Unleashing the Power of Convergence to Advance Mobile Money Ecosystems - World Bank Document

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

57510

Public Disclosure Authorized

Public Disclosure Authorized

Public Disclosure Authorized

MOBILE MONEY SUMMIT 2010

Unleashing the Power of Convergence to

Advance Mobile Money Ecosystems

Piya Baptista and Soren Heitmann

Public Disclosure Authorized

Written by Piya Baptista and Soren Heitmann Designed by Alison Beanland © 2010 IFC and the Harvard Kennedy School ACKNOWLEDGEMENTS This report draws heavily on the experience of speakers and participants in the third annual GSMA Mobile Money Summit, co-organized by IFC, CGAP, and the UK Department for International Development, held May 24-27, 2010 in Rio de Janeiro, Brazil. In particular the authors would like to thank various speakers and industry experts for generously sharing their time and insights through in-depth interviews during and after the summit. The authors would like to thank Andi Dervishi, Arata Onoguchi, and Ian Larsen for their strategic guidance and input into this report. The authors would also like to thank the Harvard Kennedy School’s Beth Jenkins for her careful review, substantive input and editing of various drafts as well as her ongoing dedication to this project. This report would not have been possible without the institutional and financial support of IFC and the Government of Netherlands. All quotes and content for this report are drawn from conference sessions, working groups, speaker interviews and presentations during the Mobile Money Summit 2010. Material from other sources is referenced in the endnotes. RIGHTS AND PERMISSIONS The material in this publication is copyrighted. Quoting, copying, and/or reproducing portions or all of this work is permissible using the following citation: Baptista, Piya and Soren Heitmann. 2010. “Unleashing the Power of Convergence to Advance Mobile Money Ecosystems.” Washington, DC: IFC and the Harvard Kennedy School Photographs © GSM Association; Digicel; Zain Zap; MTN; Roshan; YellowPepper, O2

MOBILE MONEY SUMMIT 2010 Unleashing the Power of Convergence to Advance Mobile Money Ecosystems Piya Baptista and Soren Heitmann

Defintions and Acronyms Used in this Report

Acronyms

AML: Anti Money Laundering G2P: Government to Person MFI: Microfinance Institution

B2B: Business-to-Business KYC: Know Your Customer m-wallet: Mobile Wallet

CFT: Combating Financing of Terrorism MNO: Mobile Network Operator NFC: Near Field Communication

e-money: Electronic Money m-money: Mobile Money P2P: Person-to-Person

Definitions1

Agent: A person or business that is value is typically stored in a microprocessor regulators, international financial institutions

contracted to facilitate transactions for users. chip embedded in a plastic card or and donors, and even civil society

The most important of these are cash-in and “smartcard.” On the other hand, network organizations.

cash-out (i.e. loading value into the mobile based products use specialized software

money system, and then converting it back installed on a standard personal computer for Mobile Payment: A movement of value that

out again); in many instances, agents register storing the “value.” The loading of value is made from a mobile wallet, accrues to a

new customers too. Agents usually earn onto the device is akin to the withdrawal of mobile wallet, and/or is initiated using a

commissions for performing these services. cash from an ATM, and the product is used mobile phone. Sometimes, the term “mobile

They also often provide front-line customer for purchases through a transfer of value to payment” is used to describe only transfers to

service—such as teaching new users how to the merchant’s electronic device. pay for goods or services, either at the point

initiate transactions on their phone. Typically, of sale (retail) or remotely (bill payments).

agents will conduct other kinds of business Float: The balance of e-money, physical cash,

in addition to mobile money. The kinds of or money in a bank account that an agent Mobile Money Provider:4 Any institution

individuals or businesses that can serve as can immediately access to meet customer that plays the lead role in a mobile money

agents will sometimes be limited by regulation, demands to purchase (cash in) or sell (cash deployment. In this report, “mobile money

but small-scale traders, microfinance out) electronic money. provider” refers to MNOs, banks or third

institutions, chain stores, and bank branches parties that provide mobile money services.

serve as agents in some markets. Some Know Your Customer (KYC): Rules related

industry participants prefer the terms to AML/CFT which require providers to carry Mobile Money Transfer: A movement of

“merchant” or “retailer” to describe this out procedures to identify a customer. value that is made from a mobile wallet,

person or business to avoid certain legal accrues to a mobile wallet, and/or is initiated

connotations of the term “agent” as it Liquidity: The ability of an agent to meet using a mobile phone.

is used in other industries. customers’ demands to purchase (cash in) or

sell (cash out) e-money. The key metric used Mobile Wallet (m-wallet):5 An account that

Anti Money Laundering/Combating to measure the liquidity of an agent is the is accessed using a mobile phone. A mobile

Financing of Terrorism (AML/CFT): A set sum of their e-money and cash balances (also money provider can offer a wide range of

of rules, typically issued by central banks, that known as their float balance). services to facilitate financial transactions via a

attempt to prevent and detect the use of mobile wallet. These services could include

financial services for money laundering or to Interoperability: The ability of users of remittances, person-to-person money

finance terrorism. The global standard-setter different mobile money services to transact transfers, bill payments, proximity payments,

for AML/CFT rules is in the Financial Action directly with each other. Given the technical, airtime top up, loan repayments, etc

Task Force (FATF). strategic, and regulatory complexities that

enabling such transactions would entail, no Unbanked: Customers, usually poor, who do

Cash in: The process by which a customer mobile money platforms to date are fully not have bank accounts or transaction accounts

credits his account with cash. This is usually interoperable with each other. However, at formal financial institutions.

via an agent who takes the cash and credits many mobile money services allow users to

the customer’s mobile money account. send money to non-users (who receive the Under-banked: Customers who may

transfer in the form of cash at an agent). have access to basic transaction accounts

Cash out: The process by which a customer offered by formal financial institutions, but still

deducts cash from his mobile money account. Mobile Banking: When customers access a have financial needs that are unmet or not

This is usually via an agent who gives the bank account via a mobile phone; sometimes, appropriately met. For example, they may not

customer cash in exchange for a transfer from they are able to initiate transactions. be able to send money safely or affordably.

the customer’s mobile money account.

Mobile Money (m-money): A service in

Electronic Money (e-money):2 Electronic which the mobile phone is used to access

money is defined as a stored value or prepaid financial services.

product in which a record of the funds

or value available to the consumer for Mobile Money Ecosystem:3 Networks of

multipurpose use is stored on an electronic organizations and individuals that must be in

device in the consumer’s possession. place for mobile money services to take root,

This definition includes both prepaid cards proliferate and scale up. They are

(sometimes called electronic purses) and characterized by interdependence and

prepaid software products that use computer coordination among any number of

networks (sometimes called digital cash). In actors—such as MNOs, banks, airtime sales

the case of card-based products, the prepaid agents, retailers, utility companies, employers,

Table of Contents

IFC FOREWORD 4

PREFACE: THE OCCASION FOR THIS REPORT 5

SECTION 1: STRATEGY 7

SECTION 2: MARKETING 13

SECTION 3: OPERATIONS 17

SECTION 4: GROWTH 23

LOOKING FORWARD 27

APPENDIX 1: MOBILE MONEY SUMMIT 2010 AGENDA 29

APPENDIX 2: MOBILE MONEY TRACKER 32

APPENDIX 3: ENDNOTES 34

APPENDIX 4: USEFUL REFERENCES 35

APPENDIX 5: LIST OF INTERVIEWEES 36

MOBILE MONEY SUMMIT 2010 3

e 2010 Mobile Money Summit marked an important moment in the evolution

of the mobile financial services ecosystem. No longer is mobile money an enticing

possibility or an unproven concept. In the two years since the first summit, mobile

money has provided millions of people around the world with access to finance,

and demand continues to increase.

Kent E. Lupberger

Over the next two years, the number of people with access to a mobile phone but

Senior Manager,

Telecom and Information not to traditional financial services is expected to grow from one billion to 1.7

Technology, billion, and Mobile Network Operators (MNOs) are poised to earn $7.8 billion in

Global Infrastructure & Natural direct and indirect revenues from more than 350 million clients.

Resources Department,

International Finance Whether it is for paying salaries, reimbursing suppliers, or sending remittances home

Corporation from abroad, mobile money is allowing people to conduct transactions at lower cost

and with greater efficiency than physical transactions. With mobile money, users

are moving out of cash-based informal systems and are fully participating in the

formal economy, making it a key way to improve livelihoods.

Clearly, mobile money is proving its potential.

But scaling up the industry to meet demand requires a deep understanding of

money, individual market nuances, stakeholders, strategies, and roadblocks to

success.

e Mobile Money Summit 2010 was convened to help the industry better

understand how the ecosystem has grown and how each of these factors affects

mobile money’s role in developing a larger e-money economy: one in which cash

wallets are replaced with mobile wallets and other electronic payment instruments.

To continue its growth and begin to fulfill the promise of an e-money economy,

industry stakeholders must work together to unleash convergence, drive customer

acquisition, and refine enabling technology. Mobile money must have a clear appeal

to consumers, the public sector, and the private sector.

e Mobile Money Summit 2010 identified a number of key lessons for all of the

industry’s stakeholders. Primary among these was that mobile money’s development

value rests in its ability to facilitate financial sector inclusion. To do so will require

financial institutions and MNOs to work together with regulators on a

country-by-country basis. Providers will need to introduce basic mobile money

services where they do not already exist and foster the consumer’s appetite for more

sophisticated services. Effective distribution networks must be developed in order

to reach critical mass in the industry.

IFC has produced Unleashing the Power of Convergence to Advance Mobile Money

Ecosystems to capture these and other key lessons learned during the Mobile Money

Summit 2010. e report serves as a valuable resource to anyone who seeks to

understand the state of the mobile money industry – or to anyone working to grow

the industry further, a goal shared by IFC and the entire World Bank Group.

4 MOBILE MONEY SUMMIT 2010

The Occasion for this Report

T

his report is written on the occasion convincing is needed of the mobile money

of the third Mobile Money opportunity. e Rio Summit brought

Summit, held May 24-27, 2010 in together 58 speakers and 643 participants

“Mobile money

Rio de Janeiro, Brazil. e discussions at from 63 countries. Approximately 51%

sustainability can be

this year’s summit reflect the evolution in of attendees were senior management.

the mobile money industry since the first As in previous summits, the participants achieved through the

summit was held two years ago. As represented every sector of the mobile development of the

GSMA Mobile Money Director Gavin money industry—including financial full ecosystem but

Krugel stated, “We have evolved from service institutions, mobile network must be done jointly:

hype in 2008 to regulatory and other operators (MNOs), development organ- banks, governments,

challenges in 2009 to a deeper level of izations, technology vendors, regulators MNOs, merchants,

conversation based on real experience in and academics. regulators.”

2010.” is experience is based on an e Mobile Money Summit 2010 Report George Held, Group Marketing

increase in the number of mobile money aims to provide readers with a high level Director, Zain

deployments worldwide from 60 in 2008 summary of the key discussion points and

to 120 in 2009 to 160 as of August 2010. takeaways from this year’s conference. It is

Of these 160 deployments, 73 are live and based on the main conference proceedings

87 are expected to go live in 2010 (see on May 25 and 26, interviews with 23

Mobile Money Tracker on pages 32-33). speakers and other experts during and

is increase in the number of mobile after the conference, and on pre- and post

money deployments, as well as the conference events, namely the Mobile

continued diversity of speakers and Money for the Unbanked Working

participants at the Mobile Money Group on May 24 and the Leadership

Summit, indicate that no further Forum on May 27. e report explores

MOBILE MONEY SUMMIT 2010 5

E-money: Setting the Electronic Money Context in this Report

Mobile money services are financial individuals to engage the formal an electronic transaction. As retailers

services accessed via a mobile phone. financial system through electronic and individuals use and accept e-money,

The mobile phone is the newest of many transactions. it will become more common and more

vehicles used to access financial services. However, the mobile phone is useful in the marketplace and decrease

Credit cards are a well-established what makes mobile money services the need to cash-in or cash-out.

mechanism for electronic payments, revolutionary. Mobile money describes this broad

and it has been possible to send money Mobile phones provide individuals a collection of financial services that are

orders since the telegraph. Current convenient access point to financial accessed by mobile phones, enabling

mobile money deployments provide services, permitting the user to initiate individuals to spend, accept, store and

person-to-business electronic transactions from anywhere transfer electronic money. Mobile money

payments, like and send them anywhere, including services will soon serve the breadth of

purchasing air time other mobile phones. More significantly, today’s daily financial transactions,

top-up, or international the money used through mobile money potentially making mobile phones the

person-to-person services is fungible so that someone primary access point for daily economic

remittance services, for can loan a friend lunch money, for transactions and electronic money

example. These services initiate an example, in a way that credit cards the primary means of settling those

electronic transaction that is functionally cannot possibly do. Because the store transactions.

similar to the act of swiping a credit of value is maintained and potentially

card in a store or sending money with spent or re-sent anywhere, this describes

Western Union. All these services enable electronic money (e-money), not simply

select themes, practices and challenges to divided into four sections: strategy,

unleash the full potential of mobile marketing, operations and growth. Each

money for the benefit of consumers section presents one to two questions

worldwide—the banked, the unbanked, and insights drawn from the discussions

and the under-banked. e report is at the Rio summit. ese include:

SECTION KEY QUESTIONS

Strategy • How do we unleash the power of convergence?

• What is the recipe for launching and sequencing services?

Marketing • How do you drive customer acquisition and usage?

Operations • How do you develop and implement an optimal agent network strategy?

• How does technology enable a successful mobile money deployment?

Growth • How can we accelerate the acceptance of mobile money services?

Previous Mobile Money Summit Reports new mobile money industry marks a

focused on ‘developing’ and ‘accelerating’ critical, powerful point of convergence

mobile money ecosystem development. between banks and MNOs. In his

is report focuses on ‘deepening and opening remarks, Krugel asked

broadening’ mobile money ecosystems. participants to “unleash the power of

Cross-sector partnerships among MNOs, convergence.” In other words, to think

banks and others are leading to the about what we can do together to jointly

emergence of deeper, more inter- target new market segments. “It’s not you

connected networks and new entrants are or us,” he says, “it is us together that will

broadening these networks. Partnerships create a market for mobile money.” By

between MNOs and banks in particular joining forces, the telecommunications

facilitate the development of the mobile and banking industries have the power to

money industry as a whole, in a way that change the way people across the globe

these individual industries may not easily transact, and especially to address the

accomplish. Cooperatively growing this financial needs of the poor.

6 MOBILE MONEY SUMMIT 2010

1 STRATEGY

Strategic Partnerships: The key to unleashing the power of convergence is

strategic partnership between banks and MNOs. Together, these partners have

the infrastructure capability and institutional know-how to meet regulatory

challenges and successfully launch a mobile money service. But clear roles and

dedicated leadership are required for a mutually beneficial relationship.

Product Sequencing: Each market has its own demands and constraints,

implying there’s no single recipe for launching a mobile money service, or even a

clear answer for what that service should be. A successful service will meet

customer needs and demand, but requires a deep knowledge of the market.

“MNOs have the customer base and understand mass consumer behavior. Banks want

to go down-market and tap this wider opportunity utilizing more cost-effective

methods of service delivery. With the aligned objectives of increasing access to financial

services at lower cost, MNO-bank partnerships will be an underlying theme for the

next five years.”

RIZZA MANIEGO-EALA, PRESIDENT, G-XCHANGE INC.

MOBILE MONEY SUMMIT 2010 7

1 STRATEGY

How do we unleash the power of convergence?

❚ Partner for Power

“Mobile money has the potential to impact scale. “e role of the financial institution

billions of people globally,” observes George gives the regulator comfort,” explains Held,

Held, Group Marketing Director, Zain. making them more likely to come to the

is potential lies at the intersection table when approached by an MNO-bank

of modern telecommunications and partnership than an MNO alone.

traditional banking. is is the power of Partnership with financial institutions can

convergence: through union between these also help expand services and reach new

industries, mobile money can reach customer segments. In the Philippines, for

emerging and developed markets alike with example, Globe Telecom’s mobile money

tremendous opportunities in the form of platform provided by its wholly-owned

new services for greater financial inclusion. subsidiary, G-Xchange Inc., has enabled

“What’s the best way It is no coincidence that all successful millions of Filipinos living abroad to send

to get a mobile money mobile money deployments in the world money home to GCASH customers

today involve an MNO and a financial though partnerships with PayPal, BICS,

service off the ground?

institution. ese strategic partnerships Western Union, Xoom and numerous

Making sure you have have emerged as best practice for other large remittance companies. Rizza

the right ecosystem unleashing the power of convergence. Maniego-Eala, President of G-Xchange

partners behind you.” Partnerships combine know-how when Inc., describes such partnerships as huge

engaging the regulator and capacity to scale assets for the growth and success of mobile

Amit Mattatia,

service offerings. Zain’s Zap service boasts money. ese partnerships create the

President & CEO, Trivnet

over 12 million customers6 in Africa and essential components of the foundation

the Middle East and partnerships with that will allow more financial services to be

CitiBank and Standard Chartered were key offered to mobile subscribers.

factors enabling this level of international

❚ Challenges for Partnerships

ere are two fundamental components regulator’s help and support must be

of a successful mobile money sought early on to identify problems and

deployment: infrastructure and regu- find solutions, or else it will be impossible

latory approval. “If your mobile money to get the mobile money deployment

strategy wants to cover a mobile area and off the ground. MNO-bank partnerships

your network doesn’t, that’s a conflict,” are a perfect match to address mobile

says Koji Ono, Chief Strategy Officer for money needs, but both must be fully

Robi. e same type of conflict can arise committed to the project’s success. e

when trying to launch a service that challenges will push partners into

doesn’t meet compliance standards. Being unfamiliar territory and the mobile

compliant is seldom trivial, in part money service itself will likely represent a

because mobile money is so new that divergence from their respective core

regulators have yet to fully codify how business models. Dedication from top

these services need to work. e management is a key factor for success.

8 MOBILE MONEY SUMMIT 2010G-Xchange Inc.’s partnerships

enable G-Cash customers in

the Philippines to receive

money from relatives abroad.

Roles and responsibilities are also may fear competition and back away.

critical success factors. ese need to e required commitment to cooperation

be clearly defined, not only to meet and shared benefit increases as services

regulatory challenges, but also to ensure expand and partnerships grow. For

that the partnership is based on shared MTN Ghana, there are nine partner

risk and shared benefit. Coenraad banks. “It was a challenge to get

Jonker, Director of Community everyone to understand why they

Banking, Standard Bank of South Africa needed to share,” says Bruno Akpaka,

acknowledges that banks may be wary General Manager, MobileMoney, MTN

when approached by an MNO seeking Ghana, “but now everyone understands

to enter the financial services space. If their role” — and this has spelled success

the MNO seeks to provide mobile for the partnership, which expects over

money as a value-added service to 2 million mobile money customers

increase its margin or customer base, the within the first year of deployment. In

bank is ready to help the partnership this example, MTN Ghana led the

succeed. But if the MNO seeks to go partnership due to its initiative, strong

deeply into financial services, the bank brand and customer base among a

A Strong Partnership Solves Regulatory Challenges

The Méditel-BMCE Bank partnership included requiring that only bank AML concerns, but also to improve the

identified a strong opportunity for mobile employees register new users and that service offer.

banking services in Morocco, with 31% of cash-in transactions happen only at bank Thanks to strong commitment and

the population banked and 76% using branches. Banks needed to have cooperation from both Méditel and BMCE

mobile phones as of 2008. A careful study governance control over IT infrastructure, top management, the parties managed to

of the market found demand for money imposing requirements on the overcome these regulatory challenges by

transfer, bill payment and airtime top-up partnership’s business model. Finally, signing an “Intermediary in Banking

services. banks were responsible for payments Operations” mandate. This mandate

However, initial regulatory requirements accounting, but SIM cards and phones allows Méditel to commercialize mobile

posed a significant hurdle: money transfer were inadequate identifiers. money using its own agent network to

services needed to be executed in Early on, Méditel and BMCE shared the collect money from customers on behalf

dedicated premises that included guards project with the central bank to ensure of BMCE.

and security cameras. With Méditel’s agent regulation was addressed in the scope of

network consisting of small grocers, these the project. Many working sessions

prohibitive requirements meant no allowed the partners not only to comfort

widespread deployment. Other hurdles the central bank about security, KYC and

MOBILE MONEY SUMMIT 2010 91 STRATEGY

largely unbanked population. Strong MNO, a third party may be best

leadership is critical, and this role must equipped to lead, such as in Ecuador

also be decided. But who leads is highly where YellowPepper brings a host of

dependent on the market and the assets mobile money ecosystem stakeholders

each partner brings to the table. While and customer segments together under

an MNO might lead in a market like the tri-branded MONY service.

Ghana, a bank might lead in a country Regardless of who fills the role, uniting

where the ATM network vastly outstrips under strong and dedicated leadership

an MNO’s agent network. In settings is necessary for stable, beneficial

without a clearly dominant bank or partnership.

What’s the recipe for launching and

sequencing services and products?

❚ The Killer Application

ere is no recipe for launching or target unbanked populations or those

sequencing mobile money services. with low financial literacy, as these

However, the ingredients are well segments are less likely to demand

known: success is predicated on a formal financial tools or be familiar with

thorough understanding of the market their use. Herein lies the challenge

and target customer, a positive of identifying the so-called killer

regulatory environment, and the right application. But Richard Mwami, Head

partnerships. Knowing each country’s of MobileMoney for MTN Uganda,

needs and regulatory nuances is critical offers three basic principles for guidance:

to identifying the right opportunities, think big, start small, and scale fast. e

says Hesham Shawki, Chief Innovation right sequencing will present itself once

and Partnership Officer for Orascom initial services take off, says Aletha Ling,

Telecom Holdings, but the use case is Executive Director and Global Head of

what ultimately drives and defines Business Development for Fundamo:

success. e problem with the use case “Your customers will surprise you, not

is that the customer doesn’t always know just on volume, but on demand for more

what they need or what they want to do services.”

when it comes to mobile money services.

is can particularly trouble services that

10 MOBILE MONEY SUMMIT 2010MTN agents interact

face-to-face with customers

to explain the product and

service offering.

❚ Think Big

Mobile money services are generally offer numerous different services, but

categorized in terms of the transaction there’s no correct sequence or starting

stakeholders: person-to-person (P2P) is point; the only requirement is that the

perhaps the most basic and currently the service meet the customer’s needs. Know

most common. But many possible the customer, know how they spend

applications and permutations exist their money, and how they want to

among governments, businesses, spend their money. is can also mean

customers and all stakeholders within the knowing how a customer wants to

ecosystem, both horizontally and receive or send money. For Zain this

vertically. Opportunities for mobile meant approaching Coca-Cola in

money exist throughout the customer Tanzania—whose big, red trucks

spectrum, from the base of the pyramid advertised a driver carrying cash along

on up, says Roberto Rittes, Director for insecure, rural routes—and asking, “Do

Oi Paggo, with products ranging from you have a cash collection problem?”

traditional remittance services to With drivers receiving payments using

microinsurance or government benefits mobile money, Coca-Cola’s problem

payments. found a solution and Zap stimulated the

An expanding deployment will likely broader ecosystem. Knowing how

Introducing Mobile Money Services in Diverse Markets

In Kenya, Safaricom piloted M-Pesa as a a critical customer mass, Safaricom is necessary for creating a rich mobile

service for microfinance borrowers to now addressing the demand for savings commerce experience. Going beyond

repay loans, but discovered that users products frequently seen in unbanked “2D” services is the sort of innovation that

wanted remittances. M-Pesa refocused markets. Ramsden believes is necessary to really

to meet this stronger demand and quickly Developed markets need a different excite customers and stimulate demand in

gained over 9 million customers. Safaricom value proposition. O2, for example, developed markets, where people are

is now expanding its offering by partnering targeted London to pilot its O2 Wallet, highly banked and already use numerous

with Equity Bank to launch M-Kesho, an which combined three industries by placing financial services. Micro-savings accounts

interest-bearing micro-savings account held an Oyster NFC transport card and a aren’t going to excite customers in London,

by Equity Bank and offered to M-Pesa Barclay’s credit card into a NFC enabled and mobile wallets currently lack demand

clients. M-Kesho will be a powerful draw mobile phone. This created the “3D” in Kenya. The right mobile money service is

for customers looking for alternatives to experience that Andy Ramsden, Head of the one that fits the market and is

“saving under the mattress.” First reaching Payment Products at O2, describes as introduced at the right time.

MOBILE MONEY SUMMIT 2010 111 STRATEGY

Coca-Cola wanted their drivers to everywhere, and Olga Morawczynski,

receive money made it an easy entry, says Financial Literacy Project Manager at

George Held, Group Marketing the Grameen Foundation’s AppLab,

Director, Zain, who advises: remember reminds us that the poor are active

corporate customers too, not just money managers too, who show

end-users, when looking for market particular demand for savings products.

opportunities. But opportunities are

❚ Start Small

e first service should be one that Officer at Orascom Telecom Holdings,

enhances the provider’s image or bottom and “once you have gained your

line. It does not necessarily need to be consumers’ confidence, and they are

complex or game-changing. MTN hooked to a simple but useful product,

Uganda introduced a straight P2P they will demand more from your

money transfer service to bring people technology.” Prompted by this demand,

onto the platform, says Richard Mwami, the evolution of a company’s mobile

Head of MTN MobileMoney in financial services roadmap for the

Uganda. For now, they’re staying small, unbanked could evolve as follows:

waiting for a critical mass of subscribers sophisticated payments; money storage

and double-digit penetration rates or accumulators; interest-bearing savings

REGULATORY TAKEAWAYS

• Who’s accountable for

regulatory compliance: before offering more services. Rapidly products; access to credit; and finally

the bank or the MNO? introducing new products can over- insurance. However, a mobile money

Different environments whelm customers or risk diluting the strategy targeting a financially

have different mandates.

In Mexico, banks are

service quality as managerial capacity sophisticated customer segment or

held accountable; in the may be forced to address competing developed markets may target

Philippines, the MNO must demands across multiple new market convenience services and develop in a

see that agents follow segments. “Do a few things, but do totally different direction. In Shawki’s

protocol. The regulator

must clearly articulate

them exceptionally well, as many opinion, real success will happen at the

which party is ultimately customers don’t tolerate complexity and crossroads of both segments. Again,

responsible in order for lack of focus,” says Hesham Shawki, there is no one recipe for product

partners to define clear Chief Innovation and Partnership sequencing.

roles and responsibilities.

❚ Scale Fast

“Achieving critical mass is difficult—but government-to-person (G2P) strategy

it’s the way to achieve success,” says offers access to a large customer base. A

Rittes, who recommends establishing critical mass is just the start. “You may

partnerships with large merchants first, get customer uptake with a given

thereby providing customers with more product; but you may not get the

opportunities to use the product at the volume you really need without going

earliest stages. Indeed, focusing on beyond basic product offerings,” says

merchant buy-in is one way to scale a Mark Pickens, Microfinance Specialist

mobile money operation quickly for CGAP. Spanning customer segments

because if the merchants are convinced, and stakeholders is a crucial next step.

consumers will use and adopt e-money. True scale is marked by integrating the

Or in the case of Roshan, focusing on a entire mobile money ecosystem.

12 MOBILE MONEY SUMMIT 20102 MARKETING

Key Message: Know the customer to craft a message that expresses the

value-add of a service in a way the customer values. Then drive acquisition

and usage with a strong marketing campaign.

“Consumers today demand cash because it’s what they are used to. We have to help

them understand that cash is not always the only option and perhaps not always the

best option. It is our role to educate consumers that mobile money is safer, more secure

and more convenient.”

ZAHIR KHOJA, EXECUTIVE DIRECTOR OF MOBILE COMMERCE, ROSHAN

MOBILE MONEY SUMMIT 2010 132 MARKETING

How do you drive customer acquisition

and usage?

❚ Know the Consumer: Sending the Right Message

Understanding the market is critical where people already do mobile airtime

for identifying strategic product transfers, so they are accustomed to

opportunities, but to drive uptake and sending something of value via a mobile

usage within the market, you must know phone. is provides a lever for

the customer. is is a necessity for marketing P2P-type services. Under-

successful marketing and strategy, standing the customer goes beyond

echoed repeatedly at the Rio Summit. providing the right service; it means

As a speaker put it, “You have to know knowing how to successfully

your customers. If you do not know communicate with the customer by

“The final polish that them, you cannot do business with offering that service in a way that

them.” resonates with what the customer already

converts a diamond

Knowing what potential customers in the understands, and ultimately, what he

from a rough stone market already do can reveal strong levers wants to accomplish.

to a precious gem in for driving adoption of mobile money Use-based marketing messages have

the eyes of consumers services. In Kenya and Uganda, for proven successful for many mobile

lies in direct and example, Bruno Akpaka, General money services precisely because they

Manager of MobileMoney for MTN appeal to what a customer already wants

effective marketing,

Ghana, explains that sending money back to do. Simple ideas, like MTN Uganda’s

once fundamental home is already a deep cultural “now you can send money to your

elements such as characteristic. Remittance services are parents,” offer a ready solution for a

organization of the immediately understood, and relatively customer seeking remittance services

company, distribution little effort needs to be spent educating without dwelling on the service itself.

the customer about something they However, in many circumstances

points and a certain

already do, already know and already potential customers may be unaware of

regulatory framework value. By comparison, in many West what they can do, making lifestyle

are in place.” African countries, he says, money may be messaging a better approach. Yellow

remitted, but without the same cultural Pepper’s ad campaign offers customers

Rizza Maniego-Eala, President,

G-Xchange Inc. expectations: “It’s a help, but money “more time for yourself,” through services

transfer will not be the main driver in that provide greater convenience by

these markets. Each market needs to limiting the time spent waiting in line at

identify what will be the main driver.” the bank or making trips to the utility

Knowing these types of cultural norms is company to pay bills. e advantages

instrumental in effecting customer uptake of these conveniences are readily

and demand for mobile money services. understood. It’s a message that resonates

For example, Haridas Nair, Area Vice with customers, and for many, “more

President of mCommerce at Sybase 365, time for yourself ” means more time to

Inc., points to Latin American markets, earn money. For Roshan’s M-Paisa in

14 MOBILE MONEY SUMMIT 2010Afghanistan, although the service also make a purchase or another possibly

offers time savings benefits—and even time-consuming transaction, you have

safety benefits by enabling customers to more time to stay at home. Lifestyle

potentially avoid difficult or dangerous benefits resonated strongly with M-Paisa’s

transit—initial marketing campaigns that customers: by staying home and spending

focused explicitly on ideas of convenience time with his family, a father is seen as

fell short. “Marketing convenience is being a better father, explains Khoja.

difficult in Afghanistan,” says Zahir e successful marketing campaign

Khoja, Executive Director of Mobile communicates the service in terms of

Commerce and Product Marketing for what the customer already values, and is

Roshan. “e population has never characterized as providing something the

experienced it. ey do not know what it customer already desires.

tastes like.” But if you’re not going out to

❚ Marketing, Marketing, Marketing

e right message will grab the and usage is critically driven by

customer’s ear, but this is only a piece of traditional marketing, and lots of it.

the puzzle: whether broadcasting that Branding is one of the first issues to

message (above-the-line marketing) or address in developing a strong marketing

reaching out to individuals (below-the- campaign: the customer must trust the

line marketing), customer acquisition message and the product. e strongest

Differentiating Your Product From the Competition

A Zain TV advertisement shows a proposition with a message that resonates out to his mother, who is working in the

payments evolution from shiny shells to with the customer. That message should garden back home. Clearly cash doesn’t

plastic cards, stating, “throughout history, also help distinguish the product from the fly: M-Pesa is better. Different services

money has changed hands and forms.” competition. Although multiple operators and markets will have different value

The next change comes in the form of may offer mobile money services, today, propositions, but articulating why mobile

Zap, bringing a “revolution in commerce.” the real competition is cash. M-Pesa’s Send money is better than cash is both a

The message articulates that Zap is just Money Home campaign differentiates compelling message and one that

another form of money, but better itself from cash with a TV spot showing a promotes the broader adoption of

money. A marketing campaign needs to young man in an office sending money e-money.

communicate the product’s value home: cash bills fly from his cell phone

MOBILE MONEY SUMMIT 2010 152 MARKETING

brand in a partnership should lead in the Uganda 1,000 existing agents bolster its

target market, although when multiple overall sales force.

partners are strong in the market, a Promoting ongoing service use is as

co-branded mobile money service may critical as customer acquisition.

provide a better vehicle. And while a YellowPepper encourages customer

brand name may help bring a customer buy-in up front by charging a

to the table, the technology device or registration fee that preloads an

REGULATORY TAKEAWAYS

• Customer acquisition may platform itself is the ultimate custodian equivalent amount of airtime. By

be accelerated with of the marketing campaign: it is the first putting something at stake, the customer

proportional KYC experience a customer has upon is incentivized to try the service at least

regulation. Unbanked and

registration. For many customers in the to get her money’s worth. Loyalty

under-banked customers

may face financial exclusion mobile money space, a complex user schemes and airtime bonuses also

because they lack ID cards interface can immediately undermine promote ongoing usage, as do ancillary

or the ability to verify IDs customer uptake and belief in the incentives, like micro-health and burial

due to absence of faxes,

product. insurance coverage that YellowPepper

photocopiers or even

electricity. This segment Nontraditional marketing channels customers receive with their initial

engages in low-risk can often be very effective ways to reach registration fee. However, incentivizing

transactions, often below new mobile money customers, where the players in the ecosystem can have

$20. Regulators need to

target market is more receptive to significant knock-on effects for

consider alternative KYC

requirements for these below-the-line marketing. For customers stimulating customer uptake and usage.

groups, allowing further who may be illiterate, who lack any For example, if wholesale suppliers offer

customer uptake while experience with formal financial tools, or shopkeepers discounts or inventory

keeping risks low.

who simply live in rural areas difficult to bonuses when making purchases using

• For providers, incentivizing

reach with broadcast marketing, direct mobile money, these small shops will

an agent network as a

marketing and sales force is sales engagement is the most successful encourage mobile money uptake among

also a KYC issue. It must be channel. MTN Uganda, for example, their customers simply by providing the

done properly, to minimize credits its direct sales model with its ability to transact using mobile money

perverse incentives: agents

soaring growth. Over 2400 trained sales services. is is the ultimate marketing

eager to earn a new

customer commission may agents travel significant distances into tool: providing customers more

disregard KYC requirements, rural areas to promote mobile money opportunities to buy, spend and send

presenting a risk far greater and educate communities. By focusing using e-money. “We’re introducing a

than merely signing up

on below-the-line methods, MTN new form of money into society:

frivolous accounts.

Uganda achieved just short of one electronic money,” says Andi Dervishi,

million customers in its first year. MTN Practice Lead, Electronic Payments and

Ghana employs other below-the-line Marketplaces, IFC, “and every time such

tools, such as viral marketing and an endeavor has been attempted, success

demonstration effects, by promoting depended on whether sellers or

service use and word-of-mouth merchants accept the new money as

advertising among employees, their payment. Marketing that will drive

families and existing customers. acceptance by one seller can trigger

However, one of the strongest adoption by a much larger number of

opportunities for personal engagement buyers. Merchants influence consumer

is leveraging existing agent networks to behavior and are the ‘queen bees’ of a

both sell and aggressively promote transacting community.”

mobile money services: for MTN

16 MOBILE MONEY SUMMIT 20103 OPERATIONS

Agent Network Development: Agents are the face of the mobile money service to

the customer, playing the vital roles of customer education, sign-up and transaction

support. A customer’s interaction with an agent creates the trust that is critical to

adoption and use. Building a trustworthy, ubiquitous, liquid and profitable agent

network is key to a successful deployment.

Enabling Technology: The technology platform is what enables mobile money

operations to succeed: processing transactions, mediating regulatory requirements and

binding partners and customers together. Technology will also help spur NFC-integrated

phones and broader e-money ecosystems.

“We don’t use the term ‘agents,’ but ‘merchants.’ The reason we believe the merchant

is very important is the sustainability of the business model. If a person sells orange

juice or magazines, and at the same time he is using mobile payments as a means of

payment, it makes a sustainable business versus if his job is just to perform cash-in and

cash-out.”

GEORGE HELD, GROUP MARKETING DIRECTOR, ZAIN

MOBILE MONEY SUMMIT 2010 173 OPERATIONS

How do you develop and implement an

optimal agent network strategy?

❚ Build a Trustworthy, Ubiquitous Network to Achieve Uptake

If customers, especially the poor, are to goods companies. In others, mobile

adopt mobile money services, they must money providers need to build

trust that their money is safe. Selecting relationships from scratch with

trustworthy agents who can educate independent “mom and pop” shops or

customers about the value of shifting from select agents within existing mobile phone

cash to e-money is key. is process airtime distribution networks. GSMA’s

begins when agents sign up customers research indicates that successful operators

and continues when they facilitate grow agent networks in phases.7 In the

transactions. Easy access to agents for first phase, an adequate number of agents

these services helps customers to need to be recruited throughout the

experience the principal benefit of mobile market to support launch. In the second

money: convenience. Types of agents, phase, resources need to be redirected

however, vary by country. In some from agent recruitment to customer

countries, it is easy to leverage the large acquisition. In the third and final phase,

retail footprints of supermarkets, numbers of agents and customers need to

pharmacies and fast-moving consumer grow in parallel.

“If a person wants to ❚ Agent Liquidity and Profitability are Key to Customer Trust

cash out his salary and Mobile money providers should pay electronic money for daily transactions.

the agent does not strong attention to how their agents is reality makes it important for agents

have the money, the manage liquidity to ensure sufficient to have sufficient cash on hand.

reserves of e-money are available for Ultimately, as Serge Elkiner, President of

SMS message on his

cash-in transactions, such as sending YellowPepper, notes, “enabling customers

phone has no value. remittances, and physical cash for to use the system not only to cash-out, but

Agent liquidity is cash-out transactions, such as receiving also to make payments and purchases, is a

paramount to the remittances. An agent’s inability to way to address the liquidity challenge.”

success of mobile perform these transactions could Agent liquidity and profitability are also

negatively impact customer trust. Richard closely related since maintaining fixed

money.”

Mwami, Head of MTN MobileMoney amounts of cash and e-money reserves, or

Zahir Khoja, Executive in Uganda, notes, “if your customer walks float requirements, comes at a cost. An

Director, Mobile Commerce into the agent, he expects to find agent can face increased operating costs as

and Product Marketing, electronic money and cash. If he cannot a result of frequent trips to the nearest

Roshan find the money, he won’t come back.” bank or other lender to withdraw cash;

Currently, customers in most mobile high interest rates on working capital

money deployments are performing more loans needed to main float; or theft of

cash-out than cash-in transactions since physical cash by employees at an agent’s

there are not many places where they can store. All these factors can eat into an

use their mobile phones to pay with agent’s profit margin. Recognizing that

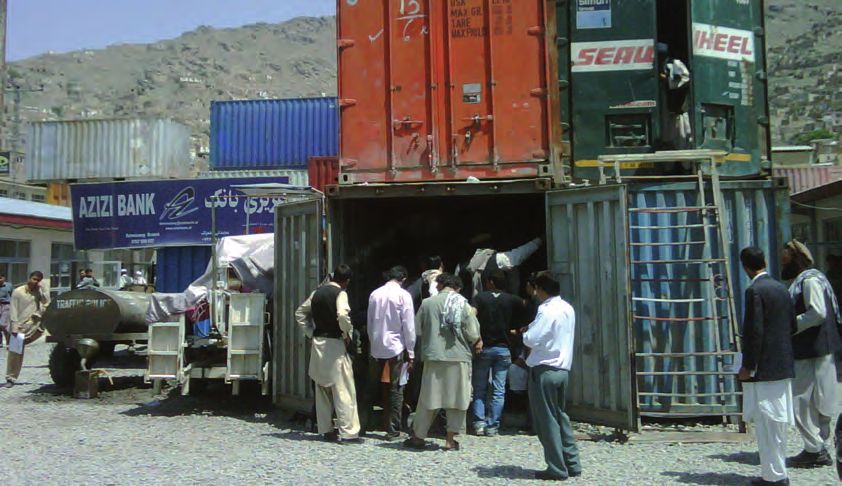

18 MOBILE MONEY SUMMIT 2010M-Paisa agents in

Afghanistan leverage

Roshan’s partnership

with Azizi Bank to ease

liquidity challenges.

agents in rural areas face bigger challenges and other services to ensure a profitable

in managing liquidity, some mobile agent model require judicious structuring.

money providers are offering higher In general, an agent is likely to stop

commissions for cash-out transactions to offering mobile money services if it’s

compensate these agents for the extra unprofitable. is in turn may lead a

time, effort and money needed to customer to lose trust in mobile money’s

maintain the float. Commissions for reliability.

customer registration, cash-in, cash-out

❚ Agent Training and Management Ensure a Positive and Consistent

Customer Experience

“One must build in the cost of agent an independent company, Top Vision, to

training and management to ensure that train its M-Paisa mobile money agents on

agents continue to adhere to established KYC/AML requirements to ensure

procedures, that the system remains intact, regulatory compliance; branding and

and that customers build and maintain marketing to increase the visibility of the

trust,” says Elkiner. While some providers M-Paisa service and customer foot traffic;

use in-house staff for agent training and and liquidity management to ensure agents

management, others outsource this have sufficient float to maintain a positive

function to third parties. Mobile network and consistent customer experience.

operator Roshan, in Afghanistan, has hired

Approaches to Managing Agent Liquidity Challenges

“There’s limited trust in the banking its preferred agents about the amount of branch, so agents don’t have to travel far

system in Afghanistan today, due to money to be transferred and the locations to convert e-money into cash during high

historical losses. We have one chance to where agents will need to have cash on demand periods. In addition, if an M-Paisa

prove the value to the customer. We need hand. These preferred agents, in turn, agent runs out cash, M-Paisa customers

to build this trust,” says Khoja. Roshan contact other agents in their areas may visit the Azizi Bank branch to convert

relies on a preferred agent approach on regarding expected cash needs. Roshan has their e-money into cash, which is especially

salary disbursement day to ensure that also partnered with Azizi Bank, one of the important on salary disbursement days. In

members of the Afghan National Police country’s largest banks, which has areas where there are no rural bank

and employees of other entities availing of extensive nationwide reach, to ease the branches, Roshan ensures that a strong

M-Paisa’s salary transfer service are able to liquidity burden. About 70% of M-Paisa emphasis is placed on liquidity

cash out. In this approach, Roshan informs agents are within reach of an Azizi Bank management during agent training.

MOBILE MONEY SUMMIT 2010 193 OPERATIONS

• Regulators seeking financial with mechanisms to ensure its own. This approval for a

REGULATORY TAKEAWAYS

inclusion should resist regulating customer integrity, protection network-based license allows

m-money agents in the same way and security. The Philippines G-Xchange Inc. to expand its outlet

as traditional banks, since the exemplifies what can be achieved network faster while taking full

former are often micro and small by progressive regulation. In early responsibility for the KYC/AML

businesses who cannot bear the 2010, the Central Bank of the requirements of its network,

high overhead costs that can stem Philippines allowed G-Xchange continuing to fully comply with

from compliance with complex Inc., Globe Telecom’s m-commerce regulations that will ensure

regulations. Progressive regulatory subsidiary, to extend its remittance financial integrity and the

frameworks balance the ground license to its accredited agents protection of consumers.

realities of branchless banking instead of each agent applying for

How does technology enable a successful

mobile money operation?

❚ The Technology Glue

“Technology is what makes these projects careful consideration, both because it

possible,” says Aletha Ling, Executive shapes the customer experience and

Director, Fundamo. But mobile money because there is relatively little industry

providers are not selling technology; in precedent to guide developers. Mobile

fact, the platform should remain largely money operations need to consider the

transparent to the user. e service applications layer from the outset or risk

platform sits behind the scenes, yet acts alienating customers or limiting future

as the glue that binds the mobile money service offerings. “Many deployments

ecosystem together. Well-established today fall short and do not engage

technology already connects the broader application developers to the extent that

financial system and underpins global they should,” according to David Sharpe,

telecommunications, but two additional Head of Products, Digicel Haiti. “Banks

layers are needed for mobile money and MNOs need to do this, but the level

solutions: first, one to connect finance of thought required for applications that

and telecommunications, and second, an sit on top of mobile money hasn’t gone

applications layer that connects the in.”

customer. is applications layer bears Although attention must be given to

“An MNO as a carrier is an enabler. Google and Apple

provide the platform, but put out to the development

community for applications software. If Apple didn’t have

thousands of applications, it wouldn’t succeed. The MNO

needs to provide applications on top of its platform, too.”

David Sharpe, Head of Products, Digicel Haiti

20 MOBILE MONEY SUMMIT 2010Agents play a key role in

educating customers

about the value of

shifting from cash to

e-money.

the applications layer, the first connective call may fail,” said a speaker, “but a

layer is perhaps more critical: the financial transaction cannot go down.”

technical platform that turns money And this means flawlessly handling

mobile. Here, both regulatory and potentially millions of transactions an

business requirements are major hour, and handling them with absolute

considerations for the platform’s security. “Security is the backbone

technical specifications. Mobile money of mobile money services,” says

solutions are beholden to the same Jean-Pierre Gressin, Head of Alliances

security and reliability mandates as & Partnerships, Oberthur Technologies,

traditional financial services. “A phone and lack of security carries enormous

Integrating NFC into Phones and into the Market

NFC technology started with contactless to integrate the broader e-money ecosystem.

cards and is now moving to fully-integrated Pilots such as Tap and Pay help

mobile phones that will enable the full demonstrate that electronic wallets

range of mobile and financial services that implemented through NFC-integrated

comprise the electronic wallet. ViVOtech, phones have the potential to redefine the

for example, is working to establish these merchant-customer relationship to be more

electronic wallets in the marketplace by convenient, more targeted and more

developing mobile payments, loyalty, personalized. Consumers will benefit by

merchandising and marketing applications having everything in one place, be able to

software for existing and NFC-enabled enjoy an enhanced shopping experience,

mobile devices. By also deploying over making quick payments and seeing lower

750,000 contactless and NFC payment risks associated with loss, theft or fraud.

terminals across 35 countries, ViVOtech Customers may also take advantage of

is providing both the software and personalized in-store offers by tapping their

infrastructure necessary to bring mobile NFC phones to smart posters, which similarly

payments into the retail world. This will benefits merchants, who can engage in

offer consumers numerous payment one-to-one marketing, offer instant,

conveniences and give merchants new individualized offers, and better track

payment and marketing channels. customer loyalty. With networks and mobile

ViVOtech’s wallet software technology money services intermediating these

drove Citi’s Tap and Pay pilot, for example, benefits, operators will see additional

and this is helping to push payment systems revenue sources as NFC-integrated phones

to include and go beyond m-money services and related services take hold in the market.

MOBILE MONEY SUMMIT 2010 21You can also read