RMBS Performance Watch: Australia - Market Overview - As of June 30, 2020 - S&P Global

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RMBS Performance Watch: Australia - Market Overview As of June 30, 2020

Australian Macroeconomic Environment Recovery from lockdown will be bumpy and protracted

S&P Global Ratings Economic Outlook: Australia

2020f 2021f Outlook Effect on credit quality

Real GDP (4.0) 5.3 Outside of Victoria, Australia has Negative. Reduced economic growth

forecast (% year flattened the COVID-19 curve. The will add debt-serviceability pressure

over year) economy reopened and consumer for some borrowers. Stimulus

activity rebounded in May. Recovery packages, lower interest rates, and

may take longer than expected. access to superannuation should help.

Unemployment 7.5 6.9 Activity is lower than normal, Negative. Rising unemployment will

rate (year subduing labor demand. We do not put pressure on certain borrower

average; %) expect a return to pre-COVID cohorts, influenced by the sectors in

unemployment levels until 2023. which they are employed.

CPI (%) 1.0 1.5 Wage growth remains well below long- Negative. Weak wage growth is likely

term averages. Spare capacity in the to persist for some time. This will be

labor market will keep wage growth offset by historically low interest

subdued for some time. rates.

Policy rate, end 0.25 0.25 The RBA has said it will not increase Positive. Policy rate cuts tend to be

of year (%) the cash rate until unemployment effective in Australia because they

improves. feed through to mortgages, which are

mostly variable rate.

f--Forecast. CPI--Consumer price index. Source: S&P Global Ratings.

3

Job Losses Will Differ By Sector And Geography

Employment exposure Effect on debt serviceability

First wave: The first employment casualties of Leisure, tourism, hospitality

Accommodation and food

Tourism, leisure, COVID-19 due to their sensitivity to workers are more likely to work

services comprise around 7% of

hospitality, lockdowns and closure of international part time and are less represented

total employment.

airline sector borders. in home ownership.

Not severely affected in Q2 due to the A big employer in Australia. A

existing pipeline of work. Construction significant hit to employment in this

Second wave: Construction comprises around

work continued during the first sector could result in debt

Construction 9% of total employment.

lockdowns. A fall in new dwelling serviceability pressures in the so-

approvals may lead to job losses. called mortgage belt.

Not directly affected because Workers typically in higher income

Third wave: employees are more able to work Professional, technical, and and housing debt quartiles.

Professional remotely. Weaker business sentiment scientific services comprise Borrowers who are more highly

services could lead to scaling back of non- around 9% of total employment. leveraged are more vulnerable to

essential consultancy services. income declines.

Source: Employment Exposure Data, Australian Bureau of Statistics; S&P Global Ratings.

4

S&P Global Ratings’ Australian RMBS Outlook

– COVID-19 caused a significant economic contraction in the first part of Q2. A recovery

began during the latter part of Q2 when the economy started to reopen and confidence

returned.

– Household income has been supported by enormous fiscal stimulus, including

JobKeeper payments and access to superannuation withdrawals. Lower interest rates

and mortgage payment deferral schemes have eased debt serviceability pressure.

– Repayment buffers due to a prolonged period of low interest rates will help many

borrowers.

– Setbacks will foster uncertainty for firms and households, leading to cautious behavior.

This will influence investment and hiring decisions.

– Debt-serviceably pressure will likely emerge in Q4 2020, followed by losses beginning in

Q2 2021.

– Lower-rated tranches of nonconforming transactions are more susceptible to ratings

downgrades.

5

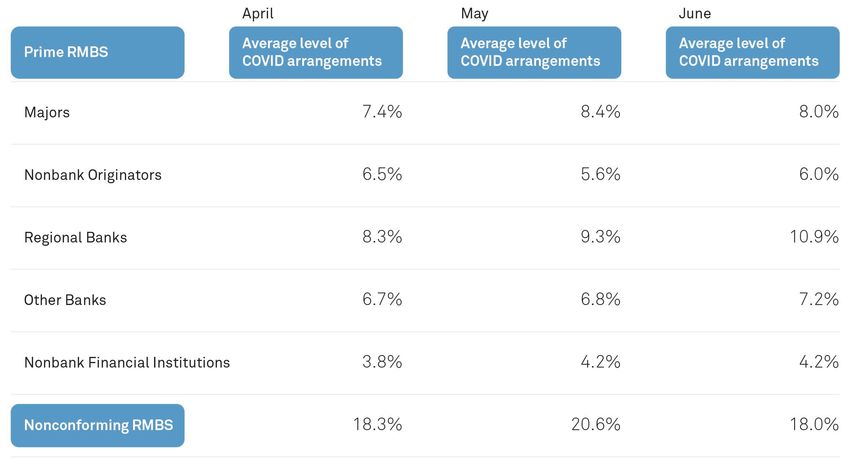

Australian RMBS COVID-19 Profiles What do COVID-19 support profiles reveal in the Australian RMBS sector?

COVID-19 Profiles: LTV Ratio Distribution

Prime LTV Distribution – COVID-19 does not materially discriminate

by loan-to-value (LTV) ratio LTV profile.

Total RMBS COVID-19 Hardship

hardship

– Loans with >80% LTV loan exposures make

50% up a greater proportion of loans under COVID

40% arrangements compared to the broader

30% RMBS universe.

20% – This trend is more pronounced in the

10% nonconforming sector.

0% – Half of the loans under COVID-19

and 70%> and 80%> and 90%> and >100% arrangements in the nonconforming sector

100%

COVID-19 Profiles: COVID Support Levels Across

RMBS Originator Types

Average level of Average level of Average level of – Borrowers who work in the airline, tourism,

COVID-19 arrangements COVID-19 arrangements COVID-19 arrangements

and hospitality sectors are more likely to be

under COVID-19 support arrangements.

– COVID-19 support levels are higher in the

nonconforming sector.

– Nonconforming sector has a higher exposure

to self-employed borrowers which comprise

around 50% of total loan exposures in trusts.

– COVID-19 support levels peaked in May-

June, according to anecdotal feedback from

originators.

– COVD-19 hardship levels started to taper

from July, except in Victoria, where

borrowers are less likely to exit COVID-19

hardship given the Stage 4 restrictions in

place.

Data are as of June. 30, 2020. % refers to average % at a trust level.

RMBS--Residential mortgage-backed securities. Source: S&P Global Ratings.

8

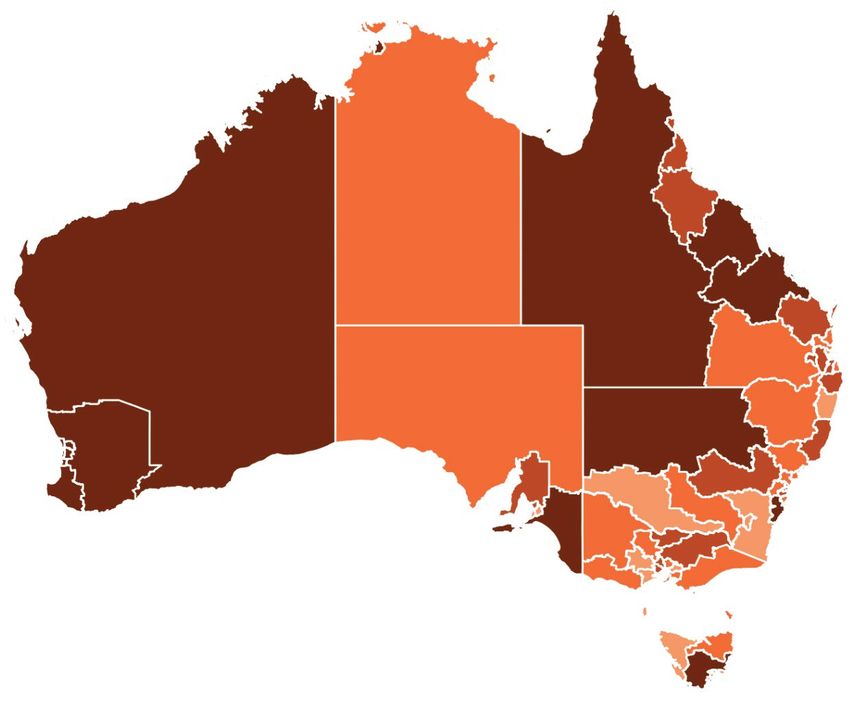

COVID-19 Exposure By State

COVID Hardship

COVID-19 hardship Total RMBS Sector

sector

Cairns

1% 1%

Gold Coast

Northern

Territory

24% 23%

Queensland Sunshine Coast

10% 10% Western

Australia

0% 10% 20%

4% 6% South

Australia

33% 32%

1% 2%

New South

Wales Australian

Capital

25% 25% Victoria Territory

1% 2% Tasmania

Data as at June. 30, 2020. %s shown for Cairns, Gold Coast and Sunshine Coast are expressed as a % of total loans in Queensland.

RMBS--Residential mortgage-backed securities. Source: S&P Global Ratings.

9

COVID-19 Hardship Hot Spots

Exposure Exposure Proportional

Area State total RMBS COVID-19 loans increase

Sydney - Inner

NSW 3.31% 4.37% 32% – Popular tourism locations and the outer

South West

suburbs of major capital cities have

Gold Coast QLD 3.13% 4.21% 35% disproportionally higher levels of COVID-19

Melbourne - South support arrangements.

VIC 2.50% 3.21% 28%

East – COVID-19 support levels are likely to remain

elevated in areas where it takes longer to

Melbourne - North

VIC 2.50% 3.25% 30% return to business as usual.

East

– Tourism-dependent areas affected by the

Sunshine Coast QLD 1.55% 1.88% 21% closure of international and state borders

Melbourne - North are likely to have larger employment losses .

VIC 1.30% 1.65% 27%

West – Victoria’s Stage 4 lockdown could result in an

Mornington increase in COVID-19 support levels in

VIC 1.27% 1.93% 52% August.

Peninsula

Sydney - Outer – Borrowers already under COVID-19 hardship

NSW 1.03% 1.25% 21% arrangements in Victoria are more likely to

South West

seek extensions to original mortgage deferral

Richmond - Tweed NSW 0.97% 1.33% 37% arrangement terms than in other parts of the

country.

Sydney - South

NSW 0.89% 1.31% 47%

West

Darwin NT 0.67% 0.93% 38%

Data as at June. 30, 2020. RMBS--Residential mortgage-backed securities. Source: S&P Global Ratings.

10COVID-19 Profile: Investors

Proportion Of Investor Vs. Owner-Occupier Loans

COVID-19 subset Total RMBS

– Investor loans are not disproportionately

80% represented in COVID-19 support RMBS loan

profiles.

70% – LTV ratio profiles of investor loans are

generally more elevated than owner-

60% occupier loans, given the greater prevalence

of interest-only periods that mean the loans

50% take longer to pay down.

– Rental income pressure is likely to be more

40% prevalent for investors, especially in inner-

city areas, and the movement of AirBNB

30% rentals into the longer-term residential

market.

20% – Exposure to CBD areas across the Australian

RMBS sector is limited at less than 2% of

10% total loan exposures.

0%

Investment Owner

Data as at June. 30, 2020. RMBS--Residential mortgage-backed securities.

Source: S&P Global Ratings.

11Australian RMBS Performance When are arrears likely to surface, given the insulation effect of mortgage payment deferrals?

COVID-19’s Effect On Prime Arrears

Unlikely To Be Visible Until At Least Q4

31-60 days 61-90 days 90+ days Standard variable rates (RHS)

1.8% 12%

1.6% Prime arrears peaked at 1.69%

after the 2008 financial crisis.

10%

1.4%

1.2% 8%

1.0%

6%

0.8%

0.6% 4%

0.4%

2%

0.2%

0.0% 0%

Source: Reserve Bank of Australia. S&P Global Ratings.

13Nonconforming Arrears Likely To Rise Earlier And

At A Faster Rate

31-60 days 61-90 days 90+ days Total current loan balance (RHS)

20% 12

Nonconforming arrears

10

peaked at 17.09% after the

2008 financial crisis.

15%

8

Bil. A$.

10% 6

4

5%

2

0% 0

Source: S&P Global Ratings.

14Mortgage Payment Deferral Levels

Aren’t An Indicator Of Future Arrears Performance

– Mortgage arrears are closely correlated with rises in unemployment because loss of

income is a key cause of mortgage default.

– COVID-19 arrangement levels provide some insight into debt-serviceability pressures but

are not an indicator of imminent mortgage default.

– Borrowers’ underlying credit quality is a driver of mortgage deferral utilization.

Operational considerations such as initial approaches to granting COVID-19 hardship

also play a part.

– Small bank (eg. Credit unions) and some nonbank lenders in the prime RMBS sector

generally have adopted a case-by-case approach to granting COVID-19 hardship, while

several larger bank lenders used a more automated deferral approach for the initial

assessment.

– The stage of economic recovery when support measures expire will affect the degree of

rises in mortgage arrears.

– COVID-19 levels for most publicly rated RMBS trust are available in the June pool

statistics.

15Prime Prepayment Rates Surprise On The Upside

Prime prepayment rate (Inc. Non-Capital Market Issuance)

– Prime prepayment rates including noncapital

Nonconforming prepayment rate

market issuance jumped to 30.2% in Q2 from

10-year long-term average prime prepayment rate 17.4% in Q1, mainly due to loan maintenance

Prime prepayment rate (Exc. Non-Capital Market Issuance) activity in bank internal self-securitization

programs.

40% – Prime prepayment rates excluding

noncapital market issuance rose to 20.8% in

35%

Q2 from 17.5% in Q1.

30% – Increases in prepayment rates (outside of

loan maintenance activity) reflect strong

25% refinancing activity in the first half of 2020.

20% – Nonconforming prepayment rates rose to

23.80% in Q2 from 22.03% in Q1.

15%

– We do not expect prepayment rates to

continue to increase at this rate. Most

10%

borrowers that were wanting and able to

refinance their loans have likely already done

5%

so.

0%

Data as at June. 30, 2020. Source: S&P Global Ratings.

16COVID-19’s Effect On Losses

Will Start To Emerge In Q2 2021

Property prices are likely to fall about 10% from the onset of the pandemic. Strong growth in property prices could return,

underpinned by increased demand when international borders reopen, low interest rates and potential supply shortages.

The modest LTV ratio profile of the Australian RMBS sector will help to minimize losses.

Cumulative Gross Loss By Vintage Of Cumulative Gross Loss By Vintage Of

Origination - Prime RMBS Origination - Nonconforming RMBS

0.09% 0.9%

0.08% 0.8%

0.07% 0.7%

0.06% 0.6%

0.05% 0.5%

0.04% 0.4%

0.03% 0.3%

0.02% 0.2%

0.01% 0.1%

0.00% 0.0%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

RMBS--Residential mortgage-backed securities. Source: S&P Global Ratings. RMBS--Residential mortgage-backed securities. Source: S&P Global Ratings.

17These timelines are based on current time periods related to existing wage subsidy programs. Further extensions to these programs could alter the timeframes when

arrears and foreclosure periods are expected to occur.

18These timelines are based on current time periods related to existing wage subsidy programs. Further extensions to these programs could alter the timeframes when

arrears and foreclosure periods are expected to occur.

19Arrears Performance Nationwide Arrears will vary by state in line with their different paths to economic recovery

Reporting Nuances Mask COVID-19’s

True Effect On Arrears

Australia Arrears are likely to increase nationwide in the months

ahead as rising unemployment flows through to debt

serviceability pressures for some borrowers.

Enormous fiscal stimulus measures are

helping many borrowers whose income has been hit

by COVID-19. This will support household income

and aid debt serviceability.

Mortgage payment deferrals are masking COVID-19’s

true effect on arrears. This is because most lenders are

not including loans under COVID-19 hardship

arrangements in their traditional arrears reporting

during mortgage-relief periods.

Mortgage arrears are likely to exhibit greater variability

during mortgage-relief periods. This is partly due to

operational nuances in the approaches lenders adopt in

their reporting of loans that were in arrears before being

granted COVID-19 hardship arrangements.

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Map boundaries are based on the ABS SA4 geographical classifications. Some areas on the map have been merged graphically. Source: S&P Global Ratings.

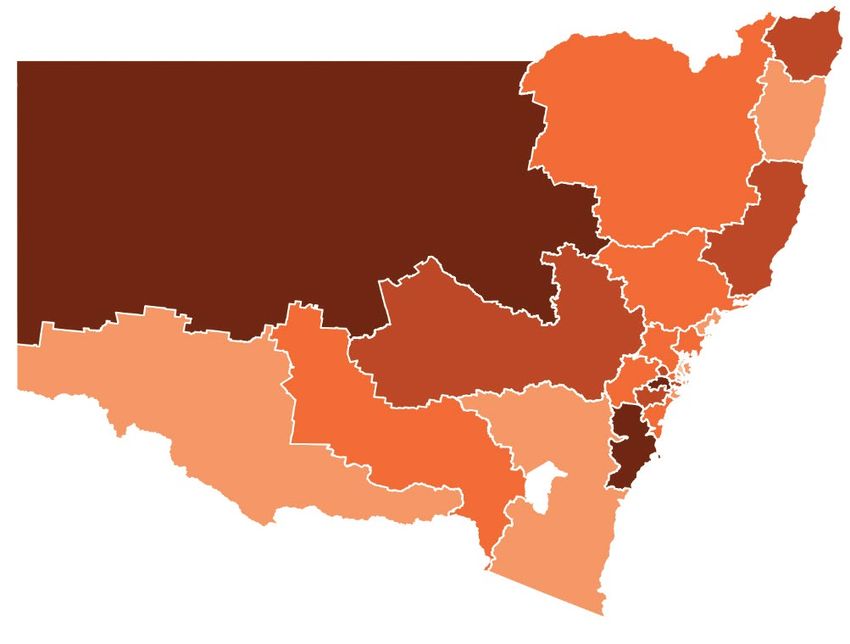

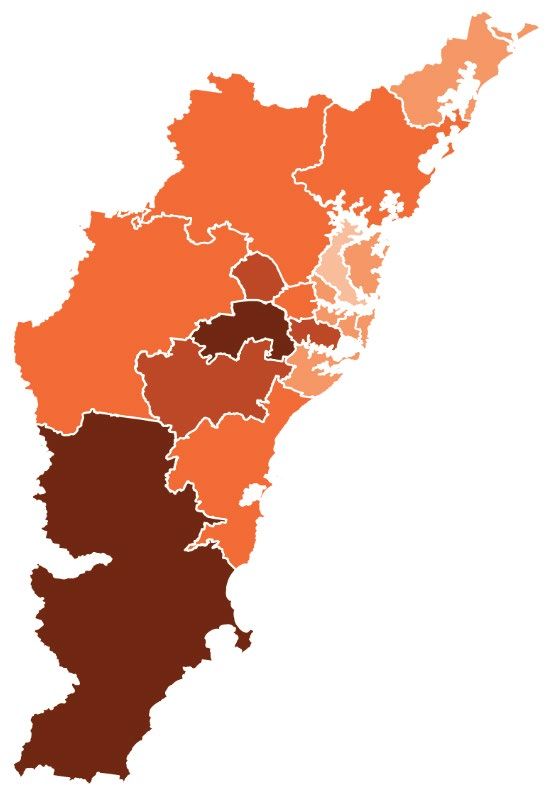

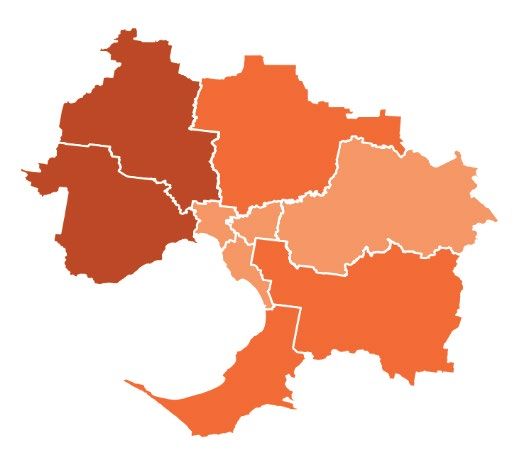

21New South Wales: Containing COVID-19’s Spread

And Keeping The Economy Open 111

212

115 102

110 104

121

105 116 122

125

127

108 119

106 124

123 128

103

107

109

113

114

101

NSW has managed to keep its economy largely open and

stay on top of localized virus clusters. Managing this will

be crucial in keeping the economy open, preserving jobs,

and restoring the state’s strong arrears track record.

Current 30+ Peak 30+ Unemployment Exposure

Days Arrears Days Arrears Rate Across RMBS

1.33% 2.69% 7.2% 32%

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Source: Australian Bureau of Statistics. S&P Global Ratings.

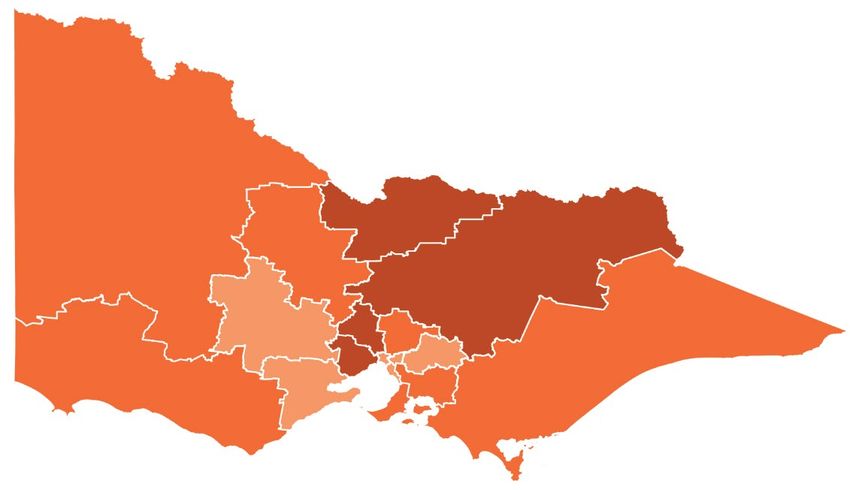

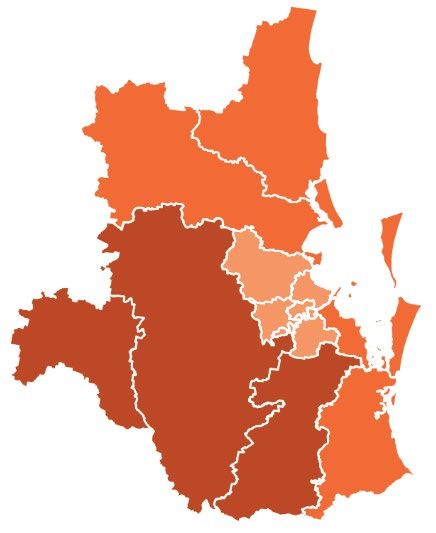

22Victoria: Lockdown 2.0 Puts The Brakes On

Economic Recovery

Victoria’s Stage 4 lockdown will impede its

path to economic recovery, affecting

employment, housing markets, and debt

serviceability. A more protracted lockdown is

likely to lead to higher job losses and a greater 215

effect on property prices than in other parts of

the country. We expect more borrowers from 216

Victoria to request extensions to existing 202

204

mortgage deferral arrangements than in other

states, given the dislocation in economic

activity is likely to persist for some time. 201

Victoria is likely to see the largest increase in 205

214

mortgage arrears above pre-COVID-19 levels.

Current 30+ Peak 30+ Unemployment Exposure 203

Days Arrears Days Arrears Rate Across RMBS

1.37% 1.86% 6.8% 25%

210

209

211

213

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

212

Source: Australian Bureau of Statistics. S&P Global Ratings. 214

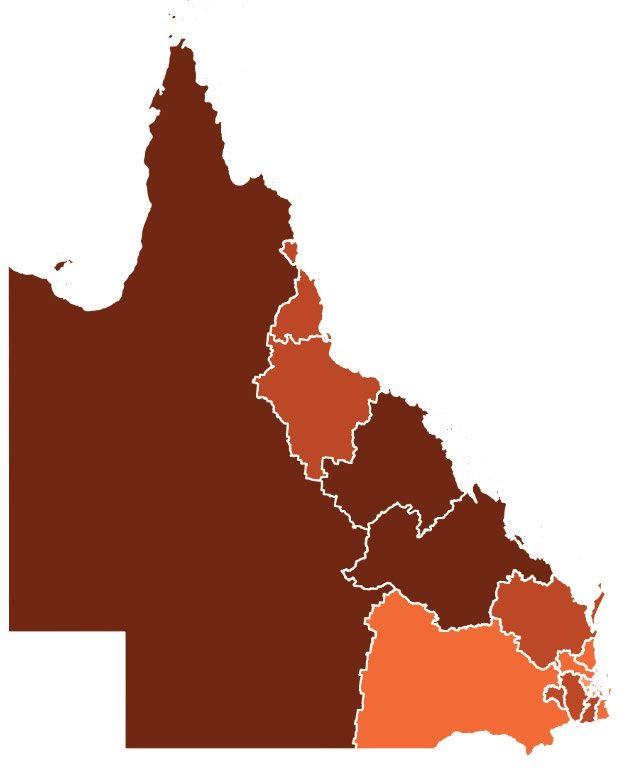

23Queensland: Tourism Hotspots Have A Higher

Share Of COVID-19 Hardship Levels

Arrears were already more elevated

in Queensland than other parts of

316

the country, reflecting its exposure

313 to mining and drought-affected

regions. With the COVID-19

pandemic, tourism hot spots are

306 struggling from the closure of

international and some state

317 310 borders. Tourist towns have a

318 disproportionate share of loans

under COVID-19 hardship

312 arrangements and will likely see

309 higher arrears in the months ahead.

315 311

308

319

307

Current 30+ Peak 30+ Unemployment Exposure

Days Arrears Days Arrears Rate Across RMBS

1.58% 2.17% 8.8% 23%

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Source: Australian Bureau of Statistics. S&P Global Ratings.

24Western Australia: Longer-Dated Arrears Weighing

On Arrears Performance

Western Australia has been home to the

nation’s highest arrears for a number of

years, reflecting borrowers’ increased

505 debt-serviceability pressures since the

end of the mining boom. COVID-19’s

economic effect is unlikely to be as

504

508 negative as other parts of the country,

given its good progress on containing

503 the virus and the strong demand for

iron ore. Longer-dated arrears

meanwhile will still weigh on overall

507 506 arrears performance. These loans are

unlikely to cure.

509

502

507

Current Peak 30+ Peak 30+ Unemployment Exposure

Days Arrears Days Arrears Rate Across RMBS

2.67% 3.10% 8.3% 10%

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Source: Australian Bureau of Statistics. S&P Global Ratings.

25South Australia: Unemployment Eased In July

As Economic Recovery Continues

South Australia’s unemployment rate fell to 7.9% in July from

a month earlier but remained above the national average of

7.5%. The state has made progress in containing COVID-19’s

spread and reopening its economy. This will help with debt

serviceability when fiscal stimulus measures expire.

406

Current 30+ Peak 30+ Unemployment Exposure

Days Arrears Days Arrears Rate Across RMBS

1.36% 1.81% 7.9% 6%

405

407

402

404

401

403

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Source: Australian Bureau of Statistics. S&P Global Ratings.

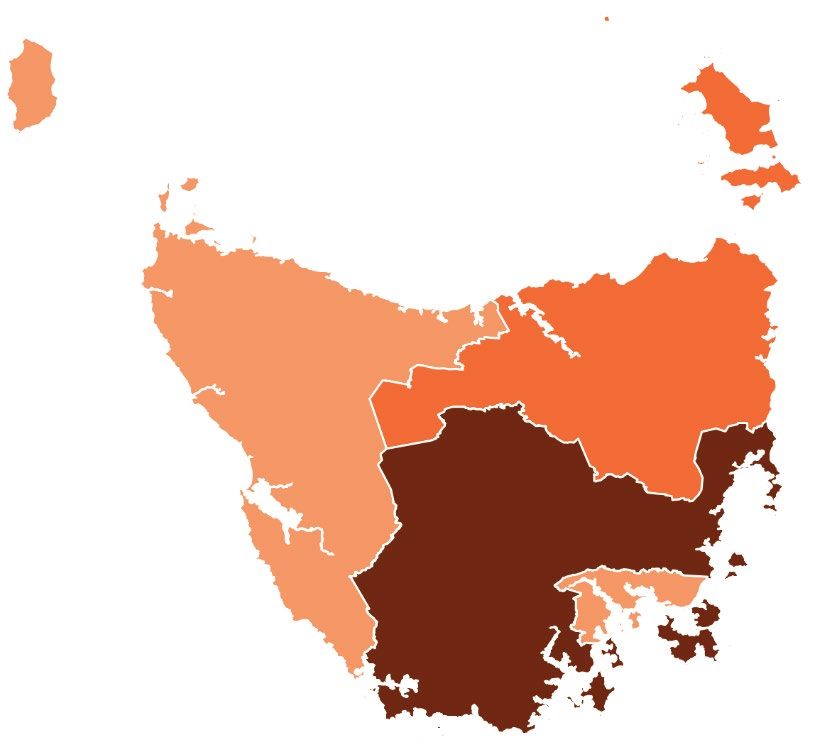

26Tasmania: Unemployment Rate Lower Than

Most Other Parts Of the Country

Tasmania in July recorded one of the largest declines in

unemployment rate from the previous month. Its

current unemployment rate of 6% was well below the

604 602 national average of 7.5%. Tasmania has also made

good progress in containing the spread of the virus and

reopening its economy. This is likely to lead to less

pronounced increases in arrears in the months ahead

as the return to business as usual is more progressed.

603

601

Current 30+ Peak 30+ Unemployment Exposure

Days Arrears Days Arrears Rate Across RMBS

1.10% 2.02% 6.0% 2.0%

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Source: Australian Bureau of Statistics. S&P Global Ratings.

27The Territories: Northern Territory’s Unemployment

Rate Will Put More Pressure On Arrears

701

Northern Territory has the most volatile arrears

performance due to small exposures in portfolios. Darwin

has a disproportionate share of COVID-19 hardship

arrangements, reflecting the border closure’s effect on

the tourism sector. Unemployment in the territory was

7.5% in July, up from 5.7% in June.

702

Current 30+ Peak 30+ Unemployment Exposure

Days Arrears Days Arrears Rate Across RMBS

2.73% 3.50% 7.5% 1.0%

Australian Capital Territory has the lowest arrears, at

0.99%, as of June 30, 2020. This reflects its stronger

employment profile and lower unemployment.

0%-0.74% 0.75%-1.24% 1.25%-1.74% 1.75%-2.24% +2.25%

Source: Australian Bureau of Statistics. S&P Global Ratings.

28SA4 Listing Arrears And Exposure

30+ days 30+ days 30+ days 30+ days

Geographic arrears arrears Exposure Geographic arrears arrears Exposure

area map level level across area map level level across

code Regional name State June 2020 June 2019 RMBS code Regional name State June 2020 June 2019 RMBS

101 Capital Region NSW 1.09% 1.56% 1.23% 124 Sydney - Outer West and Blue Mountains NSW 1.45% 1.16% 0.94%

102 Central Coast NSW 1.31% 1.42% 1.51% 125 Sydney - Parramatta NSW 1.33% 1.35% 2.15%

103 Central West NSW 1.79% 1.71% 0.48% 126 Sydney - Ryde NSW 0.89% 0.50% 0.49%

104 Coffs Harbour - Grafton NSW 1.15% 1.18% 0.36% 127 Sydney - South West NSW 2.33% 2.23% 0.88%

105 Far West and Orana NSW 2.26% 2.90% 0.18% 128 Sydney - Sutherland NSW 1.24% 1.55% 0.79%

106 Hunter Valley exc Newcastle NSW 1.47% 1.42% 1.41% 201 Ballarat VIC 1.16% 1.39% 0.66%

107 Illawarra NSW 1.41% 1.33% 1.71% 202 Bendigo VIC 1.49% 1.72% 0.34%

108 Mid North Coast NSW 1.81% 1.79% 0.44% 203 Geelong VIC 0.82% 1.14% 1.11%

109 Murray NSW 1.04% 1.58% 0.70% 204 Hume VIC 2.09% 2.22% 0.31%

110 New England and North West NSW 1.46% 2.36% 0.23% 205 Latrobe - Gippsland VIC 1.64% 1.75% 0.60%

111 Newcastle and Lake Macquarie NSW 0.84% 0.98% 1.66% 206 Melbourne - Inner VIC 1.10% 0.94% 4.23%

112 Richmond - Tweed NSW 2.06% 1.90% 1.02% 207 Melbourne - Inner East VIC 1.22% 1.10% 1.73%

113 Riverina NSW 1.40% 1.48% 0.11% 208 Melbourne - Inner South VIC 0.95% 1.04% 2.16%

114 Southern Highlands and Shoalhaven NSW 2.52% 1.03% 0.26% 209 Melbourne - North East VIC 1.56% 1.78% 2.50%

115 Sydney - Baulkham Hills and Hawkesbury NSW 1.30% 1.29% 1.91% 210 Melbourne - North West VIC 2.09% 1.82% 1.29%

116 Sydney - Blacktown NSW 1.78% 1.54% 2.45% 211 Melbourne - Outer East VIC 1.04% 1.09% 2.43%

117 Sydney - City and Inner South NSW 0.82% 0.81% 2.92% 212 Melbourne - South East VIC 1.61% 1.77% 2.49%

118 Sydney - Eastern Suburbs NSW 0.85% 0.78% 0.87% 213 Melbourne - West VIC 1.80% 1.61% 2.63%

119 Sydney - Inner South West NSW 1.85% 1.76% 3.30% 214 Mornington Peninsula VIC 1.54% 1.76% 1.26%

120 Sydney - Inner West NSW 0.85% 0.63% 1.28% 215 North West VIC 1.29% 1.49% 0.12%

121 Sydney - North Sydney and Hornsby NSW 0.63% 0.61% 2.29% 216 Shepparton VIC 1.95% 2.22% 0.12%

122 Sydney - Northern Beaches NSW 0.87% 0.65% 1.48% 217 Warrnambool and South West VIC 1.50% 1.63% 0.22%

123 Sydney - Outer South West NSW 2.03% 1.31% 1.02% 301 Brisbane - East QLD 1.31% 1.38% 1.50%

29SA4 Listing Arrears And Exposure

30+ days 30+ days 30+ days 30+ days

Geographic arrears arrears Exposure Geographic arrears arrears Exposure

area map level level across area map level level across

code Regional name State June 2020 June 2019 RMBS code Regional name State June 2020 June 2019 RMBS

302 Brisbane - North QLD 1.03% 1.02% 2.06% 405 Barossa - Yorke - Mid North SA 2.04% 2.91% 0.16%

303 Brisbane - South QLD 1.13% 1.34% 2.86% 406 South Australia - Outback SA 1.38% 2.14% 0.13%

304 Brisbane - West QLD 1.00% 0.98% 1.32% 407 South Australia - South East SA 2.25% 1.80% 0.31%

305 Brisbane Inner City QLD 1.10% 1.06% 0.96% 501 Bunbury WA 2.66% 3.26% 0.46%

306 Cairns QLD 2.24% 2.09% 0.89% 502 Mandurah WA 3.65% 4.20% 0.32%

307 Darling Downs - Maranoa QLD 1.58% 2.28% 1.00% 503 Perth - Inner WA 1.28% 1.65% 1.04%

308 Fitzroy (Central Queensland) QLD 3.32% 3.77% 1.00% 504 Perth - North East WA 2.83% 2.97% 1.36%

309 Gold Coast QLD 1.40% 1.53% 3.14% 505 Perth - North West WA 2.74% 3.24% 2.09%

310 Ipswich QLD 2.04% 2.57% 1.24% 506 Perth - South East WA 2.87% 3.04% 2.16%

311 Logan - Beaudesert QLD 1.92% 2.78% 0.54% 507 Perth - South West WA 2.37% 2.74% 1.57%

312 Mackay QLD 2.60% 3.63% 0.80% 508 Western Australia - Outback WA 3.93% 5.18% 0.42%

313 Moreton Bay - North QLD 1.38% 2.14% 1.28% 509 Western Australia - Wheat Belt WA 4.08% 4.19% 0.18%

314 Moreton Bay - South QLD 0.96% 1.14% 0.64% 601 Hobart TAS 1.03% 1.16% 0.85%

315 Queensland - Outback QLD 3.39% 4.99% 0.17% 602 Launceston and North East TAS 1.26% 1.42% 0.35%

316 Sunshine Coast QLD 1.47% 1.65% 1.57% 603 South East TAS 2.66% 2.76% 0.03%

317 Toowoomba QLD 2.19% 3.29% 0.01% 604 West and North West TAS 0.94% 1.28% 0.23%

318 Townsville QLD 2.22% 3.18% 1.11% 701 Darwin NT 2.91% 3.05% 0.67%

319 Wide Bay QLD 2.11% 2.45% 0.62% 702 Northern Territory - Outback NT 1.64% 1.73% 0.09%

401 Adelaide - Central and Hills SA 1.09% 1.17% 1.43% 703 Northern Territory - Outback NT 0.00% 0.00% 0.00%

402 Adelaide - North SA 1.81% 1.99% 1.25% 704 Northern Territory - Outback NT 0.00% 0.00% 0.00%

403 Adelaide - South SA 1.11% 1.38% 1.33% 705 Northern Territory - Outback NT 0.00% 0.00% 0.00%

404 Adelaide - West SA 1.07% 1.05% 0.78%

30The 10 Worst-Performing Postcodes

State Suburb Postcode Loans in arrears Loan count

WA Byford 6122 6.28% 430

VIC Greenvale 3059 5.94% 390

WA Maddington 6109 5.92% 273

NT Darwin 800 5.36% 266

WA Blythewood 6208 5.34% 258

NSW Chester Hill 2162 4.91% 327

WA Cooloongup 6168 4.83% 583

WA Butler 6036 4.82% 371

WA Cloverdale 6105 4.69% 427

VIC South Melbourne 3205 4.68% 330

Source: S&P Global Ratings. Data as of June 30, 2020. For a full list of suburbs/localities attached to these postcodes, please refer to the Australia Post website.

31New Zealand

S&P Global Ratings Economic Outlook

2020f 2021f Outlook Impact on credit quality

Real GDP (5.0) 6.0 The country has outperformed nearly Negative. Reduced economic growth

growth (% year all others in containing COVID-19. The will likely add debt-serviceability

over year) lockdowns hurt economic activity in pressure for self-employed borrowers,

the June quarter, but the economy whose cash flows are more sensitive

should recover in the next few years. to deteriorating economic conditions.

Unemployment 5.8 5.6 We forecast unemployment to peak in Negative. Rising unemployment will

rate (year June, and economic activity and put pressure on certain cohorts,

average; %) employment to rebound in 2021. Job- including self-employed and highly

retention measures have helped to leveraged borrowers.

reduce the level of job losses.

CPI (%) 1.7 1.8 Wage growth is likely to remain Negative. Weak wage growth is likely

subdued in the wake of COVID-19. to persist for some time.

Policy rates, end 0.25 0.25 Official cash rate is set to remain low Positive. Lower rates will support debt

of year (%) for some time. serviceability for borrowers with

variable-rate mortgages.

f--Forecast.CPI --Consumer price index. Source: S&P Global Ratings.

33New Zealand’s Response To COVID-19 Has Helped

The Economy To Reopen Faster Than Others

– The COVID-19 pandemic and restrictions to contain it led to a sharp contraction in

economic activity in the June quarter of 2020. The emergence from lockdown resulted in

a rebound in economic activity in May and June.

– Many workers affected by the COVID-19 outbreak and containment measures have

mortgage deferral schemes and access to wage subsidies and superannuation balances

to compensate for lost income.

– Mortgage deferral schemes have been extended to March 2021. The regulatory guidance

means banks can continue to offer temporary mortgage deferrals to their customers

during mortgage relief periods without those loans being viewed as being in default,

– Lower interest rates are supporting house price recovery more so than business

investment at this stage.

– Auckland was placed under Stage 3 restrictions on August 11 after the detection of the

country’s first locally acquired case of COVID-19 in three months. Auckland is scheduled

to return to Stage 2 restrictions, as per the rest of the country, from August 31st.

34New Zealand RMBS Sector Performance

Remains Stable

– The credit quality of the New Zealand RMBS sector is strong, as evidenced by:

– Weighted-average LTV ratio of 60%.

– Average loan size of NZ$191,985.

– Weighted-average seasoning of 55 months.

– Low levels of arrears in most portfolios, though we expect arrears to rise

because of a forecast increase in unemployment.

– All losses to date have been fully covered by lenders’ mortgage insurance.

– A number of pools are now “small pools,” which have greater borrower

concentration risk.

RMBS--Residential mortgage-backed securities. LTV--Loan to value ratio.

35How To Access RMBS Performance Watch

RMBS Performance Watch including arrears, prepayment, and pool statistics data

can be accessed using the link below:

CLICK HERE

Asia-Pacific

Structured Finance

Surveillance

36RMBS Analytical Contacts

Kate Thomson

Analytical Manager | kate.thomson@spglobal.com

Narelle Coneybeare

Sector Lead | narelle.coneybeare@spglobal.com

Erin Kitson

Sector Specialist Research | erin.kitson@spglobal.com

Elizabeth Steenson

Lead Analyst | elizabeth.steenson@spglobal.com

Alisha Treacy

Lead Analyst | alisha.treacy@spglobal.com

37Under S&P Global Ratings’ policies, only a Rating Committee can determine a Credit Rating Action (including a Credit Rating change, affirmation or withdrawal, Rating Outlook change, or CreditWatch action).

This commentary and its subject matter have not been the subject of a Rating Committee action and should not be interpreted as a change to, or affirmation of, a Credit Rating or Rating Outlook.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered,

reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively,

S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P

Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for

the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR

DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable

to

any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits

and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions, analyses and rating

acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P

assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its

management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P

has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw

or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any

liability for any damage alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have

information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each

analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's

public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and may be distributed through other means, including via S&P

publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

Permissions: To reprint, translate, or quote S&P Global Ratings’ publications, contact: Client Services, 120 Collins Street, Melbourne, Vic 3000 Australia, (61) 1300-792-553.

This report and the ratings contained within it are based on published information as of July 31, 2017. Subsequent information may result in the assignment of ratings that differ from the ratings published here.

Please call Standard & Poor’s Client Services at (61) 1300-792-553 for the most recent rating assigned.

For Australian Users — S&P Global Ratings Australia Pty Ltd. holds Australian financial services licence number 337565 under the Corporations Act 2001. S&P Global Ratings’ credit ratings and related research

are not intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).

S&P Global Ratings 17g-7 Disclosure Report SEC Rule 17g-7 requires an NRSRO, for any report accompanying a credit rating relating to an asset-backed security as defined in the Rule, to include a description

of the representations, warranties and enforcement mechanisms available to investors and a description of how they differ from the representations, warranties and enforcement mechanisms in issuances of

similar securities. The Rule applies to in-scope securities initially rated (including preliminary ratings) on or after Sept. 26, 2011.

Copyright © 2020 by Standard & Poor’s Financial Services LLC. All rights reserved.

STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.

Reproduction in whole or in part prohibited except by permission.

38You can also read