Sustainability Accounting Standards Board - Standards Board Meeting, Quarter 1, 2020, Public Meeting - SASB

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

g

tin

ee

M

a rd

Bo

s

rd

Sustainability Accounting Standards Board

da

Standards Board Meeting, Quarter 1, 2020, Public Meeting

an

St

Tuesday, February 25, 2020 20

20

25

b.

© SASB

Fe

Fe

b.

25

20

20

St

an

da

rd

s

Welcome & Agenda Overview

Bo

ard

M

ee

tin

g

Objectives for Today’s Meeting

g

tin

ee

M

1. New project proposals – seek Standards Board approval

rd

2. Agenda planning & schedule

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

3 2/18/2020 © SASB

Agenda

g

tin

ee

M

a rd

Bo

s

rd

da

an

St

20

20

25

b.

For public meeting materials visit the Standards Board Meeting Calendar & Archive page. The meeting recording and outcomes will be posted on the same page after

the meeting.

Fe

4 2/18/2020 © SASB

Standard-Setting Process Overview

g

tin

ee

M

a rd

Bo

s

rd

da

an

St

2 20 2

Project screening – input from: Research Program – objective: Standard-Setting Agenda:

20

• Market & public engagement Conduct research and obtain • Project determined to meet four criteria

• Standards Advisory Group market input to determine if • Prioritization informed by agenda

25

• Standards Board standard setting should be priorities (Sept. 2019 meeting)

• Staff research pursued (meets four criteria) • Initiates standard-setting process

b.

Fe

5 2/18/2020 © SASB

Criteria for Standard-Setting Projects (Agenda)

g

tin

ee

Scope/prevalence

M

Mission alignment

rd

‣ Is there an opportunity to ‣ Is the issue pervasive,

a

significantly improve including scope of industries

Bo

communication by companies or geographies impacted.

s

to investors of decision-useful

rd

sustainability information

da

Capacity

an

Feasibility ‣ Does Staff (and the Board)

St

have sufficient capacity to

‣ What is the likelihood that 20 formally address the issue;

there would be a proposed

20

and does the issue warrant

solution to put to the Board in prioritization of resources

25

a timely fashion. over alternatives.

b.

Fe

6 2/18/2020 © SASB

Agenda Prioritization

g

tin

ee

1. Governance Documents

M

2. Thematic Issue – materiality

a rd

3. Thematic Issue – measurement

Bo

4. Industry Standard: reevaluating existing content – materiality

s

rd

5. Industry Standard: reevaluating existing content – measurement

da

6. Industry Standard: evaluating new or emerging issues

an

7. Industry scope and structure issues, including new industry standards

St

8. Globalization 20

20

9. Technical Protocol Issues

25

10. Standards Application Guidance

b.

11. Alignment

Fe

7 2/18/2020 © SASB

Agenda Prioritization

g

tin

ee

M

a rd

Bo

Alignment theme

s

8. Globalization 11. Alignment

rd

da

Conceptual Practical Presentation Legal Technical

an

St

3. Thematic Issue –

1. Governance Documents 7. Industry scope and

measurement

2. Thematic Issue – materiality structure issues, including

4. Industry Standard:

reevaluating existing content –

20

new industry standards

10. Standards Application

10. Standards Application

Guidance

10. Standards Application

Guidance

5. Industry Standard:

reevaluating existing

20

content – measurement

materiality Guidance

9. Technical Protocol Issues

6. Industry Standard: evaluating

25

new or emerging issues

b.

Fe

8 2/18/2020 © SASB

g

tin

ee

M

Standard-Setting Project Proposals

a rd

Bo

s

• Measuring Performance on Raw Materials Sourcing in

rd

da

the Apparel, Accessories & Footwear Industry

an

St

• Supply Chain Management in the Tobacco Industry

20

20

25

b.

Fe

g

tin

ee

Measuring Performance on Raw Materials Sourcing

M

rd

in the Apparel, Accessories & Footwear Industry

a

Bo

s

rd

da

an

St

20

20

25

b.

FeMeasuring Performance on Raw Materials Sourcing in the

g

Apparel, Accessories & Footwear Industry Standard-Setting Project Proposal

tin

ee

Problem Statement

M

Market input and internal review suggest that the two metrics associated with the Raw Materials Sourcing disclosure

topic provide insufficient guidance that may result in inconsistent calculations and noncomparable disclosures. In

rd

addition, market input suggests that improvements to the completeness in which the metrics measure performance on

a

the topic, along with further alignment with existing industry approaches should be considered.

Bo

Proposed Project Scope & Anticipated Course of Action

s

Staff recommends that the Standards Board approve a standard-setting project to revise, clarify, and consider

rd

improvements to the following metrics (or at a minimum, the technical protocols for each metric):

da

• CG-AA-440a.1: Description of environmental and social risks associated with sourcing priority raw materials

• CG-AA-440a.2: Percentage of raw materials third-party certified to an environmental and/or social sustainability

an

standard, by standard

St

Criteria for Standard-Setting Project

20

Mission Alignment – Is there an opportunity to significantly improve communication by companies to investors of

decision-useful sustainability information?

20

Scope / Prevalence – Is the issue pervasive, including scope of industries or geographies impacted?

Capacity – Does Staff (and the Board) have sufficient capacity to formally address the issue; and does the issue warrant

25

prioritization of resources over alternatives.

Feasibility – What is the likelihood that there would be a proposed solution to put to the Board in a timely fashion.

b.

Fe

11 2/18/2020 © SASBResearch Agenda Prioritization

g

tin

ee

1. Governance Documents

M

2. Thematic Issue – materiality

a rd

3. Thematic Issue – measurement

Bo

4. Industry Standard: reevaluating existing content – materiality

s

rd

5. Industry Standard: reevaluating existing content – measurement

da

6. Industry Standard: evaluating new or emerging issues

an

7. Industry scope and structure issues, including new industry standards

St

8. Globalization 20

20

9. Technical Protocol Issues

25

10. Standards Application Guidance

b.

11. Alignment

Fe

12 2/18/2020 © SASBWhy Now? Industry Coalesces Around Sustainable Materials

g

tin

• The Year Ahead: Welcome to the Materials Revolution, January 2, 2020, Business of Fashion

ee

• More than Half of Polyester in Adidas’ Sneakers Will Be in Recycled This Year, January 21, 2020, Yahoo News

M

• Zara clothes to be made by 100% sustainable fabrics by 2025, July 17, 2019, The Guardian

a rd

• Gap commits to 100% sustainable cotton sourcing, June 7, 2019, Supply Chain Dive

Bo

• 60 Percent of Athleta’s Materials Are Now Made from Sustainable Fibers, April 18, 2019, Gap Inc. webpage

s

rd

• Walmart to use 100% sustainable cotton by 2025, April 17, 2019, fibre2fashion.com

da

• H&M pledges 100% Sustainable Cotton by 2020, April 1, 2019, Supply Chain Dive

an

St

The following companies have made commitments related to sustainable material use:

▪ H&M ▪ LVMH

20 ▪ Kering ▪ Tapestry TOTAL MARKET CAP

REPRESENTED:

20

▪ Inditex ▪ PVH ▪ VF Corp ▪ Lululemon

▪ Ralph Lauren

▪ Fast Retailing ▪ Gap ▪ Walmart $1.2T

25

▪ Nike ▪ Adidas ▪ Target ▪ Zalando (Germany)

b.

Fe

13 2/18/2020 © SASBCurrent SASB Disclosures on Raw Materials Sourcing

g

tin

ee

TOPIC: Raw Materials Sourcing

ACCOUNTING METRIC: Percentage of raw materials third-party certified to an environmental and/or social sustainability standard, by standard

M

In 2017 we sourced 17% of our cotton (Conventional, organic, recycled) as Better Cotton.

rd

In 2018, we are estimating that we sourced 33% of our cotton as Better Cotton. This was

a

calculated using the BCCU’s sourced in 2018 and assuming a 3% growth rate in PVH total

Bo

cotton consumption year over year. We also require that down used in our products be

certified by the Textile Exchange’s Responsible Down Standard (RDS) to ensure it has

been sourced responsibly

s

rd

Materials (FY18)

da

Rubber 92% environmentally preferred Polyester 19% recycled

an

Cotton 8% certified organic Corrugate 84% recycled EVA FoamMarket Input Highlights Three Key Concerns

g

tin

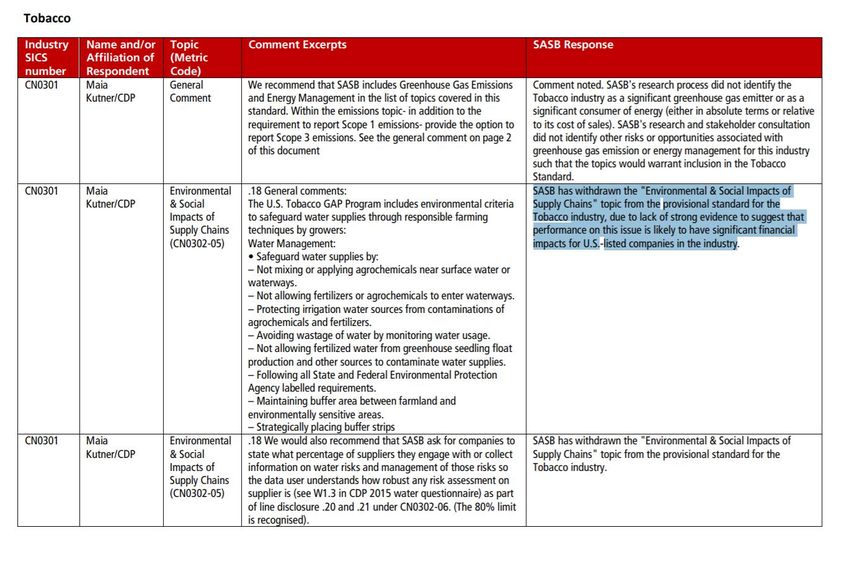

SASB has received the following feedback from a company and an industry-focused NGO on metric CG-AA-

ee

440a.1:

M

Excerpt from the Apparel, Accessories & Footwear industry standard:

Feedback that the definition of industry

rd

terms, such as “priority raw materials,” are

1.

a

not aligned with industry accepted terms,

Bo

and don’t account for materials that may

not be used in large quantities but may still

represent critical risks/opportunities to

s

rd

companies

da

an

ANTICIPATED RESEARCH

St

• Research textile industry standards intended to guide companies in their identification of “priority raw materials”

• Interview companies on internal processes for identifying “priority raw materials”

ANTICIPATED OUTCOME

20

20

• Determination on whether revisions to terms, such as “priority raw materials,” are necessary to improve completeness

• Determination on whether further alignment with an external standard may improve the completeness and comparability of SASB

25

disclosures, as well as the cost-effectiveness of the standard

b.

Fe

15 2/18/2020 © SASBMarket Input Highlights Three Key Concerns

g

tin

ee

SASB has received feedback from two companies and a third-party assurance provider on metric CG-AA-440a.2:

M

Excerpt from the Apparel, Accessories & Footwear industry standard:

a rd

Bo

2. Feedback that technical protocol

provides guidance that is inconsistent

s

with the metric title

rd

da

an

ANTICIPATED RESEARCH

St

• Research environmental and social sustainability standards for raw material certification in the textile industry

20

ANTICIPATED OUTCOME

20

• Revisions to technical protocol that cite certifications that are consistent with the metric title and facilitate comparable SASB

25

disclosures.

b.

Fe

16 2/18/2020 © SASBMarket Input Highlights Three Key Concerns

g

tin

ee

SASB has received feedback from two companies and a third-party assurance provider on metric CG-AA-440a.2:

M

Excerpt from the Apparel, Accessories & Footwear industry standard:

Feedback that the technical protocol does

rd

3. not provide complete guidance on the

a

calculation of the metric, specifically,

Bo

regarding integration of a waste factor, and

measuring the weight of finished products

s

rd

ANTICIPATED RESEARCH

da

• Research on industry standards intended to calculate sustainable material usage in the textile industry, such as the Corporate

Fiber & Materials Benchmark program.

an

ANTICIPATED OUTCOME

St

• Determination on whether further guidance is needed on:

20

1) Integrating a waste factor or loss rate into the metric calculation;

2) Measuring fiber weight in finished products; and

20

• Determination on whether further alignment with an external standard may improve the measurability of technical protocol,

25

completeness and comparability of SASB disclosures, and the cost-effectiveness of the standard.

b.

Fe

17 2/18/2020 © SASBProposed Project Characteristics

g

tin

ee

TIMELINE

• Estimated project timeline is 6-12 months

M

• Key phases:

rd

▪ Research on the aforementioned topics

a

▪ Company, investor & SME consultations

Bo

▪ Development of exposure draft

s

rd

▪ Public comment period

da

▪ Subsequent revisions

an

▪ Final proposal to the Standards Board

St

RESOURCES 20

20

• Consumer Goods Sector Lead

• Regular engagements with the Sector Committee (and full Board to a certain extent) throughout the project lifetime

25

b.

Fe

18 2/18/2020 © SASBMeasuring Sustainable Material Use in the Apparel, Accessories

g

& Footwear Industry

tin

Standard-setting Project Proposal

Recommendation

ee

M

Problem Statement

rd

Market input and internal review suggest that the two metrics associated with the Raw Materials Sourcing disclosure

a

topic provide insufficient guidance that may result in inconsistent calculations and noncomparable disclosures. In

Bo

addition, market input suggests that improvements to the completeness in which the metrics measure performance on

the topic, along with further alignment with existing industry approaches should be considered.

s

rd

Seeking the Board’s Approval on the Recommendation:

da

an

Staff recommends that the Standards Board approve a standard-setting project to revise, clarify, and consider

improvements to the following metrics (or at a minimum, the technical protocols for each metric):

St

• CG-AA-440a.1: Description of environmental and social risks associated with sourcing priority raw materials

• CG-AA-440a.2: Percentage of raw materials third-party certified to an environmental and/or social

sustainability standard, by standard

20

20

25

b.

Fe

19 2/18/2020 © SASBAppendix

Fe

b.

25

20

20

St

an

da

rd

s

Bo

ard

M

ee

tin

gKey Areas of Research & the Path Forward

g

tin

KEY AREAS OF RESEARCH

ee

• Research environmental and social sustainability standards for raw material certification

M

• Research the impact of loss rate on measuring raw materials, and methodologies for measuring raw materials in finished goods

• Research industry standards aimed at calculating sustainable material usage in the textile industry

rd

• Research the potential alignment between SASB metrics and the Textile Exchange’s Corporate Fiber & Materials

a

Benchmark Program

Bo

A POSSIBLE PATH FORWARD

s

rd

January 20, 2020

da

The Material Change Index (MCI) produced by the nonprofit Textile

Exchange, is part of that organization’s Corporate Fiber & Materials

an

Benchmark program, which enables participating companies to measure,

manage and integrate a preferred fiber and materials strategy into their

business. The index was created in part through the voluntary participation of

St

more than 170 companies, including major brands such as Adidas, C&A,

Gucci, IKEA, Inditex, Nike, Patagonia and Tchibo.

20

POTENTIAL BENEFITS OF ALIGNING WITH CFMB PROGRAM

20

• Already widely used by apparel companies (170), could alleviate reporting burden and improve cost-effectiveness

• CFMB’s requested metrics align closely with the SASB standard

25

• CFMB provides technical guidance that may improve comparability (i.e., waste factor integration and fiber uptake calculator)

b.

Fe

21 2/18/2020 © SASBg

tin

ee

M

Supply Chain Management in the Tobacco Industry

ard

Bo

s

rd

da

an

St

20

20

25

b.

FeSupply Chain Management in the Tobacco Industry

g

tin

Executive Summary Standard-Setting Project Proposal

ee

Problem Statement

Tobacco cultivation results in environmental and social externalities. Tobacco manufacturers monitor and

M

engage with their suppliers on these issues, and investors have indicated interest in disclosures on

rd

tobacco supply chain management. The Tobacco Industry Standard does not currently include any topics

a

or metrics on supply chain management and material sourcing.

Bo

Proposed Project Scope & Anticipated Course of Action

s

rd

Staff seeks Standards Board approval of a standard-setting project to reevaluate adding supply chain

da

management and/or material sourcing topic(s) and metric(s) to the Tobacco Industry Standard.

an

St

20Criteria for Standard-Setting Project

Mission Alignment - Is there an opportunity to significantly improve communication by companies to investors of

20

decision-useful sustainability information?

Scope / Prevalence – Is the issue pervasive, including scope of industries or geographies impacted?

25

Capacity – Does Staff (and the Board) have sufficient capacity to formally address the issue; and does the issue warrant

prioritization of resources over alternatives.

b.

Feasibility: What is the likelihood that there would be a proposed solution to put to the Board in a timely fashion.

Fe

23 2/18/2020 © SASBResearch Agenda Prioritization

g

tin

ee

1. Governance Documents

M

2. Thematic Issue – materiality

a rd

3. Thematic Issue – measurement

Bo

4. Industry Standard: reevaluating existing content – materiality

s

rd

5. Industry Standard: reevaluating existing content – measurement

da

6. Industry Standard: evaluating new or emerging issues

an

7. Industry scope and structure issues, including new industry standards

St

8. Globalization 20

20

9. Technical Protocol Issues

25

10. Standards Application Guidance

b.

11. Alignment

Fe

24 2/18/2020 © SASBKey stages of tobacco product lifecycle

g

tin

ee

M

rd

a

Bo

Product Product

s

Farming and

rd

manufacturing consumption Waste

curing

and distribution (consumers)

da

an

St

20

20

25

b.

Fe

25 2/18/2020 © SASBCurrent Tobacco Industry Standard addresses consumption

g

related ESG risks

tin

ee

Product

Product

M

Farming manufacturing

and

consumption Waste

and curing (consumers)

distribution

ard

Bo

s

rd

da

an

St

20

20

25

b.

Fe

26 2/18/2020 © SASBTobacco cultivation has recognized sustainability risks not

g

reflected in the standard

tin

ee

Product

Product

Farming manufacturing

M

and

consumption Waste

and curing (consumers)

distribution

a rd

Bo

Environmental Social

s

rd

da

Ecological impacts from Child labor, forced labor

an

agrochemical use

St

Agrochemical exposure

Deforestation

20

20

Green tobacco sickness

25

Source: Lecours N, Almeida GEG, Abdallah JM, et al. “Environmental health impacts of tobacco farming: a review of the literature.” Tobacco Control 2012;21:191-196; Boseley S. “Child labour

b.

rampant in tobacco industry.” The Guardian. June 25, 2018. https://www.theguardian.com/world/2018/jun/25/revealed-child-labor-rampant-in-tobacco-industry; U.S. OSHA “Recommended

Practices: Green Tobacco Sickness.” 2015. https://www.cdc.gov/niosh/docs/2015-104/pdfs/2015-104.pdf?id=10.26616/NIOSHPUB2015104

Fe

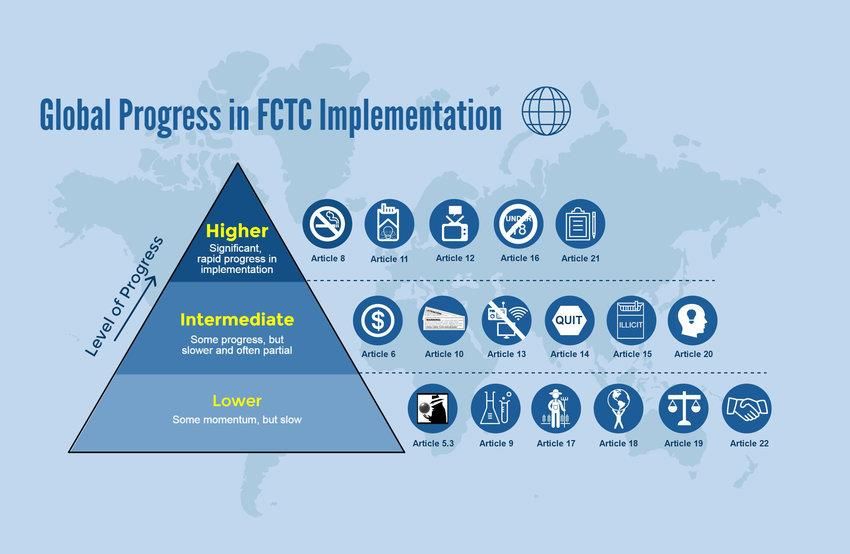

27 2/18/2020 © SASBGlobal tobacco treaty requires action on cultivation practices

g

tin

ee

The WHO Framework Convention on Tobacco Control (WHO FCTC)

M

is a global public health treaty adopted by 180+ parties covering over

90% of the world’s population; component of SDG 3.

ard

Bo

s

• ARTICLE 18 recognizes that Parties agree to have due regard to the protection of the

rd

environment and to health with respect to tobacco cultivation and

da

manufacture

an

• ARTICLE 17 requires Parties to promote, as appropriate, economically viable alternatives

St

for tobacco workers, growers, and possibly individual sellers.

20

20

25

b.

Fe

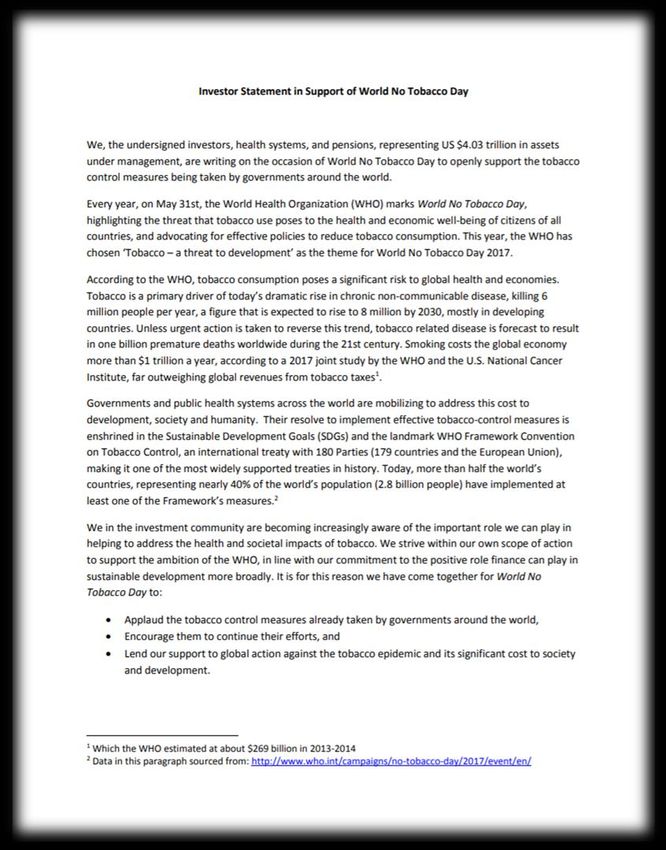

28 2/18/2020 © SASBGlobal investors recognize tobacco supply chain risks as a

g

material financial risk

tin

ee

M

May 31, 2017: Investor Statement in Support

of World No Tobacco Day

a rd

Undersigned investors, health systems, and

Bo

pensions, representing US $4.03T AUM

s

rd

da

Press Release

an

Managing director of the PRI, Fiona Reynolds,

St

added: “Aside from the obvious health issues,

20 investors are increasingly becoming aware of

the material financial risks around tobacco.

20

These include regulatory, litigation, and supply

chain risks.”

25

b.

Fe

29 2/18/2020 © SASBg

tin

ee

M

Historical Consideration of the Topic

rd

a

Bo

s

rd

da

an

St

20

20

25

b.

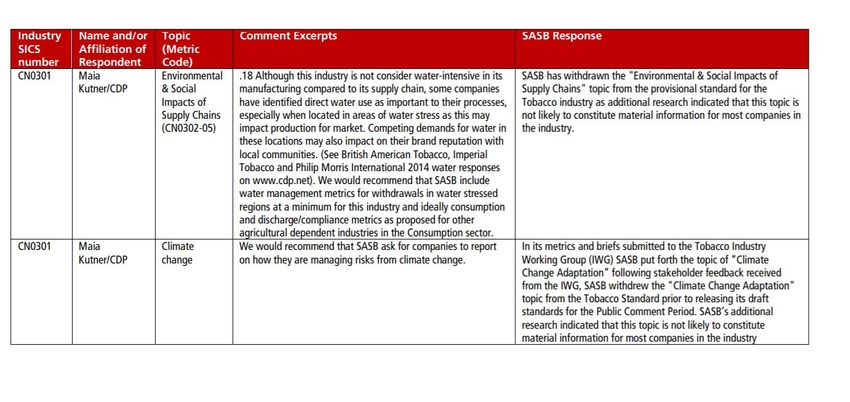

FeTopic withdrawn from Exposure Draft of the Provisional Standard

g

tin

Published January 2015

ee

Mid-2015 Response to

M

Public Comments

rd

“SASB has withdrawn the

a

Bo

‘Environmental & Social

Impacts of Supply

s

Chains’ topic from the

rd

provisional standard for the

da

Tobacco industry as

an

additional research

indicated that this topic is

St

not likely to constitute

20 material information for

most companies in the

20

industry.”

25

b.

Fe

31 2/18/2020 © SASBStakeholders expressed interest during consultations

g

tin

Input for revisions to the Provisional Standard

ee

December 2016 – Consultation with asset manager

M

• Companies should be disclosing broader social and environmental issues that are part of the

rd

tobacco supply chain.

a

• Forced labor, agricultural practices, green tobacco illness noted as topics for consideration

Bo

January 2017 – Consultation with Phillip Morris

s

rd

International

da

• All tobacco companies should demonstrate that they have assessed Environmental and

Social Impacts across their value chains

an

• Should disclose their most significant impacts and the corresponding measurement and

St

management approaches, including those due to labor practices in supply chains (e.g. child labor,

forced labor)

20

March 2017 – Consultation with investment analysts

20

broadly on agriculture industry

25

• “Origin and transparency” for any agricultural supply chain is a helpful, key theme for

investors.

b.

• Specifically noted issues of pesticide and changing climate and water stress for tobacco

Fe

32 2/18/2020 © SASBTopic proposed as Technical Agenda Item for Codified Standard

g

tin

Proposed May 2017

ee

M

a rd

Bo

“Add supply chain topic to the Tobacco industry standard. The

s

rd

suggested metrics for this topic relate to labor practices in

da

supply chains (e.g. child labor, forced labor), organizational

carbon footprint, and product waste”

an

St

20

20

25

b.

Fe

33 2/18/2020 © SASBStakeholders continue to express interest in the topic

g

tin

September 2017 – Deutsche Asset

ee

Management Tobacco Industry Report

January 2018 – Deutsche Asset Management Public Comment

to SASB

M

“There is a need to develop disclosures regarding social and

rd

environmental standards for tobacco cultivation and processing. This

a

was included in the provisional standards but not in the final exposure draft,

Bo

apparently as there was no clear evidence of company cost savings.”

Environmental and societal externalities are very large in the broad

s

agricultural sector and institutional investors have several engagement

rd

initiatives (including through PRI) asking companies to improve their

da

practices and policies. This shows investor interest, as the

environmental externalities of agricultural production have material

an

negative impacts on other aspects of an investors’ holdings.

St

As well, the UK Modern Slavery Act and California Transparency in Supply

Chains Act require investors (as listed companies) to publish steps taken to

20

ensure supply chains are free from slavery. Schroders (Aug 2016) concluded

that much tobacco production comes from countries with high modern slavery

20

risks plus MSCI 2015 found only 20% of listed tobacco companies have

programs to audit suppliers’ code of conduct compliance. This demonstrates

the need for improved disclosure of social practices in the tobacco

25

supply chain, including how companies address and manage Green

Tobacco Sickness

b.

Fe

34 2/18/2020 © SASBProject plan

g

tin

Staff Research & Market Consultation

ee

• Conduct market consultations to understand current perspectives on

M

the issue and the decision-usefulness of disclosures on this topic for

investors (Mission Alignment criterion)

rd

• Develop understanding of any evolving market and regulatory

a

perspectives on the issue

Bo

s

rd

da

Determine appropriate revisions for the

an

standard

• Determine appropriate GIC for topic and metrics

St

• If applicable, coordination with Human Capital Project

20

20

25

Staff resource: Food & Beverage analyst; support by associate analyst(s)

Estimated timeline: 6 months to one year to provide potential proposed revision to the Tobacco

b.

Industry Standard

Fe

35 2/18/2020 © SASBSupply Chain Management in the Tobacco Industry

g

tin

Recommendation / Discussion Questions

Standard-setting Project Proposal

ee

Problem Statement

M

Tobacco cultivation results in environmental and social externalities. Tobacco manufacturers monitor and

rd

engage with their suppliers on these issues, and investors have indicated interest in disclosures on

tobacco supply chain management. The Tobacco Industry Standard does not currently include any topics

a

Bo

or metrics on supply chain management and material sourcing.

s

Recommendation

rd

da

Staff seeks Standards Board approval of a standard-setting project to reevaluate adding supply chain

an

management and/or material sourcing topic(s) and metric(s) to the Tobacco Industry Standard.

St

20

20

25

b.

Fe

36 2/18/2020 © SASBAppendix

Fe

b.

25

20

20

St

an

da

rd

s

Bo

ard

M

ee

tin

gFragmented growers for a concentrated industry

g

tin

ee

Tobacco Growers Tobacco Manufacturers

M

rd

Small, independent tobacco farms, who

a

typically sell their crops to tobacco

Bo

merchants or to manufacturers under

s

contract

rd

da

an

Tobacco grown in 125+ countries

St

20 = 80%+ of total cigarette market share

20

25

b.

Fe

38 2/18/2020 © SASBPublic Comment on Exposure Draft to the Provisional Standards

g

tin

ee

M

rd

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

39 2/18/2020 © SASBPublic Comment on Exposure Draft to the Provisional Standards

g

(Contd.)

tin

ee

M

rd

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

40 2/18/2020 © SASBTobacco manufacturers have direct impact on growers

g

tin

ee

M

PMI: direct contracts with 21,000 tobacco farmers; 20 third-party suppliers representing 329,000

rd

farmers

a

Bo

BAT: 68% from 18 BAT leaf operations, which source from over 90,000 farmers; 32% from 20+

third-party suppliers, which source from over 260,000 farmers

s

rd

da

----

an

Good Agricultural Practices (GAP) programs commonplace in industry

St

20

20

25

b.

Fe

41 2/18/2020 © SASBTobacco manufacturers are managing and disclosing this topic

g

tin

ee

M

rd

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

42 2/18/2020 © SASBProgress on WHO FCTC article implementation has varied

g

tin

ee

M

rd

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

43 2/18/2020 © SASBFe

b.

25

20

20

St

Break until 12:45pm PT

an

da

rd

s

Bo

ard

M

ee

tin

gg

tin

ee

M

Research Project Proposals

rd

a

Bo

s

• Alternative Meat & Dairy

rd

da

an

St

20

20

25

b.

FeFe

b.

25

20

20

St

an

da

Alternative Meat and Dairy

rd

s

Bo

ard

M

ee

tin

gAlternative Meat and Dairy

g

tin

Executive Summary Research Project Proposal

ee

Problem Statement

Alternative meat and dairy products are growing as consumer demand for products with reduced environmental

M

impact increases & companies are adapting to this changing consumer preference. Alternative meat and dairy

rd

products are not currently addressed in the SASB Standards.

a

Proposed Project Scope & Anticipated Course of Action

Bo

Seeking approval to initiate a Research Project to establish an evidence-based view of the following:

s

1) The relevance of this trend for each of the Food and Beverage SICS industries

rd

2) How consumer demand for alternative meat and dairy products fits within the SASB’s General Issue

da

Categories within the Food and Beverage Sector

3) Whether to proceed to standard setting

an

St

20

Criteria for Standard-Setting Project

Mission Alignment - Is there an opportunity to significantly improve communication by companies to investors of

20

decision-useful sustainability information?

Scope / Prevalence – Is the issue pervasive, including scope of industries or geographies impacted?

25

Capacity – Does Staff (and the Board) have sufficient capacity to formally address the issue; and does the issue warrant

prioritization of resources over alternatives.

b.

Feasibility: What is the likelihood that there would be a proposed solution to put to the Board in a timely fashion.

Fe

47 2/18/2020 © SASBResearch Agenda Prioritization

g

tin

ee

1. Governance Documents

M

2. Thematic Issue – materiality

a rd

3. Thematic Issue – measurement

Bo

4. Industry Standard: reevaluating existing content – materiality

s

rd

5. Industry Standard: reevaluating existing content – measurement

da

6. Industry Standard: evaluating new or emerging issues

an

7. Industry scope and structure issues, including new industry standards

St

8. Globalization 20

20

9. Technical Protocol Issues

25

10. Standards Application Guidance

b.

11. Alignment

Fe

48 2/18/2020 © SASBAgenda

g

tin

ee

1) Evidence: Emerging Issue, Alignment with TCFD, Investor Interest, Standards Advisory Group Input

M

2) SASB Standards

rd

3) Proposed Project Overview

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

49 2/18/2020 © SASBEvidence

Fe

b.

25

20

20

St

an

da

rd

s

Bo

ard

M

ee

tin

gOverview of Alternative Meat and Dairy Products

g

tin

Consumer Demand

ee

Eating more plant-based foods and beverages for:

65% of Global Consumers 1) Health

M

2) Animal Welfare

rd

3) Environment

a

Bo

Products Reduced Environmental Impacts of Alternative Meat & Milk

s

rd

Impact Reduced Impact Reduced Impact

Plant Based (Meat) (Milk)

da

Land Use 47% - 99% 90-95%

an

Fermented

St

GHG Emissions 36% - 90% 75-90%

Cell Culture

20

Water Use 72% - 99% 45% - 90%

20

25

b.

Sources: FAIRR, “Appetite for Disruption”; FoodDive ,“Plant-based Eating Makes Consumers Feel Healthier, Study Says”; BBC “Climate Change: Which Vegan Milk is Best?”; Good Food

Institute “Plant-Based meat for a Growing World”

Fe

51 2/18/2020 © SASBConsumer Demand is Driving Growth for Alternative Meat

g

tin

European Plant Protein

ee

Market to reach $2.6B in

M

U.S. Grocery Store Sales of 2024 with a CAGR of 7.5%

Meat Substitutes $750M

rd

2019 → $7.2B by 2025

a

Bo

s

rd

da

14% of U.S.

an

Consumers

St

regularly use plant-

based alternatives,

86% of which are 20 Current CAGR 2029

NOT vegan or (2018/2019) (Next 5 years) (estimated)

20

vegetarian Global Plant-Based Meat Market $12.1B $140B

12%

25

Global Meat Market $945.7B 3.1% $1.4T

Sources: FAIRR, “Appetite for Disruption” MarketWatch, “Meat Market 2020 to Showing Impressive Growth by 2024 | Industry Trends, Share, Size, Top Key Players Analysis and Forecast

b.

Research”; Mordor Intelligence, “Europe Plant Protein Market – Growth, Trends and Forecast (2020-2025); Mordor Intelligence, “Protein Alternatives Market – Growth, Trends and Forecast

(2020-2025); PR Newswire “ Meat Substitutes Market Worth $3.5 Billion by 2026 - Exclusive Report by MarketsandMarkets; UK Investment Guides “Barclays Analysts Predict x10 Growth Of

Fe

Alternative Meat Market”

52 2/18/2020 © SASBConsumer Demand Drove Growth in Alternative Dairy Industry

g

tin

ee

M

Industry Example

a rd

U.S. Markets Percent Change in Sales Market Value

Bo

(2012-2017) (2017)

Alternative Milk 61% $2.11B

s

rd

Traditional Milk 15% $16.12B

da

an

St

20

20

25

b.

Sources: Bloomberg Terminal, Danone, Dean Foods, FAIRR “Plant-Based Profits: Investment Risks & Opportunities in Sustainable Food Systems”; Food Dive “Non-Dairy Milk Sales Surge as

Fe

Shoppers Sour on the Popular Cow-Based Alternative”

53 2/18/2020 © SASBCompanies are Acting Based on This Trend

g

tin

SASB Industries Companies Acting Based on Changing Consumer Demand

ee

Agricultural Products

M

Alcoholic Beverages

rd

a

Food Retailers & Distributors

Bo

s

rd

Meat, Poultry & Dairy

da

an

Non-Alcoholic Beverages

St

Processed Foods

20

20

25

Restaurants

b.

Tobacco

Fe

54 2/18/2020 © SASBAlignment With TCFD

g

tin

ee

M

rd

TCFD Implementation Recommendations for Agriculture, Food & Forest Products Group

a

1) Increasing efficiency by lowering level of carbon and water intensity per unit

Bo

2) Reducing inputs and residual waste

3) Developing new products and services with lower carbon and water intensity

s

rd

da

an

St

20

20

25

b.

Sources: FAIRR, “Appetite for Disruption”; FoodDive ,“Plant-based Eating Makes Consumers Feel Healthier, Study Says”

Fe

55 2/18/2020 © SASBThere is Evidence of Investor Interest in Alternative Meat

g

tin

ee

“KFC and the Beyond Nuggets and the extent to which you view this as sort of sustainable versus a short-

M

term be a very healthy lift but maybe less of the core part of the menu.”

rd

- Sara Senatore, AllianceBernstein, Yum Q3 2019 Earnings Call

a

Bo

“You guys started to test out the beyond plant-based burger in Canada. I'm wondering as the quarter

s

unfold, did you , I think that not having a meatless burger was a headwind to your sales. How are you

rd

thinking about that opportunity here.”

da

- Katherine Fogertey, Goldman Sachs, McDonalds Q3 2019 Earnings Call

an

St

“I wanted to follow up on Happy Little Plants launch that you guys discussed at the Analyst Day. I was curious

what type of retailer and foodservice interest you're seeing so far? And how you guys are thinking about the

20

contribution from this launch this year?”

20

- Rupesh Parikh, Oppenheimer & Co., Hormel Foods Corp Q4 2019 Earnings Call

25

b.

Fe

56 2/18/2020 © SASBInvestor Interest Has Grown Since 2016

g

tin

FAIRR, is a non-profit whose “mission is to build a global network of investors who are focused and engaged on

the risks linked to intensive animal production within the broader food system. FAIRR helps investors to exercise

ee

their influence as responsible stewards of capital to engage and safeguard the long-term value of their investment

M

portfolios..

rd

Phase 1: 16 global retailers/manufacturers & 36

a

Investors with $1.25T AUM

Bo

s

Phase 2: 16 global retailers/manufacturers &

rd

57 Investors with $2.3T AUM

da

an

Phase 3: 25 global retailer/manufacturers & 74

St

investors with $5.3T AUM

20

20

Phase 4: 25 global retailers/manufacturers & 88

investors with $11.2T in AUM

25

b.

Sources: FAIRR, “Appetite for Disruption”

Fe

57 2/18/2020 © SASBStandards Advisory Group Preliminary Engagement

g

tin

ee

Stakeholder Feedback

M

View that company strategy around this

rd

Food and Beverage Analyst trend could help mitigate risks and

a

create opportunities to capture market

Bo

share

s

Restaurant This trend was not a priority

Standards Advisory

rd

Group Workshop

da

(December 2019) Willing to engage with SASB on this

an

Industry Group trend (changing viewpoint from the

workshop)

St

20 Actively working with investors in this

20

Non-profit space & interested in engaging with

SASB

25

b.

Fe

58 2/18/2020 © SASBFe

b.

25

SASB Standards

20

20

St

an

da

rd

s

Bo

ard

M

ee

tin

gIndustry Standards Do Not Include Environmental Impacts of

g

Alternative Meat and Dairy Products Environmental

tin

Impacts of Alternative

SASB Industry Health/Nutrition Animal Welfare

ee

Products

Agricultural Products

M

rd

Alcoholic Beverages

a

Food Retailers & Disclosure Topic: Animal Care & Welfare

Bo

Distributors

Meat, Poultry & Dairy Disclosure Topic: Animal Care & Welfare

s

Disclosure Topic: Antibiotic Use in Animal

rd

Production

da

Non-Alcoholic Disclosure Topic: Health &

an

Beverages Nutrition

St

Processed Foods Disclosure Topic: Health &

Nutrition

20

20

Restaurants Disclosure Topic: Supply Chain

Management & Food Sourcing

25

Tobacco Disclosure Topic: Public Health

b.

Fe

60 2/18/2020 © SASBCompanies in Five Industries Have Strategies Related to

g

Environmental

Alternative Meat and Dairy Products

tin

Impacts of

SASB Industry Health/Nutrition Animal Welfare

ee

Alternative Products

Agricultural Products

M

rd

Alcoholic Beverages

a

Food Retailers & Disclosure Topic: Animal Care & Welfare

Bo

Distributors

Meat, Poultry & Dairy Disclosure Topic: Animal Care & Welfare

s

Disclosure Topic: Antibiotic Use in Animal

rd

Production

da

Non-Alcoholic Disclosure Topic: Health &

an

Beverages Nutrition

St

Processed Foods Disclosure Topic: Health &

Nutrition

20

20

Restaurants Disclosure Topic: Supply Chain Management &

Food Sourcing

25

Tobacco Disclosure Topic: Public Health

b.

Fe

61 2/18/2020 © SASBFe

b.

25

20

20

St

an

da

rd

Research Project Objectives

s

Bo

ard

M

ee

tin

gObjectives of a Research Project is to Answer Questions Related

g

to Scope of SASB Industries

tin

ee

Standard-Setting Criteria

M

Mission Alignment: Investors find this topic relevant

rd

Scope / Prevalence:

1) The relevance of this trend for each of the Food and Beverage SICS industries

a

2) How consumer demand for alternative meat and dairy products fits within the SASB’s General Issue Categories within the

Bo

Food and Beverage Sector

3) Whether to proceed to standard setting

s

rd

Capacity: Lead Analyst and Associate Analyst within the Food & Beverage Sector

da

Feasibility: SASB estimates that this research project will take between 9-12 months

an

St

Expected Outcomes

20

20

Identify applicable SICs industries and potential disclosure topics

25

Understand how this topic fits into SASB General Issue Categories

b.

Recommendation for Standard-Setting Project(s)

Fe

63 2/18/2020 © SASBAlternative Meat and Dairy

g

tin

Recommendation / Discussion Questions

Research Project Proposal

ee

Problem Statement

M

Alternative meat and dairy products are growing as consumer demand for products with reduced environmental

impact increases & companies are adapting to this changing consumer preference. Alternative meat and dairy

rd

products are not currently addressed in the SASB Standards.

a

Bo

Recommendation / Discussion Questions

s

SASB Staff recommends approval of a research project on this subject.

rd

da

1) Do you agree that the scope/prevalence as it relates to the SASB industries is the right focus area for this project?

an

• Defining the issue through the lens of industries and general issue categories

St

2) Do you agree that this should move forward as a Research Project?

20

20

25

b.

Fe

64 2/18/2020 © SASBAppendix

Fe

b.

25

20

20

St

an

da

rd

s

Bo

ard

M

ee

tin

gThis Issue Arose to Our Attention with the Increase in Media

g

Coverage of the Alternative Meat Industry

tin

ee

M

a rd

Bo

s

- NewsWeek

rd

da

an

- FoodDive

19. Beyond Meat

St

The terrifying images of the burning Amazon forests in 2019 marked

20 another setback in the battle to slow global warming and insatiable

demand for beef was blamed as a root cause of the fires…As

20

alternative proteins become ubiquitous, 2020 should be the year

diners can casually pair combating climate change with tasty

25

meals. - Financial Times

b.

Sources: Financial Times, “20 things to Watch in 2020”; FoodDive, “Disruptor of the Year: Beyond Meat”; NewsWeek, “Burger King Launches Three New Plant-Based Burgers Following

Impossible Whopper Success”; Starbucks, “Starbucks Commits to a Resource-Positive Future”

Fe

66 2/18/2020 © SASBRemaining Status Quo Can Increase Risk to Companies

g

Environmental/Supply Chain Risk

tin

ee

Industry Risk Effect

Meat, Poultry & Dairy & all downstream industries Restaurants putting downward pressure If JBS, a leading processor of beef, and other customers of

M

on meat, poultry & dairy producers → McDonald’s do not change practices, they could lose

McDonalds has committed to source business affecting revenue & their ability to operate

rd

deforestation-free beef

Meat, Poultry & Dairy & all downstream industries Increased GHG Emissions from Increase cost of revenue, cost of capital & capex (?)

a

production

Bo

Volatility in Supply & Price Risk

s

rd

Industry Risk Effect

da

Meat, Poultry & Dairy & all downstream industries African Swine Hormel Foods, which produces Spam, said on Thursday that African swine fever

Fever in China drove up pork costs, weighing on its quarterly earnings and contributing

an

to a cut in its full-year earnings and sales outlook.”

St

Pork prices are high, affecting restaurants bottom lines

Meat, Poultry & Dairy & all downstream industries Droughts, Floods Australia lost $72M and 43,000 cattle. Supply could decrease, profits could

Meat, Poultry & Dairy & all downstream industries

20 & Storms

Droughts &

decrease, prices to restaurants could increase

Feed costs are volatile and could be higher with flooding impacting grain supply

20

Floods for Egg producers

Restaurants; Food Retailers & Distributors; Process Poor management Lose market share (?) , reputation risk (?)

25

Foods of ESG impacts in

supply chain

b.

Sources: Financial Times, US Food and Restaurant Chains Hit by Rising Pork Prices; Bloomberg “Climate Change is Already Costing Meat and Dairy Producers a Lot” , Harvard Business

Review “A Look Inside the World’s Largest Beef Producer: Is JBS Slaughtering Cows – or the Environment?”

Fe

67 2/18/2020 © SASBAlternative Proteins and Milk Provide an Opportunity to Lessen

g

Environmental Impacts

tin

ee

Alternative vs. Conventional Meat Alternative vs. Conventional Milk

M

a rd

Bo

s

rd

da

an

St

20

20

25

b.

Sources: BBC, “Climate Change, Which Vegan Milk is Best”; Good Food Institute, “Plant-Based Meat for a Growing World”

Fe

68 2/18/2020 © SASBGrowth of Plant – Based Categories Exceeds Animal Based

g

Categories in 2019

tin

ee

Globally, meat substitutes share of

Dollar sales growth (%) in plant-based categories total meat/seafood purchases

M

compared to animal-based categories, year ending

April 2019

rd

a

Bo

s

rd

da

an

St

20

20

25

b.

Fe

69 2/18/2020 © SASBThe Meat & Poultry Industry

g

tin

Company Activity Impact

ee

Created own plant-based protein products

Investment

M

a rd

Bo

s

Disrupter IPO outperformed Uber & Lyft’s IPO, annual revenues expected to

rd

grow form $16M in 2016 to $200M by end of 2019

da

an

St

Founded in 2016, is now available in 17,000 restaurants including

Disrupter Burger King, and launched in U.S. Grocery Stores

20

20

September 2019, announced creation of Happy Little Plants, a

25

Creator plant-based food product line, already seeing interest from

retailers

b.

Sources: FAIRR. “Appetite for Disruption.” 2019. Greenbiz. “Rebekah Moses of Impossible Foods says it products are a climate mitigation tool.” 2019.

Fe

70 2/18/2020 © SASBProcessed Food Companies

g

Company

tin

Activity Impact

ee

Created own product line, Incogmeto, in 2019 to be

M

Investor launched in 2020.

a rd

Incubator 301 Inc. Invested in Beyond Meat and Kite Hill, a

Investor

Bo

plant-based dairy company.

s

rd

“To take the lead on this urgent issue [climate change], we’re

da

transforming our business to reduce GHG emissions, end

Creator

deforestation, reduce food loss and waste, improve soil health

an

and move toward offering more plant-based proteins.”

St

“By promoting plant-based alternatives and committing to

Creator and Investor sourcing 100% of our agricultural raw materials

20 sustainably, we will reduce our environmental impact and

provide people with more choice.”

20

Acquired Gardin which has 11% market share in

25

alternative meat industry and Pinnacle Foods which

Acquired

helped raise net sales by 35.7% and led to best single-

b.

day gain in share prices since 1989.

Sources: FAIRR. “Appetite for Disruption.” 2019.;Nestle. “Climate change leadership.”; “ Unilever. “More plant-based options.”

Fe

71 2/18/2020 © SASBFood Retailers

g

Company

tin

Activity Impact

ee

“The biggest impact we can make as individuals, for our health but also

that of the planet, is to eat more plants. At Tesco we’re making that easier

M

than ever by providing the widest and best range of plant-based options

available on the UK high street. We’ve turbo charged our innovative

rd

Creator

original Wicked Kitchen snacks and meals. For those looking for everyday

a

delicious meal swaps, we’re launching the exciting Tesco Plant Chef

Bo

range. To make these foods easier to find we will be launching dedicated

plant-based and vegetarian zones in stores.

s

rd

Launched a vegan sausage roll & total sales rose by 7.2% year-

da

on-year in 2018 to £1.03 billion, compared with £960 million in

Creator the previous year. Since the launch, the company’s share price

an

has enjoyed a record high, trading at £24 in July 2019 (vs. £10

same time last year)

St

20

Creator Created their own alternative protein line

20

25

b.

Sources: Tesco. “Tesco launches affordable new range of plant-based family favourites to cater for UK’s biggest food Trend.”, FAIRR. “Appetite for Disruption.” 2019.

Fe

72 2/18/2020 © SASBRestaurants

g

Company

tin

Activity Impact

ee

Seller Started selling the impossible whopper → Q3 2019 was the

strongest quarterly same-store sales growth since 2015. For a

M

store in St. Louis, sales increased by 28% and the number of

unique customers grew by 15% in 5 weeks in April 2019.

a rd

Bo

Started selling Impossible Sliders -> 4% increase in same-store

Seller

s

sales growth in 2 months

rd

da

an

“Our aspiration is to become resource positive – storing

more carbon than we emit, eliminating waste, and

Seller

St

providing more clean freshwater than we use…we will

expand plant-based options, migrating toward a more

20 environmentally friendly menu.”

20

First national fast food chain to introduce plant-based

chicken potions. KFC sold the equivalent of a week’s

25

Seller worth of popcorn chicken in beyond chicken nuggets

and wings in a day compared

b.

Sources: Restaurant Business. “Burger King St. Louis Sales Surged, Thanks to Impossible Whopper.”; CNBC, “Shares of Burger King’s Parent Fall after Tim Hortons’ Performance; Starbucks.

“Starbucks Commits to a Resource Positive Future.; Disappoints.”; Los Angeles Times, “Beyond Meat tests plant-based fried chicken in KFC trial.”

Fe

73 2/18/2020 © SASBNon-Alcoholic Beverages

g

Company

tin

Activity Impact

ee

Bought WhiteWave (producer of Silk) in 2016 after WhiteWave

Acquisition

M

had 19% CAGR from 2012-2015

a rd

Bo

Bought AdeS plant-based beverages from Unilever in 2017

s

Acquisition

Coca-Cola to expand offerings in Latin America

rd

da

an

Acquired Health Warriors, a plant-based protein bar company in

2018; created an accelerator program and collaborates with

St

Acquisition & Investment

Sophie’s Kitchen (a plant-based seafood company) and Torri Labs

20 (a plant-based beverage company)

20

Raised $225M in its most recent round of funding in 2019-2020.

25

R&D

Provides alternative milk to Starbucks

b.

Sources: Food Dive “Non-Dairy Milk Sales Surge as Shoppers Sour on the Popular Cow-Based Alternative”; Coca-Cola. “Coca-Cola Closes Acquisition of Ades Plant-Based Beverages.” Forbes, “PepsiCo

Continues Health Kick, Reveals First Startups For Its Accelerator Program.” PepsiCo. “Meet the Inaugural Class of PepsiCo's Nutrition Greenhouse North America.”; TechCrunch, “Plant-based milk substitute

Fe

market gets frothy with $225 million for Califia Farms.”

74 2/18/2020 © SASBFe

b.

25

Agenda Planning

20

20

St

an

da

rd

s

Bo

ard

M

ee

tin

gProject Pipeline – 2020 Project Timelines

g

tin

2020 Standards Board Meetings Q1

ee

Q32019 Q42019 Q1 Q2 Q3 Q4 2021

M

SR

rd

Tailings

a

Tobacco Supply Chain

Bo

Raw Material Sourcing

s

Content Moderation

rd

da

Plastics

Alternative Meat and Dairy

an

St

Human Capital

Rules of Procedure

20

20

Conceptual Framework

25

Standard- Staff Update

Research Project Other projects Board Decision Proposed Projects

b.

Setting Project (Optional)

Fe

Note: One or more standard setting projects may be proposed upon completion of a 2/18/2020 © SASB

research project.Standard-Setting Process Overview

g

tin

ee

M

rd

a

Bo

s

rd

da

an

St

Project screening – input from:

20

20

• Market & public engagement

• Standards Advisory Group

25

• Standards Board

• Staff research

b.

Fe

77 2/18/2020 © SASBExample Issues in Project Screening Stage*

g

tin

• Climate transition risk in Extractives, Transportation, and Infrastructure sectors

ee

• Climate physical risk in Extractives and Infrastructure sectors

M

• Climate risk and opportunity in bank loan portfolios

rd

• Scenario analysis metrics in Extractives sector

a

• Biodiversity metrics in Oil & Gas - Midstream industry

Bo

• GHG emissions in Multiline Retail and/or E-Commerce industries

s

• Aquaculture or fishing industry standard development

rd

• Data security metrics

da

• Customer privacy metrics

an

• Responsible use of AI and Big Data in technology

St

• E-Commerce industry structure

20

• Commercial Banks, Consumer Finance, and Investment Banks industry structure

20

• Apparel and textile manufacturing industry structure

• Access and affordability in Biotechnology & Pharmaceuticals industry

25

*Issues represent those in a staff preliminary research phase with no stated timeline on when, or if, such issues will develop into research and/or

b.

standard-setting projects or activities. SASB is receptive to unsolicited input from the public on these issues or any other issues in the SASB standards.

Fe

78 2/18/2020 © SASB2020 Standards Board Meetings*

g

tin

• June 22nd & 23rd

ee

M

• September 17th & 18th

rd

• December – TBD

a

Bo

Standards Board Meeting Calendar & Archive page contains full details of meeting dates and registration

s

rd

links to access live stream of the public meetings. Recordings and a summary of meeting outcomes are

da

available shortly after each meeting.

an

St

20

20

25

*Dates are tentative. Public Standards Board meetings are announced a minimum of 10 days prior to the meeting date.

b.

Fe

79 2/18/2020 © SASBg

tin

ee

M

a rd

Bo

s

rd

da

an

St

20

20

25

b.

Fe

80 2/18/2020 © 2014 SASB™ CONFIDENTIAL & PROPRIETARYYou can also read