan Africa (9.8 percent). Remittances to the Middle East and

North Africa regions were $53 billion in 2017 in US Dollars and are projected to grow by 9.1 percent

to $57.7 billion in 2019, followed 7 percent growth in 2020. The growth rate is driven by Egypt’s

projected rapid remittance growth of 14%. Beyond 2019, the region is expected to experience

continued growth in remittances, although at a slower pace of 2.7 percent in 2020. Lower oil

prices are expecting to moderate growth in GCC countries and remittance outflows will also be

dampened by nationalization policies of Saudi Arabia, notably in sectors banning foreign workers

as of 2018.

Remittances to Sub-Saharan Africa continued to accelerate in 2019 and are estimated to grow

by 9.8 percent to $50 billion in 2019. Projections indicate that remittances to the region will keep

increasing but at a lower rate of 4.2 percent in 2020. The upward trend observed since 2016 is

driven by strong economic conditions in advanced economies. In addition, because of large

intra-regional migration flows in the region, remittance flows are expected to keep increasing

due to projected strong regional economic growth in 2019.

Informal channels: Due to the relatively high costs of remittance through formal channels, many

migrants prefer to remit through informal channels. With the exponential growth of ownership of

smartphones throughout Africa, this will be the chosen method within a few short years.

Remittances: Transaction costs, determinants, and Informal flow; migrants prefer informal

channels because they are faster and more convenient, are not constrained by any regulatory

banking and foreign exchange regulations, and do not require remitters to have bank accounts.

An improvement in financial services and greater competition will decrease transaction costs.

Informal remittances may be anywhere from 46 to 65 percent of total remittances, with the most

extreme use of informal channels found within Sub-Saharan Africa, Eastern Europe, and Central

Asia. In 2017, the region received remittances valued at $ 53 billion.

19Africa Moving cash within Africa is an untapped opportunity for money transfer firms. Nigeria topped African recipients with $24.3 billion in 2018. Liberia was the African country for whom remittances accounted for the highest share of GDP at 25.9%. The mobile phone has been vital in enabling the ease of connection, more migrants send smaller amounts more frequently now, with apps, mobile money, and traditional bank accounts all playing their role. While much focus is often on migrants in Western countries, the largest amount of people moving to new countries is within Africa. One of the biggest challenges that faces those who have moved to African countries is the lack of infrastructure to facilitate for them and citizens the movement of money between neighboring countries. Indeed, Africa has the highest remittances costs in the world. Based on statistics from the World Bank, it typically costs on average $9.10 to transfer $200, while the global average of $7.20. This is an important opportunity for us to tap into and improve a multi-billion-dollar money transfer problem between neighboring African countries. This wouldn’t just have a significant impact on the hundreds of thousands of Africans moving between countries in search of a decent living, but also for those traveling on short business trips. Not only does technology add convenience to the process but in Africa, it brings a layer of transparency to things like exchange rates which should have a significant impact and encourage more economically beneficial movement between countries. We project that OneWorldMessenger will have a strong impact across the globe and Africa may be one of the regions that will be most positively affected. Africa has a very weak banking infrastructure and very high costs of remittance. 20

European Union

Market Overview: Europe’s International Remittance Market is moderately concentrated and is

currently in the growth stage. The market includes both formal and informal payment service

providers including banks, money transfer operators, mobile wallets, and postal networks.

Prominent and major players are adopting new business strategies to adjust to the changing

world of remittance and to position themselves in this expanding market. Those strategies

include forming an extensive network with an expanded and improved reach, new services,

better pricing as well as more handy/transparent operations.

The market has been fueled by increased migration, increasing government support for new

competitors, improved banking knowledge and increased awareness towards digitalized

remittance services. Over the next 5 years, players have been expanding through acquisitions,

tie-ups, increased digital methods of money transfer and increased payout networks across and

outside Europe.

Market Size: The market has displayed steady growth in terms of transaction value, supported

by an increase in both inbound and outbound remittances. The total transaction value expanded

at an average growth rate of close to 4%. This was mainly fueled by a rise in the outbound

remittances, which is led by stronger growth in the employment prospects in the Euro area.

Moreover, the appreciation in the currency is also a contributing factor for such growth of

remittance in the region.

By Channel: Choice of a remittance channel depends on the ease of access for payer and

payee, cost involved, as well as the range of products and services offered. As of 2018, banks

dominate the inbound remittance market in terms of volume of transactions followed by MTOs,

m-wallets and other channels including postal networks, credit unions, and informal channels.

The outbound remittance market of the region is dominated by MTOs in terms of the transaction

volume as of 2018.

By Point of Contact: The inbound remittance market is dominated by branch pick-ups and

mobile & online transactions, followed by prepaid cards in terms of remittance transaction

volume.

21European Union By Major Inbound Remittance Countries: As of 2018, the top remittance receiving country in EU is Poland. The inflow is due to the high volume of remittance sent by the Polish emigrants from other countries to Poland as well as the remittance received from the family of foreign students in Poland. Poland is among the leading countries receiving remittance from within and outside European countries. Remittance has risen significantly in Poland over the last twenty years and now amounts to a noticeable share of the economy. Poland was followed by Portugal, Italy, UK, Romania, and other EU-28 countries. By Major Outbound Remittance Countries: The outbound remittance is dominated by France in terms of transaction value in 2018. Its leading position is directly related to the high number of the migrant population entering the country each year. It is considered one of the major destinations in Europe where people migrate in search of jobs and education. The major sending destinations from France are Morocco, Algeria, and Tunisia that are recipients to most of France’s flows. Other countries receiving important flows from France include China, Vietnam, Lebanon, and Senegal. Algeria, Comoros, and Madagascar rely greatly on France for remittances. France was followed by Spain, UK, Italy, Germany, and other EU-28 countries. By Corridors: Europe’s remittance corridor with Asia accounted for the highest share in the remittance market of the region in 2018. People from the Asian countries migrate to Europe due to the education, employment opportunities and living conditions in European countries such as Germany, UK, Spain, France, and others. Economic growth driven by revenues from oil exports and a shrinking domestic labor force has attracted millions of labor migrants. Competition Stage and Positioning: The European market is moderately concentrated with the majority of the market being captured by MTOs and Banks. There are 5 major MTOs in the market namely Western Union, MoneyGram, Ria Money Transfer, Transferwise and, UAE Exchange. Four major banks include HSBC Bank, Lloyds Bank, BNP Paribas and, Barclays Plc. The major m-wallet in the region is Xoom by Paypal. Major competing parameters for the entities include fees charged, transfer speed, services offered, reach of service providers, payout networks, technological advancements, promotional offers, and transparency in costs. Future Projections: The expected average growth rate is close to 4% for inbound remittance and about 7% for outbound remittance during 2018-2023.. 22

Oceania

Australia’s USD$7 billion plus remittance industry will continue to grow, driven by the influx of

migrants. According to a study by the Australian Centre for Financial Studies (ACFS), that market

still has an opportunity to improve costs and services to consumers through collaboration within

the financial services sector.

“Given that 70% of remittances go to developing countries and form a significant part of the

income of those nations, there is strong public interest as well as sound commercial reasons for

greater collaboration between banks and traditional money transfer organizations to reduce

the cost of transactions,” said Professor Ralston of the ACFS. Professor Ralston concluded: “The

Australian banking sector has the opportunity to expand its reach and revenue potential by

merging its technology with, and drawing on the significant resources of, MTOs to expand

services beyond its traditional national borders, particularly to those countries at the nation’s

doorstep.”

Australia is expected to continue to lead the way in the Oceana market, with a heavy focus on

building remittance channels between Australia and the booming economies of neighboring

Asia and its population of over 2 billion people. This market remains untapped with growth

expected at about 4 times that other regions in the world.

ACFS estimates the direct contribution remittances impact on the Australian GDP to be in the

range of AUD $336 million AUD $588 million per year.

GLOBAL WORKER TRENDS/COST

• The increasing globalization of the workforce means that millions of people are leaving their

home countries to work abroad. For these individuals, convenient and fast access to international

remittance services is important to support their families at home, particularly families in rural or

less developed areas.

• The high fees faced by migrants and others for sending money have been an issue of concern

for policymakers both in Australia and internationally. The very low fees offered by our system will

be a tipping point for our success in Oceania as well as other regions throughout the world.

23Oceania AUSTRALIAN BANKS • Banks transmit most international remittances through the SWIFT network in the form of transfers from one bank account to another and as international bank drafts, with funds delivered within a timeframe of one to three days. These remittances require a customer to have a bank account during the whole or part of the transaction cycle. • They also do not serve consumers, including their own account holders, who require end-to- end service to areas unserved or under-served by banks, or who need to send cash to recipients virtually instantaneously. MONEY TRANSFER OPERATORS • Specialist money transfer operators (MTOs) such as Western Union, MoneyGram, and a large range of smaller institutions and informal operators have developed the networks, technology, and skills to provide virtually instantaneous transfers of funds between individuals in remote parts of the region, including rural and less served areas. • MTOs lead transfers were the principal for remittances in the $1,000 to $5,000 USD range. Remittances higher than $5,000 are normally conducted through banks. Providing service at lower levels particularly in countries with poor financial services infrastructure is a resource- intensive and costly activity that banks have been unwilling or unable to provide. REGULATION • The Australian Government has taken a global leadership position in its response to the perceived risk of remittance transfers with the recently strengthened Anti-Money Laundering and Counter-Terrorism Financing Act (2006 – section 6). • The more stringent reporting and registration requirements coupled with the public availability of the register and enforcement of digressions suggest that Anti-Money Laundering and Counter- Terrorism Financing risks associated with compliant remittance service providers have been significantly reduced as a result of AUSTRAC’s actions. 24

Profit Potential

We are offering a very generous profit sharing formula to all MBIT holders. 40% of Messenger

Fintech profit will be disbursed back to token holders as profit sharing and an additional 30%

will be invested in marketing, advertising and further growing and improving our system and

network.

PROJECTED YEARLY USERS:

Based on our conservative projections and market studies, we expect our user base to grow

steadily.

First-year projections indicate that we will have about 15 million users.

2020 projections, about 17 million users for a cumulative number of 32 million users.

2021 projections, about 20 million users for a cumulative number of 52 million users.

2022 projections, about 25 million users for a cumulative number of 77 million users.

2023 projections, about 33 million users for a cumulative number of 110 million users.

2024 projections, about 60 million users for a cumulative number of 170 million users.

2025 projections, about 80 million users for a cumulative number of 250 million users.

25Profit Potential PROJECTED YEARLY REMITTANCE AMOUNT: Based on our conservative projections and market studies, we expect the following dollar amount of global remittance volume: First-year projections indicate that we will have about $54 billion in total remittance. 2020 remittance projections, about $61 billion; cumulative about $115 billion. 2021 remittance projections, about $72 billion; cumulative about $187 billion. 2022 remittance projections, about $90 billion; cumulative about $277 billion. 2023 remittance projections, about $118 billion; cumulative about $396 billion. 2024 remittance projections, about $216 billion; cumulative about $612 billion. 2025 remittance projections, about $288 billion; cumulative about $900 billion. 26

Profit Potential

PROJECTED NET PROFIT:

Thanks to our high tech and efficient fintech and blockchain system, we expect a highly

profitable operation. Our net profit projections:

First-year projections indicate that we will have about $130 million in net profit.

2020 remittance projections, about $147 million; cumulative about $277 million.

2021 remittance projections, about $173 million; cumulative about $450 million.

2022 remittance projections, about $216 million; cumulative about $665 million.

2023 remittance projections, about $285 million; cumulative about $950 million.

2024 remittance projections, about $518 million; cumulative about $1.47 billion.

2025 remittance projections, about $690 million; cumulative about $2.16 billion.

27The Process & System It only takes a few easy steps to get one of the most advanced bank cards on the planet: Users can easily find the closest loading point by simply logging into oneworldmessenger.io and finding the closest retail location on a map. An account holder will have a choice between one of the following fully functional permanent bank cards: Midnight Black Cobalt Blue • Cost: $200 (valid for three years, auto-renewal) • Cost: $50 (valid for three years, auto-renewal) • 2%Cash back on all purchases (paid in crypto) • 1%Cash back on all purchases (paid in crypto) • All basic features • All basic features • Individual withdrawal limit based on region • Up to $3000 withdrawal per month • $0.75 withdrawal free • $0.75 withdrawal fee 28

Regulations & Auditing Control

FINMA is a public-law institution in Switzerland which is the equivalent to the UK’s Financial

Conduct Authority (FCA). One of FINMA’s core objectives is to protect all clients of financial

institutions – creditors, investors and policyholders – against institutional insolvency,

disreputable business practices and to ensure equitable stock exchange execution. FINMA’s

mandate is to supervise banks, exchanges and securities dealers, and collective investment

schemes.

Messenger Fintech License Information

• MessengerFintech GmbH

• Limited Liability Company

• UID – CHE-101.029.610

• UID Status – ACTIVE

• UID Extension – HR/MWST

• VAT Number – CHE-101.029.610 MWST

• VAT Register Status – ACTIVE

• Reference Number – CH-170.4.002.326-5

• RC Status – ACTIVE

• Address: Blegistraße 25, 6340 Baar

• Online Verification Link: https://www.zefix.ch/en/search/entity/welcome

MessengerBank is the first decentralized bank and was established in 1999. With over 100

executive staff members, over 4 million customers in 63 countries worldwide. We are regulated

by FINMA, Switzerland’s governing body and independent financial-markets regulator. FINMA

is there to ensure that we meet all regulatory requirements at the highest level.

29Disclaimer And Investment Risks All investments is speculative in nature and involves substantial risk of loss. We encourage our investors to invest carefully. We also encourage investors to get personal advice from your profes sional investment advisor and to make independ ent investigations before acting on information that we publish. We do not in any way warrant or guarantee the success of any action you take in reliance on our statements or recommendations. Past performance is not necessarily indicative of future results. All investments carry risk and all in vestment decisions of an individual remain the re sponsibility of that individual. There is no guaran tee that systems, indicators, or signals will result in profits or that they will not result in losses. All investors are advised to fully understand all risks associated with any kind of investing they choose to do. Hypothetical or simulated performance is not indicative of future results. Unless specifically noted otherwise, all return examples provided in our websites and publications are based on hypo thetical or simulated investing. We make no rep resentations or warranties that any investor will, or is likely to, achieve profits similar to those shown, because hypothetical or simulated performance is not necessarily indicative of future results. Don’t enter any investment without fully understanding the worst-case scenarios of that in ‐ vestment. If you require any future information, please sign our standard Non-Disclosure-Agreement (NDA) and send it to us by email (ceo@messengerbank.io). All calculations and data presented within the MessengerBank publications and digital mar ‐ keting and media including but not limited to web sites, brochures, presentations and return models are deemed to be accurate, but accuracy is not guaranteed. The projected pro forma returns on investment are intended for the purpose of illus trative projections to facilitate analysis and are not guaranteed by MessengerBank, or its affiliates and subsidiaries. Past performance is not an indi cator of future results. The information provided herein is not in tended to replace or serve as a substitute for any legal, tax, or other professional advice, consul tation or service. The prospective buyer should consult with a professional in the respective legal, tax, accounting, or other professional area before making any decisions or entering into any con tracts pertaining to the property or properties de scribed herein. 30

List of Countries in Territory

Region 1: North America (504,000,000)

Region 2: Central America (84,397,000)

Region 3: South America (373,687,000)

Region 4: Europe (935,584,000)

Region 5: Asia (3,295,865,400)

Region 6: Africa (1,220,924,000)

Region 7: Australia & Oceania (65,892,000)

31Region 1 North America (504,000,000) U.S.A Canada Mexico Population: 2017 Estimate Population: 37,242,571 Population: 123,675,325 (11th) 327,167,434 (3rd) (38th) Presidential Democratic Federal Parliamentary Federal Presidential Constitutional Republic Constitutional Monarchy Constitutional Republic Remittance Outbound: Remittance Outbound: Remittance Outbound: $138,165,000,000 $655,000,000 $1,754,000,000 Remittance Inbound: Remittance Inbound: Remittance Inbound: $6,547,000,000 $881,000,000 $28,126,000,000 Markets: Upload Administrators Upload Administrators / POS: Upload Administrators / POS: / POS: The United States has Hypermarket/Supercenter/ FEMSA Comercio, S.A. de C.V., millions of POS locations to Superstore, Sobeys, Hudson Bay, Convenience/Forecourt Store; upload prepaid debit and credit CompanyMetro Inc., Overwaitea Beacon Payments, LLC , Labor cards. The infrastructure and Food Group etc. Unions, etc (Engaged with a facilities make it the #1 country number of large point of sale in the world for remittance. operators). Green Dot has partnered with OneWorldMessenger in the U.S., which is monumental news for the domestic remittance market. The bank card will be released July 2019 and the market will continue to grow as the OneWorld essenger’s ecosystem grows. The bank card can be utilized in a minimum of 180,000 upload points domestically and Messengerbank will be located in most big box stores including Walmart, 7-Eleven, Walgreens and CVS Pharmacy to name a few. 32

Region 2

Central America

(84,397,000)

Antiqua & Barbados Belize

Barbuda

Population: 100,963 (199th) Population: 285,709 Population: 374,681 (182th)

Unitary Parliamentary Unitary Parliamentary Unitary Parliamentary

Constitutional Monarchy Constitutional Monarchy Constitutional Monarchy

Remittance Outbound: Remittance Outbound: Remittance Outbound:

$5,000,000 $3,000,000 $3,000,000

Remittance Inbound: Remittance Inbound: Remittance Inbound:

$9,000,000 $61,000,000 $87,000,000

Upload Administrators / POS: Upload Administrators / Upload Administrators / POS:

Boutique and independent POS: Premium payout Premium payout locations

stores, coffee shops, cafes locations consist of Co- consist of Co-Operators and

will pick up most of the Operators and general general insurance, coffee

remittance exchange insurance, coffee houses, houses, boutiques and SurePay,

throughout this small boutiques and SurePay, Western Union

country. Western Union

Summary: Barbados

tourism continued to surge;

Barbados is reporting

453,645 stayover visitor

arrivals through

September, a 7.4 percent

increase compared to the

first nine months of 2017.

Greater tourism numbers is

a reason for larger

remittance numbers and

we expect Barbados to

grow in remittance.

33Costa Rica Cuba Dominica

Population: 4,857,274 (123rd) Population: 11,221,060 (82nd) Population: 74,000 (182nd)

Unitary Parliamentary Unitary Marxist–Leninist Unitary Parliamentary Republic

Constitutional Republic one-party Socialist Republic

Remittance Outbound: Remittance Outbound: Remittance Outbound:

$40,000,000 $1,000,000 $1,000,000

Remittance Inbound: Remittance Inbound: Remittance Inbound:

$368,000,000 $77,000,000 $12,000,000

Upload Administrators / POS: Upload Administrators / Upload Administrators / POS:

Premium payout locations POS: Only two American Cambio Man, Money Gram, JN

consist of Co-Operators banks are licensed to Money Transfer

Walmart, Auto Mercado, Mas X carry out transactions

Menos, Mega Super, Jumbo, with Cuban entities, the

and Pricesmart either accept Stonegate Bank and the

remittance or are gearing up to Banco Popular de Puerto

accept remittance. Rico (BPPR). Both banks

can issue MasterCard

cards to be used in point

of sale terminals in stores,

hotels and restaurants

operated by companies of

the Cuban state. They can

also be used to withdraw

money from ATMs

34Dominican El Salvador Grenada

Republic

Population: 10,735,896 (82nd) Population: 6,344,722 Population: 107,317 (185th)

(99th)

Unitary two-party parliamentary

Unitary Presidential Republic Unitary Presidential system under a constitutional

Constitutional Republic monarchy

Remittance Outbound: Remittance Outbound: Remittance Outbound:

$37,000,000 $11,000,000 $11,000,000

Remittance Inbound: Remittance Inbound: Remittance Inbound:

$4,088,000,000 $4,194,000,000 $1,200,000

Upload Administrators / POS: Upload Administrators / Upload Administrators / POS:

There are more than 294 POS: There are more than RENWICK THOMPSON AND CO

cash pickup locations 112 cash pickup locations LTD

available in Dominican available in El Salvador.

Republic. Cash is available to Super Selectos

collect from branches of Maxidespensa, Despensa

Banco Union, Banco BHD, de Don Juan, and

Banco Ademi, Cooperativa Despensa Familiar

San Jose, National including Western Union.

Association and Banco

Adopem, Carrefour

35Honduras Jamaica Nicaragua

Population: 9,112,867 (95th) Population: 2,890,299 Population: 6,167,237

Unitary dominant-party

Presidential Republic Unitary parliamentary presidential constitutional

constitutional monarchy republic

Remittance Outbound: Remittance Outbound: Remittance Outbound:

$7,000,000 $19,000,000 $8,000,000

Remittance Inbound: Remittance Inbound: Remittance Inbound:

$10,000,000 $1,737,000,000 $646,000,000

Upload Administrators / POS: Upload Administrators / Upload Administrators / POS:

Paiz, Banco Atlantida and POS: JN Money Transfer, Bancentro, Banco LaFise,

BAC, Banco Atlantida, Western Union, Teledolar, Western Union,

Western Union Moneygram, JMMB MoneyGram

Money Transfer, Alliance

Financial Services,

Victoria Mutual, Super

Plus Food Stores

36Panama Saint Kitts & Saint Lucia

Nevis

Population: 4,034,119 Population: 54,821 Population: 178,015

(209th)

Unitary presidential Federal parliamentary Unitary parliamentary

constitutional republic constitutional monarchy constitutional monarchy

Remittance Outbound: Remittance Outbound: Remittance Outbound:

$25,000,000 $2,000,000 $1,000,000

Remittance Inbound: Remittance Inbound: Remittance Inbound:

$402,000,000 $52,000,000 $13,000,000

Upload Administrators / POS: Upload Administrators / Upload Administrators / POS:

BAZ LOS ANDES, EKT POS: MoneyGram, Ria, MoneyGram, Ria, Western Union

CHORRERA, Western Union, Western Union

MoneyGram, Machitazo,

Conway, Price Smart Grocery

Store Chains

37Saint Vincent Trinidad & Grenadines & Tobago Population: 109,643 (196th) Population: 109,643 (196th) Unitary parliamentary Unitary parliamentary constitutional monarchy constitutional republic Remittance Outbound: Remittance Outbound: $1,000,000 $1,000,000 Remittance Inbound: Remittance Inbound: $15,000,000 $97,000,000 Upload Administrators / POS: Upload Administrators / MoneyGram, Ria, Western POS: MoneyGram, Western Union, WorldRemit Union, Xoom 38

You can also read