VRL Logistics Gaining grounds - Company Report - Prabhudas Lilladher

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Company Report

Industry: MidCaps

VRL Logistics

Gaining grounds...

Nishna Biyani (nishnabiyani@plindia.com) Keyur Pandya (keyurpandya@plindia.com)

+91-22-66322239 +91-22-66322247

VRL Logistics

Contents

Page No.

What’s making us bullish? .......................................................................................... 4

Best placed amongst domestic listed players ............................................................ 5

Investment Rationale.................................................................................................. 6

Market leader in goods transportation with largest owned truck fleet ............................................ 6

Focused player on high-margin LTL business .................................................................................... 6

Strong cash flows and healthy balance sheet, makes VRL Special .................................................... 7

Company Background ................................................................................................. 8

Management Personnel .................................................................................................................... 8

Industry Dynamics ...................................................................................................... 9

Surface Transportation, dominated by unorganized segment ........................................................ 10

GST can improve volumes for LTL organized operators .................................................................. 12

Business Segments ................................................................................................... 13

GT segment is the focal point contributing 77% of revenues ......................................................... 13

Passenger segment consolidating, focus is on premium routes ..................................................... 14

Air Charter Business ........................................................................................................................ 15

Wind Power Generation Business ................................................................................................... 16

VRL is looking to replicate its LTL business model in other regions ......................... 17

VRL has diverse clientele with no customer concentration ............................................................ 18

Efficient Working Capital Management .......................................................................................... 19

Fuel accounts for 34-37% of total operating costs; efficient cost management holds the key ...... 19

Use of Bio-diesel and lower crude prices to help in sustain margins .............................................. 20

In-house body design facility and maintenance enhances profitability .......................................... 20

Assumptions ............................................................................................................. 21

Financials .................................................................................................................. 22

VRL revenues growing @10.7% CAGR over FY15-FY18E ................................................................. 22

Business mix tilted towards Goods Transportation segment .......................................................... 22

EBITDA Margins bounce back to FY12 levels ................................................................................... 22

Robust operating performance over the past four years ................................................................ 23

IPO well received this time, raised Rs4.7bn in April 2015 ............................................................... 23

Return Ratios and Asset turnover impressive ................................................................................. 24

Valuation and Outlook .............................................................................................. 25

Limited free-float in the sector to command premium................................................................... 26

Risk and Concerns ..................................................................................................... 27

Shortage or non-availability of skilled drivers ................................................................................. 27

Inability to pass on increase in operating cost, particularly fuel price hikes ................................... 27

Outstanding litigations and proceedings against VRL ..................................................................... 27

Annexure................................................................................................................... 28

Road Safety and Transport Bill, 2014 .............................................................................................. 28

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that

the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

December 07, 2015 2Company Report

December 07, 2015

VRL Logistics

VRL Logistics (VRL) is the largest pan-India surface logistics and parcel delivery

Rating BUY service provider with an experience of four decades in the Indian markets. The

Price Rs429 company owns and operates Pan-India a fleet of Commercial Vehicles (3713) in

Target Price Rs534 goods transportation (GT), while Bus operations (368 buses) are concentrated in

Implied Upside 24.5% Southern and Western regions of India. VRL provides general parcel and priority

Sensex 25,638

parcel delivery (less than truckload services -LTL), courier and full-truckload (FTL)

Nifty 7,782

services through its widespread transportation network covering more than 1000

(Prices as on December 07, 2015) locations. VRL is expected to have earnings CAGR of 24% over FY15-FY18E period

led by strong performance in Goods and Transport Segment. However, if reforms

like New Road Transport and Safety Bill & GST Bill gets implemented in time, then

VRL may emerge as a key beneficiary with almost double-digit volume growth as

Trading data we anticipate the LTL to garner significant volume shift likely from unorganised to

Market Cap. (Rs m) 39,143.5 organised segment. We initiate coverage on VRL with a ‘BUY’ and a TP of Rs534

Shares o/s (m) 91.2 implying a 28x FY18E PER and 13.2x EV/EBITDA FY18E. The premium is justified

3M Avg. Daily value (Rs m) 148 considering: 1) Strong management pedigree with proven track record 2) High

visibility on operating cash-flows 3) Superior returns ratios (above 25% RoE) amidst

listed logistics players 4) Steady margins on the back of lower fuel prices and

Major shareholders efficient use of Bio-diesel and 5) Strong balance sheet (D/E of 0.47x FY16E).

Promoters 69.57%

Foreign 10.78% Goods transportation leads business growth, niche play and scale at work:

Domestic Inst. 8.19% VRL, over the last decade, has shown impressive execution prowess in

Public & Other 11.46% maintaining a large fleet and growing the fleet size @6.3% CAGR to 3713

vehicles, with ~30% fleet addition happening in the last five years alone. The

company’s focus on owning the fleet makes the business asset heavy. However,

Stock Performance it brings in advantages of lower hiring and operational cost, reduced

(%) 1M 6M 12M dependence on third-party vehicles and better control over time-bound

Absolute 17.6 49.8 NA delivery. Andhra Pradesh and Telengana is its stronghold with ~20% of

Relative 20.6 54.5 NA branches/agencies in these two states alone. VRL intends to expand its network

in Northern and Eastern region over the next couple of years.

How we differ from Consensus Key financials (Y/e March) 2015 2016 2017E 2018E

EPS (Rs) PL Cons. % Diff. Revenues (Rs m) 16,712 18,151 20,417 22,617

2017 16.6 18.1 -8.2 Growth (%) 11.9 8.6 12.5 10.8

2018 19.0 21.6 -11.8 EBITDA (Rs m) 2,728 3,213 3,461 3,777

PAT (Rs m) 912 1,276 1,513 1,738

EPS (Rs) 10.7 14.0 16.6 19.0

Growth (%) 60.0 31.1 18.6 14.8

Price Performance (RIC: VRLL.BO, BB: VRLL IN)

Net DPS (Rs) 4.0 5.0 5.7 6.7

(Rs)

500

Profitability & Valuation 2015 2016 2017E 2018E

400 EBITDA margin (%) 16.3 17.7 16.9 16.7

300 RoE (%) 27.5 28.3 25.6 25.3

200 RoCE (%) 15.8 19.6 20.4 21.1

100 EV / sales (x) 2.5 2.3 2.0 1.8

EV / EBITDA (x) 15.0 12.9 11.8 10.6

0

PE (x) 40.3 30.7 25.9 22.5

Jul-15

Sep-15

Jun-15

Aug-15

May-15

Oct-15

Nov-15

Apr-15

P / BV (x) 10.3 7.2 6.2 5.3

Net dividend yield (%) 0.9 1.2 1.3 1.6

Source: Bloomberg Source: Company Data; PL ResearchVRL Logistics

What’s making us bullish?

Exhibit 1: VRL has grown its fleet at a CAGR of 12%, but revenues Exhibit 2: Asset Turnover above 2.5x in Goods Transport segment

grew faster at 24% over the last 20 yrs

2.7 Asset Turnover (x)

Turnover (Rs. m) Fleet Size (No) (RHS) 2.6

20,000 2.5

2.4

15,000 2.3

10,000 2.2

2.1

5,000 2.0

1.9

-

FY07 FY09 FY12 FY13 FY15

FY95 FY01 FY06 FY11 FY15

Source: Company Data, PL Research

Source: Company Data, PL Research

Exhibit 3: Most efficient working capital management amongst peers Exhibit 4: VRL’s growth has come at healthy Return Ratios

Receivable days for FY15 RoE RoCE

70 66

59 30.0

60 25.0

50 20.0

40

(%)

15.0

30 20 10.0

20

5.0

10

0.0

0

FY15 FY16E FY17E FY18E

VRL Transport Corp Gati

Source: Company Data, PL Research Source: Company Data, PL Research

Exhibit 5: Operating cash flows looks robust with decent visibility Exhibit 6: Debt inching down, Balance sheet strong with D/E of 0.47x

FY16E

Operating Cash Flows

Total Debt (Rs m) Debt/Equity Ratio (x) (RHS)

3000

2500 7000 3.00

6000 2.50

2000

5000

(Rs m)

1500 2.00

4000

1000 1.50

3000

500 2000 1.00

1000 0.50

0

FY14 FY15E FY16E FY17E FY18E 0 0.00

FY12 FY13 FY14 FY15 FY16E

Source: Company Data, PL Research

Source: Company Data, PL Research

December 07, 2015 4VRL Logistics

Best placed amongst domestic listed players

VRL compares well with Transport Corp (TCIL) in Freight, Express and Supply chain divisions in

surface transportation. While, VRL is an asset-heavy model where it owns fleet, TCIL is more

focused on third-party trucks. VRL segment capital employed is, thus, deployed to own assets,

whereas TCIL capital employed is mostly working capital. VRL, thus, commands higher margins

than TCIL as it has lower hired lorry charges. Even after owning assets, VRL RoCE is 16% vis-à-

vis 12% of TCIL

VRL focuses on asset owning and leverage Exhibit 7: VRL Vs TCIL a Snapshot in similar business operations

on its distribution vis-à-vis other industry VRL *TCIL

participants. Owned Fleet 3,500 ~1200

Hired Fleet (approx) 360 5,800

Own Fleet/Hired Fleet ratio 0.88 0.17

Receivable days (Consolidated) FY15 20 66

Full Truck Load (FTL) 11% ~65%

Less Than Truck Load (LTL) 89% ~35%

EBIT margins (H1FY16) 12.7% 4.5%

Capital Employed (Rs M) 4,277 5,386

Locations covered 1,000 1,500

Segment Revenues (H1FY16) (Rs M) 6,824 10,410

Source: Company Data, PL Estimates * Freight, Express & Supply chain division included

VRL’s earnings are expected to grow faster than the industry and with sustained

margins over foreseeable future. RoEs above 25% and a dividend Payout ratio of 30-

35% are impressive which emphasises management focus on profitable growth and

creating value for stakeholders.

Exhibit 8: Comparative Financials of key surface logistics players in India (Rs m)

VRL Transport Corporation Gati Ltd

FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E

Revenue 16,712 18,151 20,417 24,167 27,059 31,105 16,481 18,910 22,056

EBITDA 2,728 3,213 3,461 1,974 2,231 2,642 1,412 1,420 1,768

Margin (%) 16.3 17.7 17.0 8.2 8.5 8.8 8.6 7.5 8.0

PAT 912 1,276 1,513 814 1,01 1,215 412 416 554

RoE (%) 27.5 28.3 25.6 14.6 18.3 19.3 6.2 7.4 9.2

EV 40,123 27,829 19,371

Source: Company Data, Bloomberg, PL Research

December 07, 2015 5VRL Logistics

Investment Rationale

Market leader in goods transportation with largest owned truck fleet

VRL is the market leader in GT segment with ownership of 4081 CVs which includes

3713 GT Vehicles & 368 buses. VRL has strong presence in the Southern and Western

markets (~80% of business revenues) and intends to replicate its LTL model in the

Northern and Eastern markets over the next 2-3 years. Given the sheer size of the

market, we feel the growth opportunity for an organised and process driven player

like VRL is huge. Further, as a large fleet operator, VRL benefits from scale and

higher control over key operational levers which include freight rates, fuel costs,

fleet utilisation and load flexibility.

Exhibit 9: GT Business has grown @16% CAGR for past 10 yrs Exhibit 10: Vehicle Split varies from 1T to 32T capacities helping to

cater different business needs

GT Revenues (Rs m) EBIT Margins (RHS)

LCV HCV Tanker & Cranes Car Carriers

14,000 14.0%

12,000 12.0% 4000

10,000 10.0%

8,000 8.0% 3000

6,000 6.0%

2423 2460

4,000 4.0% 2000 1916 1941 2210

2,000 2.0%

- 0.0% 1000

883 883 882 975 1002

FY06 FY09 FY12 FY15

0

FY12 FY13 FY14 FY15 H1FY16

Source: Company Data, PL Research

Source: Company Data, PL Research

Focused player on high-margin LTL business

Focus on LTL has helped VRL record better VRL has adopted a differentiated consignee-driven business model with a focus on

profitability when compared to other large the high-margin LTL business. The company primarily caters to the requirement of

organised players who largely focus on the small and mid-sized customers who are not serviced by large players due to their

FTL business small cargoes. VRL’s widespread network of collection and delivery points enables it

to service a larger number of customers across different geographies. This reduces

its reliance on few large customers and thereby, the business concentration risk. The

India-wide network of collection and delivery points and its strategically located

transhipment hubs have enabled VRL to focus on the attractive LTL business. The LTL

service offers higher rates per load compared to the FTL service as it involves

consolidation and transportation of freight from numerous customers to multiple

destinations and, thus, generates higher net revenue per vehicle.

December 07, 2015 6VRL Logistics

Exhibit 11: LTL forms almost 78% of GT segment revenues

LTL FTL Priority Parcel Courier , Car and Liquid Transit

14,000

12,000

10,000

8,000

(Rs m)

6,000

9,063 10,050

4,000 7,766

6,865

2,000

-

FY12 FY13 FY14 FY15

Source: Company Data, PL Research

Strong cash flows and healthy balance sheet, makes VRL Special

VRL has generated operating cash flows of Rs7.6bn during FY12-FY15 despite

subdued volume growth and tough operating environment. The next three years are

looking even stronger with operating cash flows expected to average Rs2.6bn/year.

VRL currently is in a sweet spot with strong balance sheet (D/E ratio of 0.47x FY16E)

and improving Return ratios. Considering capex of Rs1bn/yr and no working capital

requirements, VRL is a strong franchise which can be debt-free over the next three

years.

Exhibit 12: Return ratios looks impressive Exhibit 13: D/E ratio inching lower

RoE RoCE 2.00

30.0

1.50

25.0

20.0

(x)

1.00

(%)

15.0

10.0 0.50

5.0

0.0 0.00

FY13 FY14 FY15 FY16E FY17E FY18E FY13 FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research Source: Company Data, PL Research

December 07, 2015 7VRL Logistics

Company Background

Exhibit 14: About The Company VRL was founded in 1976 by Dr. Vijay Sankeshwar in Gadag, a small town in North

Employees ~17000 Karnataka with a single truck. VRL gradually expanded its services to Bengaluru,

28 States, 4 Union Hubli and Belgaum. From this humble beginning, VRL has today grown into a

Geographical Reach

territories

nationally renowned logistics and transport company which is also currently the

Strong Regions South and West

largest fleet owner of commercial vehicles in India with a fleet of 4081 Vehicles

Cities Covered 662

(Including 368 Passenger Transport Vehicles & 3713 Goods Transport Vehicles

Transshipment Hubs 48

amongst others). Mr. Vijay Sankeshwar has been joined by his son Mr. Anand

Touch Points 1015

Sankeshwar now for over a decade, which brings in newer strategies to further drive

Owned branches 20 the growth of the company.

3713 CVs

Fleet Size

368 PVs Over the years, VRL has pioneered in providing a safe and reliable delivery network

Petrol Pumps 2 ( in Karnataka) in the field of parcel service. The company has spread its operations to Courier

Source: Company Data, PL Research Service, Priority Cargo & Air Chartering to meet the growing demands of its

burgeoning customer base.

3PL & Warehousing solutions offered by VRL are tailor-made and cater to unique

needs of its diverse customer base. With the largest goods transportation network in

India, VRL parcel service is indispensable for a large number of Corporate Houses.

This network spans the length and breadth of the country and is supported by

strategically located transhipment hubs. The network spans across 1015 Branches

and franchisees to cater to the remotest locations of the country.

Management Personnel

Dr. Vijay Sankeshwar, CMD - Dr. Vijay Sankeshwar is actively involved in the

Exhibit 15: Key Shareholders

day-to-day affairs of the company as a Whole Time Director. He is a former

Major Share Holders % Share Holding

member of parliament. He was also part of Committee of Finance, Committee of

Vijay Sankeshwar 34.8

Transport and Tourism etc. in the past. He has an industry experience of over

Anand Sankeshwar 34.3 three decades and has received many awards for contribution to the logistics

New Silk Route PE 5.2 sector.

Goldman Sachs 4.4

Ashoka PTE 2.3 Mr. Anand Sankeshwar, Joint MD - Mr. Anand Sankeshwar, aged 42 years, is a

HDFC AMC 1.7

graduate in Commerce from Karnataka University, Dharwad. He is associated

with VRL for more than twenty years and is active MD of the company since

Vani Sankeshwar 0.4

2005. He directly oversees the finance and marketing function of the Company.

Source: Bloomberg, PL Research He has 14 years of experience in the media industry as well and is also MD in

VRL Media which is carrying Printing and Publication of Kannada daily

Newspaper under the brand name of “VIJAYAVANI”

Mr. Sunil Nalavadi, CFO - Mr. Sunil Nalavadi, aged 37 years, is the Chief

Financial Officer of the Company. He holds a bachelor’s degree in commerce

from the Karnataka University, Dharwad and is a qualified associate of the

Institute of Chartered Accountants of India. He is with VRL for almost a decade

now.

December 07, 2015 8VRL Logistics

Industry Dynamics

The domestic freight transportation industry is largely dominated by road transport.

However, this segment is highly fragmented and dominated by large number of

small players. This provides consumers with high bargaining power and intensifies

competition amongst them. The industry broadly consists of transport operators,

intermediaries, brokers and consignors or end-users. In India, road freight

constitutes around 63-65% of the total freight movement which consists of ~2.2m

heavy duty trucks and 0.6m light duty trucks.

Despite being an economical mode of transport, railways has lost market share in

freight movement to roads primarily on three counts: 1) Govt impetus on improving

road connectivity 2) Cost effectiveness and flexibility on Road and 3) Capacity

constraints and poor quality of service in railways.

Exhibit 16: Share of Roadways dominate total freight traffic Exhibit 17: Share of Transport in Public Sector Expenditure in different

movement Five-Year Plans since independence

Rail (% Share) Road (% Share) Total Transport Sector (LHS)**

Railways (% of Total)

Roads (% of Total)

100

8,000 60

80

60 6,000

40

40 4,000

20

20 2,000

0 - 0

1951-85

1985-90

1992-97

1997-02

2002-07

2007-12

Source: Ministry of Road Transport and Highways, PL Research Source: Planning Commission 2013, PL Research

*(GDP = 6.9 per cent) ** (At Current Prices in Rs bn)

Railways capacity in both freight and The freight transport market is driven mostly by the rapid growth in industries such

passenger traffic has not increased enough as automobiles, pharmaceuticals, FMCG and retail; increase in trade of chemicals,

simply due to inadequate investment when Textiles, and miscellaneous products with the world & government initiatives in

compared to road. Also, profitability of development of logistics infrastructure. However, sluggish economic activity and

freight division in railways is used to poor monsoon for the past two years have impacted growth of the freight transport

subsidize the passenger movement business to some extent. But considering a decisive government mandate and clear

message of spurring investments in infrastructure, we feel IIP numbers and GDP

growth are looking up over the foreseeable future. According to the published

estimates of IMF in Oct 2015, Indian GDP growth is expected to grow @7.3% in 2015

and 7.5% in 2016. This augurs well for the logistics sector at large which grows at a

multiple of 1.2-1.5x of GDP growth.

December 07, 2015 9VRL Logistics

Exhibit 18: IIP numbers clearly showing signs of bottoming out Exhibit 19: GDP growth looking to inch higher

20 9

8

15

7

10 6

5

(%)

(%)

5

4

0 3

2

-5

1

-10 0

Sep-10

Feb-11

Sep-15

Jan-14

Sep-12

Sep-13

Sep-14

Sep-15

Mar-13

Dec-11

Jun-14

Mar-13

Mar-14

Mar-15

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Jul-11

Aug-13

Oct-12

Apr-10

May-12

Apr-15

Nov-09

Nov-14

Source: Bloomberg, PL Research Source: Bloomberg, PL Research

At the simplest level, roads provide basic Unlike other modes of transport, roads address the demand for goods to cities as

accessibility to the rest of the world. No well as remote areas of the country. Since 1999-2000, road freight has increased

other piece of transport infrastructure can from 467 billion tonne kilometres (BTKM) to 1,250 BTKM in 2011-12, at a CAGR of

replace the street outside one’s home 8.6%. According to the Ministry of Road Transport and Highways, road freight is

expected to reach 1,987 BTKMs by 2016-17E, a CAGR growth of 9.8%.

Exhibit 20: Road transportation freight movement in BTKM is growing @9.8% for past 12 yrs

2500

2000

(Bn tonnes km)

1500

1000

500

0

1970-71 1990-91 2004-05 2011-12 2016-17E*

Source: National Transport Development Policy Committee, PL Research

Surface Transportation, dominated by unorganized segment

The transport operators are broadly classified as small fleet operators (SFOs),

medium fleet operators (MFOs) and large fleet operators (LFOs). Road freight

transport due to its highly fragmented nature is dominated by small operators

having 65-70% share. However, SFOs have very restricted geographical reach as

compared to LFOs who enjoy nationwide presence. LFOs are preferred by large

corporate due to their reach, service quality and timely delivery. Introduction of GST

can further accelerate this trend as the price differential in freight rates will narrow

down between organized and unorganized segment.

December 07, 2015 10VRL Logistics

SFOs are small fleet operators owning up Exhibit 21: LFOs gain share over the past three decades but SFOs still dominant

to five vehicles, MFOs are medium fleet

SFO MFO LFO

operators owning between six and twenty

vehicles whereas LFOs are large fleet 100 2 2 6

13 11 18

operators owning more than twenty trucks 17

80 15

15

60

(%)

98

40 85

77 74 67

20

0

1978-79 1993-94 2002-03 2008-09 2014-15E

Source: Company Data, PL Research

Exhibit 22: Forces which impacts Road Freight

Threat of New Entrant - HIGH

Initital Investment of Rs.3-5lacs with

LTV ratio upto 90%

Easy licensing availability

Labour with basic skills are required

Rivalry Among Exisiting Players - MODERATE Threat of Substitutes - LOW

Lack of any USP makes price the only Other modes like Rail, Air and Waterway

differentiator can be substitutes

Unorganized players resort to price cutting to Due to last mile connectivity and supply

attain higher utilization constraints, rail isn't a large threat in the

short term

LFOs face less of price rivalry but more focus is

on quality of service Forces Lower fuel prices favours road over

other modes

impacting

Road Freight

Bargaining Power of Suppliers - LOW to MODERATE Bargaining Power of Cutomers - HIGH

As the fuel prices are market determined, there isn't Large consigners and organisations

much to bargain for both the parties have better bargaining power due to

Transporters with larger share of outsourced truck have bulk volumes

less bargaining power, especially in peak seasons Due to unorganized nature of

Transporters which own fleet have better bargaining business, pricing remains the key to

power on bulk purchases garner business

Source: Company Data, PL Research

December 07, 2015 11VRL Logistics

GST can improve volumes for LTL organized operators

VRL is well positioned to benefit from GST Goods and Service Tax (GST) is expected to change the existing indirect tax structure

implementation and already holds in India. Under existing structure, industry is levied tax both at centre (Excise, Service

leadership position in the LTL freight Tax etc.) as well as state level (VAT, Octroi, Sales Tax etc). This double taxation has

movement in India forced companies to keep their warehouses in multiple cities across different states.

Under proposed GST, tax will be levied by both centre and state simultaneously

with easy mechanism of input tax credit.

With GST, companies which are currently forced to set up many small warehouses

across multiple cities can set up just a few, big warehouses region wise and can

follow the hub-and-spoke model for freight movement from the warehouses to the

different manufacturing plants, wholesale outlets, retail outlets and the various

points of sale. These large warehouses will help organised players like VRL to

position themselves as one point solution providers across the warehouses of

companies. This shall also shift volumes from the unorganised sector which thrives

on small inter-city routes in different states towards the organised sector.

Waiting time for trucks to go down: While most states have replaced the octroi

gates (on city borders) with a local body tax (LBT), it has still not reduced the waiting

On an average, a truck is idling for 25% of

time for vehicles. Similarly, at check posts on state borders, different requirements

times waiting at different check-posts across

for documentation and tax payment lead to considerable delays. However, post GST,

India for documentation requirements and tax

the waiting time for trucks is expected to reduce significantly which may result in

payments.

higher utilization of trucks for goods transit rather than waiting at check posts.

December 07, 2015 12VRL Logistics

Business Segments

VRL primarily operates in two business segments, namely, Goods Transportation

(GT) and Passenger Transportation (BT).

GT segment is the focal point contributing 77% of revenues

VRL offers services for transportation of goods across India to its customers using

LTL, FTL and priority services. The company owns 3713 commercial vehicles covering

all major cities and towns spread across 28 States & four Union Territories. It has an

extensive network with nearly 1000 plus branches and franchisees that enables it to

provide connectivity covering most remote locations as well. The branch network is

further complemented by 48 strategically located transhipment hubs.

The GT business is broadly divided into General Parcel and Priority parcel. General

Parcel basically caters to godown-to-godown movement of consignments across the

country and is mainly used by wholesalers, retailers and other non-corporate

entities. VRL Priority caters to door-to-door movement of consignments and this

service is mainly availed by corporate customers. The other verticals include car

carrying, liquid transportation and courier activities.

Exhibit 23: GT Business is further divided into four segments, general parcel dominates

Segment Description % Contribution to GT revenues for FY15

General parcel It primarily includes godown-to-godown movement of goods 77.9%

Priority Parcel It involves door-to-door movement of cargo 7.7%

Full Truck Load Caters in regions and routes to optimize return traffic 10.6%

Others It include car carrying, liquid transportation and courier activities 3.8%

Source: Company Data, PL Research

Exhibit 24: Fleet Split end of period

Small Car Total

LCV HCV Tanker Cranes

Vehicle Carrier Vehicles

FY11 171 892 1575 0 7 10 2655

FY12 139 883 1916 102 27 12 3079

FY13 122 883 1941 102 27 13 3088

FY14 122 882 2210 102 23 13 3352

FY15 120 975 2423 102 16 13 3649

H1FY16 119 1002 2460 102 17 13 3713

Source: Company Data, PL Research

December 07, 2015 13VRL Logistics

Exhibit 25: Revenue Split of VRL across different business segments

75.9% 77.2% 78.2% 78.9%

Goods Transport Bus Operations Wind Power Air Charter

25,000

20,000 17.2%

18.5%

15,000 18.9%

19.8%

(Rs m)

20.7%

10,000

75.9% 77.2% 78.2% 78.9% 80.4%

5,000

-

FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research

Passenger segment consolidating, focus is on premium routes

VRL operates passenger buses in high density urban markets such as Bengaluru,

Mumbai, Pune, Hyderabad, Ahmedabad, Jodhpur & Panjim. It also connects

metropolitan and Tier-II cities such as Hubballi, Dharwad, Hospet, Mangalore,

Bagalkot, and Bhatkal. VRL has pioneered the country’s largest commercial bus route

of nearly 2,000 km, from Bengaluru to Jodhpur. The passenger transportation

business operates in the key states of Karnataka, Maharashtra, Andhra Pradesh,

Telangana, Tamil Nadu, Gujarat, Rajasthan and Goa through its fleet of 368 buses.

This division operates through 81 branches (74 lease and 7 owned), 739 franchisees,

including web agents and 416 prepaid. Bus operations contributed 19.8% of overall

revenues in FY15.

Exhibit 26: VRL’s key bus routes

Bengaluru-Ahmedabad Bijapur-Bengaluru Hospet-Mumbai

Bengaluru-Jodhpur Bengaluru-Mangalore Belgaum-Bengaluru

Hubballi-Bengaluru Bengaluru-Goa Belgaum-Mumbai

Hubballi-Mumbai Bengaluru-Shirdi Belgaum-Pune

Mumbai-Bengaluru Hubballi-Pune Hyderabad-Goa

Mumbai-Mangalore Bijapur-Bengaluru Hyderabad-Mangalore

Bidar-Bengaluru Hopset-Bengaluru Hyderabad-Bengaluru

Gulbarga-Mangalore Goa-Mumbai Hyderabad-Mumbai

Gulbarga-Bengaluru Pune-Nagpur Hyderabad-Shirdi

Source: Company Data, PL Research

December 07, 2015 14VRL Logistics

Exhibit 27: Revenues strong despite fall in fleet implies focus on premium routes

Total Bus Segment Reveneus (Rs m) Total Buses (RHS)

4500 600

4000

500

3500

3000 400

2500

300

2000

1500 200

1000

100

500

0 0

FY13 FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research

Currently, VRL is concentrating on VRL has become leaner by 100 buses over the past one year primarily due to a

premium routes connecting major cities to conscious decision to let bus permits expire and wait for the New Road and Safety

perk up the realization and utilization transport bill to be passed. The Bill proposes a unified vehicle registration system like

the commercial vehicles and simpler online transfers of vehicles across various

States in India, which will significantly improve operating efficiencies and reduce

operational costs for the passenger transportation segment. This is expected to

make the inter-state passenger transport smoother and efficient, as compared to

current complex and restrictive rules.

Air Charter Business

VRL entered the air charter business in 2008 by purchasing a new Premier 1A aircraft

from Hawker Beechcraft Inc., USA. The Premier 1A aircraft is a twin engine

sophisticated aircraft with space for two pilots and six passengers. Further in 2013,

VRL purchased a second hand aircraft from M/s Force Motors, Pune for a

consideration of Rs120m. VRL offers charter services, bulk-charters or any

customized requirement and offer services to individuals, corporate clients and

Government of Karnataka. Most of management travels and allied expenses are a

part of this division. Capital employed in this division is Rs378m and it has generated

revenues of Rs51m and EBIT of Rs (17m) for H1FY16.

Exhibit 28: Air Charter business Snapshot

Air charter Business FY14 FY15 H1FY16

Revenues 78 117 51

EBIT (21) (23) (17)

No of aircrafts 2

Capital Employed Rs 378m

Source: Company Data, PL Research

December 07, 2015 15VRL Logistics

Wind Power Generation Business

In 2006 VRL commenced its wind power business in Southern India at Kappatgudda,

Gadag district in Karnataka by setting up a wind farm of 42.5MW. The wind farm

consists of 34 Wind Turbine Generators (WTGs) having individual capacity of

1.25MW. The turbines are of S66 technology developed by Suzlon Energy and the

power generated is sold to Hubli Electricity Supply Company (HESCOM) under six

Power Purchase Agreements (PPAs). The project is registered with United Nations

Framework Convention on Climate Change (UNFCCC) and necessary approvals for

the trade of carbon credits have been procured.

Exhibit 29: Wind Power Business Snapshot

Wind Power FY14 FY15 H1FY16

Revenues 250 222 166

CER 61 - -

EBIT 71 48 84

Power Capacity 42.5 MW

Capital Employed Rs 1259m

Source: Company Data, PL Research

December 07, 2015 16VRL Logistics

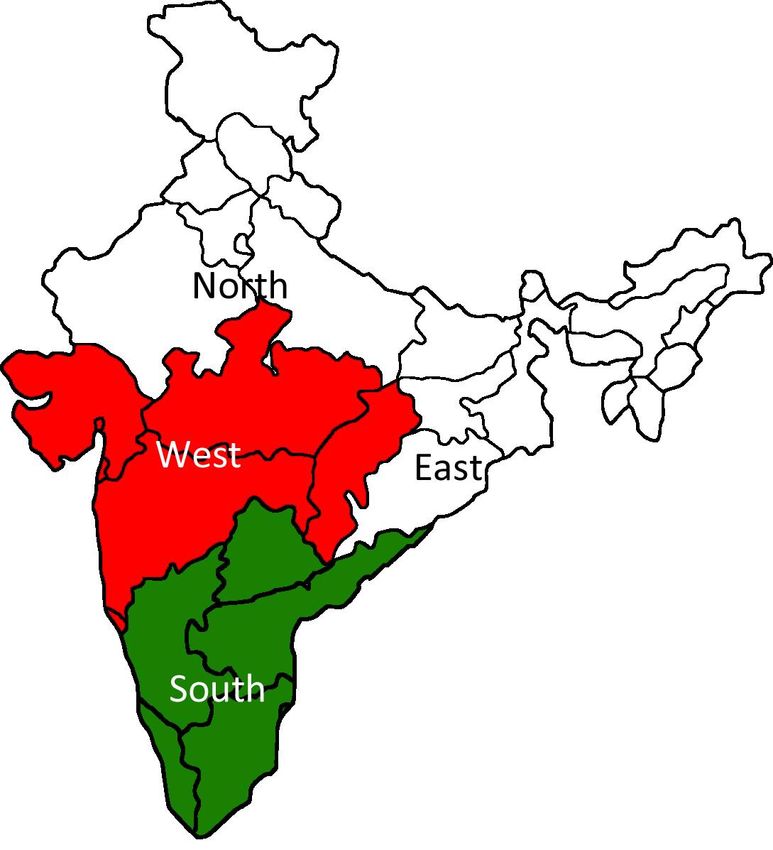

VRL is looking to replicate its LTL business model in other

regions

VRL has adopted a differentiated consignee-driven business model with a focus on

the high-margin LTL business. It primarily caters to the requirement of small and

mid-sized customers. VRL’s widespread network of collection and delivery points

enables it to serve a larger number of customers across different geographies. VRL

has strong presence in the Southern and Western markets (~65% of originating

business revenues). Over the next 2-3 years, it is planning to replicate its LTL model

in the Northern and Eastern markets as well.

Exhibit 30: VRL has strong foothold in the South and West market, Focus is to enhance reach in Northern and Eastern markets

North

Agencies 56

Branches 76

Transshipment Hubs 6

East

Agencies 7

Branches 38

West Transshipment Hubs 3

Agencies 81

Branches 119

Transshipment Hubs 10

South

Agencies 202

Branches 391

Transshipment Hubs 29

Source: Company Data, PL Research

December 07, 2015 17VRL Logistics

VRL has diverse clientele with no customer concentration

VRL services customers across a wide range of industries which include

Pharmaceuticals, FMCG, Paper, Wood, Automotive parts & machinery, Plastics,

Appliances, Furniture, Metal & Metal products etc. In the Goods transport business

for FY15, the client concentration is relatively low, with the largest customer and top

10 customers accounting for only 1.1% and 6.1% of revenues, respectively. VRL has a

strong recovery system with bad debts not exceeding Rs1m a year for the past five

years. In addition, working capital requirement has moved down from 25 days in

FY12 to 20 days in FY15.

Exhibit 31: VRL’s caters across wide range of industries

Pharma

FMCG Plastics

VRL

Paper Machinery

Wood Automotive

Source: Company Data, PL Research

Exhibit 32: Revenue Contribution from the largest and Top Ten Customers

Largest Customer Top 10 Customers

10.0

8.0

6.1

6.0 5.1 5.3 5.4

(%)

4.0

2.0 1.3 1.5 1.1

0.9

0.0

2012 2013 2014 9MFY15

Source: Company DRHP, PL Research

December 07, 2015 18VRL Logistics

Efficient Working Capital Management

VRL runs a process driven business and is always selective in choosing freight on

their business terms. It has strong internal systems to ensure that collection

mechanism is robust and they do not have to compromise in any manner. This has

resulted in lower receivable days for VRL as compared to industry players, which

again reinforces the fact that it does not compromise on its business principles even

if it results in sub-par revenue growth for some time. ~70% of business in GT

segment does not require any working capital.

Exhibit 33: Receivables tilted towards upfront payments

Paid Option To Pay Option Ongoing accounts Others

100

8 11 11 14

80 23 22 18 17

60

(%)

40 58 56 59 57

20

11 11 11 12

-

FY12 FY13 FY14 FY15

Source: Company Data, PL Research

Fuel accounts for 34-37% of total operating costs; efficient cost

management holds the key

Fuel cost is an important element which constitutes ~34-37% of total operating

costs. Out of the total requirement of ~2,50,000 litres/day, VRL gets ~60% fuel from

IOCL. Further, VRL owns two fuel stations in Karnataka which constitutes ~25% of

fuel requirement. Also, they have tied up with IOCL across 80-100 locations in India

and drivers are required to purchase fuel from these company designated fuel

pumps only during transit.

Exhibit 34: Split of operating costs amongst various constituents (FY15)

Clearing and Tyres, flaps and re- Vehicle taxes

Others

forwarding treading 3% 3%

3% 4%

Stores and spares Vehicle operation-

consumed diesel cost

4% 38%

Hamaali

5%

Agency

commission

Rent

5%

6%

Bridge and toll Vehicle running, Lorry hire

charges repairs & 11%

8% maintenance

10%

Source: Company Data, PL Research

December 07, 2015 19VRL Logistics

Use of Bio-diesel and lower crude prices to help in sustain margins

VRL has devised an innovative way to

control its fuel cost by rewarding those VRL has started blending Bio-diesel for both Passenger and Goods Transportation

drivers in cash incentives who consume less business in FY16. It started with 12.5% blending in Q1FY16 and has gradually ramped

fuel than estimated by VRL on a particular it up to optimum levels of ~36% in Q2FY16. This has reduced the fuel cost per litre by

route ~Rs4-5, resulting in almost 200bps savings in fuel costs. However, savings from lower

fuel costs in H1FY16 were netted off against high employees cost.

Exhibit 35: Diesel price Movement (in Rs) Exhibit 36: Crude movement USD

70.0 160

140

60.0

120

50.0 100

80

40.0 60

40

30.0

20

20.0 0

Nov-02

Nov-03

Nov-04

Nov-05

Nov-06

Nov-07

Nov-08

Nov-09

Nov-10

Nov-11

Nov-12

Nov-13

Nov-14

Nov-15

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Apr-11

Apr-12

Apr-13

Apr-14

Apr-15

Source: IOCL Website, PL Research Source: Bloomberg, PL Research

In-house body design facility and maintenance enhances profitability

VRL has focussed on cutting cost by VRL has in-house body design facility at Hubli where it buys chassis from the

sourcing spare parts and Tyres from OEMs manufacturer and fabricates the vehicles with lighter and longer bodies which

at discounted rates. Also, most of the fleet reduces the overall weight of the vehicle and ensure higher payloads without

maintenance is carried in-house which not violating permissible payload limit. VRL also has two major workshops in Hubli where

only curtail costs but also enhances fleet all the major servicing is done.

life

Ashok Leyland & VE commercial (Volvo) have established their own spare parts yard

in VRL’s premises, resulting in procurement of spare parts directly from

manufacturers at factory rates and saving on carrying cost. Further, company has

arrangement with Michelin India and CEAT which allows it to get tyres at ~7-8%

cheaper than the retail selling price.

December 07, 2015 20VRL Logistics Assumptions Exhibit 37: Assumptions (Rs m) Y/e March FY13 FY14 FY15 FY16E FY17E FY18E Goods Transport Revenues 9,923 11,334 12,908 14,132 16,025 18,093 Fleet Size 2,946 3,214 3,518 3,718 3,958 4,238 Additions per year 8 268 304 200 240 280 Revenue/Tonne (Rs) 4,200 4,710 4,967 5,254 5,517 5,792 Volume Growth 1.7% 1.8% 8.0% 3.5% 8.0% 8.0% Realization Growth 13.0% 12.2% 5.4% 5.8% 5.0% 5.0% EBIT Margins 10.1% 11.0% 12.9% 13.5% 13.0% 12.7% Bus Transport Revenues 2,848 3,091 3,316 3,406 3,759 3,872 Fleet Size 460 477 375 368 380 385 Additions per year 37 17 (102) (7) 12 5 EBIT Margins 6.6% 0.7% 10.9% 13.5% 12.5% 13.0% Tax Rate 28.1% 25.7% 33.8% 33.0% 32.0% 32.0% Diesel Cost (Rs/litre) 48.4 56.5 59.7 54.0 57.0 60.0 Segment overview Revenues Goods Transport Business 9,923 11,334 12,908 14,132 16,025 18,093 Passenger Transport 2,848 3,091 3,316 3,406 3,759 3,872 Segment EBIT Goods Transport Business 1,003 1,251 1,670 1,908 2,083 2,298 Passenger Transport 187 23 362 460 470 503 Capital Employed Goods Transport Business 4,127 4,395 4,912 5,177 5,542 6,017 Passenger Transport 1,742 1,537 1,318 1,150 1,200 1,250 Wind Power 1,469 1,370 1,256 1,142 1,027 913 Air chartering service 251 382 358 339 320 301 Un-allocable assets 2,063 2,092 1,687 1,700 1,650 1,600 Segment RoCE Goods Transport Business 17.5% 21.1% 22.5% 24.7% 25.6% 26.0% Passenger Transport 7.7% 1.1% 18.2% 26.8% 26.6% 27.4% Source: Company Data, PL Research December 07, 2015 21

VRL Logistics

Financials

VRL revenues growing @10.7% CAGR over FY15-FY18E

VRL is expected to grow revenues @10.7% over FY15-FY18E, primarily on the back of

12% growth in GT segment and 6% growth in BT segment. GT segment is expected to

benefit from sustained volume recovery with improved road infrastructure and fleet

addition of ~720 trucks over FY16-FY18E period. We have not yet factored in

significant ramp-up in BT segment since VRL is only concentrating on profitable

routes and is consolidating its Bus operations.

Exhibit 38: GT Business looking strong over FY15-FY18E period Exhibit 39: BT segment consolidating, margins inching higher

Revenues (Rs m) EBIT Margin (RHS) Revenues (Rs m) EBIT Margin (RHS)

20,000 15.0% 5,000 15.0%

4,000

15,000

10.0% 10.0%

3,000

10,000

2,000

5.0% 5.0%

5,000

1,000

- 0.0% - 0.0%

FY13 FY14 FY15 FY16E FY17E FY18E FY13 FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research Source: Company Data, PL Research

Business mix tilted towards Goods Transportation segment

VRL derives 77% of its revenues from Goods Transportation segment and 20% from

Passenger Transportation, while wind power generation, air charter operation and

other contribute 1.35%, 0.7% and 0.9%, respectively. LTL contributes 86% of the

Goods Transport segment, while remaining is contributed by FTL, Car Carrier, Liquid

Transport and Courier service

EBITDA Margins bounce back to FY12 levels

VRL has always strived to optimize revenues and curtail operating costs by investing

in technology, in-house facilities for body building and maintenance, operate fuel

pumps, tie-up with IOCL for fuel refilling and use of Bio-diesel. However margins

slipped in FY13-FY14 owing to the Telangana stir and rapid rise of diesel prices which

were not being passed to the end customers entirely because of overall slag in

economic activity. With normalization returning back in Telangana, margins have

recovered back to FY12 levels. VRL currently is focusing on LTL business which

ensures optimum utilization of fleet and ensures higher margins than the traditional

FTL business.

December 07, 2015 22VRL Logistics

Exhibit 40: EBITDA and OPM over FY12-FY18E Period

EBITDA (Rs m) Margin (RHS)

4,000 18.0%

3,500

17.0%

3,000

16.0%

2,500

2,000 15.0%

1,500

14.0%

1,000

13.0%

500

- 12.0%

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research

Robust operating performance over the past four years

VRL has generated operating cash flows of Rs7.6bn during FY12-FY15 despite

subdued volume growth and tough operating environment. These were used to

create assets worth Rs4.7bn and debt repayment of Rs1.85bn over the same period.

With Rs1.17bn raised from the IPO and capex program of Rs1bn for FY16, VRL is a

strong franchise which can be debt-free over the next three years.

Exhibit 41: Operating Cash flows averaging Rs 2.6bn/yr for next 3 yrs Exhibit 42: Debt inching down over FY14-FY18E period

3,000 Avg. Rs2.6bn 6,000

2,500 5,000

2,000 4,000

(Rs m)

(Rs m)

1,500 3,000

1,000 2,000

500 1,000

- -

FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research Source: Company Data, PL Research

IPO well received this time, raised Rs4.7bn in April 2015

VRL raised Rs4.7bn through an IPO route in April, 2015 which included Rs1.17bn of

fresh issue and Rs3.5bn of offer for sale from promoters (Rs0.5bn) and New Silk

Route PE (Rs3bn) at a price of Rs205/share. The object of the issue was to purchase

goods transportation vehicle of ~Rs674m and repayment of borrowing worth

~Rs280m. VRL has repaid debt out of the said proceeds and purchased vehicles

worth Rs230m till H1FY16.

December 07, 2015 23VRL Logistics

Return Ratios and Asset turnover impressive

VRL’s return ratios are amongst the best in listed logistics space with RoE in excess of

25%. Optimum utilization of fleet in GT segment and focus on premium routes in BT

segment has enabled VRL to report healthy return on investment. Asset turnover,

too, over the years have been above 2x which re-enforces confidence in the hub-

spoke model and optimum utilization of fleet infrastructure.

Exhibit 43: Return Ratios continue to impress Exhibit 44: Asset turnover above 2x for the GT and BT business

RoAE (%) RoACE (%) 3.00

30.0 2.50 Avg. 2.19x

25.0 2.00

20.0

(x)

1.50

15.0

10.0 1.00

5.0 0.50

0.0

0.00

FY14 FY15 FY16E FY17E FY18E

FY14 FY15 FY16E FY17E FY18E

Source: Company Data, PL Research Source: Company Data, PL Research

December 07, 2015 24VRL Logistics

Valuation and Outlook

VRL is expected to almost double its earnings over FY15-FY18E period led by strong

performance in Goods and Transport Segment. However, if reforms like new Road

Transport and Safety Bill and GST Bill get passed in time, then VRL may emerge as a

key beneficiary with almost double-digit volume growth as we anticipate the LTL to

garner significant volume shift happening from unorganised to organised segment.

We expect VRL to have a payout of ~35% as operating cash flows remain strong and

capex requirements ease off. We initiate coverage on VRL with a ‘BUY’ and a TP of

Rs534, implying a 28x FY18E PER and 13.2x EV/EBITDA FY18E. The premium is

justified considering:

Strong management pedigree with proven track record

High visibility on operating cash-flows and high dividend payout ratio

Superior returns ratios amidst listed logistics players

Efficient working capital management

Margin improvement due to lower fuel prices and efficient use of Bio-diesel

Strong balance sheet to leverage emerging opportunities in logistics space.

Exhibit 45: Comparative Valuation

Mcap Sales (Rs Bn) PE (x) RoE (%) EV/EBITDA (x) FY15-FY17E CAGR (%)

COMPANY

(Rs bn) FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E Sales EBITDA PAT

Road Freight

Blue Dart 169 22.7 27.4 33.7 130.8 88.0 64.4 27.2 50.2 51.6 76.5 50.3 38.3 21.8 41.3 43.1

VRL Logistics 40 16.7 18.2 20.4 40.2 30.7 25.9 27.5 28.3 25.6 14.7 12.5 11.6 10.5 12.6 28.8

Transport Corp 25 24.2 27.1 31.1 29.7 24.7 20.5 14.6 18.3 19.3 14.1 12.5 10.5 13.4 15.7 22.2

GATI 15 16.5 18.9 22.1 36.9 36.3 27.2 6.2 7.4 9.2 13.7 13.6 11.0 15.7 11.9 15.9

Multi Modal / CFS

Cont. Corp. 276 61.5 65.6 75.9 26.2 27.8 23.2 14.7 12.5 13.5 17.8 18.3 15.1 11.1 8.4 5.1

AllCargo Logistics 48 56.3 60.9 67.1 19.9 16.2 13.7 13.0 14.5 15.0 10.5 8.7 8.0 9.2 14.4 20.4

Gateway

35 11.1 11.4 13.7 18.7 22.8 18.2 21.3 15.1 17.6 11.7 12.6 10.0 10.9 7.7 0.9

Distriparks

Navkar Corp. 28 3.3 3.3 3.8 38.4 33.5 18.6 12.4 10.8 6.1 23.4 21.2 14.0 31.3 29.4 44.3

Source: Company Data, Bloomberg, PL Research

December 07, 2015 25VRL Logistics

Exhibit 46: VRL have commanded higher one yr fwd multiple in its limited trading history

600

500 31x

27x

400

23x

300 19x

15x

200

100

0

Apr/15 May/15 Jun/15 Jul/15 Aug/15 Sep/15 Oct/15 Nov/15

Source: Company Data, Bloomberg, PL Research

Limited free-float in the sector to command premium

We observe that the promoter ownership in the sector is quite high, barring Gati.

Institutional ownership in most logistics stocks is yet to cross even 20%. We feel VRL

can continue to trade at premium valuations considering its leadership position and

scarcity premium.

Exhibit 47: Institutional ownership less than 20% in most stocks-Scarcity premium remains

SHAREHOLDING PATTERN (%) VRL TCIL Gati Blue Dart

Promoters 69.6 66.5 41.4 75.0

FIIs 10.8 2.9 9.3 7.1

Banks and FIs 8.2 6.5 0.3 5.8

Public 11.5 24.1 49.0 12.1

Source: Company Data, PL Research

December 07, 2015 26VRL Logistics

Risk and Concerns

Shortage or non-availability of skilled drivers

Shortage of qualified drivers in the transportation industry could force VRL to either

increase driver compensation further or hire third-party owned trucks which may

not be available at commercially viable rates. Thus, VRL needs to attract and retain

sufficient number of skilled drivers. Any inability to do so would force VRL to rely

heavily on hired transportation which can result in idling of owned vehicles and limit

profitable growth.

Inability to pass on increase in operating cost, particularly fuel price

hikes

Fuel costs, Toll charges and Rent represent almost 37% of total costs for VRL. Thus,

any rapid increase in diesel prices can adversely affect its profitability since it may

not be able to pass through increased fuel costs to the customers on a real time

basis. However, historically VRL has been able to pass on fuel price hikes and other

operating costs to its customers by way of increase in freight rates or bus ticket

prices with a lag of 4 to 6 weeks.

Outstanding litigations and proceedings against VRL

There are 1171 civil complaints filed against VRL involving a total amount of

Rs1244m most of which pertains to road accidents involving death of a person,

damage of goods in transit, transportation of goods not permitted, goods theft etc.

However, substantial portion of the expected liability/payment arising out of these

cases would devolve on third parties such as insurance companies.

Exhibit 48: Outstanding litigations and proceedings against VRL

Nature of cases Number of cases Amount involved (Rs m)

Criminal 9 0.9

Civil* 1171 1244.1*

Writ 1 NIL

Labour 103 78.4

Consumer Cases 38 9.1

Tax 8 161.3

Source: Company Data, PL Research * As on March 28, 2015

December 07, 2015 27VRL Logistics

Annexure

Exhibit 49: Company Timeline

1976 Commencement of Goods Transport Service by Mr. Vijay Sankeshwar with single truck

1983 Business being converted into a private limited company by the name of Vijayanand Roadlines Private Limited

1992 Commencement of Courier Service within the State of Karnataka

1994 Vijayanand Roadlines Private Limited becomes Deemed Public Limited Company

1996 Commencement of Passenger Transportation Business

1997 The status of the company changed to Public Limited Company

2003 Vijayanand Printers Limited becomes a wholly owned subsidiary

2003 Entry in to LIMCA BOOK OF RECORDS as the single largest fleet owner of commercial vehicles in the private sector in India

2004 Commercial operation of gigantic infrastructure facility at Varur, Hubballi

2005 ISO 9001:2000 Certification for providing passengers travels service at Hubballi, Bengaluru, Belgaum (presently ISO 9001:2008)

2006 Entire stake in Vijayanand Printers Limited divested to Times Group

2007 Company diversified into power generation and installed 34 Wind Turbine Generators with capacity of 1.25 MW each

2008 Company entered into air charter business and purchased a brand new IA aircraft from Hawker Beechcraft Incorporation

2009 UNFCCC approval for Company’s wind power project – Eligible for carbon credits

2010 Efforts of Company being recognised by way of several awards and recognitions

2011 Foray into New Logistics Verticals – Car Carrying and Liquid Transportation

2012 CER income recognised for the first time in accounts

2012 Private Equity investment by NSR PE Mauritius LLC in the Company

2013 Addition of one more Aircraft to the Air Charter business of the Company

Source: Company Data, PL Research

Road Safety and Transport Bill, 2014

Passenger transport to enjoy same The Government has proposed a new Road Safety and Transport Bill, 2014 to amend

flexibility as goods transport with ease of the existing Motor Vehicles Act, 1988 to provide a comprehensive framework for

movements between states goods transportation and passenger transportation activities in India.

The Transport Bill proposes unified, transparent and single window driver licensing

system with simplified procedures, relaxed requirements for drivers to obtain driving

licenses, automated driving tests, unified biometric systems and adoption of

technology-based driver testing facilities which are likely to result in increased

availability of qualified drivers through the introduction of simplified licensing

procedures.

The Bill also proposes a unified vehicle registration system and simpler online

transfers of vehicles across various states in India, which will significantly improve

operating efficiencies and reduce operational costs for the passenger transportation

segment. This is expected to make the inter-state passenger transport smoother and

efficient as compared to the current complex and restrictive rules.

December 07, 2015 28VRL Logistics

Income Statement (Rs m) Balance Sheet Abstract (Rs m)

Y/e March 2015 2016 2017E 2018E Y/e March 2015 2016 2017E 2018E

Net Revenue 16,712 18,151 20,417 22,617 Shareholder's Funds 3,563 5,458 6,355 7,375

Raw Material Expenses 11,794 12,433 14,139 15,719 Total Debt 4,434 2,550 2,500 2,000

Gross Profit 4,918 5,718 6,278 6,898 Other Liabilities 973 990 1,022 1,055

Employee Cost 1,980 2,269 2,552 2,827 Total Liabilities 8,969 8,998 9,877 10,430

Other Expenses 211 236 265 294 Net Fixed Assets 7,159 7,080 7,158 7,136

EBITDA 2,728 3,213 3,461 3,777 Goodwill — — — —

Depr. & Amortization 877 932 1,002 1,072 Investments 846 811 811 811

Net Interest 586 436 303 270 Net Current Assets 962 1,107 1,909 2,483

Other Income 114 60 70 120 Cash & Equivalents 166 249 747 971

Profit before Tax 1,379 1,904 2,225 2,555 Other Current Assets 1,359 1,443 1,607 1,767

Total Tax 467 628 712 818 Current Liabilities 563 585 445 255

Profit after Tax 912 1,276 1,513 1,738 Other Assets — 1 — —

Ex-Od items / Min. Int. — — — — Total Assets 8,968 8,998 9,877 10,430

Adj. PAT 912 1,276 1,513 1,738

Avg. Shares O/S (m) 85.5 91.2 91.2 91.2

EPS (Rs.) 10.7 14.0 16.6 19.0

Cash Flow Abstract (Rs m) Quarterly Financials (Rs m)

Y/e March 2015 2016 2017E 2018E Y/e March Q3FY15 Q4FY15 Q1FY16 Q2FY16

C/F from Operations 2,317 2,438 2,581 2,846 Net Revenue 4,299 3,974 4,479 4,272

C/F from Investing (491) (750) (850) (850) EBITDA 746 590 832 694

C/F from Financing (1,812) (1,605) (1,233) (1,771) % of revenue 17.4 14.8 18.6 16.3

Inc. / Dec. in Cash 15 83 498 225 Depr. & Amortization 232 185 223 224

Opening Cash 125 140 223 721 Net Interest 145 136 103 74

Closing Cash 140 223 721 946 Other Income 21 58 19 23

FCFF 1,827 1,688 1,731 1,996 Profit before Tax 390 327 525 420

FCFE 472 (637) 1,161 959 Total Tax 139 133 172 130

Profit after Tax 251 194 354 290

Adj. PAT 251 194 354 290

Key Financial Metrics Key Operating Metrics (Rs m)

Y/e March 2015 2016 2017E 2018E Y/e March 2015 2016 2017E 2018E

Growth Segment Revenues

Revenue (%) 11.9 8.6 12.5 10.8 Goods Transport 12,908 14,132 16,025 18,093

EBITDA (%) 32.0 17.8 7.7 9.1 Bus Operations 3,316 3,406 3,759 3,872

PAT (%) 60.0 39.9 18.6 14.8 EBIT

EPS (%) 60.0 31.1 18.6 14.8 Goods Transport 1,670 1,908 2,083 2,298

Profitability Bus Operations 362 460 470 503

EBITDA Margin (%) 16.3 17.7 16.9 16.7 Source: Company Data, PL Research.

PAT Margin (%) 5.5 7.0 7.4 7.7

RoCE (%) 15.8 19.6 20.4 21.1

RoE (%) 27.5 28.3 25.6 25.3

Balance Sheet

Net Debt : Equity 1.2 0.4 0.3 0.1

Net Wrkng Cap. (days) 20 21 21 24

Valuation

PER (x) 40.3 30.7 25.9 22.5

P / B (x) 10.3 7.2 6.2 5.3

EV / EBITDA (x) 15.0 12.9 11.8 10.6

EV / Sales (x) 2.5 2.3 2.0 1.8

Earnings Quality

Eff. Tax Rate 33.9 33.0 32.0 32.0

Other Inc / PBT 5.7 3.2 3.1 4.7

Eff. Depr. Rate (%) 7.1 7.0 7.0 7.0

FCFE / PAT 51.8 (49.9) 76.7 55.2

Source: Company Data, PL Research.

December 07, 2015 29VRL Logistics

THIS PAGE IS INTENTIONALLY LEFT BLANK

December 07, 2015 30VRL Logistics

THIS PAGE IS INTENTIONALLY LEFT BLANK

December 07, 2015 31VRL Logistics

Prabhudas Lilladher Pvt. Ltd.

3rd Floor, Sadhana House, 570, P. B. Marg, Worli, Mumbai-400 018, India

Tel: (91 22) 6632 2222 Fax: (91 22) 6632 2209

Rating Distribution of Research Coverage PL’s Recommendation Nomenclature

50% 44.7% BUY : Over 15% Outperformance to Sensex over 12-months

42.7%

Accumulate : Outperformance to Sensex over 12-months

40%

% of Total Coverage

Reduce : Underperformance to Sensex over 12-months

30% Sell : Over 15% underperformance to Sensex over 12-months

20% 12.6% Trading Buy : Over 10% absolute upside in 1-month

10% Trading Sell : Over 10% absolute decline in 1-month

0.0% Not Rated (NR) : No specific call on the stock

0%

BUY Accumulate Reduce Sell Under Review (UR) : Rating likely to change shortly

DISCLAIMER/DISCLOSURES

ANALYST CERTIFICATION

We/I, Mr. Nishna Biyani (BE, MBA-Finance), Mr. Keyur Pandya (Mcom, MBA-Finance), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research

report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in

this report.

Terms & conditions and other disclosures:

Prabhudas Lilladher Pvt. Ltd, Mumbai, India (hereinafter referred to as “PL”) is engaged in the business of Stock Broking, Portfolio Manager, Depository Participant and distribution for third party financial products. PL is a

subsidiary of Prabhudas Lilladher Advisory Services Pvt Ltd. which has its various subsidiaries engaged in business of commodity broking, investment banking, financial services (margin funding) and distribution of third

party financial/other products, details in respect of which are available at www.plindia.com

This document has been prepared by the Research Division of PL and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to

others without prior permission of PL. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security.

The information contained in this report has been obtained from sources that are considered to be reliable. However, PL has not independently verified the accuracy or completeness of the same. Neither PL nor any of its

affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein.

Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend

upon the recipient's particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor.

Either PL or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies

referred to in this report and they may have used the research material prior to publication.

PL may from time to time solicit or perform investment banking or other services for any company mentioned in this document.

PL is in the process of applying for certificate of registration as Research Analyst under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

PL submits that no material disciplinary action has been taken on us by any Regulatory Authority impacting Equity Research Analysis activities.

PL or its research analysts or its associates or his relatives do not have any financial interest in the subject company.

PL or its research analysts or its associates or his relatives do not have actual/beneficial ownership of one per cent or more securities of the subject company at the end of the month immediately preceding the date of

publication of the research report.

PL or its research analysts or its associates or his relatives do not have any material conflict of interest at the time of publication of the research report.

PL or its associates might have received compensation from the subject company in the past twelve months.

PL or its associates might have managed or co-managed public offering of securities for the subject company in the past twelve months or mandated by the subject company for any other assignment in the past twelve

months.

PL or its associates might have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months.

PL or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months

PL or its associates might have received any compensation or other benefits from the subject company or third party in connection with the research report.

PL encourages independence in research report preparation and strives to minimize conflict in preparation of research report. PL or its analysts did not receive any compensation or other benefits from the subject

Company or third party in connection with the preparation of the research report. PL or its Research Analysts do not have any material conflict of interest at the time of publication of this report.

It is confirmed that Mr. Nishna Biyani (BE, MBA-Finance), Mr. Keyur Pandya (Mcom, MBA-Finance), Research Analysts of this report have not received any compensation from the companies mentioned in the report in

the preceding twelve months

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his

or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

The research analysts for this report has not served as an officer, director or employee of the subject company PL or its research analysts have not engaged in market making activity for the subject company

Our sales people, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein,

and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all o

the foregoing, among other things, may give rise to real or potential conflicts of interest.

PL and its associates, their directors and employees may (a) from time to time, have a long or short position in, and buy or sell the securities of the subject company or (b) be engaged in any other transaction involving

such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company or act as an advisor or lender/borrower to the subject company or may have any

other potential conflict of interests with respect to any recommendation and other related information and opinions.

DISCLAIMER/DISCLOSURES (FOR US CLIENTS)

ANALYST CERTIFICATION

The research analysts, with respect to each issuer and its securities covered by them in this research report, certify that: All of the views expressed in this research report accurately reflect his or her or their personal

views about all of the issuers and their securities; and No part of his or her or their compensation was, is or will be directly related to the specific recommendation or views expressed in this research report

Terms & conditions and other disclosures:

This research report is a product of Prabhudas Lilladher Pvt. Ltd., which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are

resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to

satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and

trading securities held by a research analyst account.

This report is intended for distribution by Prabhudas Lilladher Pvt. Ltd. only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and

interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon

this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Prabhudas

Lilladher Pvt. Ltd. has entered into an agreement with a U.S. registered broker-dealer, Marco Polo Securities Inc. ("Marco Polo").

Transactions in securities discussed in this research report should be effected through Marco Polo or another U.S. registered broker dealer.

Digitally signed by RADHAKRISHNAN SREESANKAR

December 07, 2015 RADHAKRISHNA DN: c=IN, o=Personal, cn=RADHAKRISHNAN

SREESANKAR,

serialNumber=8859da2df03122989b585ad520865a4

32

N SREESANKAR f59be69fbc1b7ba2c5315941f987f41de,

postalCode=400104, st=MAHARASHTRA

Date: 2015.12.07 14:42:57 +05'30'You can also read