River Islands Public Financing Authority (Community Facilities District No. 2003-1) - Webflow

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 River Islands Public Financing Authority (Community Facilities District No. 2003-1) $37 Mln. Special Tax Bonds, Series 2019A Terence M. Smith, April 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 1

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019

Introduction

Smith's Special Tax Bond Gradings are driven by a proprietary critical information system that are triggered by

specific events, such as fast-moving pandemics or slow-moving changes to demographics, that may threaten

the repayment of public projects financed by Van Eck’s High Yield ETF. Smith’s Special Tax Grades are a subset

of Smith’s Land Secured category. Over the past two decades, Smith's Municipal Bond Gradings have become

more anticipatory with a greater understanding of the event risks.

Smith’s Special Tax Bond Grades for California Communities

Smith’s land-secured bonds are typically issued through special taxing districts, which are independent

governmental units that exist with varying degrees of administrative and fiscal independence from local

governments. Each State has its own laws which govern the structure and sale of land-secured bonds. But, the

structures, debt security features and issuance procedures often share many similarities. Basically, a land-

secured bond works like this: Within the special community district, a tax lien is placed on property benefiting

from the public infrastructure constructed with proceeds from the bond issue. This lien is paid off over time via

periodic assessments or taxes, which thoughtfully leverages the public’s capital over the useful life of the

assets. The tax revenues generated from the assessments are used to pay debt service on the bonds. This is

described as a “special tax” or “assessment lien” because it is senior to any mortgage on the property. Smith’s

land-secured gradings are usually initially unrated bonds but may be rated by the credit rating agencies after

the development is built out.

Security Features Support the Bonds

Land-secured bonds are generally a higher-risk sector. However, the risks may decline as additional vertical

development occurs and taxpayer diversity increases, which gives a fully developed Mello-Roos district many

of the same characteristics of a limited G.O. bond.

In addition, land-secured bonds carry additional credit features:

Value-to-lien ratios: The value-to-lien ratio represents the degree of leverage in the bond financing. It is

calculated by dividing the value of the land within the district by the district’s outstanding debt. The ratio is

the debt allocable to individual parcels. Certain land-secured bonds stipulate a value-to-lien ratio of 3:1 or

higher. The higher the loan to value ratio, the more protection is provided to investors as a measure of security

against future declines in land values. It also provides some protection against the variables involved with the

appraisal process. A 3:1 ratio means that the property value is at least three times the principal amount of the

bonds sold, plus all other bonds outstanding. A higher value-to-lien ratio indicates the property owners or

mortgage holders are more likely to promptly pay the taxes and or assessments due. The willingness to pay

reflects the reality that if taxes are not paid on time then foreclosure may commence.

Foreclosure covenant: Municipalities issuing bonds have no legal obligation to pay the bond debt if revenues

from taxes or assessments are insufficient. However, the municipal issuer has the right to foreclose against

delinquent property owners once delinquencies reach a specified level. The method and length of time it takes

to foreclose and sell property or tax liens varies across states. However, such ability may have little or no effect

on forestalling a default.

Reserve funds: A debt service reserve fund is generally funded with bond proceeds at issuance and provides a

measure of cushion if tax delinquencies in the district cause tax revenues to be insufficient to make a full debt

service payment.

RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 2

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019

Market Focus: California

Development in California over the last few decades has increased the issuance of land-secured municipal

bonds. Roughly half of the land-secured bonds issued in the United States originate in California. From a big

picture perspective, there are two types of land-secured bonds issued in California: Special Tax District or CFD

(Community Facilities District) bonds are issued under the “Mello-Roos Community Facilities Act”. Special

Assessment District bonds, or simply assessment bonds, are based on the “1915 Bond Act”.

CFD bonds are most common, which frequently finance infrastructure for new development on the local

government level. CFDs provide more flexibility to address shortfalls due to delinquencies, such as the ability

to increase taxes (within limits), and are less of a legal burden to prove the specific benefit of the infrastructure

improvement project to the property. However, formation of a CFD requires a two-thirds vote from existing

property owners, whereas the formation of an Assessment District requires a 50% ballot approval. California

structures offer advantages. CFD bonds have experienced minimal distress as compared to structures in some

other states. Although there were some distressed CFDs due to the severe downturn in the real estate market

in the late 2000s, California CFDs held up well with very few defaults, primarily due to these factors:

• Disclosure and structuring improved due to the lessons learned from defaults in the 1990s. For

instance, a significant amount of vertical development has now typically occurred before bonds are

issued.

• Districts are controlled by a city, county or government entity (versus developer-controlled in states

such as Florida).

• An appraisal is required by policy, which is not always required in other states. The foreclosure process

is aggressive and can begin quickly (approximately 180 days after delinquency) by stripping the special

tax portion of total tax bill and beginning the judicial process.

• A minimum 3:1 value-to-lien ratio is required.

• Development and financing is phased, often with multiple owners at issuance. The developer

frequently puts up its own money (since infrastructure is needed to begin development) to be

reimbursed when bonds are issued.

• While property is generally largely developer-owned at bond issuance, it is eventually transferred to a

diversified pool of land owners and the investor effectively holds a limited tax general obligation bond.

• California has a large economic base and will likely recover faster than weaker markets. Bonds are

typically sized to maximize special taxes, which is typically a 1.10 to 1.25 coverage multiplier. This

offers some measure of protection against delinquencies.

Current market shows significant improvement

Although California was roiled by the housing downturn from 2008 to 2011, only a small handful of CFDs

defaulted. The market has dramatically improved, with the California land-secured sector enjoying significant

credit improvement. Property values have recovered significantly and homebuilders have resumed

development on projects once mothballed, leading to substantial new home absorption. In addition, land

values in most markets have increased as homebuilders put money to work acquiring land for future deals.

Given the resurgence of the California economy, there is strong housing demand and a shortage of lots in more

coastal locations. This demand has led to the strong success for some of the few large scales developments like

RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 3

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 The Great Park in Irvine and Sendero and Esencia within the Orange County Rancho Mission Viejo Masterplan. As evidence of the strength of California CFD’s, there is roughly $16.9 billion in Mello-Roos Bonds outstanding across 921 CFDs and 1,455 separate bond issues and, according to the California State Treasurer, only 7 issues experienced draws on reserve funds in 2017. This is a very low number, given the size of the market, and a testament to the strength of the market for California land secured bonds. During the real estate market stress between 2008 and 2011, CFD delinquency rates soared, in some cases reaching 25%. However, debt service was still paid due to the excess debt service coverage, the sponsoring municipalities’ ability to increase the tax levy and strict foreclosure rules for special tax delinquencies. California passed a critical test in the 2008 to 2011 period by exiting such a difficult period with a low level of defaults. However, each project is unique and must be individually evaluated, as default risk will always exist in this high yield and credit intensive sector. Flash Report Issuer: River Islands Public Financing Authority Obligor: Community Facilities District No. 2003-1 Issue: $38,490,000 Special Tax Bonds, Series 2019A Use of Proceeds: Public Improvement. (i) finance the costs of public improvements eligible to be funded by the District, (ii) make a deposit to a reserve fund that secures payment of the 2019A Bonds and certain other bonds issued for the District, (iii) fund capitalized interest on the 2019A Bonds through September 1, 2019, (iv) repay bond anticipation notes issued by the Authority in 2018, and (v) pay the costs of issuing the 2019A Bonds. Security Provisions: Pledge Under the Fiscal Agent Agreement. Pursuant to the Fiscal Agent Agreement, the Bonds are secured by a first pledge of all of the Special Tax Revenues (other than the Special Tax Revenues needed by the Authority in each Fiscal Year to pay Administrative Expenses, but not in excess of the annual Priority Administration Amount), and all moneys deposited in the Bond Fund, the Reserve Fund and, until disbursed in accordance with the Fiscal Agent Agreement, in the Special Tax Fund. Debt Service Reserve: The Reserve Fund is required to be funded in an amount equal to, as of any date of calculation, the lesser of (i) the then Maximum Annual Debt Service for the Bonds, (ii) one hundred twenty-five percent (125%) of the then average Annual Debt Service for the Bonds, or (iii) ten percent (10%) of the then outstanding principal amount of the Bonds. NOTE: The Reserve Fund will be available to pay the debt service on the 2019A Bonds, the 2015 Bonds and any future Parity Bonds in the event of a shortfall in the amount in the Bond Fund for such purpose. The Reserve Requirement as of the date of issuance of the 2019A Bonds will be $15,763,093.68. A portion of the proceeds of the 2019A Bonds in the amount of $1,712,574.03 will be deposited to the Reserve Fund; which amount, together with funds already on deposit in the Reserve Fund, will increase the amount on deposit therein to the amount of the Reserve Requirement as of the date of issuance of the 2019A Bonds. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 4

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Authorized Denominations: Issued Book Entry in the principal amount of $5,000 and any integral multiple thereof. DTC. Redemption Features: The 2019A Bonds maturing on and after September 1, 2027 are subject to Optional Redemption prior to their stated maturity on any Interest Payment Date occurring on or after September 1, 2026. The 2019A Bonds maturing on September 1, 2038 bearing interest at 5.00%, are subject to Mandatory Sinking Payment Redemption in part on September 1, 2034, and on each September 1 thereafter to maturity. The bonds are also subject to Mandatory Redemption from Special Tax Prepayments. In lieu of redemption as described above, moneys in the Bond Fund may be used and withdrawn by the Fiscal Agent for purchase of Outstanding 2019A Bonds. Payment Dates: Semi-Annually. March 1 and September 1, starting Sept. 2019. Maturity: $9.32 Mln. Serial Bonds. Underwriter: Hilltop Securities Bond Counsel: Quint & Thimmig LLP, San Francisco, California Fiscal Agent (Trustee): Wilmington Trust, National Association Property Developer/Manager: River Islands Development, LLC Location: River Islands is a planned community located in Lathrop, California. The Property is located west of I-5 at Louise Avenue and immediately west of the San Joaquin River. Lat: 37.795306 Long: -121.333145 Review Date: April 3, 2019 Smith’s Grading: 55/4/0 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 5

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Description of Issuer: The Authority was formed on January 23, 2003 pursuant to a joint exercise of powers agreement between the Lathrop Irrigation District and Island Reclamation District No. 2062. The territorial jurisdiction of the Authority is within the City of Lathrop, California. The District was formed under the authority of the Mello-Roos Community Facilities Act of 1982, as amended, commencing at Section 53311, et seq., of the California Government Code, which was enacted by the California Legislature to provide an alternative method of financing certain public capital facilities and services, especially in developing areas of the State. The Act authorizes local governmental entities to establish community facilities districts as legally constituted governmental entities within defined boundaries, with the legislative body of the local applicable governmental entity acting on behalf of the district. Subject to approval by at least a two-thirds vote of the votes cast by the qualified electors within a district and compliance with the provisions of the Act, the legislative body may issue bonds for the community facilities district established by it and may levy and collect a special tax within such district to repay such bonds. The Act has provisions that allow for the legislative body of a community facilities district to designate portions of the community facilities district as improvement areas. After the designation of an improvement area, proceedings relative to the rate and method of apportionment of special taxes and bonded indebtedness apply separately for the improvement areas. The District includes two improvement areas. Regionally, the Property is centrally located in San Joaquin County, with regional shopping opportunities available approximately 10 to 15 minutes to the west in Tracy or 10 to 15 minutes to the north in Stockton and east in Manteca. A regional hospital is just 10 minutes to the north at I-5 and French Camp. Principal employment centers include Stockton, Tracy, eastern Alameda County, and the larger San Francisco Bay Area to the west. New homes in the neighborhood are generally priced between $400,000 and $650,000. The Lathrop area has historically offered a more affordable residential alternative to areas to the west that are closer to the San Francisco Bay Area and Silicon Valley job markets. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 6

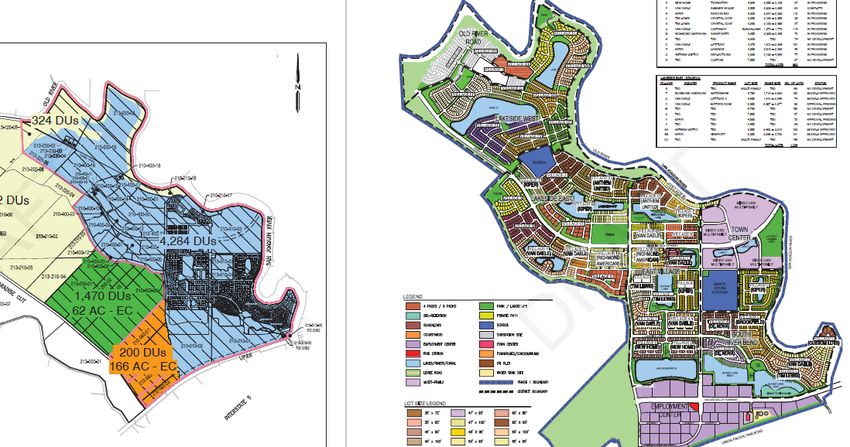

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Use of Proceeds: Public Improvement. (i) finance the costs of public improvements eligible to be funded by the District, (ii) make a deposit to a reserve fund that secures payment of the 2019A Bonds and certain other bonds issued for the District, (iii) fund capitalized interest on the 2019A Bonds through September 1, 2019, (iv) repay bond anticipation notes issued by the Authority in 2018, and (v) pay the costs of issuing the 2019A Bonds. Overview: The District is located in the City of Lathrop, in San Joaquin County, California. The County is located in the Central Valley of California, approximately 60 miles east of San Francisco and is south of Sacramento and north of Stanislaus County. The City is 55 miles south of Sacramento and 10 miles south of Stockton at the junction of U.S. Interstate Highway 5 and State Highway 120. The District was formed by the Board of Directors pursuant to proceedings conducted under the Act on June 12, 2003. The Improvement Areas of the District currently include approximately 1,573 acres of land within Phase 1 of a planned development community known as River Islands at Lathrop (referred to in the Official Statement as “River Islands Phase 1”), and an additional approximately 670 acres of land being developed as part of Phase 2 of the River Islands at Lathrop Development (“River Islands Phase 2”). At buildout, the property within the District is currently expected to include approximately 3,741 single family detached homes, 100 apartments and 967 townhouses, as well as a 61.9 acre commercial “town center” expected to be developed with retail uses, and a 166.0 acre commercial “employment center” expected to be developed with research and development and office uses. River Islands Phase 2, most of which is not included in the District, is expected to be developed in the future with 6,176 housing as well as commercial space, parks and schools. The acquisition of potable water rights and the construction of an offsite sanitary sewer plant for River Islands Phase 1 began in 2003, and at that time Califia, LLC and The Cambay Group, Inc. owned all of the property in the District. Beginning in 2005, Califia, LLC and The Cambay Group, Inc. began construction of flood control improvements and other onsite infrastructure. Califia, LLC and The Cambay Group, Inc. sold the majority of the land in River Islands Phase 1 over the last five years to River Islands Development, LLC which has become the primary entity responsible for the construction of infrastructure improvements needed for the property (referred to in this Preliminary Official Statement as the “Master Developer”). The Cambay Group, Inc. no longer owns any property in the District. Califia, LLC currently only owns the town center area and the flood protection levee within Phase 1. The Developer The Master Developer, which is an entity related to the Cambay Group, Inc., has continued to develop the property and began selling finished lots within River Islands Phase 1 to homebuilders in 2013. Single-family home construction began in 2014. As of November 30, 2018, the Master Developer advised that it has contracted to sell 2,055 parcels for single family homes to homebuilders, of which 1,343 parcels have actually been sold to homebuilders; and homebuilders have sold 1,128 homes to homebuyers, 890 of which sales have closed escrow. Between November 30, 2018, and January 31, 2019, the Master Developer reports that 104 additional parcels had actually been sold to homebuilders; and between the end of November, 2018, and December 31, 2018, homebuilders had sold an additional 53 homes to homebuyers, and an additional 51 home sales had closed escrow. Sales of homes by the homebuilders are ongoing. The remaining property in the District is in various states of development. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 7

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Data for Annual Administration On or about July 1 of each Fiscal Year, the Administrator shall identify the current Assessor’s Parcel numbers for all Taxable Property. The Administrator shall also determine: (i) within which Improvement Area each Parcel is located, (ii) whether each Assessor’s Parcel is Developed Property or Undeveloped Property, (iii) for Developed Property, which Parcels are Single Family Detached Property, Single Family Attached Property, Multi-Family Property, and Non-Residential Property, (iv) for Single Family Detached Property, the square footage of each residential lot, and (v) the Special Tax Requirement. If, in any Fiscal Year, an Assessor’s Parcel includes both Developed Property and Undeveloped Property, the Administrator shall determine the Acreage associated with the Developed Property, subtract this Acreage from the total Acreage of the Assessor’s Parcel, and use the remaining Acreage to calculate the Special Tax that will apply to Undeveloped Property within the Assessor’s Parcel. To determine the square footage of each Parcel of Single Family Detached Property, the Administrator shall rely first on Assessor’s Parcel Maps or, if the square footage is not yet designated on such maps, on the Final Map recorded to create the individual lots. In addition, the Administrator shall, at least twice each Fiscal Year, determine: (i) whether changes have been proposed or approved to the Formation Land Use Plan; and (ii) whether Final Maps that have been proposed for approval or already approved by the City are consistent with the Formation Land Use Plan. If changes to the Formation Land Use Plan have occurred, or if Final Maps are inconsistent with the Formation Land Use Plan, the Administrator shall apply the steps set forth in Section D below. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 8

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Pursuant to Section 53321 (d) of the Act, the Special Tax levied against a Parcel used for private residential purposes shall under no circumstances increase more than ten percent (10%) as a consequence of delinquency or default by the owner of any other Parcel or Parcels and shall, in no event, exceed the Maximum Special Tax in effect for the Fiscal Year in which the Special Tax is being levied. Method of Levy of the Special Tax Each Fiscal Year, the Administrator shall determine the Special Tax Requirement to be collected in that Fiscal Year, and the Special Tax shall be levied according to the steps outlined below. Step 1: The Special Tax shall be levied Proportionately on each Parcel of Developed Property within the CFD up to 100% of the Maximum Special Tax for each Parcel for such Fiscal Year determined pursuant to Section C; Step 2: If additional revenue is needed after Step 1, and after applying Capitalized Interest to the Special Tax Requirement, the Special Tax shall be levied Proportionately on each Assessor’s Parcel of Undeveloped Property within the CFD, up to 100% of the Maximum Special Tax for Undeveloped Property for such Fiscal Year determined pursuant to Section C; Step 3: If additional revenue is needed after applying the first two steps, the Special Tax shall be levied Proportionately on each Parcel of Association Property within the CFD, up to 100% of the Maximum Special Tax for Undeveloped Property for such Fiscal Year determined pursuant to Section C; Step 4: If additional revenue is needed after applying the first three steps, the Special Tax shall be levied Proportionately on each Assessor’s Parcel of Excess Public Property, exclusive of property exempt from the Special Tax pursuant to Section G below, up to 100% of the Maximum Special Tax for Undeveloped Property for such Fiscal Year determined pursuant to Section C. F. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 9

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Collection of Special Tax The Special Taxes for CFD No. 2003-1 shall be collected in the same manner and at the same time as ordinary ad valorem property taxes, provided, however, that prepayments are permitted as set forth in Section H below and provided further that the Authority may directly bill the Special Tax, may collect Special Taxes at a different time or in a different manner, and may collect delinquent Special Taxes through foreclosure or other available methods. The Special Tax shall be levied and collected until principal and interest on Bonds have been repaid and authorized facilities to be constructed from Special Tax proceeds have been completed. However, in no event shall a Special Tax be levied after Fiscal Year 2075-76. Prepayment of Special Tax The following definitions apply to this Section H: “Outstanding Bonds” means all Previously Issued Bonds which remain outstanding, with the following exception: if a Special Tax has been levied against, or already paid by, an Assessor’s Parcel making a prepayment, and a portion of the Special Tax will be used to pay a portion of the next principal payment on the Bonds that remain outstanding (as determined by the Administrator), that next principal payment shall be subtracted from the total Bond principal that remains outstanding, and the difference shall be used as the amount of Outstanding Bonds for purposes of this prepayment formula. “Previously Issued Bonds” means all Bonds that have been issued on behalf of the CFD prior to the date of prepayment. “Public Facilities Requirements” means either $88,734,000 in 2003 dollars, which shall increase on January 1, 2004, and on each January 1 thereafter by the percentage increase, if any, in the construction cost index for the San Francisco region for the prior twelve (12) month period as published in the Engineering News Record or other comparable source if the Engineering News Record is discontinued or otherwise not available, or such lower number as shall be determined by the Authority as sufficient to fund improvements that are authorized to be funded by the CFD. The Public Facilities Requirements shown above may be adjusted or a separate Public Facilities Requirements identified each time property annexes into CFD No. 2003-1; at no time shall the added Public Facilities Requirement for that annexation area exceed the amount of public improvement costs that are expected to be supportable by the Maximum Special Tax revenues generated within that annexation area. “Remaining Facilities Costs” means the Public Facilities Requirements (as defined above), minus public facility costs funded by Outstanding Bonds (as defined above), developer equity, and/or any other source of funding. The Special Tax obligation applicable to an Assessor’s Parcel in the CFD may be prepaid and the obligation of the Assessor’s Parcel to pay the Special Tax permanently satisfied as described herein, provided that a prepayment may be made only if there are no delinquent Special Taxes with respect to such Assessor’s Parcel at the time of prepayment. An owner of an Assessor’s Parcel intending to prepay the Special Tax obligation shall provide the Authority with written notice of intent to prepay. Within 30 days of receipt of such written notice, the Authority or its designee shall notify such owner of the prepayment amount for such Assessor’s Parcel. Prepayment must be made not less than 75 days prior to any redemption date for Bonds to be redeemed with the proceeds of such prepaid Special Taxes. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 10

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 11

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Land Valuation The Property is located west of I-5 at Louise Avenue and immediately west of the San Joaquin River. This is a low-lying level area of an irregular shape. The mature portion of the community of Lathrop lies to the east of the San Joaquin River and I-5. To the south of Louise Avenue, on the east side of I-5, is the Crossroads Commerce Center, a large development improved with light manufacturing and warehouse uses. Krauss Appraisal, LLC has prepared an appraisal dated January 24, 2019 with a valuation date of December 12, 2018, estimating the market value of the parcels within the District that are subject to the Special Tax securing the Bonds. The Appraiser concluded that the estimated market value of the property in the District as of December 12, 2018 on a bulk sale basis was $786,700,000, which is approximately 4.13 times the total of initial principal amount of the 2019A Bonds and the current outstanding principal amount of the 2015 Bonds (total of $190,535,000). RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 12

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 13

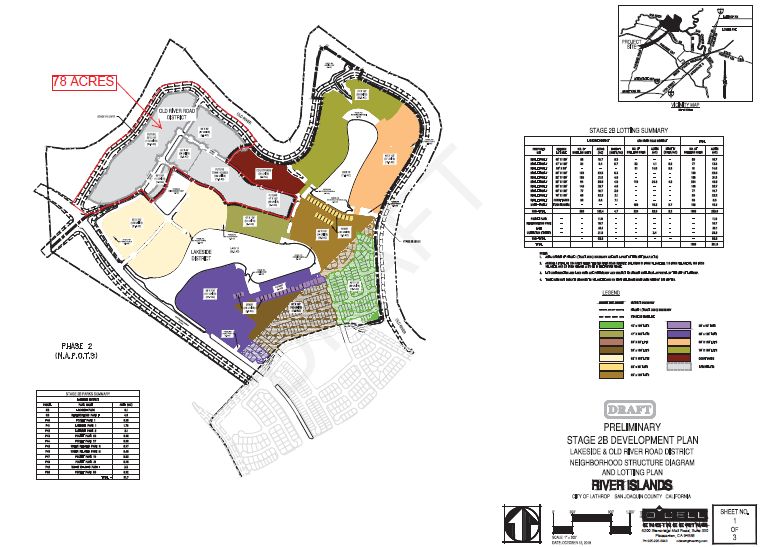

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Property History The Property had historically been used for agricultural purposes, largely row crops. The Property is part of a larger proposed development area known as the West Lathrop Planning Area and is included in the West Lathrop Specific Plan, produced in 1996, but substantially revised in October 2002. The Property, along with other surrounding properties in the West Lathrop Planning Area, were annexed to the City of Lathrop in early 1997, and together they have been the focus of a substantial amount of planning and development activity. River Islands is a planned community located in Lathrop, California, on land adjacent to the San Joaquin River system. The large, nearly 5,000-acre project area is also identified as the Stewart Tract. River Islands is expected to eventually accommodate a community of 11,000 homes, a town center and an employment center, as well as an extensive open space system, schools and other public land use areas which will take advantage of the site’s location on the San Joaquin River. Flood Plain A review of FEMA flood plain maps 06077C0615F, 06077C0620F, and 06077C0605F indicate that all the development area of Phase 1 is located in flood plain X and AE. Three Letter of Map Revisions (LOMR) have been recorded on Stages 1, 2A, and 2B. The first was recorded effective April 19, 2017 and includes most of the areas being actively developed. The second was effective on October 23, 2017 and includes Stage 2A. The third was recorded on July 9, 2018 and includes Stage 2B. The LOMR’s brought the areas out of the flood plain and allowed for development. The areas included in the LOMR’s are identified as having a reduced flood risk due to levees. Eventually the entire project, including Phase 2 will be protected by 200-year flood levees. As of the date of value only 78 acres of Phase 2 was levee protected. The lake portions of the Property are located in FEMA Zone AE. Development of areas in flood Zone AE would require removing them from the flood plain or flood insurance. It is noted the eastern portion of the Property is adjacent to the San Joaquin River. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 14

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Competitive Analysis The Kraus Appraisal reported, “In summary, with regards to supply, there will be competition for buyers of homes built at the Property from other developments in the West Lathrop area. To some extent, there will be modest competition from the communities of Manteca and Tracy, but demand generally improves as you move west towards the major employment centers. Homes in Tracy have historically sold at a premium over homes offered in the Lathrop area, but the supply will be limited in the future due to development restrictions. Some demand is anticipated from Manteca to the east, but with limited scale and this area is further from the major employment centers. Mountain House will also offer a competitive product, but prices are likely to be higher, due to its closer proximity to the Bay Area job market. Projects located north of the Property, in the areas of Stockton and Lodi, will not create significant competition for the Property due to their location, which is further from the Bay Area job market.” RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 15

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 16

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Demand Meyers Research Report of December 2018 found: 1) Market conditions have slowed in the last 3 months however absorption on average remains fairly healthy at approximately 4.0 homes per month per project. 2) Base Prices for the Subject should range between $430,000 and $687,500 and average $520,385. 3) We expect continued solid absorption from phases 2a and 2b. Full sellout of these next phases is expected to occur in 2025 with the majority of units sold by 2022. Phase 2a will begin selling in 2019 with the bulk coming online in 2020. Phase 2b will begin selling in 2021 with the bulk online by 2022. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 17

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Retail and Commercial Demand Within the District area, there are approximately 454.2 acres of land designated for retail and employment commercial use. This includes 226.2 acres in Phase 1 and an additional 228 acres of land that is included in Phase 2, but is not levee protected. The most important retail development in western San Joaquin County is the West Valley Mall regional shopping district located on the north side of I-205, approximately 10 minutes west of the Property, within the City of Tracy. This retail area, which includes a regional mall with tenants such as Target, Best Buy, JCPenney, Macy’s, Sears, and others, has developed along with satellite retail and service commercial uses over the past 20 years. At present, there are several auto dealerships adjacent to the mall, as well as other stand-alone retail and service commercial uses consisting of numerous fast-food restaurants, a Home Depot, Bed Bath & Beyond, Michael’s, and Costco. Approximately six miles to the east is the Promenade Shops at Orchard Valley in Manteca, which is another regional center that is anchored by Bass Pro Shops. This is a 721,000 square foot center that has significant vacancy after opening around 2008. Additional tenants include JC Pennys, AMC Theatres, Red Robin, Banana Republic, Guess, and Vans. This center was recently marketed for sale, but does not appear to have sold. As a result of this regional development, there is likely to be limited demand in the immediate future for regional retail and commercial uses at the location of the Property. Within the Property, there are approximately 226.2 acres of land designated for either retail commercial use or employment commercial use that is currently flood protected. The total acreage for the town center use is 61.9 acres. The total land designated for employment commercial use is 164.3 acres. The 228 acres in Phase 2 is not flood protected and does not have an approved tentative map. The demand and build-out for the non-residential sites within the Property is more difficult to quantify than the residential RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 18

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 use as discussed in the previous section. Key considerations include: 1) The River Islands Business Park offers a good location for office, flex/ R&D and eventually retail use, though the commercial development will be dependent on increased household growth and traffic levels within River Islands. 2) Competitive retail sites limit the opportunity for retail development. 3) Our Retail Supply-Demand analysis indicates an opportunity for a neighborhood-oriented retail center by 2028. 4) Our office demand model supports approximately 33,000 square feet of office space at River Islands Business Park over the next ten years. 5) Our Flex/ R&D demand model supports approximately 37,000 square feet of office space at River Islands Business Park over the next ten years. The following table indicates the total value of the areas included in Phase 1 of the District based on varying discount rates and the resulting net present value of the District. The table supports a wide range of value depending on the discount rate relied on. Discount Rate NPV 10.5% $ 815,600,000 12.5% $ 797,200,000 14.5% $ 780,600,000 16.5% $ 765,500,000 18.5% $ 751,800,000 Discussions with home builders, the results of yield rate surveys, and the Appraiser’s experience is relied on to estimate a discount rate for the analysis. A value that is near the middle of the range is selected to account for the large scale of the project and the risks associated with the project. A rate of 14.5% is estimated for this analysis. The present value of the net cash flows from remaining land that hasn’t been transferred to homeowners and homebuilders, as reflected in the cash flow model, is $249,100,000 for the Property, rounded. To this amount several line items are added to account for items that are either completed or add value to the Property. Last, the estimated value of the areas in Phase 2 that are included are added to yield the final estimated value of $822,000,000 ($749,970,000 + $20,500,000 + 51,500,000, rounded). THE CMA revolves around the 205 commute corridor into the Bay Area. Markets further west in this CMA tend to be more expensive as they get closer to the core bay area and commute times shorten. The River Islands Market tends to position below Tracy and Mountain House. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 19

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 20

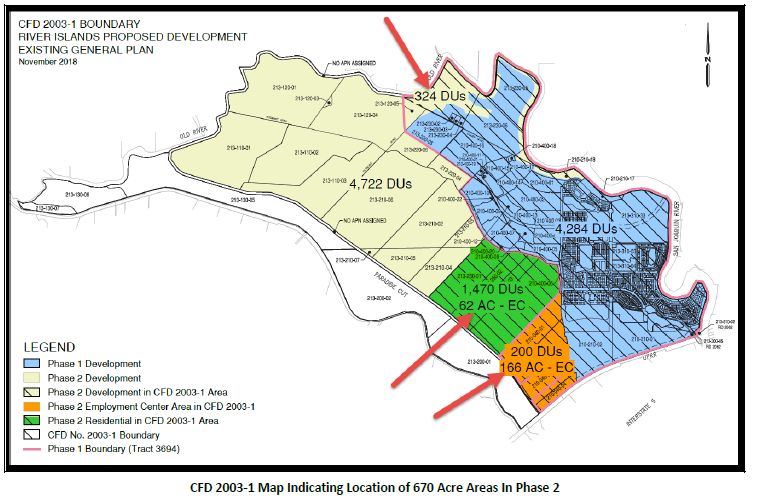

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Phase 2 The remaining area of Phase 2 has limited development potential until it is flood protected, which is not anticipated to happen until Phase 1 is nearing completion. The current plan is to complete levees that will flood protect all of Phase 2, which are anticipated to be completed in the next two years. The area that is not flood protected is currently planned to be developed with 228 acres of Employment center uses and the remaining area is planned for residential development or other suburban uses typical of River Islands. Until a tentative map is recorded, any land use is speculative, but maps provided indicate the area is planned to accommodate 1,670 dwelling units. The following map indicates the approximate location of the areas that make up the 670 acres in Phase 2, the area are identified with red arrows. The areas include the entire orange and green highlighted areas on the map and an irregular shaped beige area at the northern end of Phase 1 (identified as the 78-acre area on the previous map). RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 21

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 Appraisal SEVEN HUNDRED EIGHTY SIX MILLION SEVEN HUNDRED THOUSAND DOLLARS -$786,700,000- The above value estimate represents the Appraiser’s estimate of the market value of the Property on a bulk sale basis consistent with the definition of “Market Value” as included in the addendum of this report and is net of all property taxes including assessment liens and special taxes authorized to be levied under the Act by the District or by any other community facilities district formed under the Act. RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 22

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 23

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 24

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019 RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 25

SMITH'S RESEARCH & GRADINGS APRIL 3, 2019

© Smith’s Research & Gradings, 2019

This report is provided for information purposes only.

Smith’s Research & Gradings makes no representations as to the adequacy or accuracy of the information.

RIVER ISLAND COMMUNITY DISTRICT NO..2003-1, CA. TERENCE M. SMITH 26You can also read