What's the rush? New housing market absorption rate metrics and the incentive to slow housing supply

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

What’s the rush? New housing market absorption rate

metrics and the incentive to slow housing supply

Cameron K. Murray∗

June 2, 2022

Abstract

Why do housing developers voluntarily slow their rate of new housing production when

they make money from selling new homes? This question lies at the heart of current aca-

demic and political debates about the effect of planning and zoning on housing markets.

Any answer must consider the market absorption rate—the rate of new sales that max-

imises economic gains to property ownership over time. How this rate varies with market

conditions, outside of any potential planning constraints, is hard to observe.

We propose four new absorption rate metrics; 1) the development rate ratio (DRR),

2) development rate variability (DRV), 3) the delay premium ratio (DPR) and 4) delay

premium variability (DPV). We calculate these metrics for a sample of nine approved major

Australian housing subdivisions (>3,000 dwellings), showing the enormous variation in the

pace of new housing lot supply and gains from delay.

The average rate of new housing production is 34% of the maximum rate (DRR) and the

minimum rate is just 7% of the maximum (DRV). Total revenue in these sample projects was

82% higher than the counterfactual of setting the price at the start and selling all new lots

at that minimum price (the DPR metric). A 204% difference in total revenue was available

if all new dwellings were sold at the highest observed price rather than the lowest price over

the project life (the DPV metric).

Keywords: Housing supply, Absorption rate, Variability

JEL Codes: R30, R31, R52

∗ HenryHalloran Trust, The University of Sydney, Camperdown NSW 2006. Email: c.murray@sydney.edu.au

This project was funded by the Henry Halloran Trust. https://sydney.edu.au/henry-halloran-trust/

1

1 Introduction and motivation

Current academic and policy debates about housing prices often focus on planning and zoning

regulations (Ihlanfeldt, 2007; Quigley & Rosenthal, 2005; Rodrı́guez-Pose & Storper, 2020). The

mechanisms by which different planning regulations can affect the private choices of property

owners to develop housing are debated (Greenhalgh et al., 2021). Empirical approaches to

identifying links between planning and housing market outcomes necessarily rely on assumed

counterfactuals about the density, location, and importantly, the overall rate of new housing

supply in the absence of such regulations. Missing from the debate is an understanding that

even in the absence of planning regulations there is a constraint on the rate of new housing

supply known as the market absorption rate (Letwin, 2018; Murray, 2022).1 This rate is the

result of many property owners of candidate development sites in a region making choices about

when and how fast to develop new housing.

In this paper we take a closer look the private choices of property owners regarding the rate at

which they develop housing when there are no regulatory barriers on their choices—that is, after

major subdivision projects are approved and sales have commenced. Doing so highlights how

variation in the absorption rate is determined by market conditions, not planning policy settings.

This helps refine our understanding of the potential mechanisms by which planning systems may

affect private new housing supply choices.

The economic logic behind the market absorption rate is described in (Murray, 2022). Property

owners maximise their returns over time via their choice of development density and their choice

of development rate. Higher density does not automatically mean faster new housing supply

since the optimal rate of supply is not related to development density.2 When demand is rising,

increasing the rate at which undeveloped property assets are developed to new housing increases

overall returns. But when market demand is falling or thin, with few buyers at current prices,

slowing the rate of new housing development increases returns.3 A barrier to communicating

the market absorption rate concept is that the value to delaying development is difficult to see.

After all, it can seem odd that housing developers will voluntarily slow their rate of new housing

production even though they make money from selling new homes.

The main contribution of this article is to present new market absorption rate metrics that show

the variability of new housing supply and the economic payoff from varying housing production

in response to market conditions. The metrics are as follows.

1. Development rate ratio (DRR) – average production rate to peak rate ratio

2. Development rate variability (DRV) – minimum production rate to peak rate ratio

3. Delay premium ratio (DPR) – average minus minimum price divided by minimum price

4. Delay premium variability (DPV) – maximum minus minimum price divided by minimum

price

1 TheUnited States Census Bureau adopts this language in their Survey of Market Absorption of New Multi-

family Units (SOMA), which describes the rate that new multi-family units are rented or sold into the market.

2 This can be seen by imagining a project with 100 approved dwellings selling at 5 per month. While selling,

the project is granted a new approval to double the density of later stages so that there are now 125 potential

dwellings in the project. If this future density change increases the current rate of sales, then the previous sales

rate was already sub-optimal.

3 Other factors like interest rates (the return on the cash gained after a sale), taxes on land ownership (that

reduce the return to retaining ownership of undeveloped land), and the ability to vary the density of development

in the future (a flexible planning system can make delay more profitable by allowing higher density in the future,

increasing the return to delay), all can have small effects on this optimal rate.

2

These metrics can be applied to major housing projects after approval to make visible how

the absorption rate regulates the pace of new housing and answer the question of why housing

developers choose to slow their rate of supply.

The DRR and DRV metrics describe the distribution of housing supply rates relative to their

peak rate. The peak rate demonstrates a rate of supply that is possible. Deviations below this

rate are private choices of property developers and the size of this deviation on average and at the

extreme is captured in these metrics. The DPR and DPV metrics describe the price distribution

over a project life relative to the minimum price in that project. Since the minimum price sold

reflects a profitable choice, deviations above this price reflect gains from delaying sales to future

periods with higher prices rather than selling all new housing at a set price as quickly as possible.

Both benchmarks for these metrics—the peak rate of supply and the minimum price—reflect

common arguments about how housing developers will sell as quickly and cheaply as possible but

for planning and zoning regulations. With a heated policy debate taking place in many countries

facing quickly-rising dwelling prices, simple metrics like these that can be easily understood by

a broad audience are valuable for communicating key the importance of the absorption rate

concept for housing supply policy.

For example, using these metrics we show that in a sample of large housing projects in Australia

with over 3,000 dwellings approved and sales data for at least five years, the average DRR is

about 34%, and the DRV is 7%. This is an enormous amount of variability in response to market

conditions, not planning regulation. We also show that varying the sales price over time increased

prices received in these projects by 82% on average (the DPR) compared to a counterfactual of

setting the price based on cost at the outset and selling all new dwellings at that minimum price.

Potential economic gains to delay can be large, with a 204% increase in price available if all new

dwellings were sold at the highest observed price rather than the lowest price over the project

life (the DPV).

To determine the robustness of this approach to understanding variation in the absorption rate

we also apply the metrics to housing development company data and to city planning data.

Doing so helps determine whether a similar level of variation to that seen at a project level also

occurs at higher levels of aggregation, like cities and companies, and hence housing markets as a

whole. These results are consistent with the project level data.

2 Relevant literature and policy context

Unlike previous housing booms, the 2000s housing boom led to a new focus on explanations from

the supply side of housing markets, which became broadly popular in the late 2010s as housing

markets recovered globally from the 2008-09 bust. Glaeser (2018) summarised the static cost-

based supply-side approach that has been widely adopted in these debates and informs many

recent academic debates.4

A parallel economic literature has taken a more dynamic approach to the question of housing

supply (Capozza & Li, 1994; Murphy, 2018; Murray, 2022; Guthrie, 2022). Unlike the static

cost-based analysis that focuses on optimal density, this research focuses more on the rate of

supply and the inter-temporal trade-off between developing more housing now or later.

Unfortunately, the concepts of density, location, and the rate of supply (the absorption rate)

4 Such as in Urban Studies in 2021 (Rodrı́guez-Pose & Storper, 2022; Manville et al., 2022) and elsewhere (Been

et al., 2019).

3are often conflated, hindering communication and understanding when different concepts are

applied. For example, upzoning an area can increase the density of development that occurs in

that area, but it may also shift development to that area away from neighbouring areas, with

potentially little or no impact on the total rate of housing supply across all areas.

This academic debate is closely tied to a policy debate about the effect of planning regulations

on new housing production. In the United Kingdom, the Barker Review of 2004, and Letwin

Review of 2018 both focussed on supply and planning regulation. In New Zealand, Auckland

City Council conducted a widespread major upzoning with their Unitary Plan in 2016, motivated

by supply-side arguments. In Australia, the 2022 Parliamentary Inquiry into Housing Supply

(the Falinski Inquiry) focussed on planning regulation and prices. These reviews occasionally

note the existence of the market absorption rate as a constraint on the rate of new supply, but

usually dismiss it. For example, during the Falinksi Inquiry, housing developers under oath said

that “rezonings won’t necessarily lead to lower housing prices” (Standing Committee on Tax and

Revenue, 2021). Before that, the Letwin Review concluded as follows.

...it would not be sensible to attempt to solve the problem of market absorption

rates by forcing the major house builders to reduce the prices at which they sell their

current, relatively homogenous products. This would, in my view, create very serious

problems not only for the major house builders but also, potentially, for prices and

financing in the housing market, and hence for the economy as a whole.

(Letwin, 2018, pp.8-9)

The absorption rate is a key issue in both the academic and policy debates, but one that is

ignored, overlooked, or assumed away. Finding a way to shine a light on this important concept

can help progress both debates and improve our understanding of housing markets.

3 Metrics and their interpretation

In this section, we note how each absorption rate metric answers a specific question. describe

how each metric can be applied to property sales data, and briefly note how the metric can be

interpreted in the context of housing supply policy debates.

3.1 Development rate ratio (DRR)

How fast did housing development occur compared to how fast it could have if all

housing was developed at the maximum observed rate?

The development rate ratio (DRR) is the ratio of the average production rate to the maximum

rate (see Equation 1). We use both the average monthly rate of sales over a three-month rolling

window and over a twelve-month window to smooth out any idiosyncratic variation. Sales can

be used as the measure of the speed of development in the case of build-to-order model (as is

the standard in Australia, for example) or new rentals in the case of build-to-rent models (as is

common in multi-family housing in the United States, for example). Both measures capture the

mechanism by which the rate of new housing supply is managed based on market conditions.

A lower number indicates that the new housing development proceeded more slowly than was

demonstrated to be possible in the observed sales or new rentals.

Average production rate

DRR = (1)

Maximum production rate

4This metric is a sense-check for claims that new housing is being built as fast as the planning

system allows. Once a subdivision or apartment building is approved by the planning system, only

the private choices of the developer determine how fast the approved new housing is developed.5

A DRR at, or close to, one means that the project was built near its maximum rate over its life.

However, a low DRR suggests that market choices lowered the rate of supply below what was

possible. For example, a DRR of 0.5 means that the rate of supply was on average half as fast

as it could have been. Or described differently, it is how much shorter the project timeframe

could have been if maximum production rates were sustained; a 10 year project with a DRR of

0.5 could have been completed in 5 years.

3.2 Development rate variability (DRV)

How much slower will developers produce housing compared to the maximum rate?

Development rate variability (DRV) is the ratio of the minimum production rate to the maximum

rate (as per Equation 2). Again, we use here the average monthly rate over three-month and

twelve-month rolling windows. The DRV shows the observed extent that private property owners

are willing to slow the rate of production in response to the market conditions even from approved

projects already under development. Like the DRR, rental rates or sales rates can be used

depending on the relevant market.

Minimum production rate

DRV = (2)

Maximum production rate

Calculating the DRV for a range of projects in a region provides evidence about the degree to

which the rate of new housing supply over time is being regulated by market conditions rather

than planning. For example, if the DRV for a range of projects was seen to be in the range of

0.05 to 0.20, then market conditions are generating variation in the rate of supply by a factor of

5 to 20 times.

3.3 Delay premium ratio (DPR)

How much higher are actual prices received compared to the minimum price?

The delay premium ratio (DPR) is the difference between the average price of dwellings in a

project and the minimum observed price as a ratio of that minimum price (see Equation 3). We

use three-month moving averages of price to remove noise.

Average price − Minimum price

DP R = (3)

Minimum price

The DPR metric highlights the economic gains available from regulating the rate of sales to

ensure they across time periods where prices are higher rather than selling as fast as possible at

the minimum price (usually the initial price). For example, a DPR of 0.5 means that the average

price, and hence revenue, was 50% higher than the minimum price over a project life. It would

also suggest that pricing of new dwellings is not based on costs and that controlling the rate of

5 Apartment projects often cannot be built in stages, but they will be sold over a long time period, usually

many years, with sales occurring before constructions (to hit pre-sale risk hurdles), during construction, and often

for years post construction. Even though construction itself might take 1-2 years, the sales make take 3-5 years,

or longer.

5supply to sell at opportune times vastly increases project revenues. It highlights the potential

magnitude of the economic incentive to produce new housing slower than is possible under given

planning conditions.

To further understand the magnitude of this incentive, it must be noted that profit margins are

usually a small share of the price, normally in the 10% to 30% range. In terms of the variation

in net economic returns, selling at an average price 50% higher than the minimum over a project

life, assuming a profit margin of 20% if sold at the minimum price, is a more than tripling of

profits (3.5 times the profit). How big these gains are in the dollar value terms can be calculated

by multiplying the DPR by the minimum price and by the number of dwellings in a project.

3.4 Delay premium variability (DPV)

How much higher is the maximum price received compared to the minimum price?

The DPV metric shows the full range of variation in price over a project lifetime as a ratio of

that minimum price (see Equation 4). We again use three-month moving averages of price to

remove noise.

Maximum price − Minimum price

DP V = (4)

Minimum price

Like the DPR, the DPV highlights the scale of economic gains from delay, though in this case it

shows the size of the full range of price changes over a project life. A DPV of 0.9, for example,

means that the maximum price received was 90% higher than the minimum price. If all new

dwellings were sold at the maximum price instead of the minimum this is also the proportional

gain in revenue available. In situations where the price at the end of the project is highest, and

lowest at the beginning, it shows the size of the value gains had the whole project to date been

delayed to instead start in the latest high value period, and hence points to the value of delaying

housing projects altogether.

4 Application of metrics

For this demonstration we use complete Australian property sales records sourced from data re-

seller CoreLogic. Our available data covers the period January 2001 to January 2020 in the major

states of Queensland, New South Wales and Victoria. The ultimate sources of these records are

state land titles offices, where property transaction dates and prices are recorded.

We focus on major land subdivisions with over 3,000 housing lots that were actively selling for

more than five years during the period of data coverage. Focussing on land alone neatly shows

the net financial incentives without having to account for construction costs of new homes to

determine the net gains from property development. We chose nine major housing subdivisions

spread across the major states on the outskirts of the capital cities. Descriptions of each subdi-

vision project are Table 1. These projects were chosen because of their size (being a substantial

share of local new housing supply), their location (on the fringes of capital cities) and because

they are predominantly land subdivisions, and hence prices can be applied on a per land area ba-

sis to the DPR and DPV counterfactuals for the subset of sales that are land only (i.e. prices for

these two metrics are on a dollar-per-square-metre basis and total production for these metrics

is measured by land area not lots).

6Table 1: Description of major subdivision sample projects

Project State Start Total Lots in Owner Type Location

name year lots sample

Atherstone VIC 2012 4,300 1,372 Lendlease Public 40km W of Melb.

Aura QLD 2016 >20,000 1,188 Stockland Public W of Caloundra

Googong NSW 2012 5,961 1,454 Mirvac Public Outskirts of ACT

Jordan Springs NSW 2010 4,800 2,890 Lendlease Public 55km W of Syd.

Manor Lakes VIC 2004 4,996 2,832 D.F.2 Private 37km W of Melb.

Springfield QLD 19941 >32,000 9,814 S.L.C.3 Private 32km SW of Bris.

Willowdale NSW 2013 3,722 2,098 Stockland Public 40km SW of Syd.

Woodlea VIC 2015 6,584 1,563 V.I.P. 4 Private 39km W of Melb.

Yarrabilba QLD 2011 >17,000 3,165 Lendlease Public 38km S of Bris.

1

Data from 2001 only. Subdivision began in 1994 and is ongoing as of 2022.

2

Denniss Family.

3

Springfield Land Corporation often in conjunction with other developers for delivery of project stages.

4

Victoria Investments and Properties Pty Ltd (partnered with Mirvac).

To select the relevant new property sales data from the complete record of property sales, latitude

and longitude property coordinates are used to ensure sales reflect new lots falling with the

subdivision boundary. Sales dates are chosen to be after the start date of the first stages of each

project, with only the first sale of each lot being used. Lot sizes are selected to include only those

falling within the range of sizes in the subdivision plan. In many cases the projects included

townhouses and apartments and these sales were not included. All projects remained in progress

as of the end of 2020. We use the data to calculate the absorption rate metrics to sales contracted

prior to January 2020, as investor publications of some of the publicly-listed companies in our

sample show that during financial year 2020-21it became common for new sales contracts to be

signed, and deposits taken, that are conditional upon completion of future stages that were not

ready for settlement.

We also note that there is likely some missing data in our sales records. If we compare this sales

data and the reported sales in financial reports of the publicly-listed companies that own some

of the sample projects, the sales data is generally lower than the company-reported reported

sales and settlement data. For example, Mirvac, owner of Googong and Woodlea projects, has

reported project level sales and/or settlements in some of their end of year results. In 2016 the

company reported 889 sales in Woodlea and only 415 settlements, while Corelogic records have

560 sales that year. In Googong that year the company reported 343 sales and 525 settlements,

while the Corelogic records showed 208 sales. There is clearly both a long delay between sales

and settlement, and smoothing of sales into settlements across different time periods. This

makes sense, as listed companies have incentives to stabilise revenue streams by smoothing out

settlements, when full payments occur, and to stabilise rates of physical construction activity.

To determine whether potential missing data is undermining the accuracy of the metrics we also

look at company data in Section 5 and city level data. With additional diversity of supply at

these higher levels of aggregation, they represent upper bounds of project level metrics, and a

close correspondence would imply that market as a whole has similar absorption rate constraints

as individual projects.

7Table 2: Application of metrics to selected major subdivisions

Project DRR DRR DRV DRV DPR DPV DPR DPV DPR

3 m. 12 m. 3 m. 12 m. 3 m. 3 m. × prod. × prod. per lot

($m) ($m) ($’000)

Atherstone 0.21 0.46 0.04 0.14 0.42 1.15 61 170 44

Aura 0.45 0.57 0.29 0.39 0.15 0.37 36 89 30

Googong 0.42 0.47 0.08 0.11 0.53 1.06 193 385 133

Jordan Springs 0.34 0.40 0.04 0.07 0.59 1.33 333 753 115

Manor Lakes 0.29 0.37 0.03 0.07 1.25 4.13 215 711 76

Springfield 0.25 0.44 0.04 0.12 3.03 7.27 1,201 2,880 122

Willowdale 0.38 0.46 0.08 0.23 0.53 1.05 228 455 108

Woodlea 0.32 0.39 0.03 0.07 0.46 1.23 98 264 63

Yarrabilba 0.37 0.42 0.06 0.07 0.43 0.78 161 290 51

Mean 0.34 0.44 0.07 0.14 0.82 2.04 83

!

Adjacent to the ACT border and hence a satellite of Canberra.

∗

Data from 2001 only. Subdivision began in 1994 and is ongoing as of 2022.

In Table 2 we summarise the four absorption rate metrics. The 0.34 mean DRR shows that the

average rate of new housing production is a third of the demonstrated maximum possible rate,

which is a little higher when using twelve month moving average rate of monthly sales, at 0.44.

A DRR value this low suggests that the rate of new housing production is not being maximised

but managed. This is further shown by the low DRV metric across all projects. Looking at three

month windows, the DRV was 0.07 on average, though this would be only 0.05 if the newest

project, Aura, was excluded from the sample. Even using a twelve month average rate, the DRV

was 0.14 on average, and 0.11 if Aura is excluded. This means that some years the rate of sales

is seven to nine times higher than other years during a project life.

To show visually the patterns the DRR and DRV metrics are capturing, Figure 1 shows a

histogram of the monthly rate of sales for all projects combined. The strong left skew is not

expected in a scenario where planning the binding constraint on the rate of new supply. If that

were true, there would be a strong right skew towards supplying new homes near the maximum

rate from approved projects.

Moving to the metrics of the premium from delay, we see a delay premium ratio (DPR) of 0.82

across these sample projects. This implies that the price received per square metre on average

across all new land sales was 83% higher than the minimum sale price. If we assumed that the

minimum price covered costs, this metric highlights just how large the gains are for landowners

from managing their production rates over time to both avoid flooding the market to decrease

prices, and selling in later periods when prices are higher. In terms of the dollar value of this

additional revenue, these were typically in the tens to hundreds of millions (third to last column).

It is easy to see how such large values arise. For example, an extra $200/sqm for a 400sqm lot is

$80,000. Multiply this by just one hundred lots and that is already $8 million. Prices per square

metre of land were on average $653/sqm in this sample of projects, and varied by $517 between

their lowest and highest prices. If profit margins are 25% at the minimum price, then a DPR of

0.83 implies a 332% increase in profits by managing sales rates to achieve higher prices later .

8Figure 1: Distribution of monthly sales rates in sample projects combined

Indeed, the DPV of 2.04 shows that the difference in revenue between selling all lots that max-

imum price rather than the minimum would have generated 204% more revenue. If all new

housing lots are sold quickly at the initial price, these higher priced future sales opportunities

are missed. This also shows the payoff in terms of the change in the value of land for a neighbour-

ing property owner who has the option to develop but chooses instead to wait. The same applies

to staging of these project themselves. Future stages of this sample of projects, if considered

as their own individual projects, will earn a price 204% higher than the first stages. Longer

term projects, such as Manor Lakes and Springfield, saw much higher DPR and DPV metrics,

as expected given the housing price growth seen in Australia since 2000.s

The additional revenue obtained in these projects because of selling above the minimum price is

exceptionally large in dollar terms, ranging from $60 million to $1.2 billion. On a per lot basis

across all projects the average lot was sold $83,000 above the corresponding minimum price in

that project.

We can look in more detail at one of the projects, Atherstone, to see the underlying patterns

reflected in these metrics. In Figure 2 we see in the top left panel the land price per square

metre over time during the life of the project. When the project began the price was around

$400/sqm in 2012. It stayed relatively flat until 2017 when it jumped to around $600/sqm. This

was a period in which sales increased from five per month to over 60 per month, a twelvefold

increase (top right panel). The relationship between price growth and supply is more clear in

the bottom left panel, and the low average rate of supply alongside huge variation in it is shown

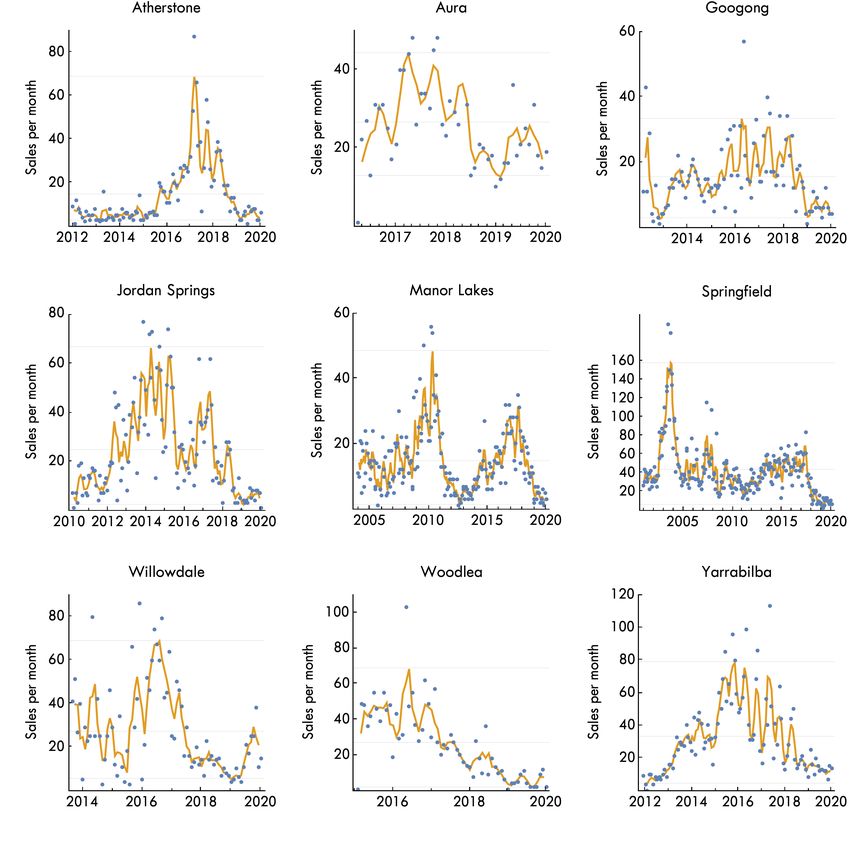

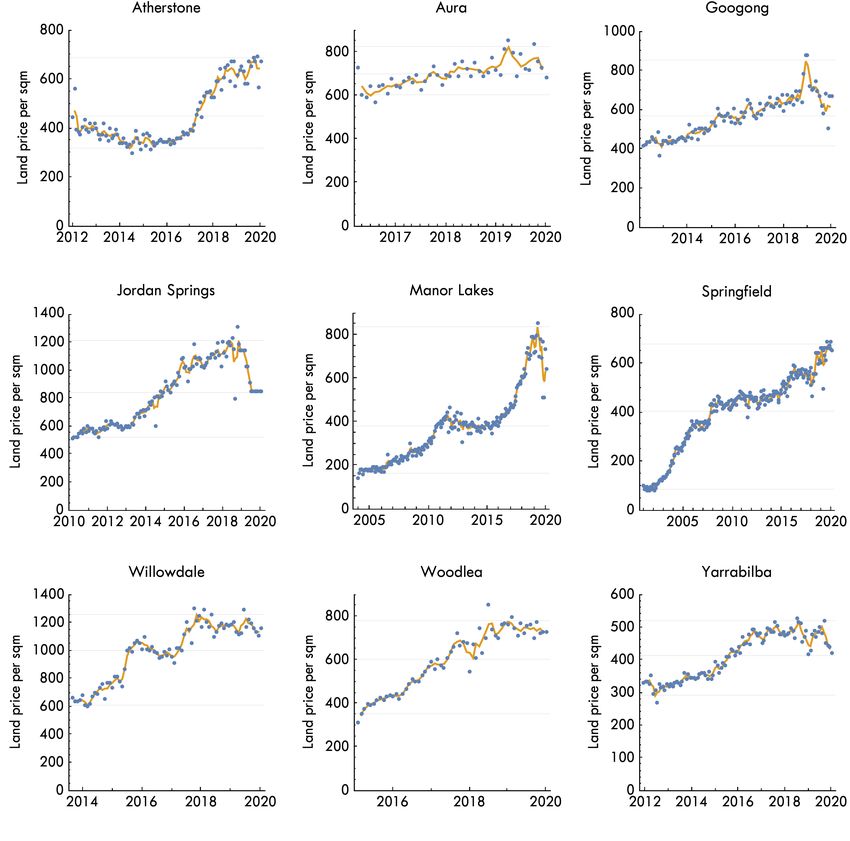

in the bottom right histogram.6 Plots of the rate of new lot sales and land prices in each project

are in Figures A1 and A2 of the Appendix.

6 Land price growth and sales rates in the bottom left panel are plotted after applying a gaussian filter over a

three month window to each variable.

9Figure 2: Sale rate and prices for the Atherstone project (Victoria)

5 Alternative metric applications

Though we focus on approved housing projects to highlight how variation in the rate of supply

arises after planning approvals, the absorption rate metrics can also be applied to other data.

Doing so reveals whether larger markets operate similarly to individual projects in terms of the

absorption rate being heavily regulated by market factors.

5.1 Development company data

Using company data directly as the basis for absorption rate analysis can be done using state-

level residential sales data reported by Stockland, a publicly-traded company that has projects

in our main data sample. They are the only company that reports quarterly sales data across

the four states they operate in, which they have done since 2012 for all types of dwellings within

their residential projects. The DRR and DRV absorption rate metrics applied to this data are

10in Table 3, using both quarterly and annual periods, and the quarterly rate of new housing lot

production in each state is in Figure A3 of the Appendix. These metrics reveal less variability

than the DRV and DRR using 3 month average rates at a project level from Table 2, which is

expected as there is a diversity of projects in each state.

What this exercise shows is that even across many projects in a state, the variability in the rate

of supply is quite large, with the minimum rate of sales usually being only 22% of the maximum

rate, and the average rate about half, suggesting a large degree of sensitivity to market conditions.

Even taking a whole year period, the average year has 60% of the sales of the peak year, and

the minimum year has 34% in each state. Given that this applies to across 10 projects in each

state on average suggests that the variation in the rate of supply at a project level must me

much larger, implying much lower DRR and DRV metrics. As such, these measurements allay

concerns about any missing data in the property sales records being a major factor creating an

abnormally low value of the DRR and DRV metrics.

The interpretation of the metrics applied at this scale is less clear, however. Planning may

influence the variation in sales. But it is nevertheless interesting to read the company source

reports, as they make no mention of planning rules being the cause of the rate of sales. These

reports instead note that market conditions are the most important determinant of the rate of

sales.

Table 3: Company level housing production

State Projects DRR DRR DRV DRV

in state Quarterly Annual Quarterly Annual

Queensland 18 0.68 0.74 0.41 0.55

New South Wales! 7 0.39 0.46 0.11 0.20

Victoria 10 0.52 0.65 0.18 0.32

Western Australia 6 0.46 0.56 0.19 0.29

All states total 41 0.66 0.75 0.37 0.53

Mean of states 10 0.51 0.60 0.22 0.34

!

Includes Australian Capital Territory

Data from 1Q2012 to 4Q2021 from annual reports

5.2 Aggregate city data

Another application for these absorption rate metrics is city-wide planning data. This can show

the degree to which variation in new dwelling supply arises from market choices to develop

housing out of the stock of approved projects. Small DRR and DRV metrics would imply a high

degree of variation that is hard to explain based on planning rules rather than market conditions

regulating the rate of new housing supply. They would instead support the idea that regional

markets as a whole face similar absorption rate constraints to individual projects.

In Table 4 we show the DRR and DRV using the quarterly new housing lot registration data

for councils in south east Queensland from March 2002 to December 2021 for both attached and

detached dwellings.

Notice that even at a regional market level (council area rather than subdivision project area)

that there is a similar degree of variation to that seen in individual major subdivision projects.

11The DRR is just 0.39 across all council areas, and the mean DRV of 0.10 implies that the

maximum rate of new housing production in a quarter is ten times the minimum. Plots of the

quarterly rate of new housing lot registrations (attached and detached) in each council area are

in Figure A4 of the Appendix.

To show that the stock of approvals was not a factor at play, we show in the final column of Table

4 the mean ratio of quarterly lot completions to the stock of approvals. The data on the stock

of approvals, however, is only available for detached housing lots, so we only include detached

lot and approvals data. The amount of dwellings in the approved pool in was typically 10 to

20 times larger than the quarterly lot completions, and grew over this period for nearly every

council, suggesting that the approval process was not a constraint on these rates of supply. At

a city level, the pace of new housing appears to market conditions with a similar amount of

variation as individual housing project.

Table 4: Council lot registration absorption metrics

State DRR DRV Mean ratio

Quarterly Quarterly (qtrly new lots per

approved stock)

Brisbane 0.43 0.20 0.11

Gold Coast 0.48 0.12 0.09

Ipswich 0.41 0.07 0.07

Lockyer Valley 0.31 0.01 0.05

Logan 0.48 0.13 0.08

Moreton Bay 0.64 0.30 0.10

Noosa 0.22 0.01 0.11

Redland 0.41 0.06 0.10

Scenic Rim 0.26 0.02 0.05

Somerset 0.17 0.00 0.04

Sunshine Coast 0.48 0.12 0.09

All councils total 0.61 0.30 0.07

Mean of councils 0.39 0.10 0.08

Data from 1Q2001 to 4Q2021 from Queensland Government Statisti-

cian’s Office

Lot registrations for DRR and DRV are for detached and attached lots.

Mean ratio of new lots to stock of approved lots is for detached only, as

stock of approved lots is not available for attached dwellings.

6 How these metrics contribute to current debates

Taken together, this suite of new metrics highlights the central role of the market absorption rate

in determining how fast new housing is produced. Their application to major housing projects

in Australia shows that housing producers are extremely sensitive to market conditions in their

choice of the rate of new supply, and that the financial gains to adapting sales rates and prices

to market conditions are substantial. We show that our approach to using property sales records

12matches closely the approach of using company sale records, where available, though there is

some discrepancy about the overall extent of variation in the rate of sales (the DRV). Adding

to this, we have applied the new absorption rate metrics at a company level to show the high

degree of variation in the rate of new supply even at this aggregate level. A further level of

aggregation to council areas shows similar variability in the rate of supply to that seen at a

project level. These new metrics can be applied in many ways to illustrate that the absorption

rate of new housing appears predominantly market determined rather than the result of planning

regulations.

The fact that the rate of supply on major approved projects is typically far below the maximum,

and varies by a factor of 14 or more, suggesting that any mechanism by which planning regulations

lead to housing price effects must deal with an additional constraint in the form of the absorption

rate.

If there is an optimal absorption rate, individually and collectively for new housing in a market,

how might planning regulations affect this rate? This is a missing question in both the academic

and policy debate. But with this new way of communicating the importance of the absorption

rate and the economic motive behind it, perhaps such debates can quickly evolve.

To progress these potentially more fruitful debates we briefly outline a handful of potential

arguments about the relationship between planning regulations and the market absorption rate,

and address each by drawing on the evidence generated by these new metrics.

One potential line of reasoning is that the planning system is not responsive enough, and hence

delays for planning approvals cause delays to supply when market conditions turn favourable,

and when market conditions revert there is not incentive to “catch up” with supply. However, the

argument implies that market housing producers are incapable of investing in a buffer stock of

approved sites to accommodate variability in demand. Indeed, the DRR and DRV show that the

market does invest in large buffer stocks of approvals, as does the evidence of council approvals

in Table 4. Even if this were an accurate representation of how planning affected the absorption

rate, then the quantity effects would be extremely small even over decades, as there are few

infrequent boom periods.

Another argument is that planning or zoning reduces supply because only a small share of

developable sites are economically viable, creating market power. Large scale rezoning creates

many more viable sites (where price exceeds development cost) resulting in faster production

because of price competition. This is the mechanism Glaeser (2018) describes as the way planning

regulations modify the “supply curve”. However, the housing development market is competitive

by any standard measure, such as the Herfindahl-Hirschman Index (HHI). In 2018 the top twelve

Australian housing developers supplied only about 9% of new homes nationally, suggesting a

HHI in the range of 0.0016 to 0.0025 (Murray, 2020).7 This is below the tenth percentile of

HHI estimates for Australian industries, indicating an extremely competitive market (Bakhtiari,

2019). Furthermore, the same high property prices, unequal access to property ownership, and

enormous land price cycles happened historically before the invention of zoning, and were defining

characteristics of the property markets of the 1800s in countries like Australia the United States

and United Kingdom. Market power seems inherent to property systems (Posner & Weyl, 2017).

Lastly, an argument might be that without planning regulations (or zoning) the same variability

in the absorption rate will occur but at a higher average rate. However, if at every point in time

7 The upper end of the range is based on the next dozen housing developers being equally as large as the first

dozen, before market share drops below 1%, and the lower end is if market share of the remaining firms are all

below 1%.

13the market wishes to develop housing faster, it could, as the variation in the absorption rate

shows what is possible. This line of reasoning relies on the idea that under the same market

conditions and the freedom to choose the rate of supply, the very existence of a zoning system

changes the optimal rate. It appears to be a competition argument in disguise.

7 Conclusion

New ways to communicate the market absorption rate and the economic motives behind it are

an important step in progressing academic and policy debates about planning, housing supply

and prices. By highlighting the variability of the absorption rate with new metrics that can be

applied at a project level, company level, or city level, a clearer picture of how market conditions

regulate the supply of new housing emerges. Future studies of planning regulations and their

effects on housing supply must address the mechanism by which planning regulations affect the

absorption rate.

14References

Bakhtiari, Sasan. 2019 (September). Trends in Market Concentration of Australian Indus-

tries. Research Paper 8/2019. Department of Industry, Innovation and Science. Australian

Government.

Been, Vicki, Ellen, Ingrid Gould, & O’Regan, Katherine. 2019. Supply skepticism:

Housing supply and affordability. Housing Policy Debate, 29(1), 25–40.

Capozza, Dennis, & Li, Yuming. 1994. The Intensity and Timing of Investment: The Case

of Land. The American Economic Review, 84(4), 889–904.

Glaeser, Edward, & Gyourko, Joseph. 2018. The Economic Implications of Housing

Supply. Journal of Economic Perspectives, 32(1), 3–30.

Greenhalgh, Paul, McGuinness, David, Robson, Simon, & Bowers, Kathryn. 2021.

Does the Diversity of New Build Housing Type and Tenure Have a Positive Influence on

Residential Absorption Rates? An Investigation of Housing Completion Rates in Leeds City

Region. Planning Practice & Research, 36(4), 389–407.

Guthrie, Graeme. 2022. Land Hoarding and Urban Development. The Journal of Real Estate

Finance and Economics.

Ihlanfeldt, Keith R. 2007. The effect of land use regulation on housing and land prices.

Journal of Urban Economics, 61(3), 420–435.

Letwin, Oliver. 2018 (October). Independent Review of Build Out Rates - Final Report. Tech.

rept. Ministry of Housing, Communities and Local Government.

Manville, Michael, Lens, Michael, & Monkkonen, Paavo. 2022. Zoning and affordabil-

ity: A reply to Rodrı́guez-Pose and Storper. Urban Studies, 59(1), 36–58.

Murphy, Alvin. 2018. A dynamic model of housing supply. American Economic Journal:

Economic Policy, 10(4), 243–67.

Murray, Cameron K. 2020. Time is money: How landbanking constrains housing supply.

Journal of Housing Economics, 101708.

Murray, Cameron K. 2022. A Housing Supply Absorption Rate Equation. The Journal of

Real Estate Finance and Economics, 64(2), 228–246.

Posner, Eric A, & Weyl, E Glen. 2017. Property is only another name for monopoly.

Journal of Legal Analysis, 9(1), 51–123.

Quigley, John M, & Rosenthal, Larry A. 2005. The effects of land use regulation on the

price of housing: What do we know? What can we learn? Cityscape, 69–137.

Rodrı́guez-Pose, Andrés, & Storper, Michael. 2020. Housing, urban growth and inequal-

ities: The limits to deregulation and upzoning in reducing economic and spatial inequality.

Urban Studies, 57(2), 223–248.

Rodrı́guez-Pose, Andrés, & Storper, Michael. 2022. Dodging the burden of proof: A

reply to Manville, Lens and Mönkkönen. Urban Studies, 59(1), 59–74.

Standing Committee on Tax and Revenue. 2021. Housing affordability and supply in

Australia (26/11/2021 transcript). Tech. rept. Parliament of Australia.

15Appendix

Figure A1: Sales rates in subdivision sample projects (three month moving average line)

16Figure A2: Prices of new detached housing lots in subdivision sample projects ($/sqm)

17Figure A3: New housing lot production rate, attached and detached, Stockland state level

18Figure A4: Quarterly new housing production (attached and detached) in Queensland councils

19You can also read