The Maven Letter: September 15, 2021 - Resource Maven

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Maven Letter: September 15, 2021 Tracking The Uranium Bull. Beaver Creek Thoughts: The Path From Here, M&A – Yay or Nay? Portfolio Review Part II. Free Trade Date Table. Full Portfolio Table & Portfolio Updates from EMX, Great Bear, HighGold, Integra, Sassy. Getting through the emails and work tasks that piled up while I was away served as a good reminder that there were advantages to not traveling for the last 18 months! But the trip to Beaver Creek was worth the slog of the last few days. I am almost ready to move on a copper stock I met and liked in Beaver Creek. It’s an advanced asset with a team known for execution and market timing. Expect that rationale next week. I am still working through the research on several others, including a polymetallic explorer, a gold developer, and two new gold players working to reinvigorate old assets. That’s next week. This week I start with a follow up on my uranium buys from the weekend, including comments on how I plan to cover the six uranium stocks that are now in the portfolio (bottom line: as a group!). Then I run through two of the macro metals thoughts that stuck with me after hours of shop talk in Beaver Creek: why metal stocks are weak when prices are strong and when the M&A cycle will kick off. After that I get back into the Portfolio Review, but I have to admit that it’s going to take a while to get through this task! The writeups will tighten up once I get to the explorers, but I’m still working through the PEA or PFS-stage projects and there is always a lot to discuss with projects of that stage. I got through just three this week, as I catch up from being away, prepare for the Metals Investor Forum starting tomorrow, and find time to communicate three financing opportunities to Maven Premium subscribers (two gold explorers preparing to IPO and a copper play also getting set to emerge). After updating those investment theses it’s the Free Trade Date table. Then it’s the Full Portfolio Table and Portfolio Updates from EMX, Great Bear, HighGold, Integra, and Sassy. --------------------------------------------------------------------------------------------------------------------

Tracking The Uranium Bull

After adding to my positions in Maven Letter holdings IsoEnergy, Uranium Energy, and

Nexgen, and adding positions in Fission, ValOre, and Denison, I am happy with my uranium

exposure. I believe the bull run that started a few weeks ago has a good distance yet to run.

Remember, it’s buying by the Sprott Physical Uranium Trust that is propelling this leg of the

market and SPUT continues to raise capital via its At The Market financing and immediately

commit that capital to physical uranium purchases. Yesterday, for instance, SPUT issued US$75

million in new shares and the trust has purchased 7.9 million lbs. of U3O8 since launching its

ATM on August 17. It has bought pounds 18 of the last 20 possible days and the fund has

something like three quarters of a billion dollars of financing capacity as yet undeployed.

While I selected uranium stocks that I like for their projects, teams, and plans, the uranium

segment of the portfolio is really a bet that we are heading into a major uranium bull run.

When uranium markets go, the shortage of uranium stocks means the few that exist enjoy

extreme buying.

Since that’s the principle, I will not cover the six uranium stocks in the Maven Letter portfolio

as individual stocks. Major news from any particular stock will still carry weight but, big events

aside, these stocks will move mostly with the market. As such I’ll comment on the uranium

market each week and will include in that note news from any portfolio company that I think

matters enough to move the stock up or down in a significant way relative to the bigger forces

at play.

-------------------------------------------------------------------------------------------------

Beaver Creek Thoughts: The Path From Here

Those of us at Beaver Creek tried our best in conversations over coffees and beers to figure

out:

Why is the gold equity market so soft when gold is worth US$1800 per oz.?

What is needed to bring investor attention to gold and gold equities?

Why are copper stocks not pricing in today’s strong copper price?

Is the outlook for copper as strong as we all think it is? Or is our optimism blinding us to

a weak link?

Why aren’t more deals happening? Majors are flush with cash – why aren’t they buying?

2

I tackle the last question in the next article, as it deserves dedicated focus.

As for the first two questions, I didn’t come away with any major new insights. Gold equities

are soft because the rest of the stock market is hot, leaving investors with little need to

diversify or hedge. What changes that could be a stock market correction – but we know the

Fed will step in to stop slides of any significance – or a move to tightening, which could change

sentiment around risk and encourage value rather than only growth but could also cause a

stock market correction.

I’ve discussed tightening ad nauseum and it remains the thing I think is needed: for the Fed to

tighten in some way (tapering bond purchases is the most likely first step) and in doing so

officially validate inflation. Gold stands for many as the first and best hedge against inflation,

which is why gold usually runs with the start of a tightening cycle.

Whether or when tightening will start is tough to know. Certainly economic data has been

pretty mixed of late, with a big miss on jobs and lower inflation in August countered by a tight

job market and inflation still running at 5.3% year over year.

We can hope for some insight next week, when the Fed has its next meeting. I think it likely

Powell will test the waters by at least talking about tapering, to see the reaction as much as

anything else. If that happens, it could well stoke gold’s seasonal fire.

Upside for gold in such a setting would likely come alongside weakness for equities. And that,

my friends, begs the question of what would come next. The Fed is now committed to

supporting the stock market so the market’s reaction will determine whether tightening ends

with tapering or continues. The Speculative Investor blog summed this relationship up nicely in

his blog post The Crisis-Monetization Cycle, from which I’ve excerpted the paragraph below.

“The US economy is immersed in a crisis-monetisation cycle, as are many other

economies. In the US, a crisis or a deflation scare or a recession or even just a steep stock

market decline prompts the Fed to start monetising assets, with the speed and

magnitude of the monetisation ramping up until equity and consumer prices resume

their long-term upward trends. This has been going on for decades and explains why the

US stock market’s valuation keeps making higher highs and higher lows.

Makes sense right? Explains how stocks have remained in a bull market despite several major

crises over the last decade. And if you agree with this outlook, you realize that there isn’t a lot

of tightening ahead because, as soon as tightening comes close to threatening debt defaults or

the debt-based growth on which the market relies, a market correction will force the Fed to

step back.

So while further tightening would be the easiest path for gold, I think a taper tantrum that

forces the Fed into more support is very likely not long after tightening gets underway.

3

Would that also work for gold? I think it would. In late 2018 the Fed tried to tighten via

tapering, the market threw a fit, and within two months the Fed backtracked. Gold benefitted

through 2019 as investors realized there really is no path out of negative real rates.

As some point, that realization will bring attention to gold equities. It will likely require gold to

best some arbitrary but emotional level, like US$1900 per oz. (which isn’t so very far away).

Until then…it’s positioning and patience.

As for the copper questions posed above, I did not encounter anyone negative on copper at

the conference. Perhaps the Kool Aid was very well distributed…or perhaps the copper

argument is just that strong. I will admit that I am more interested in copper opportunities

right now than I am in gold stocks, at least when considering adding names to the portfolio.

-------------------------------------------------------------------------------------------------

Beaver Creek Thoughts: M&A – Yay or Nay?

A question that’s been hanging over the sector for some time now is: when will the big fish

start biting?

Takeout deals are important in building a bull market. They create excitement by offering

premiums and validating projects. They liberate capital, as investors take the win and move on

to the next deal. And they support the investment thesis that underpins most stocks in the

junior mining space – that good projects will get taken out.

For the 18 months, deals have been limited. The ones that have transpired were almost all

established prior, with majors acquiring companies in which they had already taken a strategic

interest.

We can blame COVID and that’s valid, to a point. Majors do not buy projects without spending

significant time on the ground assessing everything from geology to engineering to social

license and COVID made many such site visits impossible.

But I don’t think it’s only because of COVID. My fear is that the lack of deals reveals how

reticent majors are to repeat the mistakes they made last time they had money, when they

poured cash into overpriced deals for risk-laden assets. Many of those deals ended up

spectacular failures.

Rather than risk coming even close to that again, majors are choosing to bank capital, pay

dividends, and buy back shares rather than buy anything.

At some point they will have to buy again, fear or no fear. But the longer we go without a bid

for even the most obvious of assets (like Great Bear’s Dixie or Marathon Gold’s Valentine

Lake), the more I wonder whether deals will become the force we want and expect them to

4

become in this market…or whether in this bull market majors will prioritize profits, dividends,

and cash so much that deals end up few and far between.

The numbers stand against that. Miners are depleting reserves faster than they are replacing.

And while production profiles are generally good for the next five or so years, we all know that

it takes five to ten years to do the drilling, environmental work, permitting, and engineering

needed to build a mine, at least for most projects. So every executive at a major mining

company knows they could avoid the risk of buying assets for a while…but that such a decision

would threaten the company’s production in 5 to 10 years. And no one wants to be the CEO

that failed to fill the project pipeline when projects were available and the company had the

cash to buy them.

I don’t know which way this will go. Forced to guess, I’d say the lack of deals in the last 18

months is as much because majors are scared of making bad deals as because of COVID. And I

think fear of mis-stepping will keep impeding M&A for a time.

Majors will eventually start buying. Mining by its very nature depletes its own assets so miners

simply must buy and build new mines. But I think miners will be more selective. I think they

will be more selective in where they operate, only buying into jurisdictions in which they are

comfortable. I think they will choose projects where access and infrastructures are reasonable,

if not easy. And I think they will limit the number of projects they take on, buying a smaller

number of larger assets.

There are pluses and minuses to this new M&A landscape. On the list of negatives:

Fewer liquidity events means less rotation of capital, which reduces the impact each

investor dollar can have in propelling a bull market

Fewer deals means fewer splashy headlines to attract new investor dollars to the space

For majors to be less active weakens the investment thesis for most junior

explorers/developers, which is to get bought out.

To ease the depression that list created (!), here are the pluses that I see:

The projects that do fit the bill will get bought – and for a pretty penny. When someone

finally bids for Great Bear, I’d betting a bidding war ensues. That’s great for GBR

investors and splashy for outsiders looking in

Mergers will step into the gap. If majors are not going to buy smaller assets, then mid-

tiers will merge to become big together. Mergers don’t carry the same splash but they

can create compelling value when done right.

We definitely do not want majors repeating the huge mistakes they made last cycle!

Dumb, overpriced acquisitions destroyed many billions in shareholder value and turned

many investors away from gold forever. If the sector overcorrects with caution for a

time, so be it. The deals will come; they will just take longer and be more sensible.

5These thoughts have been swirling in my head for some time but crystalized thru a few

conversations at the conference. For the moment, the reality that majors are hesitant to buy is

not great. But the fact that this hesitation stems from wanting – needing – to do better by

shareholders this time around is a good starting point.

It’s not an overall ‘good’ thing for the sector to see fewer takeouts…but if a different approach

to deals both creates a healthier mining sector and encourages some novel thinking in the

junior space, those are arguably good outcomes. In terms of novel thinking, I can imagine

explorers coming to grips with a more realistic baseline for a ‘good’ project. I could see juniors

with neighbouring projects working together to create scale instead of competing in the hopes

of individual success. I can imagine more mergers of small operators to create scale. And I

would expect more juniors with advanced projects to truly push those projects towards

production, not just saying so but actually aiming to build, supported by some of the sector’s

new funding avenues and guided by experienced operators looking for work after being

downsized from the majors.

I hope I’m partly wrong. I hope that COVID was the main reason deals have been so limited

and that, with travel restrictions largely lifted, site visits will happen and takeouts will follow.

But I’m not banking on that outcome. And if I’m onto something here and majors are more

hesitant to buy, then I hope this sector – a space full of creative capital markets minds – will

find new ways to create value for investors. I think it’s possible, as long as executives and

investors alike are open to change.

------------------------------------------------------------------------------------------------------

Portfolio Review Part II

Adventus Mining (TSXV: ADZN, USOCT: ADVZF)

Adventus has not been the most exciting stock since we bought in early April but the story has

only gotten better.

The investment thesis here is that El Domo is a high-grade copper asset that, because of its

location in Ecuador (where permitting can be quick) and management’s drive to get this mine

built, should be in production in early 2023. That’s a very quick timeline given the project has

only a PEA right now! But that’s all about to change.

The feasibility study is due out in six weeks or so. Much of the drilling that happens from PEA

to feasibility is infill so oftentimes resources don’t change all that much. That both is and isn’t

the case here: I expect the resource to grow somewhat (15%?) while of course also adding

confidence (mostly measured and indicated rather than inferred). The grade might also sneak

up a touch.

6The IRR was very strong in the PEA. I doubt it will stay at 57%, but I expect something near

45%. And the larger resource will likely support a higher NPV, likely above US$300 million.

So the feasibility study is on track and looking good, which are important. The feasibility is

required for ADZN to keep the permitting process on track. It’s also important for ADZN to

finalize construction financing.

I say ‘finalize’ because that effort is largely done, as far as I understand. That is unusual, as

companies don’t usually start looking for project financing until the feasibility study is done.

Here, ADZN did an internal pre-feasibility study that was sufficient for some permitting steps

and for a good number of parties interesting in being part of a finance package to come to the

table.

And here’s where things get interesting. ADZN has essentially lined up the dollars for the build

but won’t likely formalize that package until January, once the feasibility study is announced

and filed (which happens a few months later) and another few permitting milestones are

checked off. That creates a window from now until January when potential bidders might well

make a move, to get El Domo before it has a finance package tied to it. And most of the mid-

to large-tier miners interested in El Domo would likely want to arrange their own financing.

OK, so should an offer come in, what might it be? Other deals show valuations at 0.5 to 0.7 of

project NPV. If the NPV is US$330 to $350 million…that translates to $1.50 to $1.70 per share.

ADZN is trading at $0.91 today.

Other Ecuador happenings support the potential for a deal in the near term. One is that peer

INV Metals recently got acquired – and Dundee Precious Metals swooped in when they did

because INV was about to enter into a streaming deal on its Loma Larga project, which Dundee

didn’t want. (Buy the project before financing constraints get applied – sound familiar?)

The new president of Ecuador is also proving himself very pro-mining. A few weeks ago, for

instance, he issued a decree prioritizing support for mining; next he’s expected to pledge

armed forces support for resource projects.

A more mining-supportive president isn’t going to change many minds around Ecuador. But it

likely helps mid-tiers or majors considering the country build confidence.

I am a copper bull. There are very few copper projects that are truly shovel ready. El Domo is,

and so I am keen to own it. I think odds are reasonable that the stock attracts a takeout offer

in the next four months, before Adventus inks a finance package on the asset. If that doesn’t

happen, I think ADZN has the operational capacity and Ecuadorian abilities to build El Domo,

which if successful should lead to a re-rating from developer to producer.

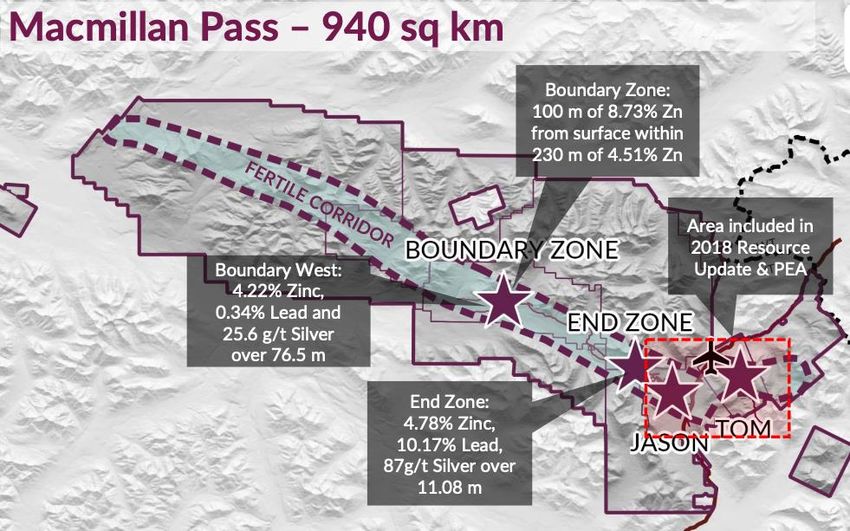

Fireweed Zinc (TSXV: FWZ)

Fireweed is the lone zinc stock in the Maven portfolio. And zinc has been doing just fine lately.

7I will admit I don’t fully understand the drivers. Zinc is not in a shortage. But it also isn’t

oversupplied, it is essential in infrastructure and electrification, and the price gains over the

last year leave the price still in the middle of its 5-year range.

As the above paragraph should illuminate, I don’t own Fireweed because I’m a big zinc bull. I

should note – I bought it in 2017 when zinc was on a tear and I was a big zinc bull. Then zinc

eased, sliding from a high of US$1.65 per lb. in early 2018 to just US$0.82 in the COVID crash.

What matters is that during those two years Fireweed turned Macmillan Pass from a good

project, one with a promising PEA based on a confirmed and slightly expanded high-grade

historic resource, to a project with truly world class potential.

The PEA was based on the high-grade but medium-sized Tom and Jason deposits. And as that

positive mine plan showed, those deposits have the grade, shape, and metallurgy that they

could make sense to mine on their own. The PEA also included the entire cost of upgrading the

road to Mac Pass in mine capital but the government has since taken on part of that $70-

million burden.

Once Fireweed established a positive PEA for Tom and Jason, focus shifted to finding

additional high-value tonnes. If they could find more high-grade mineralization, ideally

somewhere that could be incorporated early in the mine plan, then the mine economics would

strengthen. And there were lots of places to look. The history at Mac Pass involves a land

package that was broken into several pieces and a major that stopped exploring once it found

Tom and Jason. By pulling the land package together and doing proper regional exploration,

Fireweed identified a corridor of land with the structural and stratigraphic (rock type) potential

to host mineralization. Then they hit into the Boundary zone.

8The first hits at Boundary in 2019 were long intercepts of lower-but-still-good-grade

mineralization, like 230 metres of 4.5% zinc from surface. That’s impressive scale. Fireweed

immediately assessed whether a large, lower-grade, open pittable deposit would make mining

sense, including showing that ore sorting could significantly boost the grade and reduce the

volume of rock going to the mill (limiting the need to build a far bigger mill). It was a great

start.

But even those first hits suggested Boundary was more than a large, lower-grade system. The

intercept I listed above included 6.4 metre of 43% zinc, which is obviously the opposite of low

grade.

In 2020 Fireweed showed Boundary’s scale potential but also reimagined the geological setup,

with input from new geophysics. Skipping over the details, today Fireweed is pulling intercepts

from Boundary with strong grades over moderate intervals as part of long intercepts of good

grade.

It’s always hard for the market to understand the value in mixed-metal intercepts from new

zones. But Fireweed will soon make it easier: once this drill season is done the company will

update the Mac Pass resource estimate, incorporating successful step-out holes at Tom and

Jason and counting tonnes at Boundary for the first time.

Remember how I said the PEA established Mac Pass as a good project. Since it came out in

2018, Fireweed has added multiple layers of value, primarily through drilling into expansions

and new discoveries.

You always have to take forward-looking graphics from companies with a grain of salt but I

support the concepts in this one.

9Mac Pass is becoming a Tier 1 zinc asset. Its already good resource will get much bigger and

better with the resource update. Its already ok PEA will also get much bigger and better when

updated. It’s a road-accessible project with ore amenable to cost-saving options like ore

sorting, which all means a Mac Pass mine should be reasonably low cost. And Boundary is by

no means the only target on the property worth testing. In fact, there is a list of targets

offering all kinds of blue sky potential.

Zinc isn’t the story of the moment. Because of that, Fireweed isn’t likely to stand out within

your portfolio. But unlike the gold or copper sectors, where there are ample projects

competing for a few takeout bids from operators, the zinc space is very short on good projects,

let alone Tier 1 assets.

That’s why I think Mac Pass will attract a takeout offer in the next two years. Importantly, the

FWZ team has I think done a great job managing the shareholder registry so that, should a bid

arrive, they should be able to work with shareholders to really maximize value.

Generation Mining (TSXV: GENM)

I’ve discussed Generation Mining a fair bit of late, following project partner Sibanye

Stillwater’s decision to not back in for majority ownership. But I can add to those comments

today after meeting with the Generation team at Beaver Creek.

10The big question for Generation now is how they plan to fund Marathon. They need funding to

get through permitting to an official build decision and then they will need funding to build a

mine. The first requirement is about $50 million. It could be less but Generation wants to

order long lead time items for the build and complete detailed engineering over the next six

months as it awaits a permit.

I say six months…but it’s hard to know when the permit decision will happen. There are

community meetings, and then feedback periods, and then timeframes for the permitting

folks to give their yay-or-nay recommendation to the authorities and then for the federal and

provincial authorities to announce their decisions. This could all happen in six months or it

could take more like 10 months.

What I think matters is that the odds of a green light at, in my opinion, very good. The two

First Nations groups in the area are actively supporting Generation. The adjacent town of

Marathon is vocally advocating the project. And the project got most of the way through

permitting two decades ago without problem.

Generation is also confident permitting is going well, which is why it wants to spend money

now on parts for the mill that will take a long time to make and deliver and on the kind of

detailed engineering that only happens when a mine is actually going to be built. Doing those

things now will speed up to the mine build notably if permits are indeed awarded and

Generation makes an official decision to build.

That’s why GENM needs to access another roughly $50 million in the next while: that plus the

__ it has in the bank will get the company through permitting, with enough to buy those mill

parts and do that engineering work. Something like $20 million of what Generation plans to

spend over the next while will come off mine capex, pulling it down a touch from $665 million.

That brings us back to where we started: how does Generation plan to access $50 million now

and $650 million next year?

The near-term requirement will likely come from a stream or royalty on Marathon. Generation

is accepting offers right now from streaming and royalty companies. I plan to write an article

soon on the evolution of the royalty space but the bottom line is that it is now a highly

competitive business, to an extent that royalty and stream offers can (depending on the

project) make a lot of economic sense.

Marathon looks like a case in point. The chart below is a summary of base case production

from Marathon over its 14.5-year mine life. Look at the revenues from silver and gold.

11Selling a gold or precious metals stream on Marathon could work well. It would not burden the

mine notably, given that gold represents less than 4% of revenue and silver just 1%. Yet

Generation could certainly raise the capital it needs today by selling such a royalty/stream

(details to be determined).

I got the sense Generation is expecting over a dozen offers. That underlines how competitive

the royalty and streaming space is today and, by extension, emphasizes that Generation

should have some nice options from which to choose.

Of course, selling a royalty or stream to fund the last capital needs before construction also

saves Generation from issuing shares at its current valuation, which the team does not want to

do.

OK, so that’s the plan for the near-term cash needs. What about the mine? I don’t have any

deep insight to offer on that, partly because it’s too far out for any to exist, but I do want to

point out that Generation’s chair, Kerry Knoll, has faced almost exactly this challenge before.

Knoll was a founder of Thompson Creek Metals and he led that company when it, as a $100-

million company, needed to raise $600 million to build its first mine. He secured the capital,

built the mine, and Thompson Creek was born.

The past doesn’t guarantee the future but Knoll is a proven entity in the mining space with a

deep network across financiers. And he will be marketing a project grounded in palladium and

copper, the fundamentals for which are strong.

Generation’s share price keeps sliding. I did not think the fallout from Sibanye’s decision would

last this long. It might be that, or it might be the market seeing that Generation needs to raise

money and selling in the hopes of getting in on a financing. Of course, if Generation does ink a

royalty or stream deal then no such financing will happen and most investors connected to the

story know that, but traders will always sell when a company needs cash.

The next while could be a bit boring for GENM. Six to ten months both is and is not a long

time. IT’s short in the grand scheme of permitting…but it’s a bit long for investors waiting for

action.

One option is to sell and re-enter in the first half of next year. The other is to hold through, on

the belief that a good royalty/stream deal will ground a stronger valuation for GENM and its

12asset and that copper and palladium will strengthen more than they will weaken over the next

year.

I am choosing the latter option – to hold – but I can understand that the former is also

appealing.

-------------------------------------------------------------------------------------------------------

Free Trade Date Table

In the middle of each month I publish a table listing all the stocks in the Maven Portfolio that

have financing stock under hold and when those holds end. Based on the difference between

the financing price and the current price, the amount of stock issued in the raise and the daily

trading volume, the type of stock (flow through vs hard), and any other factors that matter

(like if a long-time supporter took a big chunk of the raise or if key news is expected), I rate the

risk each free trade date appears to pose to the stock. Note that these ratings will change

month to month as the story progress and the share price rises or eases.

Red means high risk (strong likelihood the free trade date will lead to a significant share price

decline)

Yellow means moderate (free trade date could have some negative share price impact but not

dramatic)

Green means negligible (free trade date not likely to impact share price)

Amount Financing shares Financing Warrant? Current Free Comment

raised (shares out) price price trade

($M) date

Kuya $9.20 4.8M (40M) $1.90 half $1.63 15-Oct Sign of the

Nevada $4.75 36.5M (131M) $0.13 whole $0.14 16-Oct times: only a

Exploration few of these

Reyna Silver $6 7.2M (93M) $0.83 half $0.72 22-Oct financings are

Edgemont $0.70 2.1M (13M) $0.30 half $0.17 23-Oct in the money

and they only

Fireweed $4.50 5M (63M) $0.90 no $0.73 03-Nov

slightly, so

Zinc

none of these

Pan Global $15.00 25M (153M) $0.60 no $0.67 07-Nov

raises currently

Visionary $3.60 19.8M (51.6M) $0.18 half $0.19 10-Nov

pose a Free

Gold

Trade Date risk

Blue Lagoon $8.10 13M (70M) $0.55 half $0.53 15-Nov

Banyan Gold $16 44M (181M) $0.28 no $0.29 19-Nov

Gold Basin $5.40 15.4M (74M) $0.35 half $0.38 23-Dec

Riley Gold $2.60 6.5M (26M) $0.40 half $0.38 23-Dec

13---------------------------------------------------------------------------------------------------------

Full Portfolio Table

Buys remain focused on uranium: Uranium Energy and IsoEnergy as bolded in the table,

NexGen that I own in my low risk portfolio, and Val Ore, Denison, and Fission, which I am

adding.

Entry Entry % Price

Company Ticker Cost base Change

Date price position today

Mine Developers

NEE.V,

18-Feb-20 $0.75 100 $0.30 -60%

Northern NHVCF.OTC

Vertex Strong Nevada exploration team merged with Northern Vertex to bring exploration prowess

to underexplored Moss mine. Move took market by surprise but it does make sense

ORE.V,

13-Jun-18 $0.81 100 $1.25 54%

Orezone ORZCF.OTC

Gold Under construction gold project with scale and strong economics, and a team that has

successfully built many mines. Value gains ahead whether ORE builds or gets bought

Telson --> ATLY.V 24-Feb-21 $0.30 100 $0.51 70%

Altaley New finance package and people will allow ATLY (which market had written off bcs of debts)

Mining to finish building gold mine, turn zinc mine around, and make $. Should re-rate significantly.

UEC.NYSE 21-Jun-15 $1.72 100 $3.69 115%

Uranium

Energy * Ready to ramp up low-cost output into developing uranium bull market that will likely

offer a premium for US output. One of few clear bets for uranium

Feasibility-Stage Projects

ERD.T, $0.36 (add @ $0.24,

08-Jan-17 $0.86 200 $0.40 11%

Erdene ERDCF.OCT COVID)

Resources Advancing dual tracks: develop BK mine and keep exploring. Exploration keeps returning new

high-grade zones. Re-rating ahead once ERD can start buildling (COVID delayed)

Advanced Assets (PEA or Pre-feasibility)

ADZN.V,

07-Apr-21 $1.00 100 $0.90 -10%

ADVZF.OCT

Adventus

Pushing El Domo deposit into production ASAP so that this high grade, open pit copper

Mining

project can feed the copper bull market. Also exploration upside around El Domo and at two

other projects (Piliji and Santiago). Lots of cash.

-$0.57 (sold half $1.67;

FWZ.V 01-Jun-17 $0.80 25 $0.82

COVID)

Fireweed

Mac Pass is a standout zinc project. 2020 drilling returned long intercepts from Boundary

Zinc

zone, which is now dramatically increasing the scale of any Mac Pass mine. 2021 will see

Boundary fleshed out (good odds of major resource boost plus testing new targets)

14GENM.V 20-Nov-19 $0.19 $0.10 50 $0.71 610%

Generation

Mining Unique PGM + Cu asset: large resource in great location with grade and scale upside.

Feasibility returned robust numbers. Permitting decision Q2 2022; high likelihood.

GSHR.V 04-Jun-21 $0.80 100 $0.69 -14%

Goldshore New gold explorer/developer advancing Moss project in Ontario. 2.4M oz at 1 g/t but major

Resources expansion potential (below, along strike) and chance of boosting grade (high grade never

modeled). Insanely strong team

ITR.V;

06-Nov-17 $0.90 $2.58 (COVID; rollback) 100 $3.18 23%

Integra ITGR.NYSE

Resources PEA outlined good, large mine already. Favoured jurisdiction, strong treasury, exploring for

high grade, updating PEA with much bigger mine plan

KUYA.C 08-Oct-20 $1.42 33 $1.34 -6%

Kuya Silver Pushing the Bethania mine in Peru back into production, with plans to expand. Low cost,

near term silver producer; strong team; tight stock. Also exploring similar geology in Ontario

MAU.T 27-Jan-21 $0.97 100 $0.67 -31%

Montage

3M oz open pit deposit in Cote d'Ivoire being advanced rapidly to development by high

Gold

caliber team. New deal, undervalued, catalyst rich 2021.

NCAU.V 27-May-20 $0.36 $0.61 (tranches) 100 $0.55 -10%

Newcore Advancing the PEA-level Enchi gold project in Ghana: resource growth, testing new targets,

Gold updating economics and mine plan. Neglected asset getting focused attention for first time.

Top tier management.

RVG.V,

30-Oct-19 $0.51 100 $0.73 43%

Revival RVLGF.OTC

Gold Strong team advancing historic asset to production in Idaho. Drilling for scale and for high-

grade UG potential

RKR.V 29-Dec-20 $0.45 100 $0.43 -4%

Rokmaster

2M oz resource in BC. High grade, growing, and metallurgical issues now addressed. Market

Resources

hesitant on balloon payment but drilling is dramatically expanding the resource

TLG.T;

19-Jun-19 $0.69 $0.765 (COVDI) 100 $0.81 6%

Troilus CHXMF.OTC

Gold Large open pittable gold resource at historic mine. PEA captured value; pending PFS will be

much better (scale, strip). Also testing regionally for additional discoveries.

GSVR.V,

17-Dec-20 $0.28 100 $0.40 45%

GSVRF.OCT

Vangold -->

Restarting El Cubo mill to process ore from El Cubo mine (previous operators focused on

Guanajuato

scale; lots of resource remains for smaller, more selective mining) and later from old El

Silver

Pinguico mine next door, which has stockpiled ore on surface and in mine, plus clear

exploration potential.

Exploration

BYN.V 17-Dec-20 $0.25 100 $0.29 16%

Banyan 1M oz resource growing steadily at AurMac, a road-accessible project between two

Gold operating mines in Yukon. Inexpensive entry on expectation this team will double this open

pittable resource by 2022.

15BLLG.CSE;

17-Dec-20 $0.69 100 $0.53 -23%

BLAGF.OTC

Blue

Producing on small scale because of previous operator's work and focus, to fund exploration

Lagoon

for more high-grade mineralization on multiple veins on very underexplored, road accessible

project in BC.

EDGM.CSE 20-Jan-21 $0.25 100 $0.16 -36%

Edgemont Exploring the Dungate project in central BC for a porphyry. Two good targets (via one historic

Gold hole with no assays but promising drill logs, geophysics, sampling, soils) on property that's

road accessible, workable year round, gentle terrain. Low market cap at entry

GGL.V 08-Oct-20 $0.18 100 $0.14 -25%

GGL Getting set to start drilling the high-grade oxide gold zone at Gold Point in Nevada.

Resources Opportunity to extend known high-grade shoots, explore around old stopes,and test other

veins/areas. Strong technical team, tight share structure.

GXX.CSE 07-Apr-21 $0.33 100 $0.38 14%

Gold Basin Under the radar company drilling with Gold Basin project in Arizona to confirm JORC

Resources resource and grow it. Good odds to define at least 1M at surface oxide gold ounces in short

order.

GBR.V, $0.48 (sold half to $0,

11-Dec-17 $0.29 50 $13.53 2719%

Great Bear GTBAF.OCT COVID)

Resources GBR doing 300-hole program to define first resource at LP Fault as fast as possible. 10M oz. is

likely. Race to resource before getting taken out

HWG.V 08-Jun-21 $0.45 100 $0.25 -44%

Headwater

Searching for high-grade gold thru focus on LSE gold systems in western US. Portfolio

Gold

approach. Strong team, newly trading

HSTR.V 30-Jul-20 $0.09 $1.35 (rollback) 100 $0.77 -43%

Unga project in Alaska has four strong targets (high-grade vein with expansion potential,

Heliostar high-grade structure ignored for 40 years because bad drilling gave bad results, drill-tested

Metals high-grade beneath old gold mine left behind bcs polymetallic, and flat-lying surface oxide

gold zone). New management advancing with focus & funding; also brought in 3 promising

Mexican projects

HIGH.V; Spinout or

$0.45 $0.41 (COVID) 100 $1.34 227%

HGGOF.OTC $0.45

HighGold

JT has high-grade deposit open for expansion (now that HIGH has figured it out) plus multiple

Mining

related targets never before tested. Market wasn't excited about 2020 results after splash of

2019 but much improved geologic model means 2021 program has strong potential

ISO.V,

12-Dec-18 $0.40 $0.44 (COVID) 100 $6.55 1389%

ISENF.OTC

IsoEnergy

* Only junior with a high grade U discovery as uranium bull market gathers momentum.

Winter drill program cancelled because of COVID restrictions. Summer drilling should start

soon, leading to maiden resource

KDK.V 18-Dec-19 $0.35 $0 50 $1.44

Kodiak Major gold-copper porphyry discovery in second drill program at MPD. Follow-up drilling

Copper started in March aimed at expanding high-grade core south and testing other very similar

targets on property.

16LBC.V,

26-May-21 $0.60 100 $0.40 -33%

Libero LBCMF.OTC

Copper & Copper explorer will drill test a porphyry in BC discovered late last year and a porphyry in

Gold Argentina discovered in 2018 but never followed up. Two good kicks at copper porphyry

discovery. Also permitting to drill a sizeable porphyry is Colombia with clear room to grow.

NGE.V,

11-Oct-17 $0.33 $0.30 (COVID) 100 $0.15 -50%

Nevada NVDEF.OTC

Exploration Stalking big gold under cover in Nevada. Have found what looks like a massive system; need

to find the hot spot therein. Drilling now underway

NRG.V 21-Apr-21 $0.13 100 $0.12 -8%

Newrange New approach and IP data outlined 3 new targets at Pamlico that are not hard-to-find veins

Gold (oxide gold at surface, skarn area, and intrusion-related gold). All three will see drilling, as

will the new North Birth project in Ontatio that offers good evidence for iron formation gold.

AGX.V 08-Oct-20 $0.80 100 $0.41 -49%

Oro X -->

now Silver

Merged with Latitude Silver to become Silver X, focused on Nueva Recuperada mine in Peru.

X

Operating zinc-silver mine with exploration upside and expansion potential. Corporate goal:

add more silver assets. Paul Matysek involved.

OSI.V 13-Apr-20 $0.69 -$0.03 50 $1.11

Osino

Gold discovery in Namibia under till. Strong team has rapidly delineated large open-pittable

Resources

deposit of good grade. Good PEA, pushing to production, and exploration keeps expanding.

OCG.V,

12-Feb-20 $0.11 0 75 $0.20 100%

MRDDF.OTC

Outcrop

Hammering the vein system at Santa Ana with holes; great success thus far hitting repeating

high-grade shoots along 14 km vein extent.

PGZ.V,

18-Feb-21 $0.48 100 $0.65 35%

PGNRF.OTC

Pan Global

Resources advancing a strong and potentially large VMS discovery at the Escacena project in Spain. Lots

of room to grow, multiple similar untested targets ( VMS's occur in clusters), and surrounded

by operating mines. Standout copper explorer

RSLV.V 23-Sep-20 $1.05 100 $0.72 -31%

Reyna

Silver Top tier technical and markets team with portfolio of Mexican silver assets. Two projects will

be drilled 2021; potential for big success

RDG.V 17-Aug-20 $0.55 100 $0.52 -5%

Ridgeline New company with three high potential Nevada gold projects. Selena developing into

Minerals significant surface oxide silver-gold zone; Swift and Carlin East are deep, high-grade targets.

Well funded, strong backers, tight structure, cheap drill contract

RLYG.V 09-Jun-21 $0.45 100 $0.38 -16%

Riley Gold First results from Tokop project in Nevada pending. Granite-hosted gold offers potential for

both high-grade and disseminated gold (via sheeted veins), over significant scale

SASY.C 08-Oct-20 $1.08 100 $0.49 -55%

Sassy

Resources Foremore project in BC has multiple strong targets. New Newfoundland land position gives

exposure to another hot district.

17SLVR.V,

29-Dec-20 $0.51 100 $0.47 -8%

SLVTF.OTC

Silver Tiger Serially successful team in finding / developing deposits in Mexico. El Tigre mine was rich;

remnant halo hosts 1M leachable gold eq. ounces. This will grow and PEA pending. Splash

from exploring the rest of the vein system. 5 rigs turning, strong shareholder group

TRG.V 08-Oct-20 $0.40 100 $0.22 -45%

Tarachi

Gold Mexico gold-silver explorer bought the Magistral tailings and process plant - path to near

term production, to create cash flow. Also exploring series of early-stge proejcts

VIZ.V 20-Jan-21 $0.18 25 $0.17 -6%

Visionary Well structured company diving into gold potential of Wyoming, which is littered with

Gold historic gold mines but has been ignored by modern explorers. Dipped a toe into this stock

for its potential to become much bigger

VZLA.V 09-Oct-19 $0.41 100 $2.63 541%

Vizsla

Resources Exciting high-grade silver discovery underway at Panuco project in Mexico. Multiple veins to

test. Strong team, cashed up, momentum, 8 drills means constant news.

Royalty Companies

EMPR.V;

30-Dec-20 $0.54 0.13 66 $0.38 188%

Empress EMPYF.OTC

Royalty New royalty co with strategy focused on buying new royalties, in deals engineered by three

strategic partners. Impressive management.

EMX.V,

14-Nov-14 $0.86 $0.98 100 $3.52 259%

NYSE

EMX

Royalty Portfolio of royalties and strategic investors developed from years of project generation and

strategic purchases. Q3 2021 saw two major deals that should vault EMX into the royalty big

leagues over the next year. Tight shareholder registry helps.

Portfolio Updates

EMX Royalty (TSXV: EMX; NYSE-A: EMX)

Per the terms of their recently closed royalty acquisition on the Caserones mine, EMX will soon

receive a royalty payment for the mine’s Q2 production. The US$974,000 payment reflects the

0.418% NSR EMX bought on the mine in a partnership with Altus Strategies, which owns a twin

0.418% royalty.

The clear benefit of buying a producing royalty is that it immediately starts paying! The biggest

pushback on EMX’s deals of late has been the somewhat expensive debt it took from Sprott

Resource Lending. I talked with Dave Cole of EMX about that at Beaver Creek and he

confirmed what I expected: it’s hard for a company that does not yet turn a profit to convince

conventional lenders to trust them with $40 million! Sprott Resource Lending, by contrast,

18knows the mining business and EMX very well, and so was able to provide the needed debt in

short order.

Getting the debt to buy the two producing royalties is one thing. Paying it back is another –

and the EMX investment bet today is believing that EMX will pay back a good chunk of the

debt in the next 12 months and will renegotiate the rest into a low-interest facility with a

mainstream bank, as such facilities will become available to the company over the next year as

revenues from these two new producing royalties pay out significant sums. This is the first

such payment.

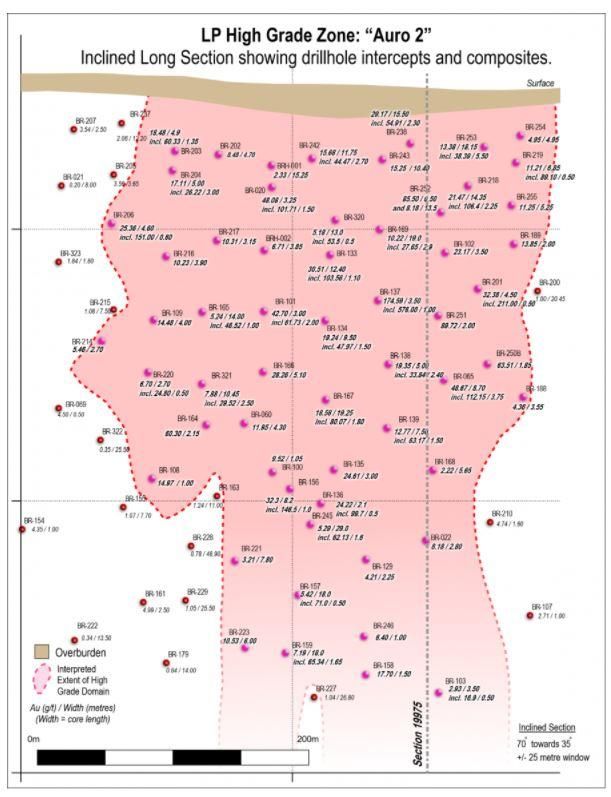

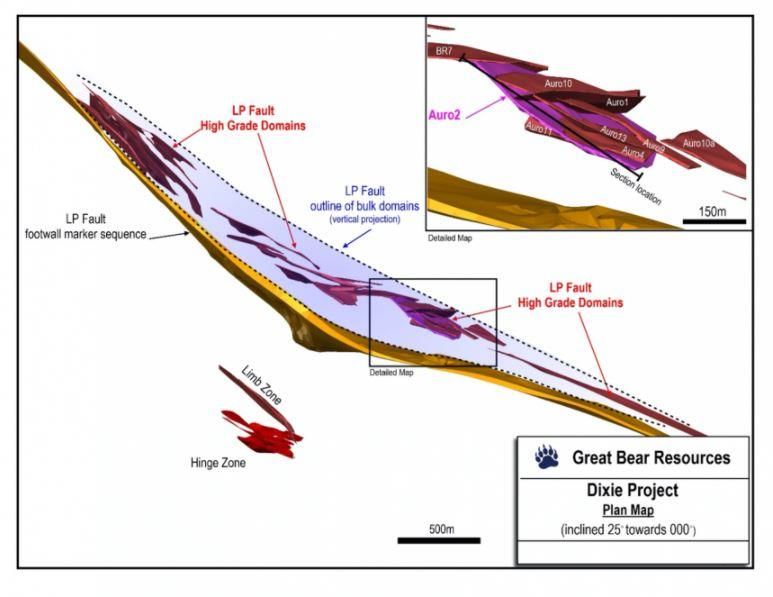

Great Bear Resources (TSXV: GBR; USOTC: GTBAF)

Great Bear’s “news” this week wasn’t news so much as all the information you could ever

need about the Auro2 high grade domain, with all the intercepts that have cut the domain, a

plan map, and a long section that gives a good sense of the scale.

The plan map shows location within LP Fault and proximity to, and size relative to, other

nearby domains.

19Auro2 is one of the larger high-grade domains. It’s hard to tell relative sizes though because

they all sit at slightly different angles, so the plan map sees each one from a different angle.

The long section of the domain gives a good sense of density of drilling and consistency of

results. It underscores that this high-grade domain extends with good consistency from

bedrock surface to 450 metres depth, where it remains open.

GBR will keep issuing releases like this over the next few months while it nears an initial

resource estimate. I think that estimate will contain at least 7 million ounces in high-grade LP

Fault domains that can be mined by an open pit. I think the overall project will have several

million ounces more from low-grade areas, from Limb and Hinge, and from deeper ounces

sitting below a pit outline. The actual numbers could well be higher than what I just noted, but

I’d rather be conservative.

For Dixie to be a truly stand-out gold asset it needs to be able to produce 500,000 oz. a year

for at least a decade. That’s a high bar, but that’s why projects that meet such a bar are truly

20Tier One assets. I think Dixie will meet that bar with its initial resource estimate and its first

PEA, which will follow shortly after the resource.

A resource estimate and PEA with that gravitas will, I think, attract offers for GBR. And the

resource is only three, maybe four, months away. GBR hasn’t had a lot of trading over the

summer but I would think buying will ramp up as the resource estimate nears and funds want

to get in ahead of any offers.

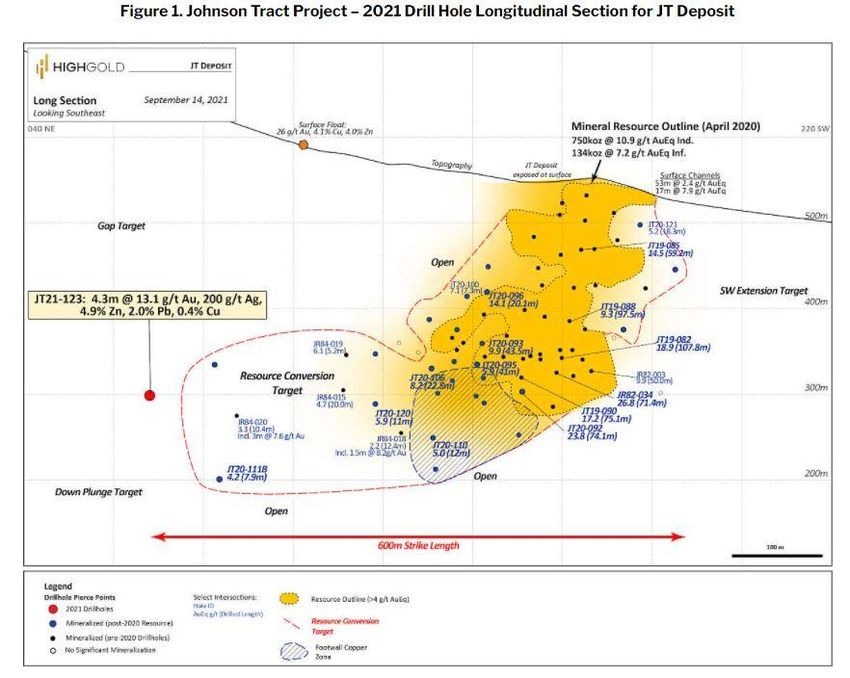

HighGold Mining (TSXV: HIGH; USOTC: HGGOF)

The initial hole from HIGH’s 20,000-metre drill program at Johnson Tract has produced a nice

hit that extends known mineralization by 100 metres along strike. Hole 123 cut 4.3 metres of

13.1 g/t gold, 200 g/t silver, 4.9% zinc, 2.0% lead, and 0.4% copper. In doing so, it extended the

strike length of the JT deposit to 600 metres.

The good grades and the strike extension this hole delivered bode well for the resource update

HIGH will do at the end of this season. But the intercept also came from mudstones, rather

21than the dacite lapel tuff that hosts the majority of the JT deposit. Mudstone-hosted

mineralization is not new at the project – HIGH pulled some great VMS-style hits in mudstone

last year 600 meters to the northeast – but finding strong VMS-style, mudstone-hosted

mineralization right beside JT opens up the scale potential of that deposit (i.e. the resource is

not limited to the tuff) and underlines the overall mineral endowment of the area, with many

kinds of rocks carrying strong mineralization of different kinds.

Bottom line: this is a great first hit for HIGH. It’s in different rocks, which underlines the

potential for the main JT deposit to keep growing across rock type boundaries. It is rich in gold,

which the VMS-style mineralization that HIGH hit last season was not. It extended the strike to

600 metres, which means the updated JT resource will undoubtedly best 1 million gold

equivalent ounces already and 2021 drill results have only just begun. And it amplified the

potential to extend the resource upwards, from the area marked as “Resource Conversion

Target” (where HIGH hit good mineralization but needs more holes for it to count in a

resource) towards the surface where there’s a boulder grading 26 g/t gold, 4.1% copper, and

4% zinc (and as CEO Darwin Green noted in our last conversation: “Boulders don’t roll uphill.”)

It’s too bad labs are again so darn slow, but they delivered a zinger for the first hole of HIGH’s

2021 season.

Integra Resources (TSXV: ITR; NYSE-A: ITRG)

ITR is filling up its coffers with a US$15-million bought-deal financing that will issue 5.9 million

shares priced at US$2.55 per share. The offering also includes an 885,000-share over-

allotment option.

No one likes raising money at a 52-week low share price, but what’s worse is letting

momentum wane on a good project in what is a good market, albeit with annoyingly long

strong ebbs and flows, for lack of capital. And so ITR is raising.

I did try to secure an allocation for Maven Premium subscribers but was unable. Bought deal

financings are not my favourite. The advantage for the company is that the bank (or syndicate

– group – of investment banks) leading the deal takes on responsibility to fill the book. They

also manage the actual raise, dealing with all the paperwork and similar, which is a load off for

the issuer.

The downside is that the company has little control over who gets into the deal. Of course,

companies only work with banks they know and trust, so it’s not a matter of getting lousy

investors. It is a matter, though, of not being able to secure allocations for smaller retail

investors. There simply isn’t a mechanism. The bank running the book, in this case Raymond

James, will take orders from its clients preferentially and so any outside orders get squeezed

out.

22It’s really strange that the company issuing the shares has almost no control over who buys

those shares, but that’s how it goes in a bought deal raise. I would love to see companies

doing bought deals run small non-brokered raises alongside, specifically to accommodate

engaged retail investors, but so far that isn’t the case here. I get that bought deals have lots of

advantages for issuers…but they have no advantages for me or my Premium investors.

Sassy Resources (CSE: SASY; USOTC: SSYRF)

Drilling on the Foremore project’s Westmore target continues as does surface work to validate

anomalies identified elsewhere on Foremore.

We bought Sassy as a bet on the discovery potential at Westmore. As they are drilling there

now, we’ll see what happens. Of course, slow labs mean we have to keep waiting for drill

results.

Since we bought Sassy for its BC Westmore, the company also established an entire

Newfoundland portfolio, which will be spun out as Gander Gold in the near term. Gander will

not drill this summer; they are doing the groundwork to establish drill targets. But given all the

excitement in Newfoundland right now, I will hold at least until I get Gander shares in my

hands. And while we wait for that, we will get results from Westmore, which will give a better

idea of how that opportunity is shaping up.

-----------------------------------------------------------------------------------------------------

EDITORIAL POLICY AND COPYRIGHT: Companies are selected based solely on merit; fees are not paid. This

document is protected by copyright laws and may not be reproduced in any form for other than personal use without prior

written consent from the publisher.

DISCLAIMER: The information in this publication is not intended to be, nor shall constitute, an offer to sell or solicit any

offer to buy any security. The information presented on this website is subject to change without notice, and neither

Resource Maven (Maven) nor its affiliates assume any responsibility to update this information. Maven is not registered as

a securities broker-dealer or an investment adviser in any jurisdiction. Additionally, it is not intended to be a complete

description of the securities, markets, or developments referred to in the material. Maven cannot and does not assess,

verify or guarantee the adequacy, accuracy or completeness of any information, the suitability or profitability of any

particular investment, or the potential value of any investment or informational source. Additionally, Maven in no way

warrants the solvency, financial condition, or investment advisability of any of the securities mentioned. Furthermore,

Maven accepts no liability whatsoever for any direct or consequential loss arising from any use of our product, website, or

other content. The reader bears responsibility for his/her own investment research and decisions and should seek the

advice of a qualified investment advisor and investigate and fully understand any and all risks before investing.

Information and statistical data contained in this website were obtained or derived from sources believed to be reliable.

However, Maven does not represent that any such information, opinion or statistical data is accurate or complete and

should not be relied upon as such. This publication may provide addresses of, or contain hyperlinks to, Internet websites.

Maven has not reviewed the Internet website of any third party and takes no responsibility for the contents thereof. Each

such address or hyperlink is provided solely for the convenience and information of this website's users, and the content

of linked third-party websites is not in any way incorporated into this website. Those who choose to access such third-

party websites or follow such hyperlinks do so at their own risk. The publisher, owner, writer or their affiliates may own

securities of or may have participated in the financings of some or all of the companies mentioned in this publication.

2324

You can also read