Proactive Investors Conference Shelbourne Hotel - 28 February 2012 Tom Hickey

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Proactive Investors Conference

Shelbourne Hotel

28 February 2012

Tom Hickey

• Company Overview and Strategy

• Algeria

•History

•Appraisal Results

•Development Planning

• Kurdistan Region of Iraq

• Italy

2

Corporate Overview

Petroceltic (AiM: PCI.L; IEX, PCI.ID) • Highly experienced team with Major E&P

Ordinary Shares in Issue 2,370 mm Company backgrounds

• Board

Market Capitalisation – Stg£ 208.4 mm

• Management

Market Capitalisation – US$ 330 mm • Technical and Commercial Teams

52 Week High-Low, Stg p 3.8 – 13p

• Recently completed 6 well appraisal

Average Daily Liquidity 13.4 mm shares

programme on multi-TCF gas condensate

Top 20 Holders(at 31 Dec 2011) 60.70% field development in Algerian Sahara Desert

• Major project, sanction in 2012, first

gas in 2017

• Recent entry into Kurdistan Region of Iraq,

2 Highly Prospective Blocks with Hess

• Over $100 mm received from ENEL in Feb

2012 , further $25-$50mm in 2012

• $30 million Macquarie Facility fully repaid

• Actively seeking new projects in MENA

region

3

A Clear Strategy To Add Value

Appraise and Monetise Algerian Asset

• Multi-Well appraisal campaign successfully completed

• Farm-out to Enel concluded

• Field “Final Discovery Report” to be filed imminently

Diversify and Balance our Business

• Maintain focus on MENA

• Skills/Expertise focus extends throughout Africa/Middle East

• Target to secure low risk post-appraisal plays

Target Transformational Growth

• Acquire or discover assets with material resource potential

• Target high initial equity interests with operator status preferred

• Active risk mitigation through farm-out and partnering strategy

• Prepared to be Opportunistic

4

Petroceltic’s Current Core Areas

• Core areas in Algeria, Kurdistan Region of Iraq and Italy in which Petroceltic

has multiple potential „company makers‟

• Significant exploration potential identified

• A portfolio of Oil and Gas Development opportunities

Isarene Permit – 6

well appraisal

campaign in 2011

5

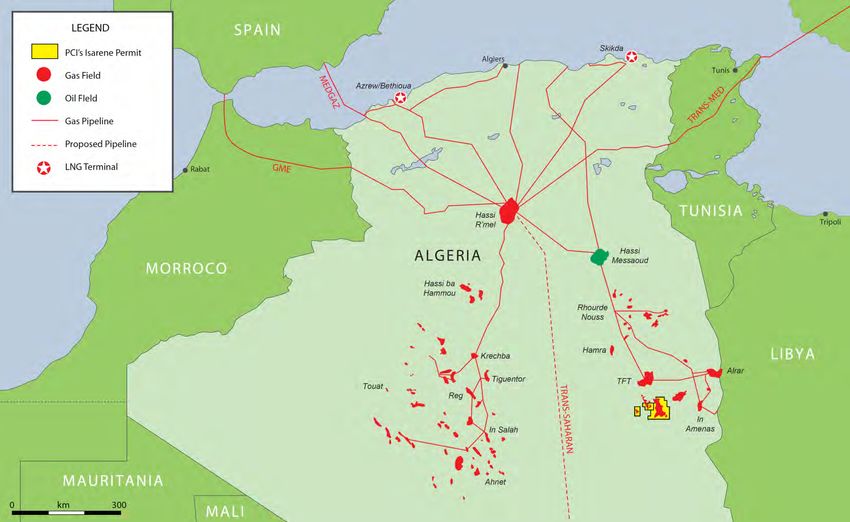

Algeria Gas Infrastructure Natural Gas Market & PCI’s Isarene Permit 6

Isarene Permit Location South Illizi Basin 7

Algeria: Successful Appraisal Programme

Well Type Objective Comment

AT-4 Vertical GIIP Outside Glacial Valley AT-8

AT-5 Pilot + Flow Rate Pop-Up (1)

Horizontal

AT-6 Vertical GIIP SE Valley AT-9

AT-7 Vertical GIIP SW Valley

AT-8 Vertical GIIP/Flow Northern Area

Rate

AT-9 Pilot + Flow Rate Pop-Up (2)

Horizontal

• 2011 drilling programme moves project towards bookable

recoverable reserve status in 2012

• Major GIIP Upgrade from appraisal programme

• AT-9 Flowed 67.6 mmscfd pre-fraccing –demonstrating

potential for high deliverability within Ain Tsila complex and

underpinning commerciality

8

Ain Tsila Gas-Initially-in-Place (“GIIP”)

• Appraisal wells have demonstrated greater gas columns and better than

expected reservoir properties - close to, or better than P10 predictions

• The range is still wide due to the large field area relative to the number of wells

• Appraisal well “step-outs” are typically >10 km

• Entire North Sea fields would fit into the gaps!

• High quality seismic covers only a part of Ain Tsila

• With a 30 year field life, higher GIIP is a key source of long-term value

Case GIIP – TCF *

Low 5.7

Mid 10.3

High 20.8

* Current Petroceltic Internal Estimates

9

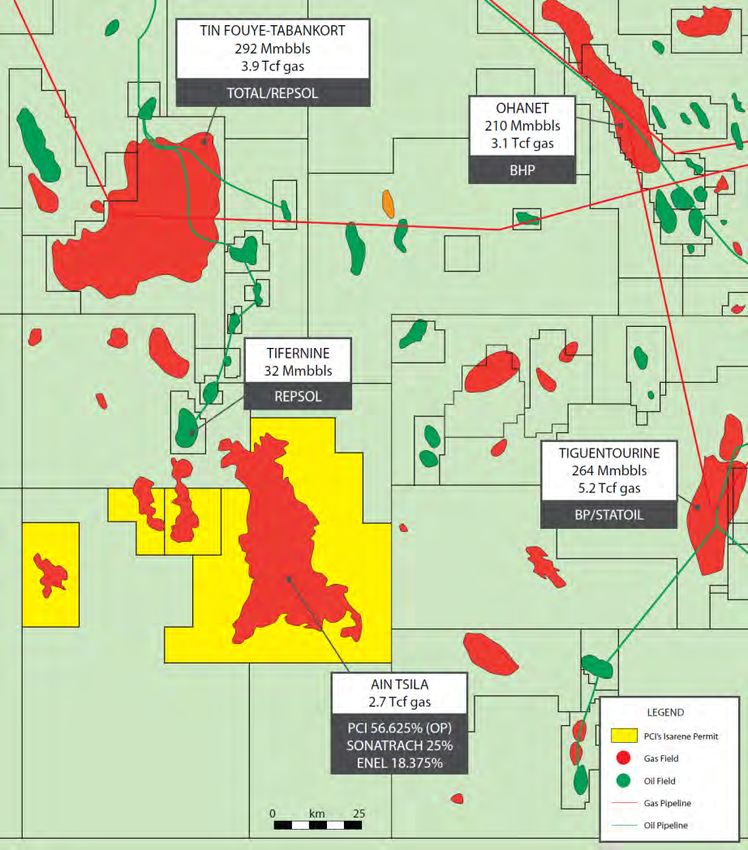

Ain Tsila Ordovician Analogues – It’s been done before

• Tignuentourine (BP/ Statoil)

– 1000 MMscf/d wet gas plateau

– ~30 wells, 3 trains

• Tin Fouye-Tabankort (Total/ Repsol)

– 700 MMscf/d wet gas plateau with

– ~40 wells, 2 trains

• Ohanet (BHP Billiton)

– 350 MMscf/d wet gas plateau

– ~12 wells, 2 trains

• Key Development Issues

– Distribution of „good‟ facies

– Distribution & density of open fractures

– Optimisation of hydraulic frac design

– Learning while drilling (tie to 3-D seismic)

• Experienced PCI team

– Ex Burlington, BHP Ohanet – directly relevant

experience

10Summary of Ain Tsila Development Concept

• Mid Case development scenario - Region 1

economically and technically robust High perm.

• Projections based on field “Sector High Fractures

Models” supported by appraisal evidence Region 2

Low high perm.

• 11-13 yr wet gas plateau rate of 400 High Fractures

mmscfd

• 654 MMboe saleable volume Region 3

• 35 wells pre first gas, > 200 wells in total, Low high perm.

• 2.4 TCF dry gas Medium Fractures

• 106 Mmboe condensate

• 109 Mmboe LPG

• Simple single train central processing

Region 5

facility, to standard industry design Region 4 No high perm.

• Significantly positive economic outcome High perm. Low fractures

for Algerian State Low fractures

• AT-9 result indicates scope for further

productivity upside – well above high-

case expectations

11Ain Tsila Outline Development Plan

First Gas

600 2,000

Cumulative Gross Capex MM USD

1,800

500

Gross Capex MM USD

1,600

400 1,400

1,200

Self

300 Financing

1,000

800

200 600

100 400

200

- -

2014 2015 2016 2017 2018

Year

Drilling Facilities Cumulative

• 35 wells to establish 400 MMscf/d wet gas plateau

• Around 200 wells in total to maintain plateau for 11-13 years, 2-3 rigs/ annum

• Gas calorific value of 1045 btu/cf

• Condensate yield 41.7 bbl/mmscf, Liquified Petroleum Gas (LPG) yield 42.9 bbl/mmscf

12Ohanet Central Processing Facility

Gas/

LPG Condensate/

spheres LPG export

Flare stacks

Condensate Gas

tanks compression

Two 350 MMscf/d Evaporation

processing trains ponds

Slug catcher

13% From Algeria

% From Libya

16%

33 34 12

% % 33 %

% 13

%

16

%

14Enel Farmout

• Enel Farm-out Announced 28th April 200

• $36.75 million in historic costs

180

• 2 for 1 Appraisal Carry– to max of $71

160

million ($145 million programme)

Contingent

• Reserves-Based contingent consideration 140 Payments

up to $75 million 2011/12

120

Contingent Bonus

• Maximum potential attributable value of c.$1 US$M

Contingent Carry

100

billion to overall Isarene project (PCI 56%) Costs- Enel

• Farm-out fully approved 80 Work Carry - PCI

Back Costs

• PSC Addendum signed 28 April 60

• Government Ratification – 18 Dec 2011 40

Firm

• Initial payment (cUS$101million)received Payments

20 2011

February 2012

0

• Contingent Payment Q3 2012 Value

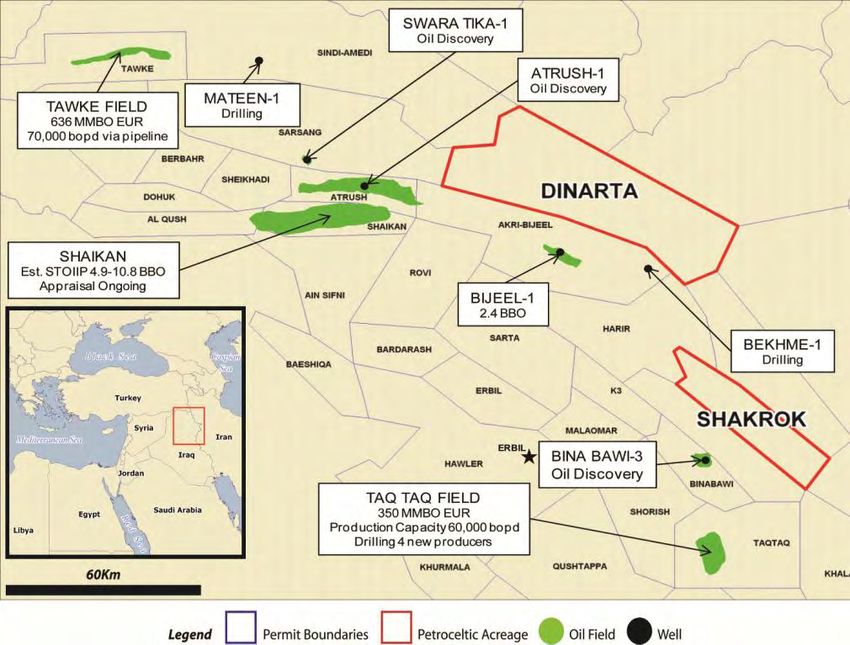

15Kurdistan Region of Iraq – High Impact Exploration Blocks 16

Dinarta and Shakrok Blocks - Transaction Overview

• Petroceltic has a 20% interest (16% participating

interest) in two highly prospective blocks in the

Kurdistan Region of Iraq

• Hess Middle East is operator of both blocks with an

80% interest (64% participation)

• Kurdistan Regional Government (KRG) has a 20%

carried interest

• Blocks were approved by the KRG on 27 July 2011,

PSC‟s fully agreed and signed.

• First Phase Financial Commitment of appx. $72

million net to PCI, inclusive of all Signature and

Capacity building Bonuses

• Recent material entrants and fundings include Hess,

Maersk, Repsol, Afren, Vallares, Gulf Keystone,

Exxon Mobil and Total

Dinarta and Shakrok both undrilled and on trend with major discoveries

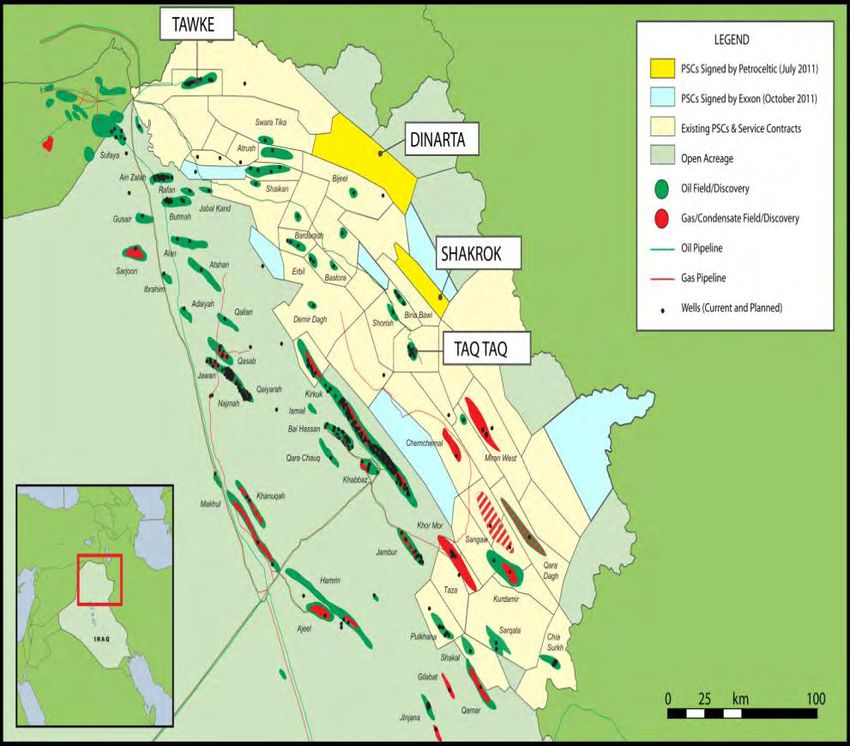

17Kurdistan Region of Iraq

Emerging World Class Province – Acreage Awards & Rapid Discovery

2007 2011

18Dinarta: Very Significant Exploration Potential

Major undrilled anticlines adjacent to world-class discoveries

• Joint Venture: Hess 64%, PCI 16%, KRG

20% (carried)

• Unexplored 1,319 sq km block with major Shireen

surface structures and extensive oil

seeps

• Multiple leads, each with very significant

reserve potential across multiple horizons Chinara

• On trend with Shaikan, Atrush and

Swara Tika oil discoveries Bradost

• Demonstrated regional productivity

• First phase work programme 500 km 2D

and 1 Exploration well Dinarta Block

• Operations to commence 2012 – 2D - 1319 sq km

seismic crews currently mobilising to field 10km

19Shakrok: Significant Exploration Opportunity

Undrilled anticlines on trend with Taq Taq field

• Joint Venture: Hess 64%, PCI 16%, KRG 20%

(carried)

• Unexplored 418 sq km Block with major surface

structures and extensive oil seeps Shakrok

• Leads with billion barrel potential across multiple

horizons

• Adjacent Taq Taq field (Addax/Sinopec)

produces 60,000 boepd of 46° API oil

• Offsetting Bina Bawi oil discovery

Pelewan

Shakrok Block

• First phase work programme 250 km 2D and 1 418 sq km

Exploration well 10km

• Operations to commence 2012 – 2D seismic

contract recently awarded

20Kurdistan Region of Iraq

Undrilled Surface Anticlines

Undrilled Pelewan Anticline, Shakrok Block

21Italy – Building for Success 22

Petroceltic Italia

Major value creation potential in Italy (in spite of DL 128…)

• E&P activity continues despite challenges

created by DL128

• Onshore

• Offshore outside 12 mile zone

• Rovasenda - potentially transformational

• Planned 4Q 2012 spud

• Risk mitigation via farm-down

• Strongly positioned to exploit success

• Offshore Abruzzo

• BR268 suspended for duration of legal

appeal

• Applications outside 12 nautical mile limit

progressing towards award

23Petroceltic Italia

Western Po Valley Core Area

2010 Award of Ronsecco Permit

2011 Transfer of Carisio Operatorship to Eni effective

– Licence for all seismic data in Carisio & Ronsecco

2012 Rovasenda Well – permitting, site selection, commercial planning, PCI farmout, drilling

preparations.

24Petroceltic Italia

Offshore Abruzzo Core Area

Granato

• BR268 suspended pending judicial review 35 mmbbl PR

• E&P restricted within 5-12 nautical miles of

coastline (DL 128)

• Extension of high-graded Elsa

play fairway into outboard area

– Environmental applications approved for

4 of these applications; 1 pending

– Expectation that licences will be

awarded in 1H 2012

• Fast-track technical evaluation once licences

Opale

awarded – with seismic acquisition

220 mmbbl PR

25Corporate Overview

Petroceltic (AiM: PCI.L; IEX, PCI.ID) • Highly experienced team with Major E&P

Ordinary Shares in Issue 2,370 mm Company backgrounds

• Board

Market Capitalisation – Stg£ 208.4 mm

• Management

Market Capitalisation – US$ 330 mm • Technical and Commercial Teams

52 Week High-Low, Stg p 3.8 – 13p

• Recently completed 6 well appraisal

Average Daily Liquidity 13.4 mm shares

programme on multi-TCF gas condensate

Top 20 Holders(at 31 Dec 2011) 60.70% field development in Algerian Sahara Desert

• Major project, sanction in 2012, first

gas in 2017

• Recent entry into Kurdistan Region of

Iraq, 2 Highly Prospective Blocks with Hess

• Over $100 mm received from ENEL in Feb

2012 , further $25-$50mm in 2012

• $30 million Macquarie Facility fully repaid

• Actively seeking new projects in MENA

region

26You can also read