Real Assets and Inflation Hedge Investing

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Real Assets and Inflation Hedge Investing

Edward J. O’Donnell III, CFA

Consultant

Executive Summary

An allocation to Real Assets can play an important role in a long-term investment portfolio. Real As-

sets encompass an array of investment strategies whose values are sensitive to inflation and include

TIPS, commodities, commodities-linked stocks, commodities-oriented hedge funds and hedge funds of

funds, and direct investments in real estate, energy, farmland, timber, and infrastructure.

In strategic asset allocation, we recommend that clients balance the risk in their portfolios among equi-

ties, fixed income, alternatives (hedge funds and private equity), and Real Assets. An allocation to

Real Assets can provide significant diversification due to the relatively low correlation of most Real As-

sets strategies to traditional economic-growth sensitive assets such as stocks (both U.S. and non-U.S.)

and credit-linked securities such as corporate bonds. An allocation to Real Assets can also provide

protection for an investment portfolio against high inflation, an extreme economic outcome that can be

very damaging to many investment portfolios. Real Assets can benefit from rising input prices and

thereby offer purchasing power protection to investors by acting as a hedge against inflation.

In the current environment, fiscal and monetary policy-makers in the U.S. and abroad are pursuing

heavily stimulative policies to combat deflation and spur economic growth. Central banks also intend

to prevent high inflation. The risk we face is that the Fed and others fail to execute a “soft landing” be-

tween these two extreme environments. We believe that high inflation represents a significant risk.

As a result, NEPC recommends that clients allocate between 5% and 15% of their capital to a Real

Assets portfolio. Clients with more inflation-sensitive liabilities, such as defined benefit plans with

COLAs or endowments seeking to maintain purchasing power of assets, may want to allocate more to

Real Assets. Given the current environment, we recommend building a diversified Real Asset program

and allocating toward the high end of the strategic range.

Real Assets and Strategic Asset Allocation cation and risk budgeting processes. Understand-

ing how different financial instruments, and client

Scenario analysis is an integral component of the investment portfolios, respond to these various en-

asset allocation process at NEPC. As part of our vironments guides the framework for our asset al-

ongoing strategic research, we examine market location recommendations.

conditions and consider how changes in various

critical factors (e.g. interest rates, economic From the strategic perspective, rising inflation is

growth, volatility, inflation) contribute to broad in- one market condition that we recommend many

vestment and economic regimes such as stagfla- clients consider hedging their portfolios against.

tion, expansion, or recession. Properly positioning We recommend a 5-15% strategic allocation to

investment portfolios to weather these various mar- Real Assets. For those clients facing explicit infla-

ket regimes is an important part of the capital allo- tion hedge needs, a higher allocation may be war-

Real Assets Investing 1 August 2009

ranted. Real Assets can play an important role inventories—potentially leading to higher prices

in institutional client portfolios by helping to pre- in Real Assets over the long term.

serve their purchasing power as inflation rises,

providing a “real” or inflation-adjusted return. Thus, both dollar inflation and commodity input

Heightened attention to meeting liabilities and a price inflation could increase over the long term

rapid expansion in the magnitude and scope of horizon. Higher inflation is among the greatest

exogenous events—among them rising infla- risks investment portfolios face. Unfortunately,

tion—highlight the strategic advantages of Real many plans are under-exposed to Real Assets.

Assets to investment portfolios. Fortunately, insurance against inflation is rela-

tively cheap.

Potential Tactical Opportunity

Benefit: Inflation Protection

Whereas the strategic recommendation is to

hedge portfolios against the base case of infla- Many institutions face annual liability require-

tion (e.g. 3% long-term average), current market ments and employ liability-sensitive investment

conditions may present an attractive entry point. strategies to help meet them. One of the big-

The current cost of inflation insurance, or invest- gest threats to meeting a liability can be the loss

ing in Real Assets, relative to the longer term of purchasing power due to inflation. Endow-

risk of inflation rising is quite compelling. The ments and foundations face particular chal-

dislocation in valuation seems large enough to lenges with regards to inflation, as their principal

be attractive and actionable. Investment pro- liability — an annual spending target — is very

grams face a small but credible chance of high inflation-sensitive. The liabilities of many other

inflation; a “fat tail” against which it may make institutional clients can also be inflation sensi-

sense to protect the portfolio. tive, especially if they contain a cost-of-living

adjustment (COLA).

As global central banks increase money supply

to inject liquidity and confidence in their mar- There may, however, be circumstances in which

kets, one natural consequence of these mone- certain investment portfolios (e.g. corporate

tary policies is the potential devaluation of paper pension plans employing asset-liability matching

currency relative to real—or inflation-adjusted— strategies) actually benefit from rising inflation.

assets (i.e. the US dollar will be worth less while The status of the net plan (liabilities less assets)

commodities will be worth more). Further, with for these portfolios may improve during rising

the current lower commodity prices comes a inflation. The decreased liability due to a higher

decline in capital spending by commodity pro- discount rate may outweigh any asset-related

ducers; global inventories are low, causing re- declines caused by higher inflation. Further, cli-

cent supply destruction. ents with strategies already emphasizing a ris-

ing rate environment may need to size their allo-

Yet longer term demand for commodities is cation to inflation hedging assets accordingly, to

likely to rise. The sequence of recovery in balance the portfolio’s positioning relative to a

global capital markets may likely be improving variety of potential economic scenarios.

credit and liquidity conditions in bond markets,

followed by earnings growth and valuation ex- Nevertheless, rising inflation can significantly

pansion in equities, followed by rising demand erode the value of an institution’s financial as-

for global natural resources—buoyed in part by sets. Gains in inflation can mean losses in a

stimulus packages. Future higher global de- traditional investment portfolio, as they can de-

mand for natural resources would meet with low crease the value of dollars spent and may re-

Real Assets Investing 2 August 2009

quire liquidation of assets to continue funding for an example of Real Assets’ impact on portfo-

liabilities. lio risk and return).

We expect inflation to rise longer term. Unfortu- The low correlation of returns among Real As-

nately, many institutional investors have low ex- sets provides an additional diversification bene-

posure to the types of assets that can protect fit. A well-diversified Real Asset program has

their portfolios against inflation. exposure to a variety of asset classes, taking

advantage of this low correlation and mitigating

Benefit: Portfolio Risk Reduction the portfolio risk of any one asset class or mar-

ket sector experiencing a short-term correction.

Real Assets can benefit an investment program (See Appendix, Exhibit 5, for Real Asset intra-

by diversifying the portfolio, thanks to the low correlations)

correlation of Real Assets to most other finan-

cial instruments. The counter-cyclical nature of Real Asset Classes

Real Assets can help the overall portfolio

achieve better risk-adjusted returns. There are several distinct categories of invest-

ments considered Real Assets. Each has

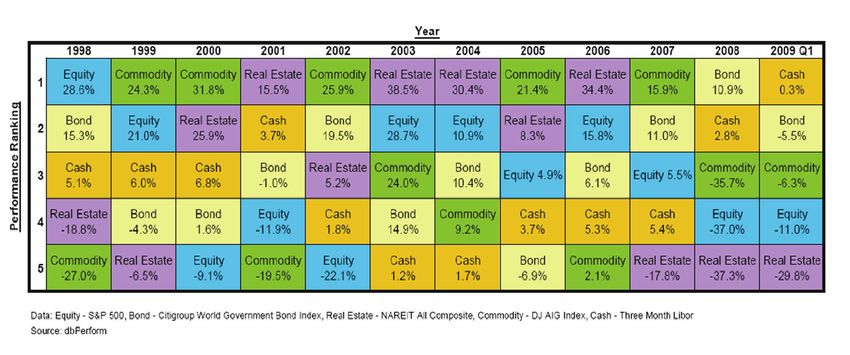

Exhibit 1, below, depicts how different asset unique characteristics (e.g. risk/return profile;

classes perform in diverse market environ- liquidity) and a different degree of inflation

ments. Real Assets can rise in value when eq- hedge. Real Asset investment categories span

uities and fixed income instruments fall. This is many markets and asset classes, including:

because the underlying return drivers for Real

Assets are distinct from the market forces that Treasury Inflation Protected Securities

drive most stock and bond prices. The conse- (TIPS) and global inflation linked bonds

quent low correlation to these traditional assets Commodities: Energy, Industrial & Pre-

can enhance portfolio diversification and reduce cious Metals, Agriculture & Livestock

overall risk. Inflation-sensitive equities: Energy; Real

Estate; Infrastructure; Metals; Agriculture

Note the low correlation between Real Assets Real Estate

(e.g. commodities) and traditional markets Direct investments in Energy, Timber,

(stocks & bonds) in Exhibit 2. A strategic alloca- Farmland, and Infrastructure

tion to Real Assets can help improve risk-

adjusted returns for a variety of long-term in-

vestment portfolios. (See Appendix, Exhibit 6,

Exhibit 1

Real Assets Investing 3 August 2009Exhibit 2

The categories above and the historic correlations relate to the proxy assets and their actual quarterly returns generally over the period of 1991 to 2009. The

correlations calculations are based on the historical returns. The actual correlations in the future of each of the asset classes may differ substantially from the

historic correlations of these assets. The use of historic correlations is to demonstrate the relative market movements of distinct asset classes.

As global economic dynamics change and mar- a variety of market environments.

kets evolve, “inflation” becomes redefined with

new consumers and products emerging. Sec- Liquid commingled funds are available that can

tors such as Agribusiness and Climate Change provide investors either dedicated or broad ex-

are poised to benefit from global secular trends; posure to public inflation hedge markets. Mean-

growth in these investment themes may out- ingful exposure to some Real Assets (e.g. TIPS,

pace inflation. Importantly, investment in these Commodities) may also be gained through di-

new inflation-hedge sectors may help provide versified Global Asset Allocation managers.

an effective hedge against inflation, as part of a

well diversified Real Assets strategy. For specific, dedicated access to a given asset

class (e.g. Energy, Agriculture) investors can

Real Asset Investment Strategies hire managers with strategies focused on one

investment theme. For more broad Real Asset

There are many ways for investors to access diversification within one portfolio, there are also

Real Assets. These range from liquid expo- managers who invest in several strategies

sures in Commodities funds and publicly-held oil across the Real Asset spectrum. Some manag-

or mining companies to commodities-focused ers will even tactically allocate among these

hedge funds and direct investments in real es- sectors, seeking additional opportunities to en-

tate, energy, farmland, timberland, or infrastruc- hance return and/or mitigate portfolio risk.

ture. Exhibit 3 summarizes Real Asset invest-

ment strategies. Real Asset-related hedge funds, particularly

those employing a long/short strategy, may di-

We recommend pursuing a Real Asset invest- minish some of the potential inflation benefit as-

ment program that is well diversified by asset sociated with Real Asset investing due to their

class and along the liquidity spectrum—to maxi- use of shorting. Their potential to generate su-

mize the program’s risk-return potential through perior absolute returns within global natural re-

Real Assets Investing 4 August 2009Exhibit 3

Source: NEPC, LLC

source investing, and to provide downside pro- eral important characteristics such as its liquid-

tection, however, can make these hedge funds ity, risk, time horizon, and sensitivity to dynam-

an important component of a well-diversified ics in the underlying commodities. Importantly,

Real Asset investment strategy. these factors also impact an asset’s inflation

hedging potential. The closer a company is to

Direct private investments in less liquid closed- the commodity or “upstream” the more likely it is

end Energy, Real Estate, Infrastructure, or Tim- an effective inflation hedge; the closer it is to the

ber funds are also available, and can represent consumer or “downstream” the lower its inflation

a robust component of a long-term Real Asset hedge potential. This is especially true for infla-

program for investors willing to make allocations tion-sensitive equities (e.g. companies in the

to illiquid vehicles. Energy, Agriculture, and Mining industries).

Degrees of Inflation Protection Where an investment lies along the liquidity

spectrum in global capital markets can also in-

Over the long term, we expect traditional global fluence its potential to provide inflation protec-

equities to continue to provide investors a good tion and correlation benefits to the portfolio.

inflation hedge. Many rising input costs can ulti- Publicly-traded companies are more closely

mately be passed along the value chain to linked to stock markets and may not outperform

maintain company profit margins. Nevertheless, during periods of rising inflation. However, di-

it is during extended periods of rising inflation, rect inflation-sensitive investment opportunities

especially of the unanticipated variety, that Real are less correlated with traditional markets

Assets offer investors the best inflation hedge (stocks and bonds) and can be more highly cor-

and portfolio diversification benefit — just when related with inflation. A good example of this

it’s needed most. difference is private Energy investing as op-

posed to public, downstream Energy equities.

Where a company lies along the supply chain in

a given industry has direct implications for sev- The degree to which Real Asset-related invest-

Real Assets Investing 5 August 2009Exhibit 4

Asset Sensitivity Liquidity Ease of Degree of Return profile Comments

to Inflation Implementation Market

Efficiency

TIPS Moderate High High High Low volatility Pegged to the CPI

Modest income – inflation not

Longer duration included in this

index will not be

reflected in TIPS

Commodities High High High High High volatility Most volatile

No income

Real Estate – Low High High Moderate/ Volatile returns; REITs correlate

Public (REITs) High some REITs have historically most

high dividends highly with s/mid

cap stocks

Real Estate -- Moderate Low Low Low Depends on Infl. sensitivity

Private strategy (some depends on type

with more income, of real estate (e.g.

some with more construction);

cap. appreciation) current

environment

Energy – Public Low to High High Moderate/ Volatile returns Energy stocks are

Moderate High volatile and

affected by swings

in stock market

Energy – Private Low to High; Low Low Low Depends upon Volatility depends

see Return commodity hedge on strategy risk

and position in and hedge to

Profile “value chain” commodity

Timber/Farmland High Very Low Very Low Low Lower volatility; Limited universe

income component of managers.

Source: NEPC, LLC

ments have leverage on their balance sheets (a Exhibit 4 summarizes the relative attributes of

high debt-to-equity ratio) impacts their ability to Real Asset investment strategies in greater de-

protect against rising inflation. The inherent in- tail.

terest rate risk associated with higher leverage

can diminish the inflation-protection potential. Risks of Real Asset Investing

Within inflation-linked bonds, non-US$ bonds

There are important risks to consider with Real

may offer superior inflation protection than US

Asset investing and each underlying public as-

TIPS alone, as investors seek to protect against set class comes with its own unique risks. A

a loss of dollar value in their portfolios. TIPS-specific risk may be the inherent weak-

Conditions in Real Asset markets will vary over ness of CPI as a true measure for inflation; for

time; along with these changes comes a fluctua- Commodities it could be spot price volatility; for

tion in each asset class’ inflation hedge poten- the Energy sector it may be geopolitical tension;

tial. For example, current conditions in the di- for Timber it could be fire; for Agriculture the

rect Real Estate markets are not favorable for weather is an important risk to consider.

inflation protection, due in part to declining

In addition to these asset-class specific risks,

valuations, high vacancy rates, and high debt

private investments in Real Assets bring other

ratios.

Real Assets Investing 6 August 2009risks to consider. Among these are illiquidity Conclusion

(long lead times are required; lock ups are

likely); vintage year risk (market cycle timing); We recommend that clients strongly consider a

and lack of a transparent pricing mechanism. strategic allocation to Real Assets. The poten-

Nevertheless, all Real Asset investments share tial portfolio benefits are considerable and the

some common risks, principally low correlation risks are manageable. A 5-15% strategic alloca-

to paper assets, high sensitivity to macro- tion in an investment portfolio can help maintain

economic cycles, and manager selection risk. purchasing power, preserve asset value, and

enhance risk-adjusted returns. The specific com-

While the counter-cyclical nature of Real Asset bination of Real Assets investment strategies

strategies can provide good portfolio diversifica- (e.g. asset class allocations and liquidity) should

tion benefits, particularly during times of rising be determined based upon client-specific invest-

inflation—when stock markets suffer, this low ment objectives and constraints.

correlation can be a hindrance during periods

when stock markets generate high returns. In We believe that making a long term commitment

strong bull equity markets, investments more to Real Assets is important, as the key benefits

correlated with rising stock prices would likely are strategic in nature. Further, a long-term ho-

perform best. rizon helps reduce some concerns about illiquid-

ity, volatility, and vintage year risk. Though

Real Assets as a group are very sensitive to near-term conditions may present an attractive

macroeconomic trends, which can be highly cy- entry point, a broader perspective on the strate-

clical. The level of global demand for natural gic benefits of a Real Asset allocation to your

resources like copper and zinc, oil and natural investment portfolio for long-term investors is

gas, corn and wheat, and gold and silver impact also important. As they build their Real Asset

commodity prices as well as the values of the programs, we believe that investors should:

related companies and industries a great deal.

Understand the potential benefits of adding Real

Rapid growth in developing market countries, Assets to your portfolio. Consider the possible

led by the industrialization and urbanization of long-term advantages of inflation protection,

emerging markets like China and India, has cre- volatility reduction for the overall portfolio via low

ated a surge in demand for energy, metals, and correlation, and higher risk-adjusted returns.

food amid continued supply constraints in global Ensure that all investment decisions are driven

natural resources. The resulting supply/demand by sound policy rationales: think strategically,

imbalance has caused dramatic price volatility in and consider acting tactically.

many commodities. An economic slowdown in

these emerging markets, particularly China and Balance the potential benefits of Real Asset in-

Brazil, could certainly impact expected returns vesting with other client-specific requirements.

among Real Assets. Consider liquidity needs and time horizon, which

impact your risk tolerance and asset allocation.

Changes in the value of the US dollar also have

a strong impact on commodities and commodity- Position your portfolio strategically by diversify-

related equities, as most global commodities are ing the inflation-hedge approaches you employ.

traded and priced in USD. Manager selection is Expand the opportunity set with broad exposure

an important consideration for Real Asset invest- to the many asset categories and take advan-

ments. The disparity of manager returns is often tage of the low correlations among Real Assets.

wider among alternative asset strategies. Leave tactical shifts to proven active managers.

Real Assets Investing 7 August 2009A well-diversified strategy should include expo- Manage risk by using an approach that is well-

sure to several Real Asset investments (e.g. diversified by asset class and liquidity, making a

Commodities, REITs, Agriculture, Energy) as long-term commitment to inflation hedges, and

well as exposure to different levels of liquidity, ensuring in-depth manager due diligence.

for example from the high liquidity of TIPS to the

long time horizon of a direct Energy investment. We look forward to working with clients to help

them evaluate and implement, as appropriate,

Start simple. Begin with the most liquid ap- an effective Real Assets program.

proaches, later incorporating less liquid invest-

ments as part of a longer-term strategy. Begin

with core diversified funds and complement I would like to thank Erik Knutzen for his tireless

these with more direct investments over time, support and guidance, Mark Cintolo for his help

working gradually toward a core-satellite ap- with data and charts, and Cheryl Grant for her

proach. Global Asset Allocation portfolios are invaluable editorial insights.

one way to gain some Real Asset exposure.

NEPC, LLC is an employee owned, full service investment

consulting firm. Founded in 1986, NEPC is one of the largest

Be aware of the risks associated with Real Asset independent firms in the industry. We are headquartered in

investments. There are asset class-specific Cambridge, Massachusetts and have additional offices in Detroit,

risks, liquidity-related risks, and macroeconomic Michigan; Charlotte, North Carolina; Las Vegas, Nevada; and

San Francisco, California. You can reach us at (617) 374‐1300.

risks — each with potential consequences. www.nepc.com

Appendix

Sources for charts and tables throughout the Appendix is NEPC, LLC, unless otherwise indicated.

Exhibit 5

1/1/1991 to 3/31/2009; Source: S&P/GSCI; DJ/UBS

Real Assets Investing 8 August 2009Exhibit 6

Exhibit 7

Note: Asset class return streams, as indicated in Exhibit 7, were used for the correlation chart in Exhibit 2 and the

efficient frontier chart in Exhibit 6.

Real Assets Investing 9 August 2009You can also read