OUTLOOK 2021 MEDTECH COVERAGE - REPORT EXTRACT - Informa

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

December 2020 OUTLOOK 2021 MEDTECH COVERAGE REPORT EXTRACT

Early Cancer Detection: Will New Screening Technology

Disrupt Cancer Care?

Executive Summary Healogix; and Azra Raza, Chan Soon-Shiong

The emergence of multi-cancer blood tests for professor of medicine and director of the MDS

early detection is captivating investors and driving Center at Columbia University in New York City.

multi-billion-dollar acquisitions. Companies such Raza, an oncologist and researcher who has

as GRAIL, Thrive Earlier Detection and Guardant treated cancer patients for over 20 years, lost her

are predicting revolutionary change in the way husband, Dr. Harvey Preisler, director of the Rush

cancer is diagnosed and treated. The biggest Cancer Institute in Chicago, to lymphoma in 2002.

hurdle, however, may be coaxing health care He was 61 years old.

systems and health insurers to join the revolution.

Watch The Early Cancer Detection Panel

Discussion Here (22 October, 2020)

https://youtu.be/NK-nupn5f28

Early cancer detection diagnostics, along with

the success of anti-smoking campaigns, are the Raza, author of The First Cell: And the human

two biggest reasons for declining mortality rates costs of pursuing cancer’s last, published in

in cancer over the last several decades, even as October 2019, is an outspoken advocate for early

immunotherapies, precision oncology treatments cancer detection. “Early detection can be curative

and other innovations targeting late stage cancers for a lot of patients,” said Raza. Currently in the

are improving outcomes – to an extent. To truly US, “we are spending something like $27bn in

bend the mortality curve in oncology, early cancer screening measures, and we detect 9 million

detection is needed beyond the five cancer positive cases,” said Raza. “But of those 9 million,

types for which routine screening products and only 200,000 are real cancers, and 8.8 million are

national guidelines already exist: breast cancer, false positives. We need sophisticated molecular

cervical cancer, prostate cancer, colon cancer and and genetic markers for screening healthy

lung cancer in high-risk individuals, according individuals, to find illness before it has become a

to a growing number of clinicians and cancer bona fide clinical disease, and to prevent it. We

researchers, and early detection diagnostics are still using the old techniques of slash, poison

product developers. and burn [to treat cancer] and that has got to

stop.”

In late October 2020, In Vivo and MedTech Insight

convened a virtual panel to better understand the High false positive rates in single cancer detection

potential impact of early, multi-cancer detection may contribute to adoption and reimbursement

diagnostics, as well as the significant challenges barriers for emerging multi-cancer early detection

to broad adoption and commercialization. diagnostics, a situation similar to the way that

Panelists included Sam Asgarian, chief medical adverse immune responses to early cell therapies

officer, Thrive Earlier Detection; Helmy Eltoukhy, in the 1990s created a higher burden of proof for

CEO, Guardant Health; Harris Kaplan, managing the next generation of cell and gene therapies.

partner, Red Team Associates and CEO of Single cancer screening tests save lives, but they

2 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)

“focus on sensitivity, and give up on specificity, Early Multi-Cancer Detection

which leads to a lot of false positives,” Josh Ofman, Early studies point toward wider detection and

chief medical officer and external affairs at GRAIL, lower false positive rates with multi-cancer

an early cancer detection diagnostics company, screening technology, or ‘liquid biopsy,’ which

told In Vivo. “The efficiency to find cancer today is requires only a blood draw, instead of the

pretty poor. You’re spending most of your money standard tissue biopsy for making a cancer

on false positives; it can cost on average up to diagnosis. And the market for molecular

around $90,000 to $100,000 to diagnose a case of diagnostics in cancer is expected to grow

cancer today.” substantially in the next five years, according to

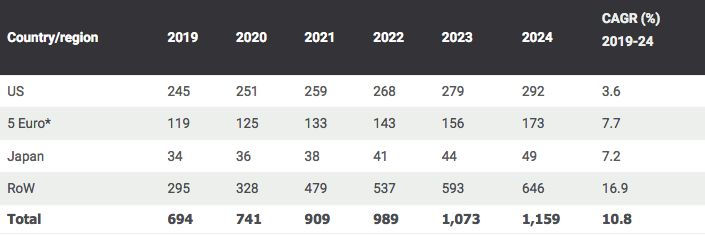

Meddevicetracker (see Exhibit 1).

Exhibit 1. Combined Market Forecast For Molecular Diagnostics Products ($m)

*5 Euro = five major European markets of France, Germany, Italy, Spain and the UK

Source: Meddevicetracker, ‘Molecular Diagnostics’ September 2020

Thrive Earlier Detection, which launched just In its interventional DETECT-A study, published

over a year ago with $110m in series A financing, in April 2020, Thrive screened 10,000 healthy

is developing the CancerSEEK liquid biopsy, a women aged 65 to 75 for multiple cancers, and

technology licensed in from Bert Vogelstein’s lab detected 26 previously unknown tumors among

at Johns Hopkins University. In October, Thrive the participants, or twice the number found with

was acquired for $2.15bn by Exact Sciences Corp., conventional screening. The two key outcomes of

a cancer screening and diagnostics company the study, said Asgarian, were to “detect cancer

marketing the Cologuard screening test for colon early enough so that the treatment is curative, and

cancer, as well as Oncotype tumor profiling tests to find of it we can do it in a safe way.” Notably,

that help guide treatment decisions for cancer cancer types with no currently approved screening

patients. test, such as ovarian cancer, were detected in the

study. There were 101 false positives. The study

3 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)

was a success, and Thrive now plans to “work example, physicians can evaluate those signals in

very closely with the FDA” to design a pivotal specific locations or regions, or refer the patient to

registration trial across multiple cancers. the appropriate specialist to the do the work-up.

“Right now, we practice sick care, secondary and

Primary Care Coordination tertiary care beyond the reach of primary care

GRAIL is also developing a liquid biopsy test for providers,” said Asgarian. With a simple blood

multiple cancers, called the Galleri test, capable draw, a primary care doctor can “work with the

of detecting over 50 cancer types at early stages. patients and population that he or she knows

Originally spun out of Illumina, a genomic so well. They are diagnosing diabetes, allergies,

sequencing company, in 2016, GRAIL attracting all these other diseases and illnesses, and now

high profile investors including Jeff Bezos and Bill they will have the tool and can do the same

Gates, as well as pharma companies including thing but apply it to cancer. Not to treat it, but to

Johnson & Johnson, Bristol-Myers Squibb coordinate the care and allow a specialist to see

and Merck & Co. In September 2020, Illumina it at an earlier stage where the treatment can be

announced that it would acquire the company curative.”

back for $8bn. Of the 50 cancers the Galleri test

can detect, 45 have no recommended screening, Guardant Health was founded in 2012 and taken

Ofman notes, adding that “70% to 79% of all public in 2018. The company’s Guardant360 liquid

cancer deaths in the US occur in cancers that don’t biopsy test has been validated by more than

have a recommended screening test at all.” The 150 peer-reviewed publications, and more than

FDA granted a breakthrough device designation 150,000 tests have been used to date. However,

to the Galleri test in May 2019, but the company the Guardant360 test is used for genomic profiling

plans to launch the product as a lab-developed in advanced cancer patients, to guide drug

test in 2021. Potential FDA clearance for the test is therapy decision-making. For example, it serves

still “a couple of years out,” said Ofman. as a companion diagnostic for AstraZeneca’s

non-small cell lung cancer drug Tagrisso

Studies conducted by GRAIL, including the STRIVE (osimertinib). Guardant360 is “able to detect

prospective study of 100,000 women receiving very low concentrations of cell-free DNA and

mammograms, the SUMMIT study of 25,000 men reconstruct the genomics of the tumor in those

and women ages 50 to 77 with a high risk of lung patients. Then we can match the mutations in the

cancer, and most recently, the investigational genome with the best possible therapies,” said

PATHFINDER study enrolling 6,200 patients and Eltoukhy, Guardant’s CEO. Guardant is currently

evaluating the impact of the Galleri test in clinical testing its LUNAR-2 assay in the 10,000-volunteer

practice, aim to demonstrate the utility of multi- ECLIPSE trial for the early detection of colorectal

cancer early detection. The PATHFINDER study is cancer. “When we started the company eight

important in that it addresses a needed shift to years ago, there was $90m total of NIH funding

primary care for early detection, and treatment for early detection, out of 10s of billions of dollars.

guidance, something GRAIL and Thrive see as the Now you see the funding rounds, with Thrive,

future. with other companies, with Guardant. It has

been gratifying to see that investors really do

Since the multi-cancer tests also predict a tissue appreciate the impact that early detection can

of origin, such as ovarian or head and neck, for have on this space.”

4 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)Reimbursement Challenges it comes to screening, I think payers are very

Despite the dazzle of early study results for multi- sensitive to paying twice.” For example, if a patient

cancer screening, real challenges exist in driving gets a positive result from an Exact Sciences

adoption and product reimbursement. Part of Cologuard test, which costs $600, the next step

the reason that Guardant is going after early is a colonoscopy to confirm the result. Even so,

detection of colorectal cancer in its ECLIPSE study, revenues for Exact Sciences’s cancer screening

is because the pathway to commercialization tests tripled between 2017 and 2019, according

has already been forged by companies like to Meddevicetracker. And more than 335,000

Exact Sciences and Cologuard. “The technology Cologuard tests were covered by Medicare in

is moving against reimbursement headwinds,” 2018, with payments of over $170m (see Exhibit

said Kaplan at Red Team Associates. “When 2).

Exhibit 2. Molecular Testing Services/LDT Market ($m)

Source: Meddevicetracker, ‘Molecular Diagnostics’ September 2020

5 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)Many companies are now working to develop for circulating tumor cells and they come and tell

early detection diagnostic technologies. But the me Dr. Raza, we are finding adenocarcinoma cells

extent to which new screening technology will hanging around in your blood, the next thing I’ll do

be adopted by the health care system, and how for myself is run to get a PET scan, and see which

quickly, remains an open question. There is a gland in my body is producing cancer,” said Raza.

pathway in colorectal cancer screening, paved by “Let’s say the PET scan comes back negative. Now

Exact Sciences, which “laid out the way to get into what do I do? How many times do I repeat this

clinician workflows, into screening guidelines, and blood circulating tumor cell test on myself? And

most importantly, to get reimbursement, because should I schedule another PET scan in six months?

we’re piggybacking on colonoscopy where It’s going to expose me to a lot of radiation. And

multiple studies have shown the med-health all these months I’m going to be very anxious.”

benefit … that helps thing move much more

quickly,” said Eltoukhy. Ultimately, however, detecting a cancer early

means there’s more chance to manipulate it to the

“I would say that 80% of the challenge is patient’s advantage, Raza believes. Earlier cancer

actually getting a technology that works into detection may also lead to better treatment

the health care system, changing the standard options, if screening tools are used for clinical

of care, changing clinician workflows, getting trial recruitment to investigate new therapies.

reimbursement, getting into [screening] guidelines “We think this is going to be really helpful for drug

… all of those things are frankly much harder developers who are trying to test the value and

and a much bigger expense” than technology effectiveness of their products in earlier stage

development, said Eltoukhy. “We’re starting cancers,” said Ofman. “The problem we have right

with a single cancer, but then we’re going to now is that we don’t detect very many early-stage

multi-cancer quickly, with liquid biopsy for the cancers, so it’s really hard for [biopharmaceutical

metastatic setting starting with lung cancer and companies] to study their drugs” in those cohorts.

then expanding horizontally from there to over a

hundred cancer types. We believe the same thing Screening Guidelines

can happen in early detection, but you really have Thrive and GRAIL would both like to see their

to pick your beachhead.” multi-cancer screening tools added to cancer

screening guidelines that already exist. “Once a

Companies such as GRAIL and Thrive may need year, if you’re over the age of 50, which means

more data, in the form of long-term, multi- you’re at an elevated risk of cancer, add a multi-

year studies, to demonstrate overall survival, cancer early detection blood test, so we can look

in order to get over reimbursement hurdles for all those other cancers,” said Ofman. “We’ll

and accelerate adoption of early detection for find some additional breast cancer, colon cancer,

multiple cancers. There is also the issue of positive others … but the majority of the value will be

early cancer results in healthy, asymptomatic finding cancers that we’re not currently screening

patients. Raza acknowledged that widespread for.”

multi-cancer screening would be very hard to

apply to the entire population right away. There According to Raza, the US health care system

is also the danger associated with a positive test does not have a choice about moving to early

screening. “If today I go and get my blood tested cancer detection, and away from the current focus

6 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)on extending life in advanced stages of cancer. with Simplistic clinical trials, and High fiscal cost. She uses the acronym “CRUSH” to describe the “It’s unconscionable that 42% of people who problem: Complexity of cancer addressed by are diagnosed with cancer lose every penny of Reductionist approaches, creating Ultra hype their life savings in two-plus years,” she said. “It’s about minor advances (in mouse models), paired obscene, and we shouldn’t be doing it.” 7 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)

One-Stop Shop: EU Devices And Diagnostics Regulatory

Outlook Through May 2021

Change, change and more change: Is timely compliance with the EU’s MDR

and IVDR still possible?

Executive Summary Eudamed medical device database and standards.

The end of the traditional EU holiday period is

nearing, and the pace of regulatory activity is The one-year delay to the full application date

expected to pick up sharply as September gets of the MDR to 26 May 2021 mean the problems

underway. What can medtech expect for the rest foreseen have been averted – for now.

of 2020 and into the first half of 2021, in these

unprecedented times? But the big question is whether these problems

will be solved by the one-year delay, or whether

they will they resurface again next May, when the

deadline hits.

During the first eight months of 2020, politics and

pandemic panic heavily influenced the regulatory MDR Delay

momentum of the medtech sector. Companies A delay in the full application of the MDR was

flexible enough and with sufficient resources to something industry had long lobbied for.

adapt to the changing demands and landscape The European industry association, Medtech

are most likely to weather these storms. But we Europe, was convinced that the sector was not

are constantly warned that not all will. Many feel sufficiently ready in the early part of 2020. And

battered by constant change and are unprepared. it was not alone; even representatives of EU

That is especially the case among SMEs, which competent authorities and the US Food and Drug

make up 90-95% of medtech companies. Administration had been adding their voice to

the plea for extra time. All feared that products

So where are we now? And how can industry best essential for health care would have to be pulled

prepare for nine months until 26 May 2021, the from the market on 26 May 2020.

date of full application of the EU Medical Device

Regulation (MDR)? But the European Commission was not convinced

by this argument; it continued to make plans

Firstly, it is worth remembering that up until late based around its original 2020 timetable,

April this year, the medtech sector was expecting confident its program of designating notified

the MDR to fully apply by 26 May 2020. bodies and posting MDR guidance documentation

would be sufficient for successful – even if not

If that had happened, many in the sector would fully complete – implementation to take place on

have experienced problems, some companies time.

even failing to be compliant in time because of

the lack of guidance and notified body capacity, It was not until COVID-19 struck and overwhelmed

and due to the ongoing absence of fundamental the devices sector that the priorities and ways of

elements of the infrastructure, such as the working of medtech stakeholders – authorities,

8 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)notified bodies and manufacturers, as well as the bodies are generally not taking place. This is

commission itself – had to shift. At this point, the placing obstacles in the way of notified bodies

commission conceded to the need for a one-year auditing products against the new MDR and

delay to the MDR, making the new deadline 26 IVDR – and this is likely to remain the status

May 2021. (Also see “EU’s MDR One-Year Delay quo for the near- to mid-term too, creating a

Now Official As Amending Regulation Is Published potential paralysis in certification against the

In EU Official Journal” - Medtech Insight, 24 Apr, MDR which is only nine months away; and

2020.)

• Dealing with COVID-19 products is going to

But the postponement is not the solution many continue to be a major feature of notified body

had wished it would be. This is for many reasons, work over the near future.

including:

In other words, it was COVID-19 and its challenges

• The one-year delay applies only to the MDR and that brought about the MDR’s one-year delay.

not the IVDR; But the problems around trying to address the

coronavirus crisis are also the most likely obstacle

• This means that there will be just one year to the successful full implementation of the MDR

between full application of the MDR on 26 May next May too.

2021 and the IVDR on 26 May 2022, putting

pressure on those players who have staff The EU seems to be on the brink of a possible

working on both, including at authority and even second wave as cases start to climb rapidly again

commission level: in many countries, such as France, Germany and

Spain, meaning that physical audits of and by

• The grace period, which allows many MDR notified bodies will continue to be impacted.

products, and some IVDR products, to remain

on the EU market until 26 May 2024 (where Virtual Audit Solution

compliant with the current medical device Indeed, for those new products that must comply

directives), has not been extended, meaning the with the MDR by 26 May 2021 that cannot

grace period will be three years, instead of four, benefit from the grace period and that need the

for products under the MDR and remain two for involvement of a notified body, EU rules require

those under the IVDR. So, auditing under the physical audits.

new regulations will need to be concentrated

into less time; But these are not taking place generally because

of COVID-19 social distancing rules and ongoing

• The Eudamed medical device database, a critical travel restrictions around the EU.

factor in transparency and traceability, is not

likely to be fully ready until 26 May 2022; There are cases where virtual audits are

permitted; but this is mainly for products that are

• Because COVID-19 has resulted in social already CE-marked under the MDD as well as for

distancing and travel restrictions, physical audits emergency products needed to treat patients with

of notified bodies by designating authorities COVID-19.

and physical audits of manufacturers by notified

9 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)The European Commission’s Medical Devices position paper stating that the medtech sector will

Coordination Group (MDCG), which supports the not derive any benefit from the one-year delay

commission with implementation, has issued because of COVID-19 travel restrictions and social

Guidance 2020-4 on permitting surveillance, distancing, which have made on-site audits nearly

recertification audits and audits triggered by impossible for now.

changes under the existing medical device

directives (the active implantable, medical device MedTech Europe says: “This leads to situations

and IVD directives) virtuall. But it does not really where manufacturers who aim to transition to the

address audits under the MDR, many of which are new regulations as early as possible are currently

likely to be initial audits. held back by notified bodies’ assumptions that

audits under the MDR/IVDR must be conducted at

This means that timely compliance for a whole the manufacturer’s premises, ie on-site…”.

swathe of innovative and often high-tech

devices will depend on how COVID-19 spreads Critical Documents And Planning

and on social distancing and travel rules; this Despite the obstacles for the sector in making

is particularly the case because it can take nine productive use of the MDR one-year delay,

months to be assessed and receive conformity there is some good news. The pace of guidance

assessment by a notified body – and there are being published has really stepped up and many

only nine months left until the MDR fully applies. more documents are in the wings and due to be

published soon.

Virtual MDR Initial Audits

While there are no signs yet of the European Guidance

Commission extending virtual audits to include There are now some 60 guidance documents

initial audits under the MDR, it acknowledges on the European Commission’s MDR guidance

that months of activity have been lost by notified webpage to support the implementation of the

bodies because of COVID-19, so it has put in place MDR, some of which has already been revised.

a series of measure to monitor device availability

to prevent or remedy potential device shortages. This guidance, most of which has been endorsed

by the European Commission’s Medical Device

In other words, while the date of application Coordination Group, supports the interpretation

has been delayed for a year, fears over devices of the MDR with respect to unique device

suddenly becoming unavailable have not gone identification (UDI); the Eudamed medical device

away, particularly given the current restrictions on database (Eudamed); the European Medical

notified body activities caused by the COVID-19 Device Nomenclature (EMDN); notified bodies;

pandemic. clinical investigation and evaluation; new

technologies; and other topics.

But while the commission is monitoring the

situation now and will over coming months, it has The European Commission also has a page on its

not responded to the plea made by industry for website detailing ongoing guidance development

MDR virtual audits to be allowed. within the MDCG subgroups, which was last

updated in July 2020. There are 42 items on this

This is despite MedTech Europe having issued a list with estimated dates of when the documents

10 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)will be endorsed by the MDCG. More Documents To Come

The European Commission’s MDR/IVDR Roadmap

While manufacturers and other stakeholders are gives an overview of all the work that has been

hungry for guidance to better understand how planned under the two regulations, along with a

to comply with the new regulations, far more high, medium or low priority grading.

guidance is being produced than had originally

been expected. Indeed, when the MDR and In early July this year, competent authority expert

IVDR were first drafted – accompanied by much Thomas W. Møller explained how work on a

astonishment at how much more detailed they third of the implementation tasks remained to

were than the directives –, the authorities argued be started. “Of the 165 separate items listed, 50

that existing guidance under the medical device have been completed, while 47 are ongoing and

directives had been absorbed into the regulations. 68 have not even been started yet,” Møller said

at that time. He is section manager of medical

But now the need for guidance to explain the devices at the Danish Medicines Agency, and

regulations has meant that a huge amount of newly elected as chair of the executive board of

additional guidance has been written, and much the EU’s CAMD (Competent Authorities for Medical

more is still being drafted. Devices) group.

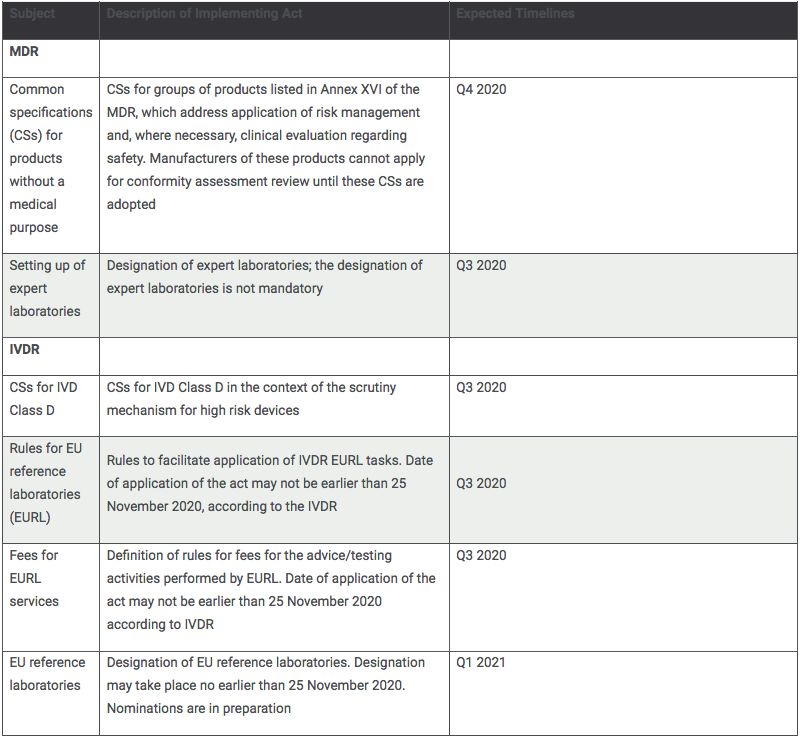

Implementing Acts Having these 165 activities ready for the 26 May

The MDR and IVDR foresaw that some of the 2021 MDR application date is just not tenable, he

regulations would need to be explained in told Medtech Insight in summer 2020. “We have

subsequent implementing or delegated acts. grouped these remaining activities as ‘necessary,

Drafting these acts is a lengthy procedure. While important, or nice to have,’ to create a prioritized

there are some 80 acts, 12 have been prioritized list moving forward towards the implementation

as needing to be ready by the time the MDR fully date,” he said at that time. (Also see “Competent

applies. Authorities Warn EU Industry Not To Expect All

MDR Implementation Tools In Time” - Medtech

But the only acts that are ready so far are: the Insight, 2 Jul, 2020.)

Commission Implementing Regulation on the

definition of the list of codes and corresponding The late timelines will be particularly tight for

types of device for specifying the scope of the much-needed common specifications,

designation of notified bodies, which was detailed technical requirements, which are being

adopted and published on 24 November 2017; developed, among other products, for medical

the Commission Implementing Decision on the devices without a medical purpose, known as the

designation of one or more entities to operate Annex XVI products. Annex XVI products include

the system for the assignment of unique device dermal fillers, liposuction equipment, breast

identifiers, published on 7 June 2019; and implants, skin resurfacing equipment and brain

the more recent Commission Implementing stimulation products.

Regulation on Common Specifications (CSs) for

the reprocessing of single use devices (SUDs). This means that these products, which are being

11 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)regulated for the first time at EU level, may The expected timelines for other much struggle to be compliant by 26 May 2021. Many needed documents under the MDR and IVDR of these products are coming under regulatory is being continually updated in the European control for the first time as they are not regulated Commission’s MDR rolling plan which is available nationally, so any delays leave patients exposed to via its website. risks that the commission, European Parliament and Council of the EU were keen to avoid by The expected publication date of implementing regulating these products under the MDR. acts with the highest priority are as follows: 12 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)

The IVDR As there has been a one-year delay to the date of

Although medical devices and IVDs are being full application of the MDR, the IVD industry is still

regulated under the same broad framework, the hopeful that it will benefit from the same kind of

sectors have their own EU regulation because of delay. It is also lobbying for a greater number of

the differences in the nature of the products and, IVDs to be able to benefit from the grace period.

therefore, require different approaches.

It is encouraged by the recent concession

So, while many of the problems that are besetting granted by the European Commission to class

the medical device industry which needs to I upclassified medical devices under the MDR,

comply with the MDR are also impacting the IVD which were latterly included in the list of products

industry, the IVD industry has its own challenges have been able, latterly, to benefit from this grace

in ensuring it is compliant by the IVDR full period in addition to other products already listed

application deadline of 26 May 2022. The scale in the original regulation.

of these is particularly great and there is growing

concern among experts in the industry that the Readers can expect strong lobbying to continue,

IVD industry is slow to understand the urgency in a bid to seek a “stay of execution” for these

with which it needs to begin compliance activities: products.

These are the some of the issues the IVD industry COVID-19 has had an enormous impact on many

is facing: manufacturers’ ability to transition to the IVDR

according to their original plans and timelines

• There has been no delay to the full date of Some companies who were as ready as they

application to the IVDR; it will now follow merely could have been at this stage in terms of IVDR

a year after the 26 May 2021 full application compliance have had plans their heavily impacted.

date of the MDR; This might have been, for example, because

audits cannot go ahead with their notified body or

• Some 85-90% of IVDs do not need the because they were expecting their notified body

involvement currently of a notified body under to be designated under the IVDR this year and the

the EU IVD Directive. But under the IVDR, about timeframes are no longer clear.

85-90% will, meaning a steep learning curve for

manufacturers and notified bodies alike and Many IVD manufacturers now have clinical studies

considerably more work; on pause too, because of COVID-19, and some

estimates suggest it could be nine months before

• Given that 85-90% of IVDs will need to involve a they can restart them. This obviously delays when

notified body for the first time, these products they can file for conformity assessment.

will not be eligible to benefit from the grace

period, which is two years for products under MedTech Europe is also frustrated that the

the IVDR where it applies; and EU chose not to opt for the possibility of pan-

European derogations from the need for full

• IVDs will be subject to performance evaluation conformity assessment procedures for IVDs

for the first time, the IVDR equivalent of clinical intended to help in the COVID-19 pandemic as

evaluation under the MDR. well as for medical devices, within the amending

13 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)regulation. This means that manufacturers must But industry said its own experience suggests

seek national derogations in every member state otherwise.

where their product is to be marketed and this

could cause them to prioritize the bigger markets. It is also noteworthy that there are already six

notified bodies based in Germany that have been

Notified Body Developments designated against the MDR and three in the

As of mid-August, there were now 20 notified Netherlands. But no other country has more than

body designations in total, 16 under the MDR one designation.

and four under the IVDR. These include two

designations for BSI UK – under the MDR and Questions arise over whether there is likely to

the IVDR. BSI is due to lose its designation status be a hiatus now in the nomination of notified

on 31 December at the end of the EU/UK Brexit bodies designated under the MDR and IVDR

withdrawal period, which means just 18 of the due to COVID-19 and due to the challenges for

current designations will remain valid from the joint assessment teams to carry out audits of

beginning of next year. notified bodies at a time when social distancing is

enforced.

The hope is that there will be more designations

in the meantime. But notified bodies cannot even Sources close to the commission told Medtech

begin testing under the MDR and IVDR before they Insight that the majority of current applications

are designated, so each day of delay could further have passed the on-site assessment stage, as

threaten their ability to finalize the conformity is indicated in the information on state of play

assessment of MDR products before the 26 May of the designation process presented recently

2021 deadline. There are, of course, many other to the European Commission’s Medical Device

factors that are compromising the likelihood of Coordination Group (MDCG) and stakeholders.

timely compliance (for example the appointment

of expert panels in the case of higher risk In other words, although the travel restrictions

products). imposed as a result of the pandemic have had an

impact on the scheduling of on-site assessments

The figure of 20 notified bodies under the MDR relating to the receipt of new preliminary

and IVDR compares with over 80 designations assessment reports (PARS) since the outbreak,

under the Medical Devices Directive at its height the subsequent steps of the designation process,

(there are 54 now), and 22 under the IVD Directive. for example, the review of the corrective and

preventive action (CAPA) plans, notification and

The European Commission had originally designation, have not been affected, and continue

promised 20 designations under the MDR and to progress.

IVDR by the end of 2019. But it has defended its

record by stating that the larger notified bodies Standards Request Rejected

were among the first designated and therefore In yet more news about delays in the

there has not been the kind of capacity issue infrastructure that is critical to the full

shortfall at notified bodies that such a number implementation of the MDR and IVDR, late June

would suggest. saw the European standards bodies CEN and

CELENEC reject the European Commission’s

14 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)already late standards request. While Eudamed 3 was intended for launch at the

same time as the full application of the MDR, the

The existing standards under the current medical database has been beset by the type of delay that

device directives need to be aligned with the new was predicted by many experts who cite historic

regulations so that industry can cite compliance problems with the vast majority of EU databases

with the updated standards as evidence that developed by the European Commission..

it should be in compliance with the General

Safety and Performance Requirements (the MDR The database is now due to go live in its entirety

equivalent of the MDD’s Essential Requirements). in May 2022. The notice to trigger the go-live will

be published in 2022, after a positive independent

It looks unlikely that a new standards request will audit to assess that Eudamed has achieved

be presented to CEN and CENELEC before the full functionality and meets the functional

first quarter of next year, meaning that one of specifications..

the cornerstones of the new EU medical device

regulations will simply not be ready on time. After much debate over whether individual

modules of the database could go live before the

EU medtech industry association MedTech Europe database goes live in its entirety, the commission

was already pre-empting the lack of availability of has now agreed that from 1 December this year,

standards earlier this year, and has come up with medtech manufacturers should be able to register

a pragmatic way forward based around existing – voluntarily – in the actor registration module.

standards.

Authorized representatives, importers, and

But with nothing yet official, industry is effectively system/procedure pack producers will also

in a legal limbo. be able to register from that date. The Single

Registration Numbers (SRNs), which each

The Eudamed Medical Device Database Eudamed user must have, are also due to be

Delayed available by then to support registration.

The new version of the European medical device

database, Eudamed 3, is being designed to So now, an important document to look

support the implementation of the MDR and IVDR out for during the third quarter of this year

and has six main modules: actor registration; is an implementing act providing detailed

unique device identification (UDI)/device arrangements for setting up and maintaining

certificate registration; notified body certificates; Eudamed 3, as well as news on other modules

clinical investigations; market surveillance; and going live early.

vigilance.

Expert Panels

It is a cornerstone of the new MDR and IVDR, Last month saw progress, at last, on the

providing critical transparency and traceability. Its appointment of members to the expert panels,

six main modules are interlinked and will provide with the aim of nominations being made public by

an unprecedented oversight of which products are the end of July.

on the EU market where, how they are performing

and how safe they are. These panels need to be in place for notified

15 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)bodies to be able to complete conformity time before certificates are issued, especially

assessment of certain high-risk devices. because notified bodies’ auditing activities are

being hampered by social distancing and travel

These panels have a variety of roles in supporting restrictions and they are only able to conduct

the more technical and product-specific aspects virtual audits.

of implementation, and need to be in place for

notified bodies to be able to complete conformity Guidance so far states that initial audits should

assessment of certain high-risk devices by generally not be carried out virtually but should

performing a review of the notified body clinical be conducted in person. (Also see “Manufacturers

evaluation consultation procedure (under the That Are Nearly MDR-Ready May Lose Their

MDR) and performance evaluation consultation Advantage Unless Audits Can Take Place Virtually”

procedure (under the IVDR) for certain high-risk - Medtech Insight, 7 May, 2020.)

devices, namely class III implantables and class

IIb active devices intended to administer and/ PRRC Challenges

or remove a medicinal product and Class D IVDs The challenges inherent in the new role, under

under the IVDR. the MDR and IVDR, of the Person Responsible for

Regulatory Compliance (PRRC) meant that the

The next step will be to establish expert panels launch of a not-for-profit European association

for the MDR’s clinical evaluation consultation representing those taking on this role in June

procedure and IVDR’s performance evaluation attracted a high level of interest.

consultation procedure.

The MDR and IVDR require that the supervision

Notified bodies that assess class III implantables and control of the manufacture and the post-

and class IIb active devices intended to administer market surveillance and vigilance activities

and/or remove a medicinal product should, of medical devices are carried out within the

except in certain cases, be obliged to request manufacturer’s organization, and also at the level

expert panels to scrutinize their clinical evaluation of authorized representatives and importers,

assessment reports and submit an opinion on by a PRRC, who, among other things, oversees

them. manufacturing.

The process, known as the Clinical Evaluation With many unknowns regarding new this role, a

Consultation Procedure (CECP), in the case of the new association, TEAM-PRRC, has taken on the

MDR, can take up to 60 days, and must happen remit of supporting its members by analyzing

before notified bodies are able certify new available relevant requirements and guidance

products as conforming to EU requirements. and trying to influence related developments.

It aims to promote greater security of the PRRC

Because of the delays in setting up the professionals themselves, given that the function

expert panels, there will now be a build-up carries considerable responsibility and potentially

of applications for clinical evaluation of these weighty personal liability.

innovative devices.

Brexit, Swixit and Turkey

It could therefore take some considerable It is already clear that the medtech sector has

16 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)some very big technical and political challenges most BSI UK medtech and IVD certificates have

ahead and is swimming in uncertainty and in been transferred. BSI Netherlands is designated

urgent need of greater clarity. against the medical device directives and the MDR

and IVDR. BSI UK had been among the first of the

But the political situations between the UK EU notified bodies to be designated under the

and the EU and between Switzerland and the MDR and the IVDR.

EU, as well as Turkey and the EU, have made

implementation of the MDR and IVDR even more Also announced by the MHRA is that there will

complex. be a new UK regulatory pathway and product

marking from 1 January 2021 for products being

The UK’s future regulatory pathway was still under placed on the UK market for those that wish to

discussion up until Medtech Insight was going use it. This will be enforced from 1 July 2023,

to press and a new announcement was made. when companies will have to meet new UK

This meant that it had been unknown whether requirements and place a UKCA mark on devices

the UK would essentially continue to falling into launched in Great Britain. (Also see “UKCA Mark

line with EU rules after 31 December and the Will Be The Post-EU Route To The British Medtech

end of the EU/UK Brexit withdrawal period, or Market In January 2021” - Medtech Insight, 2 Sep,

whether it would choose to apply its own rules or 2020.)

even associate itself with the rules of a different

market, like the US, for example. This means that there will be new rules that

industry will be able to choose to comply with, and

At last there are more clues about how the UK will these are still under discussion in the context of

move forward. The latest news, just published by the UK’s Medicines and Medical Devices Bill.

the UK regulator, the Medicines and Healthcare

products Regulatory Agency (MHRA), is that the UK From 1 January 2021, the MHRA will be able to

will continue to use and recognize the CE marking designate UK conformity assessment bodies

for medical devices and IVDs until 30 June 2023. (CABs) to conduct assessments against UK

Certificates issued by notified bodies based in the requirements for the purpose of the UKCA mark.

European Economic Area will, therefore, continue UK notified bodies, known as “Approved Bodies,”

to be recognized in the UK until that date. with designations under the MDD, IVDD or

AIMDD, will have their designations rolled over

This puts an end to the previous UK position, and automatically, without having to undergo a new

to concerns that if the UK still leaves the EU with designation process.

at the end of the year with no deal that EU notified

bodies and their certificates would no longer be Switzerland, meanwhile, is still trying to work out

recognized in the UK. the basis for its future relationship with the EU,

and indeed the UK. It currently has one notified

Ironically, this would have included the only body, SQS – Schweizerische Vereinigung für

remaining UK notified body, BSI UK. Qualitäts- und Managementsysteme, designated

under the MDD (although none under the IVD

This will be a welcome reprieve for BSI, although it Directive), and no new Swiss notified bodies are

had already set up a Dutch notified body to which expected to be designated under the new EU

17 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)regulations until the Swiss-EU mutual recognition Conclusion

agreement is finalized. So, in conclusion, the next nine months are

critical for the medtech sector. Is this a time

And, because of a similar political issues, no when as many obstacles as possible are going to

Turkish organization can apply to be a notified be removed so that the sector can focus whole-

body under the MDR or IVDR until the Turkish heartedly on compliance, rather than on the

customs agreement has been signed. This is politics and uncertainties?

a potentially big hit to notified body numbers,

as Turkey has five notified bodies under the Or are we now at a stage where deadlines are

MDD and one under the IVDD but none can be going to need to be continually put back while

designated under the IVDR or the MDR until the COVID-19 wreaks havoc on the industry?

Turkish customs agreement is finalized.

18 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)Calm Before The Storm – But Some Medtechs Already Reflect

The Ravages Of COVID-19

Executive Summary products and diabetes supplies and consumables

2019 saw fewer revenue-boosting major were in high demand, however.

acquisitions by top-tier medtechs. Companies that

reported after the calendar year-end were the first Managing through the coronavirus was a

to see the consequences of the pandemic on their challenge new CEO Geoff Martha would not

annual figures. have chosen, as he succeeded Omar Ishrak in

April 2020, also taking on the board chair role

in December. Marhta has quite an act to follow:

Ishrak, the group’s first non-American CEO, left

Our sales ranking of the top 100 publicly traded with a nine-year record of growing emerging

medtech manufacturers is COVID-19-affected markets, innovating and overseeing creative

for a relatively sizeable proportion of companies business models.

– those whose reporting periods closed during

2020. The effect of the pandemic on their sales But the group has not provided financial guidance

was often significant and gave a foretaste of what in Q4 2020, and will not Q1 of its fiscal 2021.

the rest of the industry will experience when filing

calendar year 2020 accounts. Among the leading 20 medtech companies,

only Cardinal Health, Inc., Becton Dickinson AB

The first implications of the pandemic became and Siemens Healthineers AG report later than

apparent for health care provider systems in Medtronic. The Japanese firms in the global top

countries beyond China at the end January 30, reporting on 31 March 2020, also saw the

2020, the global implications were clear by late initial effects of COVID-19 on their year-end sales.

February, and a pandemic was declared in mid-

March. Before the start of the second quarter, Other Top 100 companies already reporting

medtechs were in pandemic response mode, a coronavirus-related effect on annual sales,

and, depending on their product mix, were either include: ResMed, Inc., Elekta AB, Smiths Medical,

rushed off their feet or concerned about business LivaNova PLC, Cochlear Ltd., Cantel Medical

sustainability. Corp., Myriad Genetics, Inc., Abiomed, Inc.,

AngioDynamics, Inc., Accuray Incorporated and

Medtronic First Again, But In Another Sense Sectra.

Medtronic plc’s April 2020 year-end meant that a

full month of post-lockdown, coronavirus-affected Respiratory and sleep apnea group ResMed’s

business was reflected in its annual revenues. product mix helped ensure its sales to June

This group reported a 5.4% drop in annual sales 2020 rose by over 13%. But the group pointed to

(and a fourth quarter fall of 26%), bringing it another key factor that has been welcomed by the

below the $30bn threshold it had broken through global devices industry: the repeal on 1 January

temporarily in its fiscal 2019. Spine sales for the 2020 of the 2.3% excise tax on US device sales. In

year dropped by 5.7% and cardiac and vascular force since 2013, the tax was an element of the

sales were down by 9%. Extracorporeal life 2010 US Affordable Care Act that was designed to

support products, ventilators, pulse oximetry, support the cost of insurance expansion.

capnography, advanced parameter monitoring

19 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)On the diagnostics side of the industry, Myriad it normally files annual results after the Top 100

Genetics said it began to see a business impact is compiled. For 2019-2020, new CEO Tom Polen

from COVID-19 from the end of March. In early announced on 5 November 2020 that fourth

April, predominantly elective tests volumes quarter revenues were up 4.4%, driven by a 97%

(such as for hereditary cancer, potential drug rise in diagnostic system sales due to COVID-19

interactions and rheumatoid arthritis) declined by testing demand. Annual sales of $17.12bn were

70-75%, and prenatal tests by 20-25%. reported for the 2020 fiscal year.

In common with industry counterparts, the group Announcing its 2019 results, the word coronavirus

stopped in-office visits, restructured to ensure lab not yet uttered, the group issued guidance for

operation continuity, implemented cost-saving a 4-4.5% revenue increase in 2020. But as seen

initiatives, initiated furloughs and obtained a debt with Medtronic, once the crisis began, companies

covenant waiver until March 2021 from creditors. declined to issue guidance. As it transpired, BD’s

Towards the end of its fourth quarter, it began sales were 1% down in FY 2020. Its 2019 reported

to see a significant recovery, with test volumes sales were 5.2% up at $17.29bn, in a year when

averaging 75% of pre-pandemic levels it made no significant purchases, and when its

divisional sales rises were more in keeping with

Cardinal Health’s PPE Business Limits Negative traditional medtech market averages – BD Medical

Impact segment increasing by 5.2% to $9.1bn; and BD

Cardinal Health estimated that the COVID-19 Interventional up 5.2% at $3.9bn. Between fiscal

pandemic had a net negative operating earnings 2015 and 2019, BD’s M&A – including CR Bard in

impact of $100m across its pharma and medtech 2017 and CareFusion in 2015 – helped the group

segments in fiscal 2020. to expand by 68%.

Reporting on the year ended 30 June 2020, the Siemens’ Varian Purchase Offers Respite From

Dublin, Ohio group’s medical products segment COVID Gloom

saw lower sales volumes overall, apart from in Siemens Healthineers’ news in August 2020

PPE products, such as masks, gowns and gloves. that it would complete the €16.4bn purchase

Cardinal manufactures and distributes PPE. The of precision oncology systems company Varian

COVID-19 negative impacts will likely continue in Medical Systems, in H2 2021, provided a

fiscal 2021, the group said. distraction from the pandemic. But its Q3 2019-

2020 results delivered at the same time showed

The adverse effects of the pandemic were partially that diagnostic division sales were down by 15.9%,

offset by growth from Cardinal Health at-Home while imaging and advanced therapy revenues

Solutions, which distributes medical products were down by 3.3% and 1.8%, respectively.

to patients’ homes in the US. This limited the

group’s drop in annual sales to 1%. Cardinal’s Resilience (along with “uncertainty”) has become

range of products (syringes, incontinence, the word of a choice among medtechs whose

nutritional delivery, wound care, cardiovascular/ adjustments and efforts are helping to bring

endovascular, fluid suction, urology and OR them through coronavirus. CEO Bernd Montag

supplies) puts it in competition with, among employed the term accurately on 2 November

others Owens & Minor, Medline and Becton when reporting on a Q4 recovery, and annual

Dickinson (BD). sales for the 2019-2020 year that were down by

just 0.4% on a reported basis. The strengthening

BD’s reporting year ends on 30 September, and of the Euro currency by 5% against the US dollar

20 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)in 2019 worked against Siemens Healthineers growth of 10.5%. Its diagnostic sales increased by

in terms of its dollar-ranked sales and ranking 5.9%, excluding the impact of foreign exchange.

position in the latest Medtech Insight Top 100.

Mixed Fortunes In Orthopedics

And In BC (Before Coronavirus) Times J&J’s DePuy Synthes is the leading orthopedics

While coronavirus was not a factor for the global organization worldwide, but the only one of the

second-leading medtech group, Johnson & big four arthroplasty companies to record a sales

Johnson, its medical devices sales in 2019 dipped fall in 2019, its 0.5% reverse resulting from a

by 3.8%, only slightly less than industry leader negative currency impact of 1.7% which erased

Medtronic’s decline. Negative currency impacts operational growth of 1.2%. It had growth in

accounted for 2.1% of its sales fall. Its sales were hips, in knees (outside the US) and in trauma but

split fairly evenly among the US ($12.4bn) and underwent base business declines in spine.

OUS ($13.6bn) divisions.

Stryker’s reported sale rose by 9.4%, with spine

The divestitures of LifeScan and Advanced sales showing 31% growth, to top $1bn, and

Sterilization Products (ASP) had negative growth the neurotechnology/spine divisions posting

impacts of 3.8% and 1.6%, respectively. But there an increase of 19.2%, as reported. The larger

was growth in wound closure, hips, knees (in orthopedic and medsurg divisions posted

the OUS region), trauma and vision products. increases of 5.2% and 8.8% for the year, as

The standout was interventional products, with reported. The group completed $802m-worth

approaching $3bn of sales, driven by atrial (plus $294m contingent on future milestones

fibrillation procedure growth and catheter sales. being reached) of acquisitions. POC companies

Mobius Imaging and Cardan Robotics were

Royal Philips completed three acquisitions, bought for $360m plus $130m in milestones. They

including that of the Healthcare Information will join the spine business. In March, rotator cuff

Systems business of Carestream Health. Its gross tears specialist OrthoSpace Ltd was acquired for

revenue of €19.5bn (including license fees and $110m plus $110m milestones.

royalties) was 8% up on 2018 in local currency.

Connected care had a “challenging year,” with The November 2019 offer for extremities and

sales of €4.7bn. Diagnosis & treatment, at biologics specialist Wright Medical Group NV did

€8.5bn, saw improved revenues based on strong not trouble the annual sales compilers in 2019,

innovation flow in the delivery of precision as it was only approved by UK and US merger

diagnosis and targeted therapy. The group also authorities in November 2020. Wright was a

teamed up with US insurance company Humana, top 10 orthopedic manufacturer in the $53bn

to improve care for at-risk, high-cost populations. global orthopedics market in 2019. Its sales in

2019 were made in upper extremities ($448m),

GE Healthcare and Abbott Laboratories were level lower extremities ($340.5m), biologics ($113.5m)

pegging in 2019, at just under $20bn sales, but and sports medicine ($19m). The US market for

whereas GE had flat growth, Abbott continued surgical products used by extremities-focused

to expand, as in the previous two years, due to surgeons is valued at some $3.56bn, said Wright.

general volume growth and the 2017 acquisitions

of St. Jude Medical and diagnostics group Alere, DJO Global, the eighth-largest orthopedic

in particular. Diabetes care, structural heart, company in 2018, was acquired by Colfax for

electrophysiology and heart failure sales drove $3.15bn in February 2019, and became the

much of Abbott’s 2019 medical device segment fabrication technology company’s medical

21 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)technology segment. Purchasing the injury

prevention-to-rehabilitation group was part of There were no such immediate problems for

Colfax’s strategic plan to build a platform in high- fellow European group Roche, the global leading

margin orthopedics. Colfax’s net sales for 2019 diagnostics organization in an industry segment

from its new orthopedic segment were $1.1bn. where compliance with the EU’s “revolutionary”

Colfax said it had grown that business by over 4% Vitro Diagnostics Regulation is not enforced

since acquiring it. until May 2022. The Swiss group reported sales

of CHF12.9bn, an increase of 3% at constant

Zimmer-Biomet’s sluggish annual growth exchange rates, the growth coming mainly from

continued in 2019, when it scored a meagre centralized and POC solutions (accounting for

0.6% increase in overall sales (including dental, 60% of sales) and immunodiagnostics especially.

bone cement and office based technologies) But a modest 0.6% reported sales increase and a

after posting just 1.6% growth in 2018. The group strengthening of the Swiss franc meant its dollar-

is number 1 in both hips and knees globally ranked 2019 sales went backwards compared

(Source: Zimmer Biomet’s 10K). In February 2020, with 2018. Its molecular diagnostics sales were up

the group was forecasting up to 3.5% growth in 6%, due to increased demand in blood screening,

2020, but cautioned that this did not factor in while diabetes care sales increased by only 1%.

any impact from outbreaks of coronavirus and its

potentially “near-term and long-term effects.” A Year Of Difficult Performance Comparisons

In a year where organic growth was largely more

EU Regulations Ahead important than M&A-assisted growth for the

B. Braun, a top 20 global company and Germany’s leading medtech companies, sales performances

second-largest medtech group, increased its of the individual groups should in theory have

sales by 8.2% in 2019. Its orthopedic instruments provided more meaningful comparisons.

division, Aesculap, expanded its sales by

7.9%, driven by growth in China (especially in But against the backdrop of COVID-19, and

interventional therapies), the US (sterile goods factoring in the different reporting schedules

management) and Russia. The scheduled of many companies, analyzing their 2019

implementation of the EU Medical Device performances was, if anything, more difficult.

Regulation in May 2021 put a strain on sales, even The rankings for 2020 will be colored by the

if the “evolution” to the MDR, as the European entire industry’s struggles with the effects of the

Commission has described it, was delayed by a full coronavirus, even if those with certain product

year to spring 2021 as a result of COVID-19. offerings stand to gain from the pandemic.

To access the complete In Vivo Outlook 2021 Report

sign-up for a free In Vivo trial now

22 / December 2020 © Informa UK Ltd 2020 (Unauthorized photocopying prohibited.)You can also read