The Maven Letter: January 27, 2021 - Resource Maven

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Maven Letter: January 27, 2021

Reddit Power…Coming Soon To Silver? Mailbox. Pucara Gold: Selling and Lessons Learned.

Maven Buys: Montage Gold (TSXV: MAU). Why Maven Bought: Rokmaster Resources (TSXV:

RKR). Full Portfolio Table and Portfolio Updates from Bluestone, Erdene, Fireweed, Great Bear,

HighGold, Osino, Orezone, Outcrop, Revival, Scottie, Silver Tiger, Uranium Energy, Vizsla.

Just a quick editorial today, as company investment rationales and updates take priority this issue.

(Seriously, did everyone put out news?!?)

But I still have to comment on the crazy moves happening of late in stocks like Gamestop and AMC

Entertainment. So that’s first up.

Next I answer a Mailbox question about how long to hold stocks. It’s complicated…

After that I offer up Selling Pucara Gold (TSXV: TORO) And Lessons Learned. A big exploration

miss.

Then it’s two investment rationales: Montage Gold (TSXV: MAU), which I sent a note out about earlier

today so I could buy before news breaks tomorrow morning on their resource update, and Rokmaster

Resource (TSXV: RKR), which I bought around Christmastime and just hadn’t managed to write up

until now.

To close it’s the full portfolio table and then a long list of Portfolio Updates, from Bluestone, Erdene,

Fireweed, Great Bear, HighGold, Osino, Orezone, Outcrop, Revival, Scottie, Silver Tiger, Uranium

Energy, Vizsla.

--------------------------------------------------------------------------------------------------------

Reddit Power…Coming Soon To Silver?

There have been some absolutely crazy things happening with select stocks in recent days.

AMC Entertainment Holdings was up as much as 230% at one point today. GameStop is up more

than 700% in a week. Neither moved because of news but because investors communicating on

online platforms (primarily Reddit) have decided to (1) teach the big funds and banks a lesson by

squeezing their short positions and (2) make a pretty penny for themselves by working together to

send particular stocks soaring.

GameStop (NYSE: GME)

GameStop was the first stock to solicit the attention of this Reddit crowd. They chose it because

several funds had proclaimed their short positions (bets the stock would fail) as it struggled in a

gaming industry that’s increasingly going online. The retailor lost $1.6 billion over the last 12 quarters

and its stock fell for six straight years before rebounding some in 2020.

Why am I talking about any of this? A few reasons.

First, it’s straight up interesting that retail investors are finding ways to work together and manipulate

the market. That has long been something only the big banks could do! ;)

Second, equity valuations are already at all-time highs. Distortions that push prices higher could have

a negative side effect: increasing daily value at risk, a measure that prompts money managers to cut

their risk appetite. Bottom line: if these crazy price distortions continue they could be the straw that

breaks the ever-rising stock market’s back, to some degree. It could well not have that much impact,

but we saw how significant Robin Hood traders were in the market in the spring and summer. Don’t

discount the little guy these days!

2

Third, talk in the Reddit world today started to swirl around silver. It makes sense: silver has

long been a manipulated arena but only big banks and funds have had the power to do so, it’s a small

enough sector that an army of retail can absolutely have an impact, and there are always lots of silver

shorters out there.

I don’t know a lot about all of this, but my sense is that the Reddit retail crowd doesn’t likely have the

power to influence the price of silver significantly. They very much could, though, send particular

silver stocks through the moon if they decided to do so. As I look, Fortuna Silver is up 3.2%, Pan

American Silver is up 3.8%, and Endeavour Silver is up 3.4% in aftermarket trading. Those aren’t big

enough moves to merit caring – but I will certainly be watching the silver space with interest this week

to see if Team Reddit moves in.

---------------------------------------------------------------------------------------------------------

Mailbox

I started building my mining portfolio late last summer and invest regularly. I selected 20 stocks

based on companies you’ve been covering, and thank you for the good exercise and great

learning process. My question is around holding period, from the perspective of what stage the

company is in when I buy in. How do you think about holding period, and what factors do you

take into consideration when you sell?

Reader MK

This is a question that will take a bit of answering… I think the easiest way to answer is to break it

down by stage, as you suggest.

Explorers: it’s all about the investment thesis and the results. Those divide into three broad

categories:

Success: drills hit and return something exciting. The share price responds. I almost always

sell some into a discovery price spike. Excitement runs a price like nothing else. Reality

(waiting for the next result, what the next result is) almost always brings it back down, at least

to some extent. This pattern happens time and again. If the stock has doubled or better, I sell

enough to take my cost base to zero. Play with the house’s money!

Neither up nor down: drill return some of what was sought but not enough. The market is

nonplussed and the stock doesn’t do much. Here the decision rests with the details of the

results - how does it grow or change the geologic theory and therefore outlook? - and what’s in

the hopper - more results still pending? different area/approach or same? pause because of

funding or seasonality? All of these things feed into a decision about whether to stick with or

sell and move on

Results disappoint: stock drops. Decision here again rests with the details of the results (did

the result invalidate the whole thesis or just part of it? did the drilling work -reach intended

target and good core recovery?) and with what else is pending (more holes testing another

idea/approach? or that’s it?). I think you have to go through that assessment and come out

pretty optimistic about the potential to hold if a stock has tanked on drilling news simply

3

because the market is hesitant to give projects a second chance, so the bar for success

ironically gets higher with each failure…

Resource growth/developers: it’s about two things: catalysts and the market

are there clear catalysts on the horizon? testing new zones, a maiden resource, a PEA? If so,

holding to and through these events can work well (unless, of course, the news disappoints).

speculation ahead of the news can also generate lift, so sometimes it makes sense to sell into

that wave.

In a rising market, defined ounces/pounds that are taking clear steps forward and

demonstrating tangible value along the way provide great leverage. A strong management

team that drums up and maintains excitement over the stock’s potential as a takeout really

helps (drives retail investors in). Marathon Gold is a great example of a great project

advancing steadily and successfully that has takeout target written all over it - it has

outperformed peers by a mile.

Mine builders: this is the golden runway. In general, it makes sense to hold builders until first pour.

PGM is a great example. Once the mine starts up the stock could keep rising but the risks of failure

increase for sure (metallurgical issues, processing problems, rock competency challenges, debt

walls, etc).

I haven’t given you ANY actual timelines, but that’s because there is simply nothing to say that

applies across the spectrum of stocks in our sector. It’s all about what the investment premise is, how

new data feeds into it, and how the stock has performed.

It’s SO easy to hold onto underperformers thinking a recovery is around the corner. It’s also so easy

to hold onto outperforms, thinking there’s more coming. In both of these situations, it comes down to

relative appreciation potential.

If your investment thesis pans out, what might the stock be worth? What is the risk it doesn’t work

out? What other forces will impact the share price in the meantime (need to finance, free trade date

from a financing a few months ago, seasonal restrictions on when they can work, etc)? And have you

already gained or are you already down??

Consider those concepts and then think about whether you’d rather have your money in that stock or

in another stock, perhaps one you just learned about that you really like. that’s what I mean by

relative appreciation potential - would your capital have better odds of generating the kind of gains

you seek in this stock or in another?

--------------------------------------------------------------------------------------------------------

Selling Pucara Gold (TSXV: TORO) and Lessons Learned

Well that really sucked.

If you missed it, Maven portfolio holding Pucara Gold released results from its entire Phase I drill

program at Lourdes yesterday morning. The stock is down 60%.

4

The evidence for a high sulphidation epithermal system at Lourdes was very strong. Between soil and

rock samples, alteration mapping, minerology in structures, multiple kinds of geophysics, rock type,

and locale, Lourdes ticked every box on the list of HSE charateristics.

And the people behind Pucara are some of the people who essentially wrote that list, having

discovered some of the best HSE gold systems known to date.

Put it together and TORO was an exciting story.

Unfortunately, the rocks had other ideas. Pucara released results from all 25 phase I drill holes and,

long story short, they failed. Only six holes returned gold and those intercepts were less than 0.3 g/t

gold.

It looks like the system, if it exists, is much deeper than the team thought. The alteration in the drill

cores looks very distal – far from – the core of any HSE system.

What now? Pucara will return to Lourdes in April to test the side of the project that they didn’t get to in

Phase I. The south and southeastern parts of Lourdes are steeper, which is the main reason they

weren’t drilled in Phase I – Pucara couldn’t establish good access in time. Now that topography could

be on their side, as the steep hills mean access to deeper parts of the system.

There are some good numbers in this southeastern area, including from the Cascadia diatreme,

which actually generated the longest trench and channel samples of gold from across the property.

So they may yet hit into something there.

However…Pucara is not the story it was three days ago. Even if they do hit into something in Phase

2, the lack of gold across the targets tested in Phase 1 means the huge HSE gold system they

thought they might drill into isn’t close to surface, which very much changes the bar of success.

This was an exploration speculation. And the strength of the targets plus the people behind it meant it

attracted a lot of speculators. As you will have seen, many of those speculators sold out yesterday as

soon as the results hit the wires. The stock lost 50% yesterday.

It’s now a $20-million market cap company with $5 million in the bank, a good structure and support

from lots of deep pocketed, resource investing savvy investors, and two projects. Lourdes isn’t dead

and will see more work, though the size and likelihood of hitting the prize are significantly diminished.

They also have Pacaska, which is another HSE target in Peru. Pacaska has similar evidence of a

HSE gold system. Pucara is working on permits and expects to be able to drill by Q3. The failure at

Lourdes means the market is not likely to build up such anticipation for Pacaska, but that doesn’t

change the rocks. They might hold a HSE gold surprise. Pucara will be able to do surface work, like

trenching and sampling, while they await permits there.

At $20 million, this company is fairly valued, given its team, backers, and projects. That doesn’t mean

I am particularly interested in owning it right now. I bought in tranches with an average price of $0.75.

The stock closed today at $0.30 and, now that I’ve communicated with all of you, I’ll sell in the

morning. A 60% loss certainly stings but such is the risk of exploration speculation.

I have to admit – these results took me by surprise. They missed?!? But the evidence was so good!

And the geologists were global HSE experts! How?!?

Of course, the answer is that geology is tricky and drilling is the only way to really know what’s going

on beneath the surface. The surface gives hints; geophysics adds to those hints. Geologists use all

the available data to theorize. But we never actually know until we drill.

So that’s the first take away lesson from Pucara: never forget that exploration is incredibly high risk,

no matter how good the evidence appears.

5

Of course, we have to rely on the evidence to make a decision to invest. As part of that we consider

the people presenting the information: whether their experience and track record makes us more or

less inclined to believe the theory.

But that’s where it gets tricky. Because everyone wants to make a discovery. And that want can

overshadow caution for even the most experienced explorers, especially when the pre-drilling

evidence is strong.

That’s what happened here. This group of HSE gold experts got carried away by their theory. And a

lot of speculators went along with them, myself included, because they are such experts.

I’m not saying they should not have been excited. They saw the data and truly thought they had a

very good shot at making a major HSE gold discovery. And so that’s the story they told investors as

they brought this story to market and it was a good enough story to raise $8.5 million and support a

market cap of $50 million, which is very high for a pre-discovery explorer.

But setting the bar high leaves a lot of room to fall. And while we all expect explorers to fail, and

therefore failure certainly doesn’t destroy reputations, reputations are more tarnished when expert

explorers fail on a target that they presented as guaranteed.

The Pucara team will absolutely survive this. They have impressive track records reaching back many

years. But they will have to repair some relations. I would also guess they won’t be as confident about

any pre-drill targets in the future.

I’m sorry this one failed and that I got as swept up in the confidence as everyone else.

--------------------------------------------------------------------------------------------------------

Maven Buys: Montage Gold (TSXV: MAU)

I sent a quick note this morning that I was about to buy Montage Gold. The pre-letter note was

needed because I realized Montage is releasing its resource update tomorrow (Thursday) pre market

and I wanted to own the stock before that happened.

I can’t know whether the update will impress the market, but I’m inclined to think it will. The company

has been guiding shareholders to expect the count to double from 1.5 million ounces to 3 million.

That’s a big step, especially for a project that a lot of investors still haven’t noticed because it was

hidden behind other assets until a spin-out in October.

The team, scale of deposit, and stage of asset (it’s early but advanced, as I’ll explain in a bit) mean

this isn’t a small company: Montage has a market cap of $105 million and has $33 million in the bank.

But I think it’s undervalued relative to what it has, cheap relative to what the resource update will add,

and has very good potential to re-rate as it gains market awareness and as this team moves this

project forward at a breakneck, but doable, pace.

Montage is completely focused on the Morondo project in Cote d’Ivoire. And they know this asset

inside and out, because the team at Montage are the same guys who staked Morondo in 2008. At the

time they were the geologic drivers at Red Back Mining and had discovered two major deposits in

West Africa, Chirano and Tasiast. Red Back then gave Hugh Stuart and his crew free reign to do

grassroots exploration across West Africa.

They homed in on Morondo as the intersection of two good gold belts, did some prospecting, and

staked it. Soon thereafter, though, Kinross swept in and bought Red Back for Tasiast and Chirano.

6

Kinross focused on those two assets and did only touches of work at Morondo. Stuart kept tabs on

the asset, though, staying in touch with the communities and with the local workers who Kinross

employed on the site.

When Stuart started another company he optioned Morondo but that company ended up focused on

lithium and cobalt. After that Stuart and his group started Orca Gold (TSXV: ORG). Orca is advancing

the Block 14 project in Sudan, which is a great deposit in a tough jurisdiction. To diversify Orca’s

exposure to Sudan, Stuart bought (guess what?) Morondo.

By 2018 they had done enough work to outline a maiden 1.5-million-ounce resource, but no one

cared because when investors looked at Orca Gold all they saw was Sudan. At the same time,

Morondo had reached a point where it deserved a significant budget and a focused team. And so

Morondo was spun out, creating Montage Gold.

That happened just in October. While the corporate side was getting sorted Stuart’s team completed

8,000 metres of drilling at the project. The latest news release summarized the results of that work –

and is a good starting point to demonstrate why this asset is worth more than the market is currently

giving it.

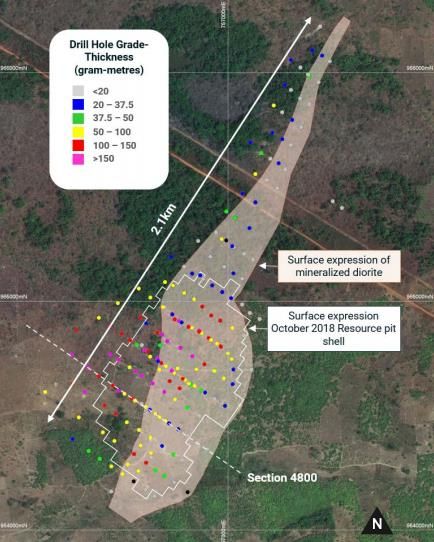

To double the outline of a 1.5-million ounce deposit along strike and at depth with 8,000 metres of

drilling stands out. It was possible because the Kone orebody is very homogeneous and very wide,

averaging 300 metres across.

Results from that drill program included 201 metres of 0.8 g/t gold, including 48 metres of 1.9 g/t gold,

331 metres of 0.58 g/t gold, including 99 metres of 0.96 g/t gold, and 226 metres of 0.77 g/t gold,

including 105 metres of 1.24 g/t gold.

Those grades might not jump out at you but those widths should. They weren’t drilling down plunge or

along strike – this thing is just that wide.

7

As this drill plan map shows, the doubling along strike part is a less significant than the depth part.

Mineralization indeed continues along 2.1 km of strike but the grade appears to weaken and it gets

skinnier.

In the main part of the deposit, though, the drill hole dots give an idea of how this thing is growing.

The cross section below does a better job.

8

The resource from 2018 stands at 52.5 million inferred tonnes grading 0.91 g/t gold for 1.54 million

ounces. It’s pit constrained but, as you can imagine looking at that cross section, there’s lots of room

for the pit to go deeper. No one wrapped a PEA around that resource but the strip ratio is about 1 to

1, which is nice and low.

Now imagine pushing mineralization all the way across the pink diorite and to depth within it. Then

imagine steepening the pit walls from 45 degree to 55 degrees, which is what geotechnical work

supports. It’s easy to imagine a much bigger pit encompassing a lot more gold, with a strip ratio that’s

still about 1 to 1.

Tomorrow’s resource update should be a big step in that direction. Montage has guided the market to

expect the resource to double, to 3 million ounces.

Two months from now we’ll know a lot more about how those 3 million ounces might be mined, as

Montage will issue a PEA before the end of Q1. Here are some of the project attributes that will

matter in that mine plan:

Met testing shows 92% gold recovery with straightforward CIL processing

The rock is soft, with a bond work index ranging from 9.8 to 10.7 kW-hour per tonne. That

means the process plant should only need one-stage crushing and power usage will not be

high.

There’s a road through the property and the national power grid, with excess capacity, is only

20 km away.

The strip ratio will likely remain in the 1:1 range, given that Geotech work supports steepening

the pit walls and that the resource will reach deeper.

9

OK. So Morondo is a large, open pittable, easily workable, low grade gold deposit. How is the story

going to generate excitement over the next year?

With speed. Montage will issue a PEA in late March and then plans to issue a feasibility study by the

end of the year.

It commonly takes 2 to 5 years to go from PEA to feasibility study, even when a project takes a fairly

straight line. How will Montage move Morondo ahead so quickly?

The answers are varied: because Stuart is so familiar with the asset. Because the deposit is so

homogenous and fits so easily into an open pit. Because the metallurgy is straightforward. Because

the PEA is really being done to pre-feasibility levels; it just can’t be called a PFS because the

resource hasn’t been drilled to indicated status yet. Because Orca did a good amount of the important

technical work already, like geotechnical and hydrological drilling and metallurgical testing. Because

this team has designed several similar mines in similar environments.

OK, if they can issue a feasibility study that quickly, the next question is what that will do. A feasibility

study is only useful if a mine can actually be built in short order – and that is also in line.

Permitting is much faster in Cote d’Ivoire than in many other places. Roxgold permitted its Seguela

project, which is just south of Morondo, recently and the process took less than a year. Montage is

working on its environmental impact assessment and expects to get that permit around this time next

year, shortly after the feasibility study comes out. The actually mining permit follows but can take just

weeks (as happened for Roxgold).

So this idea is to take this asset from little known to build ready in something like 16 months. That

would be impressive for an asset of any scale – but this is a biggie. The concept is for a mine

producing 250,000 oz a year for more than ten years.

The grade will be around the 1 g/t gold range. I know that’s not sexy but big gold mines can make big

money on 1 g/t gold if the setup is simple, if there are no major economic burdens (royalties, taxes,

etc), and if the gold price remains elevated. Those factors all line up for Morondo.

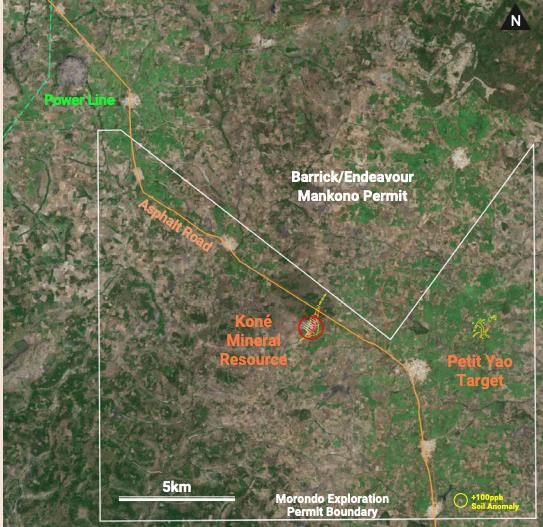

There’s another angle that could add interest, which is exploration. Kone was the first geophysical

anomaly drilled on the 1,40 sq. km land package. There are multiple other anomalies sitting untested

and Montage will advance these.

The most advanced is called Petit Yao, which is a large soil anomaly 8 km east of the Kone deposit

that might offer higher grades. A small drill program in 2019 yielded best results of 4.15 g/t gold over

12 metres from surface and 1.7 g/t gold over 15 metres from 15 metres depth. Montage will kick off a

combined drilling and trenching program there shortly. If Petit Yao is richer than Kone, it wouldn’t

have to be large to make a notable difference to the economics of a Morondo mine.

Lastly: the project is in northwest Core d’Ivoire. Several mid-tier and major gold miners operate in

Cote d’Ivoire, including Barrick, Endeavour, Perseus, and Roxgold, and an exploration boom has

yielded five significant discoveries in the last five years.

That the boom is only happening now isn’t too surprising, seeing as the country did endure two civil

wars in the last 30 years. Today it is trying to emerge from that period and miners have been made

welcome.

Structure and Valuation

Montage has 105 million shares outstanding. Orca Gold owns 31.5%, the Lundin family owns 7%,

and Sandstorm Gold has a 5.4% stake.

10The company has $33 million in the bank, which is more than enough to get through feasibility. They

will put extra cash to work on exploration should results warrant, such as at Petit Yao.

At today’s close of $1.00 it carries a $105-million market cap, or a $72-million enterprise value. With a

1.5-million ounce resource, the stock is valued at $47 per oz. That’s middle of the road. But by

tomorrow morning the resource will be 3 million ounces, or there abouts, which drops the EV-per-oz.

metric to just $24. That’s low.

But this isn’t a stock that deserves a low valuation. I get that Cote d’Ivoire will put some people off.

But this team has made multiple significant discoveries in West Africa before; they are undeniably

one of the best groups to be guiding this effort technically, in terms of expanding Kone and searching

for new deposits on the property. They are also a good capital markets team, having made a lot of

money for a lot of people in the past.

And Morondo is a project that is perfectly suited for the moment. I would class this stock as ‘active

optionality’. Morondo is about to become a 3-million ounce, low strip, soft rock, easy permitting, open

pit project. No one cared about it until now because high grade had stolen everyone’s attention. But

high-grade deposits are rarely big. And big projects are needed because big miners need big mines

to remain big into the future.

That’s why big projects attract so much attention later in gold bull markets. That’s the basic optionality

argument. The ‘active’ component here comes from the team, from the fact that the deal is still new

and undervalued, and from the fact that this project is being pushed ahead so quickly.

-------------------------------------------------------------------------------------------------------------

Why Maven Bought…Rokmaster (TSXV: RKR, USOTC:

RKMSF)

I wrote a quick note that I was buying Rokmaster on Christmas Eve. I had bids in for the open and got

a bit at $0.45 before it jumped all the way to $0.71 a few days later.

That jump happened because Crescat Capital, a fund focused on explorers and miners, invested in

RKR. The investment happened in mid-December; the share price jumped the week after Christmas

because Crescat’s technical lead, Quinton Hennigh, released a video explaining the opportunity he

sees at Rokmaster that prompted the fund to invest $2.75 million.

Hennigh is a widely respected geologist. He’s also very good at explaining geology to non-geos. As

such the videos that Crescat makes about its investment moves get a lot of views and, thus, have

impact.

Since then the price has softened some but held higher than it traded before the Crescat video, even

though there hasn’t been significant news.

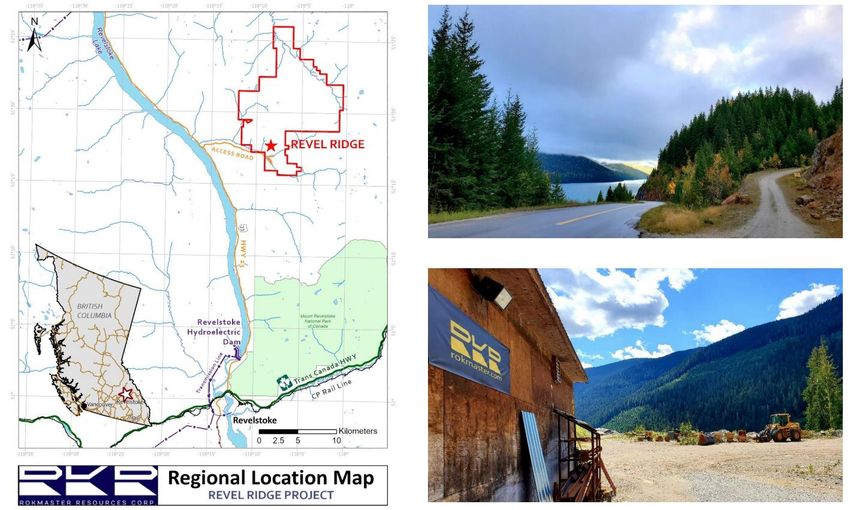

Rokmaster is a $44-million stock at the moment. It is totally focused on the Revel Ridge project in

southeast BC, some 40 km north of Revelstoke.

Revel Ridge is road accessible and has over 3 km of underground development in place. That work

means it also has its own underground mining fleet and a 40-man camp.

11Those came from Huakan Mining, the Chinese company that owned Revel Ridge for many years.

Huakan’s efforts added to a pile of work that started in 1912. In the 2000s Huakan drilled extensively

after driving 3.1 km of underground workings. The group also took several bulk samples.

By late 2010 Huakan had drilled enough to support a 43-101-compliant resource estimate, which

served as the basis for a PEA. In 2012 that resource was doubled in an update. And then everything

stopped.

Huakan shifted focused, perturbed by both their inability to solve the metallurgical challenges at Revel

Ridge and the beginning of the bear market. In 2017 a junior called Golden Dawn optioned the project

for a year and updated the resource before giving it back to Huakan.

Then in December 2019 Rokmaster inked a deal for Revel Ridge. Here’s the premise in point form:

The metallurgical challenge that stumped Huakan can be overcome. The gold is refractory but

pressure oxidation (POX) technology is now a well-established remedy. Rokmaster spent a

good part of its first year with the asset ensuring this was indeed the case; a PEA, released in

December, underlines that the ore can indeed be processed in conventional ways, plus a POX

circuit, to create easily saleable zinc and lead-silver concentrates and gold-silver dore

The resource at Revel Ridge has many positive attributes: it’s high grade (gold-silver-lead-

zinc), it’s fairly large, it sits in an amazingly consistent sheet of good width (3 metres) that dips

at a nice angle for underground mining, and it’s wide open for expansion

If Rokmaster can (1) convince the market that the metallurgy is no longer a problem and (2)

expand Revel Ridge in a few of the many ways that look possible, this deposit will be worth

significantly more than the $44 million that Rokmaster is trading at now.

There are two if’s in that last sentence. I think Rokmaster has made good progress on the first one by

issuing a PEA that shows an economic mine with a reasonably straightforward process circuit.

12The second task takes drilling and that is underway now.

The Asset

The PEA that Rokmaster just issued uses the resource estimate from 2018. That pegs the Main Zone

resource at 4.2 million measured and inferred tonnes grading 5.59 g/t gold, 53.4 g/t silver, 1.9% lead,

and 3.4% zinc plus 4.6 million inferred tonnes averaging 4.4 g/t gold, 62 g/t silver, 1.9% lead, and

2.6% zinc.

Yes, those are great grades. But what makes this deposit special is its shape. The Main zone is a

sheet, dipping about 70 degrees. It runs a very consistent 3 metres in width and is surrounded by

highly competent rock. In other words, it’s an ideal shape for underground mining.

There is another zone right beside the Main zone, called Yellow Jacket. It is a different thing. It’s a

stacked set of lenses of carbonate-hosted silver-zinc-lead mineralization sitting 5 to 30 metres into

the hanging wall of the Main zone. And it’s silver rich: most Kootenay Arc carbonate deposits of this

nature carry just a few grams silver per tonne but the Yellow Jacket zone averages 60 g/t silver.

The Yellow Jacket zone isn’t large but it’s got some scale, with a resource currently estimated at

764,000 indicated tonnes grading 9.98% zinc, 2.6% lead, and 63 g/t silver. It’s part of the PEA that

Rokmaster just put out.

That PEA outlined an underground mine tapping 9.4 million tonnes of Main zone mineralization

averaging 4.24 g/t gold, 50 g/t silver, 2.6% zinc, and 1.6% lead plus 650,000 tonnes of Yellow Jacket

mineralization averaging 7.5% zinc, 1.9% lead, and 43 g/t silver.

I know it’s hard to immediately understand the value of polymetallic rock. We all have context for gold

grades or copper grades, but it’s really hard to put polymetallic grades in context. One way is to

compare all-in sustaining costs per ounce gold, which for Revel Ridge came to US$842, and the

AISC per ounce net of by-product credits, which pull the cost to produce an ounce of gold down to

US$560.

Another way to look at it: the rock in the resource is worth $300 per tonne. The PEA pegs total

operating costs at $135 per tonne.

The mine as envisioned would produce 124,000 oz gold equivalent for year for 12 years.

The PEA generated an after-tax NPV of $423 million and a 29.5% after-tax IRR (using US$1,561 per

oz gold, US$20.55 per oz silver, US$1.07 per lb zinc, and US$0.91 per lb lead). It pegged capital

costs at $396 million.

The RKR team sees a lot of opportunity to grow the resource at Revel Ridge significantly but it was

important to do a PEA now in order to address the thing that overhangs this project: metallurgy.

The gold at Revel Ridge is refractory. For years that was a game stopper, as there was no

reasonable or economic way to recover the gold.

Now there is. RKR focused on this challenge over the last year and the PEA outlined the result: a

conventional milling, gravity, and flotation circuit to produce zinc and lead-silver concentrates for sale

to local smelters, plus an on-site pressure oxidation circuit to produce gold-silver dore.

That process is expected to recover 83.5% of the gold, 52% of the silver, 70% of the lead, and 63% of

the zinc in the rock.

While not ideal, these numbers are certainly good enough to work. And the saying ‘grade is king’

really points out that high grades make possible what otherwise would not be. At Revel Ridge, if the

13rock were not so valuable then it wouldn’t be worth treating it to get only those recoveries for silver,

lead, and zinc, and having to run a POX circuit to get the gold.

But the rock is that valuable and so it is worth doing all that.

The PEA says it makes sense to do based on what is known today. But the reason to invest is that

the exploration opportunity here is very significant.

The Exploration Opportunity

The Revel Ridge Main zone is a ductile shear zone hosting orogenic gold. It’s an incredibly consistent

and planar deposit: it averages 2.5 metres wide over the 1,500 metre by 800 metre portion that has

been drilled…and on-strike occurrences suggest the zone could continue for 8 kilometres!

Efficient and economic underground mining requires (1) competent rock, (2) wide deposits, (3)

continuous zones, and (4) a steep enough dip angle that gravity works for, not against, miners. Revel

Ridge has all of those in spades.

The rock around the sulphidic shear zone is very competent; 3 km of underground development says

so. The deposit is 2.5 metres wide and runs for kilometres. And it dips at about 70 degrees, which is

steep enough that rock falls efficiently in a mining scenario.

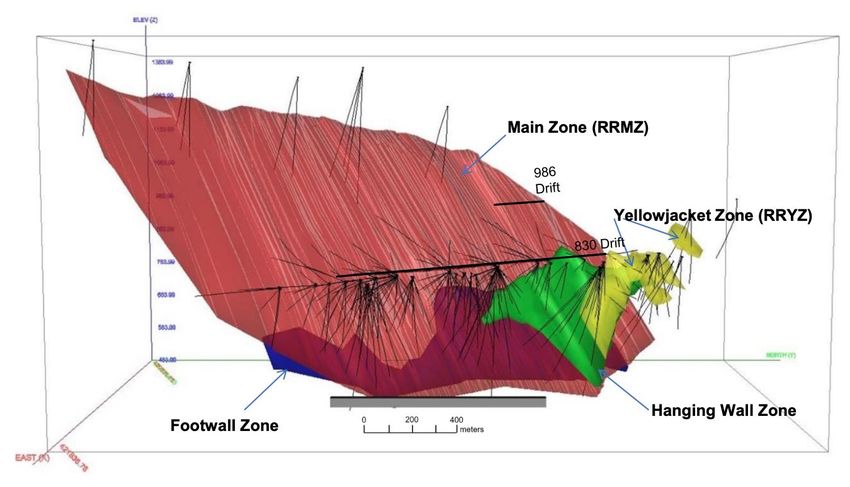

The red sheet is the Main zone. The Yellow Jacket zone is appropriately in yellow. The Hanging Wall

and Footwall zones are in green and blue; they are mineralogically similar to the Main zone but are

obviously much smaller.

The resource doesn’t come all the way to surface because the surface drilling was done on very wide

centers. So one opportunity is to drill some short surface holes to pull the deposit upward, though

grades are a bit weaker higher in the system.

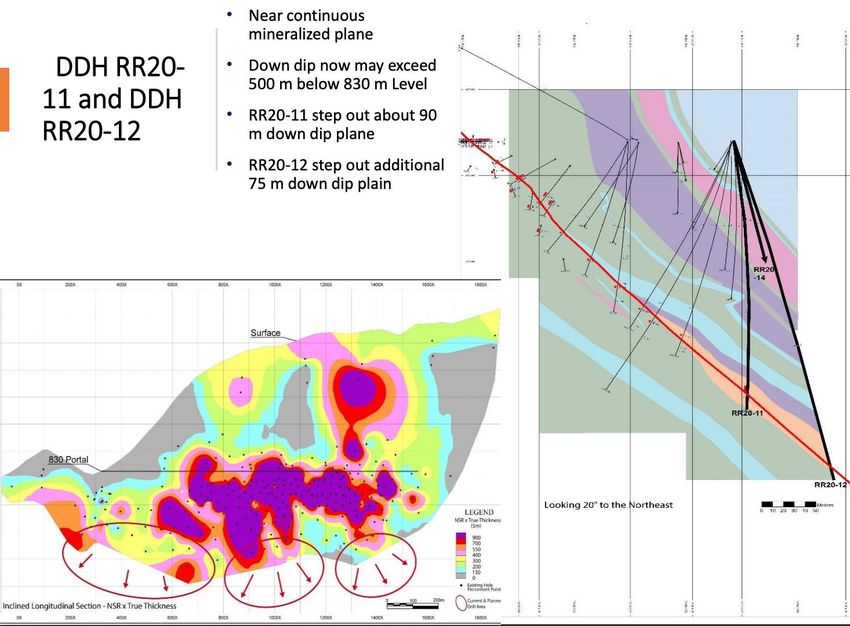

The next opportunity is the other way: to depth. Grades improve with depth and the deepest holes

have shown the zone continuing. So an important focus is drilling below the resource to pull it down.

14Rokmaster started that work last year with a few holes. Hole RR20-11 stepped 90 metres down the

dip plane and returned 3.9 metres of 5.3 g/t gold, 43 g/t silver, 1.95% lead, and 6.96% zinc. Hole

RR20-12 stepped another 75 metres downdip and results are not yet available.

Then there’s the along-strike opportunity. Mapping last summer traced the Main zone on surface “with

good continuity” for 1,500 metres northwest of the resource. There’s a coincident gold, silver, lead

geochem anomaly. This strike extent has never been drilled.

Soil samples also suggest potential for a parallel zone of mineralization in the hanging wall.

There’s great expansion potential for the Yellow Jacket zone as well. Mapping suggests the

carbonate stratigraphy continues for another kilometre to the northwest. Two historic holes from 1997

tested this area, returning 4.8 metres of 63 g.t silver, 15% zinc (!), and 2.9% lead and 4.5 metres of

53 g/t silver, 11% zinc, and 2.4% lead.

Stepping back, there’s the A&E target. This area has three historic adits and numerous trenches that

trace 400 metres of gold-silver-lead-zinc mineralization in the contact between two rock types (phyllite

and limestone), which is exactly the setup at the Main zone. Rokmaster’s reconnaissance program at

A&E last summer identified mineralization along 1.7 km of strike along trend from A&E; further extent

is obscured by glacial tills and talus boulder fields.

The potential to define a lot more ounces and pounds at Revel Ridge is very real. The Main zone is

incredibly consistent where it is drilled; there’s clear opportunity to expand it at depth, towards

surface, and along strike. In all of those directions there is reason to believe mineralization continues

and the resource is only limited by lack of drilling. The A&E zone is a bonus, a second whole area

only 5 km away that looks very similar but has not been drilled. And the Yellow Jacket zone looks

likely to grow along strike as well.

15To chase these opportunities every hole of RKR’s 16,000-metres drill plan for 2021 is outside of the

resource. This is not an infill effort; this is all about finding the next million ounces and continuing from

there.

The Deal…

That Rokmaster CEO John Mirko believed in this asset from the outset is evident in the deal he

signed and Rokmaster’s situation when he signed it: he negotiated to buy Revel Ridge from Huakan

when Rokmaster was trading at just $0.06 and had only $250,000 in the bank.

Because Rokmaster didn’t have any capital and because Mirko needed time to ensure the metallurgy

would work before putting down a lot of cash, he inked a deal wherein the majority of the payments

come in years three, four, and five. That worked really well to get Revel Ridge but it does create an

overhang.

Over the next five years the company has to make payments totalling $44 million. The majority of the

money is due in 2024 and 2025, when the payments are $13 million and $20 million.

It’s not great to have such a payment overhang. But $44 million is a reasonable price given what

Rokmaster bought: over 2 million high grade ounces defined via 315 drill holes, significant

underground development, notable permits, surface and underground mining equipment, and major

potential to add ounces and pounds.

And if Rokmaster hits into good grades under and along strike from the Main zone (let alone at A&E)

and thus demonstrates that this deposit can grow substantially, the payments won’t be a problem.

Rokmaster has 98 million shares outstanding. The company has a valuation of $44 million. Using the

gold equivalent count of 2 million ounces, the market is giving RKR just $22 per oz.

A reasonable comparable is Skeena Resource. Skeena went through similar challenges – questions

about metallurgy that they answered, balloon payments that they managed. The market now gives

SKE almost $200 per gold equivalent ounce.

That re-rating will take time – it will take drilling success and it will take ongoing marketing to keep

convincing people that the metallurgy is not a problem. But if those things happen, I think that kind of

re-rating (way more $ per ounce and far more ounces) could be in the cards for Rokmaster.

-------------------------------------------------------------------------------------------------------------

Portfolio Updates

Bluestone Resources (TSXV: BSR; USOTC: BBSRF)

Bluestone provided the market with an update on Cerro Blanco this week from a project development

perspective. It has spent the last several months optimizing the plan, including updating cost

estimates. More importantly, BSR has pushed back its timeline to produce a new resource estimate

and updated mine plan.

There are legitimate reasons for the delay, not least of which is the Covid crisis. Still, management is

electing to delay its project financing until it produces these pieces of the puzzle. This is an official

16delay (between three and six months), but I had been expecting project finance already some time

ago…so this is salt in the wound.

An interim study included in the release showed a capex increase from 2019’s feasibility study. It’s

now expected to be US$225 million instead of US$196 million. Those updated cost estimates I

referred to included an AISC increase to around US$675/oz, up from the US$579/oz projected in the

2019.

I bought into BSR on the sales pitch that this thing was going to be fast-tracked to production

because of its permitted status, extensive underground development, and build-ready team. Bottom

line: I’m done and will be selling. It’s just a relative appreciation potential decision. This stock will

remain well-supported through this long process because it has deep-pocketed and very committed

backers but I am neither of those – I need my capital to be in stocks where I see near term reason for

upside. Based on this extended timeline (and the fact that it’s taken so long to get to here) I am

exiting, wishing BSR all the best, and putting capital to work elsewhere.

Erdene Resource Development (TSX: ERD; USOTC: ERDCF)

Erdene released its final round of assays from drilling on Dark Horse. The market didn’t react but

today’s results are important. I get that 130 metres of 0.53 g/t gold (the highlight intersection of this

batch from Hole ADD-61) isn’t an attention-grabbing result on its own, but you have to take it in

context:

It was drilled 500 metres north of the closest the drill hole

It returned the longest intercept to date from this emerging zone

The interval is low grade, yes, but the few holes ERD has pegged into Dark Horse have already

shown that this area also hosts high grade (Hole ADD-58 returned 45 metres of 5.97 g/t gold starting

just 10 metres downhole). The pieces appear to be in place: a zone of significant scale and pervasive

mineralization, with high-grade components that ERD will have to figure out.

On the figuring-it-out front – it is important to remember that ERD honed its skills at the BK deposit.

It’s fair to say it took ERD several years to unlock the riddle of high grade there but now that they

17have they are hitting high grade with incredible reliability. It’s very reasonable to assume that some of

the same controls will exist here at Dark Horse, giving them a major head start.

Dark Horse looks likely to add a valuable piece to the ERD puzzle. It will take time and drilling but that

will also generate excitement while Erdene builds Bayan Khundii. Good stuff all around.

Fireweed Zinc (TSXV: FWZ; USOTC: FWEDF)

The assays are now in for those holes from Boundary that looked so good visually last year. As

expected, the results for these two holes were exceptional.

Hole 2 cut 212.7 metres of 4.4% zinc, 0.08% lead, and 10.7 g/t silver, including 5.8 metres of 25.6%

zinc, 0.14% lead, and 44.0 g/t silver. That hole was drilled perpendicularly, both to last year’s Hole 1

and to the original discovery holes back in 2019. Hole 1’s assays were impressive in their own right

and included a 5.0-metre interval grading 23.6% zinc, 0.22% lead, and 53.7 g/t silver within a 246.7

metres of 2.6% zinc, 0.06% lead, and 5.9 g/t silver.

Think about those lengths for a moment. Those are porphyry-type lengths, but this is a zinc-rich

SEDEX deposit. And a very large one, apparently.

Why are the holes perpendicular? Primarily to ensure that the 2019 discovery holes hadn’t overstated

the grade of the mineralization or misinterpreted the orientation. These results from last year’s Hole 1

and Hole 2 suggest they did not.

Looking ahead, it’s hard not to be excited about the potential scale of this discovery at Boundary.

There’s more drilling to do but a 100-million-tonne resource (to go with the large resource already

outlined at Tom and Jason at Mac Pass) seems well within the realm of possibility.

That the news didn’t goose FWZ’s share price as much as one might have expected speaks to the

market’s bias towards gold stories. Base metal projects just don’t have that sizzle, even when they

18produce assays that would almost certainly turbo-charge a gold story. No matter. The key here is that

Boundary has the potential to vastly expand an already impressive zinc story. And oh by the way,

Boundary West is still sitting there providing still more scale potential. More work is needed from here,

but it’s hard not to like the direction Mac Pass is taking with this major new find.

Great Bear Resources (TSXV: GBR; USOTC: GTBAF)

We got a couple pieces of news from Great Bear this past week. Most recently, GBR released met

results. We knew the low sulphide gold mineralization at Hinge was easy and conventional to recover.

These latest tests assessed the high sulphide gold at Limb as to its recoveries using the same

processing. Bottom line: it works great. There are lots of details yet to determine (specific grind sizes

and other additives to optimize) but at this point, so far away from mining, all we need to know is that

metallurgy is straightforward and it works.

And then there was the big financing. Management decided they needed more institutional names on

board. As I mentioned last week, GBR is ahead of itself in becoming an institutional story – it may not

yet have a maiden resource but because of the scale of this discovery, the amount we know about it,

and the value GBR is holding because of it, this stock is institutional (considered an advanced asset)

way before is usual.

It’s considered such…but it didn’t actually have many big institutional names on board. And the thing

with institutions is that they barely buy in the market. They always want to enter with big bets in a

financing; they might then add in the market.

GBR needed that adding and so needed to get these funds positioned. Retail interest has been

waning and so they needed to replace it in the market. Also, getting a prime set of funds to invest $70

million overnight gives other funds –who may have shied away to date because (1) there wasn’t yet a

big institutional shareholder base and (2) it doesn’t have a resource so how can they run their

models? – reason to start buying.

All good reasons to raise. And when your share price is this strong, you can raise $70 million and only

dilute your stock 7.5%. That’s pretty sweet. This raise will put GBR’s bank account at $100 million –

oodles of money to drill as much as they possibly can. Sure, the market balked at the price a bit. I

don’t mind. The goal here is to support the stock in new and important ways and I think it’s a good

move.

HighGold Mining (TSXV:HIGH, USOCT: HGGOF)

The market didn’t love HIGH’s last set of results from Johnson Tract. There are two things going on:

strong base metal grades are upsetting investors who wanted a high grade gold story and the

Northeast Offset hasn’t worked out as HIGH expected.

Both of these are fairly complicated to explain. I’ll try to do so here but I’m also recording a Zoom call

with Darwin tomorrow where we can dive in deeper.

The table below shows the latest result from the JT deposit.

19One scan through and you can see why gold investors were unexcited about these hits from JT. The

thing is:

JT is a complicated deposit that HighGold is still figuring out

The hits keep coming, even if base metals are stepping up and gold down in some areas

Drilling this season significantly expanded the JT deposit

20Let me start with my third point. The long section below shows the deposit as per last year’s resource

estimate in dark gold, with a back dotted outline. The red dashed line approximates how the deposit

looks now. Some of the intercepts that expanded the zone were amazing; others were more bread

and butter. But the zone is significantly bigger. And remember that the bread and butter at JT are

pretty tasty: this thing is wide (which means good economics for mining) and rich, whether more gold

or more base metals.

Continuing on the growth idea, another key conclusion from this year’s work is that JT is not cut off

down plunge. That had been the interpretation: that the Cuervo fault cut it off. But as the dashed grey

arrow in the long section above suggests, HighGold now sees no reason that the deposit end (the

Cuervo fault is not significant). HighGold also sees room to grow JT along strike to some extent to the

north (left side of the long section).

Green pointed out on our call that holes 120 and 121 are almost identical. On the long section above,

one is near the toe (if you think of the shape as a boot) while the other is way up the ankle. They’re

over 300 metres apart and they returned almost identical widths and grades. That’s just a reminder

that, while JT has a lot of variability, the overall continuity in terms of width and grade is very good.

21Going back to my list, the first point was that JT is complicated and HIGH is still figuring it out. The

second batch of results from this release points to that, in a good way. The table below shows results

from the Footwall copper-silver zone.

22Those are some very nice copper, silver, and zinc numbers. I know that gold investors don’t like other

metals ‘getting in the way’ but at JT that’s the nature of the beast. And they aren’t in the way; they’re

adding both value and information.

On the value front, the bolded lines mark intercepts running better than 50 gram-metres gold

equivalent. Gold equivalence has its weaknesses but it is a good way to capture value and this rock is

valuable.

On the information front, these hits are from a distinct zone that HighGold is calling the Footwall zone.

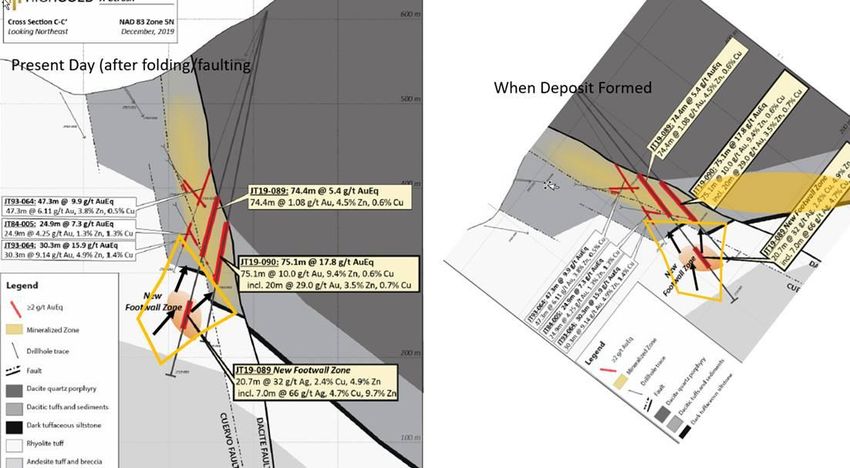

The cross section below is dated (from last year) but it shows the then-emerging Footwal zone

outlined in gold. I’m sharing this old cross section because on the right Green rotated the image 45

degrees to illustrate how he thinks this thing sat when it originally formed.

What’s important is that the Footwall zone didn’t form beside the gold-rich JT deposit; it formed under

it. It’s the feeder structure for JT. That has a few important implications.

First, it’s very much worth chasing this zone ‘down’ along its original orientation, as copper grades

could be very nice going down a feeder. In the modern orientation down isn’t down but is alongside to

the north.

Second, hitting good copper doesn’t mean that the JT deposit is ending or running out of gold. The

way this thing has been tilted (which HighGold didn’t understand until now) means gold has good

space to continue.

And this zone – the best intercept at this point runs 1% copper along 60 metres! It’s got scale and

grade (1% copper isn’t super exciting on its own but it is exciting in context).

OK, way at the start of this update I said there were two reasons the market didn’t like these results:

base metals instead of high-grade gold (which I’ve discussed) and the Northern Offset target not

working.

The Northern Offset target was an enticing idea and it certainly helped HIGH raise almost $14 million

before the summer drill program started. The idea: the Dacite fault cut the JT deposit off and the

Northern Offset could be the continuation of this incredible deposit on the other side.

Had it worked, it would have been amazing. But rocks are rarely that easy.

23The Northern Offset target returned very little gold. There were some short hits with good zinc and

copper, but the style of mineralization looks quite distal (far from) the core of a JT-type deposit.

That style of mineralization plus other evidence gathered through drilling at JT and prospecting along

the corridor has HighGold now thinking that there is less offset along the Dacite fault than they initially

thought. In other words, the ‘continuation of JT’ idea is still alive and sitting somewhere between the

Northeast Offset and JT. HighGold is refining drill targets along this untested trend for next summer.

Looking ahead: there are still results pending from JT (the holes marked in green on the long

section). Green is optimistic they will return grade, but only assays will tell how strong. So is there

reason to hold this stock from here?

Yes.

Explorers working in the north with limited summer field seasons mark out a reliable share

price pattern that includes a bottom around January-February. From there, anticipation over

next season starts to build and lifts the price through the spring. That pattern suggests selling

now would likely be selling at the bottom, which isn’t a great idea.

HIGH is also working in Ontario, testing targets on the Munro Croesus gold project near

Timmins. They drilled 31 holes in the fall and results are still pending from 23 of those holes.

Munro-Croesus has the potential to generate very high-grade results. Narrow high-grade hits

in Ontario won’t move the needle much for HIGH but (1) a series of hits could start to attract

attention and (2) simply having news to report helps.

HIGH doesn’t need to raise any cash to drill this summer in Alaska. If the market strengthens

and it seems like a good idea they might do so, but they don’t have to.

I am content to hold HIGH through the results pending from JT and MC at the very least, and likely

into next summer’s drilling where I think a now-solid base of geologic understanding sets HighGold up

well to find more of the kind of mineralization that the market so loved.

Osino Resources (TSXV: OSI; USOTC: OSIIF)

A big batch of assays from OSI’s 51,000-metre, 2020 drilling program at Twin Hills was highlighted by

some long widths of mineable-grade mineralization on the Clouds discovery. Hole 92 provided the

best interval, cutting 50 metres of 1.8 g/t gold from 88 metres downhole and 29 meters of 1.1 g/t from

31 metres downhole.

In addition, resource drilling on the Twin Hills Central target continued to deliver long intersections of

very passable grades (e.g., 184 metres of 1.1 g/t in Hole 117). The company plans to drill another

75,000 metres at Twin Hills in 2021, with details to be announced next month.

24With the maiden resource estimate for Twin Hills due out later this quarter and a PEA to follow in Q2

2021, OSI is set up with potential share price catalysts throughout the year. Given the good results

from the Clouds East area, that target is likely to contribute to those initial resource numbers. So far, it

has been traced for 350 metres along strike and is open to the east and west. The THC and the

broader Clouds target cover more than three kilometres of strike length.

The market didn’t react much to this latest batch of results, but then there was nothing earth-

shattering in them – just more good assays from a potentially open-pittable resource that’s showing

very real scale potential.

Orezone Gold (TSXV: ORE; USOTC: VGLDF)

They did it! Orezone inked a complete funding package to build Bombore. I have a Zoom call booked

with Patrick Downey to discuss some of the details further, like what all is involved in getting a

package like this across the line, what he specifically avoided and what he ensured was included (this

is NOT the first time Patrick Downey has negotiated a mine build debt package), and what the re-

rating potential on the stock looks like from here. That will happen in about 10 days, as Downey is

currently in Burkina Faso.

Until then, here are my thoughts. First, it stands out that ORE avoided any gold streams, royalties, or

early payment requirements. Such strings are really common but they are also pretty darn expensive,

adding a few percent to the overall effective interest rate. They also complicate people’s

understanding of payback. All told, they are best to avoid if possible and Downey did just that.

The facility has four components:

US$64M in medium-term debt. 5-year term. Can be drawn in multiple tranches. Repayments

deferred for first two years. 9% interest rate.

25 US$32M in short-term debt. Up to two drawdowns. 12-month term from first drawdown. Available

after medium-term loan is fully drawn. 8% interest rate.

US$35M convertible note facility. 5-year term. Available until September 30 as single drawdown.

Lender can convert to shares at any time at a rate of C$1.38 per share. Lender is Resource

Capital, which already owns 19.9% of ORE.

US$51M financing: 62M shares at C$1.05. Demand is already well above US$51M so 15%

greenshoe will likely be filled (another 9M shares).

Yes, the package will bring a good amount of dilution but that’s the cost of building a mine and going

from spending money to making it. And to management’s credit, the debt-equity ratio and the share

issuance is pretty much in line with what they’ve told everyone to expect in conversations over the

last year.

This mine is now getting built! Remember: it is permitted and engineered and most of the time-

consuming pre-construction work is done, most importantly the resettlement program. Between

Downey’s oversight (did I mention that he’s already built a whack of mines, very successfully?) and

work being carried out by EPCM, the best mine builder in West Africa, I expect this thing to be on

time and budget.

What’s the outlook for ORE shares from here? Using spot prices, ORE’s market cap is about 40% of

its net asset value (0.4 price-NAV ratio). Given this team and the fact that Bombore should generate a

better-than-90% after-tax IRR, Orezone should re-rate towards its NAV by the time it pours first gold.

Yes, I’m saying that ORE should gain at least 100%, and perhaps 150%, over the next 18 months.

(Remember Pure Gold?)

Outcrop Gold (TSXV: OCG; USOTC: MRDDF)

OCG is expanding its search for more potential high-grade shoots to test at Santa Ana. That work is

pivoting to an extensive airborne survey from recently completed ground IP and resistivity surveying

on the property. The targets identified by the ground surveying have correlated with previously

outlined soil geochemistry targets. These coincident anomalies have highlighted eight new targets.

Given the 100% success rate OCG has enjoyed so far testing possible targets, having more to put in

the drilling pipeline is a tantalizing prospect.

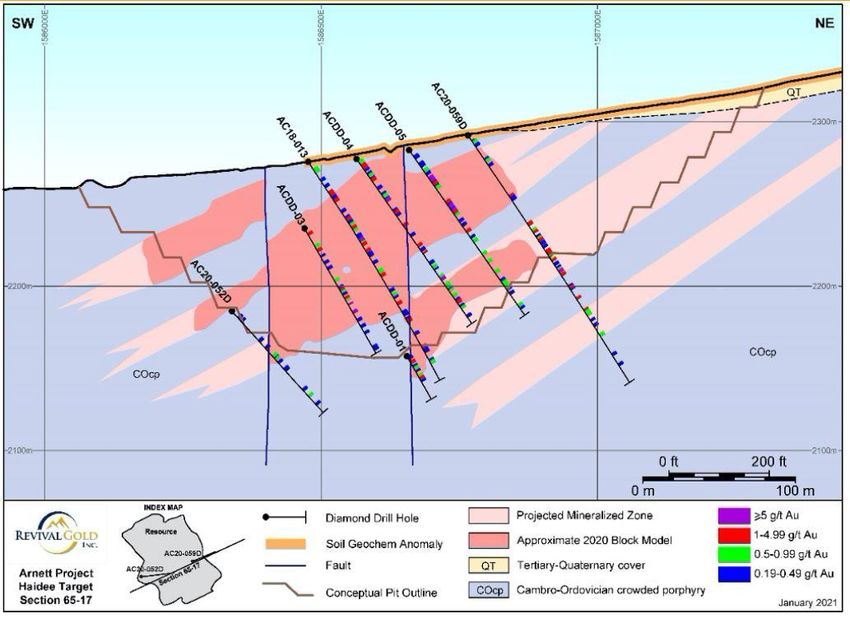

Revival Gold (TSXV: RVG; USOTC: RVLGF)

Assays for the remaining seven holes drilled on Arnett’s Haidee target hit the newswires this week. It

was more of the same – consistent, albeit middling grade intercepts of oxide gold. A couple of

examples from this batch are Hole 54D (0.55 g/t over 16.7 metres) and Hole 66D (0.53 over 20.5

metres and 0.25 g/t over 31.7 metres).

The near-surface oxide zone is now 600 metres x 400 metres and remains open in all directions. It’s

worth noting that every one of the 30 holes drilled at Haidee hit mineralization. Also, as the map

below demonstrates, the stacked zones of mineralization there extend up-dip to the northeast, which

could have positive strip ratio implications for any pit dug on the target.

26You can also read