UPI: A Brilliant Technology Idea Executed Poorly - ACS Publisher

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UPI: A Brilliant Technology Idea Executed Poorly

online banking and mobile commerce. So in our developing

Ankit Dhamija*

economy, people also need a less complex and secure mode of

Deepika Dhamija**

payments and mobile banking.

A According to reports published by Business Standard [1],

cashless payments in October 2016 increased 22%, when

Till a few years ago, nobody imagined that mobile phones would compared to October 2015, indicating that Indians have been

be used to transfer money and complete shopping transactions. steadily more accepting of various digital payments modes since

But now, one doesn't really have to visit a bank, stop by at an last year. Mobile banking transactions grew 175%, while money

ATM, or carry a plastic credit or debit card to make purchases. transacted using mobile banking grew 369% from October to

Mobile banking through mobile apps now days are on boom. The October, according to an India Spend analysis of Reserve Bank

continuous increase in mobile banking users is due to of India (RBI) data. These statistics tell that post demonetization;

technological advancements which has restored and increase our population is slowly but steadily, inclining towards using

the faith of users towards mobile banking and different payment digital modes of payments.

modes. In a developing country like India, where mobile users A recent development in this context was made easy with a new

are growing at very fast speed, because of the low cost smart mode of payment-Unified Payment Interface (UPI) which allows

phones and people can also afford that technology, the problems money transfer between any two bank accounts by using a smart

and complexity will also growing rapidly. Users expectations in phone. UPI was launched by National Payments Corporation of

terms of speed, convenience and security are now a days a major India with Reserve Bank of India's (RBI) vision of migrating

concern. The technologies like NEFT, IMPS, RTGS etc. have towards a 'less-cash' and more digital society. According to UPI

been functioning very well but what next? What is the future of procedural guidelines issued by NPCI [2], “The Unified Payments

mobile banking? To make sure that mobile payments stay in the Interface (UPI) offers architecture and a set of standard

market in future and it is used by most users, the national Application Programming Interface (API) specifications to

payment corporation of India has initiated a new payment system facilitate online payments. It aims to simplify and provide a single

called as unified payment interface(UPI) that make online interface across all NPCI systems besides creating

payments much easier without requiring a digital wallet or credit interoperability and superior customer experience.”

or debit card. You either need to know the other's person MMID

(mobile money identifier) or a Virtual Payment Address (VPA) The key aspects of the Unified Payments Interface are [2]:

and phone number. All these features of UPI will surely boost the

confidence of e-commerce and m-commerce customers as they a) The Unified Payments Interface permits payments via mobile

won't have to go through the hassled process entering the app, web etc.

credit/debit card information every time and also no need of b) The payments can be both sender (payer) and receiver

remembering the bank account numbers, IFSC code and several (payee) initiated.

pins associated with several bank accounts. c) The payments are carried out in a secure manner aligned with

the extant RBI guidelines.

Keywords: Mobile banking, UPI, NPCI, ecommerce, d) The payments can be done using Aadhaar Number, Virtual

mcommerce, payment Address, Account Number& Indian Financial System code

I (IFSC), Mobile Number & MMID (Mobile Money Identifier).

e) The payment uses 1-click 2-factor authentication, Biometric

The development of smart phones has gone and replaced a few Authentication and use of payer's smart phone for secure

things we grew up with: the watch, the alarm clock, the tape credential capture etc. are other unique features.

recorder, music players, and it seems that very soon, we can add UPI allows a customer to pay directly from a bank account to

cash and wallets to that list. It's hardly a surprise. Payment different merchants, both online and offline, without the hassle of

methods have been morphing through various channels: typing credit card details, IFSC code, or net banking/wallet

from cash to cheques, to credit cards and debit cards, and now to passwords [3].

*Assistant Professor, Amity Business School, Amity University Haryana

** Assistant Professor, Amity College of Commerce, Amity University Haryana

Trinity Journal of Management, IT & Media ISSN 2320 - 6470 December, 2017 / Page - 32The paper is further organized as follows: The next section password. So if you receive any unauthorized request, it can be

presents the objectives formulated for the paper and the easily rejected.

research methodology adopted to achieve the mentioned 10. If all the steps go correctly, transaction will be successful.

objectives. In the next section, a technical model depicting the 11. Money will be directly debited from your bank account and get

working of UPI and the role & responsibilities of various parties in credit into the bank account of the service provider. In this case,

its successful implementation is explained. Further, we analyze grocery store owner.

the penetration level of UPI since its launch. The next section tells 12. Thus neither the grocery store owner nor you would be

about the initiatives taken by various organizations to boost UPI. required to share each other's bank account details. And there is

Finally, the various barriers and problem areas that restrict UPI no need of swiping debit/credit card, keying in your confidential

adoption are highlighted. Thereafter, Future research directions PIN.

and the conclusion of the paper will follow.

O R M

Following objectives have been formulated:

Ÿ To understand the working of UPI and identify the role &

responsibilities of different parties for successful

implementation of UPI.

Ÿ To understand UPI's penetration among Indian smart phone

users to gain insights about its preference by users.

Ÿ To identify the grey areas that restricts UP adoption.

Methodology

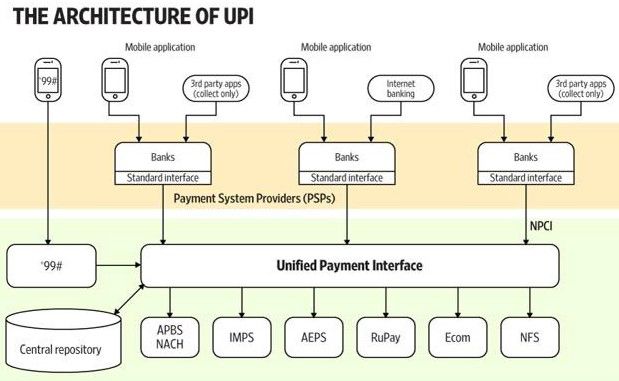

To achieve the above mentioned objectives, the authors intend to Working of the Technical Model

use descriptive research methodology. This is due to the fact that This technical model depicts UPI as a layer built on top of all

the topic under consideration is a relatively new one and the best other payment mechanisms including IMPS that gives an idea of

way to understand it and analyze it would be to do an exhaustive the wide spectrum of UPI. The UPI system will be accessed by

literature review from various news articles, published reports in the users through mobile apps that the users will be required to

print and electronic media and so on. Then, the authors will do a install on their smart phones (those who want to use it on the

careful analysis of the studies made and bring out their move, through smart phones) and also through web platforms

observations and analysis of the reports studied. (those who want to use it on desktop/laptop machines). The

users will initiate their transactions through any of the above said

W UPI medium and banks act as a very important link in this system to

Below is a step by step working of UPI system with an example. function properly as linking of user's mobile number and bank

accounts is a prerequisite for this system to function. After this

1. Banks will have to first enable UPI system linking, each user is provided with a 'virtual address' which will act

2. Customers will have to ask their banks to connect them to the as a 'first factor' in transaction authentication. Then, the users are

UPI system. supposed to create their passwords/pin, which will act as 'second

3. For making any transaction, two options are available i.e. you factor' authentication. Here, the role of payment Service

can either global or local address. Providers (PSP's) becomes important. The PSP's include

4. Global address means mobile number, Aadhar number and various online merchants and organizations who are in

bank account number. ecommerce business and who are willing to collect money from

5. Local address means a virtual address, which banks will their customers in an online mode. Presently, they are accepting

provide you. payments through debit/credit cards, net banking, COD, mobile

6. So if you want to make payment through smartphone, let's say wallets, NEFT, IMPS, cash cards, gift vouchers etc. They need to

to a grocery store owner then just provide your virtual address to modify their payment portal (on both mobile and web platform)

the owner. Normally you provide either the bank account number and make provision for accepting payments through UPI. They

or swipe your credit/debit card and enter security PIN. can do so very easily by just giving UPI as a payment option

7. Owner will then enter this address in his mobile phone. along with all other existing options, as depicted in the figure

8. You will then receive message on your cell phone requesting below.

authentication.

9. You need to then authenticate this transaction by entering a

Trinity Journal of Management, IT & Media ISSN 2320 - 6470 December, 2017 / Page - 33ROLES AND RESPONSIBILITIES OF DIFFERENT PARTIES conducting regular banking operations. That is, those banks

have not launched a separate UPI app and have just

integrated the UPI features and functionality in their existing

app.

Ÿ Then the authors have gone to the Android platform based

Google Play Store and gathered data of the number of

downloads of UPI apps and regular app for each of the banks

offering UPI service.

Ÿ After this data gathering, various types of analysis have been

made.

Government Agencies: NPCI is the owner, network operator,

service provider, and coordinator of the UPI Network. NPCI

reserves the right to either operate and maintain the UPI Network

on its own or provide or operate necessary services through third

party service providers.

PSP (Payment Service Provider): The PSP shall ensure that its

systems/ infrastructure remain operational at all times to carry

out the said transactions. The PSP shall upgrade systems and

message formats in a prompt manner, based on regulatory

requirements or changes mandated by NPCI. In case of UPI

banks are only the only Payment Service provider. The table

below shows the details of banks with their UPI app names.

Telecom Companies: As UPI only works by sending a virtual

address/global address on mobile phones. So telecom

companies play a major role in transactions through UPI.

Merchants: Merchants are the major entities when customers are

paying their bills through UPI. Taxi aggregators like Uber and Ola,

food ordering services like Zomato and Food Panda, online

grocery shops like Big Basket will be able to take advantage of

the UPI system. Going forward, such companies should be able

to register its identifier on the UPI system and receive funds from

a customer's bank account through the UPI

IT Experts: Our IT experts play a major role in UPI. They are

giving their inputs in terms of Apps development, ecommerce

sites etc.

Customers: Customer is the king of UPI because he is the only

person who uses this UPI application without the hassle of typing F

card details, passwords, pin no etc. The table mentioned above has two columns that are very

important and relevant with respect to performing an analysis of

UPI PENETRATION UPI penetration among Indian smart phone users. The following

To achieve objective 2 which is to understand the penetration of can be deduced from the above table:

UPI among Indian mobile banking users, the authors have Ÿ Axis Bank and State bank of India are the two banks whose

adopted the following strategy: UPI app is most downloaded from Google play store, i.e. more

Ÿ In the first step, a list of all banks offering UPI mobile app is than 1 million downloads.

prepared along with their app names. In few cases, some Ÿ The above table shows that there are 09 banks (United Bank

banks have same mobile app for UPI which they have for of India, UCO bank, South Indian Bank, OBC, YES Bank,

Trinity Journal of Management, IT & Media ISSN 2320 - 6470 December, 2017 / Page - 34Ÿ Bhartiya Mahila Bank, Karnataka Bank, TJSB Sahkari Bank Eaypay app: ICICI Bank has launched 'Eazypay', an app for

and Allahabad bank) that have not rolled out a new UPI app; merchants, retailers and professionals to accept payments on

instead, they have added the UPI functionality and features in mobiles from multiple digital modes. Any current account holder

their existing app itself. That is the reason for 100 % value of ICICI Bank can instantly download the Eazypay app and start

coming in the last column. using it, Also, the facility can also be used by non- ICICI Bank

Ÿ A strange fact that comes out from the above analysis is that customers.[7]

banks with customer base more than 5 million (Axis Bank) and PhonePe: Mobile payments start-up PhonePe Internet Pvt. Ltd,

bank with customer base just more than 50000 users (DCB which is owned by Flipkart, has launched its app based on the

Bank) have same percentage of UPI app downloads i.e. 20%. unified payment interface which is powered by Yes bank. [8]

This figure can be alarming for Axis Bank and at same time, Mobikwik: MobiKwik has also announced the launch of UPI

motivating for DCB as they can take solace that despite their (Unified Payments Interface) on its platform. MobiKwik users can

small customer base, they have been able to match up to Axis now put cash in their wallet with e-cash using UPI. [9]

Bank standard.

Ÿ 9 banks have got user rating of 4.0 or above and strangely, GREY AREAS & PROBLEMS IN UPI IMPLEMENTATION

SBI is at the lowest with rating of 2.9. As UPI app launched in August 2016, with several advantages

but it comes with a set of limitations also.

No app updates: Unified Payments Interface or UPI has become

a sort of buzzword since the prime minister's demonetization

announcement on 8 November last year. We have seen an

increase in the number of UPI focused apps released by banks.

But according to a latest report in The Economic Times, around

half of the total UPI apps on Android have not been updated in the

last 45-55 days. The report goes on to state that around six out of

the 38 apps tested, were not updated in 150 days according to

data from Cashless Consumer. [10]

UPI A M Now, how frequently an app is updated should not ideally be an

The following points mentioned below affirm the adoption of UPI indicator of how safe or unsafe it is. We all know that not every

by merchants too: app update deals with security issues. According to app

Yatra.com: Yatra.com is the first in the online travel agency developers we have spoken to in the past, most software goes

segment to offer UPI on its platform. It has tied up with ICICI Bank through iterative development cycles. So with this issue we can

for technical integration of the payment method. While UPI as a identify that this UPI will not be successful if a regular updates will

payment option is only available on Yatra's website now, work is not be available.

on to launch it on the firm's mobile app shortly. One benefit of this No standardization: If you look at the graphical user interface of

system is the lower merchant discount rate (MDR), or the fee a UPI apps offered by various banks, you will find that each of the

merchant has to pay a bank to access its payment infrastructure app has its own design and functionality which creates confusion

[4]. for customers as to which app is best for them. As per NPCI, a

Razorpay: Razorpay software pvt ltd has also introduced UPI to user is free to choose any app they feel comfortable with, hence

accept payments through UPI. [5] the users tend to opt for that app with which they have a bank

Paytm: Paytm has been busy launching several new features to account associated with. Later on, they may feel that the GUI of

lure users to shift to mobile wallets. To further this effort, the digital this native bank's UPI app is not much user friendly as they had

payment service has now added support for United Payments thought and they uninstall it & do not enroll for any other app and

Interface as well. The integration of UPI will inadvertently help thus a valuable user of UPI platform is lost in the process. [11]

users transfer money into their Paytm wallets more easily. Users

can now add money to their Paytm Wallets using their unique UPI Less Branding & Promotion: The concept of wallets predates UPI

ID. When adding money, a new option called UPI now shows up - for example, Paytm's wallet was introduced in 2014, and the

on the Paytm app, alongside netbanking, debit card, and credit Paytm brand has been around since 2010, whereas UPI was

card options. Once they enter their UPI ID on the payment page, introduced just last year. There's also the fact that most wallet

a collect-money request is sent to their UPI-enabled apps on their apps serve more than one purpose. You can use them to

smartphone. After they accept the payment request and enter recharge your phone, pay your electricity or gas bills, and so on.

their pin code for UPI transactions, the transaction is complete, Some of the apps also include features such as ticket booking,

and the money is instantly added to the Paytm wallet. [6] and e-commerce. Some UPI apps also offer similar functions, but

Trinity Journal of Management, IT & Media ISSN 2320 - 6470 December, 2017 / Page - 35they're not as well developed, and are limited in what all you can FUTURE DIRECTIONS & CONCLUSION do. Instead of a single, easily-identifiable logo, over 20 UPI apps In this paper, the authors touched upon the concept of UPI which that are operational today are competing to make their brand is a payment mechanism introduced by government of India. We known. But how many stickers do you think a typical business is presented facts about how mobile banking and UPI adoption going to be able to affix on its door or wall, to let customers know among Indian population is on the rise. Then we presented a that it is open to UPI payments? Let's say the merchant has a Axis working model of UPI and further we performed an analysis of Bank UPI QR code sticker or placard - only the people who really UPI penetration among Indian mobile users. Findings and results know how UPI works, would know that the PhonePe app on their show that the UPI adoption is on the rise and in coming years, phone can be used to make payment there too. [12] more & more users will adopt it as it is backed by the government Less Functionality on offer: While any member of the UPI and the most safest and easy way of conducting transactions platform can launch an app, the currently available apps are very online. A unique feature of UPI is that the user is not bound to use different from each other. Not all apps cover all the functionalities the app of his bank, they are free to use any app of their choice. that UPI offers. Users have reported transactions failing between However, the biggest challenge for NPCI is to make sure that UPI some specific app pairs. Some apps show counterparty name doesn't lose its strength points because of the grey areas like and account number in full on pre- or post-transaction security features on UPI apps, competitiveness with mobile confirmation screens—using the VPA was supposed to mask wallets, frequent app updates, motivation for banks and other such information. online traders etc. These issues must be resolved in order to reap These teething troubles don't help the UPI cause—the guidelines full benefits as promised by UPI. on how apps should be designed and information presented No doubt, UPI is here to stay and with more and more population should have been more stringent. joining hands to create a digital world around us, the authors are Bank's Differences on commission, controls and data: When hopeful that implementation of UPI will be very successful and it transactions originate from the UPI platform, banks don't get fees will become a preferred mode of making payments and more and or commissions on their products like debit and credit cards. more banks, users and traders will come together to provide Users don't log in to their Internet banking platforms. And they users with a great payment experience online. lose track of transactions—valuable data on customer spending REFERENCES habits, which helps them cross-sell and upsell their products. h t t p : / / w w w. b u s i n e s s - s t a n d a r d . c o m / a r t i c l e / e c o n o m y - So, while banks are going live on UPI, it is not a high-priority policy/post-demonetisation-digital-payments-are-down-15- project for them. And when they do go live, they are conveniently 116122700098_1.html burying the UPI functionality inside their larger wallet or Internet 1)http://www.npci.org.in/documents/UPI_Procedural_Guideline banking apps. s.pdf Resistance from Banks in promoting UPI: Banks are forcing 2) Sampad Swain (2016). An Indian Fintech Entrepreneur's “multi-homing” on their app users, not promoting UPI exclusively Views on UPI, Retrieved May 5, 2016, from- and leaving open the option of switching to an in-house platform. http://tech.economictimes.indiatimes.com/catalysts/an-indian- Hence, a quarter after the product launch, UPI has failed to fintech-entrepreneur-s-views-on-upi/1455 create a thick market. There just aren't enough participants on http://economictimes.indiatimes.com/articleshow/56409539.cm each side with whom other participants may want to interact. s?utm_source=contentofinterest&utm_medium=text&utm_cam Confusion on NPCI's role: NPCI has been just a platform provider paign=cppst and it has not done anything to being a platform administrator. It 3)https://razorpay.com/blog/product/2016/09/23/upi- should be an active participant in running a business, not just announcement.html creating the initial infrastructure for others to drive transactions. 4) http://gadgets.ndtv.com/apps/news/paytm-integrates-upi- No User Groups Categorization: To boost UPI, NPCI must have payments-system-for-wallet-recharge-1644455 targeted different user groups including traders, merchants and 5) http://www.siasat.com/news/icici-bank-launches-easypay- normal app users by introducing lucrative offers for each user app-merchants-accept-payments-mobile-1096267/ category and incentives to enroll in UPI. Small businesses have to pay anywhere from 1.5% to 4% of transaction value for participating in other digital payments platforms. For trading margins which tend to be in the range of 5% to 8%, such costs are unsustainable. With cheques considered unreliable, these businesses naturally gravitate to cash payments. Such businesses could have easily been an initial focus for UPI propagation and uptake. Trinity Journal of Management, IT & Media ISSN 2320 - 6470 December, 2017 / Page - 36

You can also read