THAILAND AMIDST COVID-19: CHALLENGES & OPPORTUNITIES - KIRIDA BHAOPICHITR 9 OCT 2020 - Joint Foreign Chambers of ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THAILAND AMIDST COVID-19:

CHALLENGES & OPPORTUNITIES

KIRIDA

BHAOPICHITR

9 OCT 2020

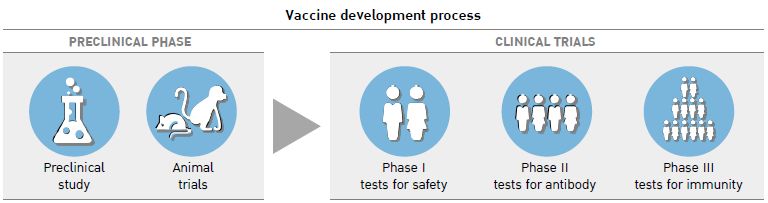

proven vaccine will be available

only at least a year from now

• Earliest planned completion date for COVID-19 is September 2021.

Vaccines currently undergoing clinical trials

Source: Vaccine Centre, London School of Hygiene & Tropical Medicine and New York Times 2

Global economy will not recover

until after 2021

• According to IMF, global GDP growth is projected to contract by 4.9% in 2020. In the baseline, global activity

is expected to bottom out in the second quarter of 2020, recovering thereafter and reaching pre-COVID levels

by the end of 2021.

• Advanced economies, including US, Euro, and Japan, will contract by more than developing economies and

will recover to pre-COVID levels only after 2021; China is the only large economy that will expand, albeit

modestly, this year.

• However, recovery will be delayed should the pandemic not end by next year or countries lockdown when

faced with future waves of outbreaks.

GDP Growth Forecasts by IMF

RUSSIA

WORLD Growth in 2020 2021

Growth in 2020 2021

EURO AREA

2019

1.3% -6.6 4.1 % %

2.9 -4.9 5.4

2019

(-5.5%) (3.5%)

% % % Growth in 2020 2021

(-3.0%) (5.8%) 2019

1.3% -10.2 6.0 % %

CHINA

ADVANCED ECONOMIES USA (-7.5%) (4.7%)

Growth in 2020 2021 JAPAN

2019

1.7%

Growth in 2020

-8.0% 4.8%

(-6.1%)

2021

(4.5%)

2019

2.3%

Growth in 2020

-8.0 4.5 %

2021

% MIDDLE EAST

2019

6.1% 1.0 8.2 %

(1.2%)

%

(7.2%)

2019

0.7%

Growth in 2020

-5.8 2.4 %

2021

%

(-5.9%) (4.7%) AND CENTRAL ASIA (-5.2%) (3.0%)

Growth in 2020 2021

ASEAN-5

LATIN AMERICA 1.0% -4.7 % 3.3% INDIA

EMERGING MARKET AND 2019

DEVELOPING ECONOMIES (Indonesia, Malaysia,

Growth in 2020 2021 (-2.8%) (4.0%) Growth in 2020 2021 Philippines, Thailand, Vietnam)

2019

3.7% -3.0% 5.9% AND THE CARIBBEAN 2019

4.2% -4.5 6.0 Growth in 2020 2021

(-1.0%) (6.8%)

2019

0.1%

Growth in 2020

-9.4 3.7 %

2021

%

%

(1.9%)

%

(7.4%)

2019

4.9% -2.0 6.2 %

(-0.6%)

%

(7.8%)

(-5.2%) (3.4%)

Note: shows increase/decrease compared to previous year; Number in bracket is forecast in April 2020; Size of circle is the size of economy

Source: World Economic Outlook (June 2020), International Monetary Fund and TDRI calculation 3

US-China trade war could step up

this year as phase 1 deal breaks down

• China is unlikely to meet the target China’s purchases of US goods under US-China Phase 1 Deal

(as of May 2020)

with phase one deal. 180 Purchase commitment

(Chinese imports)

• In first 4 months of 2020, China 160 $172.7 billion

140 Purchase commitment

imported only 45% of what it would (US exports)

120 $142.7 billion

have to buy to be on pace to meet 100

the deal. 80

• In particular, China’s imports of oil 60

40

from US is falling far behind target, $32.7 billion actual purchases, based on Chinese imports

$26.9 billion actual purchases, based on US exports

20

while it imports from Saudi Arabia

0

and Russia. 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: Peterson Institute for International Economics

• Trade war will continue post US

US view of China

elections as more Americans have 80

66

70 60

been viewing China more 60 52 50 49 51 52 55 54 55

Unfavorable

47 47

unfavorably since the trade war and 50 43 42 42 40

40

COVID-19 pandemic began. 30 39 39 38 36 36 40 37

44

35 35 38 37 38

Favorable

20 29 26 26

10

Source: PEW

0 Research Center

2005 2008 2011 2014 2017 2020 4

oil prices recovered from its trough

but will remain low until next year

Global crude oil spot prices

• In June, Brent spot price was US$40.3/barrel Crude oil, WTI Crude oil, Brent

(-37.3% yoy), up from US$18.4/barrel in April, 90

EIA Forecast

as numerous regions worldwide began to lift 75

(as of July 2020)

US dollar per barrel

lockdowns, while global oil supply fell as

60

a result of production cuts by OPEC+

45

• EIA expects monthly Brent spot prices to

average US$41.5/b (-34%yoy) in 2H2020 and 30

rise to an average of US$44/b in 2021 with 15 Jun

supply reductions and rising demand 2017 2018 2019 2020 2021 2022

Oil production and consumption

• EIA forecasts is based on US gross domestic Oil Production Oil Consumption Oil balance

product declining by 6.4%yoy in 1H2020 before 105

100

rising in Q3/2020 through 2021. Million barrel per day 95

90

• OPEC+ agrees to extend oil production cuts 85

EIA Forecast

through July 2020. 80 (as of July 2020)

75

• US oil rig count falls to lowest level since 2009 20

10

0

-10 Jun

2017 2018 2019 2020 2021 2022

Source: EIA

Note: Oil balance = Production – Consumption 5

Baht/US$ is forecasted to be

around 31-31.50 for the rest of the year

• Baht weakened from Bt31.3/USD in Index of Local Currencies to US dollar (compared to Dec 2019)

Q1/2020 to Bt31.9/USD in Q2/2020, the

weakest in ASEAN-5 after Indonesia 94

(-1.1%) (-1.1%) (0.6%) (0.6%) (3.6%) (3.8%) (3.8%) (5.6%) (6.5%) (6.6%)

rupiah. 96

Index (Q4-2019 = 100)

Strong

98

• For the remaining months of the year, the 100

100

baht is forecasted slightly appreciate to 102

31-31.50 to the US dollar as trade balance

Weak

104

improves with recovery in exports and US 106 Actual Consensus forecast

Q1-20 Q2-20 Q3-20 Q4-20

dollar weakens from H1. 108

Note: Number in brackets are %changes in exchange rate in Q2/2020 from Q4/2019;

- = appreciate (strong), + = depreciate (weak)

USD Trade Weighted Index & Thai baht Thai Baht Movement Drivers

USD Trade Weighted Index THB/USD Current Account Net direct investment SET Foreign Netbuy

128 COVID-19 pandemic 28 Strong

Dollar index (Jan 2006 = 100)

126 Thailand BEX Foreign Netbuy THB/USD (Right axis) Strong

29

124 COVID-19 outbreak in Wuhan lockdown

end

6 Forecast 29

Baht / US dollar

122 30 3 (as of Aug 20) 30

Billion US dollar

Baht / US dollar

120 31

0 31

118 32

116 -3 32

114 33

-6 33

112 34 Sep

Feb

Feb

Apr

Oct

Apr

Jun

Jul

Jun

Jul

Jan

Jan

Nov

Q3F

Q4F

May

Aug

Dec

May

Mar

Mar

Weak

Sep

Feb

Oct

Apr

Jun

Jul

Jun

Jul

Jan

Nov

Aug

Dec

May

Aug

Mar

2019 2020 Weak

2019 2020 Source: SET, ThaiBMA, BOT, CEIC and Consensus Economics Inc. (as of Aug 2020)

Source: Federal Reserve Board and Bank of Thailand Note: Current account and Net direct investment data for July 2020 are not yet released 6

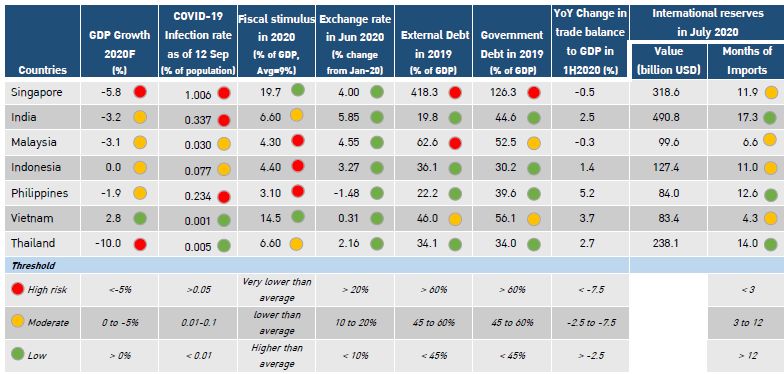

Thailand’s macroeconomic foundation is strongest among ASEAN & india • Thailand’s macroeconomic foundation remains strong even during the Covid-19 pandemic. • Thailand's GDP will contract most this year in ASEAN as its reliance on international tourism is higher than other ASEAN countries’. Source: Compiled by TDRI EIS` 7

Thai Economy

8

Thai economy will only

recover to pre-COVID levels in 2023

• Thai economy could contract by 10% this year and will not reach pre-COVID levels until 2023

as exports, tourism and domestic consumption will only start to pick up once the COVID-19

pandemic ends.

• Post-COVID, exports will be affected by lower Household debt

global purchasing power and higher trade Household debt % of GDP (right axis)

barriers; tourism will recover to pre-COVID 13.6 80

levels only in 2023 when the pandemic is 13.4 79.5

behind and international movements of 13.2 79

people fully resume.

Trillion baht

13 78.5

• With rising household debt burden and fall in 12.8 78

incomes and savings, household 12.6 77.5

consumption could take up a year to recover 12.4 77

to its pre-COVID level after the pandemic is 12.2 76.5

over. 12 76

Q3-18 Q4-18 Q1-19 Q2-19 Q3-19 Q4-19

• Rising NPLs and excess capacity will lead to Source: Bank of Thailand

a slump in private investment and delay

adoption of automation until 2022.

9Exports to recover in 2020H2

But could contract by 10% this year

Growth of Thai export value by Major Products

• In 7M2020, exports declined by 7.7% yoy; excluding Agriculture Manufacturing Arms & ammunition

gold and ammunitions, export declined by 10.2%yoy, Gold Other exports

Total exports Total exports (excl. gold, Arms & ammunition)

the lowest in 5 years. 20

• Exports to all market have collapsed with 10

the exception of US & China 0

Percent

• Exports in 2020H2 are expected to recover from H1 as -10

major markets gradually open. However, exports for -20

the entire year may contract up to 10%. -30

Q1 Q2 Q3 Q4 Q1 Q2 Jan Feb Mar Apr May Jun Jul

2019 2020

Destination %YoY Growth of Thai export %Share

Q3-19 Q4-19 Q1-20 Q2-20 May-20 Jun-20 Jul-20 2018 2019 2020YTD 2020YTD

Japan 2.8 -5.3 -5.5 -13.5 -24.2 -21.6 -17.5 13.0 -1.7 -10.5 9.7

EU 28 -5.2 -5.9 -3.9 -30.3 -39.7 -22.7 -17.0 5.2 -5.9 -16.8 8.8

ASEAN -14.2 -8.3 4.3 -22.3 -27.9 -30.3 -19.9 14.9 -8.3 -10.6 24.6

ASEAN-5 -12.7 -9.9 5.7 -19.7 -27.9 -38.8 -24.6 13.6 -9.8 -9.7 14.0

CLMV -16.2 -6.2 2.7 -25.8 -28.0 -17.8 -13.2 16.7 -6.3 -11.8 10.6

USA 7.7 5.5 -2.7 8.9 -17.3 14.5 17.8 5.5 11.8 4.5 14.5

Middle East 1.9 5.6 0.4 -19.7 -26.4 -7.9 -20.1 -0.1 0.4 -10.6 3.3

Australia 14.0 -14.9 -3.3 -16.1 -7.4 -16.7 -10.4 2.6 -5.1 -9.8 4.1

China 2.8 1.6 -0.9 12.1 15.3 12.0 -2.7 2.7 -3.8 4.5 12.8

Total exports -0.5 -4.4 0.9 -15.2 -22.5 -23.2 -11.4 6.9 -2.6 -7.7 100.0

Total exports

-5.2 -4.2 -0.5 -18.7 -27.8 -16.8 -13.6 7.7 -5.0 -10.2 95.3

excl. gold, arms & ammunition

Source: Bank of Thailand with TDRI calculation 10Tourism receipts (18% of GDP)

will be almost 70% below last year’s

Tourism receipts

• From Jan-July, tourism receipts fell Tourism receipts: Thai Tourism receipts: Foreigner

by 60%yoy with international tourists collapsing to YoY growth: Foreigner YoY growth: Thai

350 20

6.7 million visitors.

Tourism receipts (billion baht)

300 0

• International tourist arrivals for 2020 will not be

YoY growth (%)

250 -20

many more than 6.7 million (39 million last year) 200 -40

• Travel bubbles are starting with international 150 -60

visitors such as businessmen, medical 100 -80

tourists, education-related visitors, migrant 50 -100

workers, or long-stay tourists. 0 -120

Feb

Apr

Feb

Apr

Oct

Jun

Jul

Jun

Jul

Nov

Jan

Jan

Aug

May

May

Dec

Mar

Mar

Sep

2019 2020

Tourism revenue in ASEAN in 2018 Source: Ministry of Tourism and Sports

Toursin revenue (left axis) Average growth in 2008-2018

70 50%

58.08

60 39.0%

40%

50

Billion US dollar

40 30%

30 21.77 20.42 20%

10.5% 15.60 10.5% 11.4% 12.7% 10.8%

20 8.2% 10.08

6.4% 9.73 10%

10 1.3% 4.83 1.67 0.76

0 0%

Thailand Malaysia Singapore Indonesia Vietnam Philippines Cambodia Myanmar Lao PDR Source: World Bank

11Which businesses are

affected most during Covid-19?

NEGATIVE IMPACT ON BUSINESS POSITIVE IMPACT

HIGH MODERATE LOW ON BUSINESS

employees

>1 Million

• Shopping malls

• Hotels

• Retail shops • E-commerce (Food,

IMPACT ON EMPLOYMENT

online Marketplace, etc.)

• Delivery services &

• Airlines packaging

100,00 – 1 Million

• Wellness, Spa • E-services (education,

employees

• Hair salons, Barber • Restaurants banking, movies, etc.)

shops • Construction • Electronics • Digital services

• Pubs & bars • Telecom services

• Automobile and parts • Medical supplies (face

• Garments mask, alcohol, vitamins,

etc.)

• Entertainment • Public transportation • Insurance

employees

• Electricity, gasAlmost 10 million are

severely affected by covid-19

• Jobs of 9.7 million people are severely affected by the lockdown from Covid-19 outbreak, with

the largest group being retailers followed by cooks & waiters, hair dressers, tour guides and taxi,

van and motorcycle drivers.

Employed persons impact from COVID-19 by occupation (Million persons) Low impact

Low impact occupation* 12.1 million persons

Agriculturists 11.8 Moderate impact

High-skill Technicians, tailors

Retailers

3.9

5.1

15.6 million persons

Cooks, waiters, hair dressers, tour guides 1.6

Taxi, van & motorcycle drivers 1.2

Low-skill workers 0.6

Street vendors 0.4

Hotel or restaurant managers 0.3 High impact

General hired workers

Assistant cook

0.3

0.1

9.7 million persons

Head chefs, museumand art center directors 0.1

Tourism operators and hotel staff 0.04

Singers 0.02

General customer service 0.02

Controllers, technicians on ships & airplanes and pilots 0.01

Source: BOT, Labor Force Survey Q3:2019 with TDRI calculation

Note: Low impact occupation include State employees, heath care workers, chemists, physicists, computer programmers, telecom workers and

high-skilled workers 13shift from full-time employment

to part-time has been significant

Number of part-time workers by industry (million persons)

8

• The number of part-time workers rose by 5.68 Apr-2019 Apr-2020

6

5 million in April 2020 compared to April 4

4.20

2019, while 2.6 million lost their overtime 2 0.94 1.03 0.85

0.31 0.18 0.58 0.34 0.21

and 3.5 million lost their full-time jobs. 0

Agriculture Manufacturing Construction Wholesale Hotel &

• Sector wise, overtime was cut in all & Retail Restaurant

sectors, while full time workers fell in all Number of overtime workers by industry (million persons)

sectors except manufacturing. Workers 3

Apr-2019 Apr-2020

1.77

were reduced to part time in all sectors. 2 1.59

1.26

1.01 0.87 0.88

1 0.67 0.55

0.39

0.13

Number of workers 0

40 Agriculture Manufacturing Construction Wholesale Hotel &

Part-time & Retail Restaurant

35 6.0 (49 hrs. per week) 8

20 Apr-2019 Apr-2020

Full-time 6 4.99 5.17

15 4.10 4.40 4.32 3.87

24.7

(35-49 hrs. per week)

21.2 4

10 1.85 1.42 1.92 1.37

Source: Labor Force Survey 2

5

with TDRI calculation

0 0

Apr-2019 Apr-2020 Agriculture Manufacturing Construction Wholesale Hotel &

& Retail Restaurant 14Farm incomes may recover in

2020H2 but remains less than last year’s

• Farm incomes in the 5M2020 declined by 1.2% YoY Growth of Farm income by Crops (5M2020)

Price Production Farm income

yoy from down in paddy and sugarcane 30

production. 20

• In 2020H1, Production of rice fell by 35.7% 10

and sugarcane by 14% from severe drought 0

Percent

-10

• Rubber and sugar prices have declined with

-20

oil prices.

-30

• This is despite the Bt56 billion transfers

-40

under Price Insurance schemes for rice, Total Fruits Fowl Swine Sugar Rubber Cassava Shrimp Paddy

rubber, cassava , oil palm, maize from cane

Oct 2020 to July 2021. Agricultural Production

2019 2020 (Forecast)

• Farm incomes should recover in 2020H2 but -0.7%

100

remain lower than last year’s as

80 74.9 74.4

• Production and prices recover, but will

remain lower than last year’s 60 -6.6%

Million tons

+3.0%

• Overall incomes of agriculture households will 40 31.3 29.3

+1.4% +8.4%

16.8 17.3

fall this year as 65% of their incomes are from 20

4.8 4.9 4.3 4.7

remittances & non-farm work which have 0

collapsed after the COVID-19 outbreak. Sugarcane Rice Oil Palm Rubber Maize

Source: Office of Agricultural Economics with TDRI calculation

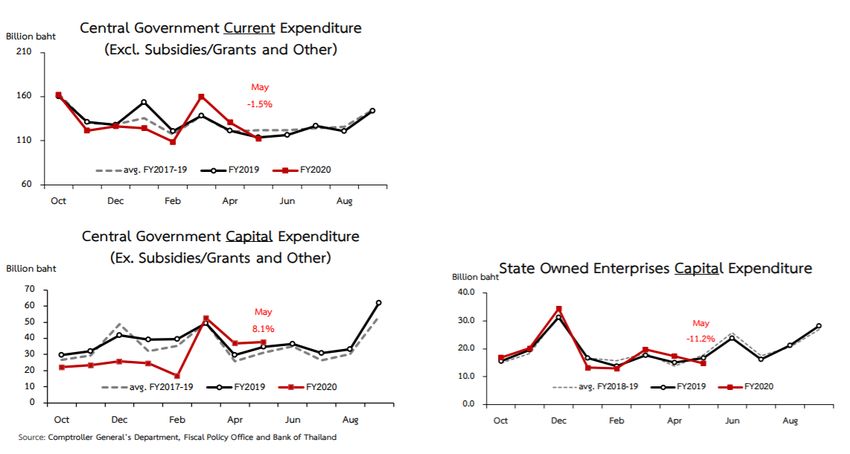

15Public investments are on-going

• The central government’s expenditures on

infrastructure has not decreased much.

• Factors that led to the lag in spending are

usually related to complications that arise

from putting plans into practice, not from

COVID-19.

• Projects in the pipeline, including those in

the EEC, are on-going.

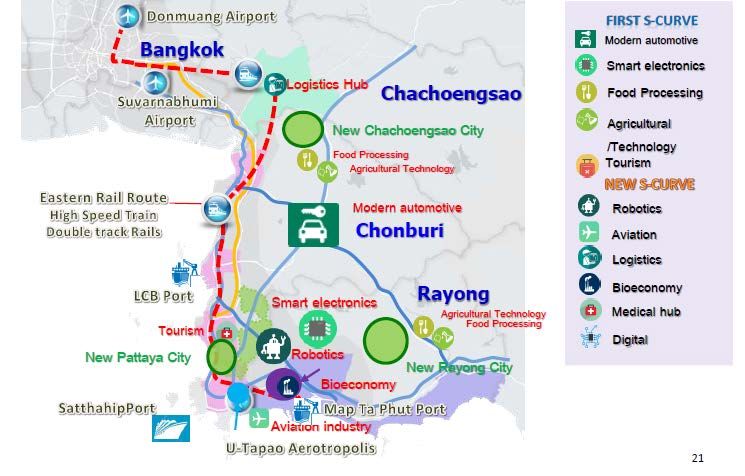

16Eastern Economic Corridor (EEC)

development is progressing

• Except for the airplane maintenance and repair operations (MRO), other projects in the EEC are

on-going.

The Eastern Economic Corridor BOI-approved investments in EEC

(Chachoengsao, Chonburi, and Rayong provinces)

BOI-approved Foreign Direct

Investments

Source: Thailand Board of Investment 17How much government cash transfers

so far to mitigate covid-19 impacts?

Government Cash Transfers

Welfare card Bt3.6bn

• Government has transferred Bt612 billion Fragile groups Bt20.3bn

Water Bt2.8bn

(4% of GDP) to almost 30 million Thais Electricity Bt32.7bn

from May to July.

• The largest number of transfers is for the Agriculture

‘We Do Not Leave One Another’ program Bt111.0bn Social Security

Bt229.0bn

in which Bt15,000 were transferred to

14.2 million informal sector workers,

followed by transfers of Bt15,000 to 7.4 612.5

Billion baht

million agriculturists.

• So far, only Bt344 billion out of the Bt600

billion loan amount are used for

the transfers.

Informal sector workers/ We Do Not Leave One Another Program

Bt213.0bn

Source: Related ministries and government agencies

18Less than BT50 has been

approved from the bt400 billion loan

• Of the Bt1,448 billion (46,111 projects) proposed, Bt93 billion baht (195 projects) have passed NESDC’s

screening, of which 70% are job creation and agriculture-sector projects, 26% are tourism related projects

and only 2% are construction projects.

• So far, only Bt38 billion or 0.25% of GDP (7 projects) have been approved for implementation by the Cabinet,

of which Bt23 billion are tourism-related and the rest agriculture-related projects; most projects are nation-

wide and can be disbursed within this September.

• For the rest of the year, out of the projects that have passed the NESDC’s screening, those that can be

quickly implemented will be prioritized such as in agriculture, job creation and SME business promotion

(the latter is Bt2 billion).

EXPECTED 2020

IMPLEMENTED BUDGET DISBURSEMENT

PROJECT NAME ACTIVITY AREAS (Billion Baht) (Billion Baht)

We Travel Together Increase consumption and boost tourism sector All provinces 20 20

Kumlungjai Increase consumption and boost tourism sector All provinces 2.4 2.4

157 wildlife refuges

Developing Potential in Wildlife Tourism Develop quality tourism 7.4 0.4

(57 provinces)

Safe Tourism Zones Develop quality tourism Potential provinces 0.15 0.06

One Tambon 1 New Agricuture Theory Develop New Agriculture Theory: self-dependence All provinces 9.8 3.9

Developing model areas in promoting quality of life

according to the new agriculture theory towards the Develop New Agriculture Theory: self-dependence All provinces 4.9 3.1

“Kok Nong Na Model”

Developing One Stop Service for Soil and Fertilizer for

Develop large and modern agriculture All provinces 0.2 0.06

Communities

Source: Compiled by TDRI; Disbursements calculated by TDRI 19GOVERNMENT STILL HAS ROOM TO SPEND

The FY2021 Budget • Total FY2021 Budget is Bt3.3 trillion (+3.1% from

3.5

3.3 FY2020); excluding debt repayment is Bt3.0

0.19 Interest Payment

trillion or 17.8% of GDP (+4.3% from FY2020)

3.0 0.1 Principal Repayment

• Current Expenditure (excl. interest payment) 70.6%

0.67 Capital Expenditure (+4.2% from FY2020)

2.5

• Capital Expenditure 20.5% (+4.7%)

2.0

• Central Fund in FY2021 Budget is Bt614.6 billion

Trillion bath

(Bt518.8 in FY2020) of which Bt40 billion are

1.5

COVID19 pandemic-related expenses.

Current Expenditure

2.33 (excl. Interest Payment) • Additional borrowing can be up to Bt1.9 trillion

1.0

in Y2021 (12% of 2021 GDP) if public debt were

0.61 Other Central Fund not to exceed the current 60% of GDP ceiling and

0.5

0.48 Expenses for

the COVID-19 Outbreak

up to Bt2.7 trillion (17% of 2021 GDP) if the public

0.1 Contingency Fund debt ceiling is lifted to 65% of GDP.

0.0 for Emergencies

FY2021 Budget Central Fund • Only Bt100 billion soft loans for SMEs have been

Source: Budget Bureau extended (out of Bt500 billion).

20Sectoral trends

post-COVID

21Digitalization will continue

to sharply expand

ONLINE COMMERCE/SERVICE FROM-HOME ECONOMY

MARCH 2020

• From-home economy will drop from current level but

will continue as it saves money and helps attract

employees, and related infrastructure has already

been invested. As a result, there will be

• demand for technology enablers (5G, platform, cloud

service, electronic device) and employment of IT

workers.

• some shifts to suburban homes for WFH workers.

TELEMEDICINE

JULY 2020

• COVID-19 has migrated patients to telemedicine

• Ping An Good Doctor’s users grew 900% (Dec

2019

65/

35

to Jan 2020) and is eyeing on ASEAN market

• Doctor Raksa, partnered with Bamrungrad, saw its

registered online users increased from 300K to

Note: Data on 400K in April 2020 alone.

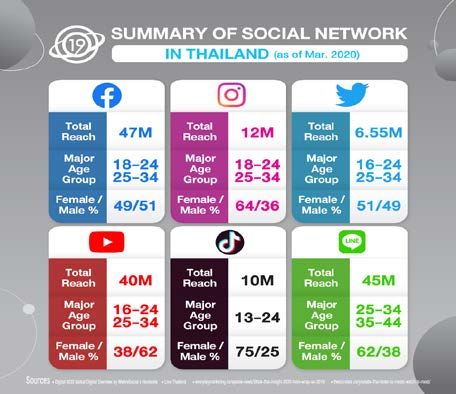

YouTube numbers

in July table are

• ASEAN has potential for telemedicine due to low

as of March 2020 access to medical services. 22tourism will recover Post-COVID

Domestic tourism • Domestic tourism will start recovering in Foreign tourism • International tourism will start to

Q3/2020 with FIT, seminars, conferences, slowly recover end-2020 with focus

and leisure travel; it will not fully recover on selected business and medical

to pre-COVID level until 2022. travelers.

• Government’s domestic tourism stimulus • Foreign tourists who are vaccinated

packages of Bt22.4 billion from July to can start to come in 2022.

October 2020 will also help.. • Full recovery will not be until 2023

TRANSITION PERIOD POST-COVID

• Health consciousness will shift pattern of tourism • Pre-COVID patterns of tourism will return.

• from mass tourism to FIT and mainly domestic tourists • There will be opportunities in medical tourism and

• from large hotels to boutique hotels health & wellness as Thailand has strengthened its

• from long distance to shorter travel distance as long- reputation from handling the pandemic e.g. Dusit

distance flights are few and more expensive.

Thani has partnered with a hospital to start a

• Air travel cost will be higher as there are fewer wellness facility in Hua Hin.

flights and aviation rules require physical • Regional tourism will increase as international

distancing in long flights. tourists, especially from China, will reduced their

• Air Asia, for example, may increase prices by 10-15% travel budgets; Chinese tourists will prefer to travel

to break even. to countries that do not have an anti-Chinese

• Many M&As in hotel and airline businesses are sentiment.

expected. • AR/VR in tourism will not happen.

23Opportunities for Manufacturing

and Agriculture

MANUFACTURING AGRICULTURE / FOOD

TRANSITION PERIOD TRANSITION PERIOD & POST-COVID

• COVID-19 has confirmed the need for companies to • Demand for food falls as demand from

balance cost effectiveness with risk management by tourists and export markets decline, and

• relocating the production for non-Chinese markets out some countries’ governments promote

of China

domestic production of staple foods.

• diversifying sources for raw materials and parts

• Some purchases will be diversified to

• increasing stock levels

Thailand to reduce supply disruptions.

POST-COVID

• Demand for meats from Thailand will be

Global supply chain for manufacturing could be in

3 overlapping models:

higher as many countries e.g. China fear

DIVERSIFICATION

animal disease outbreaks and contagion to

IN CHINA, RELOCATIO

FOR CHINA N/ON- Sourcing of raw humans.

Production SHORING materials and parts

that serves Relocation of are diversified • Bio-products such as plant based meats and

the Chinese production away from China.

market will for non- Although the cost bio-degradable products continues to be the

remain in Chinese is higher but lowers

China. market out of risks of supply new trend and can make use of abundant

China. disruption.

agricultural produce in Thailand.

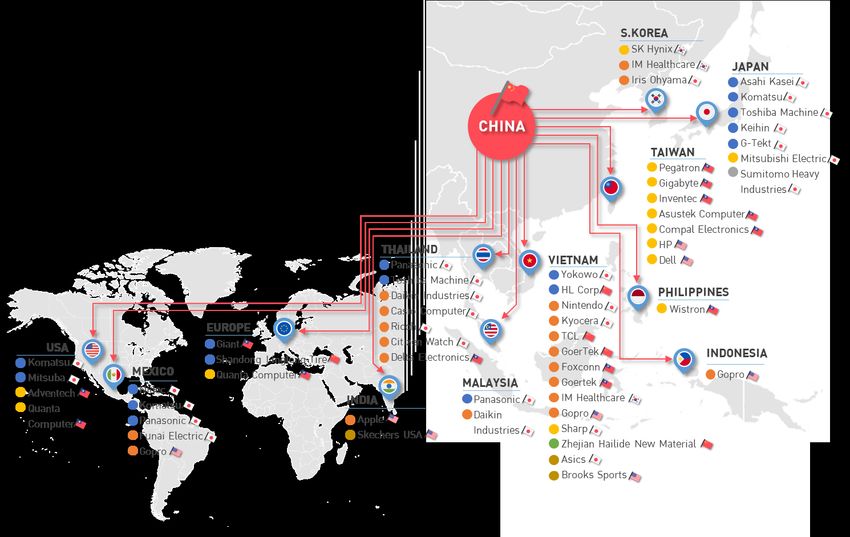

24Companies from china

have relocated to Thailand

• To diversify risks, firms have been moving out of Examples of relocation from China in 2019

China.

• Vietnam has received the majority of the

relocation in labor-intensive to high-tech

industries

• Thailand is the second highest recipient of the

relocation, with Japanese companies being the

majority, particularly in automotive parts,

electrical appliances, and electronics.

Source: TDRI EIS from various sources

Note: Automotive & Parts Computer & Parts Electrical Appliances Petro-chemical Products Footwear Machinery

are Japanese, American, South Korean, Chinese and Taiwanese companies, respectively 25Opportunities in Thailand’s

real estate market

2020 Transition Period

• The total number of registered housing units fell

• Freeze new condo projects; finish existing projects

since February both yoy and qoq as purchases

• Move to housing units

from both Thais and foreigners (around 10% of

• Reduce cost e.g. bargains with suppliers and use digital

annual purchases) fell.

technology for marketing.

• Property sales, particularly of condominiums, will

• Secure liquidity – many small developers & hotels that have

remain subdued for the rest of the year, limiting

low liquidity will need to sell their projects or refinance their

new property projects, while sale prices of units

corporate bonds at high interest rates.

in existing projects are reduced.

Post-COVID-19

• Mix of condos and houses in Bangkok will not change much; there may be small shifts to suburban

houses for those who can afford transportation and can WFH.

• Housing and condominiums in EEC and industrial estates will return as manufacturing production

picks up.

• Large hotels will be back in demand and so will co-working spaces.

• High-end senior housing and facilities as well as wellness facilities will be in increasing demand.

26Thank you

27You can also read