The Stafford Diaries The world ground to a halt: COVID-19 impact on the aviation industry Issue No.33 - Stafford Capital Partners

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Stafford

Diaries

The world ground to a halt:

COVID-19 impact on the

aviation industry

Issue No.33

January 2021 www.staffordcp.com

Authors: William Greene, David Lindsay, and Daniel Pye 2

www.staffordcp.com

Contents

1. Executive summary 4

Stafford Infrastructure 4

2. Not all airports and airlines are equal 6

Heathrow case study: how airports breakeven and make a profit 8

3. COVID-19 impact 10

4. Risk assessment 13

Revenue Risk 13

Counterparty Risk 14

Financing Risk 15

Technology Risk 16

ESG Risk 16

5. Concluding remarks 19

6. References 20

7. Contacts 22

3

1. Executive summary

COVID-19 has considerably impacted various industries and asset classes, including infrastructure. Ongoing

disruptions have hindered key supply-chains needed to advance large-scale construction projects to

completion, challenged revenues and demand, and ultimately instigated substantial changes to our everyday

lives. Infrastructure facilitates the connectivity of people and fosters the movement and accessibility of

goods, services, energy, and information. The physical aspect of this connection has been interrupted and

the transportation sector has been one of the worst affected. This has particularly impacted airports and the

aviation industry at large.

Although airports constitute a limited part of Stafford’s investment universe (less than 3% of the combined Q3

2020 NAV across all Infrastructure products), they have incurred a disproportionate impact from COVID-19. In

addition, as we continue to explore new deal opportunities, we have identified a number of underlying funds that

contain airport exposure within their portfolios. As such, we have updated our sector research on the topic.

As a prelude to what will be explored in further detail, this diary provides an overview of the types of airports and

airlines in operation, the revenue mechanisms of airports, how COVID-19 has impacted the industry, the key risks

underpinning the sector and an associated assessment, and finally an overall outlook for airports both throughout

COVID-19 and the world thereafter.

Ultimately, for airports to both rebound from the pandemic and prosper in the new normal, they will need to

question their traditional approach in serving their customers. With passenger volumes at record lows and the

future ambiguous, operational, and financial considerations are understandably key priorities for airport operators.

The prudent application of Stafford Infrastructure’s risk assessment framework dives into the most relevant

elements as COVID-19 continues to disrupt global markets. It also aids us in formulating a clearer understanding

of how rapidly changing sector and economic trends will mould the flight path of the aviation industry for years

to come. It is undeniable that the experience of COVID will imprint a lasting impact on the airport sector, but very

different depending on underlying airport characteristics: this is what we will try to understand here. Thus, any

potential airport investment we engage in must encapsulate specific characteristics we identify below to ensure a

smooth take-off.

Stafford Infrastructure

Stafford Infrastructure is a specialist investor in low risk, developed market infrastructure fund secondary

transactions that has been investing in infrastructure secondaries since 2012 and today manages more than

USD 1 billion via four infrastructure funds. It has invested over USD 700 million on behalf of its clients in 47

secondary and co-investment transactions, achieving target returns of 8-9% net and >5% yield from highly

core assets.

Stafford has made a significant commitment to its infrastructure secondaries strategy, growing its

investment team along with the growth of its assets under management. Today our 12-member team is

located in key financial markets and has an average 15 years investing experience in fields including

infrastructure asset investment, engineering, tax, and investment management.

Stafford’s infrastructure strategy was designed in 2010-2012 and is strongly influenced by the lessons learnt

from the GFC. The strategy today remains unchanged, with a focus on diversified, low risk, and high yield

assets. As such, our investment process has always relied as its starting point on a detailed proprietary

analysis of approximately 1,400 infrastructure funds and over 5,000 fund assets using a 9-factor risk model.

The approach assesses risk at the underlying asset level which is then used to determine aggregate risk at

the relevant fund level, and finally on a consolidated level for our specific infrastructure products, producing

the corresponding discounted cash flow (“DCF”) rates.

This risk assessment methodology is key in identifying a realistic assessment of the core-rating of a

target fund’s portfolio to assist in pricing, for which we consider an overall risk rating of 10% or less to

be core. In addition to investment purposes, the weighted funds discount factors are utilised for portfolio

monitoring. As we continually monitor the overall risk profile of our infrastructure portfolios and the

contribution that potential investments would make to them, we are able to absorb good transactions

with a higher risk profile, if that risk is appropriately remunerated. The same approach is taken when

considering sector exposure. This is particularly relevant amidst the relative ambiguity underpinning the

current market environment.

4

www.staffordcp.com

Figure 1 – Stafford Risk Model

Source: Stafford Capital Partners

In the context of airports, we have analysed 85 individual assets across 68 unique underlying funds and 28

countries (primarily OECD), generating an average DCF of 11.5% as of December 2019. We have revisited this

analysis and adjusted the relevant risk factors as airports globally experience slashed revenues, counterparty

concerns, postponed capex plans, financing and liquidity pressures, and fresh ESG requirements emanating from

COVID-19, identifying an average DCF of 13.0% as of September 2020, reflecting a significant 1.5% increase in

risk (independent of asset write-downs).

We hope you enjoy this latest edition of Stafford Diaries on infrastructure and welcome your comments. We look

forward to the opportunity to discuss these matters with you further.

5

2. Not all airports and airlines are equal Before we analyse the details of how COVID-19 has impacted the industry, it is important to recognise that both airports and airlines come in many shapes and forms. Firstly, there are key airport typesi: ◼ Commercial Service: publicly owned airports that have at least 2,500 passenger boardings each calendar year and receive scheduled passenger services. This is further split into Primary, with more than 10,000 passenger boardings per year, and Nonprimary Commercial Service, with at least 2,500 and no more than 10,000 passenger boardings each year. ◼ Cargo Service: airports that, in addition to any other air transportation services that may be available, are served by aircraft providing air transportation of solely cargo with a total annual landed weight of more than 100 million pounds. Cargo includes items such as perishable goods, non-perishable goods, live animals, and dangerous goods. ◼ General Aviation: public airports with less than 2,500 or more passengers annually or else do not have regularly scheduled services. They are typically niche and narrow focused airports that include national airports (provide communities access to both national as well as international markets), regional airports (interstate trade), local airports (intrastate trade), and basic airports (linking communities to the national airport system). To add to the complexity, there are three key categories of airlines. As is the case with most businesses, there is a stratification element at work. Based on revenue generated, we can classify airlines as followsii: ◼ Major: these are the industry heavyweights that achieve more than USD 1 billion in revenue per annum. Habitually, major airlines are also the largest employers among airlines. ◼ National: scheduled airlines with annual operating revenues between USD 100 million and USD 1 billion. These airlines might serve specific regions of a country but may also provide long-distance routes and some international destinations. They operate medium-and large-sized jets and have less employees than the major airlines. ◼ Regional: service particular regions of a country, filling the niche markets that the major and national airlines may overlook. This is the fastest growing segment of the airline industry and it can be divided into three subgroups of large, medium, and small regionals. Airports are effectively two-sided businesses, engaging in a commercial relationship with both airlines and passengers. They receive their revenues from two chief sourcesiii: 1) Aeronautical activities: terminal, landing, and passenger charges, noise and environmental fees, security charges, parking charges, boarding bridge charges, transfer/transit charges, and maintenance rental charges. 2) Non-aeronautical activities: fuel supply for aircraft, car parking, retail, catering, business lounges, taxi, hotel booking services, banks and currency exchange offices, game zones, advertising and sponsorship, office rentals, crew room rentals, and recharges for utilities. Typically, the larger the airport the greater the commercial footprint as well as diversification and specialisation of non-aeronautical activities. Concessions for retail sales tend to account for the largest portion of non-aeronautical revenue globally, although in the Middle East parking revenues take the top spot. Furthermore, the contribution of the two chief revenue sources tends to vary across jurisdictions. For example, commercial activities account for as much as 50% of revenues at some Asia-Pacific airports whereas this is only 32% in African airportsiv. In contrast, many smaller airports are owned by the government and charge much lower fees to entice airlines. For example, an airport that has less than 1 million passengers per year generates substantially less profit per passenger than international airports such as Heathrow. Even though there is a plethora of cargo flights and cargo airports, the greatest proportion of revenue for airports is derived from passengers on commercial flights. As illustrated below, several characteristics are key when analysing the volatility of airport revenue, profitability, and the capacity for revenue restoration alongside the sensitivity to COVID-19. 6

www.staffordcp.com

Figure 2 – Airport framework and COVID-19 considerations

Characteristic COVID-19 Sensitivity Favourable Attributes

Size/Type Smaller scale primary commercial service airports with lower overheads and ability to

cope with reduced traffic loads (e.g. Cork Airport, Lyon Saint-Exupéry Airport) + larger

capacity airports with ample liquidity and minimal finance risks to sustain ongoing

revenue losses (e.g. Amsterdam Schiphol, Aeroporti di Roma)

Geography/ Primary commercial service airports servicing continental markets with large domestic

Destination economies (such as China, USA, and Australia) or regions with strong leisure tourism

demand (such as within the European Union), e.g. Beijing Capital International Airport,

Los Angeles International Airport

Operational Strategy Commercial and cargo service airports which exhibit the ability to protect cash flow,

minimise capex/opex, improve margins, and use space intelligently, e.g. Hong Kong

International Airport, Miami Airport

Service Offering Cargo service airports and commercial airports that have mitigated lost revenue with

cargo as well as regional airports that handle significant interstate trade, e.g. Brussels

Airport, Hartsfield-Jackson Atlanta International Airport

Airline Types Protected flag carriers and/or low-cost carriers with a robust short haul network

(focused on the leisure market) boosted by government support and that do not have

credit concerns or liquidity/solvency problems, e.g. Air Canada, Wizz Air

Health Measures Airports with enhancements to facilitate social distancing, safe transit, and a clean

environment + those implementing technological upgrades to boost health and

sanitisation measures, e.g. Torino Airport, Malta International Airport

Stakeholder Airports engaged with government, tourism, and airline bodies + those which service

Cooperation countries and regions with travel corridors and bubbles in place, e.g. Singapore Changi

Airport

Digitisation Digital integration of operations and cashless capability across the premises, e.g. Lisbon

Airport, Istanbul Airport

Data Sharing Coordination with aeronautical teams, specialists & concessionaries, e.g. Copenhagen

Airport

Climate Change Acceleration of ESG initiatives, emission reduction measures, test innovations, e.g.

Hamburg Airport, Budapest Airport

The elements underpinning this framework are explored further in the diary, particularly as we delve into the

specific risks (and associated opportunities) currently affiliated with the sector. As identified above, our investment

focus is mostly concentrated on primary commercial service airports and airports which are either chiefly cargo

focused or that have the facilities to manage significant cargo.

7

Heathrow case study: how airports breakeven and make a profit

Heathrow is the busiest privately owned airport in the world. Before COVID-19 it served over 650 flights

daily, equating to around 80 million passengers flying through the facility each year. It costs approximately

USD 1.5 billion per annum to operate the airport and to break even Heathrow needs to generate around

USD 19 per passenger (combining both aeronautical and non-aeronautical revenue). The airport collects

a cut of every sale registered by the various retailers engaging in commercial activity on its territory,

generating USD 13 on averagev. This does not incorporate property and other regulated charges, which

when added, provides an extra USD 5.

Figure 3 – Heathrow Airport retail revenue split

Source: Simple Flying (2018)

Figure 4 – Heathrow Airport vs other airports (2019 non-aeronautical revenue per

passenger)

Source: 2019 annual reports for selected airports

8

www.staffordcp.com

It should be highlighted that Heathrow produces one of the highest retail revenues per passenger globally.

Heathrow’s many duty free and specialist shops, digital capabilities for advanced purchases of boutique

items, and currency exchange usage (given it is a key international transport hub) aid its superiority in the

retail revenue category vi. It effectively offers consumers a mesh of pure travel and shopping experiences.

The residual balance required to break even, and contribute to profits, is derived from flights – the greatest

revenue source. Each occasion a plane lands or takes off from the airport, Heathrow receives an average of

USD 9,500 for each landing plane (price varies depending on the plane size) and an average of around USD

50 per passenger (contingent upon passenger volume and the specific destination). On average the airport

will generate approximately USD 29 from the ticket of each passenger v. When added to the retail value and

additional non-aeronautical revenue sources the balance then exceeds the break-even threshold.

9

3. COVID-19 impact After a year of robust growth in 2019, the world’s airport industry was bracing for a strong 2020, with projected revenue of USD 172 billion with Europe at USD 59 billion, Asia-Pacific at USD 50 billion, and North America at USD 35 millionvii – then COVID-19 emerged. The International Civil Aviation Organization (“ICAO”) prepared an economic impact analysis of the impact of COVID-19 on civil aviation in November 2020, predicting an approximate 60% reduction in global passenger traffic compared to 2019, translating to an overall decrease of between 2,877 to 2,888 million passengers. This has culminated in a revenue shortfall of USD 105 billion for airports in 2020 in comparison to prior year figures. Moreover, HY1 2021 is slated to continue the perilous trend, with a forecast reduction in global passengers of around 1bnviii. To illustrate the severity and unequal impact of the crisis with some examples, Singapore has transitioned from being the 7th busiest airport in the world to 58th this year, with just 1.5% of its usual volume. In 2019 it handled 68 million passengers alone. Heathrow, which handled a record 81 million passengers in 2019, has faced a more than an 80% drop in volume. Similar passenger volume drops were reported at Frankfurt am Main Airport and Charles de Gaulle Airport in September. Sydney Airport, which had on average almost 2 million outbound passengers per month in 2019, is now processing 10,000 outbound passengers a monthvii. The ability for airports to sustain themselves throughout such volume reductions, as well as an awareness of which airports have exemplified a more muted volume reduction, are key to our understanding and investment decision making process when assessing prospective airport exposure. Figure 5 – World passenger traffic evolution 1945 – 2020 Source: ICAO Air Transport Reporting Form A and A-S plus ICAO estimates The unrelenting spread of the virus rapidly transformed many airports into largely deserted places, barely operating with limited users and negligible staff numbers. Supplementary services, once substantial contributors to airport operations, have been shut for months, and revenue losses, dwindling capital reserves and deferred or reduced infrastructure investments have manifested as the new current norm. Airport operators are navigating the shortfall storm with capital raisings, loan extensions from banks and, if privately-owned, capital injections from owners. For example, Sydney Airport has extended its credit facilities by AUD 850 million and has undertaken a capital raising of AUD 2 billion, and Heathrow Airport has halted dividend plans for GBP 300 million in 2020vii. The international-domestic traffic passenger mix encompasses significant divergence. For example, Europe and Asia/Pacific contributed over 70% of global international traffic before the crisis, whereas China and North America account for over half of the world domestic passenger traffic. When vaccines are widely accessible, they should initially aid domestic travel recovery efforts. In contrast, the international recovery hinges upon vaccine distribution and sufficient availability, regulatory approvals, and the expansion of travel corridors and bubbles and is thus expected to be protracted in comparison. 10

www.staffordcp.com

Figure 6 – Share of international-domestic passenger traffic by region (2019)

Source: ICAO estimates based on ICAO ADS-B, OAG, ICAO LTF, ICAO Statistical Reporting, and IATA Economics

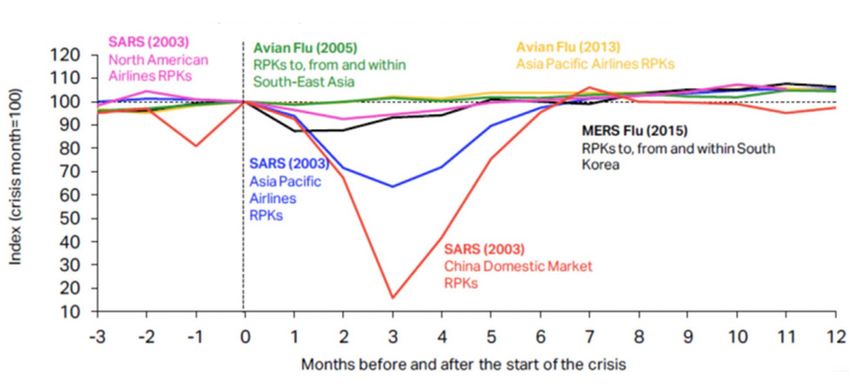

Despite the uncertainty surrounding this crisis, there is some degree of precedent. For example, past pandemics

in Asia illustrated a V-shaped impact on the industry, as shown in Figure 7. Ultimately however, aviation is linked to

economic growth and 2020 global GDP growth is anticipated to contract by 4.4% to 5.2% as forecast by the IMF

and World Bank viii, in a manner not felt since the GFC which declined by 2.9%ix in comparison. COVID-19 presents

a scenario where the contraction is significantly larger, the impact greater, and recovery projected to take longer.

Figure 7 – Past pandemic impacts on aviation

Source: IATA COVID-19 Updated Impact Assessment

As another example, the impact of COVID-19 has by now eclipsed the 2003 SARS outbreak which had

contributed to a decline of annual revenue passenger kilometres (“RPKs” - number of kilometres travelled by

paying passengers) by 8% and USD 6 billion revenues for Asia/Pacific airlinesx. However, the 6-month recovery

path of SARS does not hold full weight compared to today’s situation. Whilst some trends may be inferred via

such precedent cases, COVID-19 is a unique case. For example:

◼ China is now 16% of global GDP (in 2003 during the SARS crisis this was only 4%). The IMF approximate that

China constituted 39% of global economic expansion in 2019xi.

11◼ COVID-19 has a truly global reach, impacting all geographies and all economic output. ◼ Unknown impact on household wealth & structural unemployment. While the global economy was in a relatively strong position, the length of time that productivity is hindered will have a growing impact on consumer spending. ◼ Low oil prices of limited short-term benefit due to hedging at higher prices by most airlines. ◼ Stimulus Packages. The response to this crisis is unparalleled in size and scope. To date, around USD 7 trillion has been announced globally which includes government spending, tax breaks, loan guarantees, as well as monetary expansion. This number dwarves the amount spent during the GFC which was worth USD 1.1 trillion in 2008xi. ◼ Future fiscal tightening to repay or service increased sovereign debt may act as a drag on recovery as consumers will have less disposable income. Government intervention is deemed vital in resuscitating the industry and has been exemplified with aid to airlines, whose survival and recovery is in turn critical for the rebound of airports given the link to aeronautical revenue generation. In the US, the government has vowed support by way of USD 50 billion to the airline sector, comprised of USD 25 billion as a grant to support employees’ salaries, and a further USD 25 billion as loansxii. The prevalence of domestic travel means they are considered a key part of infrastructure, with a requirement for airlines to deliver minimum levels of service in return for the assistance granted. The European market is perceived as the most competitive and with the largest restrictions on state aid. Accordingly, many airlines may not survive. In contrast the Middle East is associated with strong state support/ownership models that translate to heightened eligibility for state aid. It is improbable that these airlines will fail. While passenger traffic has dramatically reduced, cargo flights have increased, with passenger aircraft also being converted in use to accommodate supplementary cargo. Airport operators are limited in terms of their available choices and, in addition to cargo, have aimed to maintain their operations to facilitate important people movements such as repatriation to countries of origin or residence. However, the overall effect on stabilising airport revenues is primarily limited to the largest cargo hubs. For example, Brussels Airport benefits given the city’s status as a pharmaceutical stronghold. However, cargo is on average less than 10% of total airline revenuexiii, and thus any volume uptick is not sufficient to flow on to airports and plug the 90% drop in normal passenger traffic. Stay-at-home orders alongside increased online purchases have contributed to a short-term rise in cargo volumes, although this may soften over the medium to long term. Air cargo trends typically illustrate strong correlation with GDP growth and a prolonged downturn may result in depressed volumes. For some airlines, cargo has evolved from a fixed overhead contributor to the sole source of stable revenue. COVID-19 has unleashed devastating impacts to airports as well as the 66 million global jobs supported by the wider aviation industriesxiv, pivotal to international trade and economic development for every country. As the recovery meanders through ongoing ambiguity and the crisis eventually subsides, airports will face permanent changes in the post-COVID world. 12

www.staffordcp.com

4. Risk assessment

As alluded to earlier in the diary, the 9-factor risk model is a key component underpinning our underwriting

methodology. In this section we explore some of the key risks that airports face, how these risks have changed

because of the ongoing pandemic, and how this contributes to our investment selection process when faced with

prospective airport exposure.

Revenue Risk

The impact of COVID-19 is challenging airports with both aeronautical and non-aeronautical revenue channels.

The shortfall in the number of passengers and the cancellation of flights leads to diminished revenues from airport

charges. Fewer passengers and airport staff on duty has also resulted in significantly less non-aeronautical

revenue given the downturn in onsite commercial activity, coupled with a heightened sense of caution by some

passengers. Strong pressure to cover operating expenses has surfaced, particularly given the fixed cost nature

of the industry and associated leverage. Consequently, airports around the world have significantly cut operating

costs by furloughing staff, closing terminals, postponing capital expenditure initiatives, and deferring dividends.

With the closure of international borders and implementation of stay-at-home orders, travel demand is almost non-

existent. In the United States alone, travel spending for 2020 is anticipated to decrease by around USD 400 billion,

translating into a loss of about USD 900 billion in economic outputxv. These numbers mean that COVID-19 would

have more than seven times the impact of September 11, 2001, on travel-sector revenues.

In the post-COVID-19 era, airports will operate under a “new normal”. They will have substantially higher spare

capacity than in the pre-pandemic period and will have to compete in a universe characterised by a smaller

number of financially weaker airline companies, heightening their exposure to volume risk and inflicting pressure

on their aeronautical revenues, which habitually encapsulate over 50% of total revenues. To stimulate recovery, it

is not implausible that airports may encounter augmented pressure to alleviate aeronautical charges. For example,

some US airports have offered airlines a deferral in rentals and other fees on a short-term basis under the

presupposition that traffic levels will ultimately rebound. In addition, financially depleted airlines may nonetheless

wield strong negotiating prowess in the face of lower supply and declare an unwillingness (and perhaps an

inability) to absorb contracted aeronautical fees.

Figure 8 – Pre-COVID aeronautical revenue as a % of airports’ revenue mix

Source: S&P Global Ratingsxvi

Non-aeronautical revenues for airports are also impeded not only by low passenger numbers but also by the

reduced purchasing power of consumers as the global recession persists, contributing to anticipated cuts in

average consumer spending. Moreover, revenue that airports previously expected under minimum guaranteed

volumes from retail partners may be delayed, or not materialise at all, if calculated as a percentage of sales.

13Alternatively, tenants may request rent waivers and deferrals or, in the worst case, may not survive the disruption.

Social distancing measures place additional challenges upon commercial and food & beverage services and

restrict the capacity for unhindered operations.

Conclusion: We have unsurprisingly adjusted our revenue risk rating across numerous airports in

our internal database to “high”, increasing the DCF factor. Airports that have demonstrated the capacity

to curtail costs, strategically allocate resources, maintain some degree of revenue inflow, and that have

airlines using the facilities with healthy balance sheets, sturdy credit quality, and ongoing operations are the

airports we may consider in an otherwise diversified underlying fund portfolio.

Counterparty Risk

The largest counterparty risk airports face is derived from airlines, whose services generate revenue and procure

customers who ultimately utilise the airport. Although many large airlines have enough cash to cover more than

six months of zero-capacity operations, smaller, regional airlines are especially vulnerable to financial pressures.

Widespread ratings agency downgrades could trigger breaches of covenants on debt agreements and increased

holdbacks by credit-card issuers, cutting into airline working capital at a critical juncture. For example, Moody’s

has downgraded three of the UK’s largest airports – Heathrow Finance (owner of Heathrow Airport) has seen its

corporate family rating reduced from Ba1 to Ba2, Gatwick Airport’s bond rating has declined from Baa1 to Baa2,

and Birmingham Airport’s bond rating has dropped from Baa2 to Baa3xvii. These issues then feed into airports as

their primary aeronautical revenue sources are slashed.

The mix of domestic vs international travel and leisure vs business travel are important considerations as well.

The preliminary stages of a progressive re-opening have been concentrated on domestic travel and leisure travel/

tourism. Equally, countries who have been more successful at containing the virus will have enhanced capacity at

bringing back international travellers, although this is of course contingent upon specific country advice and rules.

Conversely, business travel has been decimated and health is arguably the key factor at play. That does not

mean business trips will cease, but rather that they may be less frequent and perhaps structured in other ways

as employers ultimately have a legal duty of care to their employees and are likely to be more mindful of this and

may be reluctant to approve any non-essential travel. European business travel highlights the significant reduction

felt globally, with the April 2020 Global Business Travel Association’s (“GBTA”) member poll indicating that 78%

of companies cancelled all business trips and 20% cancelled most business trips throughout the first wave of the

pandemicxviii. In contrast, by November 2020 the GBTA poll illustrates 55% of companies cancelling all business

trips and 34% cancelling most, signalling some optimismxviii.

Over time the total number of business travellers and the amounts of money they expend in a year will surpass

the numbers recorded in 2019 merely because of population and economic growth. However, as the means of

doing business continues to evolve amidst the backdrop of technological innovation, environmental awareness,

and climate change mitigation measures, the business travel landscape may be permanently altered, with the

pandemic contributing to the acceleration of industry shifts that would have inevitably materialised.

Conclusion: With government support fluctuating by country, some airlines may procure a competitive

advantage and emerge from the crisis stronger than they were in the past, relative to their competitors,

with flag carriers (e.g. Air Canada, LATAM, Air France, Air China, etc) the most likely to be protected by their

governmentsxix. In addition, airports and airlines that entered the pandemic era with a robust balance sheet,

strong domestic network, and servicing international leisure destinations are also projected to fare better. For

example, those low-cost carriers (“LCC”) such as Wizz Air and Ryanair that can cater to short-haul travel

to popular European leisure destinations have taken advantage of rebounding leisure market conditions,

particularly given their point-to-point route networksxx. Airports with such counterparties and attributes would

be favoured for investment purposes. Travellers also acknowledge that direct flights (i.e. no connections) have

a safety advantage with fewer touch points and less time exposed to potential virus carriers in airports.

For others, of course, the contrary position may materialise as the recession shakes out weaker players

or hinders the operations of established players. Super-connectors such as Gulf state airports and airlines

such as Etihad and Emirates (notwithstanding strong government support) and those airlines without

a sturdy domestic market (and that rely on long-haul as their primary business) such as Norwegian,

Singapore and KLM are not projected to cover lost capacity from their usual operations from other

operational segmentsxix. Thus, we view these with caution over the short to medium term.

14www.staffordcp.com

Financing Risk

With revenues shoring up faster than that which cost control can accomplish – and large cost components

remaining fixed – airports are observing a substantial shift in liquidity and solvency measures. The industry debt-

to-EBITDA ratio is a direct illustration of airports’ impaired liquidity position and endangered financial health. On

average, global debt-to-EBITDA levels were reported at 4.2 in 2018. Debt levels have steadily oscillated around 5

for many years, although a declining trend has been noted in recent years. As a result of the current pandemic,

even based on assumed debt levels that have remained constant into the 2020 pandemic, the forecasted revenue

shortfall would translate into debt-to-EBITDA ratios increasing to 10 – an unnerving position for any industry xxi.

A lack of operating liquidity places many airports at risk when it comes to servicing their debt. Notwithstanding

the fact that there was a downward trend regarding accumulated debt obligations in relation to traffic volumes

over the last decade, from about USD 60 to USD 40 average on a per-passenger basis in any given year, many

airports remain deeply dependent on debt, especially in order to fund capital projects. Using North America as

an example, the significant decline in traffic has resulted in debt indicators skyrocketing whereby a 50% decline in

passenger volumes translates into doubling of debt per passenger from about USD 65 to USD 130xxi.

Moreover, the impact on solvency and debt obligations of airports is likely to increase the WACC required by

airport owners and investors. This ripple effect will inevitably push up the cost base for airport charges. Previous

studies have suggested that the global airport-industry WACC is in the range of 6% to 8% with some stability

demonstrated over the last decade, although the WACC varies according to jurisdiction, financing structure,

market conditions, traffic risk and political risk depending on where airport operators and investors place their

capital investments. Prior to the pandemic, many airport operators/parent companies with publicly listed equity

reported a beta parameter of less than one, meaning that the airport equity asset was less risky than the overall

market. As a result of the crisis, and an intensifying perceived risk by investors, beta values jumped above one for

many airport operatorsxxi.

Conclusion: In the face of airports being higher debt-leveraged and burning through cash to cover both

operations and debt repayments, it is critical to ensure potential airport investments have ample liquidity.

Supplementing this requirement, we view airports that have access to government and/or private support

more favourably, as has been witnessed with major airports across EMEA locations. In contrast, secondary

regional airports may struggle with limited support. Where airports engage proactively with debt providers

there may be capacity for fruitful cooperation which may see any airport covenant breaches waived

contingent on the correlation to COVID-19 as opposed to underlying business deficiencies. Nevertheless,

creditors may attach more onerous requirements to accept such waivers. Airports with secure, long term

financing alongside stable credit institutions, uninflated debt-to-EBITDA, and evidence of ongoing debt

servicing capabilities are on the radar.

15Technology Risk

Technology has the capacity to aid airports on a multi-faceted level and the accelerated adoption of certain

innovations can help set airports apart. As digitisation progresses, airports should perhaps deviate from a landlord

mentality and embark on a path akin to customer experience companies, merging offline and online experiences.

This customer-centric approach facilitates deeper relationships and powers the seamless digital experiences they

expect whereby a redefinition of the customer experience in turn procures potential non-aeronautical revenue

opportunities.

If airports can evolve from competition to collaboration with airlines and retailers/brands in a unified approach,

newfound shared opportunities are generated. Airports provide the fundamental infrastructure, airlines bring

the customers, retailers supply the products, and brands instil attraction and excitement. Travel retail can be

rejuvenated if airports can redefine and solidify partnership mechanics and break down the silos underpinning

a largely siloed and primarily physical consumer experience. Take for example the rise of e-commerce, which is

becoming increasingly mainstream and can serve as a competitive tool for both airports and airlines. Singapore

Airlines has established an e-commerce company (KrisShop) and a powerful lifestyle brand that utilises airline

data for a customer base on a platform that produces revenue even when its passengers are not flying. KrisShop

quadrupled its sales in just nine months and its e-commerce revenues grew by 500% throughout COVID-19. The

basket size doubled, conversion tripled, and promotions surged to 7% conversionxxii. Partnership with Changi

Airport is under early consideration and this could be particularly attractive given approximately 48% of Changi

Airport’s revenue is derived from non-aeronautical sourcesxxiii.

In parallel, airports are working on processes to reduce the health risks associated with air travel. These include

extended use of contactless technology, biometrics, more self-service kiosks and protective barriers, and

‘touchless’ screening processesxxiv. Consumers will be more inclined to recommence travel in a safe environment

and thus a penchant for reviewing and implementing necessary adjustments to the airport infrastructure itself as

well as operational protocols is needed.

Conclusion: Airports can still muster stronger revenue, control, and long-term stability by capitalising

on digital opportunities both from a revenue and safety standpoint. Open, innovative and time conscious

airports that are utilising this temporary downtime to reassess their business plans and test innovations

in advance of the recovery are those that will be able to accommodate the post-COVID-19 consumer and

traveller of tomorrow and be able to adapt more swiftly to changing consumer needs. Those that do not

ultimately risk being left behind the curve.

ESG Risk

COVID-19 has stimulated further discussion and action regarding decarbonisation processes and has also

accelerated the adoption of revamped health and safety measures. When estimating and attributing emissions,

aviation is a somewhat unique sector in that around 65% of its CO2 emissions are in international airspace and,

therefore, do not necessarily “belong” to individual nation states. Aviation also has a significant dependence

on liquid fossil fuels, tight safety regulations, as well as a long aircraft development and fleet turnover time.

Accordingly, quickfire alterations to the fleet – such as those being seen in motor vehicles – are simply not

financially viable or technologically feasible. Moreover, the international aviation sector is not part of the Paris

Agreement on climate change and is thus not addressed by individual nations in their pledges to cut emissions.

Without tackling aviation, meeting the 2C or 1.5C warming limits of the agreement is made more challenging.

What further complicates the scenario is that CO2 emissions are but one of the adverse climate impacts

connected with the aviation industry at about 34%, with the balance derived from non-CO2 impacts (primarily

contrail cirrus and emissions of nitrogen oxides)xxv.

Air transportation contributed at least 2.5% of global CO2 emissions in 2019. This figure is simply emissions from

aircraft engines measured at ground level; recent studies caution that aircraft contrails at cruising altitude could

double the global warming impact. Airline CO2 emissions have grown from 700 million tons CO2 equivalent in

2010 to 900 million tons in 2018, a 29% increase (2.9% annualized). IATA forecasts 3.5% annual growth in air

passengers over the next two decades. Such rapid growth in passengers would likely result in continued growth

in airline industry CO2 emissions. Airplane journeys may be discouraged where a viable alternative exists. For

example, 170kg of CO2 is released flying roundtrip from Paris to Marseille when the same journey can be made by

train at a CO2 ‘’cost’ of 6kgxxvi.

16www.staffordcp.com

Figure 9 - Airline industry net C02 emissions

Source: Candriam

Analysts estimate that the pandemic will result in a 5% drop in global CO2 emissions in 2020xxvi, relative to the

prior year, with air transportation contributing to 10%xxvii of the decline. It marks the first annual drop in CO2

emissions since 2009 and the most substantial annual decrease since 1950. Unfortunately, this decrease is solely

attributable to the result of political decisions around the world to suspend economic activity to slow the spread of

the virus. Unless material action is taken, it is not unforeseeable that aviation emissions could grow to become a

dominant component of human emissions as other sectors decarbonise.

Nevertheless, the pandemic has perhaps opened a once-in-a-generation window of political opportunity to

confront various global issues with audacious and extensive measures. As airports and airlines line up to receive

state aid, governments have an opportunity to balance the survival of these entities against their impact on climate

change. Proposals to make financial support for airlines conditional on cutbacks in greenhouse gas emissions

(“GHGs”) have emerged on various fronts, including European governments. For example, the French government

has linked support for Air France to climate goals, with conditions comprising halving the overall CO2 emissions

per passenger-kilometre by 2030 (compared to 2005 levels), a 50% reduction of domestic flights’ CO2 emissions,

and 2% of the airlines fuel requirements to be from sustainable sources by 2025xxviii.

Health and safety are key ESG factors and when demand does return, airports who are able to offer a seamless,

safe, contactless, and ideally as simple as possible airport experience for the customer will benefit. For example,

Gatwick Airport was the first UK airport to implement a UV disinfection system for its security trays (trays pass

through a UV-tunnel underneath the hand luggage screening systems), generating a 99.9% disinfection ratexxix.

In addition, Luton Airport has undertaken adjustments resulting in the receipt of certification from the Airports

Council International’s (“ACI”) health accreditation program, the first airport in the UK to receive such accreditation

and one of the first globally xxx. Such adjustments include optimised cleaning and disinfection of terminals,

installation of hand sanitiser units, protective screens, and increased usage of robotics.

Finally, although we do not know what new regulations may arise to regulate travel, there could be some time-

consuming supplementary checks or requirements that dissuade business or short-term leisure travellers from

taking trips. Airports getting on the front foot now to work proactively with one another, regulators, and others in

the ecosystem to ensure a smooth and consistent customer experience while guaranteeing safety may pull out

ahead in the long run. Collaboration could be increasingly important to success in the new world.

17Conclusion: Climate change is an existential threat that has widespread ramifications for the entirety

of the planet, the impacts of which we are undoubtedly now witnessing more frequently. Thus, when it

comes to potential airport investments, we are inclined to consider those that have a well-defined, realistic,

and actionable climate plan in place, and which have demonstrated an existing track record in reducing

both CO2 and non-CO2 adverse environmental impacts. Airports that service increasing regional tourism

may also be attractive, contingent upon their underlying economics. Furthermore, airports that are taking

proactive steps now to modify their health and safety operations and liaise productively with relevant

counterparties bode more favourably.

18www.staffordcp.com

5. Concluding remarks

COVID-19 evidentially presents numerous challenges to this sector. Airports have high fixed costs, and it is unclear

the extent to which their pre-COVID economic model is sustainable. To the extent that their revenue mix changes,

it remains to be seen whether other contributors to overall revenues are able or willing to fill the gap. Technological

advancements are also key in underpinning operational bounce back from airport operators and assisting to

minimise the spread of the virus.

As part of our ongoing deal origination, we are regularly faced with portfolios that include airports. The

attractiveness of our secondaries diversified approach is partly based on our ability to price via discounts the

downside case of individual investments. Based on our core focus and the increased risk and volatility of such

investments, we will however remain circumspect, in particular for airports that are business-travel oriented,

focused on long haul international offerings, void of clear government or private owner support, and for which the

cash flow and financing situation remains unclear.

The path to recovery remains turbulent and any investment appetite for airports in the short to medium term

pertains to those operators servicing a strong domestic or short haul international base (with access to markets

underpinned by travel corridors), with sufficient liquidity and stable financing in place, linked to resilient airline

counterparties, and with technological innovation, revenue supplementation plans (e.g. increased cargo), health

measures, and climate considerations as key strategic initiatives to drive their recovery.

More broadly, in the months ahead, we will continue to provide investors with the results of our research into

various sectors in the form of sector diaries, as we remain focused on building a diversified, core and yielding

portfolio capable of performing strongly even in the current volatile environment. In the meantime, we hope you

will have found this edition insightful!

196. References

i Airport Categories, Flight Literacy, https://www.flightliteracy.com/airport-categories/ and The Different

Types of Airports in the US, Aircraft Compare, https://www.aircraftcompare.com/blog/types-of-airports/

ii Types of airlines and airline business models, One Education, https://www.oneeducation.org.uk/types-

of-airlines-and-business-models/ and Belobaba. P, Odoni. A, Barnhart.C, 2009, The Global Airline

Industry, John Wiley & Sons, Ltd, Chichester, United Kingdom

iii ICAO, 2015, State of Airport Economics, produced in cooperation with the Airports Council International

(ACI), Montreal, Canada

iv What are the main sources of non-aeronautical revenue at an airport, 2018, Ikusi,

https://www.ikusi.aero/en/blog/what-are-main-sources-non-aeronautical-revenue-airport

v How airports actually make money, 2018, Simple Flying,

https://simpleflying.com/how-airports-make-money/

vi Steer Davies Gleeve, 2017, Heathrow Airport Review of Commercial Revenues, prepared for Civil Aviation

Authority, London, United Kingdom

vii Chong, F. 2020, Airport infrastructure: Poor visibility, IPE Real Assets,

https://realassets.ipe.com/travel-sector/airport-infrastructure-poor-visibility/10049135.article

viii International Civil Aviation Organization, 2020, Effects of Novel Coronavirus (COVID 19) on Civil Aviation:

Economic Impact Analysis, Air Transport Bureau, Montreal, Canada

ix Kose.A & Sugawara.N, 2020, Understanding the depth of the 2020 global recession in 5 charts,

World Bank Blogs,

https://blogs.worldbank.org/opendata/understanding-depth-2020-global-recession-5-charts

x What can we learn from past pandemic episodes?, 2020, IATA Economics’ Chart of the Week,

https://www.iata.org/en/iata-repository/publications/economic-reports/what-can-we-learn-from-past-

pandemic-episodes/

xi Willis Towers Watson, 2020, Covid-19 - What will be the impact to the aviation sector from the Coronavirus

outbreak?

xii Nguyen, T. 2020, Airlines are asking the US government for a $50 billion bailout. Should they get it?, Vox,

https://www.vox.com/the-goods/2020/3/19/21186792/airline-bailouts-coronavirus-50-billion

xiii Diamond, M. 2020, Airlines must see cargo as a ‘core business’ from now on, The Load Star – Making

Sense of the Supply Chain,

https://theloadstar.com/airlines-must-see-cargo-as-a-core-business-from-now-on/

xiv 25 Million Jobs at Risk with Airline Shutdown, 2020, IATA,

https://www.iata.org/en/pressroom/pr/2020-04-07-02/

xv Curley.A, Dichter.A, Krishnan.V, Riedel.R, Saxon.S, 2020, Coronavirus: Airlines brace for severe

turbulence, McKinsey & Company, https://www.mckinsey.com/industries/travel-logistics-and-transport-

infrastructure/our-insights/coronavirus-airlines-brace-for-severe-turbulence

xvi Yokota, J. Tsoneva.T, Iyer.P, Lu.G, Forsgren.K, Sperling-Tyler.B, 2020, Airports Face A Long Haul To

Recovery, S&P Global Ratings, https://www.spglobal.com/ratings/en/research/articles/200528-airports-

face-a-long-haul-to-recovery-11506553

xvii Thicknesse, E. 2020, Moody’s downgrades credit ratings of UK’s largest airports, City A.M,

https://www.cityam.com/moodys-downgrades-credit-ratings-of-uks-largest-airports/

xviii GBTA COVID-19 Member Poll Results, 2020, Global Business Travel Association,

https://www.gbta.org/research-tools/covid-19-member-polls

20www.staffordcp.com

xix Sloan, C. 2020, The future of air travel in the age of COVID-19: winners, losers, Airways Magazine,

https://airwaysmag.com/industry/the-future-of-air-travel-in-the-age-of-covid-19-winners-losers/

xx COVID-19 on European low-cost and regional airlines, 2020, Cirium,

https://www.cirium.com/thoughtcloud/covid-19-impact-european-low-cost-carrier-market/

xxi Lioutov, I. 2020, COVID-19: Rising financial risks in the airport industry, ACI Insights,

https://blog.aci.aero/covid-19-rising-financial-risks-in-the-airport-industry/

xxii Gould, K. 2020, Getting the magic and non-aeronautical revenue back post-COVID-19, International

Airport Review, https://www.internationalairportreview.com/article/145730/getting-the-magic-and-non-

aeronautical-revenue-back-post-covid-19/

xxiii Singapore Changi Airport 2019 Report

xxiv Dixon, S., Terry, B., Reece, D., Krimmel, L., Appelbaum, J. 2020, How COVID-19 is challenging orthodoxies

in airport customer experience, Deloitte

xxv Lee, D.S., Forster, P. 2020, Guest post: Calculating the true climate impact of aviation emissions, Carbon

Brief – Clear on Climate Change,

https://www.carbonbrief.org/guest-post-calculating-the-true-climate-impact-of-aviation-emissions

xxvi Czupryna, D. 2020, Can aviation turn the skies blue?, Candriam, https://www.candriam.co.uk/en/

professional/market-insights/topics/sri/can-aviation-turn-the-skies-blue/

xxvii Emissions reduction should play a major part in aviation’s post-COVID recovery, CAPA Centre for Aviation,

https://centreforaviation.com/analysis/airline-leader/emissions-reduction-should-play-a-major-part-in-

aviations-post-covid-recovery-536598

xxviii SAF Community, 2020, French government sets green conditions for Air France bailout,

https://safcommunity.org/news/278269

xxix Macola, I.G. 2020, Covid-19: how are London’s airports weathering the storm?, Airport Technology,

https://www.airport-technology.com/features/covid19-london-airports-weathering-storm/

xxx Aviation will emerge stronger from the COVID-19 crisis, Winter 2020, The Airport Operator, London, United

Kingdom

217. Contacts Dr Ingo Marten William Greene Head of Real Assets, Zurich Head of Infrastructure, Zurich Email: ingomarten@staffordcp.com Email: williamgreene@staffordcp.com Matthew McPhee David Lindsay Partner of Infrastructure, Boston Partner of Infrastructure, London Email: matthewmcphee@staffordcp.com Email: davidlindsay@staffordcp.com 22

23

Important Information The information in this document does not represent investment advice and should not be relied upon for investment decisions. This document neither constitutes an offer to sell nor a solicitation to invest in any of the Stafford Funds. It is for information purposes only and is not a recommendation. This document does not constitute an offer to sell or a solicitation to invest in any jurisdiction where the offer or sale would be prohibited or to any person not meeting the required investor criteria. Any opinions expressed are given in good faith but are subject to change without notice. No representation or warranty, express or implied, is made as to the accuracy, completeness, or correctness of any information in this document which has not been verified. Stafford Capital Partners Limited (formerly Stafford Timberland Limited) is a company registered in England (Company Reg: 4752750) with a registered and trading address at Fourth Floor, 24 Old Bond Street, London, United Kingdom W1S 4AW. It is authorised and regulated by Financial Conduct Authority (Firm# 225586). Stafford Capital Partners is a member of the United Nations’ Principles for Responsible Investment (UNPRI). These principles are an internationally agreed upon framework to help institutional investors incorporate Environmental, Social and Governance (ESG) qualitative considerations into investment decision-making and ownership practices. Stafford Capital Partners is acknowledged by the UNPRI, when compared against our peers, as incorporating a solid framework for ESG considerations into its investment decision process (selection, assessment, and monitoring of investments). For more information about UNPRI, visit www.unpri.org. We are obliged to protect personal data, preserve confidentiality of personal and sensitive data, and prevent the loss of data. Please read our statement on personal and sensitive data that is linked on our website www.staffordcp.com/legal. If you have any questions about our personal and sensitive data policy and framework or if you wish to exercise your rights in respect of your personal data, please email our Data Protection Officer on privacy@staffordcp.com.

You can also read