Texas Economic Performance and Outlook Amidst COVID-19 Pandemic

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Texas Economic Performance and

Outlook Amidst COVID-19 Pandemic

Laila Assanie

Federal Reserve Bank of Dallas

6/18/2020

DISCLAIMER: The views expressed are the authors’ and do not necessarily reflect the views of the Federal Reserve Bank of Dallas or Federal Reserve System.

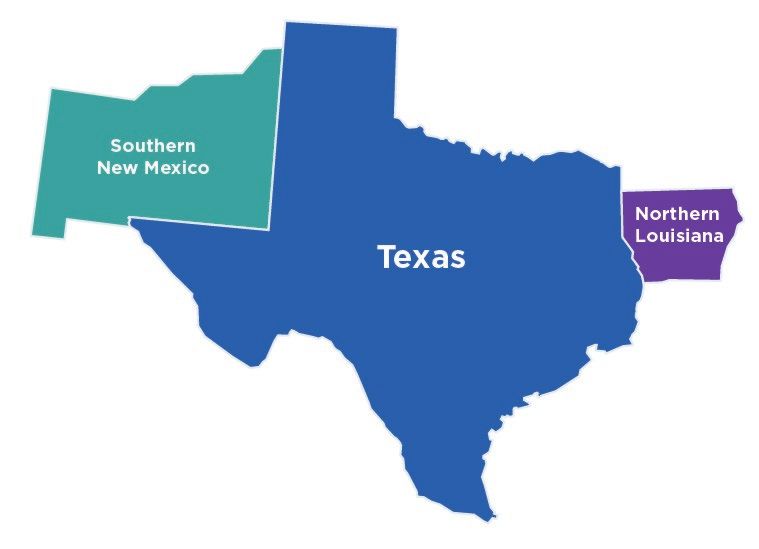

Connecting Regional Economies

Federal Reserve Districts

2

Serving the

Eleventh District

3Texas in the COVID-19 Pandemic

4Overview

Sharp, sudden contraction in economic activity and employment due to COIVD-19

induced shelter-in-place regulations

Record declines in activity in March and April, less-severe contraction in May

Activity appears to be gradually improving as economy reopens, but the path of the

virus is unpredictable, creating heightened uncertainty for businesses and

individuals

So far Texas matching or beating US performance, but this may change due to the

state’s industrial mix

Higher share of employment in vulnerable industries

The economic crisis appears to have broadly peaked but may take time to unwind

5All states shed jobs from Feb to Apr; Northeast/Midwest suffer

largest losses

Percent change, Apr 2020/Feb 2020, SA

0

-5

-10

Texas

-15

U.S.

-20

-25

MI

MA

ME

OH

WA

WI

IN

OR

MD

IL

MN

MT

IA

MO

GA

ID

MS

OK

WV

WY

VT

NY

NJ

RI

HI

NV

PA

DE

NH

CT

KY

LA

FL

TN

TX

AK

CA

U.S.

NC

SC

CO

NM

AL

AZ

VA

ND

KS

NE

UT

SD

AR

DC

SOURCES: Bureau of Labor Statistics.

6Texas job losses less severe than U.S.

(April/Feb.)

Annualized job growth (percent)

0

-9.5 -8.0

-20 -16.7

-23.8 -26.5

-40 -32.1

-37.8 -39.6

-41.8

-45.5 -45.1

-50.9 -48.3 -49.5 -49.0

-60 -52.6

-59.7 -57.2 -57.8

-68.9

-80

U.S. Texas

-100 -93.9

-98.1

-120

Total Trade, Gov't Prof. & Educ. & Leisure Mfg. Fin. Constr. Info. & Oil & Gas,

Transp. (16.6%) Bus. Serv. Health & Hosp. (7.4%) Activ. (6.3%) Other Svcs Mining Sup.

& Util. (14.5%) Serv. (7.6%) (6.8%) (4.9%) (1.7%)

(20.3%) (13.8%)

NOTE: Data show April 2020/Feb. 2020 annualized growth. Numbers in parenthesis indicate share of total state employment for April.

SOURCES: Bureau of Labor Statistics; Texas Workforce Commission; FRB Dallas.

7Texas unemployment rate spikes; still below nation’s

Percent, SA

16

14

13.3

12.8

12

10

8

6 U.S.

Texas

4

2

0

'00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

NOTES: Data through April for Texas and May for the U.S. Grey bars show U.S. recessions.

SOURCES: Bureau of Labor Statistics; Texas Workforce Commission; adjustments by the Dallas Fed.

8Unemployment claims remain elevated

Weekly total unemployment insurance claims, index, Jan. 2020 = 100

1600

1400 U.S.

1200

1000

800 Texas

600

400

200

0

Jan. Feb. Mar. Apr. May Jun

NOTE: Data through the week ending June 6.

SOURCE: Department of Labor.

9Layoffs hitting all sectors in Texas

UI claims as a share of industry employment, percent

35

30 29

26 25

25 23

21

20

20 18

15 14 13 13 13

12 11 11

9

10

7

5 4

2

0

0

NOTES: Claims data for week ending March 7 through week ending June 6. Employment for Feb. 2020.

SOURCES: BLS LAUS program; Texas Workforce Commission

10Layoffs span all Texas metros; border cities and energy centers

Claims per 1,000 workers harder hit

200 190 185

178 174

180 171 169

163 163 160

160 154 152 151

145 144 141 139

140 135 135

127 125

120 118

120 108 108

100

80

60

40

20

0

NOTES: Claims data for week ending March 7 through week ending June 6. Employment for Apr. 2020.

SOURCES: BLS LAUS program; Texas Workforce Commission

11Texas Business Outlook indexes show services,

manufacturing activity contracting more slowly in May

Diffusion index, SA

60

Revenue (Services)

40

20

12.4

9.2

0

-20 -28.0

-28.1

-40 Production (Manufacturing)

-60

-80

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

NOTES: Data through May 2020. Dashed lines are post-recession averages.

SOURCE: Federal Reserve Bank of Dallas Texas Business Outlook Surveys (TBOS).

12Most Texas firms see a sizeable dip in revenues

How do your firm’s current revenues compare with a typical May?

Revenues are up (161%)

10.18

Revenues are normal

8.62

Revenues are down

(59.9%)

81.20

NOTES: Pie chart shows the share of responses belonging to each answer. Numbers in parentheses show average response to how revenues

compare with typical May revenues within each answer.

SOURCE: Dallas Fed Texas Business Outlook Surveys, May 2020 Special Questions.

13May survey suggests nearly one-fourth of firms unable to survive

beyond six months at current revenue levels

If current revenue levels were to continue, how long could your firm survive?

1.0%

8.0%

14.2%

7.2%

59.2%

10.3%

Less than a month 1-3 months 4-6 months 7-9 months 10-12 months More than a year

SOURCE: Federal Reserve Bank of Dallas Texas Business Outlook Surveys, May 2020 Special Questions.

14Majority of firms applied for and have received PPP funding

“Have you applied for a PPP (Paycheck Protection Program) loan?”

“If you applied for a PPP loan, have you received it?”

60% 93%

of surveyed firms of those that have

have applied for a applied have received

PPP loan their loan

SOURCE: Dallas Fed Texas Business Outlook Surveys, May 2020 Special Questions.

15PPP borrowers largely able to stave off layoffs, wage reductions

How did receiving the PPP loan benefit your firm?

Share of responses, percent

90

80

78

70 66

60 52

50

40

30

21

20 15

10

0

Prevented layoffs and/or Prevented wage reductions Helped us pay bills and/or rent Allowed for rehiring of workers Other

furloughs

NOTES: Data collected from 216 business executives from May 12-20, 2020. Respondents asked to select all options that apply.

SOURCE: Dallas Fed Texas Business Outlook Surveys, May 2020 Special Questions.

16Texas firms shift to working from home

Have you taken any of the following steps regarding employment in response to COVID-19?

Share of responses, percent

80

69

70

60

50 43

40 33

30 23

20 19 17

20

11 11

10

0

Increased Reduced work Reduced or Paid time off Furloughs Layoffs Reduced wages Other None

working from hours (including suspended

home cutting overtime) bonuses

NOTES: Data collected from 389 business executives from May 12-20, 2020. Respondents asked to select all options that apply.

SOURCE: Dallas Fed Texas Business Outlook Surveys Special Questions.

17Among firms facing difficulty recalling workers, infection fears, lack

of child care cited as significant challenges

Have you attempted to recall any laid off/furloughed Were there any impediments to recalling workers or increasing hours?

workers or increase hours among current workers?

Share of responses, percent

70

60.0

60

50 46.7

43.3

Yes

33.3 40

30.0

30

20

10 6.7

No

66.7 0

Fear of infection Lack of child care Generous Other None

unemployment

benefits

NOTE: Data collected from 60 business executives from May 12-20, 2020.Question posed to respondents who indicated

NOTE: Data collected from 186 executives who that they were attempting to recall workers or increase hours. Respondents were asked to select any and all choices that

indicated that they have attempted to recall any laid applied.

off/furloughed workers or increase hours among current SOURCE: Dallas Fed Texas Business Outlook Surveys Special Questions.

workers.

18Mobility increasing and workers starting to come back,

daily new Texas COVID cases rising again

Texas Mobility and Engagement and COVID-19 Spread

Count, 7 day avg. 5/1: Phase 1 Index, 7 day avg.

2500 COVID19 daily new cases of re-

5/22: Phase 6/12: 110

2 of re- 6/3: Phase 3 Restaurants

COVID19 daily deaths opening 100

opening of re-opening

2000 Mobility and engagement expand to 90

Num. of hourly employees working 75% capacity 80

2205

1500 70

60

50

1000 40

30

500 20

26 10

0 0

-10

-500 -20

-22 -30

- 52 (4/10) -40

-1000

-50 -50

-60

-1500 -70

-80

-2000 -90

-107 (4/10) -100

-2500 -110

3/1 3/8 3/15 3/22 3/29 4/5 4/12 4/19 4/26 5/3 5/10 5/17 5/24 5/31 6/7 6/14

NOTE: Mobility and engagement index data up to June 13, 2020, Homebase data up to June 15, 2020, all other data up to June 16. Mobility and engagement index values are scaled such

that the national index average over January-February are subtracted out and divided by the national value in the week ending in April 11, the lowest national weekly value. Mobility and

engagement index value can be interpreted as mobility and engagement relative to the national trough in mobility and engagement.

SOURCES: Homebase, Johns Hopkins University, SafeGraph, Federal Reserve Bank of Dallas.

19Restaurant reservations in Texas lose some momentum in June

Percent change, y/y, 7 day moving average

20

-50

0 -60

-70

-80

-20

-90

-100

-40 Texas

Houston

-60 San Antonio

Dallas

-80 Austin

U.S.

-100

Feb Mar Apr May June

NOTE: Data through June 16, 2020. Data refers to year/year percent change in seated diners at restaurants on the OpenTable network across all channels: online

reservations, phone reservations, and walk-ins.

SOURCE: OpenTable.

20So far Texas matching or beating US performance, but

this may change

Negative factors

Low oil prices

Texas job growth is less than nation’s when oil prices fall to very low levels

Less remote work capability

Texas has a lower share of workers that can work from home

More vulnerable industries

Texas has a greater share of employment in industries harmed by social distancing

Texas more exposed to international trade, Mexico

Positive factors

Typically grows faster than nation

Flexible labor markets, good business climate

Fewer COVID risk factors?

Low density metros, lack of mass transit

21Fewer can work remotely in Texas

U.S. 0.39

Texas 0.37

Male 0.34

Female 0.42

No college degree 0.27

With college degree 0.57

Income=$60,000 0.57

White 0.47

Black 0.33

Asian 0.50

Hispanic 0.23

Houston 0.40

Dallas/Fort Worth 0.42

Austin 0.48

San Antonio 0.37

Other areas in Texas 0.28

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

Percent of Workers Compatible with Remote Working

NOTE: All samples, except for the top bar are restricted to workers in Texas.

SOURCE: IPUMS; Dallas Fed; author's calculations.

22Texas has more employment at risk in pandemic

Share of total employment

25

20

9.6 Accommodations & food services

Administration & support services 9.2

15

Transportation & warehousing

Energy

10 6.1

Arts, entertainment & recreation 5.8

5 4.2

3.7

1.7 0.3

1.2 1.6

0

Texas U.S.

NOTE: Data is from March 2020.

SOURCES: Bureau of Labor Statistics; Texas Workforce Commission; seasonal and other adjustments by the Dallas Fed.

23DFW Economy Amid the COVID-19 Pandemic

24Business-Cycle Indexes indicate sharp contraction in DFW

Percent, year/year Dallas

10

Fort Worth

5

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

-5 -6.04

-10

-12.33

-15

NOTES: Business-cycle indexes through April 2020. Dashed lines are long-run (20-year) averages.

SOURCE: Federal Reserve Bank of Dallas.

25Mobility increasing and workers starting to come back,

daily new COVID-19 cases rising again in DFW

Dallas-Fort Worth Social Distancing and COVID-19 Spread

Index, 7 day avg.

Count, 7 day avg. May 1: Most retailers, dine-

in restaurants allowed to June 3: Phase 3 June 12:

open at 25% capacity May 22: Phase 2 of re-opening Restaurants expand

of re-opening to 75% capacity

700 120

604

600

COVID19 daily new cases

500

Mobility and engagement (Index) 80

400 Num. of Hourly Employees Working (Index)

300

40

200

100

0 0

-100

-200 -23 -40

-300

-59

-400

-80

-500

-600

-700 -120

3/1 3/7 3/13 3/19 3/25 3/31 4/6 4/12 4/18 4/24 4/30 5/6 5/12 5/18 5/24 5/30 6/5 6/11 6/17

NOTE: Mobility and engagement index data up to June 12, 2020, Homebase index up to June 16. Case data through June 17, 2020.

SOURCES: Homebase; Johns Hopkins University; SafeGraph.

26DFW leads major Texas metros in net migration gains since 2010

Net migration, thousands

800

700

600

500

400

300

200

100

0

-100

DFW Houston Austin San Antonio El Paso

NOTE: Data are for July 2010 to July 2019.

SOURCE: U.S. Census Bureau, Population Division.

27Reason for migrating to Texas versus elsewhere

Reason Texas Non-Texas

Relocated for job 50.9 41.3

Family Reasons 26.6 26.6

Amenities 17.8 23.8

Other 4.7 8.3

NOTE: Data refer to 2010-2019.

SOURCES: CPS-ASEC; author’s calculations.

28Texas and DFW Real Estate Markets

29Residential construction weakens

Index, Jan.‘10=100, 5 MMA, SA

600 Single-family Multifamily

(percent growth) (percent growth) Multifamily permits DFW

2019 2020 YTD 2019 2020 YTD

500 DFW -3.7 17.7 4.4 -0.8

Texas -0.3 17.9 22.8 5.8

400

300

Multifamily permits Texas

200 Single-family permits DFW

Single-family permits Texas

100

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

NOTE: Last data point is April 2020. Table refers to percent growth in annual totals. Table 2020 YTD data for January-April 2020.

SOURCES: U.S. Census Bureau; seasonal adjustments by FRB of Dallas.

30Apartment rent payments slightly below 2019

Percent June 1-13, 2020 June 1-13, 2019

95

93.9

94 93.5 93.5

93.2 93.2 93.2 93.2

93 92.7

92.2

91.9

92

91

90

89.0 88.9

89

88

87

86

Austin Dallas San Antonio Fort Worth Houston U.S.*

NOTE: US data are from National Multifamily Housing Council. Texas metro data provided by RealPage Inc.

SOURCES: RealPage Inc.; National Multifamily Housing Council.

31Home sales fall sharply in the wake of COVID-19

Index, 3MMA, Jan. 2011 = 100, SA

170

Fort Worth

160

Texas

150

Dallas

140

U.S.

130

120

110

100

90

2012 2013 2014 2015 2016 2017 2018 2019 2020

NOTE: Data through April 2020.

SOURCES: Multiple Listing Service; seasonal and other adjustments by Dallas Fed.

32Home sales dip across price points

Dallas-Fort Worth-Arlington

Index, Mar. 2011=100, 3MMA, SA

700 6% $400-499k

12% $300-399k

600 12%

10%

$200-299k

500

More than $499k

22%

38%

400 $150-199k

Less than $150k

300

200

100

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

NOTES: Data are through April 2020. Pie chart data for 2020 YTD. Underlying data in nominal dollars.

SOURCES: Multiple Listing Service, seasonal and other adjustments by FRB Dallas.

33Inventories tight

Dallas-Fort Worth-Arlington

Months of Inventory, SA More than $499k

14 $400-499k

$300-399k

12

$200-299k

10

$150-199k

8 Less than $150k

6

4.5

4 3.5

2.9

2.1

2 2.0

1.8

0

2011 2012 2013 2014 2015 2016 2017 2018 2019

NOTES: Dashed line at six months of inventory indicates balanced level of supply. Data are through April 2020.

SOURCES: Multiple Listing Service, seasonal and other adjustments by FRB Dallas.

34House price appreciation holding steady

Percent, year/year, SA

12

10 DFW

8

6

4 U.S.

2

0

-2

-4

-6

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

NOTES: Data through March 2020. Case-Shiller HPI for DFW is used to approximate Texas.

SOURCE: Standard & Poor’s CoreLogic Case-Shiller Home Price Index.

35What business contacts are saying about

new-home sales in DFW

“Sales remain solid to this point.”

“DFW, San Antonio, and Austin were pretty strong. Houston was a little slow. Dallas is

shaping up to have a better month than we expected. We expect monthly sales for

April to be about 2/3 of what they were last year.”

“… over the past few weeks we have done a really good job of moving our prospects

to contract and this week was a rebuilding prospect week. We have a better start to

the week already with multiple contracts in the works.”

“We had a good week here in Dallas. We were almost double last week’s gross

number. We ended up netting about 90% of plan. I have heard quite a few deals

already in the process that should finish in the next couple of days. Keeping fingers

crossed.”

36DFW office absorption softens ahead of the pandemic

Net absorption, millions

16

14 DFW

12 Houston

Austin

10 San Antonio

8

6

4

2

0

-2

-4

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Q1 2020

NOTE: Data through Q1 2020. San Antonio data missing in Q1 2014, Q2-Q4 2016.

SOURCE: CBRE Research.

37Outlook for 2020

38Texas employment expected to rebound in second half but

Percent, SAAR

end the year below 2019 levels

150.0

Percent, Y/Y 116.8

5.0

100.0 0.0

-5.0

-10.0 -3.8

-15.0

50.0

0.0

-50.0

-69.0

-100.0

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

NOTE: Forecast scenario estimates Texas payroll employment for May based on initial claims data and the remainder of the year based on US GDP growth of -42.3% Q2, +16.3% Q3, and

+22.8% Q4, as well as direct COVID-19 impacts from March to May and WTI prices following the futures contract curve as of 6/1.

39Texas unemployment rate expected to slowly decline

Percent, SA

16

14.9

14

12.8

12

10

8 8.9

6

3.5

4

2

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

NOTE: Forecast scenario estimates Texas payroll employment for May based on initial claims data and the remainder of the year based on US GDP growth of -42.3% Q2, +16.3% Q3, and

+22.8% Q4, as well as direct COVID-19 impacts from March to May and WTI prices following the futures contract curve as of 6/1.

Unemployment rate forecast assumes a labor force participation rate of 63.8 and a payroll/household employment ratio of 0.97 at year-end.

40Summary

Pandemic is unprecedented and has many aspects of a natural disaster instead of a

typical recession

Economic activity is slowly recovering; path of the virus and consumer demand and

business responses highly uncertain

Most economists expect a sharp decline in Q2 and recovery in the second half – but

still expect to end the year down more than in the Great Recession

Weakness in the energy industry will likely be drag on Texas, dampening the state’s

recovery in the second half of 2020

Factors such as a central location, low cost of living, flexible labor markets, good

business climate will be favorable for DFW in the long run

4142

Stay Connected

Find COVID-19 updates and resources

dallasfed.org/covid federalreserve.gov/covid-19

Sign up for Dallas Fed content of interest

dallasfed.org/subscribe

43You can also read