Page 1 of 19 - Singular Research

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Page 1 of 19

13th Annual Best of the Uncovereds2018

THANK YOU FOR ATTENDING & PARTICIPATING IN OUR CONFERENCE

Page 2 of 19

13th Annual Best of the Uncovereds 2018

Page 3 of 19

13th Annual Best of the Uncovereds 2018

“We invite companies for one reason and one reason only: Because we believe they can

generate Alpha for our clients, not because they will pay, not because it will do investment

banking deals.”

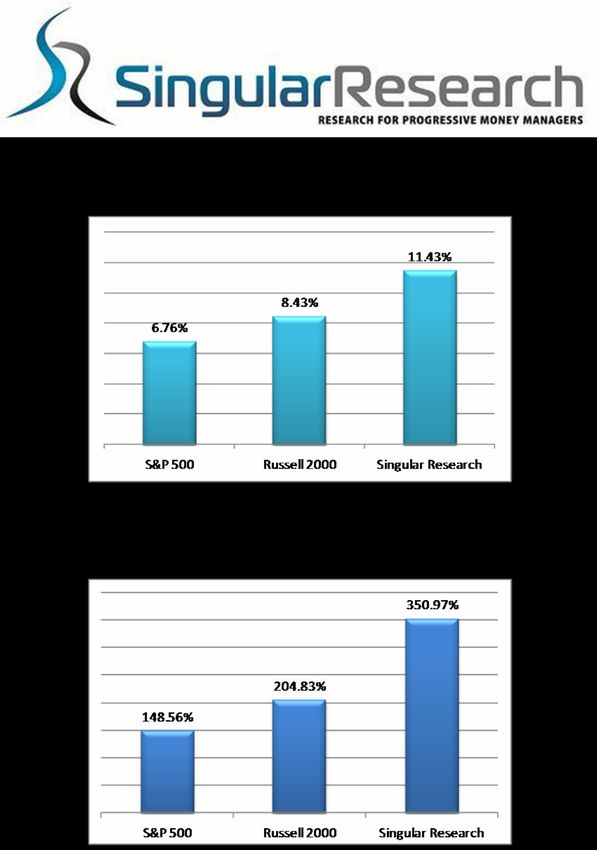

Last year at our Midwestern Values Conference you could hardly avoid making money.

• General Finance (GFN) + 208%

• Emergent Bio-systems (EBS) + 55%

• Kulicke & Soffa (KLIC) + 27%

• Bladex (BLX) -22%

• Aceto which we dropped -20%.

We believe we have some very strong Alpha generating candidates again this year.”

--- Robert Maltbie, CFA

President, Singular Research

Seeking Alpha is a crowd-sourced content service for financial markets.

Stock market Insights & financial analysis, including free earnings call transcripts,

investment ideas and ETF & stock research written by finance experts.

WHY SINGULAR RESEARCH?

• Unbiased Equity Research

• Focus on Uncovered Small Caps & Micro Caps

• Superior Track Record

• Experienced Staff of Analysts

• Attractive Value Proposition

• Superior ROI

• Great value!

Singular Express service is available for $99 month, with Seeking Alpha!

Singular Research Free Trial Subscription Link

https://seekingalpha.com/checkout?slug=singular-research

Page 4 of 19

13th Annual Best of the Uncovereds 2018

Page 5 of 19

Dallas Midwestern Values Conference 2018

Singular Research

22287 Mulholland Highway, #417

Calabasas, CA 91302

(818) 222-6234

www.singularresearch.com

ROBERT MALTBIE, CFA

PRESIDENT

(818) 222-6915

Robert@singularresearch.com

Alicia M. Velgos

Marketing and Public Relations

(818) 515-0344

Alicia@singularresearch.com

Tom Kill

Institutional Sales

(805) 260-4606

tom@singularresearch.com

Chris Saki,

CFA

Institutional

AnalystSales

(818) 222-6234

chris@singularresearch.com

Page 6 of 19

13th Annual Best of the Uncovereds 2018

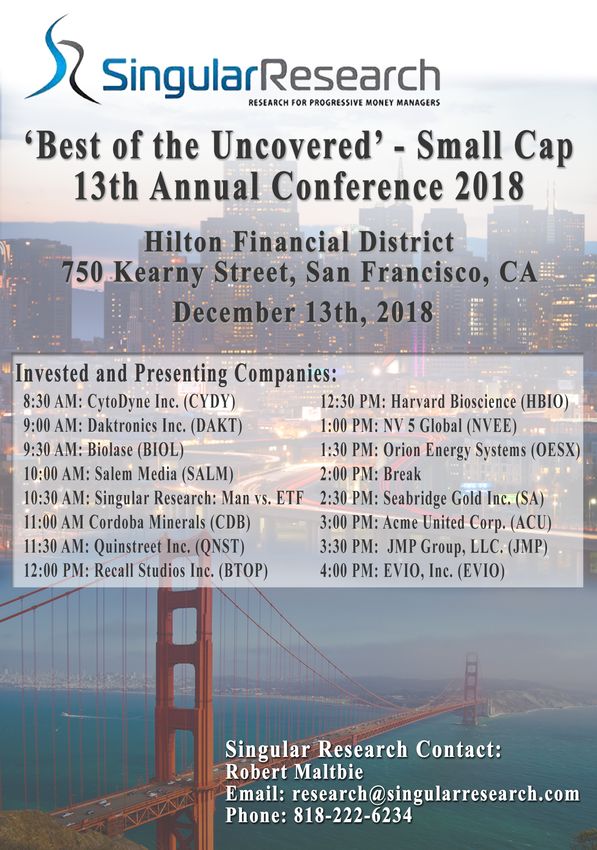

13th Annual Best of the Uncovereds

December 13th, 2018

Time Ticker Company Speaker

8:30 PST AM (11:30 AM EST) CYDY CytoDyn Inc. Dr Nader Pourhassan/ CEO

9:00 PST AM (12:00 PM EST) DAKT Daktronics Inc. Sheila Anderson/ CFO

9:30 PST AM (12:30 PM EST) BIOL Biolase John Beaver /CFO

10:00 PST AM (1:00 PM EST) SALM Salem Communications Corp. Evan Mayr/CFO

10:30 PST AM (1:30 PM EST) Singular Research: Man vs. ETF Robert Maltbie CEO

11:00 PST AM (2:00 PM EST CDB Cordoba Minerals Corp. Mario Stifano/ CEO & President

11:30 PST AM (2:30 PM EST) QNST Quinstreet, Inc. Gregory Wong/ CFO

12:00 PST PM (3:00 PM EST) BTOP Recall studios Inc. John C. Textor/ CEO

12:30 PST PM (3:30 PM EST) HBIO Harvard Bioscience Jeff Duchemin/CEO

1:00 PST PM (4:00 PM EST) NVEE NV 5 Holdings Michael Rama/CFO

1:30 PST PM (4:30 PM EST) OESX Orion Energy Systems, Inc Michael W. Altschaefl/CEO

2:00 PST PM (5:00 PM EST) Break

2:30 PST PM (5:30 PM EST) SA Seabridge Gold Inc. Rudy Fronk/CEO

3:00 PST PM (6:00 PM EST) ACU Acme United Corp. Walter Johnsen CEO

3:30 PST PM (6:30 PM EST) JMP JMP Group, LLC Joe Jolson/ CEO

4:00 PST PM (7:00 PM EST) EVIO EVIO, Inc. William Waldrop/ CEO

*5:00 PST PM --- Cocktails at Hilton FInancial

Page 7 of 19

13th Annual Best of the Uncovereds 2018

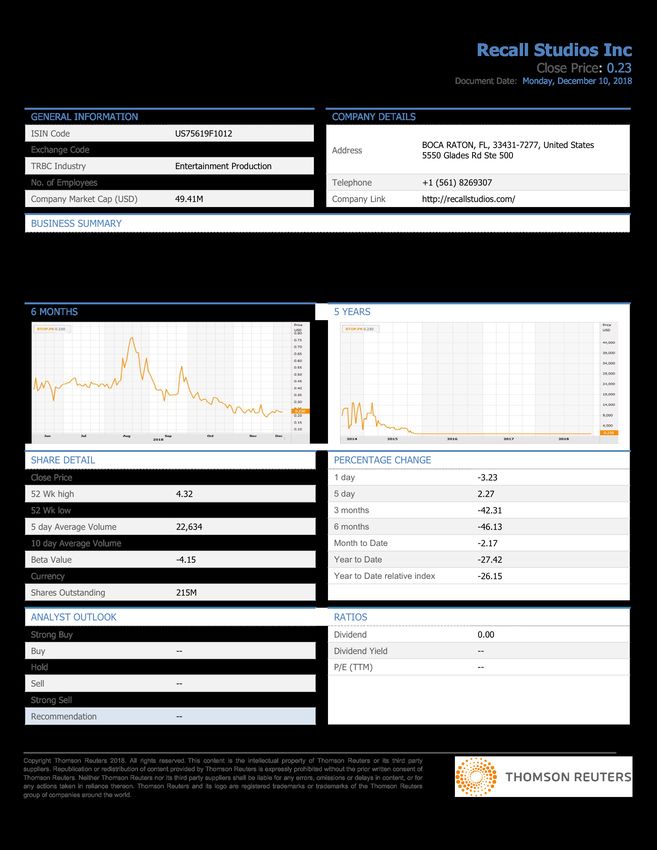

CytoDyn Inc

Close Price: 0.58

Document Date: Monday, December 10, 2018

GENERAL INFORMATION COMPANY DETAILS

ISIN Code US23283M1018

VANCOUVER, WA, 98660-2970, United States

Exchange Code OTC Address

1111 Main St Ste 660

TRBC Industry Biotechnology & Medical Research

No. of Employees 6 Telephone +1 (360) 9808524

Company Market Cap (USD) 147.34M Company Link https://www.cytodyn.com/

BUSINESS SUMMARY

CytoDyn Inc. is a clinical-stage biotechnology company. The Company is focused on the clinical development and commercialization of humanized monoclonal

antibodies to treat Human Immunodeficiency Virus (HIV) infection. The Company's lead product candidate, PRO 140, belongs to a class of HIV therapies known as

entry inhibitors that block HIV from entering into and infecting certain cells. The Company's product pipeline also includes Cytolin and CytoFeline. Cytolin is a mouse

monoclonal antibody developed to identify a specific type of immune cell called a cytotoxic T cell, or cytotoxic T lymphocyte (CTL). CytoFeline is an anti-lymphocyte

function-associated antigen-1 (LFA-1) antibody for the treatment of Feline Immunodeficiency Virus (FIV) infection. PRO 140 blocks HIV from entering a cell by binding

to a molecule called C-C chemokine receptor type 5 (CCR5). The Company has finished Phase II clinical trials for PRO 140 with demonstrated antiviral activity in man.

6 MONTHS 5 YEARS

SHARE DETAIL PERCENTAGE CHANGE

Close Price 0.58 1 day -2.75

52 Wk high 0.84 5 day -1.27

52 Wk low 0.40 3 months -4.51

5 day Average Volume 142,362 6 months 23.91

10 day Average Volume -- Month to Date 0.43

Beta Value 0.24 Year to Date 5.79

Currency USD Year to Date relative index 7.42

Shares Outstanding 258M

ANALYST OUTLOOK RATIOS

Strong Buy 0 Dividend 0.00

Buy 1 Dividend Yield --

Hold 0 P/E (TTM) --

Sell 0

Strong Sell 0

Recommendation Buy (2.00)

Copyright Thomson Reuters 2018. All rights reserved. This content is the intellectual property of Thomson Reuters or its third party

suppliers. Republication or redistribution of content provided by Thomson Reuters is expressly prohibited without the prior written consent of

Thomson Reuters. Neither Thomson Reuters nor its third party suppliers shall be liable for any errors, omissions or delays in content, or for

any actions taken in reliance thereon. Thomson Reuters and its logo are registered trademarks or trademarks of the Thomson Reuters

group of companies around the world.

Page 8 of 19

13th Annual Best of the Uncovereds 2018

c

h

r Daktronics, Inc. (DAKT)

December 10, 2018 DAKT reported better than expected Q2:19 revenues and EPS. We rate

se

a these shares Buy and maintain our $10 target price.

e Price (as of close on

R Dec 7, 2018)

52-Week Range $7.14 – $10.11 Total Debt $15.7 mil

ar

l $8.25 Shares Outstanding 44.9 million Debt/Equity 4.2%

u Insider/Institutional 18.5% / 56.7% ROE (LTM) 5.1%

g

ni Rating Public Float 36.8 million Book Value/Share $4.5

S Market Capitalization $375.5 million Daily Volume (3 mo. Avg.) 151,542

BUY

FYE APR FY 2018A FY 2019E FY 2020E

Price Target EPS ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Jul $0.19A $0.10A $0.10A $0.14E $0.10E

$10.00 Q2 Oct $0.16A $0.19A $0.19E $0.24E $0.23E

Q3 Jan ($0.14)A ($0.04)E ($0.05)E ($0.03)E ($0.02)E

Lisa Springer Q4 Apr ($0.09)A ($0.00)E ($0.01)E $0.01E $0.02E

818-222-6234 Year $0.12A $0.25E $0.24E $0.36E $0.34E

research@singularresearch.com P/E Ratio 67.1x 33.2x 23.3x

Change (%) -46.6% 101.6% 42.6%

FYE APR FY 2018A FY 2019E FY 2020E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Jul $172.7A $154.2A $154.2A $161.9E $161.9E

Q2 Oct $169.3A $172.7A $169.5E $181.3E $177.9E

Q3 Jan $130.3A $129.6E $145.9E $136.1E $153.2E

Q4 Apr $138.2A $149.2E $149.2E $156.6E $156.6E

Year* $610.5A $605.7E $618.8E $636.0E $649.7E

Change 4.1% -0.8% 5.0%

* Numbers may not add up due to rounding.

Q2:19 Highlights

Ø Q2:19 revenues were $172.7 million, up 2% YOY as a result of good performances

across the Commercial (+34.0% YOY), Transportation (+9.7% YOY), High School

& Recreation (+6.5% YOY) and International (+8.6% YOY) business units. DAKT

ended the quarter with a backlog up 6.4% YOY to $151 million.

Ø Q2:19 gross margins dropped 40 basis points to 24.8% from 25.2% in Q2:18

primarily due to higher commodity costs.

Ø Overall orders rose 6.4% and increased in the Commercial, High School Park and

Recreation and Transportation business units. Orders fell in the Live Events and

International business units.

Ø EPS improved 19% YOY to $0.19 in Q2:19 from $0.16 in Q2:18.

Ø Management expects modest sales declines in Q3:19, causing us to reduce our

Q3:19 EPS estimate.

Ø Management’s favorable comments regarding DAKT’s longer-term outlook are

reflected in our increased FY:20 EPS estimates. We rate these shares a Buy, and

reiterate our $10 target price, which implies capital appreciation potential of

approximately 20%.

Company Description

Daktronics, Inc. is the world’s leading PRIMARY RISKS

supplier of electronic scoreboards, large

electronic display systems, and digital Ø DAKT’s results can be negatively impacted by weak economic activity; rising

messaging solutions for use in sports, commodity input costs; timing of customer orders; foreign exchange fluctuations;

transportation, and communications.

and competitor pricing

Ø There are significant competitors in many of the firm's operating segments,

including large multi-nationals such as Mitsubishi and Panasonic, and DAKT may

Equity Research

lack resources to compete effectively.

Please refer to the end of this report to obtain important disclosure information.

Page 9 of 19

13th Annual Best of the Uncovereds 2018

Singular Research

Biolase (BIOL)

November 15, 2018 US laser sales improve 22% YOY. Sales efforts in southern CA

Price (as of close on produce 127% YOY laser sales growth in that market and BIOL

November 14, 2018) launches a similar regional initiative in Dallas/Fort Worth. We maintain

$1.24 our BUY Long-term rating and $4.00 buyout-based price target.

Rating 52-Week Range $1.53 – $3.05 LT Debt (millions) $0.2

Shares Outstanding 20.6 million Debt/Equity 0.01%

BUY Long-term Insider/Institutional 31% /35% ROE (LTM) NM

Public Float 14.4 million Book Value/Share $0.92

Buyout-based Price Target Market Capitalization $28.5 million Daily Volume 57.4k

$4.00 FYE DEC FY 2017A FY 2018E FY 2019E

EPS* ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar ($0.25) A ($0.23) A ($0.23) A ($0.18) E ($0.21) E

Lisa Springer Q2 Jun ($0.20) A ($0.20) A ($0.20) A ($0.11) E ($0.13) E

818-222-6234 Q3 Sep ($0.20) A ($0.19) A ($0.21) E ($0.15) E ($0.17) E

research@singularresearch.com Q4 Dec ($0.25) A ($0.16) E ($0.17) E ($0.11) E ($0.11) E

Year* ($0.90) A ($0.78) E ($0.81) E ($0.54) E ($0.62) E

P/E Ratio NM NM NM

Change

FYE DEC FY 2017A FY 2018E FY 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar $10.9 A $10.0 A $10.0 A $11.0 E $11.0 E

Q2 Jun $12.7 A $12.2 A $12.2 A $13.4 E $13.4 E

Q3 Sep $10.8 A $10.9 A $11.1 E $12.0 E $12.2 E

Q4 Dec $12.6 A $13.0 E $13.2 E $14.3 E $14.6 E

Year* $46.9 A $46.1 E $46.6 E $50.7 E $51.2 E

Change -9% -2% - 10% -

* Adjusted EPS. Numbers may not add up due to rounding.

Q3:18 Performance

Ø Q3:18 sales increase 1% YOY to $10.9 million as strong gains in US laser sales

are offset by lower sales of non-core imaging products. Excluding these non-core

products, revenues increase 9% YOY. US laser sales increase 22% YOY and

sales of consumable products rise 9% YOY.

Ø More than 62% of all-tissue laser sales made during Q3:18 were to new

customers, boding well for future recurring revenues from consumables sales.

Ø The Southern CA-focused marketing initiative continues to deliver strong results

Company Description with all-tissue later sales up 127% YOY in that market. BIOL measures success

Biolase (BIOL) is a world leader in by sequential and YOY sales growth, increasing customer awareness and new

customer captures.

the emerging market for dental

lasers. To date, the Company has Ø Late in Q3:18, BIOL rolled out a similar regionally-focused sales initiative in the

installed more than 33,000 dental Dallas/Fort Worth market, where more than 350 dental offices have already been

lasers in over 90 countries. visited by BIOL reps.

Compared to traditional dental Ø New CEO Todd Norbe shared a performance goal of BIOL turning EBITDA-

instruments, lasers cause less positive approximately four quarters from now in Q4:19.

trauma, pain and bleeding and Ø $12.5 million secured from a new term loan should provide sufficient funding to

improve patient outcomes. BIOL support BIOL’s operations until it meets its Q4:19 goal of EBITDA profits.

sells its dental lasers and related Ø The outlook for laser and consumable sales is improving, although BIOL remains

products direct in the US, Canada, several quarters away from profitable growth. We determine a price target based

Germany and India and through on BIOL’s value as a potential JV partner or takeover candidate. Our $4 price

target assumes a buyout of BIOL at roughly 2X revenues. We thus rate BIOL

Equity Research

distributors in other countries. The

shares BUY Long-term and reiterate our $4 price target.

Company is headquartered in

Irvine, CA.

PRIMARY RISKS

Ø BIOL has recorded consecutive years of net losses. We anticipate quarterly net

losses in FY:18 and FY:19.

Please refer to the end of this report to obtain important disclosure information.

Page 10 of 1913th Annual Best of the Uncovereds 2018

November 12, 2018

Salem Media Group (SALM)

Q3:18 operating income improves 25.4% YOY due mainly to

Price (as of close on expense declines on slight revenue gains. EPS rises to $0.05.

November 9, 2018)

Political ad spending likely to exceed $4 million for 2018. We

$3.05 maintain our Buy Rating and $6.00 price target.

Rating

52-Week Range $2.88 – $6.25 LT Debt (million) $240.2

BUY Shares Outstanding 26.3 million LT Debt/Equity 106%

Insider/Institutional 46% /40% ROE (TTM) 11.0%

12- Month Target Price Public Float 12.2 million Book Value/Share $8.61

$6.00 Market Capitalization $80.4 million Daily Volume (90 day Avg) 64.0k

FYE DEC 2017 2018E 2019E

EPS($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Lisa Springer Q1 Mar $0.04A $0.03A $0.03A $0.08E $0.08E

818-405-0242 Q2 Jun $0.05A ($0.08)A ($0.08)A $0.07E $0.10E

research@singularresearch.com Q3 Sep $0.00A $0.05A $0.09E $0.03E $0.07E

Q4 Dec $0.85A $0.07E $0.14E $0.06E $0.13E

Year* $0.94A $0.07E $0.19E $0.24E $0.38E

P/E Ratio 3.2x 43.5x 12.7x

Change 242%

FYE DEC 2017A 2018E 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar $65.0A $63.8A $63.8A $64.4E $62.5E

Q2 Jun $66.1A $66.3A $66.3A $66.9E $65.6E

Q3 Sep $65.4A $65.5A $66.1E $64.9E $64.87E

Q4 Dec $67.2A $66.5E $69.9E $65.2E $68.5E

Year $263.7A $262.1E $266.1E $261.4E $261.4E

Change -1% -1%

• Numbers may not add up due to rounding and may be pro-forma.

Q3:18 HIGHLIGHTS

Ø Total revenues rise 0.1% to $65.5 million as improvements in Broadcast

revenues offset flat Digital Media revenues and lower Publishing revenues.

Ø Broadcast revenues rise 0.8% YOY to $48.8 million. Same station Broadcast

revenues improve 1.9% YOY to $47.8 million and same station operating

income improves 2.3% to $12.1 million, marking the for the third consecutive

quarter of growth.

Company Description

Salem Media Group is America’s Ø Digital Media revenues remained flat YOY at $10.4 million. Publishing

leading Christian and conservative revenues drop 3.7% YOY to $6.3 million due to a reduced pipeline in the self-

multi-media company. The publishing business which SALM is in the process of rebuilding.

Company operates through Radio

Broadcast, Digital Media and Ø Corporate expenses decline 5.8% YOY to less than $4.0 million as a result of

Publishing segments. It owns and reduced spending for professional services and stock-based compensation.

operates 116 radio stations, many

in the top 25 media markets, and Ø Long-term debt declines to $240.2 million from $249.6 million at the beginning

produces several of the largest of this year.

nationally syndicated radio shows

Ø SALM records a Q3:18 EPS of $0.05 versus EPS of $0.00 one year ago. The

on the air today.

gain is due to higher revenues and lower corporate expense, which more than

Equity Research

offset increases in Broadcast expense and interest expense.

Ø We derive a $6 price target by applying a 0.7x P/B multiple to SALM’s book

value of $8.61 per share.

Please refer to the end of this report to obtain important disclosure information.

Page 11 of 1913th Annual Best of the Uncovereds 2018

NEED An update

BARRON’S

Q&A

2 Unloved Stocks to Buy And 3 To Dump (or

Short)

Millennium Asset's Robert Maltbie likes to buy hidden

gems and bet against overhyped growth stocks.

Robert Maltbie began his career as a retail stockbroker for Dean Witter and quickly learned

that there was more to job than understanding the nuances of buy and hold ratings. He saw

firsthand the inevitable conflicts of interest posed by investment banking, and came to

recognize the steep odds against individual investors.

So in 1999, he set out on his own, launching Calabasas, Calif.-based Millennium Asset

Management, specializing in smaller, underfollowed companies on the long side and bigger

companies on the short side. In 2005, he founded Singular Research, which now sells

small-cap research to Fidelity Investments and other big money managers. Four years ago,

Maltbie returned full time to his first love, managing money. Today, Millennium Asset

Management manages about $150 million, including a hedge fund called Argonaut

Partners, which began operations in 2005. Last year, Maltbie, 55, launched a mutual fund

called LoCorr Long/Short Equity I (ticker: LEQIX). Both buy undercovered smaller

companies that have historically traded at a 20% to 30% valuation discount and short mid-

to large-cap companies whose prospects Maltbie thinks are deteriorating. After a strong

performance out of the gate, the LoCorr fund is down sharply this year as investors sell off

smaller companies. Some of Maltbie's holdings also had growing pains, including Advanced

Emissions, the largest position in the LoCorr fund. But Maltbie is staying put in the sector,

arguing that eventually institutions will discover the charms of the names he owns, prices

will climb, and the companies will be added to the indexes. The LoCorr fund's longer-term

performance, he maintains, will rebound: Argonaut, which is almost "a mirror image," has

returned 11.3% a year since inception, versus 7.4% for the Russell 2000 and 0.53% for the

HFRX Equity Hedge index. As the market rises, Maltbie's research is also turning up a

number of short positions. To learn what they are, keep reading.

Analyst Bio

Name: Robert Maltbie Jr.

Age: 55

Title: President, chief investment officer, Millennium Asset Management, Calabasas, Calif.; Chairman, Singular Research

Education: B.A., political science, UCLA

Hobbies: Basketball, golf, movie going

Page 12 of 1913th Annual Best of the Uncovereds 2018

Page 13 of 1913th Annual Best of the Uncovereds 2018

c

rh QuinStreet Inc. (QNST)

Nov 8, 2018 The company announced better than expected revenue and adjusted

se

a EBITDA versus our estimates. We remain optimistic on QNST’s growth

e Price (as of close on Nov 7,

R 2018) prospects amid investments in new products and media strategies. The

ar

l $17.48 ongoing shift from traditional to digital ad spending is a secular trend and

u will provide a significant tailwind to QNST. We maintain our BUY rating and

g

ni Rating increase our target price to $20.00 per share.

S

BUY 52-Week Range $8.24 – $17.52 Total Debt $0.0 mil

Shares Outstanding 49.1 million Debt/Equity 0.0%

Price Target Insider/Institutional 11.4% / 87.6% ROE (LTM) 6.5%

$20.00 Public Float 42.5 million Book Value/Share $5.9

Market Capitalization $857.9 million Daily Volume (3 mo. Avg.) 761,938

FYE JUNE FY 2017A FY 2018A FY 2019E

Staff

EPS ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

818-222-6234

research@singularresearch.com Q1 Sep $0.01A $0.08A $0.08A $0.14A $0.10E

Q2 Dec $(0.04)A $0.07A $0.07A $0.11E $0.10E

Q3 Mar $0.06A $0.16A $0.16A $0.18E $0.21E

Q4 Jun $0.06A $0.13A $0.14A $0.20E $0.19E

Year* $0.11A $0.45A $0.46A $0.63E $0.61E

P/E Ratio 158.9x 38.6x 27.7x

Change 569.1% 311.5% 39.4%

FYE JUNE FY 2017A FY 2018A FY 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Sep $73.4A $87.4A $87.4A $112.8A $102.3E

Q2 Dec $65.6A $87.5A $87.5A $106.7E $94.4E

Q3 Mar $79.2A $117.9A $117.9A $129.7E $129.7E

Q4 Jun $81.5A $111.5A $97.0A $127.1E $127.1E

Year* $299.8A $404.3A $389.8A $476.4E $453.6E

Change 0.7% 34.9% 17.8%

* Numbers may not add up due to rounding.

* All numbers are non-GAAP.

Q1:19 Highlights

Ø Q1:19 revenues were $112.9 million, up 29% from Q1:18, on account of strong

performance across all business verticals.

Ø The Financial services client vertical represented 69% of Q1:19 revenues and

grew 32% YOY; the education client vertical represented 20% of Q1:19 revenues

and grew 24% YOY; the home services vertical and B2B technology sector

represented the remaining 11% of Q1:19 revenues and grew 22% YOY.

Ø Management sounded cautious regarding the Education vertical in the near term,

though their long-term outlook remains optimistic.

Company Description Ø Adjusted EBITDA in Q1:19 was $10.3 million vs. $6.5 million in Q1:18, an increase

of ~56% YOY.

QuinStreet Inc. specializes Ø Management expects FY 2019 revenue to be up at least 15 to 20% YOY and

in performance marketing adjusted EBITDA margin to expand to ~10%.

products and technologies. Ø We marginally adjust our estimates based on the quarter end results and

The company serves clients management commentary. We maintain our BUY rating and increase our target

in high-value, high- price to $20.00, with an implied capital appreciation potential of 14%.

consideration market

verticals, including financial PRIMARY RISKS

services, IT / technology,

home services and Ø Client concentrations remain a key risk. A loss of a key client or a failure to

education. renew a large contract could significantly impact financial results.

Ø A reduction in digital marketing spending due to an economic downturn could

negatively impact earnings.

Please refer to the end of this report to obtain important disclosure information.

Page 14 of 1913th Annual Best of the Uncovereds 2018

Page 15 of 1913th Annual Best of the Uncovereds 2018

Singular Research

Harvard Bioscience (HBIO)

November 6, 2018 HBIO delivers 15% YOY revenue growth and 33% gain in non-GAAP

Price (as of close EPS. The recently acquired DSI business was the primary contributor

on November 5, 2018) to sales growth, with DSI sales up 19% YOY. We reiterate our BUY

$4.06 rating and $6.50 target price.

Rating 52-Week Range $2.95 – $6.70 LT Debt (millions) $59.3

Shares Outstanding 37.3 million Debt/Equity 73%

BUY Insider/Institutional 13% /76% ROE (LTM) 8.7%

Public Float 32.0 million Book Value/Share $2.19

12- Month Target Price Market Capitalization $152.9 million Daily Volume 221.0k

$6.50 FYE DEC FY 2017A FY 2018E FY 2019E

EPS* ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar $0.02A $0.03A $0.03A $0.04E $0.01E

Lisa Springer Q2 Jun $0.03A $0.07A $0.07A $0.10E $0.08E

818-222-6234 Q3 Sep $0.03A $.0.04A $0.04E $0.06E $0.05E

research@singularresearch.com Q4 Dec $0.05A $0.07E $0.07E $0.10E $0.09E

Year* $0.12A $0.20E $0.20E $0.29E $0.23E

P/E Ratio 33.8x 20.3x 14.0x

Change 67% 45%

FYE DEC FY 2017A FY 2018E FY 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar $24.2A $27.7A $27.7A $28.5E $27.6E

Q2 Jun $25.2A $31.5A $31.5A $32.5E $32.5E

Q3 Sep $25.1A $28.6A $$29.6E $29.5E $30.0E

Q4 Dec $27.5A $32.0E $33.0E $33.0E $33.9E

Year* $101.9A $120.0E $120.8E $123.5E $124.5E

Change 18% - 3% -

* Non-GAAP EPS. Numbers may not add up due to rounding.

Q3:18 Highlights

Ø GAAP revenues improve 53% YOY. Non-GAAP revenues, which include

revenues generated by the divested Denville business, improved 15% YOY. The

acquired DSI business was the primary growth driver. Ex DSI, organic sales

declined 6% YOY.

Ø The electrophysiology business was the main reason for the organic sales

decline, which HBIO attributed to timing-related issues, with some anticipated Q3

Company Description

orders rolling instead into Q4, and some customers who have in the past ordered

Harvard Bioscience (HBIO) through the electrophysiology segment placing their orders instead through DSI.

develops, manufactures and

markets scientific equipment, Ø Reflecting the contribution from higher margin DSI products, non-GAAP gross

systems and consumables that are margins rose 920 basis points YOY from 46.6% to 55.8%. This is in-line with

used by thousands of researchers HBIO’s non-GAAP gross margin target of 54% to 57%.

worldwide. The Company was Ø DSI contributed approximately $11.2 million or 39% of Q3:18 revenues. The DSI

founded in 1901 by a Harvard business, which was acquired in January, improves the diversification of HBIO’s

Medical School professor and has customer base, contributes higher margin products and is expected to deliver

grown through a combination of between $2.5 million and $3.5 million of combined top-and-bottom-line synergies.

new products and acquisitions. Ø HBO launched product line extensions within its BTX and Harvard Apparatus

HBIO is headquartered in Holliston, brands and new DSI software enhancements during Q3. Several new

Massachusetts and has sales electrophysiology products are scheduled to launch at the Society for

and/or manufacturing operations in Neuroscience annual meeting in November. This is HBIO’s largest industry trade

the US and Canada, the UK, show.

Equity Research

Germany, Sweden France, Spain Ø We reiterate our BUY rating and target price of $6.50.

and China.

PRIMARY RISKS

Ø HBIO is a small player in an industry dominated by large global companies.

Ø The Company derives approximately 40% of revenues from outside the US and

is affected by foreign currency fluctuations.

Please refer to the end of this report to obtain important disclosure information.

Page 16 of 1913th Annual Best of the Uncovereds 2018

c

rh NV5 Global, Inc. (NVEE)

Nov 13, 2018 NVEE reports 14% increase in Q3:18 revenues and 9% adjusted EPS

se

a growth. High single-digit organic growth, a strong M&A pipeline and new

e Price (as of close on

R Nov 12, 2018) project wins position NVEE for continued robust gains. NVEE shares are

ar

l $81.10 up more than 50% YTD. We rate these shares BUY and reiterate our $100

u price target.

g

ni Rating

S 52-Week Range $40.01 – $96.70 Total Debt $35 million

BUY Shares Outstanding 12.5 million Debt/Equity 3.5%

Insider/Institutional 22.2% / 54.5% ROE (LTM) 14.1%

Price Target Public Float 9.9 million Book Value/Share $25.92

$100.00 Market Capitalization $1.0 billion Daily Volume (3 mo. Avg.) 81,061

FYE DEC FY 2017A FY 2018E FY 2019E

EPS ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Lisa Springer Q1 Mar $0.39A $0.59A $0.59A $0.70E $0.72E

818-222-6234 Q2 Jun $0.56A $0.91A $0.91A $0.94E $1.16E

research@singularresearch.com Q3 Sep $0.75A $0.82A $0.98E $0.98E $1.37E

Q4 Dec $0.71A $0.94E $0.86E $1.23E $1.23E

Year* $2.38A $3.27E $3.25E $3.84E $4.48E

P/E Ratio 34.1x 24.8x 21.1x

Change 55.9% 37.5% 17.5%

FYE DEC FY 2017A FY 2018E FY 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar $64.0A $94.5A $94.5A $115.3E $115.3E

Q2 Jun $83.7A $104.0A $104.0A $126.9E $126.9E

Q3 Sep $91.2A $104.2E $109.5E $127.1E $133.6E

Q4 Dec $93.9A $120.2E $108.0E $146.7E $131.8E

Year* $333.0A $423.0E $416.1E $516.0E $507.6E

Change 48.7% 27.0% 22.0%

* Numbers may not add up due to rounding.

* All numbers are non-GAAP.

Q3:18 Highlights

Ø Q3:18 revenues rise 14% YOY to $104.1 million, fueled by 8% organic growth

and contributions from recent acquisitions. The Company exited the quarter

with backlog up 24.6% YOY to $342.3 million and 8.6% higher sequentially.

Company Description NVEE targets FY:18 revenues 25-29% higher at $415-$430 million.

NV5 Global, Inc. is a provider of Ø EBITDA improved 10% YOY to $14 million and EBITDA margins were flat at

professional and technical engineering and

consulting solutions in the infrastructure,

17% in Q3:18 versus Q3:17.

energy, construction, real estate and Ø Adjusted EPS grew 9.3% YOY. NVEE is guiding for FY:18 adjusted EPS 36-

environmental markets. The Company’s

clients include the U.S. federal, state and 45% higher at $3.23-$3.43.

local governments, and the private sector.

Ø During Q3, the Company was awarded a $5 million contract with the New Jersey

Equity Research

DOT, a $10 million contract with the New York City DOT and a $20 million contract

with California Transportation District 10.

Ø NVEE continues to have plenty of acquisition candidates in the pipeline that can

expand its geographic footprint and service lines. The November acquisition of CHI

Engineering provides a strong platform for NVEE’s expansion in the LNG, LPG and

natural gas markets.

Ø We rate these shares BUY-Long-Term and reiterate our $100 price target.

PRIMARY RISKS

Ø An economic downturn could restrict the Company’s access to capital markets

and slow acquisition-related growth.

Please refer to the end of this report to obtain important disclosure information.

Page 17 of 1913th Annual Best of the Uncovereds 2018

Orion Energy Systems, Inc.

Close Price: 0.74

Document Date: Monday, December 10, 2018

GENERAL INFORMATION COMPANY DETAILS

ISIN Code US6862751087

Exchange Code NAQ MANITOWOC, WI, 54220-9662, United States

Address

2210 Woodland Dr

Electrical Components &

TRBC Industry

Equipment

No. of Employees 153 Telephone +1 (800) 6609340

Company Market Cap (USD) 21.28M Company Link http://www.oesx.com/

BUSINESS SUMMARY

Orion Energy Systems, Inc. is a designer and manufacturer of lighting platforms. The Company researches, develops, designs, manufactures, markets, sells and

implements energy management systems consisting primarily of commercial and industrial interior and exterior lighting systems, and related services. The Company

operates through three segments: Orion U.S. Markets Division (USM), Orion Engineered Systems Division (OES) and Distribution Services Division (ODS). The USM

division develops and sells its commercial lighting systems and energy management systems to the wholesale contractor markets. The OES division develops and sells

lighting products, and provides construction and engineering services for its commercial light emitting diode (LED) and high intensity fluorescent (HIF) lighting and

energy management systems. The ODS division focuses on selling its lighting products through manufacturer representative agencies and a network of broadline North

American distributors.

6 MONTHS 5 YEARS

SHARE DETAIL PERCENTAGE CHANGE

Close Price 0.74 1 day 1.02

52 Wk high 1.25 5 day -7.19

52 Wk low 0.68 3 months -20.59

5 day Average Volume 77,733 6 months -11.61

10 day Average Volume 53,610 Month to Date -2.50

Beta Value 0.15 Year to Date -15.62

Currency USD Year to Date relative index -16.42

Shares Outstanding 30M

ANALYST OUTLOOK RATIOS

Strong Buy 0 Dividend 0.00

Buy 1 Dividend Yield --

Hold 2 P/E (TTM) --

Sell 0

Strong Sell 0

Recommendation Hold (2.67)

Copyright Thomson Reuters 2018. All rights reserved. This content is the intellectual property of Thomson Reuters or its third party

suppliers. Republication or redistribution of content provided by Thomson Reuters is expressly prohibited without the prior written consent of

Thomson Reuters. Neither Thomson Reuters nor its third party suppliers shall be liable for any errors, omissions or delays in content, or for

any actions taken in reliance thereon. Thomson Reuters and its logo are registered trademarks or trademarks of the Thomson Reuters

group of companies around the world.

Page 18 of 1913th Annual Best of the Uncovereds 2018

Page 19 of 1913th Annual Best of the Uncovereds 2018

c

h

r Acme United Corp. (ACU)

November 6, 2018 The third quarter results were below our expectations with both revenue

se

a and EPS missing our projections. The management also lowered its 2018

e Price (as of close on Nov 5,

R 2018) guidance marginally. However, robust product pipeline and productivity

ar

l $17.75 initiatives gives us optimism for solid earnings growth beyond FY18. We

u maintain our BUY rating and lower our target price to $22.5 per share.

g

n

i Rating

S 52-Week Range $15.31 – $25.55 Total Debt $50.5 mil

BUY Shares Outstanding 3.4 million Debt/Equity 83.8%

Insider/Institutional 12.2% / 59.9% ROE (LTM) 6.4%

Price Target Public Float 2.9 million Book Value/Share $14.7

$22.5 Market Capitalization $60.3 million Daily Volume (3 mo. Avg.) 5,626

FYE DEC FY 2017A FY 2018E FY 2019E

EPS ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Jim Marrone, B. Sc., MBA, CFA Q1 Mar $0.18A $0.21A $0.21A $0.23E $0.25E

818-222-6915 Q2 Jun $0.75A $0.67A $0.67A $0.72E $0.75E

research@singularresearch.com Q3 Sep $0.32A $0.23A $0.36E $0.30E $0.54E

Q4 Dec $0.16A $0.18E $0.19E $0.24E $0.24E

Year* $1.42A $1.30E $1.53E $1.49E $1.78E

P/E Ratio 12.5x 13.7x 12.0x

Change -13.1% -8.8% 14.8%

FYE DEC FY 2017A FY 2018E FY 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Mar $27.7A $31.7A $29.8E $33.9E $33.9E

Q2 Jun $38.8A $39.7A $39.7A $40.9E $40.9E

Q3 Sep $33.8A $34.7A $36.3E $36.8E $38.6E

Q4 Dec $30.1A $32.5E $32.5E $34.5E $34.7E

Year* $130.5A $138.7E $140.3E $146.2E $148.2E

Change 4.8% 6.3% 5.4%

* Numbers may not add up due to rounding.

* All numbers are non-GAAP.

Q3:18 Highlights

Ø Q3:18 revenues were $34.7 million, up 3% from Q3:17, on account of strong

performance across US (+3% YOY), Europe (+2% YOY) and Canada (+2%

YOY). The results were driven by strong sales of first aid products, Camillus and

DMT sharpening tools.

Ø Online sales were strong in 3Q18 though slightly weak compared to previous quarters.

Online sales have increased in excess of 100% annually for the past three years.

Ø Gross Margins for Q3:18 were 36%, which was flat compared to 36% in Q3:17.

Ø Earnings per share in Q3:18 was $0.23 vs. $0.32 in Q3:17, a decrease of ~28%

YOY.

Ø The management guided for sales of ~$139 million, net income of $4.7 million

and earnings per share of $1.30.

Company Description Ø We lower our earnings estimates for FY:18 to $1.30 per share factoring in the

latest management commentary. We maintain our BUY rating and lower our

Acme United Corporation is one of the

largest worldwide suppliers of innovative

target price to $22.5, with an implied capital appreciation potential of ~26%.

cutting devices, measuring instruments

and safety products for the school, home, PRIMARY RISKS

office and industrial markets. The company

has facilities in the U.S., Canada, England, Ø ACU’s results can be negatively impacted by weak economic activity; rising

Germany, Hong Kong and China. Acme commodity input costs; timing of customer orders; foreign exchange fluctuations;

sells its products in countries. It had 421 and competitor pricing

Equity Research

employees at the end of 2017.

Ø There are significant competitors in the firm's operating segments, including

J&J and Fiskars, and barriers to entry are relatively low

Please refer to the end of this report to obtain important disclosure information.

Page 20 of 1913th Annual Best of the Uncovereds 2018

Page 21 of 1913th Annual Best of the Uncovereds 2018

c

h

r EVIO Inc. (EVIO)

October 4, 2018 EVIO announced subdued Q3:18 results with revenues decreasing 18.3%

se

a to $634,338 much below our estimates. However, we remain optimistic on

e Price (as of close on Oct 3,

R 2018) EVIO’s growth prospects amid the rollout of new laboratories and

ar

l $0.85 equipment upgrades at existing facilities. Favorable sector tailwinds

u (cannabis industry set to double by 2021) should drive growth as well. We

g

ni Rating maintain our BUY rating and lower our target price of $1.75 per share.

S

BUY 52-Week Range $0.47 – $2.70 Total Debt $4.2 mil

Shares Outstanding 22.8 million Debt/Equity 20.6%

Price Target Insider/Institutional 19.9% / 0.0% ROE (LTM) (288.7%)

$1.75 Public Float 20.0 million Book Value/Share $0.21

Market Capitalization $20.3 million Daily Volume (3 mo. Avg.) 139,749

FYE SEP FY 2017A FY 2018E FY 2019E

Staff

EPS ($) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

818-222-6234

research@singularresearch.com Q1 Dec $(0.09)A ($0.04)A $(0.04)A ($0.04)E ($0.01)E

Q2 Mar $(0.06)A ($0.05)A $(0.05)A ($0.04)E ($0.04)E

Q3 Jun $(0.05)A ($0.11)A $(0.05)E ($0.04)E ($0.04)E

Q4 Sep $(0.17)A ($0.04)E $(0.05)E ($0.04)E ($0.03)E

Year* $(0.37)A ($0.25)E $(0.19)E ($0.16)E ($0.12)E

P/E Ratio NM NM NM

Change -25.4% -31.4% -35.0%

FYE SEP FY 2017A FY 2018E FY 2019E

Revenue ($ mil.) ACTUAL CURRENT PREVIOUS CURRENT PREVIOUS

Q1 Dec $0.7A $0.9A $0.9A $1.6E $1.6E

Q2 Mar $0.8A $0.7A $0.7A $1.2E $1.2E

Q3 Jun $0.8A $0.6A $1.7E $1.0E $2.9E

Q4 Sep $0.7A $1.5E $1.5E $2.5E $2.5E

Year* $3.0A $3.8E $4.8E $6.4E $8.4E

Change 438.5% 26.2% 69.9%

* Numbers may not add up due to rounding.

* All numbers are non-GAAP.

Q3:18 Highlights

➢ Q3:18 revenues were $634,338, down 18.3% from Q3:17, on account of subdued

performance of testing services segment. Testing service segment revenues were

down 22.4% to $595,701. While consulting services segment was up ~313.5% to

$38,637.

➢ EVIO suffered a gross loss of $195,113 in Q3:18 vs. gross profit of $122,954 during

Q3:17. This was primarily attributable to lower revenues and higher cost of revenue.

➢ EVIO was focused greatly on broadening its footprint. The company expanded its

presence in California by acquiring additional labs as well as have plans to open

Company Description two more labs in the region by the end of 2018.

EVIO Inc. is a leading provider of quality ➢ EVIO invested heavily in new equipment upgrades at its labs which should result

control testing, consulting and advisory in increased testing volumes and higher operating efficiency.

services to the cannabis industry. The ➢ The management does not provide any guidance, though company’s CEO, Mr.

company owns 9 laboratories serving five William Waldrop sounded optimistic about the growth in 2018.

states in the US – California, Colorado,

Massachusetts, Oregon and Florida.

➢ We adjust our estimates based on the results and management commentary. We

maintain our BUY rating and lower our target price of $1.75, with an implied capital

appreciation potential of 97%.

Equity Research

PRIMARY RISKS

➢ Delay in executing the planned expansion or improvement projects at its

properties remains a concern

➢ The growth of cannabis testing market is subjected to favorable regulatory

environment. Any adverse regulation could materially impact growth trajectory.

Please refer to the end of this report to obtain important disclosure information.

Page 22 of 19Dallas Midwestern Values Conference 2018

Conference

Personal Notes Section

THANK YOU FOR ATTENDING & YOUR PARTICIPATION

Page 23 of 19Dallas Midwestern Values Conference 2018

22287 Mulholland Highway, #417

Calabasas, CA 91302

(626) 405-0245

www.singularresearch.com

Page 24 of 19You can also read