Running the numbers on your next big move - Alternative grad gifts - Charles Schwab

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Alternative grad gifts The other Roth The inflation effect

Page 5 Page 8 Page 30

I NSIGHTS FOR C LI ENTS I NVESTED I N T H E I R F I NANC IAL F UTUR ES | SUM M E R 2021

Running the

numbers on your

next big move

Page 24

Dear Client,

The pandemic has prompted a record number of Americans to upsize, downsize, or otherwise

relocate—and millions more could follow suit this year, especially if the trend toward working

remotely continues. If you’re contemplating a move—whether across town or between states—be

sure to avoid the four common financial mistakes outlined on page 24.

Elsewhere in this issue you’ll find a breakdown of the financial implications of owning an RV (page

13), a status report on the post-pandemic municipal bond market (page 18), tips for responding to

inflation concerns (page 30), and much more.

If you have questions about how these topics apply to your own finances, I encourage you to reach

out to us at 877-297-1126. We welcome every opportunity to help you achieve your goals.

Sincerely,

Joseph Vietri

Senior Vice President, Investor Services

See page 42 for important information. (0621-1XZZ)

Summer 2021 CONTENTS

5 15 24 28

D E PA R T M E N T S F E AT U R E S

2 NEWSLETTER NEWS 13 ASK CARRIE 24 Migration Nation

Schwab Investing Insights is The ins and outs of RV Four common moving mistakes

getting a whole new look. ownership. to avoid.

By Carrie Schwab-Pomerantz

3 CEO’s NOTE 28 Impulse Control

Thank you for standing with us. PERSPECTIVES How to curb the self-defeating

By Walt Bettinger 15 Could you weather an earlier- behaviors that can get in the

than-expected retirement? way of your goals.

By Rob Williams

THE BOTTOM LINE

5 Graduation gifts that last. 18 How municipal bonds stayed 30 The Inflation Effect

strong. Why an uptick in prices could

6 Understanding the “kiddie tax.” By Cooper Howard be good for investors.

7 What to do with a delisted

stock. 21 TRADING 34 Orchestrating Your Estate

Behavioral biases that can cloud Using estate planning

8 Three reasons to consider a your trading decisions. instruments to create a more

Roth 401(k). By Randy Frederick harmonious life and legacy.

9 Beware the framing effect.

Onward (ISSN 2330-3514) is published quarterly.

38 SPOTLIGHT

This publication is mailed at Standard A postal

Wasmer Schroeder™ rates. ◆ If you prefer not to receive Onward,

11 FAMILY MATTERS Strategies; Schwab Assistant; please call 877-908-0065. ◆ POSTMASTER:

How to pass on a family home. Strategic borrowing from Send address changes to Onward, Charles

Schwab & Co., Inc., P.O. Box 982600, El Paso,

Schwab and Schwab Bank. TX, 79998-2600. Onward does not assume any

liability resulting from actions taken based on the

information included in this magazine. Mention

of a company or security does not constitute

44 ON YOUR SIDE

endorsement. Some contributors to Onward may

Staying the course. have active positions in securities or companies

By Charles R. Schwab discussed in this issue. MAG105674Q221-00

O N T H E C O V E R : I L L U S T R AT I O N B Y D AV I D M O O R E SUMMER 2021 | O N WA R D | 1

Newsletter News

Schwab Investing

Insights is getting a

whole new look.

Schwab Investing Insights,

Schwab’s monthly email

newsletter, is relaunching this

summer.

Why it’s happening

The new Schwab Investing Insights

will deliver more in-depth news

and commentary tailored to your needs,

interests, and goals—with a user-friendly

new look.

What you can do

Log in to your account at schwab.com

to confirm the email address we have on

file for you.

Look for the revamped Schwab

Investing Insights in your email inbox

this summer.

2 | C H A R L E S S C H WA B | SUMMER 2021

CEO’s NOTE

Thank You

t’s difficult to reckon with the It’s hard to look at the painfully

I magnitude of the COVID-19 lonely deaths, the missed moments

pandemic: millions of cases, hundreds with family members and friends, and

Clients like you made our of thousands of deaths, tens of millions the many shuttered businesses and see

pandemic response possible. of job losses, hundreds of millions of a silver lining. Perhaps the best we can

vaccine doses, trillions of dollars of do is take heart that the worst appears

federal relief. Yet even these unfath- to be behind us and look forward to

omable numbers fail to adequately the future.

capture the challenges we’ve all faced. As our country and the world

continue to reopen and life returns

We all have an to something resembling normal, we

opportunity to all have an opportunity to take a fresh

take a fresh look look at our priorities and decide anew

what’s most important to us.

at our priorities For me, it is a sense of gratitude for

and decide anew my family, friends, and colleagues—

what’s most and a deep appreciation for all the

important to us. clients who stood with us as we

endeavored to deliver our historically

award-winning service in the face

of unprecedented volume and our

employees working from home.

I have no profound words to share,

nothing to ask of you. I simply want

to say, from the bottom of my heart:

Thank you.

Sincerely,

Walt Bettinger

President & CEO

See page 42

for important

information.

(0621-16H7)

SUMMER 2021 | O N WA R D | 3

It’s good to be back. Schwab branches have reopened with new lobby protocols and sanitation measures, social distancing markings, and contactless service options. Go to schwab.com/reopening to learn about how we’re keeping visitors and employees safe, what to expect when you visit a branch, and more. (0621-18XW)

CONTENTS GRADUATION GIF TS | KIDDIE TAX | STOCK DELISTINGS | ROTH 401(k)s | AND MORE

Next-Level Grad Gifts

in retirement could be tax-free,”1 says

Presents with the potential to keep on giving. Chris Kawashima, CFP®, a senior

research analyst at the Schwab Center

ith graduation season upon us, you might consider these gift alterna- for Financial Research.

W you may be thinking of reward- tives that have the potential to last.” Note that your contribution toward

ing your new grad with a fancy keep- a Roth IRA will be limited to your grad’s

I L LU S T R AT I O N B Y C H I A R A G H I G L I A Z Z A

sake or even a check—but why not 1 Help establish a Roth IRA: A jump- total earned income or the annual max-

consider something more purposeful? start on retirement savings can help imum ($6,000 in 2021 for individuals

“Cash, gift cards, or personal items pave the way for financial well-being younger than 50)—whichever is less.

are certainly fine gifts,” says Susan down the road. “A Roth IRA, in partic-

Bober, a Schwab wealth strategist based ular, is a great way to go because the 2 Help them buy stock: Introducing

in Indianapolis, “but if you really want money can grow tax-deferred during young people to the inner workings of

to help your grad get off to a good start, their working years, and withdrawals the stock market is a lesson in financial

SUMMER 2021 | O N WA R D | 5

T H E B OT TO M L I N E See page 42 for important information. ◆

Schwab Stock Slices is not intended to be

investment advice or a recommendation of

literacy. “Helping them invest a cash you might match their student loan any stock. Investing in stocks can be volatile

and involves risk, including loss of principal.

gift allows you to teach them import- payments for a specified period. “That Consider your individual circumstances

ant concepts, such as research, diversi- way, they’re still on the hook for prac- prior to investing. ◆ The S&P 500® Index is a

fication, and rebalancing to maintain ticing good money habits like paying product of S&P Dow Jones Indices LLC or its

affiliates (“SPDJI”), and has been licensed for

their ideal asset allocation,” Susan says. their bills on time,” Susan says. use by Charles Schwab & Co., Inc. (“CS&Co.”).

Standard & Poor’s® and S&P® are registered

trademarks of Standard & Poor’s Financial

3 Lighten their student loan load: Monetary gifts aside, one of the best

Services LLC (“S&P”); Dow Jones® is a

Federal loan forgiveness measures may things you can give a new grad is the registered trademark of Dow Jones Trademark

be on the horizon, but for now the benefit of insight. “Imparting some Holdings LLC (“Dow Jones”). Schwab Stock

Slices is not sponsored, endorsed, sold,

average student loan debt is $37,693, of your own hard-earned wisdom— or promoted by SPDJI, Dow Jones, S&P, or

NEXT according to Educationdata.org. Instead including your mistakes—can help their respective affiliates, and none of such

STEPS of contributing a lump sum, however, them make smarter financial decisions parties make any representation regarding

the advisability of using Schwab Stock

in their own lives,” Chris says. Slices or investing in any security available

With Schwab Stock Slices™, your new grad can through Schwab Stock Slices, nor do they

buy a fractional share of any company in the have any liability for any errors, omissions,

1

To qualify for tax-free withdrawals of earnings, or interruptions of the S&P 500 Index. ◆

S&P 500® Index for as little as $5. Learn more at account holder must be 59½ or older and have Investing involves risk, including loss of

schwab.com/stockslices. owned the account for at least five years. principal. (0621-1UNR)

Understanding

the Kiddie Tax

What to know if your child has unearned income.

D

o your children have income- of the tax year (or full-time students Refund, anyone?

generating assets in a custodial younger than 24) and works like this: If your family paid the kiddie

account? If so, be sure you understand tax in 2018 or 2019, you could be

the so-called kiddie tax. The first $1,100 of unearned eligible for a refund.

This law was passed to discourage income is covered by the kiddie

wealthier individuals from trans- tax’s standard deduction, so it isn’t The Tax Cuts and Jobs Act of 2017

ferring assets to their children to taxed. effectively raised the kiddie tax by

basing it on the tax rates used for

take advantage of their lower tax The next $1,100 is taxed at the

estates and trusts, instead of the

rates. The kiddie tax has seen many child’s marginal tax rate. rates used for parents. That change

iterations (see “Refund, anyone?” at Anything above $2,200 is taxed at has since been repealed, so if you

right), but current rules tax a minor the parents’ marginal tax rate. calculated your child’s liability using

child’s unearned income—including estate and trust tax rates in 2018 or

capital gains distributions, dividends, If your child also has earned income, 2019, you have the option to file an

and interest income—at the parents’ say from a summer job, the rules amended return using your tax rate

for your child’s unearned income

tax rate if it exceeds the annual limit become more complicated. To learn

instead. Just be sure the potential

($2,200 in 2021). more, see IRS Publication 929 (irs.gov/ refund is worth the additional

The tax applies to dependent pub/irs-pdf/p929.pdf ) or consult a tax paperwork and any associated

children under the age of 18 at the end advisor. preparation costs.

See page 42 for important information. ◆ This information does not constitute and is not

NEXT intended to be a substitute for specific individualized tax, legal, or investment planning advice.

STEPS Find more tax planning insights at Where specific advice is necessary or appropriate, Schwab recommends consultation with a

schwab.com/taxes. qualified tax advisor, CPA, financial planner, or investment manager. (0621-17PS)

6 | C H A R L E S S C H WA B | SUMMER 2021

Making the

1 The company fails to meet listing 3 The company files for bankruptcy:

requirements: You generally have a Bankruptcy commonly wipes out a

Delist

few options: company’s original shares, and usually

shareholders aren’t entitled to newly

n Hold and trade the shares via a issued stock as a replacement if the

What to do if a stock dealer network—also known as over- company emerges from bankruptcy.

you own is delisted from the-counter trading (OTC)—rather “You could see some cash from the

a U.S. exchange. than on a centralized exchange. That liquidation of the company once

said, “Be aware that failing to meet creditors, bondholders, and preferred

minimum listing requirements may shareholders are paid out, but it’s likely

stock can be delisted—or indicate a company is struggling, so to be only cents on the dollar,” Randy

A removed from a major stock reassess your reasons for holding the says. “A better approach is to keep close

exchange—for a variety of reasons, shares before going the OTC route,” tabs on your holdings so you aren’t

including for failing to meet says Randy Frederick, vice president blindsided.”

market-capitalization or share-price of trading and derivatives at the

minimums. However, the issue Schwab Center for Financial Research. Investing in stocks via an exchange-

made headlines late last year when n If you’re holding delisted American traded fund or mutual fund can help

the Holding Foreign Companies depositary receipts or American mitigate these and other risks by

Accountable Act (HFCAA) required depositary shares—which represent spreading your investment dollars

foreign companies to submit their foreign ordinary shares (ORDs) owned across dozens or even hundreds of

financial audits to U.S. regulators—or by a sponsoring bank—you could companies. “Plus, it’s the fund man-

face being delisted.1 either sell them back to the bank or ask ager’s job to stay on top of important

The law puts investors in the more the bank to convert the shares to ORDs, developments—including potential

than 200 U.S.-listed Chinese companies likely for a fee. ORDs can then be traded delistings,” Randy says.

in a particularly precarious position on a foreign exchange (if available) or

1

As things stand now, securities regulators

because the Chinese government OTC through your brokerage. could bar trading in a company’s stock—

doesn’t allow outside oversight into n Sell your shares before the stock including trading over the counter—if the

company fails to provide the required

its auditing processes. is delisted. (This is your only option documents for three consecutive years.

So, what happens when a stock you if your shares are being delisted as a

own is in danger of being delisted— result of the HFCAA.)

I L LU S T R AT I O N S B Y C H I A R A G H I G L I A Z Z A

and what can you do in response? That

depends on the reason for the delisting. 2 The company is acquired or goes See page 42 for important information.

LEARN private: Shareholders typically vote ◆ Investors should consider carefully

MORE information contained in the prospectus

on the terms of the sale or buyout, and or, if available, the summary prospectus,

generally can exchange their shares including investment objectives, risks,

To screen for funds using a variety of criteria, log for cash in the case of a private sale, or charges, and expenses. Please read it

carefully before investing. ◆ Investing

in to the ETF screener (schwab.com/ETFscreener) or for cash and/or shares in the acquiring involves risk, including loss of principal.

mutual fund screener (schwab.com/fundscreener). company in the event of an acquisition. (0621-17GP)

SUMMER 2021 | O N WA R D | 7

T H E B OT TO M L I N E

The Other Roth

trigger a big tax bill,” Hayden says.

“Saving in a Roth 401(k) could be a

better way to go if the taxes on a Roth

Three reasons you might want to consider a Roth 401(k). IRA conversion are prohibitive.”

n Higher contribution limits: In 2021,

ccording to the Plan Sponsor of tax and financial planning at you can stash away up to $19,500 in a

A Council of America, two-thirds the Schwab Center for Financial Roth 401(k)—$26,000 if you’re age 50

of employers now offer Roth 401(k)s as Research. “However, Roth 401(k)s offer or older.2 Roth IRA contributions, by

part of their retirement plans. If your additional benefits that should not be comparison, are capped at $6,000—

employer is among them, you may be overlooked.” Chief among them: $7,000 if you’re 50 or older.

wondering how a Roth 401(k) differs

from a Roth IRA. n No income limits: Anyone can n Matching contributions: Roth

“Both Roth IRAs and Roth contribute to a Roth 401(k), if avail 401(k)s are eligible for matching

401(k)s are funded with after-tax able, regardless of income level. In contributions from your employer,

dollars—meaning there’s no upfront contrast, only individuals earning less if offered. That said, your employer’s

tax benefit for contributing—but than $140,000 in 2021—$208,000 matching contributions are pretax

once you get to retirement, you for married couples—can contribute and will be placed in a regular, tax-

can withdraw the contributions to a Roth IRA. “Higher earners often deferred 401(k) account, which means

and earnings totally tax-free,”1 says access Roth IRAs by converting their you’ll be taxed once you start taking

Hayden Adams, CPA, CFP®, director traditional IRAs, but doing so can distributions.

One disadvantage in choosing a

Roth 401(k) is that you’ll have to take

IRS-mandated required minimum

distributions (RMDs) starting at

age 72. To avoid these mandatory

distributions and keep your money

invested, once you leave your job you

can roll over your Roth 401(k) into

a Roth IRA, which is not subject to

RMDs.3 Another drawback is that you’ll

be limited to the investments offered

by your company’s plan instead of the

variety available with a Roth IRA from

a brokerage. Investment fees may also

be higher.

“Nevertheless, Roth 401(k)s can

still be a great tool—especially for

high-wage earners and/or those who

anticipate higher taxes in retirement,”

Hayden says.

1

Account holder must be 59½ or older and

have owned the account for at least five years.

| 2You may choose to split your contributions

between Roth and traditional 401(k)s, but your

combined contributions can’t exceed $19,500

($26,000 if you’re age 50 or older). | 3Be aware

that the five-year rule applies to the length of

time the Roth IRA has been open, regardless of

how long the Roth 401(k) was open.

For additional tax planning insights, visit See page 42 for important information. ◆ This information does not constitute and is not

LEARN intended to be a substitute for specific individualized tax, legal, or investment planning advice.

MORE schwab.com/taxes. Where specific advice is necessary or appropriate, Schwab recommends consultation with a

qualified tax advisor, CPA, financial planner, or investment manager. (0621-1P3L)

8 | C H A R L E S S C H WA B | SUMMER 2021See for

Yourself

How the framing effect

can skew your investing

decisions.

he way information is

T presented can influence our

decision-making—sometimes to our

detriment—thanks to a cognitive tic

psychologists call the framing effect.

“Research has repeatedly shown

that whether an investment’s perfor

mance is framed as a gain or a loss

can push investors to buy or sell—

irrespective of its objective merits,”

says Mark Riepe, head of the Schwab

Center for Financial Research.

One way to counter the framing

effect is to use appropriate bench

marks. “For example, investors often

judge assets by comparing their

performance to that of a broad market

index,” Mark says. “But using a broad

market index won’t tell you how an Some investors might call that a loser. overweight? Or will it complement

asset performs relative to its peers Others might see a winner. Both could the finely tuned asset allocation you’ve

or within its sector—a stock that has be right depending on their time assembled?

outperformed the S&P 500® Index may horizon. “Ultimately you want to focus

still be a laggard within its industry, A better approach is to ask whether on what really matters—and that’s

for instance—nor does it speak to the the stock’s current market price whether an investment is a good fit

riskiness of the asset.” accurately reflects the company’s for your long-term goals,” Mark says.

Another strategy is to get back to earnings, growth potential, riskiness, “If you’re not sure, a financial advisor

basics. Say you’re interested in buying and other fundamentals. Then look for can help you zoom out and make clear-

I L LU S T R AT I O N S B Y C H I A R A G H I G L I A Z Z A

a stock that’s down 20% year to date counterarguments that might cause headed decisions.”

NEXT but has recently enjoyed a strong run. you to reconsider your conclusions,

STEPS such as news that could alter the

company’s growth trajectory. See page 42 for important information. ◆

Listen and subscribe to Financial Decoder™, in Finally, it helps to judge every Each investor needs to review an investment

which host Mark Riepe explores the emotional potential investment in the context strategy for his or her own particular

situation before making any investment

biases that can cloud your financial judgment and of your other holdings. Will it add to decision. ◆ Investing involves risk, including

cost you money, at schwab.com/financialdecoder. areas of your portfolio that are already loss of principal. (0621-1UPM)

SUMMER 2021 | O N WA R D | 9Enjoy exclusive discounts and

low interest rates with Schwab Bank.

0.250% 0.500% 0.750%

interest rate discount interest rate discount interest rate discount

$250K - $999K $1M - $4.9M $5M+

in qualifying assets1 in qualifying assets1 in qualifying assets1

The more qualifying assets you have with Schwab and

Schwab Bank, the more you may save on home loans.1

Call Quicken Loans at 877-524-2932 or visit schwab.com/mortgages to get started.

Brokerage Products: Not FDIC Insured • No Bank Guarantee • May Lose Value

In order to participate, the borrower must agree that the lender, Quicken Loans, may share their information with Charles Schwab Bank, and Charles Schwab Bank

will share their information with the lender, Quicken Loans. Nothing herein is or should be interpreted as an obligation to lend. Loans are subject to credit and collateral

approval. Other conditions and restrictions may apply. This offer is subject to change or withdrawal at any time and without notice. Interest rate discounts cannot be

combined with any other offers or rate discounts. Hazard insurance may be required.

1. Investor Advantage Pricing (IAP): Loans are eligible for only one IAP discount per loan. Select mortgage loans are eligible for an interest rate discount of 0.250%

- 0.750% based on qualifying assets of $250,000 or greater. Discount for ARMs applies to initial fixed-rate period only. Qualifying assets are based on Schwab and

Schwab Bank combined account balances, including select brokerage, bank, and retirement accounts. For more information, please visit Schwab.com/IAP.

Quicken Loans, LLC; NMLS #3030; www.nmlsconsumeraccess.org. Equal Housing Lender. Licensed in 50 states. AL: License No. MC 20979, Control No. 100152352;

AR, TX: 1050 Woodward Ave., Detroit, MI 48226-1906, (888) 474-0404; AZ: 1 N. Central Ave., Ste. 2000, Phoenix, AZ 85004, Mortgage Banker License #BK-0902939;

CA: Licensed by Dept. of Business Oversight, under the CA Residential Mortgage Lending Act and Finance Lenders Law; CO: Regulated by the Division of Real Estate;

GA: Residential Mortgage Licensee #11704; IL: Residential Mortgage Licensee #4127 – Dept. of Financial and Professional Regulation; KS: Licensed Mortgage Company

MC.0025309; MA: Mortgage Lender License #ML 3030; ME: Supervised Lender License; MN: Not an offer for a rate lock agreement; MS: Licensed by the MS Dept. of

Banking and Consumer Finance; NH: Licensed by the NH Banking Dept., #6743MB; NV: License #626; NJ: New Jersey – Quicken Loans, LLC, 1050 Woodward Ave.,

Detroit, MI 48226, (888) 474-0404, Licensed by the NJ Department of Banking and Insurance; NY: Licensed Mortgage Banker – NYS Banking Dept.; OH: MB 850076;

OR: License #ML-1387; PA: Licensed by the Dept. of Banking – License #21430; RI: Licensed Lender; WA: Consumer Loan Company License CL-3030. Conditions may

apply. Lending services provided by ©2000 – 2021 Quicken Loans, LLC, a subsidiary of Rock Holdings Inc. “Quicken Loans” is a registered service mark of Intuit Inc.,

used under license.

Charles Schwab Bank, SSB and Charles Schwab & Co., Inc. are separate but affiliated companies and subsidiaries of The Charles Schwab Corporation. Brokerage

products offered by Charles Schwab & Co., Inc. (Member SIPC) are not insured by the FDIC, are not deposits or obligations of Charles Schwab Bank, SSB, and are subject

to investment risk, including the possible loss of principal invested. Charles Schwab & Co., Inc. does not solicit, offer, endorse, negotiate, or originate any mortgage loan

products and is neither a licensed mortgage broker nor a licensed mortgage lender. Home lending is offered and provided by Quicken Loans, LLC. Quicken Loans, LLC

is not affiliated with The Charles Schwab Corporation, Charles Schwab & Co., Inc., or Charles Schwab Bank, SSB. Deposit and other lending products are offered by

Charles Schwab Bank, SSB, Member FDIC and Equal Housing Lender.

Charles Schwab Bank, PO Box 982605, El Paso, TX 79998-2605

©2021 Charles Schwab Bank, SSB. All rights reserved. Member FDIC.

(0521-1LWV) ADP112973OI-00 (03/21) 00252892No Place Like Home

How best to pass on real estate to your kids.

hen it comes to estate planning, of trust services consulting at Charles that go with it, but does he or she

W a family home can be among Schwab Trust Company. “But you actually want to live there? If you have

I L LU S T R AT I O N B Y J I N G L I

the most valuable—and compli- need to think about not only your multiple heirs, is it realistic for them

cated—assets to pass down. own needs and wishes but also those to co-own the property or will such an

“It’s perfectly natural to want to of your heirs.” arrangement create conflict?

see a cherished home stay within the For example, your child may love You also need to consider the role

family,” says George Pennock, director the family home and all the memories the house will play in your later years.

SUMMER 2021 | O N WA R D | 11FA M I LY M AT T E R S

“Do you plan to stay in the home, or is However generous of allowing you greater control over

it possible you may need or want to how the property is managed and

move at some point?” George asks. your intent, the under what conditions it can be sold.

“All of this factors into how—and bequest of a home The home would remain part of your

whether—you transfer the property estate until your death, at which time

to your kids.”

can be an albatross if it would pass to your heirs outside

With that in mind, here are three not accompanied by probate.

ways to pass along a home to your additional funds to

heirs—both during and after your However generous your intent,

lifetime. help cover taxes and George warns that the bequest of

other costs. a home can be an albatross if not

Sell it: If you’re looking to accompanied by additional funds to

1 move or put your home’s equi- help cover improvements, insurance,

ty to use elsewhere, selling the home maintenance, and taxes—particularly

to a child or other heir could be a if you plan to leave it to multiple heirs.

good option. Doing so removes the “You don’t want to make your kids

property from your taxable estate and The tax consequences could be house rich and cash poor,” George

establishes a new cost basis—mean- even more severe for your heirs. “If says. “Nor do you want them fighting

ing the capital gains on any future sale you give a home to your child during about the costs of ongoing mainte-

will be calculated using the value of your lifetime—such as through a nance and upkeep.” In such cases,

the home on the date of the transfer deed transfer—the cost basis doesn’t setting aside funds in a trust dedicated

rather than your original purchase change,” Marianne says. That means for this purpose can help ensure the

price. “Be aware, however, that if you the capital gains on any future sale home is well maintained for years to

sell the home for less than its fair mar- will be calculated using your original come.

ket value, the difference between the purchase price rather than the value of Regardless of the method you use

sale price and the market value could the home on the date of the transfer. to pass down the home, it will receive

be subject to gift taxes,” says Marianne a new cost basis upon your death,

Hayes, CPA, a senior wealth strategist Pass it down: Generally meaning any capital gains taxes

at Schwab.

3 speaking, there are three meth- resulting from a future sale would be

ods for leaving a home to your heirs: calculated using the fair market value

Gift it: As generous as it is to at the time of the transfer.

2 gift a home to an heir during n Last will and testament: You can use

your lifetime, it could have negative your will to designate to whom the Talk it out

tax repercussions. That’s because home should go and in what propor- Whether you sell, gift, or pass down

such a gift counts toward your tions. That said, wills are required to your property, the transfer could

lifetime gift tax exemption. That go through probate—the sometimes trigger a reassessment of the home’s

might not seem like an issue now lengthy and often costly legal process property taxes, so be sure to factor

that the combined gift and estate tax of validating your will—which can that into your plan—ideally with the

exemption is $11.7 million for indi- slow down the transfer of ownership help of an attorney or a tax advisor.

viduals ($23.4 million for married to your heirs. In addition to consulting financial

couples) in 2021, but that number is n Transfer-on-death deed: If probate professionals who can help you put

set to come down by half starting in is a concern, you may be able to sign your plan in place, “the most import-

2026, if not sooner. If that happens, a transfer-on-death deed—available ant thing you can do is to make sure

such a gift could result in a federal es- in 29 states and the District of all family members are part of the

tate tax of up to 40%, depending on Columbia—which allows you to pass conversation,” George says. “That

the size of your estate. State-level the property to your heirs outside way, everyone has the chance to see

gift, estate, and inheritance taxes probate upon your death. their needs and wishes reflected in

could also be a factor, depending on n Trust: Another way to avoid pro- the plan for your home, which can

NEXT where you live. bate is to transfer the property into avoid unnecessary conflict down the

STEPS a living trust, which has the benefit road.” n

Your Schwab financial consultant can help you See page 42 for important information. ◆ This information does not constitute and is not intended

think through the details of your estate plan to be a substitute for specific individualized tax, legal, or investment planning advice. Where

and connect you with other Schwab specialists specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax

advisor, CPA, financial planner, or investment manager. ◆ Charles Schwab & Co., Inc. (“Schwab”) is

who can help implement it. Call today to affiliated with Charles Schwab Trust Company (CSTC), the corporate trustee for Schwab Personal

schedule an appointment. Trust Services (SPTS). (0621-1HJ5)

12 | C H A R L E S S C H WA B | SUMMER 2021B Y CAR R I E SCHWAB - POM E RANT Z

Q A

Shopping

Dear Carrie, Dear Reader,

for an RV? If months of being cooped up at home have you

We’re a young family dreaming of the open road, you’re not alone. Sales

that wants to travel safely of recreational vehicles jumped 6% in 2020, with

suppliers hustling to keep up with an even greater

Tap the brakes

and cost-effectively. Is demand for 2021.

before you buy. buying an RV a good idea? Interestingly, owners are getting younger, with

the under-45 crowd representing the fastest-growing

And where should we

segment of RV owners. Indeed, we’ve come a long way

start? from tossing a cooler and a couple of sleeping bags in

a VW bus (as a colleague of mine nostalgically recalls

I L LU S T R AT I O N B Y J I N G L I

SUMMER 2021 | O N WA R D | 13A S K CA R R I E

doing with her young family in the Loan ranger

’70s). Now we want a place to sleep in

A longer-term loan may make for more manageable monthly payments,

the wilderness and a modern office to but don’t overlook the true cost of such financing.

take on the road.

But as much as you might love the

idea of “RVing,” the reality of owning Five-year loan 10-year loan

and maintaining an RV could become

Amount borrowed $45,000 $45,000

a bit of a financial headache if you’re

not careful. Here are a few things to Interest rate 5.5% 6%

consider before buying an RV.

Monthly payment $860 $500

Be realistic about

what you want Interest paid over life of loan $6,573 $14,951

Understanding how—and how

Total cost $51,573 $59,951

often—you’ll use the RV will help

you determine the type to buy. Are

Interest rates are hypothetical and for illustrative purposes only but are reflective of prevailing rates for

you looking for basic amenities or five- and 10-year loans by borrowers with excellent credit as of 01/27/2021. Totals have been rounded

deluxe features? Do you need space to the nearest dollar.

for an office or additional guests?

Most important, how much RV can

you afford? From a used camper van neighborhood or city—so you may by looking at your budget to see if and

to a state-of-the-art motor home, the need to factor in storage costs, as well. how it fits in—and remember, this is a

differences in features and cost can You may think that what you’ll want, not a need, and belongs on your

be staggering; prices can range from save on typical vacation expenses like nonessentials list.

several thousand dollars to well over airfare, hotel bills, and restaurants will Next, ask yourself what short-

$500,000. balance out these additional costs, term trade-offs you’ll have to make

When you step aboard one of the and that’s a good point. But be sure to to handle this new expense. If you

new, completely decked-out models, also factor in campsite fees and related finance the vehicle, will it increase

you’ll be wowed. But remember: A charges like propane. And with the your debt load beyond a manageable

brand-new RV, like any other vehicle, recent popularity of RV travel, you may level? More important, are there any

will likely lose a significant chunk of its have to reserve your campsites well long-term consequences to consider?

value as soon as you drive it off the lot. in advance—which can undercut the If the cost of buying and maintaining

So, before you open your wallet, take thrill of spontaneously hitting the road. an RV will leave your savings for other

a deep breath and carefully evaluate If you plan to finance the purchase, goals running low—especially when

your priorities. also think about how much that loan the goal is retirement—it may be best

will cost you over the long haul. Recent to hit the brakes.

Don’t underestimate statistics show the average amount

ongoing costs financed for an RV is $45,000, with Try before you buy

Let’s say you find the RV you want at a terms typically ranging from five to You don’t have to own an RV to

price you can handle. Have you thought 10 years—or as long as 20 years if your experience life on the road. National

about expenses beyond the purchase loan is in the hundreds of thousands rental companies and marketplaces

price? For example, the usual expenses of dollars. Choosing a longer-term (similar to Airbnb) can point you to

that come with owning and driving a loan can make the monthly payments a range of RVs for hire in your area.

vehicle—gas, insurance, maintenance, more manageable, but it also means Renting could mean the trip of a

registration, and repairs—could cost you’ll be paying more interest (see lifetime and convince you that buying

a lot more for an RV than they do a “Loan ranger,” above)—and rates for an RV is right for you. Or it may help

regular car or truck. Plus, having a RV loans tend to be higher than those you avoid a major case of buyer’s

large RV parked in your driveway may for auto loans. remorse down the road. n

not sit well with the neighbors—and

could even be against the rules in your Don’t let your other goals Carrie Schwab-Pomerantz

(@carrieschwab), CFP®, is president of

take a back seat Charles Schwab Foundation and senior vice

NEXT While I totally understand the allure president of Schwab Community Services

STEPS of an RV, especially after the cabin

at Charles Schwab & Co., Inc.

fever we’ve all been experiencing, you

Read more insights about real-world money should approach such a purchase as a See page 42 for important information.

matters at schwab.com/askcarrie. financial decision like any other. Start (0621-119E)

14 | C H A R L E S S C H WA B | SUMMER 2021CONTENTS EARLY RE TIREMENT | MUNICIPAL BONDS UPDATE

The Accidental Retiree

Could you weather an earlier-than-expected

exit from the workforce?

By Rob Williams

ost of us have an age at which we’d

M

I L LU S T R AT I O N B Y S T E P H A N I E S I N G L E TO N

like to stop working—but what if

circumstances change and retirement comes

early? According to a 2020 survey conducted

by the Employee Benefit Research Institute,

nearly half of retirees reported leaving the

workforce earlier than anticipated.

SUMMER 2021 | O N WA R D | 15P E R S P E CT I V E S | E A R LY R E T I R E M E N T

That said, just because early retire- Making the shift from of seeing you through retirement.

ment isn’t part of your plan doesn’t Be aware, however, that this rule is

mean it isn’t doable. So, how do you saving to spending conservative and doesn’t account for

know if you’re adequately prepared for can be challenging fluctuations in spending or market

early retirement? Follow these steps to performance. A financial planner can

find out.

under the best of help you develop a retirement plan,

circumstances. The including a personalized spending rate

Step 1 key is to plan your based on your needs and time frame.

Review your finances

retirement with as n Is my asset allocation in line with

To begin, ask yourself four questions: much detail as possible. my time horizon, risk capacity, and

risk tolerance? Maintaining a diver-

n What are my expenses now? It sified, balanced portfolio becomes

can be helpful to split your current even more important in retirement to

expenses into two categories: must- so make sure to compare all available help prevent taking on too much—or

haves like groceries and housing, and options, including COBRA, private too little—risk. For example, if you’re

nice-to-haves like eating out and travel. insurance, and your spouse’s plan, if facing a retirement that could last a

available. You may also be eligible for decade longer than planned, holding

n How will my expenses change discounted coverage through organiza- more stocks in the early years will help

in retirement? While some costs, tions such as AARP. guard against the risk of outliving your

such as payroll taxes and retirement savings. Just be sure you take a more

contributions, will go away, others, Step 2 conservative approach with the money

particularly health care, are likely to Assess your portfolio you’ll need to tap in the next few years.

increase. Also factor in the potential Striking a balance between short-term

for major one-time expenses, such Now that you have a clear picture of income needs and longer-term growth

as a child’s wedding, a new car, or a your income needs, ask yourself three is critical in retirement.

roof replacement. And don’t overlook questions to help determine the over-

the cost of long-term care—which all strength of your portfolio: Step 3

roughly 70% of retirees will require at Dig into the details

some point in their lives, according to n Am I prepared to weather a down-

longtermcare.gov. turn? Having adequate short-term Making the shift from saving to

reserves can help you avoid having to spending can be challenging under

n What’s my potential income? Tally make a portfolio withdrawal during the best of circumstances. The key is

up income from pensions, Social a bear market. We suggest having to plan your retirement with as much

Security, and any other nonportfolio enough cash on hand to cover a year’s detail as possible—as well as with the

sources. Subtract that number from worth of retirement expenses, plus understanding that you can’t predict

your target annual income to deter- another two to four years’ worth of everything and will likely need to

mine how much money you’ll need spending needs in short-term invest- make changes as your needs come

to generate from your portfolio. For ments such as certificates of deposit into focus. A planner can help you take

example, if you need $90,000 a year in and Treasury bills. a hard look at your finances and make

income and expect to receive $40,000 the necessary adjustments to keep

from nonportfolio sources, you’ll need n Is my withdrawal rate sustainable? your retirement on track—no matter

$50,000 from your portfolio to meet Keep in mind the 4% rule, which says when it hits. n

your spending needs. that withdrawing 4% of your portfolio

in your first year of retirement—and

n What about health care? If you’re adjusting that number annually for

no longer covered by your employer- inflation—will give your portfolio a Rob Williams is vice

sponsored health insurance, you’ll high probability of lasting 30 years. president of financial

planning at the

need coverage until you become eligi- Thus, if you want to withdraw $50,000 Schwab Center for

ble for Medicare at age 65. Health care in your first year, a $1.25 million port- Financial Research.

NEXT can take a big bite out of your income, folio ($50,000/0.04) has a good chance

STEPS

Schwab Plan™ can help clients create a

See page 42 for important information. u Diversification and asset allocation strategies do not

complimentary digital financial plan for retirement. ensure a profit and cannot protect against losses in a declining market. u Investing involves

Learn more at schwab.com/schwabplan. risk, including loss of principal. (0621-1DH6)

16 | C H A R L E S S C H WA B | SUMMER 2021What’s your emerging market strategy missing?

The full power of an Asia expert.

Introducing the Matthews Emerging Markets Equity Fund

on Schwab Mutual Fund OneSource®

With Asia representing 80% of the emerging market investment universe, having a deep

understanding of this complex region is critical. The Matthews Emerging Markets Equity

Fund applies our 29 years of investment expertise in Asia to other emerging markets

around the world, so that you don’t miss out on some of the most attractive investment

opportunities today.

Uncover new investment opportunities at MatthewsAsia.com/Emerging-Markets or view

the Matthews Asia Funds available on the Schwab Mutual Fund OneSource Select List ®.

Investors should consider the investment objectives, risks, charges and expense of the Matthews Asia Funds carefully before making

an investment decision. This and other information about the Funds is contained at matthewsasia.com. Read the prospectus

carefully. Investing involves risk including the possible loss of income. Funds that invest in emerging market foreign securities may involve certain

additional risks, exchange rate fluctuations, less liquidity, greater volatility and less regulation. Distributor: Foreside Funds Distributors LLC

Schwab, Mutual Fund OneSource ® and Mutual Fund OneSource Select List ® are trademarks of Charles Schwab & Co., Inc. and used with permission.

Matthews Asia and Charles Schwab & Co., Inc. are not affiliated. Charles Schwab & Co., Inc. (member SIPC) receives remuneration from fund

companies in the Mutual Fund OneSource ® service for recordkeeping and shareholder services, and other administrative services. Schwab also may

receive remuneration from transaction fee fund companies for certain administrative services. The amount of fees Schwab or its affiliates receive from

funds participating in the Mutual Fund OneSource service is not considered in the Select List selection, nor does any fund pay Schwab

to be included in the Select List.

© 2021 Matthews International Capital Management, LLC

2021_Q2_OO_Mathews Asia_no url.indd 1 4/12/2021 11:09:02 AMP E R S P E CT I V E S | M U N I C I PA L B O N D S U P DAT E

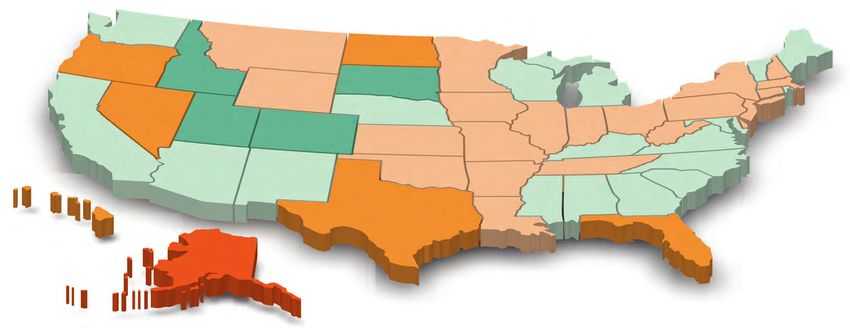

The State of Munis

which often have strong legal pro- credit of the issuer, and are usually for a given muni bond in its official

tections. Which is not to say that a considered fairly secure. However, Cooper Howard, statement.

CFA, is director

downgrade isn’t a problem—it signals some state and local governments

of fixed income

Why local governments are proving more resilient that an issuer’s ability to meet its debt were hit harder by the pandemic strategy at the Mind your risk

than expected. service has weakened in the opinion than others, putting a strain on their Schwab Center for

Financial Research.

By Cooper Howard of the ratings agencies, possibly to tax revenues. That said, state and Although credit risks are lower now,

the point that its bonds are no longer local governments received $350 it’s wise to focus the bulk of your port-

hen the COVID-19 pandemic a number of provisions to help support suitable for your situation. billion of direct aid in the relief bill folio on issuers rated A/A and higher,

W struck in early 2020, state and economic growth, which should even- And, despite an improving credit passed in March, which should go with some exposure to issuers at the

local officials braced for the worst. tually flow to many municipalities via outlook for many issuers, it’s import- a long way toward shoring up their in sectors that already had a fair lower end of the investment-grade

With tens of thousands of businesses higher income, sales, and other tax ant not to paint the whole muni finances. amount of risk before the pandemic, spectrum (BBB/Baa) if your risk toler-

shuttered nearly overnight, millions of revenues. market with the same broad brush. If you’re considering a GO bond, be such as those issued by unrated health ance allows it. n

Americans out of work, and concerns However, if state and local gov- Whether you’re reassessing your cur- sure to check the financial situation care and hospital issuers. Going

that tax revenues would soon be in ernments do struggle, we’re likely to rent muni holdings or looking to add of the issuing municipality. That forward, bonds backed by tax revenues

steep decline, many analysts feared see an increase in rating downgrades new issues, be sure to consider how includes demographic trends of the that were significantly impacted by the See page 42 for important information. u Investors should

the municipal-bond market could face rather than defaults: 49 out of 50 states the revenue source backing a bond area, its reliance on certain revenues, pandemic—such as hotel occupancy consider carefully information contained in the prospectus

or, if available, the summary prospectus, including

a tsunami of defaults. are legally required to balance their could affect its risk. For example: and the issuer’s overall credit rating. taxes—may put such bonds at higher investment objectives, risks, charges, and expenses.

But as 2020 wore on, state and local operating budgets—Vermont being risk, at least in the short term. Please read it carefully before investing. u Tax-exempt

governments appeared to be holding the lone exception—and spending cuts n General obligation (GO) bonds are n Revenue bonds, on the other hand, For the time being, it may make bonds are not necessarily a suitable investment for all

persons. Information related to a security’s tax-exempt status

up better than expected, due in part aren’t likely to affect debt payments, often backed by the full faith and are backed by revenue generated sense to stay away from issuers (federal and in-state) is obtained from third parties and

to Congress’ quick action to blunt the from specific services or projects, whose risks are similar to those faced Schwab does not guarantee its accuracy. Tax-exempt income

economic impact of the crisis. In par- such as toll roads or utilities. Of the by the private sector or those that may be subject to the Alternative Minimum Tax (AMT). Capital

ticular, the Coronavirus Aid, Relief, and

Glass half full muni bonds that went into default have such narrow tax pledges behind

appreciation from bond funds and discounted bonds may be

subject to state or local taxes. Capital gains are not exempt

Economic Security (CARES) Act estab- Despite the economic crisis brought on by COVID-19, nearly half of all states saw last year, most were revenue bonds them. You can find the revenue sources from federal income tax. (0621-1TAV)

year-over-year increases in tax revenues from April through December 2020.

lished a $150 billion Coronavirus Relief

Fund to help state and local govern-

ments pay for expenses incurred due to

COVID-19. The CARES Act also pro- WA VT NH

2.5% 2.2% –2.0%

vided small-business grants, temporary MT

ME

ND 2.2%

medical facilities, and unemployment –5.6%

OR –14.8%

benefits, which further softened the MN

–10.5% ID

economic blow. SD

–2.5% NY

10.4% WI

What’s more, higher-earning indi- WY 6.3% MI –4.1% MA –2.8%

0.5%

viduals remained disproportionately –8.5% 0.3%

IA RI 0.8%

employed, and real estate and equity NV NE PA –3.1%

–2.0% OH

markets bounced back fairly quickly— –11.8% UT 0.7% IL IN CT –2.5%

8.0% CO –0.9% WV

all of which helped buoy tax revenues CA –2.0% –2.4% NJ –2.4%

5.7% KS MO –4.3%

in certain states (see “Glass half full,” 1.2% –2.7% VA 1.2%

–2.7% DE –7.3%

right). KY 1.5%

AZ NC 2.1% MD 0.1%

As a result, the municipal bonds OK TN –1.3%

NM

issued by state and local governments 2.4% –4.0% AR SC

4.3% –0.2%

proved similarly resilient, with defaults AL

1.7%

MS GA

in 2020 tracking well below the totals 0.3% 3.7% 1.9%

TX LA

realized in the wake of the Great –10.4% –7.5%

Recession. HI

–17.0% FL

The worst may be behind us AK –11.3%

Indeed, credit risks in the muni market –42.5%

are waning, largely due to the recently

passed $1.9 trillion relief package,

which provided substantial direct aid

NEXT Source: The Urban-Brookings

to many muni issuers. It also contained Tax Policy Center.

STEPS

Change in tax revenue

To research muni-bond funds for your portfolio,

log in to schwab.com/fundscreener. –42.5% –20% –10% 0% +5% +10.4%

18 | C H A R L E S S C H WA B | SUMMER 2021 SUMMER 2021 | O N WA R D | 19Helping investors reach their retirement goals for over 80 years. T. Rowe Price’s strategic investing approach has helped inform confident investment decisions since 1937. By asking the right questions at the right time, we seek to uncover opportunities and manage risk to continue guiding our clients through a variety of market conditions. Explore 37 funds on the Q1 2021 Mutual Fund OneSource Select List®. Visit Schwab.com/troweprice Request a prospectus or summary prospectus at Schwab.com/OneSource; each includes investment objectives, risks, fees, expenses, and other information that you should read and consider carefully before investing. All funds are subject to market risk, including possible loss of principal, and are subject to management fees and expenses. Charles Schwab & Co., Inc., Member SIPC, receives remuneration from fund companies in the Mutual Fund OneSource® service for recordkeeping and shareholder services and other administrative services. Schwab also may receive remuneration from transaction fee fund companies for certain administrative services. The amount of fees Schwab or its affiliates receive from funds participating in the Mutual Fund OneSource® service is not considered in the Select List selection, nor does any fund pay Schwab to be included in the Select List. Schwab, Mutual Fund OneSource® and Mutual Fund OneSource Select List® are trademarks of Charles Schwab & Co., Inc. and used with permission. T. Rowe Price and Charles Schwab & Co., Inc. are not affiliated. T. Rowe Price Investment Services, Inc., Distributor.

Vision Quest

How to take a more clear-eyed view of your trading decisions.

By Randy Frederick

t can be difficult to keep our Here’s how to take a clear-headed, emotionally speaking, as gaining it

I

I L LU S T R AT I O N B Y A M R I TA M A R I N O

emotions from upending our more-considered approach to four is pleasurable—a psychological effect

decision-making—especially when potentially fraught trading situations. known as loss aversion.

we have money on the line. The

problem is particularly acute for stock 1 You’re holding on to a loser The fix: A common trading maxim

traders, who can often find themselves applies here—cut your losses short

in emotionally charged situations Research has shown that losing and let your winners run. The best

with considerable sums at stake. money is roughly twice as painful, way to do so is to create an exit

SUMMER 2021 | O N WA R D | 21TRADING

strategy before you place a trade, n If you have a Schwab Trading mentality. In such cases, many traders

such as setting a stop-limit order to Services™ account, you can track let positions stay open too long, even

automatically sell if the stock drops your ratio of gains to losses using when they’ve surpassed their profit

to or beyond the limit price—say, 5% the Gain/Loss Analyzer tool. Log in targets. Some even cash out long-term

or 10% below what you paid. (Note to schwab.com, click the Trade tab, positions to free up more funds to

there is no guarantee that a stop-limit then the Trade Source tab. trade, potentially exposing themselves

order, once triggered, will result in an to unwanted risk.

order execution.) 3 The market is tanking

Making this kind of upfront The fix: Above all, remember that

commitment can help remove your Few scenarios trigger hasty or irra- gains aren’t gains until you’ve sold the

emotions from the selling process. tional decisions quite like a massive position at a profit, so don’t let a trade

(For more on commitment devices, market decline. As panic sets in, greed, stay open too long.

see “Impulse Control,” page 28.) loss aversion, and wishful thinking Also keep an eye out for red flags

For positions you already hold, ask can all collide. Instead of performing that might lead to a reversal. It can be

yourself: Would you buy the stock at our usual due diligence, we allow tempting to take on more risk when

its current price if you didn’t already price alone to dictate our trade deci- prices are rising, but doing so can leave

own it? If the answer is no, it’s proba- sions, believing it’s an opportunity you overexposed if an unexpected

bly time to sell. for quick and easy gains. At the same correction occurs.

time, we may double down on losing And finally, be sure you’re not

nL

earn more about stop and positions in the hope that the market risking too much of your investment

stop-limit orders at schwab.com/ will rebound quickly—and our trades capital in your trading portfolio. Many

stoporders. along with it. traders like to set a limit, such as not

taking positions that represent more

2 You’ve had a string The fix: First, don’t overlook the than 20% of their overall taxable

of losses possibility that the downtrend could portfolio.

continue. Rather than getting into

Losing streaks can happen to the a trade while the market is falling, nT

o determine what percentage

best of us, but sometimes a bout of consider waiting for a few consecutive of your portfolio a single stock

bad luck can actually be a problem positive days before opening a new represents, log in to schwab.com/

with our trading strategy. Attributing position. And be sure to do your usual positions.

successes to our own skills but failures homework on any stock you’re consid-

to uncontrollable outside forces is ering—bargain-basement prices alone Wait and deescalate

known as self-attribution bias. aren’t reason enough to buy a stock.

The point here is not to become a

The fix: To begin, make sure you nS

chwab Equity Ratings® can help robot but rather to be on the lookout

know whether you’re losing or you identify stocks that have for those times when emotions can get

making money on a net basis, then the potential to outperform or the best of us.

look for patterns in your wins and underperform the market. To view a If you have trouble distancing your

losses. stock’s Schwab Equity Rating, log in emotions from your trading decisions,

For example, if your winning to schwab.com and enter its ticker it’s never a bad idea to slow down or

trades employ fundamental analysis symbol. even take a break. Cooler heads usually

and your losing trades are based on prevail, and trading is no exception. n

technicals, you might want to focus 4 The market is soaring

more on fundamentals for a while.

As you work to figure out what Biases don’t just rear their heads Randy Frederick

needs fixing, there’s no harm in when we’re under stress—strong (@randyafrederick)

is vice president of

reducing the size of your trades. Once bull markets, too, can trigger a host of trading and derivatives

your results get back on track, you can suboptimal responses, including over- at the Schwab Center

for Financial Research.

increase your risk-taking. confidence, self-attribution, and herd

See page 42 for important information. u The information provided here is for general informational purposes only and should not be considered

an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone.

Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. u Schwab Equity

Ratings and the general buy/hold/sell guidance are not personal recommendations for any particular investor or client and do not take into account

the financial, investment, or other objectives or needs of, and may not be suitable for, any particular investor or client. Investors and clients should

consider Schwab Equity Ratings as only a single factor in making their investment decision while taking into account the current market environment.

u Investing involves risk, including loss of principal. (0621-1VJA)

22 | C H A R L E S S C H WA B | SUMMER 2021You can also read