Pre-Budget 2021 Submission - September 2020 - IBEC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Pre-Budget 2021

Submission

September 2020

1

PII Pre-Budget 2021 Submission

Contents

1. Summary .................................................................................................................................. 3

2. Introduction .............................................................................................................................. 3

3. An Equity Loan Scheme to support home ownership........................................................... 4

4. Enhancing Affordability and Viability of Housing Development .......................................... 6

5. Reduce VAT for new housing construction ........................................................................... 8

6. Commission for Housing ........................................................................................................ 9

7. Delivery of social housing....................................................................................................... 9

8. Modern Methods of Construction (MMC) ............................................................................. 10

9. Establish a Housing Delivery Cost index ............................................................................. 10

10. Support for Remote Working ................................................................................................ 10

11. Provide stability through Policy Certainty ........................................................................... 11

12. Facilitating Cash-Flow ........................................................................................................... 12

13. Resourcing of Infrastructure................................................................................................. 12

14. About Property Industry Ireland ........................................................................................... 14

2

PII Pre-Budget 2021 Submission

1. Summary

Given the on-going crisis associated with Covid-19 and the imminence of Brexit many of the

challenges facing the housing market remain to be addressed. Key policy recommendations

from Property Industry Ireland for Budget 2021 include:

• An Equity Loan Scheme to support home ownership

• Enhancing Affordability and Viability of Housing Development

• Reduce VAT for new housing construction

• Establish a Commission for Housing

• Delivery of social housing

• Utilise Modern Methods of Construction (MMC)

• Establish a Housing Cost index

• Support for Remote Working

• Provide stability through Policy Certainty

• Facilitating Cash-Flow

• Resourcing of Infrastructure

2. Introduction

Ireland needs more homes to solve the housing crisis. This is accepted by all commentators

and political parties. There is less consensus, however, about how this can be achieved.

The ultimate solution to supply is to get all housing functioning normally at the earliest

opportunity. Property Industry Ireland (PII) remain of the view that there is no single solution.

Homes will need to be supplied across the full range of tenures to meet demand from across

the full income distribution.

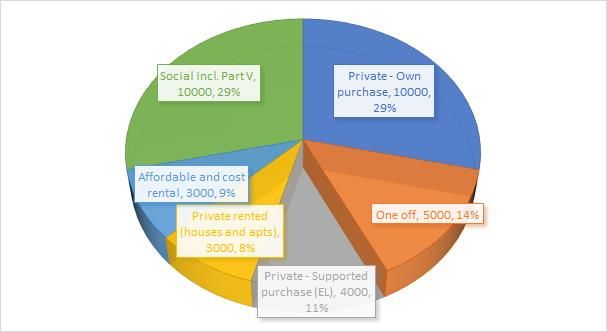

PII have estimated that annual new household formation is approximately 35,000. Figure 1.1

sets out how this housing need might be met – including demand supported by the Equity

Loan scheme proposed by PII in June 2020 and outlined later in this submission.

Figure 1.1

Ireland is now also facing additional challenges in a post-Covid world. Anecdotal evidence is

suggesting that people are less interested in living in urban locations, Dublin included. This,

3PII Pre-Budget 2021 Submission

coupled with a fall in interest in office space in many urban locations, is of serious concern for

the future of our city centres.

3. An Equity Loan Scheme to support home

ownership

A significant proportion of Irish households are caught in a situation where their borrowing,

and by extension, purchasing power is not sufficient to buy a new build home on key transport

corridors and in urban centres. This is evident when average CSO household incomes,

combined with maximum borrowing limits are compared to the entry level SCSI housing

delivery costs, particularly for apartments and urban centre locations.

Of the 21,241 new homes completed in 2019, just 4,334 (approx. 20%) became homes for

First Time Buyers. This relative lack of First Time Buyers’ presence reflects primarily those

individuals and families in this ‘Locked-Out Generation’ cohort who do not qualify for social

housing supports and cannot afford a new A-rated home of their own.

Based on Revenue data, the Locked-Out Generation accounts for approximately 440,000

households in Ireland. A State supported solution, striking the right balance of fairness, is

required for this cohort of society. This scheme, potentially self-financing, is focussed on

facilitating home ownership for those whose incomes mean that they are close to home

ownership but, because of increased costs of housing and restrictions on borrowing, are

unable to do so.

The challenges of the Locked-Out Generation are not unique to Ireland. Similar difficulties are

evident in many jurisdictions globally. From the research conducted in drafting this paper, we

have identified Homes England and its support schemes as the most relevant to the Irish

residential market. The English equity loan scheme has been operating successfully since

2013 with more than 250,000 new homes supported by the scheme to date, many of whom

were not able to purchase a new build home in advance of the scheme being implemented,

which is a testament to its success. While similar to shared equity, an equity loan scheme is

different and is demand-led.

The equity loan structure is modelled on the experience of the Homes England scheme.

However, the Homes England scheme has some shortcomings, particularly its lack of

qualifying criteria and that it is not focused on helping specific cohorts of household incomes.

Therefore, the suggested Irish structure includes additional qualifying criteria to ensure it is

appropriately focused on helping to create a fair society, while in parallel ensuring the

scheme does not drive house price inflation.

The equity loan scheme criteria can be summarised as follows:

o The scheme is for First Time Buyers looking to purchase a new build A-rated

home.

o These purchasers must have household incomes below €95,000 and can apply

to get an equity loan of up to 30% of the home value for the difference between

the purchase price and the sum of their maximum mortgage borrowings and

deposit.

o The purchasers must live in the home as their primary residence and cannot

rent the property out.

o Home price caps and equity loan caps will differ for houses and apartments in

recognition of the different development costs. This will also enable more

4PII Pre-Budget 2021 Submission

people to purchase apartments, driving urban living as targeted in Project

Ireland 2040.

o Home price caps and equity loan caps will also differ by region to ensure it is

focused on areas where the Locked-Out Generation are most impacted.

o The equity loan is a 2nd charge loan on the property linked to the % of the

home’s value on purchase. The % value is fixed and the actual value of the

loan moves, up and down, with the value of the property. This ensures an

appropriate balance of benefit and risk sharing between the State and the

citizen.

o There is no interest or mandatory principal repayment on the equity loan in

Years 1 – 5. From Year 6, interest only is charged at small annual rate [1.1%

suggested] on the equity loan’s value but this is not indexed.

o The purchaser can pay back part or all of the equity loan at any time.

o Each purchaser must have borrowed at the maximum loan-to-income (LTI)

threshold of 3.5 times income for their mortgage to then be entitled to an equity

loan for what they need.

o Table 1.1 details the suggested qualifying criteria. The home price caps are

based on 2016 and 2017 SCSI housing delivery costs for new homes and

apartments, adjusted for inflation.

Suggested Qualifying Criteria

Equity

Upper Income Home Price

Location and Home Type Loan %

Threshold Cap

Cap

Houses: Dublin €95,000 €425,000 25%

Apartments: Dublin and other city

€95,000 €485,000 30%

centres

Houses: rest of GDA, other main

€95,000 €350,000 25%

Cities, and other Growth Areas

Apartments: rest of GDA, and other

€95,000 €400,000 30%

Growth Areas

Table 1.1

A key benefit of this scheme is that mortgage lenders/state agency will be obliged to inform

First Time Buyers of their mortgage obligations and the long-term equity loan responsibilities

when selecting a home to purchase, including the possibility that the value of the equity loan

could decrease and increase. The varied preferences of households along with this

information will lead to a wide range of home prices and corresponding equity loans being

taken by purchasers, many of which will be significantly less than the capped amounts. In

parallel, the housing industry will need to provide units which qualify for the scheme.

Through this scheme, the State will facilitate the aspiration of home ownership for many of its

Locked-Out Generation citizens, many of whom would otherwise remain in the rental market.

It avoids placing excessive financial pressures on these households in the early stages of

home ownership and is structured to be consistent with the natural lifecycle of income

increments over time. Furthermore, this paper shows that many households are currently

paying significantly more rent than the combined cost of a mortgage and an equity loan.

5PII Pre-Budget 2021 Submission

The scheme carries no development risk and modest financial risk for the State. The equity

loans remain State assets which purchasers repay over time making it a much lower risk to

the State when compared to other housing support schemes. From the 1st charge mortgage

lenders’ perspective, the scheme has the advantage of getting more people into their own

home without placing further financial strain on purchasers and in-turn ensuring no additional

credit and lending risk is placed on the banks.

While the State has developed some affordable housing initiatives for State land, progress in

delivering homes to middle income households has been limited. These initiatives are limited

to State-owned lands and therefore will take considerable time to deliver homes at scale due

to the inherent challenges in mobilizing, procuring and delivering homes on State land.

In the short and medium term, a solution is required for the Locked-Out Generation. The

equity loan structure leverages the functioning private sector led housing delivery platform in

Ireland to give aspiring homeowners a time-realistic and credible pathway to home ownership.

We recommend that focus group research is also implemented with prospective purchasers in

parallel to obtain qualitative and quantitative input on the scheme.

We believe with equity loan funding of approx. €500m for an initial 2 years, 7,000 - 8,000

families from the Locked-Out Generation would be supported to purchase new homes who

would otherwise not be able to afford a new home. The VAT, Stamp Duty and development

levy contributions/returns from 4,000 units a year could total approximately €256m.

Equity loan transactions would remain a small part of the overall market. In 2019, there were

45,112 second-hand transactions and 21,241 new homes completed. Assuming a long-run

average of 40,000 second-hand transactions and achieving the target of 35,000 new home

transactions including the additional 4,000 annual sales supported by equity loans, the equity

loan sales would only represent 5.1% of the overall market. In parallel however, these 4,000

additional First Time Buyer homes annually would produce an impressive 92% increase on

the modest 4,334 First Time Buyer purchased homes in 2019.

In developing this policy, we have engaged across industry with a number of representative

bodies including Homes England, BPFI (Banking and Payments Federation Ireland), IIP (Irish

Institutional Property), IHBA (Irish House-builders Association) and SCSI (Society of

Chartered Surveyors Ireland).

PII discussion document June 2020

https://www.propertyindustry.ie/Sectors/PII/PII.nsf/vPages/Publications~the-irish-equity-loan-

29-06-2020!OpenDocument

4. Enhancing Affordability and Viability of Housing

Development

Viability and affordability of residential development remains a concern, in particular because

of the uncertainties caused by Covid-19. Covid-19 also poses a serious challenge for our

cities. Anecdotal evidence suggests that there is an exodus from our cities to suburban and

smaller communities, coupled with a fall in interest in commercial office space from

businesses who are promoting working from home as a way of tackling the spread of the

virus. If continued, this societal response will have a lasting and serious impact on the

attractiveness and liveability of our urban locations. This, coupled with the ongoing challenge

that new home and commercial property development is already more expensive than

greenfield development, ultimately adds to prices.

6PII Pre-Budget 2021 Submission

While the Equity Loan scheme can go some way to closing the affordability gap for

households with sufficient income to buy their own home, further measures can be taken on

the supply side to aid in overall housing viability. Each of the measures below would help

provide more homes.

1. Increase the threshold for cash receipts basis of accounting for VAT from €2m to

€5m to help small/medium builders.

2. Reform of section 83D SDCA 1999 with a practical focus.

Section 83 currently allows for a refund of 5.5% of the 7.5% of the stamp duty paid on

the purchase of a greenfield site which is later residentially developed. This has the

effect of giving the builder the overall 2% residential rate of stamp duty as an incentive

for increasing the housing stock on the market, but only if certain conditions can be

met.

Presently, construction must be commenced on the land pursuant to a commencement

notice within 30 months of the date of the instrument of transfer. Additionally, the

development must be completed within 24 months of the date of acknowledgement of

the commencement notice. In practical terms, 24 months can be a very short timeline

within which to complete construction of a site. This is particularly so when the site is to

be completed in phases, the builder encounters issues on the ground which require

time to resolve or the various county councils mays having differing approaches to

issuing site commencement notices.

o For example, if the builder gets one commencement notice for a site, the entire

site has to be completed within 24 months from the date of acknowledgement

of that commencement notice, regardless of the number of phases in which the

site is actually being developed. Yet, if a builder gets a commencement notice

per phase, each phase must be completed within 24 of the date of

acknowledgement of that particular commencement notice for that phase.

Further, if a particular phase won’t be completed within the 24 months and in

any event before 21 December 2023 - the refund is not available in respect of

that phase yet if there is one commencement notice and the construction is

completed in phases, if the final phase is not completed with the required 24

months, the entire site will lose out on the refund, with no apportionment for the

completed phases. It is understood that some county councils will issue one

commencement notice for the entire site, while some will issue a

commencement notice on a phased basis. The builder is at the mercy of the

particular county council issuing the notice. This section should be amended to

acknowledge the practical reality where a builder has to take a phased

approach to completion of a development, regardless of the number of

commencement notices issued.

o A further condition which can cause complications is that which states that 75%

of the total surface area of the land must be covered by the footprint of the

residential units or 75% of the gross floor space of the units must equate to

75% of the total surface area of the land . If there are a number of

commencement notices per site but it is not possible to meet the 75% test until

the last phase, if that last phase is not completed by 21 December 2023, the

refund is lost on the entire development even though the other phases where

completed within 2yrs. This complication arises as a “relevant residential

development” is defined as the entire development when you defer claiming the

7PII Pre-Budget 2021 Submission

refund until the completion of the development so as to meet the 75% test or

when the development isn’t built in phases pursuant to a construction notice for

ease phase.

From a public policy perspective, the builder is fulfilling the objective of the legislation

in increasing the availability of residential housing stock on the market to meet public

demand. The current conditions have the definite, albeit unforeseen consequence, of

penalising the builder, where, due to practical constraints the strict 24-month timelines

for the refund cannot always be met in line with the strict legislative definition.

A revision of the section to make the rules more practical to accommodate phased

construction on sites in line with the reality on the ground and increasing the timeline

for commencement of construction from 30 months to 48 months and for completion of

the development from 24 to 48 months would go a long way to meeting this public

policy objective and easing the burden on those in the construction sectorThe

Residential Stamp Duty refund scheme, currently limited to 30 months, needs to be

extended by at least a year. The timeline introduced was already a challenge in

particular for phased development of housing (the largest contributor to new housing)

and because of the delay in development caused by Covid-19.

3. Reduce stamp duty rate to 4%.

Finance Act 2019 increased the rate of stamp duty on non-residential property from

6% to 7.5%. In a period of lower capital appreciation, such high transaction costs are a

major disincentive to foreign and domestic investment in commercial property here.

Reducing the stamp duty rate to 4% in line with the average across the EU would likely

restore our competitiveness. Any cut to the rate of stamp duty is likely to stimulate

much needed market activity as an increased level of transactions has a direct

economic benefit that far outweighs the impact on tax receipts. In the present climate,

in the shadow of Covid-19, incentivising market activity is likely to be a more direct

route to much needed receipts boosting the exchequer requires.

4. The increase in the Help-to-Buy scheme for a period of 6-months is welcome but will

have limited impact on certainty and delivery because of the limited timeframe. The

enhanced scheme should be extended to the end of 2021 to help developers plan and

deliver more homes on the back of the certainty of this demand.

5. Decrease CGT for property transactions to increase activity in housing sales and

encourage property owners to sell properties to families.

6. Incentivise apartment delivery through tax incentives and / or grants for brownfield

sites as it is currently uneconomical to deliver apartments for individual sale or rental at

affordable levels for the majority of end users.

5. Reduce VAT for new housing construction

The interaction between affordability and viability is a key issue for the housing market. Data

from the recent SCSI report (reference) show that the cost a delivering a new 3 bed semi-

detached house in Dublin is just over €371,000. Their report also shows that the gap between

how much a couple can afford to borrow plus a deposit, and the cost of delivery is in the order

of €25,000.

8PII Pre-Budget 2021 Submission

The report shows that the overall construction cost (cost of building the house from foundation

to roof and completing the estate roads and drains etc.) is €178,902 which represents 48% of

the overall cost of providing the house. Thus, 52% of the cost of providing a home comes from

other costs.

The total VAT for an average house figure is € 44,164. All new homes will include a VAT

charge of 13.5%. The VAT take on an average 3-bedroom semi is 12% of the total delivery

cost. By way of comparison, new house sales in Northern Ireland and the UK attract zero VAT

rates. PII calculate that a reduction in the VAT rate from 13.5% to 9% would reduce the cost of

delivering a new home by €14,700.

Based on the SCSI report the gap between house delivery cost and affordability is €25,000.

This measure would significantly narrow the gap.

6. Commission for Housing

Dialogue between the public and private sectors will play a key role in helping address the

housing market crisis. PII supports the proposal in the Programme for Government to

establish a Commission for Housing to examine issues such as tenure, standards,

sustainability, and quality-of-life issues in the provision of housing. The Commission should

include private industry representation through Property Industry Ireland.

The format, remit and make up of this body is key to whether it can be successful. In addition

to the role identified in the Programme for Government, the focus of the Commission for

Housing should ensure that housing need is met:

• Government should set a housing delivery target by tenure for each of the next 5

years. This will create certainty and accountability, and the achievement of these

targets should be overseen by the Commission for Housing

• Population growth and core strategy of the NPF should be kept under continuous

review by the Commission on Housing

• In reviewing access to housing, the Commission for Housing should also review the

impact of the Central Bank lending rules on capable demand

• It should develop and make policy proposals and proposals on adjustments to existing

policies based on research, insight and knowledge

• It should review historical data but be forward looking and must include participation

from private sector development, planning and finance industries, civil servants from

housing and finance, key public sector and non-profit sector housing and planning

representatives

• The Commission should look to take on best practice globally and how it fits in an Irish

context

• It should use research to inform debate and not rule anything in or out from the outset.

It should enable trust and coherent collaboration to be built between public and private

sector institutions.

7. Delivery of social housing

The need for social housing provision remains as acute as ever. Government should fast-track

the social housing programme through:

9PII Pre-Budget 2021 Submission

• Housing First (for Homeless) prioritised through locally based multi-agency task forces

delivering coordinated action, with the LA using CPO powers to acquire and refurbish

homes.

• Capital Programme of investment to support delivery of Ireland’s ambition, including by

promoting the use of Modern Methods of Construction.

• Review Procurement to support the use of “all-of-life” standards. This will help with

improving the overall sustainability of construction and reduce waste.

• Develop a clear parallel investment plan to include social and productive infrastructure.

8. Modern Methods of Construction (MMC)

Supply chains for MMC homes are underdeveloped in Ireland. Government should take a lead

in aggregating demand for MMC products to encourage, support and underpin the necessary

investments in factory facilities, machinery and technology.

Sustainability and climate ambitions could be supported by linking National Climate Change

and Circular Economy targets to the delivery of new projects through offsite Low carbon

manufacturing solutions. A review of the access criteria to Government supported funds

available to the home building sector should be undertaken, with a view to introducing criteria

that supports the use of MMC and the deployment of innovative technology.

Procurement criteria should be reviewed and improved to mandate the use of innovative

technology and in particular BIM at an appropriate level, from concept to occupation phase.

This would support the longer-term maintenance of the buildings, would support an ongoing

drive for cost efficiencies and help to influence and inform stakeholders into the future.

Ensure skills programmes and apprenticeship schemes are set up that supports the attraction

and development of a young, diverse workforce towards a new modern, innovative and

digitally orientated industry.

9. Establish a Housing Delivery Cost index

Improving data and information will help understanding of how the housing system operates in

Ireland. With this goal in mind, PII urge Government to establish a Land Cost Registry without

delay.

In addition, Government should give CSO the role to publish all construction costs related to

all housing types and locations. As part of this, the CSO should research, categorise and

publish all costs associated with home delivery, including the cost of regulations on housing

costs, including:

• Planning Standards;

• Building Regulation Standards; and

• non-construction-related costs

10. Support for Remote Working

Remote working is likely to be a more permanent feature of the Irish Labour Market. The

overwhelming majority of all office-based work transitioned to employees’ homes during the

Covid-19 lockdown. With modern IT capabilities, many companies are examining how remote

working may become a permanent feature, given that the experience has been companies

10PII Pre-Budget 2021 Submission

continuing to operate remotely as efficiently as in the traditional office-based setting. Google

and Indeed have updated their policies to allow employees work from home (“WFH”) until

2021 while Facebook and Twitter have introduced permanent remote work.

The most significant benefits of WFH are environmental through reducing commuting journeys

(both in private cars and on the public transport system). Beyond environmental benefits,

WFH has a broad range of tangible social and health benefits. Reduced travel time means

people have more time for other responsibilities as well as pastimes. Furthermore, flexible

working and WFH are intrinsically linked: employees can choose from a broader range of start

and end times as well as more flexible break times.

In addition, Ireland’s regions would greatly benefit from an increased working age population,

this benefit would be both economic and social.

While recognising that it is important that staff spend some of their working week in an office

environment to ensure the collaborative side of work is enhanced and also to ensure that

younger employees benefit from direct interaction with their peers, Government should

support businesses through subsidies and tax incentives in facilitating WFH which will

continue for many Irish businesses while social distancing protocols are in place. In the

medium to long-term, it is likely that WFH will be a central pillar for businesses in their long-

term strategic planning.

For employees, additional costs arise as a result of working from home – suitable home

offices, space constraint solutions and daily home office running costs. The Irish tax regime is

currently not supportive of the cost of facilitating WFH or contributions by employers towards

the significant capital cost for employees of remote working on a (more) permanent basis –

loans by employers are subject to BIK rules which make them uneconomical for the employee

in many instances, while in certain limited instances an employer can make a €3.20 per day

tax-free payment towards remote working running costs.

Substantial taxation supports are needed to give our economy a competitive edge as global

work practices transition towards WFH. This should include a WFH tax credit for both

employees and self-employed who work from home for more than 50% of the time.

To ensure that homes are also suitable for work purposes, Government should re-introduce a

home renovation scheme. The scheme was successful in helping families enhance their

existing home and could be amended to encourage sustainability/energy efficiency

improvements and to alleviate costs related to Covid-19 such as in renovating home offices.

11. Provide stability through Policy Certainty

Many of the policies put in place over the past number of years – such as fast-track planning

and Help-to-Buy for first-time buyers etc - are helping to have a positive impact on supply with

the number of new homes being built increasing by 18.3% in 2019. An increase in supply is

needed in the private rented sector as well as for owner-occupiers.

Despite a welcome increase in apartment delivery, there has been much negative

commentary about the role institutional investors play in the housing market. Globally, private

funds play an important role in financing apartment construction. The challenging nature of

apartment development funding means most of these new apartments would not be built

without this finance. Strip out active investor demand for completed apartments and most new

11PII Pre-Budget 2021 Submission

apartment developments would not be built. There is plenty of evidence of their importance

across a range of European countries. Housing is regarded as a long-run asset so while

ownership may change the apartment (asset) remains in place.

Institutional investors are being unfairly accused of taking homes away from people. The

evidence suggests otherwise. In fact, new professional investors are facilitating the delivery of

much needed apartment accommodation into the Irish housing system by providing certainty

of end-purchaser demand. Without such certainty builders, developers and their lenders will

not engage in large scale, capital intensive apartment development, the consequence of which

will be lower supply.

The increase that we have seen in the supply of houses and apartments over the last few

years should not be taken for granted. Investing in the development of housing is sentiment

driven. Policy uncertainty will result in a slowdown in development funding and a pause in

supply growth.

Ireland is a small and open international economy. One of the most successful economic

stories in Ireland has been the ability to attract foreign direct investment (FDI). This investment

has delivered economic growth and jobs. Much of this new employment draws a young and

international workforce to our urban centres, for whom renting is the preferred form of housing

tenure. Long-run investment in the delivery of homes to the Irish housing market should be

welcomed. It is this investment that is helping to provide the homes for the jobs that business

is creating.

12. Facilitating Cash-Flow

Like many other industries affected by Covid-19, cash flow is key for many property and

construction businesses. Government can facilitate continued cash-flow through a number of

measures. These should be introduced in the form of low-interest loans, rather than

subsidy/grant/tax incentives:

1. How landlords pay tax need to be considered. Currently, if rent is due but not paid (and

the debt is not "bad") then the landlord has to pay tax on that income in the year that it

is earned (even though it may not be received for months/years). Government should

introduce a mechanism to offset this lacuna, particularly in light of the number of rent

holidays/breaks being sought from tenants in distress

2. Introduce a "borrow back" tax paid scheme, with the State providing a loan to

employers equal to 25% of tax paid in 2019 interest free. A similar scheme has been

introduced in Denmark.

3. Postpone the review of residential property tax to alleviate the burden on households

during these challenging times.

4. The planned reduction to 30% of EBIT in one year for interest limitation rules

disproportionately affect property companies because of the way that their assets are

leveraged. Government should postpone introducing these rules to 2022.

13. Resourcing of Infrastructure

Lack of responsiveness by Irish Water to new development is delaying home construction,

delaying the release of completed new homes into the market, and preventing developers

from planning ahead and submitting planning for future developments. This is because Irish

Water is not sufficiently funded to support its activities. In light of the policy decision not to

introduce a universal water charge based on polluter pays principle, Government should

12PII Pre-Budget 2021 Submission

commit additional funds to Irish Water to allow it to carry out its functions. This will lead to a

reduction in the length of time it takes to develop homes and bring them to the market.

13PII Pre-Budget 2021 Submission

14. About Property Industry Ireland

Property Industry Ireland (PII) is an independent and inclusive representative organisation for

all sub-sectors of the Irish property industry.

Vision – A sustainable Irish Property Industry which is creative, responsive, competitive and

well-integrated in meeting the socio-economic needs of all the stakeholders in the built

environment.

Mission - To be the trusted partner and provider of “evidence based” information, policies and

strategies for the property industry at National level, to the Oireachtas, Government, Local

Authorities and Agencies, and for the benefit of the people of Ireland

Objectives -

• To be the leadership forum in the Industry for the discussion of National property

issues

• To develop, propose and support a National Property Strategy, policies and solutions

to issues

• To be a research led organisation, which collates and commissions relevant and &

innovative research on Ireland's construction sector in order to promote & sustain a

competitive economy

• To be the go-to organisation for Government on all aspects of property

• To work with all stakeholders in the industry to restore it to a sustainable position in the

economy.

• To increase membership through demonstrating the achievements and outcomes in

relation to national strategy and policy

PII was established in 2011 and continues to grow its membership, which now totals almost

90 firms. The organisation is actively engaged in discussions with Government, decision-

makers, agencies including NAMA and investors to help achieve a better future for the

property sector.

PII is a sectoral association of Ibec.

14Property Industry Ireland

84 - 86 Lower Baggot Street

Dublin 2 Ireland

info@propertyindustry.ie

01 605 1666

www.propertyindustry.ie

16You can also read