Tencent Holdings (TCEHY) Deep Dive Analysis - George Gammon

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Tencent Holdings (TCEHY)

Deep Dive Analysis

August 30, 2020

This report focuses on macro updates, discusses the latest portfolio changes,

and then analyzes Tencent, the fast-growing Chinese internet titan.

U.S. Business Cycle Update

Here’s a recap of current economic conditions in the United States, divided

into a few sections.

Jobless Claims Update

The latest weekly numbers for jobless claims are that 1 million people filed

initial claims in the most recent week, while 14.5 million people filed

continued claims.

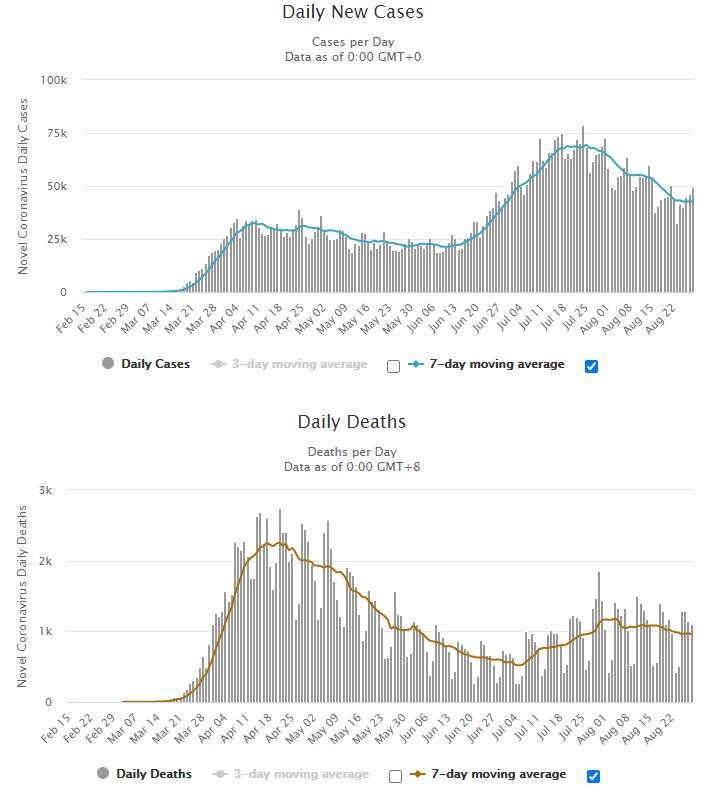

Chart Source: St. Louis Fed At the peak level of economic shutdown, nearly 25 million continued claims were filed, so more than 10 million of them fortunately went back to work since then. Continued jobless claims at 14.5 million are coming off somewhat slowly, and even at these reduced levels, remain more than twice as high as during the peak of the 2009 unemployment crisis. COVID-19 For some good news, COVID-19 daily deaths in the United States continue to stabilize and decrease:

Chart Source: Worldometer The United States has among the most cumulative death rates per capita from the virus among large developed countries, and we still continue to have

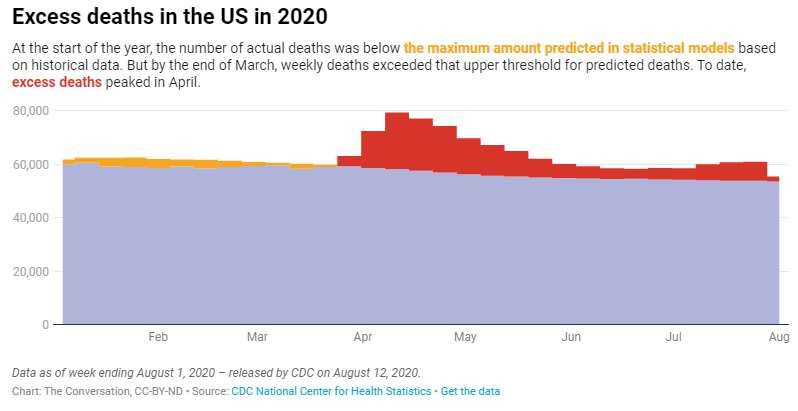

elevated new cases and new deaths compared to most peers, but the arc points firmly down now. Some people naturally question the number of COVID-19 deaths. For example, if someone dies in a hospital for unrelated reasons, can’t they be mistakenly or intentionally classified as a COVID-19 death, especially if the hospital gets more reimbursement for COVID-19 deaths than many other types of deaths? Maybe the U.S. just has higher COVID-19 deaths because we test so much now, or because we classify the deaths differently? Unfortunately, while that’s a logical line of thinking, collaborative evidence using a separate measurement method suggests that’s not the case. If we ignore the type of deaths and just looked at how many excess deaths occurred in 2020 from all causes, compared to what should statistically occur, the number actually slightly exceeds the number of official COVID-19 deaths, and in a precise shape and time that is obviously related to COVID-19: Chart Source: MarketWatch

By this count, there were more excess deaths during 2020 than the number of deaths official attributed to COVID-19, by roughly 10% or so. This tells us, through a totally different way of measuring it, that the number of reported COVID-19 deaths is relatively accurate, and if anything, understates it slightly. And this makes sense, because due to the limited nature of testing, there would naturally be more people that die from COVID-19 that were never tested and never confirmed to have had it and thus were not classified as having died from it, than people who didn’t die of COVID-19 but were mistakenly or intentionally classified as having died from it anyway. And it’s a bigger excess death count than the flu, by a lot. Most flu seasons are mild (already accounted for in statistical annual death rates during those months), and some are particularly bad (exceeding normal annual death rates), but COVID-19 is notably worse than a bad flu season, even though unusual containment measures and changes in peoples’ behavior were used to control its spread: Chart Source: MarketWatch The good news, however, is that the overall kill rate of the virus remains quite low.

As of this writing, based on the U.S. official number of cumulative confirmed

cases and deaths, the virus has about a 3% kill rate, and that mostly comes

from people with pre-existing conditions that make them vulnerable to it. If

nursing homes and other vulnerable populations are protected, the fatality

rate goes way down.

And because the majority of people were not tested, it is broadly considered

very likely that far more people have had it than the confirmed cases, which if

true means the death rate is way lower than 3%.

How bad the virus is exactly, depends on perspective, even if we just focus on

numbers in the United States.

On one hand, with a 187,000 death count and rising, this virus has so far

killed:

• More than 60x as many Americans as the 9/11 terrorist attacks did.

• More than 30x as many Americans as died fighting in the wars in

Afghanistian and Iraq combined.

• About as many Americans as died fighting in World War I and the

Vietnam War combined.

• Nearly half as many Americans as died fighting in World War II.

On the other hand, less than 0.06% of the American population has died from

the virus.

This big psychological divergence in absolute numbers and percentages makes

it a very complicated sociopolitical issue to report and discuss. It is easy to

spin it in various ways to make it either look worse or not as bad compared to

reality, in order to suit various competing agendas across the political

spectrum.

If we look broadly internationally, most countries now have the virus under

control according to reported numbers. Brazil was late, but they are starting to

contain it. India is the last major country where it’s still rising, but the rate of

change is beginning to improve, and looks set to hopefully peak in September.

Let’s see.

Jackson Hole: Fed Chair Speech

The big financial news this week involved Federal Reserve Chairman Jerome Powell’s speech at the Economic Policy Symposium in (virtual) Jackson Hole on Thursday. Every year, central bankers and other folks in high finance from around the U.S. and from international locations gather in Jackson Hole, Wyoming, to discuss monetary policy and other economic trends. This year’s event was held virtually due to the impact of the virus on travel. For months now, the Fed has been saying that they will review their policy framework and provide updated forward guidance on how they will operate. News broke early last week that the Fed’s chairman Jerome Powell would give a “pivotal” speech at the symposium about the Fed’s new policy, particularly in regards to inflation. As a long-term background for people who don’t follow this closely, the Fed has two congressional mandates, which are known as the Fed’s “dual mandate”: 1. Price stability 2. Maximum employment Historically, the Fed tightens monetary conditions (raises interest rates) to contain inflation, and loosens monetary conditions (lowers interest rates and/or uses quantitative easing, aka “money printing”) to improve employment conditions. So, how tight or loose they want to be depends on whether inflation or employment is more of a concern at the moment. Back in 2012, the Fed introduced an annual inflation target of 2%, which was roughly a ceiling on how much inflation can reach before it is considered too high and requiring more management to ensure price stability. They measure inflation with “core personal consumption expenditures” or PCE for short, which is a basket of price estimates that uses some substitution methods and policies that many argue understates actual cost of living. It’s quantifiable, even if not perfectly representative. And it factors out volatile things like food and energy. So, it is what it is. Ever since the current economic slowdown began back in 2018, the Fed began referring to this more heavily as a “symmetric target of 2%”, meaning that since inflation as measured by PCE averaged only about 1.5% over the past

decade, notably below their target, they are willing to let it overshoot to maybe 2.5-3% for a little while so that the long-term average is closer to 2%. And in FOMC meeting minutes in 2020 so far, Fed officials confirmed that they want to let inflation overshoot and run hot for some time, in response to such a long period of low inflation according to that measure, and because of the scale of the disinflationary shock that happened from the economic shutdown and job losses. Well, at the symposium, Powell solidified this symmetric approach by emphasizing average inflation targeting, and announced that they will let inflation run hot next time before actively trying to contain it. Here’s the core paragraph of Powell’s speech: We have also made important changes with regard to the price-stability side of our mandate. Our longer-run goal continues to be an inflation rate of 2 percent. Our statement emphasizes that our actions to achieve both sides of our dual mandate will be most effective if longer-term inflation expectations remain well anchored at 2 percent. However, if inflation runs below 2 percent following economic downturns but never moves above 2 percent even when the economy is strong, then, over time, inflation will average less than 2 percent. Households and businesses will come to expect this result, meaning that inflation expectations would tend to move below our inflation goal and pull realized inflation down. To prevent this outcome and the adverse dynamics that could ensue, our new statement indicates that we will seek to achieve inflation that averages 2 percent over time. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time. -Jerome Powell, Jackson Hole, August 2020 In 2018 and 2019, Powell and the FOMC began raising interest rates, even though PCE inflation was below 2.2%, because employment was pretty high. In other words, with employment at ideal levels and inflation as they measure it bouncing around near the high end of their target (even though it had averaged below their target over the past decade), Powell began trying to give the Fed additional ammo to fight the next recession, and raised rates preemptively.

The problem, in Powell’s view, was that the Fed cuts interest rates to fight recessions and boost employment levels, but the interest rate was already near-zero when he took over as the Fed’s chairman. In his mind, he had to raise rates so that whenever the next recession comes, he’d be able to cut rates back to zero. If rates are already near-zero when a recession hits, he is more limited in the actions he can take. In Powell’s speech, he basically said they won’t do this next time. They won’t preemptively raise rates at early signs of rising inflation and decent employment levels. They will let inflation run hot before they consider trying to contain it. In most ways, Powell didn’t really say anything new, at least for folks that follow FOMC meeting minutes. This was already what the Fed was planning, as they specifically said at meetings that they would likely let inflation overshoot its target level in the coming cycle. Lawrence McDonald, former head of Macro Strategy at Soc Gen (one of France’s largest investment banks), summarized the speech well in meme form (using a popular meme template based on American Chopper):

And… that’s it. The Fed can’t create inflation unilaterally, unless they use extreme measures that they probably won’t resort to. With their normal tools, including rate manipulation and bond purchases, they can only choose how much to contain inflation, and they’ve signaled in meeting minutes and now at virtual Jackson Hole, that they are not going to contain inflation as quickly in the next cycle. Even if inflation runs hot, they will be slow to raise rates, and will probably use yield curve control at some point to keep Treasury rates well below the prevailing inflation level, for quite some time. But they can’t create inflation with their normal tools. In multiple prior speeches, Powell has suggested that Congress should do more fiscal spending to boost the economy, which is a true source of inflation pressure. Congress can create inflation more-so than the Fed. In order to create inflation in the current high-debt environment, it would require massive fiscal deficit-spending that the Fed mostly monetizes, and for the Fed to stand-by and it let it all run hot. This is what happened in March 2020, except it was in response to a deflationary shock and solvency crisis, so the net result was reflationary (moving inflation back up from a briefly very low level to normal levels) rather than outright inflationary (driving up inflation to higher-than-normal levels). It’s unusual for a Fed chair, who is traditionally supposed to be apolitical, to refer so directly to fiscal policy, but being low on ammo in terms of monetary policy tools at zero interest rates, that is what he has done a number of times this year. The Fed will monetize deficit spending as needed by buying Treasury securities and containing rates, but the Fed itself can’t spend into the economy. Only Congress can spend into the economy. The Fed’s role is now secondary, having run firmly into the zero bound of interest rates and having bought a large number of bonds by expanding the monetary base. In the two trading days after the speech last week, inflation breakevens in the Treasury market went up slightly, Treasury bond yields went up slightly, and the dollar experienced a day of volatility and then fell a bit vs other major

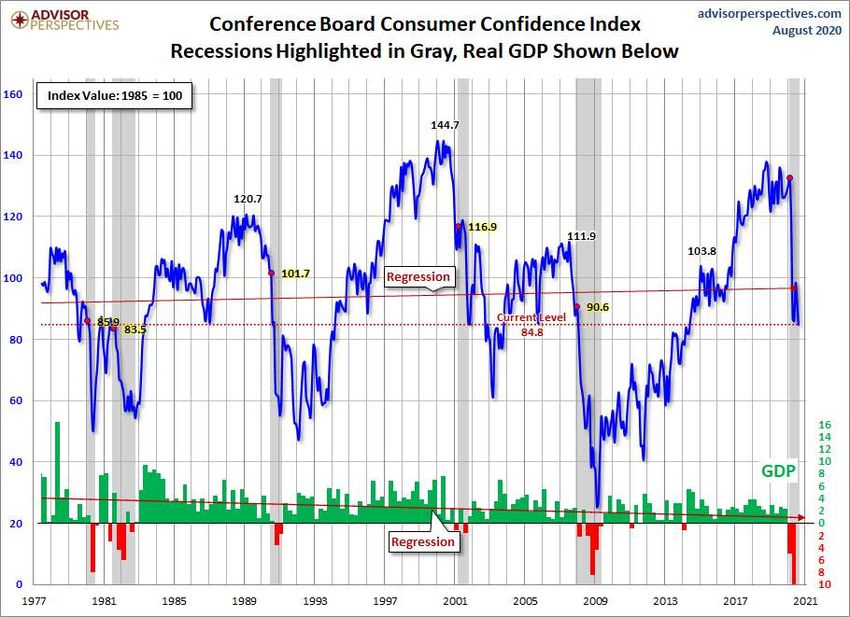

currencies. The moves weren’t huge because, again, all of this was telegraphed, and nothing was truly new or surprising. Fiscal Cliff: Still Falling Extra fiscal spending pretty much ended at the end of July, and that’s a topic we’ve been covering in these reports for months. From April through July, people received stimulus checks and extra unemployment benefits, and small businesses received loans that turn into grants, nearly $3 trillion in free grant money overall, but most of that stopped by the end of July. Some of it happened with a lag; unemployment benefits attributed to previous weeks still went out to people into mid-August. Now, at the end of August, the economy has been operating for a couple weeks in “non-fiscal” mode. Unemployed people are not receiving additional federal unemployment benefits, and businesses are pretty much on their own. Small business revenue peaked in the beginning of July and has since been on a downtrend. July consumer confidence reached a new cycle low after enjoying a brief bounce.

Chart Source: Advisor Perspectives If this situation continues with high unemployment and low government stimulus, the natural results of a major recession will play out, with many people and businesses unable to pay rent, which trickles up to landlords and banks, and results in a broad solvency crisis and many defaults. So far, national personal income was up in 2020 (rather than down as in a normal recession), due to increased government transfer payments that more than offset the loss of normal income. And that led to retail sales also being up in 2020 (largely lead by e-commerce), because consumers have that government cash to spend, even as employment conditions, imports, exports, industrial production, and capital spending are all down as per what we’d expect from a severe recession. That divergence between incomes going up and economic activity going down is not inherently sustainable, unless government spending artificially continues to sustain it.

Both political parties want another round of stimulus. The Republicans and President want about $1 trillion in stimulus, mainly targeting businesses and consumer stimulus checks again. The Democrats want $3 trillion in stimulus, targeting state budgets and larger consumer stimulus checks this time. Both sides have signaled compromise; Democrats are willing to go down to $2 trillion, and Trump is willing to go up to $1.3 trillion. Political events related to the upcoming election and unrelated to stimulus, largely involving the Post Office, have further slowed down these negotiations. The situation remains in gridlock, and so the economy has gone off the “fiscal cliff”. Analysts don’t expect S&P 500 earnings and revenue to surpass 2019 highs until 2022, even though the stock market has already reached new record highs in 2020, due to increases in valuation. As long as that fiscal gridlock remains, a disinflationary pressure and broad solvency risks grow. The Fed’s balance sheet stopped increasing nearly three months ago. Broad money supply stopped increasing about a month ago. The stock market and consumer finances are no longer held up by “money printing” at this particular time. Equities and other risk assets, which have kept going up, are vulnerable for correction in this environment.

A Global Look The global economy is somewhat in sync when it comes to rebounding. Here is manufacturing PMIs for Europe, Japan, and China, for example: Chart Source: TradingEconomics.com

Everyone experienced an economic crash in March/April as the economy shutdown. China was ahead, then Europe and broader Asia, then the United States, and then several emerging markets. Japan has been somewhat weak, while China has been reasonably strong. For the United States, many metrics are reasonably good, but the reported unemployment situation is far higher than most of our peers, due to the way our system is structured. Latest Portfolio Changes The S&P 500, having broken over 3,500, is currently at the most overbought level in terms of daily RSI since early 2018.

The S&P 500 recently became overbought based on RSI in early 2020, had the severe March 2020 correction, rebounded into a June overbought state, corrected and consolidated a bit, and is now at all-time highs in a bigger overbought state. These overbought conditions, combined with near record-low put/call ratios, and the fact that we’re off the fiscal cliff and can’t point to money-printing as propping up the index, sets the stage for another potential consolidation or correction. A correction or pullback is not guaranteed to happen here, although the index is over-stretched on multiple technical and fundamental metrics relative to the damaged economy. It’s best thought of as a probability distribution, and the likelihood of a correction or consolidation is increasing here, especially with the fiscal taps closed at the moment. No Limits IB Portfolio: As I described I would do in last week’s extra report, I bought TCEHY and sold BBL this week. Fortress Income Portfolio: For early next week, I plan to sell SYY and buy BTI. BTI is unusually cheap, has a high yield, and despite the long-term decline in tobacco usage, tobacco companies have outperformed the broad equity market over the past 25 years because they are cheap and send most of their cash back to shareholders while maintaining high returns on invested capital. As a note, I don’t personally invest in tobacco companies. There are very few industries that I avoid outright, and tobacco companies are the key industry I avoid. So, while I think BTI is a great value/dividend investment at this price level as part of a diversified portfolio, I would not buy it in my large personal Schwab account, for example. However, the model portfolios are mainly meant for members, rather than myself, so I am willing to add BTI to the Fortress Income Portfolio because I

think it objectively increases the risk-adjusted forward return potential of the portfolio at this price level for the stock, and will not overlay my own personal preferences to those portfolios if they conflict with my forward return expectations. Investors each have their own decisions about what investments they might choose to exclude for reasons other than risk-adjusted forward return potential and dividend income. Other Holdings In my Schwab/Fidelity personal accounts, I did a bit of portfolio pruning. I sold TRV, RSXJ, and SBUX. I have nothing against them and am not acutely bearish, but at this time felt that they no longer warrant individual positions. I bought TCEHY, EBAY, AMGN, and RSX. The first three stocks have all been subjects of deep dive analysis reports and were already in other portfolios, and RSX is the iShares Russian stock ETF. Russia faces heightened sanction risk at the current time but remains an interesting long-term opportunity based on my global opportunities investment report and based on past analysis of the largest Russian companies. All of my portfolios, and the global opportunities investment report, are available in the Google Drive. I update portfolio lists ahead of a purchase in the Google Drive.

Tencent Holdings (TCEHY) Deep-Dive Analysis This report focuses on Tencent as an investment idea, but a bit of background is needed first. Chinese Tech overview Years ago, the emerging markets index was characterized as being mainly a commodity play, with rather low-value industries making up the bulk of it. However, over the past 10+ years, the emerging market index has reached a greater percentage of internet and tech companies than the global developed market index, largely thanks to China, South Korea, Taiwan, India, and to a lesser extent, Singapore and others. The MSCI emerging market index is now 49% composed of the information technology, consumer discretionary, and communication services sectors, which encompasses various technology, e-commerce, and online media companies. This compares favorably to MSCI’s EAFE (developed ex-USA international markets) index which has just 25% in those sectors, and the American market that has 34% in those sectors. Several Chinese companies, like Alibaba, Tencent, JD.com, Baidu, Huawei, and others, have been a big part of this change, and in several ways they mimic the American “FAANG” group of internet companies that includes Facebook, Amazon, Apple, Alphabet, Netflix, and informally Microsoft (but at lower relative valuations). Alibaba is similar to Amazon and Netflix and Paypal, in the sense that it offers e-commerce and cloud platforms and a large e-payment network. JD.com is also big in the e-commerce space. Tencent is similar to Facebook, Paypal, Netflix, and aspects of Microsoft, in the sense that it provides a social network, gaming, and a large e-payment network.

Baidu and Sohu are similar to Alphabet in the sense that they focus on online searching and some AI development, although Tencent has been entering the search market as well, by operating its own search engine and offering a buyout of Sohu. Huawei is like a smaller combo of Apple and Cisco, in the sense that it offers consumer electronics and various networking equipment. Alibaba and Tencent together have a pretty firm duopoly on Chinese payment systems, thanks to the network effect. There are many funny stories of foreigners going to China, with a wallet full of Chinese cash and international credit cards, and yet street vendors and other businesses don’t accept those payments, and only want Alipay or WeChat Pay from a mobile device. Developed markets gradually went from cash to credit/debt cards to mobile payment systems over the past several decades, and is still firmly in the credit/debit card dominance period. Emerging markets went from cash, mostly skipped over physical credit cards, and are now leading the way on mobile payment adoption as a percentage of payments. This includes China, India, and others. With relatively low GDP per capita, not everyone has a PC in developing markets, but basically everyone has a smartphone. Those developing Asian economies came of age economically in the era of the smartphone. And yet, Alibaba has a market cap of under $800 billion, and Tencent is under $700 billion, while Apple, Alphabet, Amazon, and Microsoft are all well over $1 trillion each (with Apple being above $2 trillion, and Microsoft not far behind). So, with China’s large population that is more than 4x as high as the population of the United States, there is plenty of growth potential in the internet, media, and e-commerce space in Chinese stocks over the next decade. They are big, but have room to get a lot bigger.

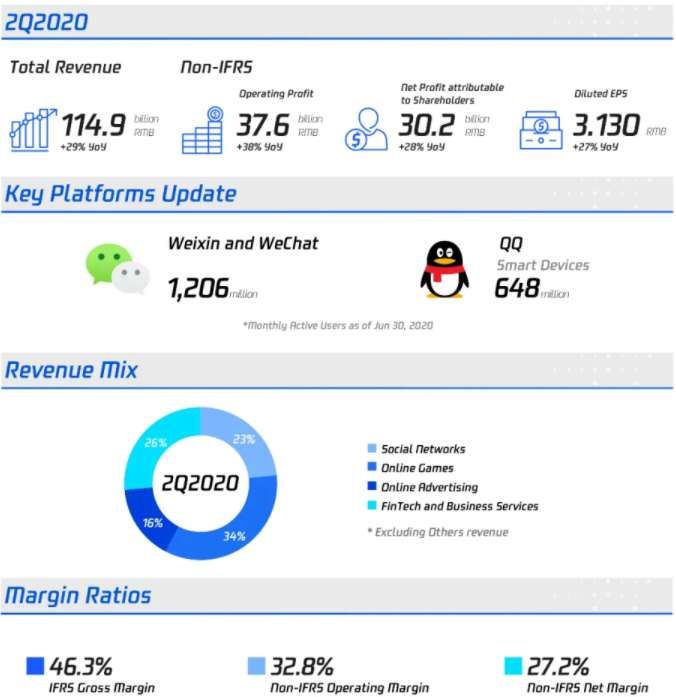

Tencent Focus Tencent Holdings, founded in 1998, is China’s second largest company by market capitalization after Alibaba. Investors can buy their shares on the Hong Kong Stock Exchange, but for this report, the American ADR with ticker TCEHY is the baseline security that I’ll use here. It’s available over-the- counter, rather than on a major American exchange like Alibaba or JD.com, despite its massive size. Tencent operates two social networks, WeChat and QQ, which generate advertising revenue. By extension, they also operate WeChat Pay, which has become one of China’s largest mobile payment methods along with Alipay. Tencent is also a large producer and distributor of games in China and globally, and is the world’s largest video game company. Here’s Tencent’s overview, from their 2020 interim results presentation:

In addition to their own core platforms, Tencent owns key equity stakes in a variety of global gaming companies and other internet/software companies. Notably, Tencent owns: • 9% of Swedish streaming and media company Spotify • 5% of American electric car and solar producer Tesla • 20% of Chinese e-commerce giant JD.com

• 100% of Riot Games (the American producer of League of Legends, one

of the world’s most popular games)

• 40% of Epic Games (the American producer of Fortnite, the world’s most

profitable game of 2019)

• 5% of French video game giant Ubisoft

• 5% of American video game giant Activision Blizzard

• 25% of Sea Limited, Singaporean e-commerce and gaming fast-growing

giant that focuses on Southeast Asia (Singapore, Malaysia, Thailand, the

Philippines, Taiwan)

• Stakes in a variety of other companies, including multiple international

game producers, plus Discord, Reddit, and more.

Although China has a rather large corporate debt bubble centered around its

real estate sector, Tencent as an internet company is basically net debt-free.

They have roughly as much cash as debt, and their gross debt/EBITDA ratio is

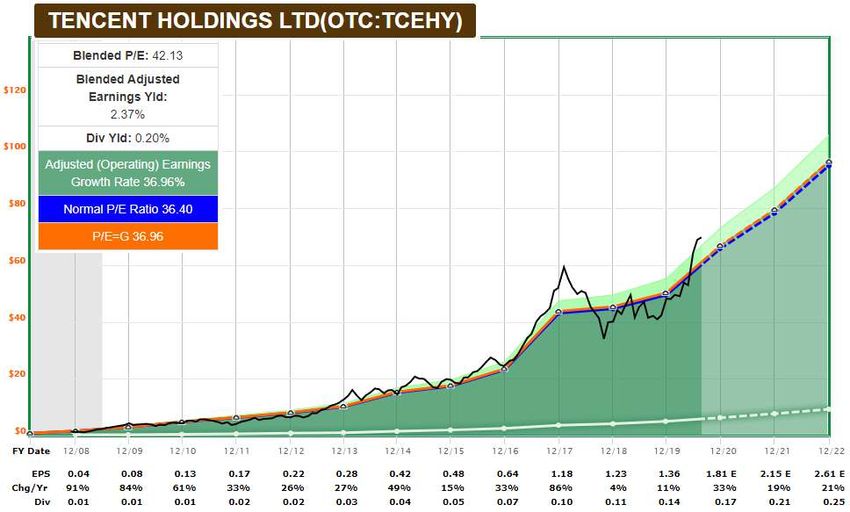

less than 1.5x.Tencent’s returns on invested capital are routinely in the double-digits, while revenue growth is very strong. By virtually all metrics, it’s an extremely successful business. Valuation Analysis Tencent stock is relatively expensive, but has high expected forward return potential and a strong balance sheet, and so overall, is fairly-valued for long- term positive returns. Its chart looks like how a lot of FAAANG stocks looked 3-5 years ago. Here’s the F.A.S.T. Graph: We can see that in early 2018, the stock got a bit ahead of itself, and then for two years the company’s fundamentals consolidated sideways. China faced the U.S.-China trade war situation, and Tencent specifically faced a nearly year- long freeze by Chinese regulators on gaming approvals.

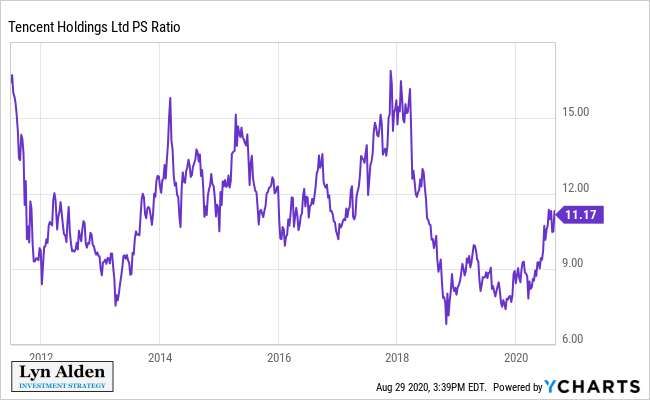

If the company meets analyst-consensus growth expectations, the fair value for TCEHY by the end of 2022 is over $90/share, compared to $70/share today. Of course, the company could grow slower than consensus expectations, or its valuation could decline below historical norms despite reaching analyst consensus targets, so such a share price is not for certain. Therefore, the $90 target is merely a baseline target based on fundamentals, and assumes a valuation that is similar to (but actually a bit lower than) today’s valuation. However, Tencent has a big lock on Chinese internet, payment, and media exposure. It trades for a smaller market cap than its American counterparts, despite the fact that China has more than 4x the population as the United States. Tencent’s long-term upward potential over the 2020’s decade is immense. Although such an outcome is not certain, there is little to stop it from potentially becoming a $1 trillion company within 3 years, and a $1.5+ trillion company in the years after that, subject to valuation changes. The company’s price-to-sales ratio (one of the most useful metrics for a fast- growing high-margin e-business) is in line with its historical average, after having become rather expensive in early 2018:

Here is a StockDelver model for Tencent, using 18% growth over the next five years, 12% growth for the five years after that, and a proposed sale P/E in ten years that is only 25x, compared to today’s level of 42x:

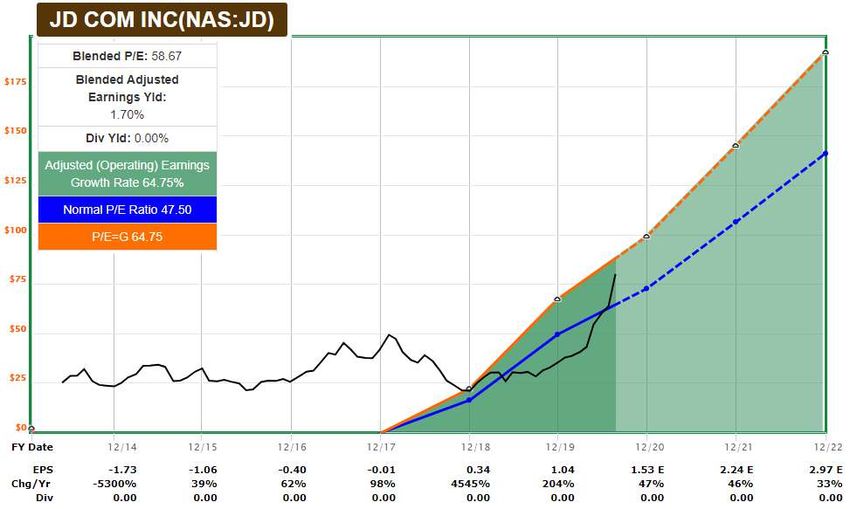

Chart Source: StockDelver Besides its core wholly-owned businesses, Tencent’s most promising investments include its stakes in Spotify, JD.com, and Sea Ltd. Here’s JD.com’s FAST Graph:

JD.com is a Chinese e-commerce giant that is a smaller but faster-growing competitor to China’s largest company Alibaba, and is beginning to enter what seems to be its profitable phase now. If things go well (and no revelation of fraud or other curve balls), there’s nothing stopping JD.com from one-day becoming a half-trillion dollar company, of which Tencent’s stake would be worth $100 billion. Even half that would be a big gain from current levels. Spotify’s revenue is soaring, and so is Sea Limited’s. Tencent has been a strong allocator of capital so far, and these are two companies to watch in particular along with JD.com. Tencent’s founder, CEO, and Chairman is Ma Huateng. With a net worth of over $50 billion, he is currently China’s richest person, and is currently in his late 40’s, so he has plenty of long-term potential in relation to Tencent leadership. Overall, Tencent has a multi-pronged set of growth opportunities in Mainland China and multiple countries in Southeast Asia from a perspective of social networks, gaming, e-commerce, and payments, and more broadly the global gaming industry outside of that super-region. As a group, this region has

faster-growing GDP than fully-developed markets, and the long-term potential is very large. It would likely require a major external disruption for Tencent (or some big revelation of fraud or other internal tail risk) to not eventually blow past the $1 trillion USD market capitalization threshold in the years ahead, although various normal outcomes can curtail or delay that advancement to some degree. Company Risks The risk situation for this stock is longer than normal, because there are plenty of risks to cover. Competition Risk Many of Tencent’s businesses, such as WeChat for social expression and online payment, enjoy huge economic moats in China, and operate in oligopoly-like status with strong network effects. Other parts of their business, like video games and other media, must continually compete with other companies with more vulnerability. Tencent’s video game interests also compete with various game developers globally, Tencent’s equity stake in JD.com competes with Alibaba and e- commerce companies, and Tencent’s stake in Tesla competes with various car manufacturers globally. Currency Risk Foreign investors have currency risk if they invest in Chinese companies. The CNY has been in a relatively tight band vs USD over the past decade, but various events could trigger a breakout or breakdown. Tencent could do well in CNY terms, for example, but if the CNY weakens vs the dollar or euro or whatever your home currency happens to be, it could do worse as priced in your currency. The opposite possibility is true as well. China Regulatory Risk

While most countries have some degree of mild regulation around media, such as ratings on games and movies related to violence or sexual content and so forth, China is not a free country and can outright disapprove the release of various media for political reasons or other reasons, which can be problematic for a media company like Tencent. No domestic or foreign publisher can publish a movie or game in China on the open market without China’s regulatory approval. For the better part of a year starting in 2018, China overhauled its regulatory process, and put a freeze on approving all new games. This contributed to Tencent’s earnings and stock price slump during the past couple years. In addition to managing politically-sensitive content, China’s regulators expressed concern with widespread video game addiction, and so they also created gaming curfews making it so that minors can only play 90 minutes of games on weekdays and 180 minutes on weekend days, and not between the hours of 10pm and 8am. In addition to broad regulator risk, if at any point Tencent’s executives are out-of-favor by the Chinese Communist Party, their business results may be impacted by any number of regulatory actions against them. As one of China’s largest companies, China has a strong incentive for Tencent to grow and prosper, but only to the extent that it doesn’t conflict with the interests of their political party and authoritarian rule. Fraud Risk Publicly-traded Chinese companies have a higher rate of fraud than U.S. companies, European companies, or Japanese companies. I consider Tencent to be somewhat lower on the risk list among Chinese companies. This is because they own some of the strongest businesses in China (it’s well-known how strong their social, payment, online, and media businesses are), and they regularly make foreign deals by using capital to buy stakes in non-Chinese companies, which is good evidence of their liquidity. However, as a Chinese business, Tencent still inherently has a higher risk of something fraudulent occurring which would have a material impact to investors, than, say, a company like Microsoft. Between the two, I would personally trust Tencent over Tesla, though. It’s all somewhat relative.

In addition, China’s government-reported macroeconomic data is vulnerable to a sizable degree of manipulation as well, and investors often use third-party data sources to try to collaborate Chinese macroeconomic data where possible. This risk can be managed with appropriate position-sizing to account for tail risks related to fraud. Natural Catastrophe Risk Over the past few months, China’s Three Gorges Dam has been in the news, and not for good reasons. The dam is so big that it measurably affected the rotation speed of our planet when constructed, so it’s not a structure that you want to be in the news for unfavorable reasons. It’s the largest dam in the world, and China has experienced epic rains at levels not seen for decades, which have flooded portions of the country and put pressure on the dam. The historically unusual amount of rain has tested the limits of what the dam was designed for, with generational highs in rain levels. According to dam operators as well as satellite images, the dam started to become a bit distorted a couple years ago, and it’s getting more attention in 2020, but dam operators say that it is safe. If this dam were to ever have a catastrophic failure, either due to a natural break or due to a terrorist or foreign military strike, a large portion of China’s densely-packed population area would be flooded, including several major cities, and electricity generation would be negatively affected. A few hundred million people would be impacted to varying degrees, and there would be severe economic implications for China specifically, and by extension a large portion of the highly-interconnected global economy. In such a scenario, the macroeconomic damage to China’s economy could weigh notably on Tencent’s performance, and introduce some major sociopolitical risks for China’s ruling regime. Cold War Risk China and the United States are increasingly in a “cold war” type of scenario with each other, as competing economic and political major powers. These

include tariffs, regulatory actions, and some degree of economic de-coupling and capital controls. Each country has the ability to perform major economic damage to each other, like the U.S. blocking Chinese exports, or China banning Apple products from their country, and things like that, if political differences deteriorate. The bulk of Tencent’s business is relatively immune to U.S. economic decisions, but some areas are vulnerable. Trump recently banned WeChat transactions in the United States, for example, which itself is an understandable decision because China bans many American social platforms. However, this ban had unintended consequences and was quickly verbally scaled back a bit, because the plan was quickly lobbied against by the likes of Apple, Walmart, and other mega-cap U.S. companies due to the fact that WeChat is the platform for how a lot of U.S. companies communicate and transact with their Chinese suppliers. And Chinese Americans use it to communicate and transact with family and friends in China. But for the most part, it’s money that speaks. WeChat has rather little usage in the United States as a percentage of its total userbase (which is mostly in China), so this hasn’t really been financially material for Tencent. It’s currently a question mark for U.S. companies with Chinese supply chains, and for Chinese Americans that wish to communicate with Chinese family and friends. Those are the groups for whom it could be impactful. The United States could also block future Tencent acquisitions of American businesses, although such a move could have reprisal from China by blocking or otherwise harming some American companies that operate there. In an extreme case, the United States authorities could block Americans from investing in Chinese companies via sanctions, which would have a dramatic impact on the index fund industry, Chinese equity valuations, and many other things. It could reduce Chinese stock valuations and force Americans to sell at an inopportune time for a loss, even if the fundamentals of the businesses are otherwise solid.

It’s a messy situation worth monitoring over time. These risks can be managed with appropriate position sizing and jurisdiction diversification. Summary The U.S. economy is at a crossroads due to running over the fiscal cliff. There is a fiscal gridlock with an upcoming U.S. election in a little over two months. This year has the most negative economic impact since the 1930’s on the U.S. economy and most of the world economy, and the system was held up over the past four months due to record amounts of fiscal stimulus at a level relative to GDP that has not been seen since World War II. Different countries have responded to it in different ways, but most responses were quite large. In the United States, fiscal spending was large enough to fully replace lost income on a national scale for four months, but tapered off into August, so now there are more disinflationry and insolvency outcomes on the table. China went through the virus effects first, and came out relatively intact, and in particular the internet companies like Tencent are well-positioned to prosper for years to come due to being less economically sensitive and benefiting from the ongoing digital shift, and without being notably overvalued. Compared to their American counterparts, Chinese internet stocks like Tencent are reasonably priced relative to their growth rates, for investors that are willing to diversify and take on some Chinese accounting risk and geopolitical risk with appropriate position sizing relative to their own risk profile. I’m bullish on a variety of Chinese internet firms, with Tencent being my preferred risk/reward play at the current time as part of a diversified portfolio.

_____ All of the analysis in this research report is presented for informational purposes about investments in general and does not constitute investment advice. Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do you own due diligence before making investment decisions. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general investment information only, is not individualized, and as such does not constitute investment advice. Every effort is made to ensure that the research content in this report is accurate, but accuracy cannot be guaranteed and all information is presented “as is”. Investors should consult multiple sources of information when analyzing investments. Investments may lose value. Investors should use proper diversification and maintain appropriate position sizes when managing their investments. Best regards,

You can also read