Portfolio Strategy October 2020 - BMO.com

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

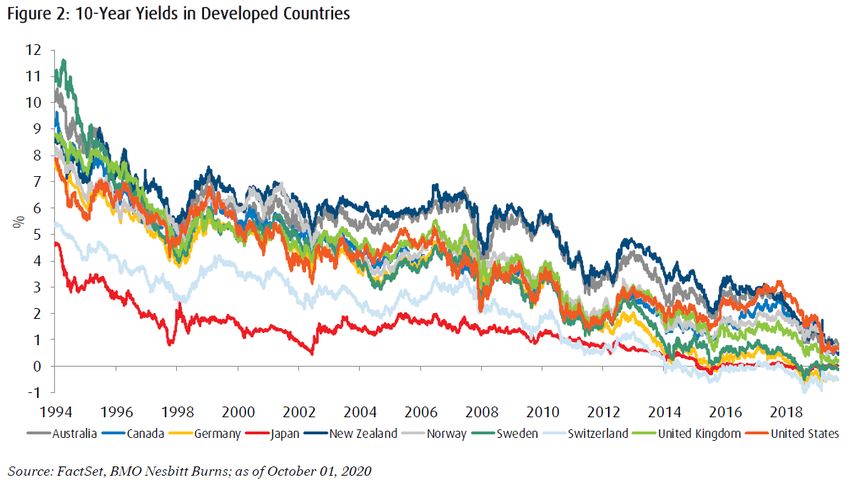

Portfolio Strategy October 2020 The following paragraphs are from the publication of Portfolio Strategy and Fixed Income Strategy August 2020, published by Stephane Rochon, CFA and Richard Belley, CFA. Equity and Fixed Income Strategy October 2020: Lower Rates Highly Supportive for Stock Market Investors have many concerns these days including rising COVID-19 cases which are leading to fears that a dreaded “second wave” is upon us. There is also the upcoming U.S. Presidential Election. The train wreck that was the first Trump/Biden debate certainly did not help ease concerns from that perspective. And yet, we believe the market will remain well-supported through year-end. This may seem like rose colored optimism to some but we believe that the most important variable for the market is the level and trajectory of interest rates, and the outlook remains very positive on that front. History solidly supports our view and we have the data to prove it. As every seasoned investor intuitively knows, lower rates are generally a good thing for stocks. A notable exception to this rule is when they signal a deflationary spiral -a la Japan- but this has been exceedingly rare in the last two centuries of economic history. Just how good they are for equity performance may, however, come as a surprise to many and that is what we address below with a number of tables and charts. Given long term interest rates are converging toward zero in North America and across developed countries, this has very positive implications for the huge real estate market (approximately 20% of the Canadian and U.S. economies), for the cost of financing for companies and governments, and for the relative value of stocks (e.g. a growing 2%+ stock dividend yield compares very favourably to a fixed 0.55% 10 year Government of Canada yield).

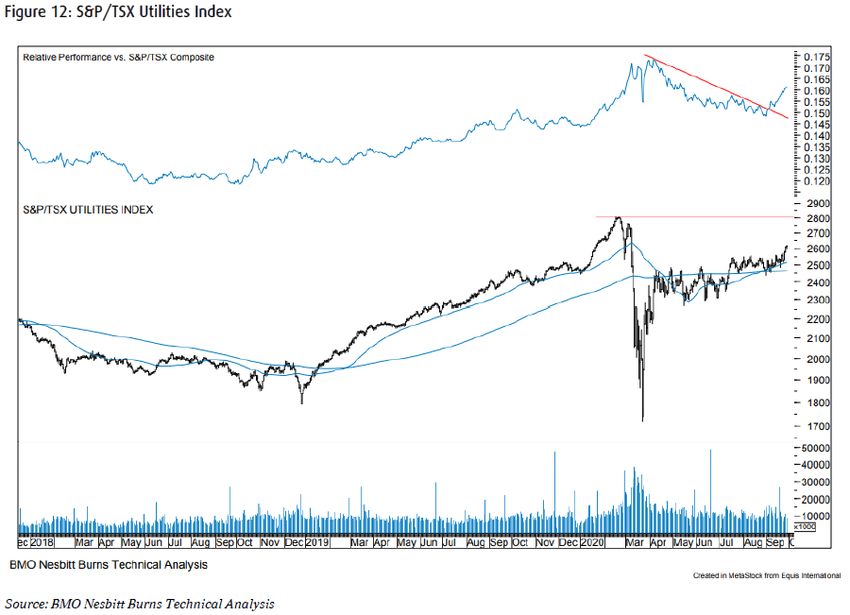

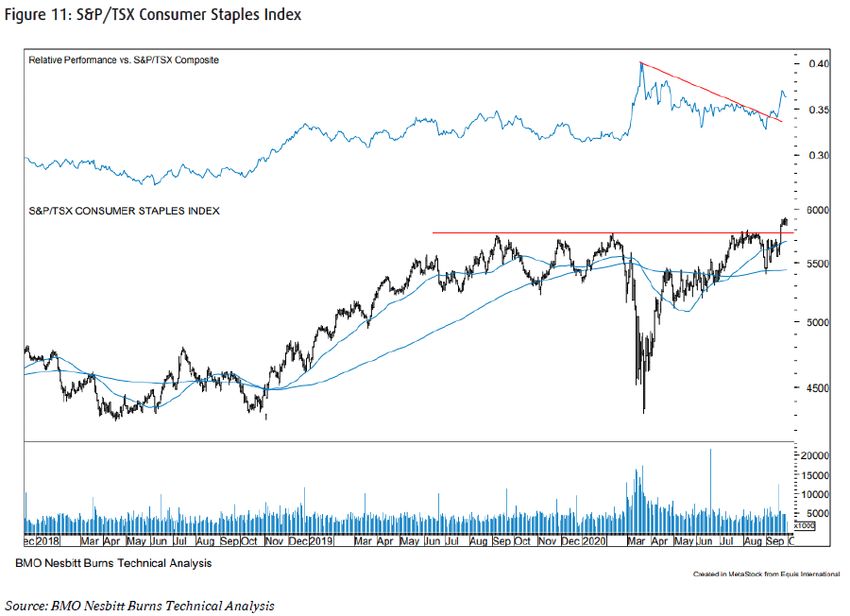

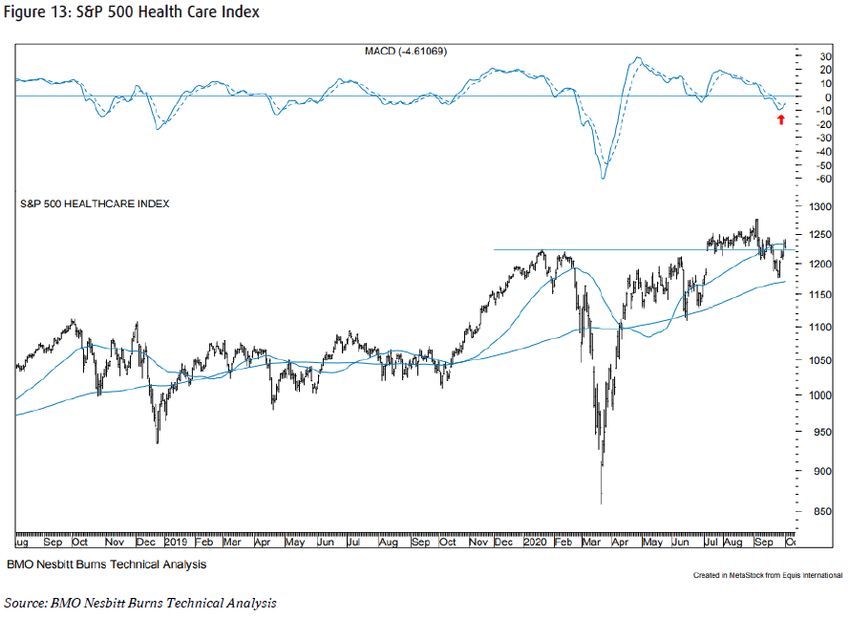

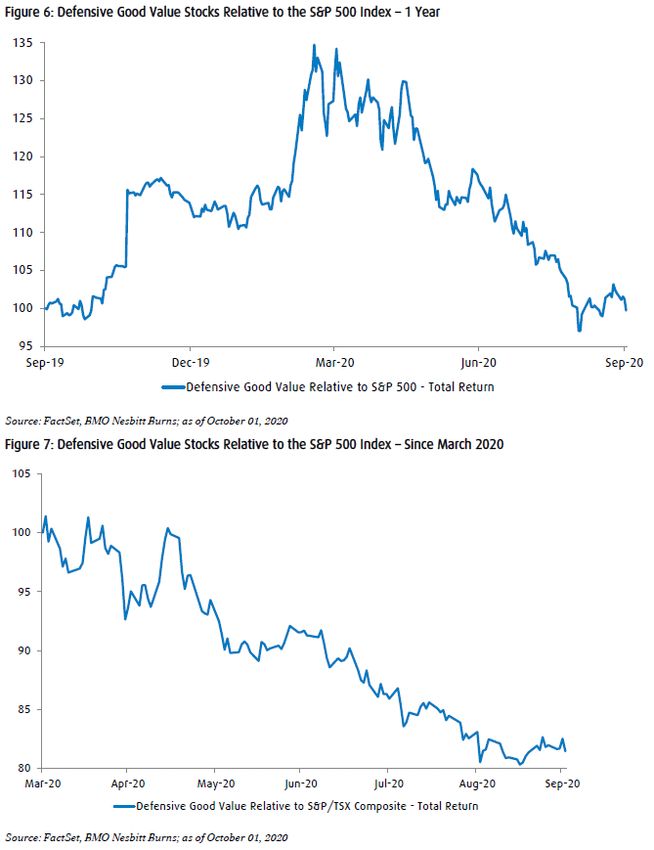

Despite our bullish stance, in August we advised investors to be selective. We remain concerned about the very high valuation of “long duration” growth stocks - particularly in the technology sector - which have benefitted disproportionately from investment flows. But, given the massive discrepancy in performance between sectors and value versus growth stocks, attractive opportunities still exist, for example in defensive and stable sectors such as Utilities, Consumer Staples, Health Care and Multi-Family REITs. The chart below illustrates our point with the TSX High Dividend Index underperforming the TSX by a massive 15% year to date. The top 10 largest holdings include well-known banks, pipelines/energy stocks and telecom companies (e.g. Enbridge, RBC, BCE, Telus, TD .etc.) which have historically performed well. Not so far in 2020, however. However, the timely opportunities we see are not currently in Banks, Pipelines or Telcos. Rather, we would focus on traditional Utilities, Consumer Staples, Health Care and apartment REITs (please refer to positive technical analysis comments on these sectors below). The common thread between these stocks is that they have solid defensive business models, strong balance sheets, high and growing dividends with very reasonable valuations relative to rock bottom interest rates. Additionally, after holding in well during the worst of the COVID-19 market panic, they have substantially underperformed in the last 6 months, hence we believe the entry point is attractive.

Lower Rates Versus Market and Sector Returns: A HUGE Positive Historically Our research partners at Ned Davis Research conducted an analysis of market performance going back to 1959. What we notice immediately is that the current

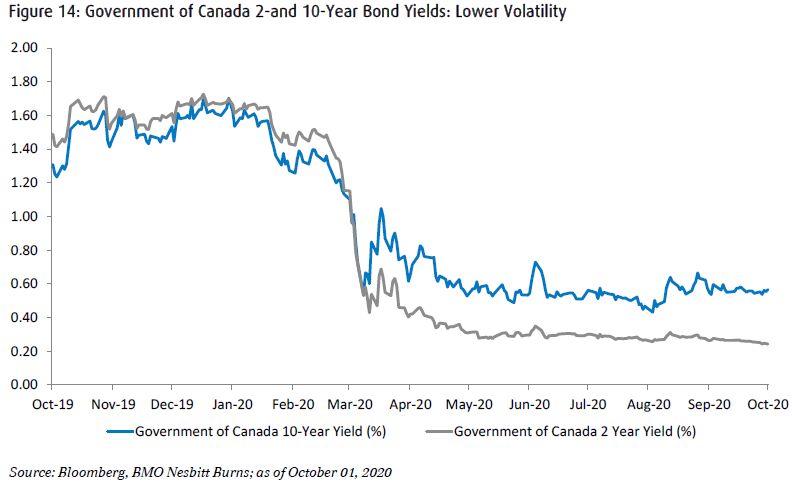

Fixed Income Perspective: In Search of Yield? After a strong and volatile first half of the year, interest rate markets were generally calmer in Q3, with short- to mid-term yields confined within a 10 to 20 basis point (bps) trading range and that was despite the record levels of new government and corporate debt. This was again a testament to the extraordinary monetary policies from central banks. This translated in more normalized monthly returns derived primarily from coupon income. Tightening in the provincial and corporate debt markets, albeit at a more moderated pace than in Q2, provided some additional capital gains. However, as we said in July, considering the already significant decline in interest rates and tightening of credit spreads this year, gains will be more difficult to generate in the near future. As the risk increases of a low growth, low inflation economic environment that will lead central banks to maintain short term rates low and monetary policies accommodative for a prolonged period, income becomes once again investors’ main focus. Intuitively, at this stage in the economic cycle investors would tactically aim at shortening portfolio duration (shorter average portfolio maturity) and increase cash allocations in anticipation of rising rates as the economy recovers. But nothing is normal with the current environment; despite the likelihood of fiscal policies helping bridge the economic recovery until a vaccine is widely available, great uncertainties remain. Ahead is a long and uncertain path to recovery that will undeniably require long term central bank support. Already, the Bank of Canada (BoC) and the U.S. Federal Reserve (Fed), and many others have paved the way for low rates for longer. Unlike previous monetary cycles, short-term rates risk remaining anchored for years, as indicated by the relatively flat short-term yield curve where no policy rate increases are expected until at least 2023, in line with central banks’ forward guidance. More importantly, central bank asset purchases that cover terms out to 30 years for government bonds will help mitigate the risk of longer interest rate significantly rising in the near future. Objectively, in a more positive economic environment that would include a vaccine, higher expected growth and inflation and moderating central bank purchases could lead both long term interest rates gradually higher and the yield curve steeper, offering better investment opportunities. However, we believe the probability of such a scenario remains relatively low over the next 6 to 12 months. Our BMO US rate strategist does believe that 10-year Treasury yield could rise above 1% before year-end but, equally, he believes that such a pullback (from today’s level of 0.65%) would present a great buying opportunity. This leaves a less attractive fixed income investment universe where most investment grade securities offer yields below 2.5%. For many, a 10-year Government of Canada bond yielding 55bps, 1.25% for a provincial bond or 1.70% for a good quality corporate bond is not considered attractive in comparison to average historical yields. Near record-low yields provide limited term and inflation protection, leading investors to increase cash allocations and naturally shorten average term. Unfortunately, cash rates have also followed a similar trajectory downward, making cash very expensive and these ultra-short rates risk declining further in the coming months. Unlike previous cycles, however, it may be too early to shorten duration as the expected path for interest rates

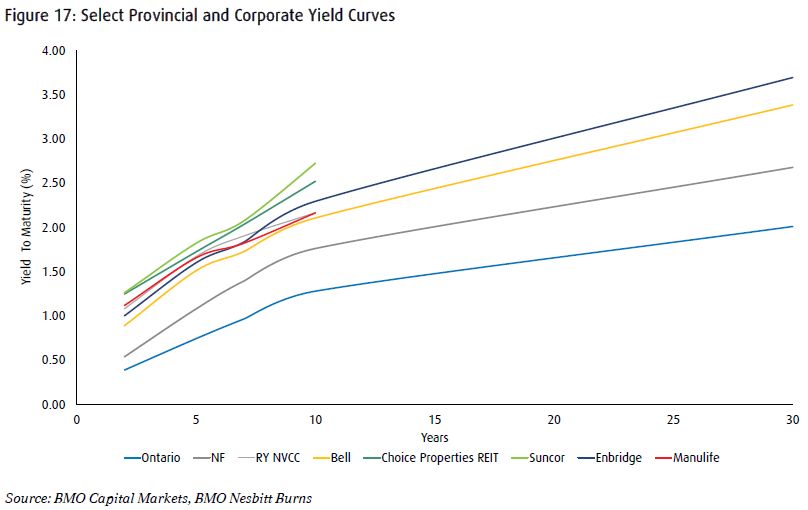

will most likely lead to investors sacrificing too much income. In fact, unless required for liquidity needs or tactical portfolio shifts, we see little incentive to maintain large cash allocations for prolonged periods. Whether we like it (borrower) or not (savers), low rates and price volatility look poised to be around for years. As a result, more than ever, we believe fixed income investors need to remain focus on income generation. With no significant yield movement expected over the next quarters, we can turn our focus more confidently to the mid-term sector (5 – to 10- year) where investors can find quality income instruments at a relatively fair price. While Government of Canada and U.S. Treasury bonds have served their purpose (safety) earlier this year, they now offer limited upside opportunities. Instead, we believe that credit products on a selective basis offer better alternatives, supporting an overweight allocation. Credit markets have performed strongly so far this year, benefitting from declining government yields and tightening spreads. On average, credit spreads have recovered most of the March/April correction thanks to central banks but, in most cases, they remain above pre-Covid levels. More interestingly, as we can see in Figure 16 above, corporate credit spreads in general have widened in September. The virus second wave hitting North America and Europe and the potential impact that renewed partial lockdowns would have on economic growth is partly to blame. A delayed U.S. stimulus package and election uncertainty also help explain some recent pressures on the sector. In our opinion, this is providing better entry points for investors. On an absolute basis, yields are near record lows, but on a relative basis the yield compensation offered for credit exposure remains elevated. The extra yield offered by corporate bonds over over government yields are actually at record high level when measured as a ratio of the total yield, adding to the sector’s attractiveness. The sector comes with risks, of course, but we note that many corporate issuers have taken advantage of the low yields to borrow in order to shore up liquidity and/or retire higher cost debt, ultimately reducing debt servicing costs. Our focus remains on higher credit quality investment grade bonds. Some of our recommendations include bank sub-debt issued by TD, Royal and BNS and from SunLife, Manulife and Industrial Alliance in the 5 to 7 year term. Selectively, BBB rated securities – the lowest rating within the investment grade universe, offers some attractive opportunities. In particular, we like the telecommunications sector given its COVID resilience, with Bell and Telus as top picks. We also like some real estate sub-sectors with our top names including Choice Properties and SmartREIT in the grocery-anchored REIT space, while we prefer Granite in the Industrial REIT area. Smaller issuers like Saputo and Dollarama also remain attractive but risk being slightly more volatile in the near term. While the Energy sector has and continues to underperform amid lower oil prices, our recommended list continue to includes large issuers Suncor, TransCanada and Enbridge where we see value. Understandably, these names may cater to the riskier allocation of an investor’s portfolio as the sector will likely remain at risk and offer greater price volatility than more conservative names.

Provincial bond yields have not backed up as much as corporates but these sub-sovereign borrowers continue to offer relative value. While most investors remain sensitive to higher premia on bonds, which reflects a higher coupon rates versus market yields, there are attractively priced provincial securities in the 7- to 10-year term space with coupon rates between 1.75% and 2.5% and yield compensation in some cases exceeding 1% above Canadas. As for lower-rated corporate credit (high yield debt), the sector may look more attractive from an absolute yield perspective, but the increased issuance has seen leverage rise considerably. Investors gained a certain degree of confidence from central bank bond purchases in credit markets but low rates do not preclude the potential for credit downgrades should the economy deteriorate and/or leverage continue to rise. We have seen multiple rating downgrades this year and more are expected in the fourth quarter. More importantly, the U.S. default rate for high yield debt has significantly increased and is approaching previous crisis highs, something which we do not believe is not reflected in spreads compensation and certainly not in absolute yields. With this in mind, for investors with flexibility to add risk, we would recommend avoiding chasing yields and instead selecting active high yield bond managers that have the expertise to navigate the risks in this space. We risk repeating ourselves more than once in the near future but with rates at or near record lows and expected to remain there for a prolonged period, income generation more than absolute yield-to-maturity should be investors’ primary focus, as over the years, coupon income has been responsible for the majority of the return from fixed income market. Longer duration, underweight federal debt, overweight mid-term provincial, municipal and investment grade corporate bonds is, in our opinion, a more attractive combination for the months ahead and should provide still attractive income in this low yield environment.

Market Performance

Index September C$ YTD C$

S&P/TSX Index -2.06 -2.06 -3.09 -3.09

S&P 500 U$ -3.80 -1.61 5.57 8.43

Dow Jones IA U$ -2.18 0.05 -0.91 1.77

NASDAQ U$ -5.16 -3.00 24.46 27.83

MSCI World Index U$ -3.41 -1.21 2.12 4.88

MSCI EAFE Index U$ -2.55 -0.34 -6.73 -4.21

Index September YTD

CDN Bond Universe 0.32 8.00

US Bond Universe (U$) 0.14 8.89

Foreign Exchange Rates September YTD

C$ in U$ -2.23 -2.63

You can also read