Rebound Perspectives 2021 - Perspectives 2021 - CONCEPT Vermögensmanagement

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Perspectives 2021

Rebound

Perspectives

2021

Perspectives 2021

REBOUND

2020 saw the biggest pandemic since 1918 and the worst recession since the World War. It will lead to bigger

changes in our (social) life than any other year before. However, for all the negatives associated with the

pandemic and the continuing challenges we face, we have also seen the willingness of people to stand

together, to come to terms with what is required of them, and their ability to adapt to dramatically changing

environmental conditions and to sustain our socio-economic system.

At this point, most readers would expect a (by now rates of over 6 %. Countries have resisted the

traditional) summary of the theses discussed here: spread of the virus with massive restrictions on

The economic stimulus measures taken by public life, economic activity and personal rights.

governments and central banks seem sensible and From A for Australia to Z for Zimbabwe, lockdowns

effective; there would hardly have been any better were the order of the day, sometimes for more

alternatives. Against the background of the than three months. Politicians and central banks

signalled willingness to continue to do everything provided considerable support to mitigate the

necessary to maintain our socio-economic economic – and thus the social – consequences of

conditions, the economic environment should be the pandemic. In contrast to the financial crisis of

able to recover its strength again. Catch-up effects 2008/09, these measures were taken in a

are possible in a number of areas, which justify and coordinated manner, simultaneously and without

further support the advance of the capital markets. hesitation. To finance aid packages, governments

A well-founded assessment of the short-term ran up a total deficit of about 11% of global GDP in

prospects is not possible in any serious way 2020, while central banks provided a total of $5

because it depends on the success trillion in “fresh money” (among other things, to

of the response to the pandemic. Financial aid has significantly increased again since spring

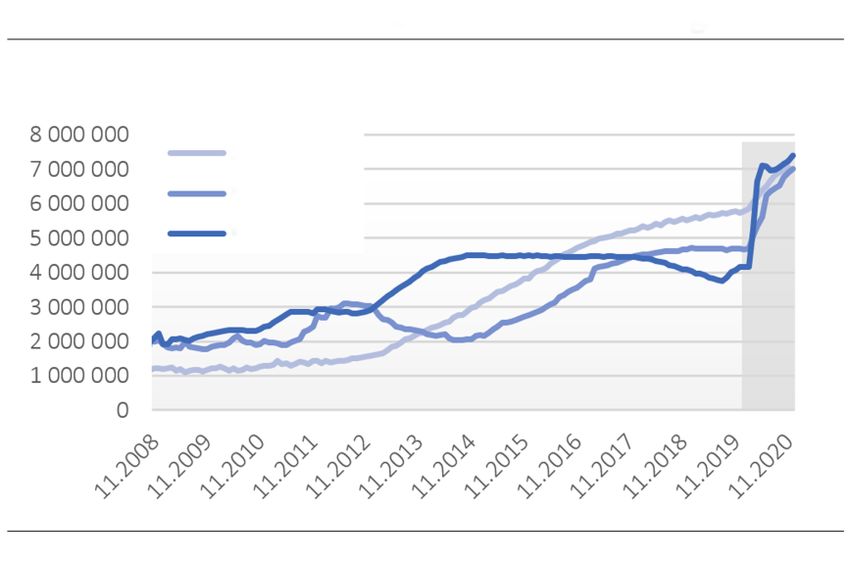

In retrospect, 2020 was the big BILL. USD

cut, when the global economy Other G20

slumped like never before after G7

the end of World War II. According

to IMF estimates, the world

economy will have shrunk by over

4 % and world trade will have

weakened by over 11 %. China is

the only country that is able to

leave the pandemic behind with a Apr 2020 Dec 2020 Apr 2020 Dec 2020

mini-growth of about 1 %, which, Subsidies Loans/guarantees Subsidies

however, is also almost COVID-19 Financial

tantamount to a recession for a crisis

Source: IMF, Fiscal Monitor 04/2020 and 10/2020

country that is used to growth

Perspectives 2021

refinance those very deficits). Where existing quarter at the latest, and thus of an early and

agreements would have limited the desired new strong recovery of the economy. This would offer

debt (Maastricht criteria in the EU), they were a medium-term perspective for the majority of the

overridden. Where there was still room for interest working population to be able to earn secure

rate cuts (in the USA), they were made. The long- income again, without which the foundation of our

stalled euro bond is now also a reality. Whether all social existence together threatens to erode. Not

of these measures were actually necessary is hard least, the refinancing of the recently raised debt is

to know, even in retrospect. Taken together, they based on the ability to generate income.

prevented the global economy from falling back

into a protracted economic and financial crisis. The events on the capital markets in the past year,

which was very challenging in this respect, were

Central banks flood the market with fresh money again interesting, sometimes striking,

but in any case instructive. You

might be tempted to say “You're

looking younger than ever” as the

100 Mill. Yen

markets do not look like they are in

Mill. Euro the deepest crisis of the post-war

Mill. USD period. Knowing that there is a 5%

world recession, hardly anyone

would have drawn the conclusion

that many stock markets – with the

exception of the Euro Stoxx, for

example – would still exit the year

with a plus. On the contrary, those

who had low investments in

equities in March, at the time of

Source: FED, OECD

the first lockdowns, were happy.

The experience of the three previous recessionary

IN THE MIDST OF THE PANDEMIC

phases1 strongly suggested staying underinvested

Nevertheless, not all problems were solved, and in anticipation of an economic slump of historic

many were merely postponed to the future. dimensions.

International public debt has reached a new level, 1 Mean loss during the comparatively weaker recessions of

and dealing with it will weaken the economy’s 1990-91, 2001, 2007-09:

potential for years. Productivity in many sectors S&P 500 28 %, DAX 38 %

may be permanently affected, and some sectors of

the economy will probably never return to their Once again, however, the markets were impressed

pre-crisis levels. In spite of all this, and despite the by the central banks’ determination to do

vaccination strategy that has been initiated in the whatever was necessary and even go beyond it as

meantime, we unfortunately cannot talk about a precaution. The further decline in interest rates

having the pandemic “under control”. and the signalled willingness of the

Currently, infection and mortality rates Some sectors of the central banks to refinance new debt

are at a peak that far exceed the peaks economy will probably indefinitely made it easier for

in the spring of 2020. New lockdowns never reach their pre- governments to adopt emergency

were and continue to be necessary. crisis levels again. budgets with substantial budget

They are tougher than in the spring and deficits, thereby selectively

will in all likelihood weaken the economic data of supporting the economy and compensating

the past year again. However, the vaccination people for the effects of the imposed recession.

campaign that has been launched worldwide is Setbacks in the fight against the pandemic only

associated with the hope of an ultimately caused irritations to the markets for a very short

successful containment of incidence rates, of far- period. We did indeed see in autumn that a

reaching relaxations of restrictions in the second worsening situation in incidence figures did trigger

Perspectives 2021

worse economic forecasts for 2020 and 2021. The Interest rates have remained low for a long

However, apart from a brief period of pre-election time. People have been saying this for a few years;

uncertainty in the US, stock market prices now it needs to be underlined. Christine Lagarde

continued to rise, as the markets expected further already pointed out at the end of October that the

support measures followed by what would ECB had sufficient intervention instruments to

probably be a delayed but even stronger rebound provide support where necessary. In doing so, she

of the economy. also called into question the unanimity principle in

the ECB Governing Council and the distribution

The current situation also appears to proportionality within the EU. At the

apply: Although we have not yet Market participants

same time, the US Fed has rejected all

overcome the worst recession of the see a future “after”

expectations that it would try to nip

last 70 years, market participants are the crisis. emerging inflationary tendencies in the

already looking ahead to the future bud. On the contrary: The inflation

after the recession. Since the vaccination target of 2% was redefined. Consequences would

campaign began, the situation appears to be be enforced only if this mark is exceeded on a

manageable and the crisis is now regarded as a multi-year average. Short-term overshooting of

foreseeable short-term disruption. The recent the mark would not be a reason for action.

exponential increase in the number of infections as

well as new lockdowns have not changed this Since last year at the latest, central banks have

attitude, because governments and central banks now entered into a liability union with

have also reacted clearly: In mid-December, for governments: With their willingness to refinance

example, the ECB increased its Pandemic even the extreme new debt by buying government

Emergency Purchase Program (PEPP) by 500 bonds, they have implicitly agreed to no longer put

billion, while the USA launched a 900 billion USD a price on money in the long run. A return to

stimulus programme just a few days ago. normal conditions, where interest was the price of

money, would trigger an economic disaster and

WHAT ARE THE ISSUES IN 2021? political earthquakes including state bankruptcies.

That is why inflation remains on the wish list of

It is safe to assume that 2021 will be dominated by those in charge, because on the one hand it is

the management of the pandemic and (administered in moderation) an enticement for

theeconomic recovery. The foundational effects the economy and on the other hand it is the basic

should not be underestimated here: In Europe, for condition for reflation, i.e. the possibility to

example, corporate profits fell by half in the devalue (government) debt via inflation at

second quarter of 2020. If they were to return to simultaneously low interest rates.

only 80% of their initial level in Q2

2021, this would correspond to an Rebound in sales and profits possible

increase of significantly more than

60%. In 2021 as a whole, profits

could rise by a good 40 % for

European companies and 25 % for S&P 500 turnover

American companies (where profits S&P 500 profit

have fallen less sharply). In order to

STOXX 600 turnover

see these kinds of rates of increase STOXX 600 profit

in the past, we have to go back to the

period after the internet bubble

burst. However, these expectations

appear realistic, provided that the

vaccination strategy achieves its

2020 Q1 2020 Q2 2020 Q3 2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4

anticipated success.

Source: Refinitiv, l/B/E/SPerspectives 2021

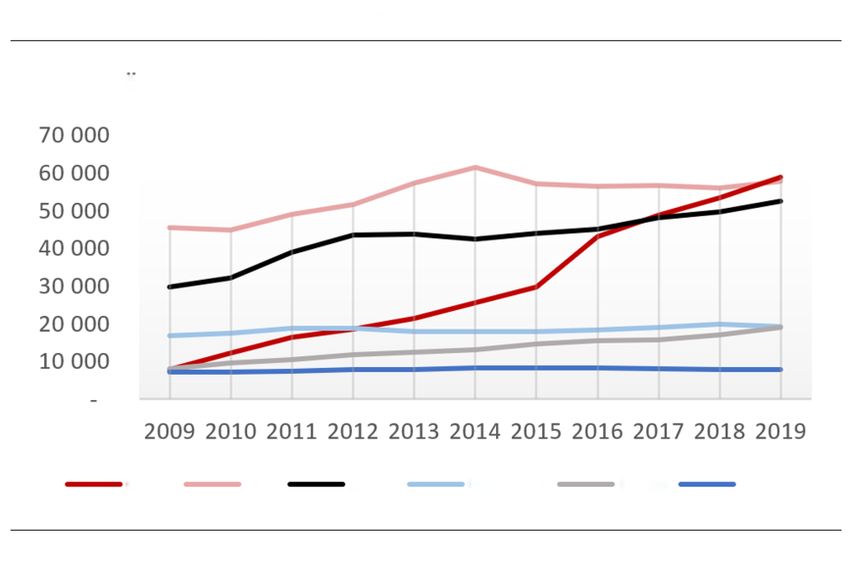

Apropos inflation: At the moment, we cannot see predicament if income is expected but this is

it anywhere. Capacity utilisation is currently low, supposed to be based on an investment strategy

employment figures are not declining more with as little risk as possible. At the latest since

strongly thanks to reduced-hours furlough and interest rates were also defined at zero in America,

comparable schemes. Consumption remains risk appetite has been the inseparable companion

subdued, and there is currently no scope for price of returns. The evergreen TINA remains at the top

increases across the board. In the USA, the of the charts. - There Is No Alternative, whereby

inflation rate was most recently 1.2 %, and in the “no alternative” once again means stocks. Even

EU - 0.3 %. Even in China, inflation has fallen previously staunch “deniers” will no longer be able

dramatically, from over 5% in January to just 0.5% to argue past this asset class and will have to

in November. This seems implausible given the accept higher risks. This will be true despite some

amounts of “fresh money”, but it can be explained expectations that achievable returns will flatten

by the lack of throughput in the real economy, across all asset classes. New risk-averse market

because money also has a viral effect. The participants may also contribute to the increase in

economic constraints affect money in the same volatility. However, especially against the

way as the virus – it is prevented from spreading. background of the expected reflation, equities

That is why so much of it is needed, not only to offer better opportunities to compensate for the

compensate for lost income, but also to prevent effects of currency devaluation.

the economy from collapsing.

The argument for stocks also remains superficially

superior to the argument that the

Inflation not an issue global economy as well as earnings

development will, on balance, take

a zero turn in 2020-21, while stock

market prices have already

increased in price. The valuations

are currently very ambitious. That

makes sense. However, Covid-19

will eventually disappear, while all

that money will stay in circulation.

The M1 money supply in the US,

Europe, Japan and China

combined has increased by about

Inflation USA

$6 trillion or 20% since February.

Inflation Euroland Inflation China

And some of it found its way not

Source: Fed, Bundesbank, global-rates.com

into the economy, but onto the

stock exchange.

It will not be easy to recapture the recent trend

towards massive debt again. That is because NOT FREE OF CONTRADICTIONS

governments have learned how easy it is, that it

costs nothing and that the reward is better public The comments made so far on interest rate and

opinion polls. Any new debt can be financed – at inflation expectations, on debt propensity and on

the moment. the tangible economic recovery are all

“mainstream” and are seen as such by the majority

NO RISK, NO RETURN of market participants. Many have internalised the

fact that Article 3 of the Cologne Basic Law2 has

Against the background of these basic also been a good stock market rule for equity

assumptions, we can no longer expect to receive a investors over the last decade.

waiver in the form of a return for supposedly risk-

free investments. Foundations, pension funds and

institutional investors worldwide are now in a

2 Cologne “Basic Law”, Article 3: Things have always gone wellPerspectives 2021

The credo here is that the central bank ultimately DIFFERENTIATION ATTEMPTS

redeems the capital markets from all evil,

whatever the cost. However, those who have In an attempt to avoid investments that could

settled into this opinion and invested their prove to be a mistake in retrospect, the relative

portfolios accordingly are no longer available as attractiveness of asset classes could be used:

buyers to drive the market further or to support it

in phases of weakness. If the majority thinks this Stocks appear expensive in an historical

way, it can be dangerous for the overall market comparison with themselves. Compared to

view. In this respect, the pro-stocks argument is bonds, however, they are cheap.

not free of contradictions. After the strong rise in growth stocks, value

stocks are still comparatively cheap.

After all, valuations are very high and rank at least Five tech giants from the 500-stock American

in the upper quartile for all asset classes – whether S&P 500 have risen exorbitantly, pulling the

for equities, real estate, bonds, or even bitcoins. whole market along with them. Things may be

Some classic valuation measures, such as the exaggerated for these five,2 while the other 495

price-earnings ratio (P/E ratio), are in some cases stocks have moved little in total and appear

no longer even discussed because they seem to be comparatively cheap.

useless. That is because in relation to the bond

In general, the American market seems more

yield, the approximately justified P/E ratio tends

expensive than Europe. Not only because the

towards the reciprocal of just under zero, i.e.

indices have performed better, but because

towards infinity. But other valuation measures,

from today’s perspective the potential for

such as the price-to-book ratio, are also high in

economic recovery may be greater in Europe.

many markets. The S&P 500 for example exceeds

A number of tech stocks have performed very

4 times its book value, which was last seen only

well because their business model proved itself

during the emerging internet bubble. While the

during the crisis and triggered rising sales and

markets fell sharply for several years at that time,

profits. Meanwhile, a number of cyclical stocks3

the stock markets in 2020 actually rose on balance.

have not yet been able to regain their pre-crisis

Finally, the risk is obvious that there could be levels. Provided the vaccination strategy takes

setbacks in the Covid-19 fight. The mutation hold, this could at least trigger an interim rally

appearing in England, for example, as well as the in the cyclicals.

recent lockdown of ten Beijing Sectoral favourite rotation towards the end of 2020

neighbourhoods due to newly

emerged foci of infection, calls for

Banks

a certain degree of humility in Energy

expecting all-too-fast progress. Insurance

Last but not least, we would do Finance

Industry

well to keep in mind that the Telecom

capital markets of this period rest Commodities

on the foundation of interest rates Consumption long-

term Performance Sept.-Oct.

that have been low for a long time.

Real estate

If this basic assumption were to Consumer goods

Performance Nov.-Dec.

falter, a reorientation would Utilities

probably be unavoidable. Technology

Health

Source: Bank for International Settlements /

Bloomberg

2 The five stocks are: Amazon, Alphabet, Apple, Facebook, Microsoft. (They are worth more than all German or Japanese or British shares put together)

3 Cyclical sectors such as chemicals, automotive, mechanical engineering and travel.Perspectives 2021

Another obvious differentiation is the search for opportunities may rarely be “too expensive” in

profiteers of the digital transformation, which the next five years.

has been particularly rapid, drastic and disruptive

in recent months. The Microsoft head’s The crisis has shaken things up. Like a child whose

Lego structure has collapsed, we will not be able

statement that the transformation process of the

next two years may have been shortened to two to put many things back together the way they

months remains without contradiction. Many were before. In many ways, a new beginning is

industrialised countries would now have to go to needed. For this new beginning, some of the

great lengths to keep up with this speed – for bridges behind us do not even need to be

example in licensing procedures – and not demolished, because they no longer exist. This is

a global experience and could give us the

weaken their companies in terms of competition.

The traditional (manufacturing) industry is no opportunity to make the shift to a sustainable

longer necessarily the centre of economic economy economy, both environmentally and

prosperity. Instead, this sector is increasingly sociologically. Global challenges need globally

being squeezed by companies from completely coordinated responses that also include the

outside the industry with innovative concepts poorest countries. This is particularly true with

regard to the mitigation of global warming.

and no historical dead weight. The most recent

example comes from Apple, which has previously Epidemics and pandemics can be fought with

been known as a manufacturer of smartphones, lockdowns and medicines, and the capital

markets can overlook them because they are

and their idea to enter into the production of

electric cars. In addition, we can see that predictable. However, the situation is likely to be

globalisation is being “rewound” and the focus in quite different as soon as tipping points are

manufacturing chains is now being directed triggered in the global climate. You do not want

more towards locality and sustainability. to overlook that if you are being honest. The post

However, this is by no means accompanied by Covid-19 world will therefore probably become

“deceleration” as we can see an increase in the more digital and local, but almost inevitably more

sustainable. It is both challenging and rewarding

speed of processes and new developments. Last

but not least, faster internet connections (5G) to identify the companies that will successfully

are promoting this development. Companies drive this development over the next ten years.

that drive these trends or take advantage of their Looking ahead to the next ten

China leads the way in innovation years, it is also worth taking a look

at Asia and China in particular.

ANNUAL OUTPUT OF INTERNATIONAL PATENTS

Assuming the growth rates to

date, the People’s Republic of

China could overtake the United

States in terms of its gross

national product around the end

of this decade. Even today, more

patents are being filed there than

anywhere else. Telecommuni-

cations technology, robotics and

artificial intelligence are at the top

Germany Korea France

of the patent lists, putting China

China U.S. Japan

on a par with the USA, Japan and

Source: World Intellectual Property Organization

Germany. China is also a pioneer

in terms of electromobility; thePerspectives 2021

share of electric cars amongst new registrations is Legal notice:

stable at more than 5 %. In relation to this, only

This publication was prepared by CONCEPT

Norway sells more e-cars, incidentally with a Vermögensmanagement GmbH & Co. KG (CONCEPT). It is for

Chinese brand in third place. The Chinese stock information purposes only and may not be reprinted or made

market, on the other hand, is currently still “only” publicly available without CONCEPT’s express consent.

half the size of the American stock market and, The information contained in this publication is based on

sources that CONCEPT believes to be reliable but has not

moreover, in some segments is inaccessible to subjected to any neutral checks. The information is publicly

foreigners. That is why the baton of “global capital available. CONCEPT assumes no guarantee and no liability for

market leader” will not be handed over any time the correctness or completeness of the information. The

soon. opinions expressed in this publication are those of the author

and are subject to change. Such changes of mind do not have

to be published.

OPTIMISTIC IN THE MEDIUM TERM

The information contained in this publication is based on

Although it is difficult to determine the direction of historical data and CONCEPT’s assessments of future market

the capital markets in 2021, as much will depend developments. These market assessments have been

on the effective fight against Covid-19, we remain obtained on the basis of analyses prepared with due diligence

and care. Nevertheless, CONCEPT cannot assume any

optimistic about the medium-term future, guarantee for their occurrence. The value of an investment

although we are also aware of the risks. Entering based on this may fall or rise, and the amount invested may

into these risks is unavoidable if you want to not be recovered.

achieve returns. Our world is still becoming more

Information on data protection in accordance with the EU

complex and many market participants are on the General Data Protection Regulation (GDPR):

lookout – for new points of orientation and for

CONCEPT Vermögensmanagement processes personal data

alternatives to returns that were previously of the recipients of this publication (last name, first name,

realisable with less risk. This can lead to both title if applicable, address and email address if applicable).

exaggerations and sudden setbacks. We take both Pursuant to Art. 6 GDPR, the processing of data is lawful on

into account in a balanced and variable investment the basis of the consent of the recipient or on the basis of the

legitimate interest of the controller.

style. In principle, precious metals also come into

play, which remain a suitable investment in view of CONCEPT Vermögensmanagement uses the data

unresolved systemic risks. Precious metal confidentially and will not pass it on to third parties. The

investments (gold and silver) are also an important recipient may object to the receipt of this information and the

part of the strategy of our CONCEPT Aurelia Global use of their data at any time. The objection may be addressed

to:

mutual fund. The latter also consistently invests in CONCEPT Vermögensmanagement GmbH & Co. KG

technology and consumer companies with an eye Welle 15, 33602 Bielefeld

to the future. With its mix of equities and precious Phone/FAX: 0521-9259970 / 0521-92599719

metals, Aurelia has become one of the most Email: info@c-vm.com.

successful global mixed funds in Germany in 2020

and the past 5 years.

We wish you and your families a predictable new

year and hope you experience joy, success,

contentment and personal happiness. Stay

healthy!

Bielefeld, 6 January 2021

CONCEPT Vermögensmanagement GmbH & Co. KG Welle 15 33602 Bielefeld

Phone 0521 - 9 25 99 70 Fax 0521 - 9 25 99 719 www.c-vm.com Email: info@c-vm.com

Headquarter: Bielefeld Register Court Bielefeld HRB 37668 BAFin-Reg-Nr. 118.788

Managing Director: Uwe Johannhörster, Matthias Steinhauer, Jochen Sielhöfer, Thomas Bartling, Frank Luge Verband unabhängiger

VermögensverwalterDeutschland e.v.You can also read