Symphony Ltd - It's going to be a 'HOT' summer - MarketsMojo

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Initiating Coverage

Symphony Ltd

It’s going to be a ‘HOT’ summer…

27 FEB 2019

27 FEB 2019 Company Report

BUY

Target Price: Rs 1,680

CMP : Rs. 1230

Potential Upside : 37%

MARKET DATA

No. of Shares : 7 Cr.

Market Cap : Rs. 8,605 Cr.

Symphony Ltd

Avg. daily vol. (6mth) : 14,797

52-w High / Low : Rs. 1992/812

Bloomberg : SYML IN

Promoter holding : 75%

Consumer Durables : N.A.

FII

It’s going to be a ‘HOT’ summer… Price performance

140

90

40

Feb-18 Jun-18 Oct-18 Feb-19

Sensex Symphony

Financial Summary Shareholding pattern

Y/E Net Sales PAT EPS Change P/E RoE RoCE DPS Q-o-Q Chg

Dec.-18

March (Rs Cr) (Rs Cr) (Rs) (%) (x) (%) (%) (Rs) (%)

FY17 765 166 23.8 40.5 - 39.6 58.1 8.0 Promoters 75.00 0.00

FY18 798 193 27.5 15.8 - 34.6 48.7 2.7 FPIs 6.20 0.02

FY19E 920 157 22.4 (18.5) 57.4 21.7 29.3 2.7 MFs / UTI 8.94 0.27

FY20E 1,145 225 32.1 43.2 39.5 25.3 32.6 3.5 Banks / FIs 0.01 (0.29)

FY21E 1,289 261 37.3 16.2 33.9 23.5 31.0 4.0 Others 9.85 0.00

Source: Company, Axis Securities CMP as on Feb 27, 2019

Pankaj Bobade – AGM - Research (Head)| pankaj.bobade@axissecurities.in | (+91 22 4267 1736)

27 FEB 2019 Company Report

Symphony Ltd

Investment Rationale Sector: Consumer Durables

Symphony Ltd, has established itself as the leading player par excellence in the evaporative air-cooling technology to

become world’s largest air-cooler manufacturer. The company offers wide range of air-coolers across residential, industrial

and commercial segment. Symphony Ltd has carved a niche for itself in the air-coolers market by offering various designs

along with innovative features to fit the pockets of variety of consumers and pander to their changing tastes. Having gone

almost bankrupt, Symphony Ltd emerged like a phoenix in the air-coolers market to become a global leader with ‘one

product, many markets’ theme and acquiring companies in Mexico, China and Australia to expand its footprint overseas

and into the industrial and commercial air-cooling market. It currently commands ~50% market share by value and

upwards of 40% by volume in the organized domestic air-coolers market.

Rising per capita income to enable improving demand for consumer durable goods

Symphony

would be Increasing electricity penetration and rise in power availability esp. in rural India

big beneficiary

of rising temperature

across globe due to Under penetration of coolers coupled with hot summers offers untapped opportunity

global warming and

changing

weather Temperature variations is a global phenomenon making cooling solutions a necessity

patterns

Industrial and commercial cooling opens up a big business opportunity

We initiate coverage with BUY rating and a target price of Rs. 1,680 i.e. 37% upside.

3

27 FEB 2019 Company Report

Symphony Ltd

Investment Rationale Sector: Consumer Durables

Air coolers- middle class Changing weather, global warming Technological innovations, under-

household’s solace in summers necessitates cooling solutions Symphony

penetrationdifferentiates itself

to drive growth

India being a sub-tropical country, the

One of the most immediate and obvious Technological innovations differentiates the

summers witnesses scorching heat. Air

effects of global warming is the increase in products; air coolers with smart looks,

coolers have proved to be one of the

temperatures around the world. The feather-touch digital control panels, remotes,

superior alternatives to Air Conditioners

average global temperature has increased auto swings, alarms and other intelligent

(ACs); air coolers provide Natural or

by about 1.4 degrees Fahrenheit (0.8 features are gaining popularity over the run-

Evaporative Cooling and score over ACs in

degrees Celsius) over the past 100 years, of-the-mill products from unorganized

terms of lower life-cycle cost and enhanced

according to the National Oceanic and segment. The air cooler market in India is

flexibility. Being a low initial cost product

Atmospheric Administration (NOAA). dominated by unorganized segment; current

(about half the price of a 1 Ton window

Rising temperatures, coupled with heavy size of market is estimated to be 80 lakh

AC to cater to a approx. 200sqft room,

urbanization and delayed and/or short units per annum growing at high single digit

with a 10ft ceiling height), the Air Cooler is

monsoons, make summers unbearable to low double digit; 30% of the market is

quite popular in the hot, dry parts of the

calling for effective cooling solutions viz. catered by organized segment, balance by

country. To top it, the running cost is only a

air coolers which are within the reach of unorganized players. Improving power

small fraction of the power-guzzling ACs

the general population. With rising availability, rising prosperity and increasing

and since there is no refrigerant to leak or

mercury, the demand for air coolers rise environmental consciousness is likely to

compressor to burn out, the maintenance

especially in the hot dry parts of the generate attractive air cooler market growth

cost is also very low. The lower cost of

country during the months of April, May over the foreseeable future; organized

ownership and constrained power supply

and June before the rainy season arrives. segment is expected to grow faster than the

situation in India, air coolers are in high

unorganized segment.

demand in India.

4

27 FEB 2019 Company Report

Symphony Ltd

Investment Rationale Sector: Consumer Durables

Focused player, asset light business Centralized Air cooling- offers Beating seasonality Rising

in the exports

business

model backed by strong brand enormous prospects opportunity

by diversifying across borders

With acquisition of Climate Technologies

Having learnt hard lessons from rampant In order to tackle seasonality in the

Pte., Australia, Symphony has widened its

diversification of product basket way back in business, the company is now focusing on

international footprint sticking to its ‘one

2004, Symphony management has now industrial/ commercial segment by offering

product, many markets’ moto. The

directed all its focus on single product viz., cooling solutions. With acquisition of

Australian acquisition not only provides

air coolers. Today, Symphony is the largest IMPCO, Mexico in 2009, Symphony got

Symphony Ltd. access to new geographies

air cooler company in India with ~50% foothold in the industrial cooling systems

viz., Australia and USA (one of the largest

market share of organized market in value and entry into lucrative USA and Latin

air cooling market is the world) but also an

terms and upwards of 40% in volume terms. American market. Acquisition of M Keruilai

opportunity of moderating its business risks

‘Symphony’ ranks amongst top trusted brands Air Treatment Equipments (Guangdong),

because of complimentary weather

in air cooling segment and has become a China (now known as GSK, China) was

conditions prevailing in India and Australia

generic name for air coolers. It outsources another step in the same direction. Both the

along with the presence of Climate

100% of its production to around 9 OEMs, companies are pioneers in evaporative

Technologies in both cooling as well as

thus following an asset light business model. cooling systems and boast of a strong R&D

heating segment. Climate Technologies

The outsourcing model enables the team. The usage of cooling improves

gets immediate access to Symphony’s

management to focus on innovation, design productivity at work place; the

international distribution network across 60

& development, marketing along with brand development of commercial real estate in

countries. Going forward, we expect the

building. No wonder the company enjoys cities and rise in industrialization has

synergies to drive the top line and bottom

excellent capital efficiency, the return on offered an enormous opportunity for

line growth for the consolidated entity.

capital employed (RoCE) has been 45% plus centralized cooling/ industrial cooling.

for last 10 years.

5

15 Feb 2019 Company Report

Symphony Ltd

Industry wide demand drivers Sector: Consumer Durables

Increasing middle class population Increasing per capita income

4,000

80

69 3,000

70

2,000

60

52

1,000

1,482

1,486

1,610

1,639

1,749

1,976

2,016

2,188

2,380

2,585

2,803

3,040

50

0

40

FY16

FY12

FY13

FY14

FY15

FY17

FY18

FY19E

FY20E

FY21E

FY22E

FY23E

2012 2020

Middle ClassPopulation (%) India Per Capita Income USD

Air coolers Penetration vs. Other Consumer Durables It is estimated that affluent middle class will constitute 69% of the

total population by 2020 and 64% will be living in urban clusters.

100%

85% 89% India’s per capita income was $1482 in FY2012 which has

crossed $2000 in FY18 and is expected to increase to almost

80% 70%

60% $3000 by FY23. Increasing per capita income will lead to higher

60% spends on aspirational goods including consumer durables.

Air-coolers penetration, being a seasonal product, is very low

40% 30% compared to other consumer durable goods. But the sweltering

25%

20% 17%

20% 10% heat witnessed in hot summer necessitates the need for cooling,

4% making air-cooler an essential consumer good.

0% Low initial investment and variable cost makes air-coolers a better

Room AC Refrigerator Washing FPD TV Air Cooler alternative to other cooling appliance viz., air-conditioning units

Machine Government’s push of electricity for all is expected to provide an

impetus for increasing demand for consumer durables in rural and

India Global

semi-urban areas

Source: Company, IMF, Axis Securities, Amber Enterprises RHP

6

27 FEB 2019 Company Report

Symphony Ltd

Industry wide demand drivers (cont.d) Sector: Consumer Durables

Untapped opportunities:

Rising temperature

Increased electrification:

Rising per capita income: Rising temperature has necessitates cooling

Power has reached every

Export opportunity:

made coolers a necessity in solutions:

The per capita income,

village & household in the summer; nearly 55% of the High temperatures in

which is the crude indicator India has been witnessing

country. Densely populated population lives in hot and summer is not restricted to

of prosperity of a country rise in summer temperature

states viz., Bihar, UP, MP dry climatic conditions. Not India, it has been a global

has been reported at USD making application of

etc have been beneficiaries more than 15% of the phenomenon. The

1964 and is expected to cooling solution a must.

of the electrification. Rising households own cooler thus developed, developing &

cross $2000 in 2018. Cost effective cooling

purchasing power coupled making it an enviable under-developed nations

Study has shown that the solutions viz., air coolers

with electrification is growth opportunity. demand low cost (both

discretionary spends rise becomes the first choice for

expected to drive the Moreover, a large part of investment and variable)

sharply as the per capita consumers given the

demand for consumer market (~70%) is still solutions to beat the heat.

income crosses $2000. seasonal need in 3 months

durable goods like coolers. dominated by unorganized

of summers

segment.

Residential cooling dominates (FY18) Having established ‘Symphony’ as a synonym to cooling, Symphony Ltd has now targeted the

business opportunities outside the residential space into commercial and industrial cooling.

Residential Prior to acquisitions of Mexico, China and Australia, Symphony Ltd was exclusively a cooling

Air product company focused on domestic sales and exports of coolers. With these acquisitions, the

Cooler, company has progressively evolved into cooling technology company with product agnostic

92% approach.

Currently, the residential air-coolers segment account for lion’s share in the revenues; going

Industrial

forward, the share of commercial and industrial cooling segment is expected to increase

& Ducted,

Low investment cost (40% of the cost required for centralized air-conditioning) and maintenance cost

8% along with low power consumption (almost 1/10th compared to A/Cs) by Industrial air coolers

makes them most sought after cooling solutions for commercial applications, thus offering immense

business opportunity

As per management, the industrial and commercial air-cooling business opportunity is likely to be

Residential Air Cooler Industrial & Ducted more or less at par with the residential cooling segment as far as margins is concerned, though the

Source: Axis Securities, Company opportunity is huge and more essentially, untapped.

7

27 FEB 2019 Company Report

Symphony Ltd

Air cooling Industry Sector: Consumer Durables

Bargaining Power of Buyers (High)

Symphony offers products

The brand ‘Symphony’ has an

There are multiple brands across different across price points & various features,

price points, thus giving the consumer a wide offering the consumer a wide choice;

excellent brand recall, thus creating

variety of choice. efficient after sales service ensures

a entry barrier for a new entrant.

Efficient after sales service ensures

Low switching cost makes it easier for the minimum downtime thus

consumer to compare products on price, differentiating itself from the

the stickiness of the clients.

features and post sales service. competition as well as unorganized

Increasing competition empowers the segment

consumer with substantial bargaining power

Bargaining Power of Suppliers (Low) Industry Rivalry (Moderate) Threat of New Entrants (High)

Air cooler is a technologically sound product Intense competition among air cooler Seasonality of the product, low capital investment

designed keeping in mind aesthetics, comfort manufacturers leads to dominance of local players in the overall

and performance; vendors supplying parts that Low entry barrier, technology adoption, market

goes into making of an air cooler have low designs, distribution network and after sales Unorganized players still control around 70% of

bargaining power as suppliers are fragmented, services differentiates the product amongst the the market share

lack wherewithal to design, market the product. crowd of air cooler producer

Symphony products have

various features which enables the

appliance serve more than just the

air cooling function thereby

commanding an edge over the

competition Symphony controls around 50%

‘Symphony’ brand has become

of the organized market (crowded by

synonymous to air coolers, thus Threat of substitute products (Low) more than 70 odd brands) despite

helping the company capitalize on the

premium pricing in all the price

increasing temperature every Air cooler, being a low priced appliance

brackets. Extensive distribution

summer; products across price points compared to ACs, has great potential given

network & high brand recall

makes Symphony a top choice to a the under penetration in Indian market

differentiates it from both local &

marginal customer. Though seasonal in nature, the need for organized players

cooling cannot be done away with in summer

8

27 FEB 2019 Company Report

Symphony Ltd

Warmer summers ahead… Sector: Consumer Durables

Indian subcontinent climate is classified under ‘Tropical climate’; Expected increase in global temperature anomaly

though the tropical climate is marked by 12 month mean temperature

of 18 degree Celsius, the extremes can be as high as 50.2 degree

Celsius reported in Nawabshah, a city in southern Pakistan’s Sindh

province on April 30, 2018.

Global warming, a phenomenon caused by excessive emissions of

greenhouse gases, is responsible for extreme weather be it hot, torrid

summers or chilling winters or even excessive rains and melting of

glaciers in Arctic zones.

The UN Intergovernmental Panel on Climate Change (IPCC) published

a report saying temperatures are likely to rise by 1.5 degrees Celsius

between 2030 and 2052 if global warming continues at its current

pace. The same was also confirmed by Berkely Earth, California, a

US based non-profit organization.

Global Average Temperature 1850-2017 US-based NASA (National Aeronautics and Space Administration) has

said that Earth’s global surface temperature in 2017 ranked as the

second warmest since 1880 when global estimates became feasible.

But the real concern lies ahead as NASA’s analysis also emphasizes

that the decades-long warming trend continues—17 of the 18 warmest

years have now occurred since 2001.

As per the analysis, Earth’s average surface temperature has risen

about 2 degrees Fahrenheit (a little more than 1 degree Celsius) during

the last century (1900-2000) due to increased carbon dioxide and other

human-made emissions into the atmosphere.

Conclusion: The extremity in climatic conditions is going to persist in

coming future; the variations in temperature is going to be wider, thus

summers are expected to be more warmer while the winters would get

chilling and frosty.

Source : Berkely Earth, Axis Securities

9

27 FEB 2019 Company Report

Symphony Ltd

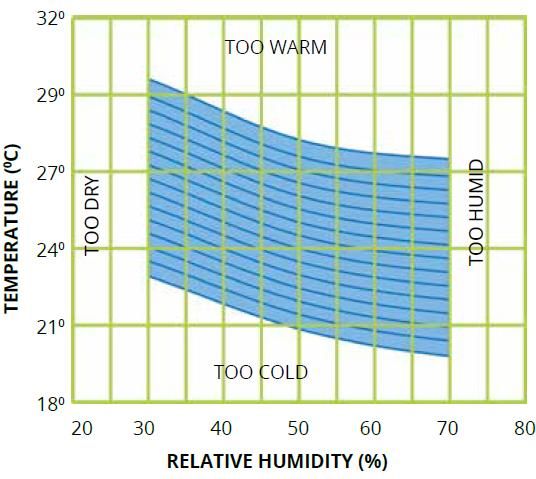

Air cooling- a pressing need of the time Sector: Consumer Durables

Cooling has become a necessity; especially in the 3 months of Climate zones of India

summer (in tropical parts of northern hemisphere) starting April to

May of every calendar year it is no more a luxury. The fans (which

has reached 65% of the households) just circulates the air; when Srinagar

this circulated air touches the sweat on the skin, it makes us feel

cool. Thus, fans fail to cool the surroundings necessitating an

additional but cost effective appliance which could cool the

surrounding to beat the hot summer.

Air coolers which work on evaporation of water technology are

New Delhi

very effective in areas which witness hot and dry climate. Air

coolers become relatively ineffective in areas with high humidity.

Thus air coolers would be effective in the states of UP, Bihar, Jodhpur

Chhattisgarh, MP, Jharkhand, Maharashtra, Gujarat, Rajasthan,

Punjab, Delhi, Northern Karnataka and western Telengana.

Evaporative cooling (the principle on which air coolers work) is

Kolkata

effective in low humidity. As relative humidity increases, the

difference between the air temperature (LHS) and the achievable

temperature (yellow & green boxes) keeps decreasing.

Temperature decrease chart for Air coolers

Air Temperature (deg. F)

Hot & Dry

Bangalore Hot & Humid

Composite

Cold

Moderate

Source: Axis Securities

1027 FEB 2019 Company Report

Symphony Ltd

Air coolers- highly underpenetrated, light on pocket Sector: Consumer durables

Summer is restricted to 3 months viz., April, May and June for majority of the hot & dry parts of India. Hence, Indian consumer looks for

cooling solution that is within his reach both on initial capital investment and operating cost. Fan- either ceiling or table fan, happens to be

the first choice given the low price, power consumption and lifetime maintenance cost.

An air cooler happens to be the first cooling solution that people purchase as and when they graduate from a fan; centralized air cooling is

used in the homes of ultra-rich, even in homes and hotels/ commercial complexes that are centrally air-cooled.

Unlike air conditioners, air coolers are light on the pocket both at the time of purchase and the power consumed in running the appliance; it

is environment friendly, portable and doesn’t overcool. Rising disposable incomes, hot summers and improved availability of electricity are

likely to support the burgeoning demand for sophisticated cooling solutions, coolers being the first choice.

Symphony will benefit from the likely shift in demand to the branded category after GST implementation. The long-term prospects of

Symphony are quite positive with the company having multiple growth and earnings drivers

~14.3 Cr HHs (~58% total HHs) reside in Air coolers score over air-conditioning units for both capital and variable costs

hot & dry climate areas Fans Air cooler AC

Initial Investment (Rs.) 500-3,000 4,000-20,000 25,000-50,000

Power cost per hour of usage

Rs 0.38@ 75W Rs 0.5@ 100W Rs 10.5@ 2100W

(Rs/hour) (assuming Rs 5/unit)

Refrigerants No Water Air polluting refrigerants

AC: 0.9 Cr

Decrease in temperature No Yes Yes

Air Coolers: Re-circulates same dry,

Circulates same air, Fresh filtered clean, cool

stale air; needs regular

2.7 Cr HHs Indoor Air quality & air inefficient & not very air with powerful air

cleaning, unclean filters

circulation effective in hot summers delivery of 1500 to 2000

may cause respiratory

esp. in spacious rooms cu.mtr/hr

problems

No Fans: 8.3 Cr HHs

Environmentally harmful

Emission No No

greenhouse gases

Complicated and

Maintenance Smple & Cost effective Smple & Cost effective

expensive

Fans: 16.4 Cr HHs Portability/ Ease of installation No Yes No

Usage Indoor & Outdoor Indoor & Outdoor Only indoor

Source: Industry, Company, Axis Securities

1127 FEB 2019 Company Report

Symphony Ltd

What differentiates Symphony from its peers Sector: Consumer Durables

After Sales service is crucial for Symphony products feature extensive

customer retention. Timely and Leader in customer Leader in terms usage of technology and innovation to

resourceful after sales service makes centric issues of innovation keep the products ahead of the

Symphony a formidable player in the competitors. At the same time, the

air cooler segment. company ensured low per unit cost

Being a crucial appliance to beat the and improved efficiency to protecting

hot summers, the management has to its margins

ensure as little downtime as possible The products provide more value for

at customer’s end. money invested vis-à-vis competition,

An efficient and timely service helps thus ensuring satisfied customer .

the company create goodwill and The company sells any of its SKU for

gives word of mouth publicity, thus around 2-3 seasons after which it is

not only retaining its customers but upgraded; company generally derives

helping enhance the customer base. 20-30% of revenues every year from

Company has 1,000 plus service the newly launched products.

centers to serve 19,000 pin-codes

Symphony enjoys around 50% of the Symphony has highest brand recall

organized air cooler market; the amongst its peers, thus helping them

management outsources position its products differently than its

manufacturing thus concentrating on competitors.

the R&D, designing and marketing.

Rich brand recall coupled with wide

Sticking to its core DNA of producing network of ~30,000 dealers covering

coolers, the company focuses on Leader Leader in brand and 5,000 plus towns helps the company

producing innovative products

keeping competition at bay in management category status reach the nook and corner of the

country

Innovation in products, high brand recall coupled with wide distribution network and efficient after sales service makes

Symphony a formidable player in growing air coolers market

1227 FEB 2019 Company Report

Symphony Ltd

One product- many functions Sector: Consumer Durables

Symphony has distinguished its product basket from the competitors

using technology and adding more punch, value to the product than

run-of-the-mill cooling function, thus making it more of a consumer

lifestyle or digital product.

The company has been successful in positioning the cooler which

used to be considered as peripheral cooling product into a

‘neighbours’ envy, owner’s pride’ by marrying technology,

aesthetics and utility into their product

Symphony has been pioneer in developing never heard of premium

range of cooling products (> Rs 10,000 per unit) and selling like hot

cakes, thus raising bar for the competition

Quality innovations helped the company position air coolers as

perennial product; various novel features are integrated into the

latest range of Symphony Air coolers. It includes:

Digital touch screen

Voice Assist

Ultrasonic Mosquito Repellent

i-Pure Technology- multistage air purification

Electronic humidity control

Wall mounted Air cooler resembling an air conditioner

Magic fill- automatic water filling

Removable tank

Cool flow dispenser

Power saver technology

Despite creating a differentiated product, Symphony Ltd has ensured

that their products are priced low enough to trigger an upgrade from

fans to coolers and attractive enough with air-conditioner like

features to generate value addition.

Source: Company, Axis Securities

1327 FEB 2019 Company Report

Symphony Ltd

Centralized Air-cooling – a BIG opportunity Sector: Consumer Durables

The ideal temperature at workplace, according to a research study, should be

between 24-30°C. The average ambient temperature has been rising steadily over

last couple of decades. Although the difference is only a few degrees, it can

change the work environment drastically. Countries across the globe have

mandated temperatures for workers. E.g. South Korea has mandated a

temperature of 24°C for its workers, New Zealand laws recommend a

temperature band of 18-24°C while US recommends a range of 20-24°C.

These days shop floor workers wear more protective gear— helmets, masks or

other apparatuses because of heightened attention to employee safety. As a result,

high workplace temperatures make the same task more onerous and sometimes

more exhausting. Even a reduction of 3-4°C in shop floor temperature can

enhance productivity by 25-30%.

Central air cooling solutions- a long runway

Opportunity and Size

Factories Universities

Warehouses Lecture halls

Shops and Showrooms Service Stations

Religious Institutions Offices

Central Air cooling Solution

Club House Poultry and dairy farms

Residence Departmental Stores

Lounges Diesel Generator Rooms

Canteens Laundry

Guest Houses Kitchens

Banquet Halls Malls

Range of Packaged Air Coolers Windows Air Cooler range

Source: Company, Axis Securities

1427 FEB 2019 Company Report

Symphony Ltd

Centralized Air-cooling – a BIG opportunity (cont.d) Sector: Consumer Durables

Packaged / Central Air Cooling Solutions Central air cooling solutions- facts and figures

Effective Temp © 24 27 29 32 35 38 41

Loss of work

3% 8% 18% 29% 45% 62% 79%

Output

Loss of Accuracy 0% 5% 40% 300% 700% >700%

Source: Study of NASA. “Comfort conditioning the Plant with Evaporative Cooling” Plants

Engineering July 8, 1976

Excessive heat in a manufacturing or warehouse environment has negative effects on workers, the production levels and even the quality of

goods produced or stored goods. An increasingly hot working environment can result in severe slowdown in production, the impact can be

either tangible or intangible. E.g. Employee sickness/absenteeism are tangible results while low productivity or defective job work due to

uncomfortable working conditions are the intangible outcomes.

Heat can affect the health of employees and also impact the health of the equipment. According to Arrhenius Equation, an electronic device

can operate for 32 years at 45°C but will last just four years at 80°C. Frequent replacement of equipment could lead to higher capex and

operating costs, thereby hurting company’s bottom line.

Machinery too produces extra heat and poor ventilation or cooling mechanisms can exacerbate the issue. Excessive heat can hurt production

levels by causing equipment to operate less efficiently or break down frequently. When equipments fail due to excessive heat, it becomes

difficult to identify the cause as the damage is often internal and prima facie, the damaged components appear to function correctly. It takes

detailed testing and analysis to locate the damage leading to more downtime and lost productivity, thereby adding to the cost.

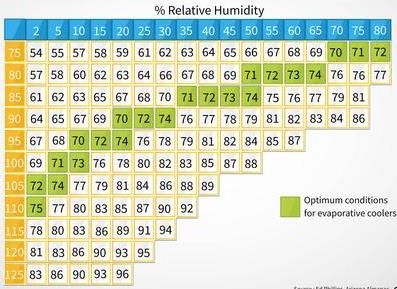

Evaporative cooling systems have the potential to reduce temperatures by 10-15°C, thus making it an ideal, cost effective way to address the

rising temperature issue on shop floors. Only caveat these coolers work effectively in dry climates, humidity should be below 60% for these

types of coolers to work best. In order to benefit from this increased productivity, companies are bound to spend on air cooling solutions for

their factories, thereby opening up a multi-million units market for Symphony Ltd which happens to be the only branded player in the organized

space. As per the company, the opportunity size of centralized air-conditioning market in India is estimated to be worth approx. Rs 4,000 cr.;

the value of centralized air-cooling market is undefined (potentially higher than Rs 4,000 cr.).

1527 FEB 2019 Company Report

Symphony Ltd

Marquee customers- Centralized air-cooling Sector: Consumer Durables

Source: Company, Axis Securities

1627 FEB 2019 Company Report

Symphony Ltd

Milestones Sector: Consumer Durables

Acquired

Climate Technologies Launched world’s Unveiled the world’s Recognition from the Government

Pty Ltd (Australia) 1 st wall mounted air cooler 1st packaged air cooler of India for R&D center

Established foothold in

Acquired Keruilai (China) Started offering central

all formats of modern retail air cooling solutions in India

2018 2017 2016 2015 2013 2012

2011

Acquired IMPCO 2009-

(North America) 2011

2009

1995- Pre- 2002- Post- Scaled up

1988 1994

2000 2005

2000 2005

2007 2005s international presence

Symphony born with Ventured into the manufacture of ACs, Suffered financial

one air cooler model washing machines and other durables stress and restructured

Got listed on Positioning: Strategic Focus:

stock exchanges ‘Many products – One market’ ‘One product –Many markets’

1727 FEB 2019 Company Report

Symphony Ltd

Global warming – an International Cooling opportunity Sector: Consumer Durables

Knowing fully well that the Indian market is underpenetrated for air

Comparison of temperatures from 1880 till Oct.2018

coolers, Symphony management did not restrict themselves to

Indian markets; they made overseas foray as the opportunity came

their way, be it exports or acquisitions (at reasonable valuations),

as the temperature variations are not country specific problems.

Today, Symphony has a presence in over 60 countries.

Extreme and unpredictable heat waves brought on by climate

change is not limited to India. Shift in weather patterns leading to

climate changes is a consequence of man-made global warming.

The chart besides shows the average global temperatures

throughout the year starting 1880 till Oct.2018; it must be noted

that the blue lines are for the temperatures in early part of 20th

century while the red lines are for last 18 years after year 2000.

The global average temperatures are higher anywhere around 1°C Temperatures crossing 28°C (82.5°F) (the definition of overheating

in 21st century compared to the same period in 20th century. under modern UK building rules) makes it unbearable for the UK

According to the World Meteorological Organization's (WMO) population. According to a study, heat-waves in the UK are up to

observations, 2016 was the warmest year on record (indicated by three times more frequent now than at the end of the 19th century,

red line at the top in the chart beside) with a central estimate of the duration of heat-waves has also increased two to threefold. UK

1.15°C above the average calculated since 1850. 2018 is likely is now an important overseas market for Symphony coolers.

to be the fourth warmest on record (indicated by dark red line) with Middle East, Africa are Symphony Ltd’s core market in addition to

the Earth's average temperature hovering close to 1°C above the India. Air coolers working on evaporative cooling technology can

levels recorded in 1850-1900. UK Met Office has predicted that cool huge open spaces and even outdoors. Symphony’s has

the global average temperature for 2019 will likely be 1.1°C successfully undertaken its biggest cooling project at Mecca — the

higher than the pre-industrial average period from 1850-1900. biggest air cooler project anywhere so far. Symphony has air-

In 2010, Russia was hit by an unprecedented and deadly heat cooled entire Mecca complex by installing 50,000 units in the

wave, the temperatures in Moscow had crossed 37°C. Soon after, residential section; it also has installed 200 giant coolers on the

Russia has been an important export market for Symphony. Jamarat Bridge, Meena, Saudi Arabia which is crossed every year

by millions of pilgrims.

Source: NOAA, Axis Securities

1827 FEB 2019 Company Report

Symphony Ltd

International acquisitions to drive earnings Sector: Consumer Durables

In 2009, Symphony acquired the Mexican assets of International IMPCo Distribution presence

Metal Products Company (IMPCo), Phoenix, US based company

that has been producing coolers since the 1930s. Its manufacturing

facilities in Mexico have opened up new markets in USA & Latin

America.

IMPCo was acquired because of the deep knowledge that it

possessed in industrial coolers, a segment where Symphony was

absent. Marrying the knowledge and experience from IMPCo with

the design, style, and aesthetics of Symphony has been a

synergistic fit.

Further, IMPCo adopted an asset light model of Symphony by

outsourcing operations to third party and focusing on brand

building and marketing. It has successfully made transition to asset

light, outsourced based manufacturing model in FY18 (Project

Renovation started in FY15) and reported profit before tax of 39.6

mn Mexican Pesos.

IMPCo has wide product basket including commercial / industrial

cooling systems which are suitable for workshops, restaurants,

gyms and indoor stadiums etc. The acquisition helped Symphony

get enlisted with marquee US based large format retail clients viz.

Walmart, Home Depot, Lowes, Costco, Coppel, Soriana, Sears,

etc. The acquisition has helped Symphony to leverage IMPCo's

relationship with these large format stores to market its popular

residential air coolers in US.

During the year, the Mexican subsidiary developed and launched

a first “All Plastic” window cooler in the Mexico market which

received a very good response. The company has charted out a

new vision which seeks accelerated growth in the next 3 years, Presence

mainly with the incorporation of new product lines.

1927 FEB 2019 Company Report

Symphony Ltd

International acquisitions to drive earnings (cont.d) Sector: Consumer Durables

Symphony acquired China-based Munters Keruilai Air Treatment Share of revenue of overseas operations to increase in future

Equipment (MKE), Guangdong for Rs 1.5 crore ($234,000) in 2016.

MKE produces energy-saving and environment-friendly evaporative air 100%

coolers under brand ‘Keruilai’, a market leading brand in China. 80%

Renamed as Guangdong Symphony Keruilai (GSK) Air coolers Ltd. China,

the acquisition boasts one of the world’s best repositories in industrial 60%

cooler knowledge, patents and product development.

40%

Post acquisition by Symphony, the Chinese subsidiary has developed and

introduced several new products for industrial, commercial as well as 20%

household applications, and, also developed several new markets - both 0%

domestic as well as international.

FY16 FY17 FY18 FY19E FY20E FY21E

GSK products have also been successfully introduced to Symphony’s 9 months

already established markets of India and Mexico, and, are very well

received in these markets. The acquisition also helped Symphony increase Domestic Operations Overseas Operations

exports of its air coolers, especially to ASEAN markets via China which

has FTAs in these markets.

The company MKE, China, which was loss-making at the time of Revenues & profitability of overseas operations expected to improve

acquisition, has already broken even in 9M ending Dec.2018 (9MFY19);

both the top-line and bottom-line is improving and is expected to provide 600 530

485

steady growth in future

364

Symphony acquired 95% equity stake in Australia based Climate 400

Technologies Pte. Ltd. in 2018. The acquired company is one of

Australia’s most recognized manufacturers of cooling and heating 200 148

127

appliances; it commands 35% and 29% market share of the domestic 79 54

9.2 16 30 41

Australian evaporative air coolers and ducted gas heaters markets, 4.6

respectively. 0

The acquisition of Climate Technologies Pte. Ltd. would help Symphony -0.5 -5.7

Ltd to moderate its business risks as Australia has complementary weather -200

conditions compared to India i.e. when there is summer in northern FY15 FY16 FY17 FY18 FY19E FY20E FY21E

hemisphere, Australia or Southern hemisphere experiences winter and

9 months

vice-versa. Moreover, Climate Tech. manufactures both heating and

cooling appliances thereby supplying products required round the year to Revenues (Rs cr.) PAT (Rs. cr.)

the target market.

2027 FEB 2019 Company Report

Symphony Ltd

Asset light business model scores over the competition Sector: Consumer Durables

Asset light business model ensures robust return ratios Symphony operates on asset light business model requiring low capital

80 investments; it outsources almost all its production to nine different OEMs

thus ensuring that it is not dependent on any one vendor.

60 This asset light strategy enables the management to concentrate on

design, development and innovation along with marketing the product

40 thus generating high return on capital employed (RoCE)

Focusing on single product viz., air-coolers helps them to keep away

20

from the other product related distractions and deliberate their energies

on developing variants of air-coolers with different features to suit the

0

changing needs of the consumer.

FY16 (9 FY17 FY18 FY19E FY20E FY21E

months) Company boasts of 50 plus models of air-coolers and wide range of

RoE (%) RoCE (%)

industrial and commercial coolers

High Inventory turnover Sales to Fixed assets have been improving consistently

9.0 14

8.5 12

8.0 10

7.5 8

7.0 6

6.5

4

6.0

2

5.5

5.0 0

FY16 FY17 FY18 FY19E FY20E FY21E FY16 FY17 FY18 FY19E FY20E FY21E

9 months 9 months

Inventory Turnover ratio Sales to Gross Fixed Assets Sales to Net Fixed Assets

Source: Company, Axis Securities

2127 FEB 2019 Company Report

Symphony Ltd

Stabilizing margins and stable WC cycles to boost profitability Sector: Consumer Durables

Margins are stabilizing… Stable working capital cycle

35% 75

30%

25% 55

20%

35

15%

10%

FY15 FY16 FY17 FY18 FY19E FY20E FY21E 15

9 months FY15 FY16 FY17 FY18 FY19E FY20E FY21E

9 months

EBIDTA margins (%) Net Profit Margins (%) Inventory Days Debtors Days Creditors days Cash Conversion Cycle

Consistent spends on advertisements Given the brand recall commanded by the company with its customers,

the distributors keep purchasing the air-coolers even in off-season paying

50 6% 100% in advance to take benefit of discounted prices offered by the

40 5% company in the off-season i.e. quarter Q2 and Q3 of every financial

4% year. Company follows the plan of increasing its prices every fortnight

30 as the season approaches.

3%

20 The cash conversion cycle for Symphony Ltd was around 42 days at the

2% end of FY18. The cycle has stabilized post the change in the accounting

10 1% year made in FY16. The company enjoys debtors days of 28 days but

payables are paid in 37 days a testimony of faith reposed by the dealers

0 0% and distributors in their products.

FY16 FY17 FY18 FY19E FY20E FY21E

The margins are stabilizing post change in accounting year and

9 months

improving profitability of the acquisitions.

Advertisement spends (Rs cr.) (LHS) Company has policy of consistent advertisement spends esp. in the

Advertisement spends as % of Sales (RHS) season which acts as an investment in long run and helps it protect its

market share.

Source: Company, Axis Securities

2227 FEB 2019 Company Report

Symphony Ltd

Turnaround in acquisitions to help improve profitability Sector: Consumer Durables

Overseas acquisitions would help Symphony Ltd to chart path of growth Steady growth in revenues and earnings of overseas acquisitions

both on topline and bottom-line. The acquisitions has brought industrial/

commercial air cooling technology with them, thus helping Symphony Ltd to 600 530

spread its wings beyond residential air-coolers and bid for the business 485

opportunities in this untapped space in India. Moreover, these companies

also offer Symphony Ltd with an entry into lucrative American market with 400 364

widely diversified product portfolio ranging from residential cooling to

commercial cooling.

200 127 148

The overseas acquisition done by Symphony Ltd in the past are showing 79

trends of profitability. The Mexican subsidiary is reporting profits from 54 30 41

4.6 9.2 16

FY16 onwards while the Chinese subsidiary has turned around in 9 month 0

ending Dec.’18. The recent acquisition of Australian subsidiary is already a

profit making entity and offers Symphony Ltd an opportunity to cross sell its

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

products in both Australian and American continent. Similarly, it enables 9 months

de-risking of business as Australian weather is complementary to Indian

sub-continent weather. Revenues (Rs cr.) PAT (Rs. cr.)

Debt/Equity ratio (x) Symphony Ltd has been net-cash (almost debt free) company in FY18.

0.25 0.23 The recent Australian acquisition has led to debt on the books of the

Australian subsidiary which would be serviced using the proceeds from

0.20 0.18 Australian operations; even post acquisition, the company is in net-cash

position.

0.15

0.15 The debt/equity (D/E) has consistently been far below 1x; the interest

coverage ratio is in mid twenties indicating better financial health of the

0.10 company

0.05 0.05

0.05 The cash on the books is deployed into Debt MFs and arbitrage funds

0.01 yielding upwards of G Sec yields for the company.

0.00 The management plans to deploy the cash for any good acquisition

FY16 FY17 FY18 FY19E FY20E FY21E opportunity or distribute it among the shareholders through dividends

9 months and share buyback at appropriate time.

Source: Company, Axis Securities

2327 FEB 2019 Company Report

Symphony Ltd

Weak quarter but the core competency remains… Sector: Consumer Durables

Quarterly Performance (Q3FY19) Symphony Ltd reported a weak set of quarterly results for Q3FY19, which

Quarterly Performance happens to be an off-season. Company reported 9% YoY growth in

consol. Sales, 41% YoY de-growth in EBIDTA and 43% YoY de-growth in

(Rs.Cr.) % Change % Change

Q3FY19 Q3FY18 Q2FY19 profit after tax for Q3FY19 on back of high channel inventory owing to

(YoY) (QoQ)

two back to back weak summers.

Sales 240 219 9 223 8

Other Inc 13.0 13.1 NA 9.0 NA Cashing on its core competency- the product, brand and product range,

the off season sales over last 6 months has been done on 100% advance

Total Revenue 253 232 9 232 9

and the company has maintained its leadership with 90% plus market

share in off-season sales.

Expenditure

Net Raw Material 85 12 597 55 55 After two consecutive bad summers in 2017 & 2018, the channel

inventory has now normalized in majority of the domestic market except

Purchase of goods 44 87 (50) 60 (27)

few pockets like Karnataka.

Personnel 29 19 55 29 0

Other Exp 39 20 95 36 8 The business for overseas subsidiaries is improving- China has posted

Total Expenditure 197 138 43 180 9 marginal profit for the first time in 9MFY19 thus ensuring that the

company is on path of recovery and steady growth. GSK, China

reported topline of Rs 47 cr, EBIDTA of Rs 2.7 cr and PAT of Rs 0.36 cr.

EBIDTA 56 94 (41) 52 8

for 9MFY19

Non-operating Income 0.0 0.0 NA 0.0 NA

Interest 3.0 0.8 280 1.0 200

Q3 is an off season for Mexican subsidiary- IMPCo; for 9MFY19, IMPCo

reported revenues of Rs 60 cr, EBIDTA of Rs 4.7 cr (excluding

Depreciation 2.0 1.8 10 3.0 (33)

exceptional income) and PAT of Rs 3.94 cr (excluding exceptional

Exceptional Item 0.0 0.0 NA (4.0) NA

income).

PBT 51 92 (44) 44 16

Tax 14.0 27.3 (49) 13.0 8

Symphony Ltd had acquired Climate Tech. Pte, Australia on July 1, 2019.

Hence at the end of 6 months ending Dec.’18, CT Australia reported

PAT 37.0 64.6 (43) 31.0 19

revenues of Rs 141 cr, an EBIDTA of Rs 9.23 cr and PAT of Rs 4.13 cr.

Oth. Comprehensive Income

(1.0) (0.8) (4.0)

(net of taxes) All eyes would now on be the upcoming summer season given that the

Total Comprehensive Income 36.0 63.7 (44) 27.0 33 last two summers were failures as far as the cooling and air-conditioning

EPS (Rs.) 5.3 9.2 (42.7) 4.4 19

sector is concerned.

Source: Company, Axis Securities

2427 FEB 2019 Company Report

Symphony Ltd

Valuation Charts Sector: Consumer Durables

One year forward P/E fan chart Valuation

Symphony Ltd is well positioned in the air-coolers industry owing to

2000

its well established brand with high recall, asset light business

1500 model, substantial market share and growth in demand for the

product on back of improving affordability.

1000

We estimate the company to grow at a CAGR of 17% and

500

earnings at CAGR of 11% over FY18-FY21E (FY19 is expected to

0 show de-growth). When computed over FY19E-FY21E, we estimate

the company to post robust growth of 18% CAGR in revenues and

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Sep-14

Nov-14

Sep-15

Nov-15

Sep-16

Nov-16

Sep-17

Nov-17

Sep-18

Nov-18

Jan-15

Jan-16

Jan-18

Jan-19

May-14

May-15

May-16

Jan-17

May-17

May-18

29% CAGR in earnings.

We value Symphony Ltd at 45x FY21E to arrive at price target of

Price 20x 30x 40x 50x

Rs 1,680 giving an upside of 37%

12mth forward P/E band Key Risks

90 Single product with seasonality: The business of Symphony Ltd is

highly dependent on single product viz., air-coolers which has

70 seasonal sales i.e. the end-users purchase the air-coolers only in

summer.

50

Competition from unorganized segment: Air-cooler market is

dominated by unorganized with 70% market share who are local

30

players with contained costs. Entry of more players in organized

segment where Symphony is a leader can create more

10

competition.

Mar-14

May-14

Mar-15

May-15

Mar-16

May-16

Mar-17

May-17

Mar-18

May-18

Jul-14

Sep-14

Jul-15

Jul-17

Jul-18

Nov-14

Jan-15

Sep-15

Jul-16

Nov-15

Jan-16

Sep-16

Nov-16

Jan-17

Sep-17

Nov-17

Jan-18

Sep-18

Nov-18

Jan-19

Unfavourable forex movement: A big chunk of consolidated

revenues are sourced from overseas market. Unfavourable forex

PE Mean Mean+1Stdev Mean-1Stdev

movement may impact profitability of consolidated entity.

2527 FEB 2019 Company Report

Symphony Ltd

Financials Sector: Consumer Durables

Profit & Loss (Rs Cr) Balance Sheet (Rs Cr)

YE March FY17 FY18 FY19E FY20E FY21E YE March FY17 FY18 FY19E FY20E FY21E

Net sales 765 798 920 1,145 1,289

Total assets 497 653 945 1,146 1,380

Other operating income 0 0 0 0 0

Net Block 75.6 77.9 97.9 97.0 95.5

Total income 765 798 920 1,145 1,289

CWIP 0.0 0.0 7.5 5.0 5.0

Cost of goods sold 525 546 691 806 907

Investments 110 177 299 299 299

Contribution (%) 31.4% 31.6% 24.9% 29.6% 29.6%

Wkg. cap. (excl cash) 265 376 405 412 420

Advt/Sales/Distrn O/H 41.2 32.8 33.9 41.6 41.3

Cash / Bank balance 47 23 135 333 560

Operating Profit 199 219 196 298 340

Other income 43 54 39 41 50

Capital employed 497 653 945 1,146 1,380

PBIDT 242 273 234 338 390

Equity capital 14.0 14.0 14.0 14.0 14.0

Depreciation 7 7 10 11 12

Interest & Fin Chg. 0 2 7 13 13 Reserves 451 598 735 936 1,169

E/o income / (Expense) 0 0 (4) 0 0

Minority Interests 0.0 0.0 4.0 4.0 4.0

Pre-tax profit 235 265 213 315 366

Borrowings 26 33 175 175 175

Tax provision 69 72 56 90 104

Profit after Tax 166 193 157 225 261 Def tax Liabilities 5.3 8.9 16.4 17.4 18.4

Source: Company, Axis Securities

2627 FEB 2019 Company Report

Symphony Ltd

Financials Sector: Consumer Durables

Cash Flow (Rs Cr) Ratio Analysis (%)

YE March FY17 FY18 FY19E FY20E FY21E YE March FY17 FY18 FY19E FY20E FY21E

Sources 129 100 291 212 245 Sales growth 71.6 4.4 15.3 24.4 12.6

OPM 26.0 27.5 21.2 26.0 26.4

Cash profit 173 201 174 248 286

Oper. profit growth 46.0 10.4 (10.8) 52.2 14.4

(-) Dividends 105 56 19 19 25 COGS / Net sales 68.6 68.4 75.1 70.4 70.4

Overheads/Net sales 5.4 4.1 3.7 3.6 3.2

Retained earnings 68 145 155 229 261

Depreciation / G. block 3.8 5.1 6.1 6.3 6.3

Issue of Equity 7.0 0.0 0.0 0.0 0.0

Effective interest rate 0.2 NA 6.9 7.4 7.5

Change in Oth. Reserves (12.2) (10.6) 4.0 0.0 0.0 Net wkg.cap / Net sales 0.19 0.40 0.42 0.35 0.32

Net sales / Gr block (x) 4.2 6.0 5.6 6.6 7.0

Borrowings 0 0 132 0 0

RoCE 58.1 48.7 29.3 32.6 31.0

Others 66 (34) 0 (17) (16) Debt / equity (x) 0.05 0.05 0.23 0.18 0.15

Applications 129 100 291 212 245 Effective tax rate 29.2 27.3 26.4 28.5 28.6

RoE 39.6 34.6 21.7 25.3 23.5

Capital expenditure (6.3) (47.9) 174.6 7.5 10.0

Payout ratio (Div/NP) 33.5 10.0 12.7 11.3 11.1

Investments (71.0) 67.0 (14.9) 0.0 0.0 EPS (Rs.) 23.8 27.5 22.4 32.1 37.3

EPS Growth 40.5 15.8 (18.5) 43.2 16.2

Net current assets 206.1 105.1 19.3 6.3 8.5

CEPS (Rs.) 25.0 28.1 22.9 32.7 37.9

Change in cash 0.1 (24.4) 112.4 198.2 227.0 DPS (Rs.) 8.0 2.7 2.7 3.5 4.0

Source: Company, Axis Securities

2727 FEB 2019 Company Report

Symphony Ltd

Disclaimer Sector: Consumer Durables

Disclosures:

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations).

1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in the Regulations, is engaged in the business of

providing Stock broking services, Depository participant services & distribution of various financial products. ASL is a subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed public

company and one of India’s largest private sector bank and has its various subsidiaries engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital,

Stock Broking, the details in respect of which are available on www.axisbank.com.

2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the Association of Mutual Funds of India (AMFI) for

distribution of financial products and also registered with IRDA as a corporate agent for insurance business activity.

3. ASL has no material adverse disciplinary history as on the date of publication of this report.

4. I/We, Pankaj Bobade– AGM, Research, CFA (ICFAI), author/s and the name/s subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect

my/our views about the subject issuer(s) or securities. I/We also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or

view(s) in this report. I/we or my/our relative or ASL does not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates may have beneficial

ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Since associates of ASL are engaged in various

financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. I/we or my/our

relative or ASL or its associates do not have any material conflict of interest. I/we have not served as director, officer or employee in the subject company in the last 12-month period.

Any holding in stock – No

5. ASL or its associates has not received any compensation from the subject company in the past twelve months. ASL or its Research Analysts has not been engaged in market making activity for the

subject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its associates may have:

i. Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research report and / or;

ii. Managed or co-managed public offering of the securities from the subject company of this research report and / or;

iii. Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this research report;

ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in connection with this report

Term& Conditions:

This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not be altered in

any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ASL. The report is based on the

facts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained from publicly available

media or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer document

or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all customers may receive this

report at the same time. ASL will not treat recipients as customers by virtue of their receiving this report.

Instead of a company visit, we have done a conference call with the company’s management.

2827 FEB 2019 Company Report

Symphony Ltd

Disclaimer Sector: Consumer Durables

DEFINITION OF RATINGS

Ratings Expected absolute returns over 12-18 months

BUY More than 10%

HOLD Between 10% and -10%

SELL Less than -10%

NOT RATED We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NO STANCE We do not have any forward looking estimates, valuation or recommendation for the stock

Disclaimer:

Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the recipient’s specific circumstances. The securities and strategies

discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific

recipient.

This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as it deems necessary to arrive at an independent evaluation of

an investment in the securities of companies referred to in this report (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. Certain transactions,

including those involving futures, options and other derivatives as well as non-investment grade securities involve substantial risk and are not suitable for all investors. ASL, its directors, analysts or employees do not take any

responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds,

changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. Past performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance.

Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements

are not predictions and may be subject to change without notice.

ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other

transaction involving such securities or earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or investment banker,

lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. Each of these entities functions as a separate, distinct

and independent of each other. The recipient should take this into account before interpreting this document.

ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this report should be aware that ASL may have a potential conflict of

interest that may affect the objectivity of this report. Compensation of Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ASL may have issued other reports

that are inconsistent with and reach different conclusion from the information presented in this report.

Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the United States or Canada or distributed or redistributed in

Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This report is not directed or

intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to

law, regulation or which would subject ASL to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of

investors.

The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The Company reserves the right

to make modifications and alternations to this document as may be required from time to time without any prior notice. The views expressed are those of the analyst(s) and the Company may or may not subscribe to all the views

expressed therein.

Copyright in this document vests with Axis Securities Limited.

Axis Securities Limited, Corporate office: Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 022 – 4050 8080 / 022 – 6148 0808, Regd. off.- Axis House, 8th

Floor, Wadia International Centre, Pandurang Budhkar Marg, Worli, Mumbai – 400 025. Compliance Officer: Anand Shaha, Email: compliance.officer@axisdirect.in, Tel No: 022-42671582.

29You can also read