Report Trends in the Virtual Work Startup Ecosystem - Travel ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

1 Report Trends in the Virtual Work Startup Ecosystem

1 Virtual Work Trends

Introduction

During the Covid-19 pandemic, most knowledge To better judge the long-term impact of the vir-

workers experienced an abrupt shift to work- tual work revolution on workplace dynamics and

from-home, and the growth of virtual work com- the resulting corporate travel activity, this re-

panies skyrocketed. port analyzes the ecosystem of over 250 rele-

vant startups that offer virtual solutions bridging

At the same time, air passenger traffic reached its physical and virtual business interactions.

lowest levels of the millennium. Business travel

came to a near standstill. In 2021, mobility re- By providing virtual alternatives to standard busi-

strictions are loosening, and travel is slowly re- ness activities, these startups undermine the

turning. However, the shift to virtual work will need for people to meet in person and thereby

continue—even when the pandemic eventually reduce the need for business travel.

concludes.

Our goal with this report is to provide an over-

The big question remains: What parts of busi- view of the startup dynamics in the Virtual Work

ness travel will return, and which will remain vir- market by analyzing Venture Capital investment

tual? Virtual work startups such as Hopin, Gather. trends where these players are concerned. We

town, and mmhmm are already disrupting busi- also provide a framework for travel companies to

ness activities such as travel for corporate events, evaluate the impact of different virtual work cat-

networking, and client meetings. egories on their business activities.

2 Virtual Work Trends

Who we are

This report has been created by the Lufthansa Our mission is to create and capture value be-

Innovation Hub with the support of Dealroom. yond flying. To do this, we invest in startups,

initiate partnerships with startups, and most

The Lufthansa Innovation Hub importantly, incubate new digital services and

products ourselves. To learn more, visit the

The Lufthansa Innovation Hub (LIH)—named LIH website or stop by our LinkedIn page.

“Germany’s Best Digital Lab” by Capital Mag-

azine—is the digital transformation spearhead In our work, we always follow the credo, “data

of the world’s largest aviation corporation, the beats opinion.” We want to act on facts rather

Lufthansa Group. than beliefs. That’s why exploring the Travel and

Mobility Tech ecosystem is the crucial founda-

The LIH discovers, evaluates, and imple- tion on which all of the Lufthansa Innovation

ments new digital business opportunities in Hub’s activities are built on.

the context of Travel and Mobility Tech with in-

dustry-leading airlines such as Lufthansa, Eu- Our insights are regularly shared on our dedi-

rowings, SWISS, and Austrian Airlines, the cated market intelligence platform, TNMT.

frequent flyer program Miles & More, as well as

other renowned Lufthansa Group entities.

3 Virtual Work Trends

About Dealroom

Dealroom as the exclusive data provider of this report is a global startup &

venture capital intelligence platform.

Dealroom.co is the foremost data provider on startup, early-stage, and

growth company ecosystems in Europe and around the globe.

Founded in Amsterdam in 2013, Dealroom works with many of the world's

most prominent investors, entrepreneurs, and government organizations to

provide transparency, analysis and insights on venture capital activity.

4 Virtual Work Trends

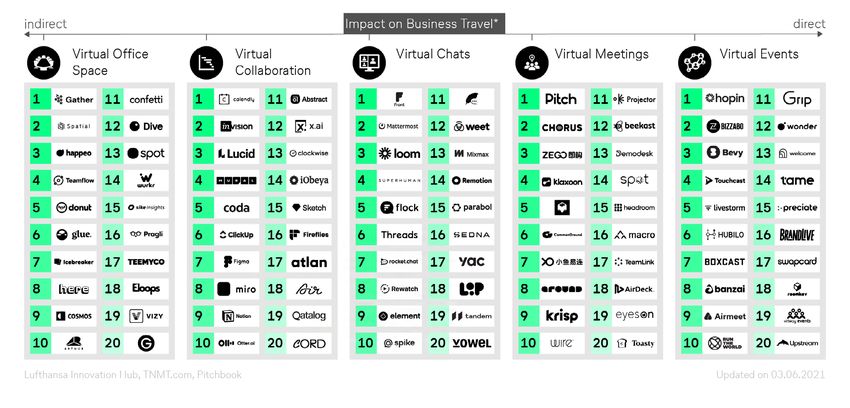

Approach

The 100 virtual work startups

challenging business travel

Startups ranked by VC funding received

To find all the relevant startups in the global vir- Given the fact that our startup scouting cov-

tual work ecosystem, we scouted hundreds of erage is better in Western countries than else-

relevant players and categorized them based where, especially Asia, we also reached out to

on their primary business focus. These include local experts where needed.

virtual events, virtual meetings (i.e., presenta-

tion and interaction tools), virtual chats (i.e., The focus of this report is exclusively on sec-

text messaging and video chats), virtual collab- ond-generation virtual work startups that are

oration (i.e., knowledge sharing, content crea- defined by an augmented, immersive solution

tion, and workflow alignment), and virtual office bridging the gap between physical and virtual

space (i.e., digital alternatives to office build- interactions, compared to the first generation of

ings and department floors). For a more detailed teleconferencing tools spearheaded by, for ex-

overview of all startup categorizations, please ample, Zoom, Skype, and Slack.

refer to the interactive Dealroom Landscape.

Furthermore, these startups address a business

To be able to do so, we utilized the Dealroom need that was often a reason for a business trip

platform, which offers an extensive venture in pre-Covid times. Hence, startups that offer

capital database built upon machine learning purely HR, legal, or back-office technology are

and data-driven information harvesting. excluded from our analysis.

5 Virtual Work Trends

#1 The virtual work mega-trend

started long before the pandemic

As demonstrated by the number of virtual work another high in 2019, driven by changing work-

startups founded globally over time, virtual force demographics with digitally-native Gen Z

work has been a mega-trend long before the workers increasingly entering the labour market

Covid-19 pandemic. Zoom, for instance, the along with the increased participation of female

company that became synonymous with the workers during this time. Both demographics

2020 virtual office shift, was founded back in are advocates for more flexible and virtual work-

2011, while Skype dates back to 2003. ing arrangements.

The first significant spike in startup founding Covid-19 provided another startup adoption

activity occurred in 2016, and can be largely launching pad on top of already accelerating

attributed to the growth of the so-called knowl- founding dynamics. A new record number of

edge economy—the concept of more flexible startups were founded in 2020, but the true

and remote work schemes pioneered by com- effects of the pandemic on founding dynamics

panies such as GitHub and Google, propelled are likely even higher due to an unavoidable lag

by the availability of more reliable and cost-ef- in tracking and reporting of most recent startup

fective software solutions. The growth reached foundings.6 Virtual Work Trends

#2 Highlighted by the pandemic,

investors intensify funding

The boost in founding activity was further accel- Even more impressively, the investor craze led

erated by growing investor attention to the vir- to several mega-rounds taking place in 2020,

tual work cause. As the entire knowledge econ- bringing the average funding amount per deal to

omy turned remote almost overnight in early $17M, up from $10M the year before.

2020, venture capitalists became aware of the

fast scaling and growth potential of virtual solu- This inflow of venture capital naturally prompt-

tions, especially as adoption skyrocketed during ed even more founders to enter the virtual work

lockdowns in many parts of the world. ecosystem—so it’s no wonder that the appe-

tite for virtual work startups is progressing into

This investor hype resulted in over 100 VC deals 2021 at the same pace, if not higher, as aver-

in virtual work startups in 2020 alone, a 66% in- age funding amounts have spiked to ~$40M per

crease from 2019 (and again, this figure is likely deal. This indicates that the motion is likely to

even higher due to reporting lags). continue in the coming years.7 Virtual Work Trends

#3 High investment growth to be

sustained by recent mega rounds

Funding trend lines are even steeper when ing total VC investments to $1.2B in Q1 alone.

turning to total dollar amounts invested in re-

spective virtual work startups instead of the The hypergrowth of these heavily-funded front-

number of deals. Total VC funding investments runners sets a strong tone for investors, and will

amounted to more than $1.8B in 2020, reveal- further accelerate innovation in the near future.

ing 226% growth from 2019. This astounding

spike was powered by multiple mega-rounds, However, it’s important to note that the current

including from virtual events startup Hopin rais- funding dynamics are most likely inflated be-

ing $166M, Bizzabo raising $138M, and virtu- cause of persisting forced lockdowns and mo-

al whiteboard startup Mural raising a total of bility restrictions in certain parts of this world.

$118M throughout the year.

Although we believe that the virtual work startup

The 2021 funding trajectory looks equally im- ecosystem will continue to expand, the growth

pressive. Two startups have raised rounds larger rate will likely slow down once workers can ven-

than $350M each (Hopin and Calendly), bring- ture out fully without restrictions.8 Virtual Work Trends

#4 Virtual work is a booming sector

but still in its nascent days

The rapid rise of upcoming virtual work start- functionalities that emulate in-person interac-

ups such as Hopin reveals a market gap for new tions, and thereby enable fluent team collabo-

software solutions and novel technology appli- ration.

cations that first-generation virtual work com-

panies such as Zoom, Skype, MS Teams, and While the hybrid future of work is still being

others were unable to capture. shaped, with no single market leader established

at this point in time, new startups continue to

What differentiates the new generation of vir- enter the market and fill this gap. This is con-

tual work ventures is that they bridge the gap firmed in our funding analysis, where the share

between online and in-person interactions, with of angel and seed rounds jumped to 25% in

additional interactive functionalities (Around) 2020—indicating that the virtual work market is

that help to captivate the audience (Klaxoon), still in its nascent days, with investors betting on

or even sense non-verbal cues (Headroom). In a wide selection of tech offerings with little or no

the context of team collaboration, startups like proven product-market fit.

Pitch, Miro, and Gather.town offer augmented9 Virtual Work Trends

#5 The West drives the remote

work shift as Asia holds back

In contrast to most other startup verticals, ing long economic shutdowns. Due to shorter

where Asia (particularly China) is a major breed- enforced home office time, Asian knowledge

ing ground for new tech startups, our data workers did not have the need to establish more

shows that the virtual work revolution is charac- sophisticated home office setups, and employ-

teristic of the Western world. An overwhelming ers largely stuck to their existing software tool

majority (about 90%) of newly-founded startups infrastructure.

are headquartered in the U.S. and Europe, while

Asia-based startups account for less than 6% of Secondly, mobile phone penetration has histor-

all companies. ically been higher in many Asian countries than

in the West, with mobile (video) chat functional-

To account for confirmation bias (although we ities more prominently integrated into people’s

cannot fully rule it out), we actively scouted for daily lives (think Tencent’s WeChat). This also

Asian virtual work startups and potential trends reduced the need for entirely new virtual work

holding back the shift in the Far East. We arrived tools, as large parts of the population were al-

at the following assumptions: ready connected virtually. Lastly, tech giants like

Tencent dominate online communication by ac-

First, Asian countries such as China, South Ko- quiring or building companies internally, making

rea, and Vietnam have contained the virus faster it difficult for new startups to succeed in this

than most countries in the West, thereby avoid- space.10 Virtual Work Trends

#6 Covid-19 benefited virtual event

and collaboration the most

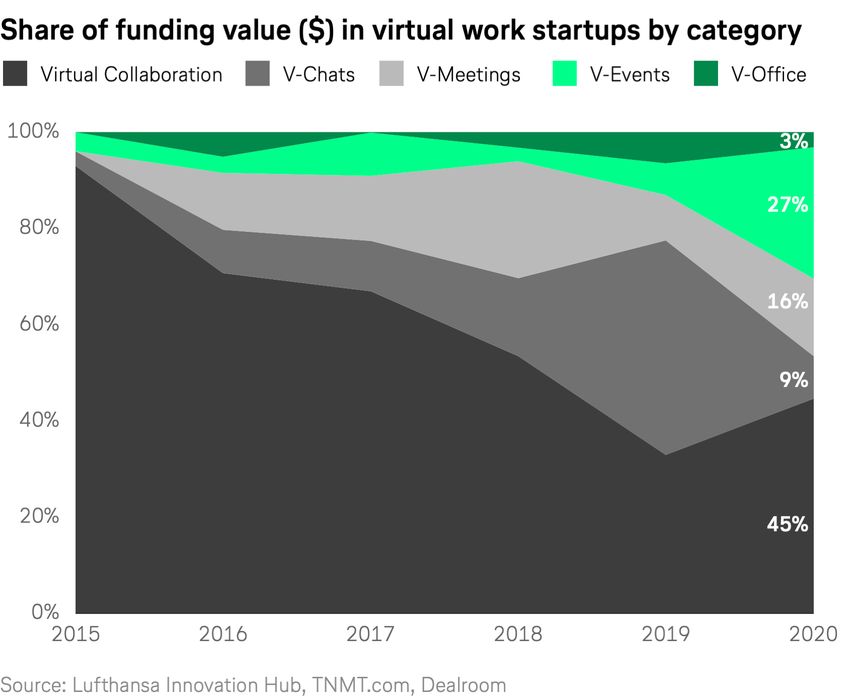

Looking at the share of funding value ($) per vir- synchronously collaborate online. In addition to

tual work category, our data tells us that start- virtual collaboration, the virtual events category

ups focusing on virtual collaboration—namely gained massive traction during the pandemic,

platforms that allow workers to create content increasing its funding share from 7% to 27% in

online, collaborate via knowledge sharing, or 2020. We expect virtual events startups to con-

align on workflow and objectives—comprise tinuously eat away market share from in-person

the first major work category to be virtualized event participation, even after the pandemic,

pre-Covid, as seen by the majority of funding with hybrid event formats slated to become the

flowing into various collaboration startups even new norm.

before 2019.

With all that being said, we project technology

Interestingly, virtual collaboration has also prov- to continue to advance rapidly, especially where

en to be the most-funded category throughout collaboration and event software are concerned.

the pandemic, with close to $1B raised in 2020. Therefore, both categories will seriously chal-

Therefore, we expect this category to remain lenge the need for business travel to corporate

prevalent post-pandemic, as an increasing num- events (and to meet with colleagues from differ-

ber of distributed teams look for solutions to ent company locations) going forward.11 Virtual Work Trends

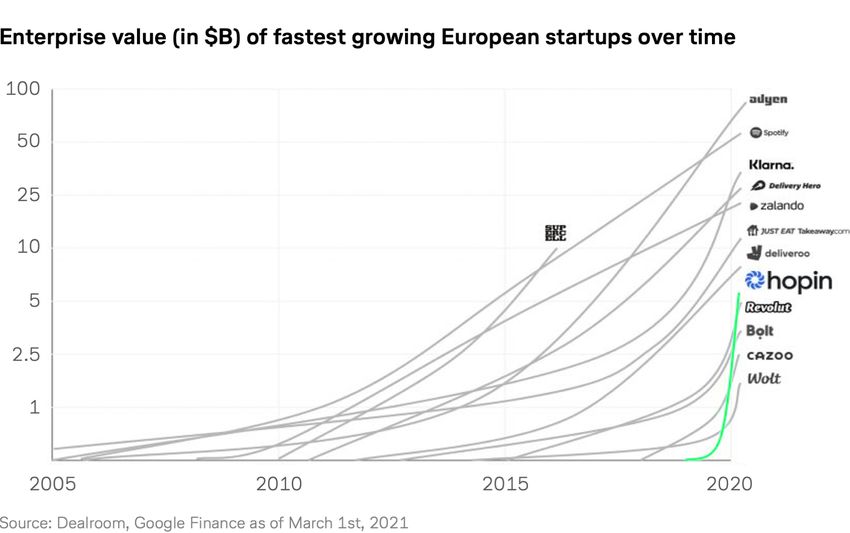

#7 Founded in 2019, Hopin is the

definition of hockey-stick growth

The pandemic has provided unprecedented Hopin is sustaining its hyper-growth via a vigor-

growth opportunities for a handful of startups, ous acquisition strategy, supported by its vast

especially in the virtual collaboration and events capital inflow. Right after its first mega-round

space as described previously. in November 2020, Hopin enriched its virtual

events business with three acquisitions: event

One of these hypergrowth players is virtual networking app Topi, and two live streaming

events provider Hopin, a company founded in platforms, StreamYard and Streamable. Through

2019 that achieved exponential growth during StreamYard alone, Hopin gained access to over

the pandemic. 100K paying customers and 3.6M users.

Visibly unaffected by scaling issues, the start- Following its second mega-round of ~$400M,

up reached a valuation of $5.65B less than two Hopin acquired voice and video collaboration

years after its founding, and grew its ARR from platform Jamm, signaling an expansion into

zero to $70M in the past 12 months, making it general video communication and collaboration

the fastest-growing European startup ever as of verticals, as the platform strives to stay relevant

June 1st, 2021. after the pandemic concludes.12 Virtual Work Trends

#8 Virtual office startups surge as

workers miss office serendipity

It is not only virtual collaboration and events tracking, and instead creating a fully-augment-

startups driving forward radical change and in- ed, immersive, and interactive virtual experience

novation in the virtual work ecosystem. A deep- of being “at work.” Highly-promising companies

er look at startup founding dynamics points to include Teamflow (with $15M in funding) and

another rapidly-emerging category: namely, vir- Spatial (with $22M in funding), which deliver a

tual office space. seamless VR experience. Companies like Gath-

er.town—currently the most-funded virtual of-

Although not as heavily funded as collabora- fice startup with $26.5M secured—offer a virtu-

tion and event players, the recent wave of new- al office environment that resembles some sort

ly-founded virtual office space ventures, repre- of Pokemon game world.

senting more than ⅓ of all foundings in 2020,

indicates that startup founders are seeing a lot We expect a lot of this startup traction to be

of untapped potential in recreating physical of- based on the fact that many workers eventually

fice spaces in a virtual manner. To achieve this, started to miss the social life of a physical of-

startups are moving beyond simply “digitizing” fice during the pandemic, and that they decided

routine office workflows like budgeting and time they no longer wanted to miss out on this.13 Virtual Work Trends

Conclusion

Virtual office solutions are yet

to see major investor interest

After analyzing various forms of funding dynamics across the virtual work

startup ecosystem, the ultimate question remains: What is here to stay

post-Covid?

To better judge the long-term impact of the virtual work revolution on office

routines and the resulting corporate travel activity, we developed a more

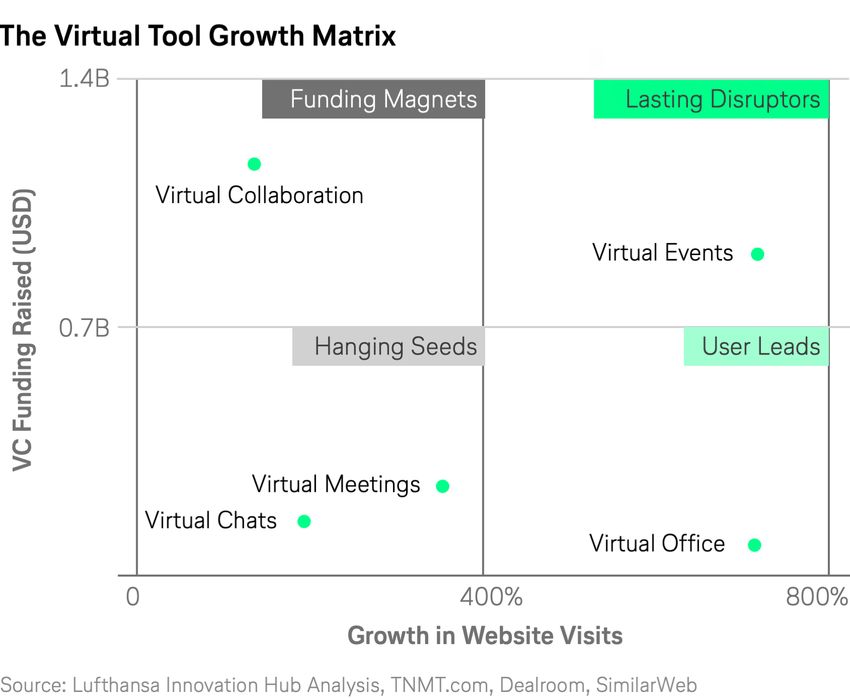

comprehensive framework coined the Virtual Tool Growth Matrix.14 Virtual Work Trends

The Virtual Tool Growth Matrix combines investor interest (gauged by VC

funding) and user interest (represented by cumulative growth in website

traffic) during the pandemic for the five defined virtual work categories we

looked at earlier. It provides a quantitative evaluation of the post-Covid lon-

gevity of various virtual work activities, thereby indicating which business

travel motives are most likely to return.

In other words, the four quadrants of the matrix classify the extent of busi-

ness travel substitution, offering founders and investors an evidence-based

view of the most attractive virtual work segments going forward.

This understanding is also highly relevant for travel providers like airlines,

allowing them to better prepare for a post-Covid future by evaluating which

software and travel motives can be used as a new complementary service

to business travel.

Looking at the bigger picture, the matrix tells us that the long-term adop-

tion of virtual tools—and their impact on business travel—will vary signifi-

cantly based on the interaction.

Additionally, the matrix shows that there are clear winners and some very

likely trends ahead. Namely, virtual event startups have captured both user

and investor attention, and in the coming months, we can expect these

platforms to keep expanding, cementing their utility for knowledge workers

and remote teams across the globe.

The matrix also reveals a discrepancy between user interest and investor

focus on different virtual tool categories. Specifically, it seems as though

most investors are predicting a return to in-person meetings—while users

are more open to long-term remote and hybrid work solutions, including

virtual alternatives to traditional office solutions.

Ultimately, the matrix reveals that users will more than likely give up office

huddling and watercooler chatter for the comfort of home, and for the flexi-

bility of permanent remote work. Only time will tell, of course—and we plan

on paying close attention to how things progress.15 Virtual Work Trends

Authors

Tran Dieu Ly Ivan Draganov

Research & Intelligence Analyst Senior Innovation Analyst

Lufthansa Innovation Hub Dealroom

dieuly.tran@lh-innovationhub.com ivan.draganov@dealroom.co

Lennart Dobravsky Louis Geoffroy-Terryn

Editor-in-Chief at TNMT.com Innovation Analyst

Lufthansa Innovation Hub Dealroom

lennart.dobravsky@lh-innovationhub.com louis.geoffroyterryn@dealroom.co

Disclaimer

This content is for general information purposes nor the Lufthansa Innovation Hub can warrant

only and should not be used as a substitute for the ultimate accuracy and completeness of the

consultation with professional advisors. Data data obtained in this manner. Results are up-

is current as of June 30, 2021. The Lufthansa dated periodically. Therefore, all data is subject

Innovation Hub and Dealroom have taken re- to change at any time.

sponsible steps to ensure that the information

contained in the report has been obtained from ©️Lufthansa Innovation Hub. All rights reserved.

reliable sources. However, neither Dealroom Please see TNMT.com for further details.

Newsletter

Visit TNMT.com and sign up for our bi-weekly

newsletterYou can also read