Retail Distribution 2015 - Full Digitalisation with a human touch - EMEA Banking Practice

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

EMEA Banking Practice Retail Distribution 2015 – Full Digitalisation with a human touch Victor Matarranz Enrico Scopa Radboud Vlaar

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 1

Retail Distribution 2015 –

Full Digitalisation with

a human touch

The digital transformation of retail banking has so far taken place in two stages – but

the most exciting and groundbreaking one is only just starting. The old retail banking

model, comprising bricks and mortar banking with digital channelsfor transactions,

will no longer work. As a result banks will have to make changes to all their distribution

channels. We believe that the key developments will be as follows:

Branch networks will be radically transformed into sales and advice outlets – they

will be 20% more productive than today and their costs will be up to 50% lower.

Digital channels will be designed to create a “wow” experience for the user,

thereby capturing these channels’ full sales potential (more than 20% of all product

sales at the moment start with an online enquiry or investigation)

Call centres will become a profitable, professional channel in which video technol-

ogy is increasingly used. As a result 15% of service requests will typically be

converted into sales.

Banks will manage these different channels so that service from the customer’s

perspective is seamless and ‘end-to-end’ and from its own perspective it captures

sales that are currently being lost.

Without decisive action, banks risk being stuck with an expensive and inflexible distri-

bution set-up. To start the journey, top management should look at metrics and gov-

ernance in a less branch-centric way and should launch a series of multichannel mini

transformations both within and across the different channels.

Retail Banking’s distribution transformation

Retail Banking’s distribution transformation can be summarised as follows:

1980-2000 – Digitalisation of payments: In this period ATMs, cards and Tele bank-

ing replaced paper-based payments as banks sought to capture new cost saving

opportunities and reach customers previously excluded from the mainstream

banking system. All banks have now completed this part of the ‘journey’.

2000-2010 – Digitalisation of basic banking: Over the first decade of the 21st cen-

tury most customers started being able to access their banks remotely 24/7 for the

bulk of low-value added activities. Benefits included greater convenience for them

and further cost efficiencies for the bank. This part of the journey is not yet com-

plete but most European players are well advanced along the road.

2010-2015 – Full Digitalisation with a human touch: Banks are only just beginning to

provide the ultimate client experience, namely digitalisation of sales and after-sales

service combined with continued face-to-face interactions for the more complex

products. Thanks in part to the development of mobile banking, sales of products

either transacted online or influenced by online marketing are expected in the medi-

um term to grow to the point where they represent roughly 60% of the total.

In the following chapters we will discuss what’s involved in the third part of the digital

journey, as well as how a bank can make the transformation happen.

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 2

Distribution 2015

We expect the typical retail bank by 2015 to have undergone a radical change in its

distribution mix and to have the following key characteristics:

Fewer branches, fully digital with a personal touch: ‘One click’ processes will

allow clients to get key information, order key products and pay for them with their

smartphone multifunction card and on iPad. As a result 99% of transactions and

service requests will be handled digitally, as well as the majority of sales leads.

When customers want to speak to someone at the bank they will interact via

telephone or VC, and the bank will link to premium clients at home. Branch net-

work will be more tailored to client needs than at present, with a range of different

branch formats to match customer profiles and needs in each location (everything

from unmanned fully automated to full service outlets). The changes, which will

create a radically different distribution profile [See exhibit 1], could free-up 30-50

percent of costs and increase sales by up to 20 percent,

More tailored to individual needs: The banks’s product and service offering will be

tailored, providing multiple value-added services to clients with targeted market-

ing campaigns based on rich CRM data. Such initiatives will increase high quality

leads and the conversion of prospects into new customers. Banks will increasingly

have different online brands so as to attract different customer sub-segments

and differentiate between them on pricing and service. Several banks are already

pursuing this strategy: in the Netherlands, for example, in the wake of its multi label

strategy focused on different segments, SNS Bank’s savings products market

share increased from 7% to 10% in three years;

Increasingly complex processes: Growing numbers of channels and different plat-

forms for digital delivery (for example, Apple and Android) will create enormous

process complexities, especially given the way customers increasingly use mul-

tiple channels while expecting the process to be seamless.

Enhanced profitability (for those that get it right): the bank’s financial ratios will be

much more attractive than they are today [See Exhibit 2]. Based on our assess-

ment, it should be possible to reduce costs structurally by 20-40%, mainly due to

lower distribution costs and changes in the distribution mix that drive down opera-

tions and indirect costs. Higher investments will be needed in new technology, the

costs of which can be offset by savings on legacy systems. The retail bank of the

future’s revenue development is more uncertain and will mainly depend on com-

petitive behaviour.

The magnitude of the looming transformation becomes clear when comparing this

retail bank of the future with the profile of the average retail bank today. The trans-

formation will require a substantial reduction in branch costs, a streamlining of end-

to-end processes and in most cases the building of many still missing digital com-

ponents. Not doing this, we believe, is simply not an option given the range of new

competitors, notably non-banking players, entering the market.

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 3

Exhibit 1

Exhibit 2

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 4

How to make it happen?

In this section we will analyse in greater depth how banks can embark on the third part

of the digital journey and what actions they need to take:

Branches: Right size and boost sales performance

Call centres: Make it the preferred channel for support

Digital: Open the Digital Bank before non-banks do

Multichannel processes: Optimise to eliminate leakage and

improve experience

Branches: ‘Right size’ and boost sales performance

Recent research by McKinsey highlighted how branches are becoming more sales

and advice oriented, and suggested that in the light of future customer needs it should

be possible to free up 30-50 percent of costs by adapting the design of the branch

network, and to increase sales per front-office employee by 20%. Any branch transfor-

mation should be structured around the following dimensions:

Light size network. Banks can optimise their branch networks by adapting both the

location of branches and branch formats to client needs.

— Tailor footprint. Branch network costs can be reduced by as much as 20%.

Sales can simultaneously be increased through improved understanding of

customer preferences and behaviour (and more importantly future behaviour)

in each micro market, as well as better aligning capacity to demand. This is not

only about cutting capacity, but about ensuring that capacity is situated where

it is needed. Whereas ‘contribution to profit’ was previously the main consider-

ation when deciding whether to maintain, open or close a branch, other param-

eters such as customer experience or access to funding may be as important

in a low interest rate environment. [See exhibit 3].

— Differentiate branch formats: Whereas the format used in the branches of many

incumbent retail banks was previously uniform across the network, there is

greater diversity today. Examples of new formats are specialised branches for

high value segments (e.g., affluent, SMEs), small service or sales points of 2-4

employees for simple products, and totally automated branches that focus

exclusively on service [Exhibit 4].

Boost sales. Banks can increase the time they spend on sales, and use that time

more efficiently. Here are a number of actions to consider:

— Free-up time for sales: by migrating low value-added activities to low-cost

channels, in particular online and in-branch automated channels.

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 5

Exhibit 3

Exhibit 4

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 6

— Increase sales effectiveness via the following levers:

□ Structure better the time spent on sales. For example, concentrated peri-

ods of commercial activity tend to be more effective and efficient than peri-

odic bursts of activity.

□ Industrialise the sales and support process. This can be one of the most

productive aspects of any branch transformation. Doing so requires choos-

ing a few routines and processes (activity planning, selection of contacts,

standard execution drills, using an activity registry) and aligning each one

to a member of the organisation so as to ensure they are performed in a

controlled fashion. In combination with the right campaigns this can boost

sales by 20%-30%, although rolling it out across the network is time con-

suming and requires an intense effort.

□ Provide branch staff with high quality leads, by using the bank’s own data

and combining this with customer insights from additional behavioural data.

— Improve performance management. In order to successfully transform a bank’s

branch network staff and managers will require strong performance manage-

ment disciplines (for example, operational KPIs that staff can influence, and

effective performance dialogues) and proactive skills development.

Call/ Video Centres: Make them the preferred channel for support

The role of call centres is changing as banks migrate their basic activities to digital

channels (notably the web and mobile), and clients dial a call or video centre to seek

advice and support. Capturing the benefits requires banks to:

Increase service to sales conversion. Call centres are potentially able to convert

service calls into sales, but to do so they must have the right capabilities. Using a

conservative ‘service to sales success’ ratio of 3% (good players go above 5%), the

sales generated by one branch would be equivalent to what four agents of a call

centre could achieve. The best call centres (with eligible calls conversion-into-sales

rates of 6-9%) try to make a sale on 20-50% more occasions than the average call

centre, aided by the intelligent call routing of customers to the best agents, use

of CRM, and an approach to performance management that aims to develop the

appropriate mindset. [See exhibit 5: Service to Sales conversion]

Upgrade quality to become the preferred channel. Many European banks are

increasingly using their call centre to provide high quality service and advice (and

sales) for customers. This remote phone channel is, today, typically exclusive to

certain segments and not available to the full customer base. In some countries like

the UK this has become the standard way to serve affluent customers. These call

centre ‘islands’ – staffed by people with higher skills – spearhead the drive for new

sales and provide excellent customer service. [See exhibit 6 for an example]

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 7

Exhibit 5

Exhibit 6

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 8

Be ready for video. The mix of people in centres may have to change, as old scripts

may no longer work and the visual aspect starts to assume a new importance

Free-up capacity: There is an additional efficiency opportunity. In this context,

many call centres have the scope to improve their demand management with

better forecasting and staffing, to reduce call times, and to optimise call routing.

Between them these can translate into a 10-20 percent cost reduction opportunity.

Digital: Open the digital bank before non-banks do

So far banks have mainly used digital channels to provide services to their customers,

but we see the emphasis rapidly switching to sales. Online and mobile channels, we

believe, will ultimately converge to create the truly digital bank. The most important

step for those embarking on this part of the transformation is to make sure their online

services are coherent and well designed, and that they engage users. One European

bank discovered recently that only 5% of its sales were made online, yet more than a

third of clients said they would prefer to buy products in this way. It turned out that the

bank’s inconvenient, poorly designed website was responsible.

This will require banks to create “the Apple experience”. As with the products and ser-

vices of the US technology company, customers of the banks that get it right will not know

exactly what’s good about the service they are using, but it will work and they will like it.

Here are key elements that need to be addressed to create the digital bank in this respect:

Make digital channels the channels of choice

— Increase penetration: Stimulate more customers to use the bank’s apps and

websites more often.

— Create a “wow” experience for clients: innovations might include easier log-on,

faster and more flexible transactions, and well laid-out screens.

— Make information easily accessible: about 20% of all products sold by banks

are first evaluated by clients on the internet, mainly via aggregators and com-

parison sites (as with insurance). If banks do not provide clear and transparent

information these aggregators will direct customers to someone else’s site.

— Address security concerns: some 45% of consumers say this is the single most

important reason why they don’t bank online. It may be more a matter of per-

ception than reality, but if so banks have to alter that perception.

Attract high quality traffic and leads

— Use event marketing to attract traffic. This will become an essential part of the

initial phase of the purchasing process as customers increasingly search for

information on the internet, notably via aggregators and online benchmarks,

before deciding which product to buy (through any channel).

EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 9

Exhibit 7

— Use CRM and behavioural data. Banks are sitting on an enviable wealth of

information, but so far most have only used the tip of the iceberg.

— Use targeted personalised marketing. The Internet enables banks to target

‘segments’ as tiny as just a single consumer. It is possible, for example, to

ascertain exactly who has logged on to a page and then to customise offers or

investment advice to that individual. One bank in an emerging market manually

segmented its clients and then asked IT to insert individualised banners to cer-

tain groups. The initiative generated strong sales from the Internet.

Increase digital conversion by improving process and support

— Introduce ‘easy’ customer support: banks should try everything from video

calls and SMS messages to the careful sifting of emails and phone calls to

addressing clients’ questions while they interact with the bank. Customers with

complex issues, or those of high value to the bank, should have access either

to a premium service number or an adviser in the branch.

— Improve online sales processes: leading players now sell all their most impor-

tant products online – but the processes behind them are not always efficient

and friendly. ING Direct sets a high bar: on its website the bank promises that

an enquirer will get an initial mortgage quote in five minutes, an agreement in

principle within 10 minutes, and completion of the application after a further 10

minutes. [See exhibit 7: Best practice times]EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 10

Exhibit 8

Join your clients in their world through social media

— Build digital fame: Banks such as JPMorgan have successfully used social

media ‘communities’ to allocate sponsorships, generating millions of new fol-

lowers and much beneficial, low-cost publicity.

— Understand Generation Y: social media is ideal for a better understanding of

client behaviour and client interests. The most advanced banking players in this

respect are leveraging these new networks to help develop new applications for

their products. Significantly, 70% of users say they believe recommendations

made through social media, whereas only 20% trust conventional advertising.

— Service clients: this can be done by responding quickly to questions on Twitter

and other digital sources of enquiry. Several banks are dedicating resources to

the management of this kind of media, even if some acknowledge that the value

still needs to be proven. If nothing else, banks realise they have to use these tools

to generate awareness and to keep close to customers, especially the young.

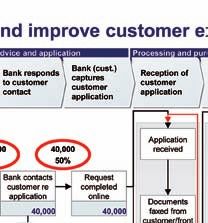

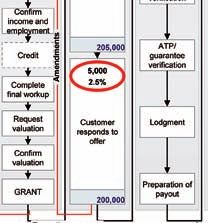

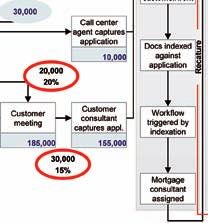

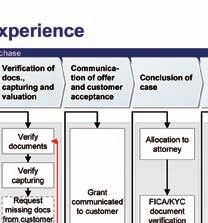

Multichannel: Improve ‘end-to-end’ processes to reduce ‘leakage’

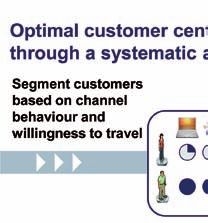

Based on joint research we conducted with EFMA1 it is clear that clients are already

using multiple channels (3-4 per person) to interact with their bank, and that there is a

growing role for online platforms when it comes to sales [See exhibit 8]. Clients voiced

1 See Future of Face 2 Face,

their frustration during the research, however, about the uneven quality of processes

McKinsey and EFMA 2010. and banks’ slow response at different points on the customer ‘journey’. Missing tele-EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 11

Exhibit 9

phone numbers and email addresses on the web, or poor communication between

call centre and branch over a customer’s follow up visit, were among the issues raised.

Inadequate search engines and complex forms result in promising leads being missed.

Often the root cause of this is that no one in the bank is responsible for integrating

products, services and channels in a way that ensures delivery of an integrated value

proposition to every customer. Revenue ‘leakage’ can be as much as 60 – 80 percent

of total generated leads as a result. To improve these processes and identify sources

of such ‘leakage’, banks should take what we call an ‘end-to-end’ approach. This

requires understanding what happens (or doesn’t happen) at different stages of the

customer ‘journey’:

Gaining awareness. Where did clients research the market? How did they decide

which bank to contact? Banks should check their search engine ranking relative to

their peers, and examine their rating by price comparison sites among others.

Consideration. Why did awareness not always convert into a formal sales enquiry?

It may be that forms were too long to hold customer attention or call centres were

unable to handle sales requests.

Purchasing. How many potential customers received an offer, or attended a meet-

ing with an adviser, and then dropped out? It could have been lack of bank follow-

up, excessive documentation or a non-distribution issue such as pricing;

After sales support. Do clients know through which channels they can change

their address or other contact details, and can this be done at the channel ofEMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 12

choice? Have the top five complaints made to the call centre been identified,

understood and addressed?

Banks should draw up and implement an action plan. We have seen banks that did

this improve their sales conversion rates by factor two or more, benefit customers by

providing a better experience, and reduce their average costs of serving each client.

[See exhibit 9]

Organising for success

The transformation journey to this “digital bank with a human face” requires alignment

around a common objective and division of the whole exercise into a portfolio of proj-

ects. Key success factors include:

IT capacity and effectiveness. The transformation will likely touch all relevant bank

systems to a greater or lesser degree; however, we believe that a portfolio of small

IT transformations is key to making the overall transformation successful.

Organisational and governance change: As mentioned earlier, all changes will likely

modify the way the bank organises and governs itself. Banks should bear this in

mind throughout the transformation – sometimes, though, a new structure can be

planned in advance and will help push things forward. Key lessons from organisa-

tional design experience include aspects such as:

— Harnessing the support of the CEO

— Involving all channels and avoiding the sense that channels other than the

branch are merely ‘alternatives’.

— Acknowledging the inevitability of a matrix structure, especially for multination-

als with multi-country outlets.

Cultural change: Change is often most difficult in very traditional banks where

regional leaders hold sway. The issues here are typically cultural, inspired by a feel-

ing that local entrepreneurship, the sense of ownership and the capability of lead-

ers to deliver are all being undermined. On the contrary, such a transformation like

the one we are addressing should be an opportunity to present these executives

with a new set of weapons for combating the challenges of the multichannel world.

Conveying this message through the organisation and making sure everyone

understands the potential is critical. It can be more costly to lose key divisional or

regional leaders than to delay the completion of the project.

New metrics [See exhibit 10]: Banks need to evolve from a retail branch network

view of reporting (product x segment) towards a multichannel view of the MIS

(product x segment x channel X). Our multichannel survey demonstrated how

few banks have an integrated, multichannel view, that their sales activities are not

always transparent, and that the number of leads generated from digital channels

is not always clear.EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 13

Exhibit 10

How to get started

The transformation journey requires action to harness all the energy and capabilities of

the bank. There are many approaches, but having seen many initiatives fail, we believe

pragmatism should be the guiding principle. We see a journey with three stages:

1. Create your own distribution 2015 vision.

The vision needs to be articulated from three angles: the future distribution mix, cus-

tomer experience opportunities and strategic orientation:

Future distribution mix: What is the best blueprint for transactions, service and

complaints as well as sales and advice.

Customer experience. Key questions include: What are the Moments of Truth, and

how can the bank create a “wow” effect? What are the biggest frustrations of cli-

ents? How can innovations lead to improvements in this area?

Strategic posture: Does the bank want to be a shaper of innovation or more a fol-

lower? Which is the greater priority - cost reduction or increasing revenue?

From these three dimensions banks should incorporate several insights to develop

their broader vision: the bank’s overall strategy, an understanding of the starting posi-

tion and current customer base, some references to the competition and a definition

of the target distribution blueprint.EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 14

2. Develop a portfolio of mini-transformations to deliver the vision

This stage is the most critical one for, in our experience; most organisations tend to

get lost. The bank needs to select the most important things it wants to change so as

to translate its vision into action by using the approaches described in the earlier sec-

tions of this article. Many of these mini-transformations will be projects in themselves.

Based on our experience, a quick diagnostic is the most helpful way to ‘size the prize’

as well as to identify the key priority areas. A series of mini-transformations increases

the chances of success and will deliver immediate benefits.

3. Lock in an integrated roadmap and execute

Once all the mini transformations have been sketched out they should be brought

together again in an integrated transformation roadmap. Banks need to:

Maintain and monitor the portfolio of mini transformations

Elaborate a high level business case for pursuing them and monitor progress

Identify the implications for IT and Governance, and monitor accordingly.

***

We have reached an unavoidable turning point in the industry’s development that

creates an opportunity for smart banks to differentiate themselves from their

competitors. The question is not “will branches disappear?”, rather how can banks

win and retain clients who are increasingly using multiple channels and serve them in a

cost efficient way. Few banks have yet taken this seriously: on average less than 5% of

retail product sales are handled online, and in the case of most players their full prod-

uct range is not even available online. We believe banks therefore need to step up their

game and radically transform their distribution model.EMEA Banking Practice

Retail Distribution 2015 – Full Digitalisation with a human touch 15

The authors would like to thank Stephanie Hauser, Nuno Catarino, Jaap Versfelt,

Johan Reiersen, Vincent Cremers, Leorizio D’aversa, Enrico Scopa, Carlos Trascasa,

Vito Giudici, and Paul Jenkins for their contributions to this article.Retail Authors:

Distribution

Victor Matarranz Enrico Scopa

2015 – Full

Principal Principal

Digitalisation Madrid Prague

with a human victor_matarranz@mckinsey.com enrico_scopa@mckinsey.com

touch

Radboud Vlaar

Principal

Amsterdam

radboud_vlaar@mckinsey.com

EMEA Banking Practice

December 2011

Copyright © McKinsey & Company, Inc.You can also read