Reinstating Loan-to-Value Ratio Restrictions - Consultation Paper, December 2020 - Reserve Bank of ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Reinstating Loan-to-Value Ratio Restrictions Consultation Paper, December 2020 Ref #9393831 v1.0

2 Submission contact details We invite submissions on this Consultation Paper by 22 January 2021. Please note the disclosure on the publication of submissions below. Address submissions and enquiries to: (E-mail) macroprudential@rbnz.govt.nz Subject line: LVR Consultation December 2020 (Hard copy) Cavan O’Connor-Close Financial System Policy and Analysis Department Reserve Bank of New Zealand PO Box 2498 Wellington 6140 Publication of submissions All information in submissions will be made public unless you indicate you would like all or part of your submission to remain confidential. Respondents who would like part of their submission to remain confidential should provide both a confidential and public version of their submission. Apart from redactions of the information to be withheld (i.e. blacking out of text) the two versions should be identical. Respondents should ensure that redacted information is not able to be recovered electronically from the document (the redacted version will be published as received). Respondents who request that all or part of their submission be treated as confidential should provide reasons why this information should be withheld if a request is made for it under the Official Information Act 1982 (OIA). These reasons should refer to section 105 of the Reserve Bank of New Zealand Act 1989, section 54 of the Non-Bank Deposit Takers Act, section 135 of the Insurance (Prudential) Supervision Act 2010 (as applicable); or the grounds for withholding information under the OIA. If an OIA request for redacted information is made, the Reserve Bank will make its own assessment of what must be released taking into account the respondent’s views. The Reserve Bank may also publish an anonymised summary of the responses received in respect of this Consultation Paper. 2

3

Contents

Introduction ............................................................................................................................................................ 4

Objective of LVR restrictions .............................................................................................................................. 4

History of Reserve Bank’s use of LVR restrictions ............................................................................................. 5

Summary of proposal ......................................................................................................................................... 5

Problem definition .................................................................................................................................................. 6

Housing market trends ....................................................................................................................................... 6

High-LVR lending to property investors ............................................................................................................. 9

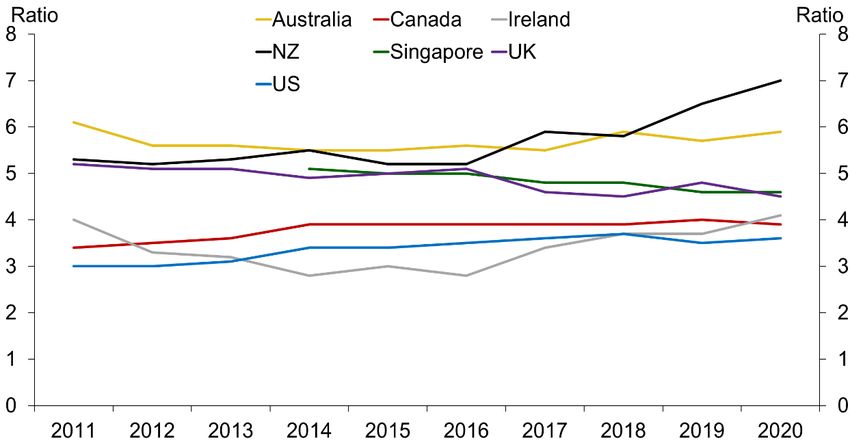

High-LVR lending to owner-occupiers .............................................................................................................. 10

Current stocks of high-LVR lending ................................................................................................................. 12

Summary .......................................................................................................................................................... 12

Policy proposal .................................................................................................................................................... 13

Timing of reinstating restrictions ...................................................................................................................... 13

Calibration of restrictions .................................................................................................................................. 14

Other options for managing financial stability risks .......................................................................................... 15

Impacts of reinstating LVR restrictions ................................................................................................................ 15

Impacts on flows of new high-LVR lending ...................................................................................................... 15

Impacts on stocks of high-LVR lending ............................................................................................................ 16

Impacts on house prices .................................................................................................................................. 18

Overall impacts on financial stability ................................................................................................................ 18

Wider economic impacts .................................................................................................................................. 19

Costs and unintended consequences .............................................................................................................. 19

Timeline for implementation ................................................................................................................................. 20

References .......................................................................................................................................................... 21

3

4

Introduction

1. The Reserve Bank is consulting on the reinstatement of loan-to-value ratio (LVR) restrictions on residential

mortgage lending from 1 March 2021. LVR restrictions set a ceiling (the ‘speed limit’) on the percentage of

new mortgage lending banks can offer at high LVRs.

2. We are proposing to reinstate the LVR restrictions at the same level as before the onset of COVID-19,

where the speed limits were set at a maximum of 20 percent of new lending to owner-occupiers at LVRs

above 80 percent, and 5 percent of new lending to investors at LVRs above 70 percent (after exemptions).

Objective of LVR restrictions

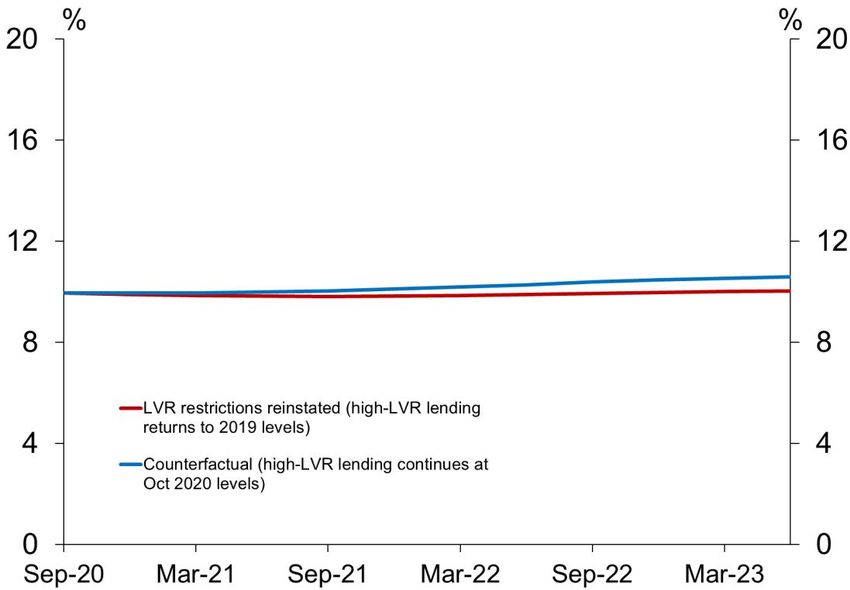

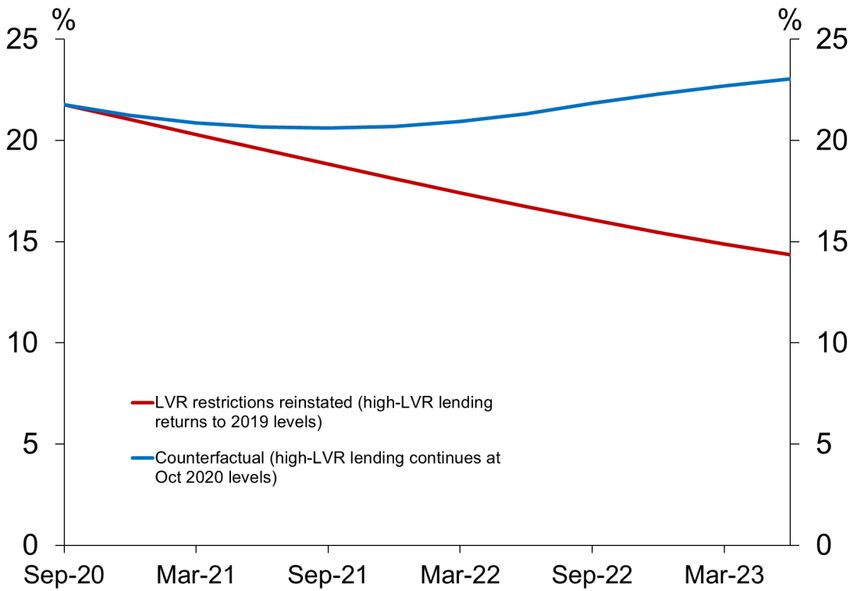

3. LVR restrictions are one of the Reserve Bank’s macroprudential policy tools. As set out in our

macroprudential policy framework document1, the purpose of macroprudential policy is to reduce the risk

associated with ‘boom-bust’ cycles in which the financial system amplifies a severe downturn in the real

economy. This in turn helps us to meet our statutory purpose of “promoting the maintenance of a sound and

efficient financial system”, as set out in section 1A of the Reserve Bank Act.

4. LVR restrictions on residential mortgage lending support financial stability, by building financial system

resilience against a disorderly correction in the housing market, and by dampening excessive growth in

credit. By placing limits on high-risk lending, LVR restrictions can make household and bank balance sheets

more resilient to a correction in property values if that occurs. This, in turn, can help avoid a negative

feedback loop emerging in the housing market, as shown in figure 1. In this situation, an initial correction

causes some borrowers to move into negative equity, which then incentivises further ‘fire sales’ of property

that depress the market further.

5. Neither the long-run level of house prices nor housing affordability are objectives of the LVR restrictions.

However, by limiting highly leveraged purchasing, LVR restrictions may moderate house price volatility

somewhat (i.e. moderating price increases in upturns and price decreases in downturns).

6. LVR restrictions can also moderate the scale of economic downturns by reducing household indebtedness

and enhancing borrower balance sheets. Given an unexpected fall in income or other stress events, heavily

indebted households may become unable to service their debts or be forced to cut consumption, which then

dampens economic activity.

———

1

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Background%20papers/Macroprudential-policy-framework.pdf

45

Figure 1 – Feedback loops in a housing market correction

House prices

fall

Increase in

Owners have

number of

decreased

houses for

equity

sale

Incentive to

sell to shore

up balance

sheet

History of Reserve Bank’s use of LVR restrictions

7. We first introduced LVR restrictions in 2013 and have adjusted them several times since then. From 2013

to 2016 we tightened the limits and adjusted the coverage of the restrictions, while from 2017 onwards we

loosened the LVR restrictions.

8. On 30 April 2020, as part of our response to COVID-19, we removed the LVR restrictions. Our rationale for

doing so was to support financial stability by eliminating a possible obstacle to the flow of credit during the

economic downturn triggered by the pandemic. In addition, lifting the LVR restrictions removed the risk

these might discourage banks from offering mortgage deferrals to their customers.

9. When we removed the LVR restrictions in April, we stated they would remain off for at least 12 months to

help support the economy. Since then, the economy has performed better than we forecast. Moreover, the

housing market has proved much more resilient than was originally predicted, with mortgage lending and

house prices both rising strongly in recent months after briefly declining during the lockdown period. Of

particular concern from a financial stability perspective, lending at higher LVRs has also increased

significantly, particularly for investors, and this trend has been accelerating.

Summary of proposal

10. We are concerned that an increase in highly leveraged borrowing, against an uncertain economic backdrop

due to COVID-19, is beginning to create risks to financial stability. We are therefore consulting on

reinstating LVR restrictions on 1 March 2021. We intend to reinstate the LVR restrictions at the level they

were before the onset of COVID-19, which was:

for owner-occupiers – a maximum of 20 percent of new lending at LVRs greater than 80 percent

(after exemptions); and

for investors – a maximum of 5 percent of new lending at LVRs greater than 70 percent (after

exemptions).

11. Reinstating LVR restrictions from 1 March 2021 will give banks time to clear their existing pipelines of high-

LVR loans that have been approved but not yet settled. In practice it is likely that new high-LVR lending will

decrease well before the reinstatement date as banks prepare for the introduction of new restrictions.

Indeed, most of the sector has already stated they are adjusting their lending standards, following our

announcement of this consultation.

56

12. In the rest of this consultation paper, we first set out the problem definition and discuss our proposal in

more detail. We then present an initial analysis of the likely impacts of reinstating LVR restrictions, and

conclude with a discussion of the timeline and next steps from here.

Problem definition

Housing market trends

13. Following the onset of COVID-19 in early 2020, the housing market was generally forecast to weaken

significantly as the economy entered recession and unemployment rose2. However, since that time the

economy has performed better than forecast and the housing market has shown considerable resilience,

with both lending activity and house prices rising strongly in recent months.

14. Figure 2 shows that the value of mortgage lending did drop sharply in April and May, but quickly rebounded

after nationwide lockdowns ended. Moreover, as figure 3 shows, annualised house price inflation is now

running above 10 percent nationally, and at 15 percent in Auckland. This trend has accelerated since

August.

Figure 2 – Total mortgage lending – change vs previous year ($m)

———

2

See: https://www.treasury.govt.nz/publications/efu/budget-economic-and-fiscal-update-2020, https://www.rbnz.govt.nz/monetary-policy/monetary-

policy-statement/mps-may-2020

67

Figure 3 – Annualised house price inflation

Source: REINZ

15. As noted previously, we do not have a mandate to directly target house prices. The pressures on the

housing market from factors such as a growing population, a limited supply of housing, and low mortgage

rates require a range of responses that are outside the scope of macroprudential policy. However, when a

strong run-up in house prices occurs alongside growth in high-risk mortgage lending, this can pose risks to

financial stability because it can increase the risk of a sharp correction and consequent financial sector

disruption. Figure 4 shows the feedback loop that can occur between house prices and the wider economy,

which can increase the size and effect of boom-and-bust cycles.

78

Figure 4 – Feedback effects in housing market corrections

Reduced

lending

Banks

House

funding

prices go

costs go

down

up

Banks

need Households

decrease

more spending

capital

Reduced

Defaults

economic

increase

activity

Unemploy

ment

increases

16. The potential risks to financial stability associated with a housing market correction are reinforced by the

fact New Zealand’s house price-to-income ratios and household debt levels are high relative to both

international comparator countries and historical averages. Figure 5 shows that house price-to-income

ratios in New Zealand have been on an upward trend and are now higher than a range of comparator

countries, including Australia, Canada, the United States and the United Kingdom. Figure 6 shows

household debt-to-income ratios have also been increasing, and are much higher for households with

mortgages than for other households – although interest rates have also fallen steadily, reducing the cost of

debt servicing.

17. If household balance sheets are highly leveraged, a downturn in the housing market can place banks and

households under pressure through rising mortgage loan losses, especially if unemployment increases. In a

worst-case scenario, this could lead to a ‘fire sale’ of distressed housing assets, which would increase the

likelihood of a negative feedback loop between the housing market and the wider economy as shown in

figure 4.

18. The banking capital adequacy framework reflects the riskiness of high-LVR borrowing, including investor

borrowing, for individual banks through higher risk weights.3 While the capital framework may capture the

———

3

Risk weight settings for standardised banks are set out in BS2A of the Banking Supervision Handbook. BS2B sets out the approach to capital

adequacy settings for Internal Ratings Based (IRB) banks. See: https://www.rbnz.govt.nz/regulation-and-supervision/banks/banking-supervision-

handbook

89

risks these borrowers pose to bank balance sheets, there are still risks from the feedback impacts these

higher-risk borrowers pose to the financial system as a whole.

Figure 5 – House price-to-income ratios for New Zealand and comparator countries

Source: Demographia

Figure 6 – Househould debt-to-income ratio

Source: Stats NZ, Reserve Bank Household Assets and Liabilities Survey, Reserve Bank estimates.

High-LVR lending to property investors

19. Investors, who own multiple residential properties, may be more likely to sell properties in response to

declining house prices, to de-leverage and strengthen their balance sheet positions before they face

serviceability pressures. International evidence suggests loss rates on investor lending are higher than on

owner-occupier lending during severe housing downturns for a given LVR ratio. Detailed studies of the

post-GFC experiences of Ireland (Kelly (2014)) and the UK (McCann (2014)) have found significantly higher

910

default rates on loans to investors than owner-occupiers. The Central Bank of Ireland (2014) and the UK

Treasury (HMT (2015)) have drawn the same conclusion from these studies.4

20. This evidence suggests a higher share of investor lending in the residential sector is likely to increase the

risk of fire-sales given a correction in house prices. This is due to both defaults (as rental incomes

deteriorate) and a trader-like incentive to exit the housing market as the cycle turns. Consequently, high-risk

lending to investors is of particular concern from a financial stability perspective.

21. As shown in figure 7, since the LVR restrictions were removed the share of new investor lending at LVRs

above 70 percent has increased to around 35 percent of total new investor lending from around 15 percent

(before exemptions).5 To date, most of the increase in high-LVR lending to investors has been at LVRs

from 70 to 80 percent. As discussed further below, the stocks of high-LVR loans to investors on banks’

mortgage books are currently at historic lows, reflecting the success of past LVR restrictions in reducing

such lending. However, we are concerned that if flows of new high-LVR lending continue to increase, this

will begin to feed through to lending stocks and increase long term financial stability risks.

Figure 7 – Share of new mortgage lending by LVR – Investors

Source: Reserve Bank LVR New Commitments Survey

High-LVR lending to owner-occupiers

22. We have also seen signs of a slight increase in higher LVR lending to owner-occupiers (both first home

buyers and other owner-occupiers), as shown in figures 8 and 9 below. However, at this stage it remains

within the restrictions that were in place before April 2020. The volume of lending to owner-occupiers has

increased substantially however, driven in part by an increase in debt values they are prepared to borrow

relative to their incomes. The share of owner-occupier lending with a debt-to-income (DTI) ratio of greater

than 5 rose to 38 percent in September from 30 percent a year ago. Commentators suggest that housing

market exuberance among owner-occupiers can be partly attributed to expectations of future price

———

4

There are caveats to applying evidence from other economies to New Zealand, including that mortgage origination standards can vary significantly

across countries and time. These problems are mitigated by focussing on the differential between default rates for investors and owner-occupiers

identified in international studies.

5

The LVR restrictions for investors were previously set at 5 percent of new lending above 70 percent LVR, but there were exemptions in place such as

for new build housing. Hence the pre-exemption figures are more comparable.

1011

increases, and the fear of missing a timely opportunity to buy.

23. Although high-LVR lending to owner-occupiers is currently of less concern than lending to investors, owner-

occupier lending remains a risk particularly given the ongoing economic uncertainty associated with

COVID-19 and forecast increases in unemployment. An increase in defaults by owner-occupier

homeowners would also contribute to the feedback effects of a housing downturn.

Figure 8 – Flow of new mortgage lending by LVR – First-time buyers

Source: Reserve Bank LVR New Commitments Survey

Figure 9 – Flow of new mortgage lending by LVR – Other owner-occupiers

Source: Reserve Bank LVR New Commitments Survey

1112

Current stocks of high-LVR lending

24. Although flows of new lending at high LVRs have increased in recent months, new lending represents only

a small share of the total stock of high-LVR lending on banks’ mortgage books. Loan stocks, rather than

lending flows, are arguably the main concern from a financial stability perspective. Figure 10 shows that, for

the four large banks6, the share of total mortgage loans at high LVRs is currently at historic lows. (A slight

increase is observable in the most recent quarter however, which is in line with the recent increase in high-

LVR lending flows.) This reflects the success of our LVR policy in constraining risky lending since

restrictions were first introduced in 2013.

Figure 10 – High-LVR mortgages as share of total mortgage lending – Large banks

Source: Reserve Bank LVR New Commitments Survey, Banks’ Disclosure Statements

Summary

25. Overall, stocks of high-LVR lending remain low and recent stress tests7 indicate New Zealand’s banks are

resilient to a range of shocks, including a significant downturn in the housing market. However, the stress

tests also show that a severe downturn that included large falls in house prices would have a significant

impact on financial stability and the wider economy, through both mortgage loan defaults and feedback

effects. This could include the possibility of a credit crunch, with banks rationing credit, even to more

creditworthy borrowers.

26. Since we removed the LVR restrictions, we have also seen some divergence between banks with respect

to high-LVR lending. Some banks have remained broadly within the previous LVR speed limits, while others

have increased their high-LVR lending shares. Given the dynamics of competition for market share in the

mortgage market, it is possible that the banks which have taken a conservative approach to date would

face increasing commercial pressure to follow other banks’ policies, in the absence of LVR restrictions. As

noted earlier, the majority of the sector has already announced that it has adjusted its lending standards

following our announcement of this consultation.

———

6

Westpac, BNZ, ANZ and ASB.

7

See https://www.rbnz.govt.nz/research-and-publications/reserve-bank-bulletin/2020/rbb2020-83-03

1213

27. In summary, we are concerned at the emerging trend of rapid house price inflation combined with growth in

high-LVR lending in an uncertain economic environment. While stocks of high-LVR lending are low by

historic standards, we consider that if current trends remain unchecked, they could lead to the emergence

of financial stability risks in the event of a correction to the housing market.

Q1: Do you have any comments on the problem definition for this policy?

Policy proposal

28. To address the concerns outlined in the Problem Definition section, we propose to reinstate LVR

restrictions on 1 March 2021. The restrictions would be calibrated to the same level as before we removed

the limits on 30 April 2020. Specifically, the restrictions would impose speed limits of no more than 20

percent of new lending to owner-occupiers at LVRs above 80 percent, and no more than 5 percent of new

lending to investors at LVRs above 70 percent (after exemptions).

29. We consider that reinstating LVR restrictions, rather than introducing or adjusting other prudential tools, is

the most appropriate option for addressing financial stability risks in the residential housing sector in the

near term. We have consulted on LVR regulations extensively since we first introduced them in 2013, and

systems already exist across the banking industry to measure high-LVR lending for key classes of

residential mortgages. LVR restrictions can therefore be imposed relatively quickly.

30. A review of the Reserve Bank’s LVR policy by Lu (2019)8 found that the policy had been effective in

improving financial stability. By mitigating the scale of house price falls during a potential downturn, and

limiting the indebtedness of households, the LVR policy was found to have made the financial system more

resilient to a housing-led downturn, as well as lessening the potential decline in household spending and

economic activity during a stress scenario. We consider that our past use of LVR restrictions was one factor

in helping cushion the financial system and economy following the onset of COVID-19.

31. Introducing LVR restrictions via speed limits recognises that, in some cases, it is appropriate for banks to

provide loans at higher LVRs. The speed limits allow banks to continue to provide a proportion of high-LVR

loans to fund purchases for more creditworthy borrowers, while taking into account each borrower’s

individual circumstances.

Timing of reinstating restrictions

32. When we removed LVR restrictions earlier this year, we advised they would remain off for at least 12

months (until 1 May 2021). We acknowledge our current proposal to reinstate the restrictions on 1 March

2021 is not aligned with this earlier commitment, and hence could be seen as undermining regulatory

certainty for the industry and wider stakeholders.

33. This is not a decision we take lightly. However, recent developments with respect to house price inflation

and higher-risk lending are opposite to what was forecast (by both the Reserve Bank and others) at the

time the LVR restrictions were removed. Under these unusual conditions, we consider it justifiable to

revise our position. Although bringing the date forward by two months is a relatively short period of time,

———

8

https://www.rbnz.govt.nz/research-and-publications/analytical-notes/2019/an2019-07

1314

the fact high-LVR lending (particularly to investors) has risen so quickly suggests there is merit in moving

early to prevent a further escalation in riskier lending.

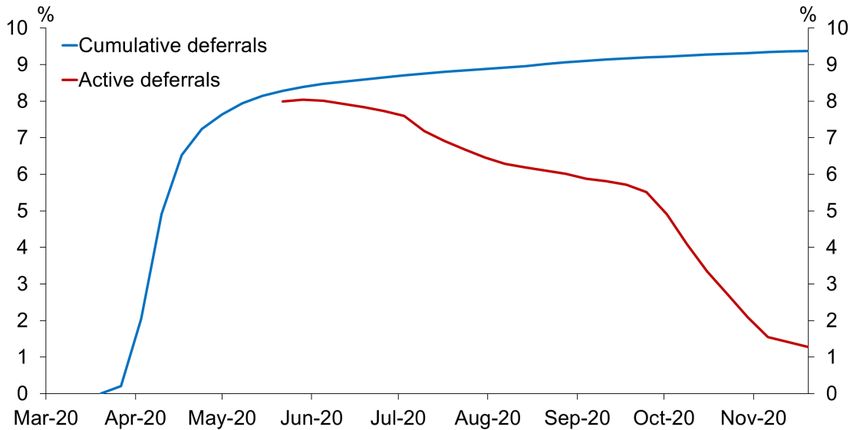

34. We also note that one reason we removed LVR restrictions in April was to ensure they did not create an

obstacle to the mortgage deferral scheme. Although the scheme has been extended until 31 March 2021,

new applications have now fallen to very low levels and the number of mortgages on deferral has also

declined significantly, as shown in figure 11 below. Our discussions with banks indicate most borrowers

who were on mortgage deferrals have resumed payments (on either the original or a restructured

schedule), with only a small proportion requiring more support. Therefore, we do not anticipate any

adverse impacts on the mortgage deferral scheme from reinstating LVR restrictions earlier than we

announced previously.

Figure 11 – Mortgage deferrals as a share of total mortgage lending

Source: Reserve Bank Bank Customer Lending Flows Survey

35. There have been calls from some stakeholders for the Reserve Bank to reinstate LVR restrictions earlier

than 1 March 2021. However, we consider 1 March 2021 is the most appropriate date, because:

It is important to allow enough time for a full consultation on our proposal, in line with our usual

practice. Although removing the restrictions was done at very short notice, this reflected the urgency

of the situation and the need to remove any barriers to implementing the mortgage deferral scheme.

Once the consultation closes we will also need time to consider submissions and consult on changes

to banks’ Conditions of Registration (CoR) if we decide to implement the proposal.

Banks have previously said they require a lead time of up to three months to comply with adjustments

to LVR restrictions, to manage their pipelines of high-LVR loans which have been approved but not

yet settled.

Reinstating LVR restrictions earlier than 1 March 2021 would have a negligible impact on high-LVR

lending stocks, particularly given most banks have already announced they have adjusted lending

standards for new loans since we announced our intention to consult.

Calibration of restrictions

36. As noted above, we are proposing to calibrate the LVR speed limits to the same level as was in place

before 30 April 2020. As we will discuss further in the Impact Assessment section below, we forecast

reinstating LVR restrictions at this level will mean that stocks of high-LVR lending to investors will

1415

continue on their previous downward trajectory, while stocks of high-LVR lending to owner-occupiers will

remain stable going forward. Maintaining the previous limits also reduces the likelihood of efficiency costs

and unintended consequences, and minimises uncertainty for the industry. We therefore do not consider

it necessary to reinstate restrictions at a higher (i.e. more restrictive) level at this time.

37. However, we will continue to monitor high-LVR lending and other indicators of risks to financial stability if

we reinstate the restrictions. We may adjust the calibration of the LVR restrictions in future (as we have

done in the past), as and when necessary to manage these risks.

Other options for managing financial stability risks

38. Other macroprudential tools are available to manage financial stability risks associated with the housing

market. For example, we have previously consulted on introducing debt serviceability restrictions, such as

debt-to-income (DTI) limits, on new mortgage lending9. Although we consider restrictions on high-DTI

lending could complement the current LVR policy, this tool has not yet been tested in the New Zealand

context and is not currently part of the Reserve Bank’s Memorandum of Understanding (MoU) with the

Minister of Finance. We are not proposing to implement DTI restrictions at this time, but intend to undertake

further work on this option following our decision on reinstating the LVR restrictions.

Q2: Do you have comments on any aspect of our policy proposal?

Impacts of reinstating LVR restrictions

39. This section presents an initial assessment of the expected impacts of reinstating the LVR restrictions on

1 March 2021, compared to a counterfactual scenario in which the restrictions remain off. We will present

more analysis in a regulatory impact assessment (RIA), which we will release when we announce our

decision on reinstating the LVR restrictions.

Impacts on flows of new high-LVR lending

40. If LVR restrictions are reinstated at the level that applied before 29 April 2020, we expect investor lending

at LVRs above 70 percent to quickly decline back to 5 percent or less of new lending commitments (after

exemptions). Under the regulations set out in BS19 of the Banking Handbook, compliance with LVR

restrictions is assessed on a three-month rolling period. Hence, if we reinstate restrictions on 1 March

2021, bank lending to investors at LVRs above 70 percent would be restricted to 5 percent or less of new

lending commitments made in the period 1 March 2021 to 1 June 2021. We expect banks to begin

adjusting their lending standards for new investor loans in advance of the proposed 1 March 2021

implementation date, and most banks have already announced they are taking this step.

41. We expect owner-occupier lending at LVRs above 80 percent to remain at 20 percent or less of new

lending commitments. As we noted in the Problem Definition section, high-LVR lending to owner-

occupiers has largely remained within the previous 20 percent speed limit since the restrictions were

———

9

https://www.rbnz.govt.nz/regulation-and-supervision/banks/consultations-and-policy-initiatives/active-policy-development/serviceability-restrictions-as-

a-potential-macroprudential-tool-in-new-zealand

1516

removed in April. Therefore, most banks will not need to make significant adjustments to their current

lending standards for owner-occupiers, but will need to ensure they maintain those standards in future.

Impacts on stocks of high-LVR lending

42. Figures 12 and 13 below show forecasted impacts on stocks of high-LVR lending for investors and

owner-occupiers respectively, using our HODOR model.10 The forecasts compare a scenario in which the

LVR restrictions are reinstated and high-LVR lending flows return to 2019 levels, with a counterfactual

scenario in which the restrictions remain off and high-LVR lending flows continue at October 2020 levels.

43. It can be seen that in the scenario where the LVR restrictions are reinstated, the stock of high-LVR

investor lending (defined as LVRs over 70 percent) is forecast to continue to decline steadily over the

next three years, from approximately 22 percent to 14 percent of total investor lending. Under the

counterfactual scenario, stocks of high-LVR investor lending are forecast to decline slightly over the next

year and rise after that. This is because LVR restrictions targeted at investor lending were only introduced

in October 2016,11 and the existing high-LVR lending stocks had not yet reached an equilibrium point.

44. The stock of high-LVR lending to owner-occupiers (defined as LVRs above 80 percent) is forecast to

remain flat over the next three years if the LVR restrictions are reinstated, as opposed to increasing by

about one percentage point if flows remain at the current level.

45. Stock forecasts under the counterfactual scenario could change if the flows of high-LVR lending grew

above current levels (or declined). Indeed, one of the main concerns motivating our proposal to reinstate

LVR restrictions on 1 March 2021 is the possibility high-LVR lending could continue to accelerate. Given

that adjustments to lending flows impact on lending stocks with a lag, we consider that reinstating the

LVR restrictions sooner will reduce risks to financial stability, as opposed to waiting until the stock of risky

loans begins to trend upwards.

———

10

A description of the model can be found in Bloor and Lu (2019).

11

See https://www.rbnz.govt.nz/news/2016/09/reserve-bank-confirms-nationwide--restrictions-on-loans-to-property-investors.

1617

Figure 12 – Forecast stocks of high-LVR lending (>70%) – investors

Source: Reserve Bank estimates

Figure 13 – Forecast stocks of high-LVR lending (>80%) – owner-occupiers

Source: Reserve Bank estimates

1718

Impacts on house prices

46. We carried out some analysis of the impact of LVR restrictions on house prices in 2018. 12 The analysis

was based on periods of significant tightening of lending standards. In 2013, when we first introduced the

restrictions, flows of lending at LVRs above 80 percent fell from around 25 percent to below 5 percent of

all new mortgage commitments. When we imposed investor-specific restrictions in 2016, flows of lending

fell from around 35 percent to around 12.5 percent (before exemptions). Overall, the study estimated that

these previous decisions to impose and then tighten LVR restrictions had moderated house price inflation

by between 3 and 6 percentage points, with most of the impact occurring in the first 12 months after

adjusting the restrictions.

47. The current proposal to reinstate LVR restrictions is likely to result in a relatively small change in lending

standards, by comparison with the decisions taken from 2013 to 2016. As discussed in the Problem

Definition section, the stock of higher-risk loans is currently at historic lows. Therefore, we do not

anticipate such large effects on house price inflation from reinstating LVR restrictions at this time. We

consider a reasonable estimate of the impact on house prices of reinstating LVR restrictions on 1 March

2021 would be a reduction in house prices of 1-2 percentage points, relative to a counterfactual in which

the LVR restrictions remained off. However, given housing markets can suffer from ‘irrational

exuberance’, LVR restrictions should help to lean against a possible further acceleration.

48. As discussed earlier in this paper, we do not currently have a mandate to directly target house prices.

Rather, our aim is to limit the risks to financial stability associated with high-risk lending in the housing

market. If the current rate of house price inflation continues, we consider this is likely to increase the risk

of a future sharp correction in house prices. This is of particular concern given the ongoing uncertainty

over the economic outlook resulting from COVID-19, and the fact housing valuations in New Zealand are

already elevated.

Overall impacts on financial stability

49. Our assessments of the LVR policy in 2019 (Lu, 2019; Bloor and Lu, 2019) outlined three main channels

by which LVR restrictions can impact on financial stability:

Asset quality channel – LVR restrictions reduce the share of new high-LVR mortgage commitments,

and consequently reduce the stocks of high-LVR lending over time. All else equal, this increases the

resilience of the banking system.

Risk weight channel – Reducing stocks of high-LVR loans leads to a decline in mortgage risk

weights, meaning less capital needs to be held by banks. This in part offsets the asset quality effect

above.

Indirect feedback effect channel – This effect arises from the LVR policy’s mitigation of the

magnitude of a potential correction to house prices. LVR restrictions can achieve this in two ways –

firstly, by reducing the level of distressed house sales in a downturn, and secondly by dampening

house price inflation during an upturn. The reduction in distressed house sales arises from a drop in

stressed mortgage default rates, together with a decline in the share of investor loans. This is

because investors are more likely to either sell their properties or default on their loans in a

correction.

———

12

See https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Discussion%20papers/2018/dp18-05.pdf.

1819

50. As discussed above, we expect reinstating the LVR restrictions to reduce both flows and stocks of high-

LVR lending, relative to a counterfactual in which the restrictions are left off. The reductions will be larger

for investors, since owner-occupier lending has remained mainly within the speed limit that applied before

removal of the restrictions. In addition, reinstating the restrictions is likely to have a small moderating

effect on house price inflation.

51. In line with the framework set out by Bloor and Lu (2019), reductions in high-LVR lending can be

expected to improve asset quality, although this may be largely offset by a decline in mortgage risk-

weights. Therefore, the main benefit to financial stability arises via the indirect feedback channel.

Specifically, by reducing the expected level of distressed house sales in a downturn (including by

reducing the share of investor lending at high LVRs), and by dampening house price inflation in an

upturn, reinstating LVR restrictions will reduce financial stability risks.

Wider economic impacts

52. LVR restrictions can affect the wider economy via their impact on house prices and housing wealth, which

in turn influences both consumption and residential investment.

53. Our own research has found that, on average, the marginal propensity to consume out of housing wealth

amounts to 3 cents of additional consumption spending for each dollar’s increase in housing wealth. The

impact on consumption is asymmetric with respect to positive and negative housing wealth shocks – a

decline in housing wealth has a larger impact (in reducing consumption) than an equivalent increase in

housing wealth (in boosting consumption).13

54. The overall economic impact of reinstating LVR restrictions is therefore uncertain. In the short term, to the

extent LVR limits are effective in moderating house price inflation, they can be expected to reduce

consumption and residential investment by comparison with a counterfactual in which the limits remain off.

However, over the longer term, if LVR restrictions are effective in reducing the magnitude of a potential

house price correction, this would support consumption in a downturn and thereby economic growth and

employment.

55. In either case, while the economic impacts of reinstating the LVR restrictions on 1 March 2021 are likely

to be relatively minor, we consider the overall economic impact will be positive over the long run. We

expect a temporary, small negative effect on economic activity, however the benefits to financial stability

and long-term economic outcomes outweigh this temporary effect.

Costs and unintended consequences

56. All prudential tools have an efficiency cost, which must be weighed against the benefits. The main

efficiency costs associated with reinstating the LVR restrictions are reduced credit access for credit-

worthy borrowers and the potential for weaker economic growth and employment in the short term.

57. As discussed in the previous section, we expect impacts on the wider economy to be limited. There may

be a small negative effect on consumption in the short term, but this should be offset by a reduced risk of

a future economic downturn that is driven by a correction in the housing market.

58. With respect to credit access, our 2019 review indicated LVR policy is likely to have had a larger impact in

constraining mortgage borrowing capacity than alternative macroprudential tools. This suggests the LVR

———

13

See: https://www.rbnz.govt.nz/research-and-publications/discussion-papers/2019/dp2019-01

1920

policy should be deployed primarily when housing and household sector risks are high. The speed limit of

high-LVR loans is an important calibration tool to mitigate the efficiency cost of the policy.

59. There is a risk that reinstating LVR restrictions on banks will create incentives for high-LVR mortgage

lending to shift into the non-bank sector, which is not subject to the restrictions. Although the provision of

mortgages by non-banks has grown since the LVR policy originally came into place, Lu (2019) found the

scale of this disintermediation remained too small to significantly erode the effectiveness of the LVR

restrictions. We will continue to monitor this issue if we reinstate the LVR restrictions.

60. Reintroducing LVR restrictions could reduce the scope for first-home buyers with low deposits to enter the

market. However, the use of speed limits (whereby 20 percent of owner-occupier lending can be at LVRs

above 80 percent) will reduce this risk. Allowing banks to provide a proportion of high-LVR loans allows

them to fund purchases for creditworthy first-home buyers and also in special circumstances. Previously,

under these settings, the first-home buyer share of the market held up at around 18 percent.

61. If the LVR restrictions on investors were to deter investment in rental property, this could put pressure on

rents. We believe any effect on rental inflation will be small. Over time, there could be some reduction in

the supply of rental property, in line with a relative shift from investor to owner-occupier purchases.

However, this transition would also result in less demand for rental properties as some renters became

property owners. In addition, the exemption regime permits high-LVR lending on new build investment

property, without this counting against the LVR speed limits.

Q3: Do you have any comments on our assessment of the impacts of reinstating LVR restrictions?

Timeline for implementation

62. The consultation period for this proposal will run until 22 January. We expect to release our final decision

in the first half of February, along with a summary of the submissions received and a regulatory impact

assessment (RIA).

63. The proposed policy change would be enacted by re-introducing section BS19 of the Banking

Supervision Handbook (“Framework for restrictions on high-LVR lending”). This will require a change to

banks’ CoR. If the decision to reinstate LVR restrictions is confirmed, we will run a short consultation

(minimum seven days) on the required changes to CoR to implement the LVR restrictions by 1 March

2020.

64. If we reinstate the LVR restrictions, we will continue to monitor financial stability risks related to the

housing market going forward, and may adjust the calibration of the restrictions in response to changes in

financial stability risk. We also intend to carry out further work in 2021 on the longer-term settings for LVR

restrictions and other macroprudential tools, including the possible use of debt-servicing restrictions (such

as DTI limits) to address financial stability risks related to the housing sector.

2021

References

Bloor C. and B Lu (2019), ‘Have the LVR restrictions improved the resilience of the banking system?’, Reserve

Bank of New Zealand Analytical Note Series.

Central Bank of Ireland (2014), ‘Consultation paper on macro-prudential restrictions’.

HMT (2015), ‘Consultation on Financial Policy Committee powers of direction in the buy-to-let market’.

Kelly R and T O'Malley (2014) ‘A transitions-based model of default for Irish mortgages’, Research Technical

Paper 17RT14, Central Bank of Ireland.

Lu B (2019) ‘Review of the Reserve Bank’s loan-to-value ratio policy.’ Reserve Bank of New Zealand Bulletin,

82(6), Reserve Bank of New Zealand.

McCann F (2014), ‘Modelling default transitions in the UK mortgage market’, Central Bank of Ireland Research

Technical Paper 18/RT/14, Central Bank of Ireland.

21You can also read