GB RETAIL AND LEISURE MARKET ANALYSIS - FULL YEAR 2020 - PUBLISHED MARCH 2021 BY LOCAL DATA COMPANY

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GB RETAIL AND LEISURE

MARKET ANALYSIS

F U L L YE A R 20 20

PUBL ISHED M A R CH 2021

BY L OCA L DATA COM PA NY

COPY R I G HT 2021

No part of this report may be reproduced or distributed without consent

www.localdatacompany.com

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

FO R EWO R D

2020 was a year like no other, as the pandemic future relationship with the EU.

impacted all aspects of our personal and professional

lives. This created one of the toughest trading With the rapid pace of change in the market, it is

climates for the retail sector, with all stakeholders important to note that these figures do not include

having to rethink, adapt and show resilience in the the closures that will happen as a result of the sale

face of a catalogue of challenges. of Arcadia and Debenhams in January 2021. This

activity will be captured alongside the other recent

This report focuses on the 12 months of 2020, which announcements including Thorntons and John

we must not forget was unaffected by the pandemic Lewis in our H1 2021 report, which will also track

until March. These first months of the year were the much-anticipated reopening of the market,

filled with relative vibrancy after the general election which begins on 12th April 2021 (correct at time of

provided some much-needed certainty on the UK’s writing).

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 2 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

C O NT E NT S

4 ABOUT LOCAL DATA COMPANY 46 2021 OUTLOOK

Openings and closures

7 KEY FINDINGS Vacancy rates

10 INTRODUCTION 49 CONCLUSION

Openings and closures

Temporary closures

50 COMMENTARY

Vacancy rates

Lucy Stainton, Head of Retail and Strategic

Failures and job losses Partnerships

18 LOCATIONS

51 METHODOLOGY

Openings and closures by location type

Vacancy rates by location type

52 GLOSSARY

Regional vacancy rates

Persistent vacancy

Redevelopment activity

Case study – West Byfleet

Hyper-localisation

Case study - Heckmondwike

29 SECTORS

Net change

Top 10 growing categories

Top 10 declining categories

Multiples vs independents

39 BRANDS

CVA/Administration activity

Case study – reoccupation of former stores

Expanding brands

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 3

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

A B O UT T H E L O C A L D ATA C OMPANY

The Local Data Company is the UK’s most accurate data is underpinned by our proprietary technology

retail location insight company. We physically track stack which supports the field research and quality

every retail and leisure business across the country. control processes. This technology enables us to

Our data powers strategy and decision making for provide our clients with unrivalled insight on over

our clients working across retail, leisure, out-of- 680,000 retail and leisure businesses, access to

home media, investment, property and financial location insight dashboards and footfall tracking

services. capabilities.

Our team of field researchers record the occupancy Our team of analysts and sector experts is committed

status of every business on a regular basis. This to understanding the unique challenges our clients’

frequency enables us to track how the market is businesses face and applying our comprehensive

changing in close to real-time. The accuracy of our data to support their strategic objectives.

OUR PRODUCTS

RICH, ACCURATE DATA

Our database contains over 680,000 addressable,

field-researched points of interest including over

400,000 independent premises and every chain

retail and leisure brand across the UK.

ANALYTICS

Local Data Online provides fast and accurate access

to market trends, competitor insights and portfolio

analysis tailored to your business.

STRATEGY

For over fifteen years our dedicated insight team has

been working in partnership with clients committed

to investing in retail via a range of strategic projects.

FOOTFALL TECHNOLOGY

Accurate counting and analysis of footfall trends is

invaluable. Our proprietary technology stack provides

this at a granular level, enabling forensic insights into

flows and trends around a physical space.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 4 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

PROJECTS WE WORK ON INCLUDE: BUSINESSES WE WORK WITH:

• Location planning and strategy

• Due diligence

• Store rationalisation

• Competitor and market tracking

• Investment strategy and asset management

• Anti-money laundering

• Alt-data projects

• COVID-19 impact analysis

• Portfolio strategic realignment

“

After opening a number of successful dark kitchens and with home delivery being

an even more critical part of our strategy due to the covid-19 pandemic, Chopstix

Group enlisted LDC to support the expansion of our dark kitchen network. LDC

analysed the existing sites to establish drivers of performance and used this as a

framework for identifying what the market capacity was for this concept as well as

providing us with a list of locations to target. It was critical for us to work with live

and accurate data for this project, and the experienced team at LDC helped up carve

out a strategic plan of action against set against a complex market background.

“

JOHN L AKE

MANAGING DIRECTOR, CHOPSTIX GROUP

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 5

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

L OCA

LOC ALL DDATA

ATAC OCO

M PA NY RESE ARC H M ETHODOLOGY

MPANY

DATA R E S E A R C H

ME T H O D O L O G Y

Our field

research

coverage

70 different data variables

includes:

collected including:

680K

retail • Brand

and leisure Every high name

businesses street, retail • Address

park and • Geocode

400K shopping • Website

independent centre • Telephone

businesses across the number Data is

country is analysed by

3,200 visited either LDC’s Quality

GB retail on a 6 or 12 Control Team

destinations month cycle.

Live data is uploaded

24 hour in real time each day to the 80k updates

update secure Local Data Company processed

cycles server per month

Database of over

680K premises

Products:

including: Equalling in excess

Online 400k

independent of 1.2 million

Insight

businesses 4,800 10 year unique records

Dashboards

national time

brands series

Rich,

Accurate

Data

Strategic

Consulting

The Local Data Company is the only business tracking the huge change taking place across

the GB retail and leisure market in near real-time.

Contact us at team@localdatacompany.com or visit www.localdatacompany.com to find

out more about accessing data and insights on the post-covid landscape.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 6 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

KEY FIN D IN GS

1. 4.

EXPOSURE TO COMPARISON RETAIL LED CHALLENGES AHEAD FOR OWNERS OF

TO INCREASED RISK FOR SHOPPING VACANT DEPAR TMENT STORE SPACE

CENTRES

With the announcements that Debenhams will close

Shopping Centres were the most negatively and John Lewis will shutter more stores, landlords

impacted of all location types in 2020, with a net have a challenging task ahead in finding reoccupiers

loss in occupied units of 5.4%. The retail mix within for large-format space. Of the House of Fraser,

these asset types tends to comprise of more ‘non- Debenhams or Beales department stores that

essential’ retailers than other location types. On closed between January 2017 and December 2019,

average, 57% of units in Shopping Centres are only 24% had found new occupiers with no capital

Comparison Goods stores, much higher than the investment required by the end of 2020. 30% of

average for the High Street at 28%. The risk that this the former department stores saw some structural

creates for Shopping Centres is evident by data on change either being demolished or split into smaller

the Comparison Goods retail sector, which declined units. This is likely to be the favoured approach for

by -6,984 units in 2020, accounting for 62% of the the 124 Debenhams stores that closed at the end

total stores that were lost in 2020. of 2020.

2. 5.

LACK OF COMMUTER AND TOURIST FUTURE DEMAND FOR RETAIL SPACE IS

FOOTFALL HIT CITIES HARD THE KEY FACTOR IN RETAIL REVIVAL

The Vacancy Rate across City Centres increased Despite the challenges in 2020, 39,060 stores

by 2.5% to 16.1% in 2020, the fastest jump seen opened their doors for the first time. 42% of these

across all town profiles analysed. The move to were prior to the pandemic with the rate of opening

remote working, loss of international tourists and after March at an all-time low. Total online retailing

cancellation of major sporting events and concerts values increased by 46.1% in 2020 when compared

which are key City Centre attractions, collectively to 2019 (Source: ONS). This jump is likely to have a

created a sharp downturn in footfall. Two town longer-term impact in 2021 as retailers opt for fewer

profiles which benefited from the pandemic were stores. However, locations suited to support online

Villages and Commuter Towns where vacancy operations such as those out of town and on retail

increased by just 0.4% and 1.2% respectively, both parks will boost store openings across 2021.

below the national average increase of 1.6%.

3.

SLOWDOWN IN REDEVELOPMENT

ACTIVITY AS THE PROPER TY MARKET

ENTERED A DEEP FREEZE

There was a slowdown in property redevelopment

activity for the first time in five years, with the number

of retail and leisure units being converted for other

use such as office and residential dropping by

16%. This was due to operational delays caused by

restrictions during lockdown, landlords and investors

delaying plans due to market uncertainty and many

businesses being unwilling to commit the capital

needed to complete work.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 7

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

T R AC K I N G FOOT FALL T R EN DS ACROSS A RE COVE RIN G M ARKET

LOCAL DATA COMPANY’S 2 ND GENERATION FOOTFALL TECHNOLOGY

THE CHALLENGE OUR PRODUCT

When the ‘non-essential’ retail market reopens The latest generation of Local Data Company

across UK high streets, shopping centres and Footfall Sensor achieves a marketing-leading level

retail parks, measurement of how and when footfall of accuracy, capturing ground-truth data on footfall

returns is key to understanding the long-term impact trends without relying on proxies or generalising

of the COVID-19 pandemic and what future strategy trends based on smaller data samples.

should be for occupiers, local authorities, landlords

and other retail stakeholders.

Our proprietary technology uses low-level radar

waves to count people walking within a set field of

vision. It has been tested to perform within a +/-

5% error margin and works consistently 24/7, in all

weather conditions.

SENSOR BASE STATION

Sensors have been designed to sit discreetly in a store environment and are installed by fully trained engineers,

briefed to cause minimum disruption during their visit.

THE OUTPUT

The unique benefit of our footfall data is not just Data is available each Monday for the previous week

the market-leading accuracy of our technology, but in a range of formats: raw data files, via our online

our ability to combine this with powerful, historical insight platform, or as bespoke reports produced by

insight on 680,000 retail and leisure units. Adding our insight team.

our contextual data enables us to tell the full story –

not just how footfall is changing, but why.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 8 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

USE CASES

It’s not only strategically important to track footfall portfolio of stores or a location can support a range

as part of the COVID-19 recovery effort. Having an of long-term strategic activities.

accurate and robust source of footfall data on a

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 9

G B R ETAIL AND LEISU RE MA RK E T A NA LYS IS - F U LL Y E AR 2 0 2 0

INTRO D UCTION

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 10 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

I NT R O D UC T IO N

2020 was the year defined by one word: COVID-19. This report will provide evidence for some of the

A new Coronavirus spread across the world at a trends noted anecdotally across the year and will

rapid pace, landing in the UK in January and causing highlight not only the intense challenges faced by the

indeterminate damage to both the nation’s health market, but the green shoots of growth for a select

and the economy. The retail and leisure market was group of winners. Our prediction is that the road to

at the core of this damage, hitting the headlines recovery is on the horizon, but for occupiers and

daily; from panic buying to the Eat out to Help Out landlords alike, the situation will get worse before it

scheme and, creeping into 2021, the sad news of gets better.

two high street giants, Debenhams and Arcadia

falling into administration and shutting up (physical)

shop for good.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 11G B R ETAIL AND LEISU RE MA RK E T A NA LYS IS - F U LL Y E AR 2 0 2 0

O P E NI N GS A ND CLOS U R ES

The retail and leisure market was one of the sectors Retail and leisure openings were down by 13% as

which was hit the hardest by the pandemic, evident many businesses paused expansion plans. There

from the 50,379 closures across GB in 2020. were 39,060 openings in 2020; the lowest number

However, this was down 6.8% on the previous since we started reporting on this metric in 2013.

year which might surprise many, but there are two Of the 39,060 openings, 43% occurred in the first

reasons for this: three months of the year. The slowdown in openings

resulted in a net loss of 11,319 units, once again, the

highest number since our records began.

• Potent Government support schemes including

the business rates holiday and protection from

evictions put the property sector into a deep

freeze. These measures enabled most retailers

to keep their head above water as landlords

50,379

took the hit on rental collections; only 54% of

retail rents were collected within 14 days of the

last December rents day according to Re-leased

(Source: Re-leased, 2021). This equated to a

year-on-year decline of 18%.

• The temporary closure of the ‘non-essential’ retail

market depressed closures as well as openings,

with total activity (openings + closures) down by CL OSURE S

9.6% compared to 2019. ACROSS G B IN 202 0

ANNUAL MARKET ACTIVITY (OPENINGS + CLOSURES), 2013 - 2020

Figure 1: Number of openings and closures across GB, 2013 - 2020 (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 12 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

T E M P O R ARY CLOS UR ES

The introduction of the first UK lockdown in March following the first round of national restrictions. June

2020 brought with it a term we would become very and July saw the biggest increases in ‘non-essential’

familiar with, as only stores deemed ‘essential’ by units reopening, with many occupiers adapting

the government were legally able to remain open. operations and store infrastructure in order to meet

Those classified as ‘non-essential’ had to close strict social distancing guidelines. The peak of the

until the virus was brought back under control. Just recovery came in September when 83% of units

19.5% of occupiers on GB high streets fell into that were eligible to reopen had done so and some

the ‘essential’ classification and just 15.4% within businesses were encouraging staff to begin the

shopping centres, which reflects the scale of the return to the office. Albeit this was short-lived with

shut down at the time. a tightening of restrictions returning fairly promptly.

Some essential retailers closed stores initially and

reopened fairly promptly once stores had been

Figure 2 shows the gradual recovery of the market adapted to meet COVID guidelines, represented in

as occupiers were given staggered dates to reopen Figure 2 by the 3% reopening rate seen in April.

REOPENING RATE BY MONTH OF VISIT

Figure 2: Monthly reopening rate across GB by month of field research visit across 2020 (Source: Local Data Company)

Analysis of the units surveyed by our field team in the first lockdown. This ‘frozen market’ will have to

September and October 2020, prior to the second thaw in 2021, with the end of the various support

national lockdown in November and circuit breaker packages for businesses and holiday on business

in Wales, showed that 3.6% of businesses had failed rates likely to force their hand. This is likely to result

to reopen and had not vacated their premises since in another jump in closures for the year.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 13G B R ETAIL AND LEISU RE MA RK E T A NA LYS IS - F U LL Y E AR 2 0 2 0

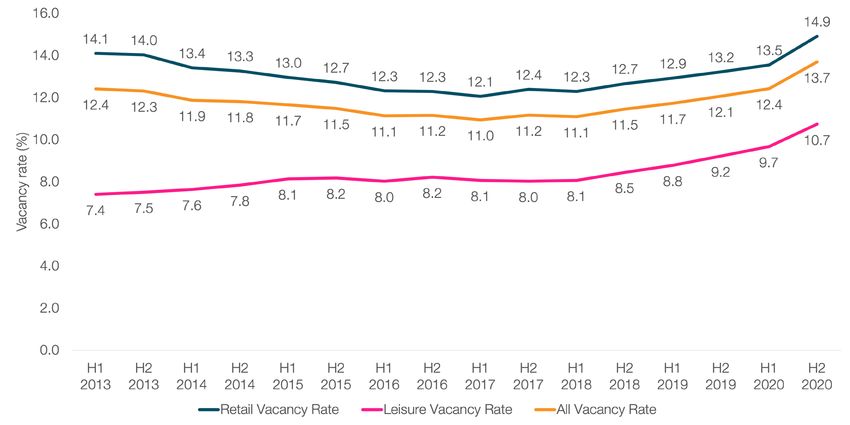

VAC A NC Y

Vacancy Rates increased significantly across the of 2020, the GB average All Vacancy Rate (retail and

board in 2020. With the reopening of the retail sector leisure combined) was 13.7% - the highest on Local

starting on the 15th June, closure activity and the Data Company records (which began in 2013). This

first visible impact of the pandemic on occupancy equates to a 1.6% increase across the year - the

became evident halfway through the year. At the end biggest annual jump in vacancy ever recorded.

HISTORICAL VACANCY RATES

Figure 3: Historical Vacancy Rates by type, 2013 - 2020 (Source: Local Data Company)

For context, even in 2018, widely coined the ‘Year of The Leisure Vacancy Rate (excludes retail units)

the CVA’, the Vacancy Rate only increased by 0.3%, increased by 1.5% in 2020 ending the year in double

emphasising the scale of the challenges faced by digits for the first time ever (10.7%). After years of

the sector in 2020. growth, the leisure bubble burst resulting in an

increase in vacancy of 0.9% in 2019 as many casual

dining brands rationalised their estates. Arguably,

The Retail Vacancy Rate (excludes leisure units) the hospitality sector was one of the worst affected

increased by 1.7% in 2020, the biggest year-on-year by the pandemic, being one of the last sectors to

jump since records began in 2011, ending the year reopen on the 4th July. Despite the brief relief in the

at 14.9%. This was the highest vacancy has been form of the Eat Out to Help Out scheme, operators

since September 2012 as many high street retailers were also hit by restrictions including the curfew and

closed stores for good including Cath Kidston, the rule of six which impacted operating hours and

Oasis, Warehouse and T/M Lewin. Retail closures party sizes, making trading more challenging.

will continue to hit the headlines throughout 2021

with the sale of Debenhams and the Arcadia brands

without their estate of bricks-and-mortar stores

signposting further decline before things improve.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 14 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 15G B R ETAIL AND LEISU RE MA RK E T A NA LYS IS - F U LL Y E AR 2 0 2 0

FA I L U R E S AND JOB LOSS ES

109,407 jobs were lost in 2020, 47% more than due to failure or a CVA compared to 5,793 in 2008,

the same figure at the height of the last recession in which is evidence of the scale of some of the stores

2008 (Source: Centre for Retail Research). Despite affected by the pandemic.

this, fewer stores were impacted with 5,214 closing

NUMBER OF STORES AND EMPLOYEES AFFECTED BY FAILING COMPANIES

Figure 4: Number of stores affected and companies failing in the retail sector, 2007 - 2020 (Source: Centre for Retail Research,

January 2021)

Additionally, the pool of potential buyers with the 53% of ‘at risk’ stores ended up closing, up from

appetite to take on a struggling retail business is low. 36.9% in 2019 (Source: Centre for Retail Research).

Data from the Centre for Retail Research shows that

109,407 JOBS WE R E

L OSTIN 202 0

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 16 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

Donate

You can help us be there #forthefour by

donating what you can. Visit

retailtrust.org.uk/forthefour-donate

Corporate donors can contact

Claire Greenwood at

cgreenwood@retailtrust.org.uk

Championing the health of retail

Join us!

Join the conversation about health

While one in four adults in the UK will and wellbeing in the retail industry.

experience a mental health problem at

some point in their lifetime, we believe we 10-11 Our virtual event will take place

should be there #forthefour in four MAY during Mental Health Awareness

colleagues who will experience a setback or Week. Join us to create health,

life event. happiness and hope for everyone

involved with retail.

Join us! Be there #forthefour Register at

retailtrust.org.uk/forthefour retailtrust.org.uk/forthefour

retailTRUST is a registered charity in England and Wales (1090136) and in Scotland (SC039684). Company No 4254201 (Company

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

limited+44

by (0)

Guarantee) Registered England & Wales. Registered office: Marshall Estate, Hammers Lane, London, NW7 4DQ.

20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 17G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

LOC ATIONS

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 18 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

LOCATIO NS

This section of the report provides a more detailed Standalone units are those that sit outside of the

review of the impact of the pandemic across various three other location types such as supermarkets,

location types and asset classes; High Streets, hardware stores and furniture retailers, which are

Shopping Centres, Retail Parks and Standalone as often located outside the main town centre boundary

well as a review of how redevelopment activity was in residential areas.

impacted in 2020.

O P E NI N GS A ND CLOS UR ES BY L OCATION TYPE

Shopping Centres have been the most negatively 1.5% loss in 2019. Standalone locations were more

impacted of all location types in 2020, with a net resilient in 2020 as the benefits of being accessible

loss in occupied units of 5.4%. There was a marginal by car and their proximity to residential hubs met the

reversal in the negative trajectory for Standalone needs of the population under lockdown.

locations with a net loss of 1.3% compared to the

PERCENTAGE NET CHANGE IN OCCUPIED UNITS BY LOCATION TYPE, 2018 - 2020

Figure 5: Percentage net change in occupied units by location type, 2018 - 2020 (Source: Local Data Company)

SHO PP I N G CENT RES HAVE BE E N THE

M O ST NEGAT IV ELY IMPACTE D OF AL L

L O C AT I O N T Y P ES

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 19G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

VAC A NC Y R AT ES BY LOCATION TYPE

The sharpest increase in vacancy was seen in distancing measures, due to the indoor nature of the

Shopping Centres, rising from 14.4% at the end assets. Shopping Centres were also the last to open

of 2019 to 17.1% at the end of 2020. This reflects following the first lockdown, especially in Scotland,

an incredibly tough year for Shopping Centres as where they were only able to reopen from the 13th

they faced the biggest challenges around crowd July.

management and implementing rigorous social

HISTORICAL VACANCY RATE BY LOCATION TYPE, 2013 - 2020

Figure 6: Historical vacancy rate across GB, by location type H1 2013 - H2 2020 (Source: Local Data Company)

Shopping Centres also have the lowest percentage Vacancy on Retail Parks increased by 1.9%, hitting

of retailers classified as ‘essential’ which resulted in double digits for the first time ever and High Streets

huge proportions of large schemes shutting down saw the smallest increase in vacancy of all three

for months at a time. On average only 15.4% of location types (+1.6%).

Shopping Centre units are classified as ‘essential’

compared to an average of 28.7% for Retail Parks.

Additionally, Shopping Centres are the most exposed

to Comparison Goods retail, which was struggling

ON AVE RAG E ON LY

15.4%

to compete with online, even before the pandemic

pushed even more consumers to shop in this way.

On average, 57% of units in Shopping Centres are

Comparison Goods stores, significantly more than

the average for the High Street (28%).

OF SHOPPIN G CE NTRE UN ITS A R E

CL ASSIF IE D AS ‘E SSE NTIA L ’

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 20 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

R E G I O N AL VACANCY RAT E S

The Vacancy Rate in Wales increased the most of all region were some of the most resilient, due to the

GB nations and regions, rising from 16.4% to 19% in fact that many are less exposed to leisure, with

2020. Wales was one of the slowest locations to be 14.4% of units in this category compared to the GB

released from lockdown, which was felt especially average of 16.2%. Vacancy increased in Shopping

hard across Shopping Centres in the nation, wher Centres in the North West by just 1.1% compared to

the Vacancy Rate increased rapidly from 15.4% at a GB average of 2.7%.

the end of 2019 to 21.8% at the end of 2020.

The second highest Vacancy Rate increase was

The North West saw the least movement in this seen in the South West, rising from 11.8% to 13.9%

metric, with a small increase in Vacancy Rate of in 2020.

0.6% across the year. Shopping Centres in this

REGIONAL VACANCY RATE, 2019 VS 2020

Figure 7: Regional vacancy rates, 2019 vs 2020. (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 21G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

PE R S IST ENT VACANCY

In 2020, the pandemic impacted both short-term to double from 0.8% in 2019 to 1.9% at the end of

and long-term vacancy, as the lack of activity in the 2020. The recent demand for Retail Park space is

market suppressed demand for space, leading to likely to see some units find new occupiers in the

many vacant units remaining as such. form of acquisitive brands looking to expand their

out-of-town portfolio. However, the risk is that not all

of these units will find new tenants, particularly those

Across GB High Streets, the percentage of units that on Retail Parks that lack strong anchor tenants,

had been vacant for more than three years increased or lack a diverse retail and leisure mix enhanced

by 0.5%. Retail Parks saw the smallest increase by grocery which has performed well during the

in long-term vacancy at 0.4%, however the flurry pandemic. Therefore, some units are likely to remain

of failures across this sector in 2018 (Mothercare, vacant for many years to come unless redevelopment

Maplin and Toys ‘R’ Us) caused the percentage of or a change of use is considered.

units lying vacant for between two and three years

PERSISTENT VACANCY BY LOCATION TYPE, 2020

Figure 8: Persistent vacancy rate by location type and length of time vacant, 2020 (Source: Local Data Company)

SOM E UN ITS ARE L IKE LY TO RE M AIN

VACANT F OR M ANY YE ARS TO COM E

U N L E SS RE DE VE L OPM E NT OR A CHAN G E

OF USE IS CONSIDE RED .

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 22 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

R E D E V E LOP MENT ACT IV IT Y

Redeveloping and repurposing retail property is had jumped by 385% since 2015. Inevitably, this

increasingly being discussed as a way to combat dipped by 16% in 2020 as the market was shut

the rising numbers of vacant units as consumer down and many investment projects were paused

demand changes. This strategy offers investors due to the uncertainty caused by the pandemic. In

and developers the opportunity to create innovative 2020, over 1 in 5 units that were redeveloped were

mixed-use schemes or change the use case for located in Greater London (23.9%) and the West

an asset, such as reworking it as a logistics or Midlands saw the biggest slowdown in this activity

warehousing hub. LDC data show that the pace of indicating that there will be regional differences in

redevelopment increased significantly in 2019 and demand for alternative uses.

NUMBER OF UNITS BEING REDEVELOPED, 2015 - 2020

Figure 9: Redevelopment activity by number of units across GB, 2015 - 2020 (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 23G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

C ASE ST UDY – WEST BY FLE E T

West Byfleet is in the top 20 towns across the demolished completely. This resulted in the Vacancy

country in regard to pace of redevelopment activity Rate improving drastically from 16% in 2019 to 5.3%

in 2020. Situated in Surrey, it is a key commuter town in 2020. Some of the brands that closed prior to the

with a journey time of 30 mins into London Waterloo, units being demolished were Costa, Londis, Boots

making it an attractive location for investment. and LloydsPharmacy.

More than a third of the total activity (openings and The proposed new mixed-use redevelopment

closures) in West Byfleet were units undergoing scheme will contain 255 residential units, 300 sqm

redevelopment or being taken out of the retail market. for a new community hub or library and up to 5,000

A total of 20 units were removed with 18 being sqm of retail and leisure space.

Figure 10: Station approach, West Byfleet prior to the demolishment (Source: Local Data Company)

As with most redevelopment plans, the West Byfleet as the surrounding oversupply of retail property is

scheme still features retail and leisure at its core. addressed. These new units are likely to attract a

This reflects the confidence from town planners strong tenant line up due to the immediate catchment

that physical retail and leisure still has a place providing a ready customer base for convenience,

in the community, and how attractive it still is to service and leisure operators to reinvigorate the local

developers in terms of income and stability - as long economy.

Figure 11: Artist’s impression of the future of West Byfleet (Source: Altitude Real Estate Limited)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 24 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

HY PE R - L OCA LIS AT I ON

With national lockdowns and ongoing restrictions service and convenience offer and higher balance

rendering consumers largely confined to their of independent retailers were more resilient in 2020,

immediate locality, the concept of hyper-localisation seeing an increase in vacancy of 0.4% compared

has been a key talking point across 2020. to the GB average of 1.6%. This is further evident

when assessing changes to Vacancy Rates across

City Centres, which have seen footfall plummet as

This trend can be evidenced through analysis of workers and student populations have been working

change in Vacancy Rates for different profiles of remotely. The Vacancy Rate across City Centres

town. Village locations, which are more residential increased by 2.5% to 16.1% in 2020, the highest of

with a smaller comparison retail offering, a larger all town profiles analysed.

VACANCY RATE BY TOWN PROFILE, 2019 VS 2020

Figure 12: Vacancy rate by town profile across GB, 2019 - 2020 (Source: Local Data Company)

The move to remote working was a catalyst for Commuter towns have been able to sustain higher

the significant loss of shops and hospitality outlets levels of weekday footfall and spend, with home

across City Centres, as the supporting retail workers visiting coffee and takeaway food stores

provision lost customers almost overnight. However, across the week. Pre-pandemic, these visits would

the surrounding commuter towns have benefitted have been within proximity to their office.

from this shift to home working, as this profile saw

vacancy increase by 1.2%, below the GB average

THE VACANCY RATE

of 1.6%.

ACROSS CITY CE NTRE S

2.5%

INCRE ASE D BY

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 25G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

C ASE ST UDY – HECK MONDWIKE

The town of Heckmondwike in West Yorkshire has home for the majority of the pandemic. 46.5% of

remained resilient during the pandemic, reflected by the working population in the local authority area

a drop in vacancy in 2020. The town sits 9 miles south are in the three top occupation groups associated

west of Leeds, 2.8 miles from nearby Dewsbury. with white collar workers (Source: Office of National

The catchment for the town is mainly comprised Statistics).

of commuters, who would have been working from

R E TA I L M IX

81.7% of the units in Heckmondwike are independent ‘essential’, above the national average of 2 in 10,

which is significantly above the GB average of 65% which will have sustained a higher volume of footfall

and has increased by 5.4% since 2017. Additionally, during the lockdowns.

3 in 10 of the town’s retailers are classified as

BUSINESS TYPE MIX IN HECKMONDWIKE, 2017 VS 2020

Figure 13: Business type mix across Heckmondwike town centre, 2017 & 2020 (Source: Local Data Company)

N O N - ES SEN T I A L V S . E S S E NT I A L

R ETAIL M IX IN HE CK MOND WI K E

Key retailers in the town centre across the

town centre that are week and throughout

classified as ‘essential’ lockdowns.

are food and discount

chains Morrison’s, Lidl

and Poundstretcher,

with these brands able

to attract footfall to the

Figure 14: Percentage of non-essential vs essential retail in

Heckmondwike as of March 2020 (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 26 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

Key retailers in the town centre that are classified as fallen into administration is limited and the town was

‘essential’ are food and discount chains Morrison’s, able to attract new, independent occupiers across

Lidl and Poundstretcher, with these brands able to leisure, service and comparison retail categories.

attract footfall to the town centre across the week

and throughout lockdowns.

Additionally, the town had reopened 95% of the

‘non-essential’ retail outlets that were forced to close

Vacancy in Heckmondwike decreased by 3.3% in in the first lockdown in September, 9% above the

2020, despite the ongoing restrictions impacting GB average of 85%, demonstrating that the level of

the retail and leisure units in the town. Exposure to footfall was enough to sustain trade over the course

national chains that have undergone CVAs or have of the pandemic.

VACANCY RATES IN HECKMONDWIKE, 2015 - 2020

Figure 15: Historical Vacancy Rate in Heckmondwike, 2015 - 2020 (Source: Local Data Company)

In total five units did not reopen after the first

REOPENING RATE OF NON-ESSENTIAL

lockdown. This equates to 5% of the total units that

UNITS IN HECKMONDWIKE

were forced to close due to their ‘non-essential’

status. Of the five units, only one remains vacant,

with the other four finding new occupiers.

95%

H E C K MONDWI K E REOP ENED

O F N O N-ESS ENT IAL RETA IL

Figure 16: Reopening rate of non-essential retailers in Heckmondwike

as of October 2020 (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 27G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

SEC TORS

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 28 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

SECTO RS

This section of the report reviews net change across the Local Data Company, quantifying the varying

the four top-level retail classifications (Leisure, performance across different corners of the market

Service, Comparison Goods and Convenience) in 2020 and historically.

and the 400 retail and leisure categories tracked by

NE T C HA NGE

Net change data across the four top-line categories moved online, with most retailers reliant on digital

tracked show a clear divergence between ‘essential’ channels for revenue during periods of lockdown.

(mainly Convenience and Service) and ‘non-essential’ With the majority of social events cancelled, there

retail (mainly Comparison Goods and Leisure). were fewer reasons for consumers to purchase new

outfits and other personal grooming items, which

also had a significant impact on fashion and beauty

The Comparison Goods market declined by a net businesses. The Shirtmakers category was one of

6,984 units in 2020, which is mainly a result of the most impacted by the pandemic, with limited

the fact that this sector was forced to close for a demand for workwear alongside the demise of T.M

large proportion of the year. The pandemic has Lewin resulting in this category shrinking by 62% in

also accelerated the pace at which this sector the year.

HISTORICAL NET CHANGE IN OCCUPIED UNITS BY RETAIL CLASSIFICATION,

2012-2020

Figure 17: Net change in units by retail classification across GB, 2012 - 2020 (Source: Local Data Company)

The impact on the leisure sector has been much category which continued to be negatively impacted

discussed and data reflects the stories that were by a change in legislation back in 2019. The Pizza

told by occupiers across the year. Pubs (-833), Italian Takeaway and Fast Food categories conversely both

Restaurants (-309), Take Away Food Shops (-245) appeared in the fastest growing categories list as the

and American Restaurants (-130) saw the highest demand for takeaways skyrocketed.

numbers of closures, following Bookmakers – a

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 29G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

There was a marginal slowdown in the decline of

both the Service and Convenience categories (which

are mostly comprised of ‘essential’ occupiers) in

2020. The Convenience category decreased by 618

stores, the lowest decline since 2016, driven by the

higher demand for local grocery stores as travel was

limited. Not all Convenience categories benefitted

from the change in consumer behaviour, with the

loss in Newsagents continuing at the same pace

seen previously. Newsagents were disadvantaged

by their lack of fresh produce, small footprint which

made social distancing difficult and the decline in

the paper newspaper and magazine market which

is increasingly moving towards digital subscription

models. Others previously relied on the high volumes

of footfall passing through transport hubs, which

was very low for most of 2020.

There was a slowdown in the decline of the Service

category, with the net loss reducing to 1,077 in

2020, compared to 1,460 in 2019. Estate agents

accounted for 56% of the total net decline, losing

605 units in the year, however this figure was also

down on the previous year (-827). This slowdown

is in part due to the stamp tax holiday introduced

in July, designed to help stimulate recovery of the

economy. The scheme has been a success, with

residential property transactions up 26% in 2020

(Source: Zoopla) despite mass job losses and the

onset of the recession.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 30 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

Making town

centre property

marketing easier

At Completely Retail we understand there has

never been a more challenging time for retail,

with vacancy levels at an all time high, especially

on the High Street. Local Authorities and Business

Improvement Districts (BIDs) are doing all they can

to bring life back into town centres.

Each BID page contains:

y A comprehensive list of all available

properties to rent within the BID

district on CompletelyRetail.co.uk,

the UK’s leading retail property

portal.

y Unlimited detail, property contacts,

Using our retail expertise and relationships

photos, brochures, plans with

with Agents and Landlords we want to help BIDs

properties shown in context on a

market their empty shops to prospective retails

town centre map.

and get the High Street buzzing again.

y Help and advice from local property

We have thousands of national and local retail

experts for local businesses and

brands searching CompletelyRetail.co.uk every

entrepreneurs looking to acquire their

week looking for their perfect premises. To make

first shop in your town centre.

the process easier for them, we will create a

page allowing visitors to see each district as a y Links to other useful local resources,

destination with glorious detail on every available shopping centres, local authority etc.

unit. There is also information about the major

shopping centres, with links to, and useful advice

from, local retail property experts.

Further details

If you would like further information

email sales@completelygroup.com

CompletelyRetail.co.uk Read more about our BID campaign at:

www.completelyretail.co.uk/BIDS

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 31G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

TO P 1 0 GR OWI NG CAT EGORIE S

Despite an intensely challenging year, some things of DIY haircuts. New Barber units were seen across

remain constant. Once again, Barbers topped the all location types, including Retail Parks which

fastest growing list for the 4th consecutive year, increased by 35%. Units increased across Shopping

with growth of 800 units, 18 more than 2019. The Centres (+9%), High Streets (+6%) and Standalone

reopening of barbers and hairdressers at the start (+5%) also.

of July was a huge relief to many, following months

TOP 10 GROWING CATEGORIES IN 2020

Figure 18: Top 10 growing retail categories across GB by net change in units, 2020 (Source: Local Data Company)

The real success story of 2020 was Convenience The Fast Food Takeaway category also saw a

Stores; after four years of decline, this category reversal in fortunes for the better, moving from

entered the top 10 fastest growing list for the first decline in 2019 (-117) to growth in 2020 (+267). 87%

time since 2015. The category grew by 149 units of this growth was driven by independent openings

across the year, feeling the benefit of the increase in across High Streets and Standalone locations, with

localised shopping, the ‘essential’ nature of their offer entrepreneurs taking advantage of the spike in

and the increased demand for grocery shopping due demand for food delivery.

to the shutdown of the hospitality sector. The ONS

reported a 4.4% annual growth in food sales in 2020

(Source: ONS Retail Sales, December 2020) which Gyms was a surprising category to enter the top

reflects this trend. 10 growth categories, given this sector was one

of the last to reopen following the first lockdown.

When they did reopen, many had to invest in refits

Supermarkets also feature in the top 10 fastest to ensure that they could meet the strict government

growing list, alongside a huge surge in demand for protocols. Again, the growth of gyms was largely

online delivery; the ONS reported that online food driven by independents, taking advantage of the

sales were up 79.3% in 2020. Despite this, the relaxed planning laws to open yoga studios, boxing

physical store network grew by 101, indicating that gyms and Pilates centres at a time when the public

bricks and mortar is still a key part of the growth had a renewed focus on health and wellbeing. Some

strategy for Supermarket brands. national chains saw growth in 2020, including Pure

Gym, The Gym, Anytime Fitness and Snap Fitness.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 32 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

TO P 1 0 GR OWI NG CAT EGORIE S – SURVIVAL RATE S

Survival rates is the measurement of the length of time Grocers had the lowest rate of survival at 62%. 100%

occupiers within retail categories remain operational of this category is independent, which tend to have

before shutting up shop for various reasons. This lower survival rates when compared to multiples.

metric can help to determine how resilient categories Grocers include mini marts and ethnic food stores

are and the likelihood of long-term survival. For this located in high density residential locations.

analysis, we review the occupiers within the top 10

growing categories that opened in 2017 and are still

operational 3 years on to determine how resilient the Interestingly, the only subcategory that saw

new units which opened in 2020 are likely to be. Of independents outperform multiples was Beauty

the 10 fastest growing categories, 7 saw more than Salons, where independents had a survival rate of

75% of new stores survive for at least three year 71% compared to multiples at 68%. This is mainly

after opening. due to the fact that limited businesses in this

category have been able to reach scale, with the

largest beauty salon operator only having 50 units

Supermarkets had the highest survival rate with nationwide.

90% still operational three years from opening, rising

to 96% when considering multiples alone. 72% of

independent supermarkets were still operational

three years from opening.

PERCENTAGE OF UNITS IN TOP 10 FASTEST GROWING CATEGORIES STILL

OPERATIONAL AFTER THREE YEAR S, 2017-2020

Figure 19: 3 year survival rate of the top 10 fastest growing categories, 2017- 2020 (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 33G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

TO P 1 0 D ECLI NING CAT EGO RIE S

Bookmakers continued to close in 2020, with a 2020 brought about further challenges for the Pubs

loss of 944, the highest rate of decline seen for any sector with lengthy periods of closure, limitations on

category in one year. The shakeout in this market group sizes and curfews restricting trading. Pubs

is mainly due to the changes to regulations of fixed declined by 833 in 2020, however many are still

odd betting terminals which came into effect in April temporarily closed following the first lockdown in

2019. The sector has seen 1,677 units close since March 2020, so this figure is somewhat diluted, and

this date. William Hill accounted for almost half of we expect to see further decline in this space.

these closures (832).

TOP 10 DECLINING CATEGORIES IN 2020

Figure 20: Top 10 declining retail categories across GB by net change in units, 2020 (Source: Local Data Company)

Another regular feature in the top 10 declining list The loss of Mobile Phone stores was mainly driven

is Fashion Stores, with many businesses falling by Carphone Warehouse, which closed 531 stores

into administration, launching CVAs or estate in March, however this was not a response to the

rationalisation programmes in 2020 including pandemic, but a strategic decision with Dixon

Cath Kidston, Warehouse, Oasis, Roman, M&Co, Carphone to combine its Carphone Warehouse

Peacocks and New Look. concept with its large format concepts, Curry’s and

PC World.

Retail sales across the fashion sector declined by

RE TAIL SAL ES

25.1% in 2020 according to the ONS (Source: Office ACROSS THE FASHIO N

25.1%

of National Statistics, 2021) – the highest annual SE CTOR DE CL IN E D BY

decline across all retail categories. The number of

Women’s Clothes Stores also fell (-390) resulting

in the overall decline across the Fashion & General

Clothing category equating to 1,846 for the year.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 34 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

MU LT I PL E S VS I ND EP END ENTS

Accelerating the trend seen since 2014, the It should be noted that 2020 data does not include

multiples market declined considerably faster than the failures of Arcadia or Debenhams which occurred

independents in 2020 – declining by a net 9,877 in early 2021. We expect the 2021 to push the figures

units compared to 1,442 for independents. The to a record once more, with market turbulence set to

contrast is even greater reviewing the figures in get worse before it gets better. There was a 7% drop

percentage terms, as independents make up 65% in overall activity (openings plus closures) across

of the total retail and leisure market. The multiples multiples in 2020, a figure driven mostly by a 21%

market shrank by 4.5%, compared to independents drop in openings.

at just 0.4%. Despite the record decline, the year-

on-year acceleration was not at fast as the increase

seen in 2017/2018 with the huge volume of CVAs

that took place in 2018.

NET CHANGE IN OCCUPIED UNITS BY BUSINESS TYPE, 2013 - 2020

Figure 21: Net change in occupied units by business type across GB, 2013 - 2020 (Source: Local Data Company)

Closures of independent units also slowed by 11% in • The extension of the lease forfeiture moratorium

2020, as businesses relied on government support allowed occupiers to continue to trade 2020

measures, both of which are likely to end in 2021: safe in the knowledge that they could not be

evicted from the premises.

• The business rates holiday that was offered

to all occupiers to the end of March 2021 It remains to be seen what success these initiatives

had the desired effect in 2020 and allowed have had in terms of securing a longer term future

more independent occupiers to weather the for these businesses. It could well be likely that a

challenges thrown at them during the course of second wave of closures occurs, especially across

the pandemic. independent businesses as the true impacts of the

pandemic are felt.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 35G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

Behaviours moving online

≠ buying online

Nick Brackenbury, Co-Founder & CEO at NearSt

One of the most discussed retail trends of 2020 was the tidal wave of shopper behaviours

moving online, as millions of people were pushed to experiment with getting the products

they want in new ways. As an industry though we have conflated behaviours moving online

with buying online, and in doing so overlooked another even more important change in

how people shop that will have a massive positive impact on the high street.

Shoppers are going online to find products locally

We all know that people are buying more online - ecommerce sales grew by 40% in 2020

- but there has been an even more dramatic increase in people going online to find

products locally.

At NearSt we power live in-store inventory in places like Google for thousands of retailers,

and each month see millions of searches for products in local stores. That’s a person tapping

into Google things like “who has gluten free flour in stock” or “where can I get men’s brown

brogues size 8” and seeing a product in search results that’s stocked nearby.

During the first lockdown these searches for in-store product availability jumped by 7x

compared to their February 2020 levels and jumped again to 8x that level during the

November and December restrictions.

NearSt Local Product Search Index. 1 = Feb 2020 average.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 36 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

Are these temporary or permanent changes?

While one might initially think that these changes are only driven by lockdown restrictions,

our data suggest there is significant long term adoption happening.

During the summer, when there were very few restrictions in place, local product search

levelled off at 3x its pre-pandemic levels. In the first lockdown many people suddenly

discovered they could easily check local in-store product availability in Google, and

continued doing it as a matter of convenience post-lockdown. Today we are sitting at 4.5x

pre-pandemic levels of local product searches.

What this means for high street shops

Retailers have an incredible opportunity to capture shoppers who are searching and

browsing online, and direct them with intuitive convenience to their local store. Shoppers

have a ton of goodwill towards their local high streets, and today there is an opportunity to

make acting on that goodwill genuinely more convenient than shopping online, using the

web to drive really meaningful footfall.

Today Google is the most advanced of the platforms enabling shops to offer this local in-store

availability to shops, but other tech titans like Facebook and Uber are rapidly developing

offerings of their own.

While the rise of ecommerce may have dominated the headlines in 2020, I firmly believe

that 2021 will be the year we’re all talking about the rise of local product discovery online,

where the web is a driver rather than detractor of growth on the high street. And that is truly

something to be optimistic about.

NearSt is a retail technology company that drives footfall for

high street retailers. Their technology makes in-store inventory

visible online in places like Google and Facebook, and is a

Global Google technology partner.

To find out more visit near.st.

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 37G B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

BRA N DS

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

Page 38 +44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.comG B RETAIL AND LEIS U RE MA RK E T A NA LYS IS - F UL L Y EAR 2 0 2 0

BR A N DS

C VA / A D M INIST R AT ION ACTIVITY

A fresh wave of occupiers launched a CVA or fell into In order to understand the likely long-term impact of

administration in 2020 as the pandemic proved to CVA/administration activity, analysis was completed

be the final straw for many already facing challenges. on the current status of units impacted by these

This has and will continue to result in many store processes in 2018. Figure 22 lists the percentage

closures as occupiers look to exit any locations of units which had been reoccupied as of January

which are not viable in the current trading climate. 2021. In total, of the 776 units that closed, 434 have

been reoccupied, 272 remain vacant and 69 have

been redeveloped (merged, split or demolished).

PERCENTAGE OF STORES THAT CLOSED IN 2018 DUE TO CVA/ADMINSTRATION

THAT ARE CURRENTLY OCCUPIED

Figure 22: Percentage of former stores reoccupied since CVA closures, as of January 2021 (Source: Local Data Company)

Local Data Company Ltd, 13-19 Vine Hill, London, EC1R 5DW. All Rights Reserved.

+44 (0) 20 3111 4393 | team@localdatacompany.com | www.localdatacompany.com

Page 39You can also read