Who is willing to buy an electric vehicle in France? Electric vehicle penetration split by household segments - eceee

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Who is willing to buy an electric vehicle in France? Electric vehicle penetration split by household segments Franck Pernollet Christophe Crocombette EDF R&D EDF R&D Avenue des Renardières – Ecuelles Avenue des Renardières – Ecuelles 77818 Moret-sur-Loing 77818 Moret-sur-Loing France France franck.pernollet@edf.fr christophe.crocombette@edf.fr Jean-Michel Cayla EDF 22 avenue de Wagram 75008 Paris France jean-michel.cayla@edf.fr Keywords electric vehicles, willingness to pay, market barriers, house- likely to be households with either low income or with limited holds, plug-in hybrid electric vehicle annual mileage. Around 2025, these people are likely to buy 30 or 40 kWh BEV since BEV TCO shall be cheaper and they are ready to have autonomy constraints. Then, in 2030, high Abstract income and long distance drivers are likely to buy PHEV in Although electric vehicles (that is to say battery electric ve- order to avoid autonomy constraints whereas medium income hicles (BEV) and plug-in hybrid vehicles (PHEV) economic and long distance drivers should prefer 80 kWh BEV which is interest seems already acquired for some mobility needs, EV a good compromise between cost and autonomy. This article adoption by households still raises questions.This paper exam- also shows that BEV should spread faster for large and medium ines EV diffusion in France taking into account monetary and vehicles than for small vehicles. In particular, without ban, a non-monetary drivers. Barriers to this diffusion are examined significant proportion of people having a small car, with me- based on a discrete choice experiment among 12,000 future dium or high revenue and small or average rider in 2040 is still vehicle buyers in France. Willingness to pay (WTP) for au- expected to buy small ICV. Finally, this paper highlights that tonomy, charging time, charging point density and EV specific people who have no easy access to charge at their homes are criteria were calculated for different household types distin- more reluctant to buy BEV. guished by standard of living, annual mileage and charging point installation facility at home. Then these non-monetary attributes were included to a traditional investment behaviour Introduction model based on a total cost of ownership (TCO) calculation Global warming is one of the 21st century major challenges. to estimate EV market share. This paper examines which type Many states settled with the Paris Agreement (United Na- of household segments are likely to buy EV at different time tions, 2015) to reach carbon neutrality by 2050. Huge efforts horizons. It shows that it is essential to take into account non- must be done by the different sectors : residential, industry, monetary attributes to correctly simulate EV diffusion. Indeed, transport. In France, the transport sector represents 30 % of even though, in the near future, BEV TCO will be lower than national GHG emissions. To reach carbon neutrality in this internal combustion vehicle (ICV) TCO, the probability that a sector, among other main solutions (vehicle energy efficiency, purchaser will not buy a BEV could also be influenced by non- demand control, modal shift), shift to electric motorization monetary constraints such as autonomy or time to refuel. By is one of the main and inevitable solutions (MTES, 2018) taking into account non-monetary attributes, we can assume (MTES 2, 2018) (Briand Y., 2017). Since light vehicules (pas- that BEV diffusion should not be as fast as expected by analy- senger car and light commercial vehicle) represent 73 % of ses that only rely on monetary attributes. In an EV-friendly GHG transport emissions in France (CGDD, 2018), we will scenario, we found that BEV buyers from 2020 to 2025 are focus on these vehicles. ECEEE SUMMER STUDY PROCEEDINGS 1035

6-103-19 PERNOLLET ET AL 6. TRANSPORT AND MOBILITY Table 1. Motorization modelled in IMMOVE-PBM. BEV (autonomy estimated for small ICV PHEV and large car in 2030) BEV 30 kWh (160-240 km) Stop-start gasoline BEV 40 kWh (210-310 km) PHEV 40 km electric autonomy Stop-start diesel BEV 60 kWh (305 - 445 km) PHEV 80 km electric autonomy Full hybrid gasoline BEV 80 kWh (395 - 570 km) PHEV 120 km electric autonomy Full hybrid diesel BEV 100 kWh (481-688 km) BEV 120 kWh (560 - 795 km) New technologies always raise questions about penetration choose between 4 cars with different characteristics. WTP for conditions and their potential diffusion speed. In recent years, autonomy, charging time, charging point density, EV specific more and more studies are dedicated to electric vehicle (EV) criteria were calculated for different household types. There- diffusion modeling (Gnann, 2018). These studies have differ- fore we can see which households are likely to buy EV and ent motorization scopes: EV, BEV, PHEV, ICV, hybrid vehicle when, and what BEV type (autonomy level) could be bought. (HV); they vary on the vehicle types which are studied: light This paper studies EV diffusion in the French market from vehicle, private personal car, company personal car, light com- 2015 to 2040 for personal private cars. In a first part we discuss mercial vehicle, fleet vehicle; on the scale studied: local (Ahka- about model specifications and data, in a second part we focus miraad A., 2018), country (Wu G., 2015), continent (Pasaoglu on characteristics of potential future EV adopters in a friendly G., 2016), world (IEA, 2018); on the geographic zone : United EV scenario, and finally, we discuss some limits of the model. States (Brooker A., 2015), China (Qian L., 2015), Germany (Pfahl S., 2013), France (Fernandez-Antolin A., 2018). Lots of approaches are used to simulate this diffusion (Al-Alwi Methodology B.M. 2013) (Gnann T. 2018): disaggregated models (Pasaoglu G., 2016) with details at individual scale (more often agent-based IMMOVE-PBM MODEL model); sales models or consumer choice models which study The main purpose of the model is to better understand the different markets or customers segments using discrete choice personal private car sales diffusion of different motorization models or logit models; aggregated models (Becker T.A., 2009) car in the long term for different household segments. We thus using diffusion rate or time series models with macro simula- combine a traditional investment behaviour model based on tions; or mixed methods (Brown M., 2013). The goal of our study TCO with WTP for non-monetary attributes. is to understand who will be willing to buy BEV and PHEV and We then study 90 car buyer household segments by consid- on what conditions. That is why we choose a sales model. ering annual kilometers (5 classes: very small rider, small rider, Our study combined a traditional investment behaviour medium rider, high rider, very high rider), income (3 classes: low model based on a total cost of ownership (TCO) and an as- income, medium income, high income), dwelling type (2 class- sessment of the willingness to pay (WTP) for main EV barri- es: easy access to charge at home and difficult access to charge), ers such as autonomy, charging time, charging point density car type (3 classes: “small”, “medium”, “large”). Household seg- in order to estimate BEV diffusion. The WTP is the maxi- ment market shares are calibrated for 2016 thanks to a survey mum price at or below which a consumer will definitely buy of 12,000 people representative of future private car buyers in one unit of a product (Varian Hal. R, 1992). Lots of studies France, in which we only selected people willing to buy a new car look on WTP for different characteristics wich are specific in their near future (6,766 people). Company cars are not looked to BEV (Hackbarth A., 2016) (Hidrue M.K., 2011) (Tanaka in this paper. We focus on new car purchasers, second hand cars M., 2014) (Pernollet 2019), or propose investment models are not considered here, that is why high income class has higher based on TCO (Wu G. 2015) but few take into account both market share (56 %) than medium income class (27 %) and than the economic aspect and the non-monetary barriers. Pfahl low income class (17 %), these market shares are differentiated (Pfahl S., 2013) proposes a global diffusion factor for EV to among car segment small, medium, large (see Figure 8). The take into account limited offer, limited charging stations and “large” class was a bit overestimated since all SUVs were consid- new technology fear but these attributes are not differentiated ered as large cars in the survey1. In 2015, each segment represents among households. Yet, some attributes like WTP for auton- a market share from 0.23 % to 5.1 %. Household characteristics omy are likely to vary greatly from household to household. (car type, income levels, annual kilometers) are supposed to Plötz (Plötz P., 2014) adds wilingness to pay more for BEV to be constant from 2015 to 2040 at the exception of the share of traditional TCO and a corrective coefficient to take limited people having easy access to charge share which change from offer into account, but instead of considering limited autono- globally 58 % in 2015 to 85 % in 2040 (see Figure 8). Finally, we my disadvantage, he simply eliminates BEV if some trips are consider 13 motorization vehicles (Table 1). not compatible with a preselected autonomy range. In our For each year, for each household segment and for each mo- study, we calculated a limited autonomy disavantage among torization, we calculate the generalized TCO: it includes the different household segments and design BEV with different autonomy levels. We did a discrete choice experiment among 12,000 future vehicle buyers in France to characterize barri- 1. In survey there were 27 % small vehicles, 32 % medium vehicles, 40 % large ers and levers to EV diffusion. Each respondent were asked to vehicles. 1036 ECEEE 2019 SUMMER STUDY

6. TRANSPORT AND MOBILITY 6-103-19 PERNOLLET ET AL traditional monetary TCO and the value of the additional non- lated considering that people buy the car and not lease the car. monetary constraints (autonomy, load point density, load time However the difference on TCO result is marginal. Leasing has and other attributes) to reach ICV performance (equation 1). more a psychological impact on purchase choice by avoiding the As the population is divided into small market shares, to sim- BEV high investment cost and changing the owning way. plify the model, households are supposed to invest in the type 1 of vehicle that presents the lower generalized TCO. More com- ∗ + ∗ ∑E &FG (1 + )& plex rules could be used (Pfahl S., 2013) TCO $%&'()*+/-$ monetary/km = TCOgeneralized = TCOmonetary + WTPautonomy Initial price = (Car initial purchase pricewithout battery + WTPcharge point density + WTPcharge time + Battery pack cost + bonusmalus + WTPmotorization + WTPincentives (1) + registration certificate – residual car price present value Figure 1 summarizes the diffusion model overall approach. – residual battery price present value + home charger price) ∗ (1 + )' MONETARY TCO Capital recovery factor CRF = ((1 + )' − 1) To calculate the monetary part of the TCO, formula (2) is used. with α is the discount rate and N is vehicle depreciation Its parameters values come from automotive constructors, pub- period lications and expert assumptions (Insee, 2011). The main values are summarized in Table 2. These assumptions rely on a scenario Annual operating cost AOC up to 2040 in which the French regulatory context foster the de- = (energy price per km + fuel tax) * consumption per km velopment of EV to reach environmental targets. TCO is calcu- * annual milage + maintenance + insurance (2) Figure 1. Global methodology for market share sales (IMMOVE-PBM model). Table 2. Main assumptions used for car TCO (price in €2015). BEV PHEV Stop-start gasoline Full hybrid gasoline 2020 2025 2030 2040 2020 2025 2030 2040 2020 2025 2030 2040 2020 2025 2030 2040 Battery cost par kWh (production without margin, tax …)($/kWh) 135 113 92 70 160 135 109 83 Battery price for BEV60 kWh ($/kWh), PHEV (including tax, margin) 257 215 174 133 305 256 207 158 Bonus/malus en € -5000 -2500 0 0 0 0 0 0 500/1000 1500/2500 2000/3000 2500/3000 0 500 666 833 Small car price without battery in € 10 208 9 551 9 361 9 361 14 491 14 301 14 301 9 815 9 741 9 741 9 741 13 294 12 971 12 781 12 781 Medium car price without battery in € 15 987 13 822 13 632 13 632 21 270 20 890 20 700 20 700 16 197 16 197 16 197 16 197 19 940 19 370 19 180 19 180 Large car price without battery in € 23 709 21 069 20 879 20 879 30 132 29 372 29 182 29 182 23 729 23 729 23 729 23 729 27 472 26 902 26 712 26 712 Consumption small L/100 km or kWh/100 km (BEV 60 kWh) 14.27 13.8 13.46 12.97 4.25 4.09 3.93 3.62 3.81 3.7 3.59 3.38 Consumption medium L/100 km or kWh/100 km (BEV 60 kWh) 16.7 16.18 15.74 15.16 4.73 4.54 4.36 4.03 3.36 3.36 3.36 3.36 Consumption large L/100 km or kWh/100 km (BEV 60 kWh) 20.75 20.15 19.7 18.97 6.15 5.9 5.67 5.23 4.37 4.37 4.37 4.37 % of kilometer drive with electricity PHEV 40 km 46% 46% 46% 46% % of kilometer drive with electricity PHEV 80 km 70% 70% 70% 70% % of kilometer drive with electricity PHEV 120 km 75% 75% 75% 75% ECEEE SUMMER STUDY PROCEEDINGS 1037

6-103-19 PERNOLLET ET AL 6. TRANSPORT AND MOBILITY NON-MONETARY ATTRIBUTE: WTP er hand, main advantages often cited were softness of driving, A representative sample of 12,000 French future vehicle buyers silence, and environment friendliness. answered an online survey in December 2016 where they were WTP_BEV_ICV is the surplus price that people are ready asked to choose between 4 cars among different motorizations to pay to have a ICV car instead of BEV car given that ICV (ICV, BEV, PHEV), in 6 different configurations (see example et BEV has the same autonomy, charging time and charging on Table 3). Each car gets different attribute levels for purchase station density. Figure 2 shows that BEV and PHEV in 2016 price, fuel cost for 100 km, autonomy, distance to fuel station/ are globally seen as less attractive than ICV since WTP_BEV_ public charging station, charging time, incentives. Table 4 ICV and WTP_PHEV_ICV are positive. People with easy shows the attributes values. We then used a multinomial logit charge possibilities at home are less reluctant to buy EV since model (discrete choice based on declared preferences) (Pons WTPmotorization is far lower. Annual mobility needs matter D., 2011) (Kanninen B.J., 2007) to determine each attribute as the bigger the annual mileage, the bigger the WTP. We can level WTP for each household segments studied without dif- generally see that higher the income is, lower the WTP be- ferentiating vehicle types (small, medium, large). comes. It can partly be explained by the fact that high income people have more often already tried a BEV compared to low WTP for motorization type income people (34 % vs 24 %) and people having already tried At the exception of autonomy, charging time and charging BEV have a far lower WTPmotorization (around €6,000 lower). station density, EV may present specific characteristics. These Since the main fears related to BEV ownership should dis- are taken into account by the WTPmotorization parameter. For ex- appear in coming years (particularly everything concerning ample, major BEV drawbacks cited by surveyed people were charge and battery), we make the following assumptions for battery life expectancy incertitude, rental battery fear, vehicle our scenario: WTPmotorization_2025 = 0.6 * WTPmotorization_2016 and resale value, vehicle charge fear, vehicle maintenance network WTPmotorization_2030 = 0.3 * WTPmotorization_2016 and WTPmotorization_2035 incertitude, home charging point installation fear. On the oth- = 0. Table 3. Example of one of the 72,000 trade-offs (one among 4 vehicles has to be chosen). Table 4. Different attribute level for each motorization for trade-off. ICV BEV PHEV Purchase price (compared to wanted 100% 70%; 85%; 100%; 115%; 130 % 115%; 130 % purchase price) Autonomy (in km) 800 200; 350; 500; 800 40;80;160 Fuel/electricity cost for 100 km (including 3;7;11;16;20 2;4;6;8;10;12;14;16;18 2;6;9;12 battery location cost for EV) No public station 11 km in rural area, 3 km in urban area 11 km in rural area, 3 km in urban area for charging station Average distance in kilometer to fuel 6.5 km in rural area, 2.5 km in urban 7 km in rural area, 2.5 km in urban area 7 km in rural area, 2.5 km in urban area for charging station station/charging public station area 7 km in rural area, 1.5 km in urban area 7 km in rural area, 1.5 km in urban area for charging station 7 km in rural area, 0.5 km in urban area 7 km in rural area, 0.5 km in urban area for charging station and fuel station 6.5 km in rural area, 2.5 km in urban area About 90 min for 200 km About 20 min for 40 km with electricity Charging time in a public station /fuel About 10 minutes for 800 km About 20 min for 200 km About 10 min for 40 km with electricity tank fulling time About 10 min for 200 km About 5 min for 40 km with electricity Public incentive No Yes or No Yes or No 1038 ECEEE 2019 SUMMER STUDY

6. TRANSPORT AND MOBILITY 6-103-19 PERNOLLET ET AL Figure 2. WTP specific to motorization for BEV and PHEV compared to ICV. Figure 3. WTP for additional autonomy kilometer for different autonomy ranges for BEV for households with easy home charge. WTP for autonomy For PHEV, it is more difficult to understand since autonomy According to rider annual mileage, and income level, WTP is already 800 km, like for ICV. However people are ready to for extra autonomy differs according to autonomy range (Fig- pay more for a PHEV with 160 electric kilometer than a PHEV2 ure 3). In the model, we calculate the WTP to reach 800 km. with 40 km (Figure 5). The more mileage people ride annually, For people with easy charge at home, WTP for extra autonomy the higher the WTP for electric autonomy for PHEV they want. in range 350 to 500 km is greater than in range 200 to 350 km We obtain similar result with people having barriers to charge or 500 to 800 km. It means that 200 km is sufficient for their at home. usual daily trips but they want more than 350 km autonomy for their long trips, but 500 km seems enough. Globally, the richer WTP specific to charging time and charge point density the people are, the higher the WTP is. For people with difficult WTP to have faster public chargers is lower for small riders charge at home, WTP for additional autonomy in range 200 to than for higher riders (Figure 5 and Figure 6). In addition, peo- 350 km is higher. ple with no easy charge at home are ready to pay more. In our It is really difficult to know how will evolve the WTPautonomy model, we calculate the charge to reach 10 minutes for filling in time. Today, WTP for autonomy is linked to people mobility the ICV tank. Some assumptions have been made on the evo- habits using ICV with large autonomy. However, given the cost to lution of chargers speed (Table 5) to simulate WTPcharging time, have more autonomy, we assume that people are likely to adjust looking at the 20,000 fastest charging stations, (around twice their mobility habits (Pierre M., 2015) and that some solutions the fuel stations number). should appear for long trips (ICV car rental, auto-train, and trailer with extra-autonomy …). Consequently, people should demand less autonomy. That is why we assume that autonomy WTPautonomy2030 = 0.73 * WTPautonomy2016 and WTPautonomy2040 = 0.55 2. An explanation may be that households expect an extra fuel economy on their bill by investing in increased autonomy range even if fuel bill is already set in the * WTPautonomy2016. These value could be discussed. trade-off. ECEEE SUMMER STUDY PROCEEDINGS 1039

6-103-19 PERNOLLET ET AL 6. TRANSPORT AND MOBILITY Figure 4. WTP for additional autonomy kilometer for different autonomy ranges for PHEV for households with easy home charge. Figure 5. WTP to reduce charging time for BEV for households with easy home charge. Table 5. 20,000 fastest charging stations power repartition in France. WTP specific to incentives In our calculation, people are willing to pay about €3,680 in 2020 2025 2030 2040 2016 to have at the same time: free parking, access to some 200 kW or more 0% 4% 15 % 35 % restricted city center, reserved lane on motorway, smaller mo- 100 kW 20 % 30 % 40 % 65 % torway tolls. In our projection, we then consider that in 2020 40 kW 30 % 50 % 30 % 0% and 2025, 60 % of incentives are applied for BEV, and 30 % for 22 kW 50 % 16 % 15 % 0% PHEV, and then it will reach respectively 25 % and 20 % in 2030 and stay constant. People who do not have possibility to charge at home, auto- matically discard the electric vehicle which prevent from quan- Result tifying public charge station density WTP. In fact, trade-off method requires that BEV must be chosen in order to determine MAIN RESULTS attributes by differentiating price with ICV motorization. Con- Figure 7 shows motorization evolution in market share sales sequently our calculation shows that charge point density should for the scenario in which French regulatory context helps to not be a significant factor. This means that, either people who develop EV to try to respect environmental agreements target. choose EV are already satisfied by the number of existing charg- We won’t detail the results for each market share or each time ing points since most of them can charge at home and they are period as some TCO may be very close in particular cases. The more interested in reducing charging time, or people who never aim here, is to understand global EV diffusion and determine choose EV do not pay attention to charge density criteria since main levers to adoption and describe EV adopters’ character- they eliminate EV for other reasons (no charge at home for ex- istics. Low autonomy BEV (30–40 kWh) would represent a ample). In this respect, charging point density is not considered majority of BEV sales in the early 2020s and about half of BEV as a significant EV diffusion driver in our model. To boost EV sales in 2040 (see next paragraph). It seems roughly nobody sales, we must focus more on helping people to have access to wants to buy ultra-high autonomy BEV (120 kWh) which are charge at home than to develop slow public charging station. too expensive but some people buy 80 or 100 kWh BEV. In 1040 ECEEE 2019 SUMMER STUDY

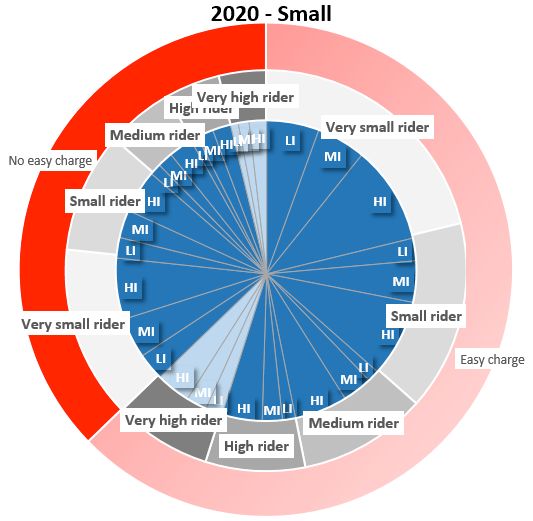

6. TRANSPORT AND MOBILITY 6-103-19 PERNOLLET ET AL Figure 6. WTP to reduce charging time for PHEV for household with easy home charge. Figure 7. Motorization sales market share modelled for France from 2015 to 2040. 2040, there are still some gasoline car buyers (we assume they cars with big engines than for small cars with small engines are not actually banned by the law). PHEV reach a maximum (see Table 2). Moreover ICV malus3 is bigger for large vehicles of 12 % sales in 2032 and are progressively replaced by high (Table 2). That is why in 2020, EV would spread faster for large autonomy BEV. Figure 8, shows in detail, for 2020, 2025, 2030, vehicles than for small vehicles. 2040 market shares for each household segment. So unlike to what may have been observed when focusing only on very early adopters whose behaviour is quite specific WHO WILL BUY ELECTRIC VEHICLES: FROM FIRST ADOPTERS TO MASS- (Pierre, 2011), households with low income may adopt BEV MARKET first as it helps them to reduce their energy bill. Indeed, these In 2020, automobile market is dominated by ICV. Very high households are more likely to accept autonomy constraints riders (and high riders for large vehicles) will choose full hybrid in exchange for fuel economy. Capital constraint to invest in vehicles since for these segments, fuel savings compensate the such vehicles would nevertheless be a constraint and policies extra investment cost. Only people with possibilities to charge and constructor should help overcome this barrier thanks to at home, small riders, with low and medium income are expect- leasing solution, battery rental system or help with access to ed to buy a 30 kWh BEV for large or medium vehicle. Low in- loan. come households are likely to buy BEV since monetary TCO is In 2025, ICV dominate sales and results are almost similar to lower and they are more likely to accept autonomy constraints 2020: there is almost no BEV purchase for people who have no compared to richer people. Figure 9 shows that WTPautonomy is easy access to charge at home, BEV diffuse faster for large cars smaller for low income than for high income people. Higher than for small cars, and particularly with people having low or riders have a WTPautonomy (Figure 3) superior and consequently they choose ICVs. People who have difficult charge have a too high WTPmotorization to choose BEV (Figure 9 and Figure 2). The 3. Malus is a tax on most pollutant new vehicles paid at the purchase (contrary to BEV and ICV motorization price difference is bigger for large bonus where money are given for clean vehicle purchase). ECEEE SUMMER STUDY PROCEEDINGS 1041

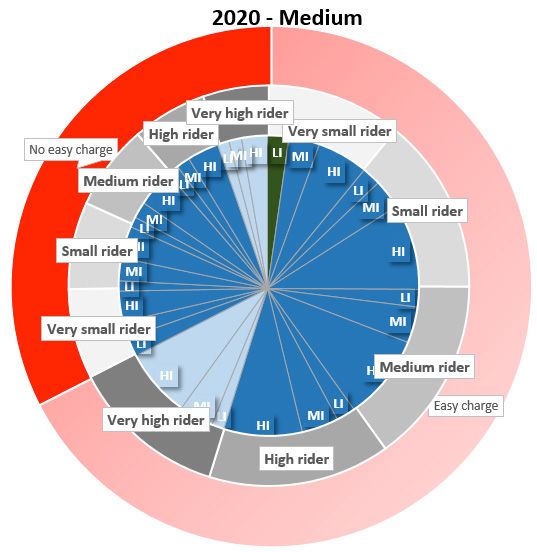

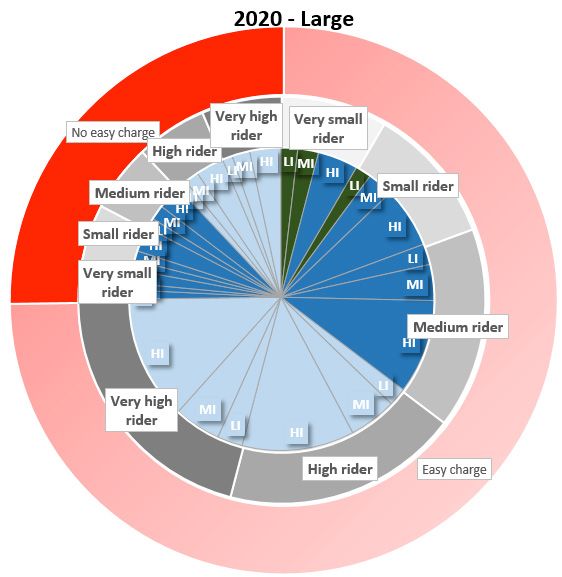

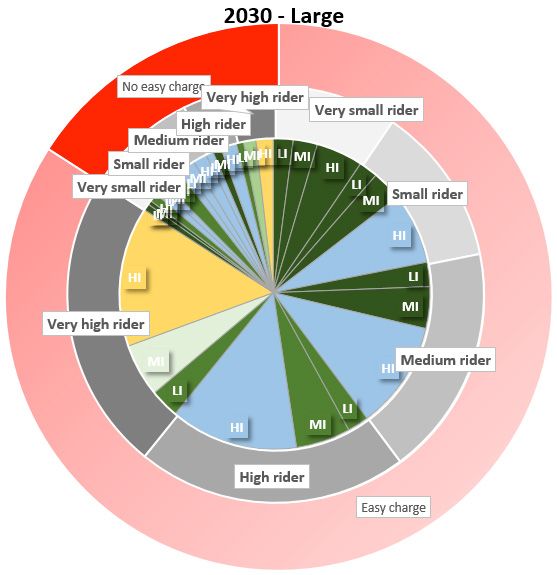

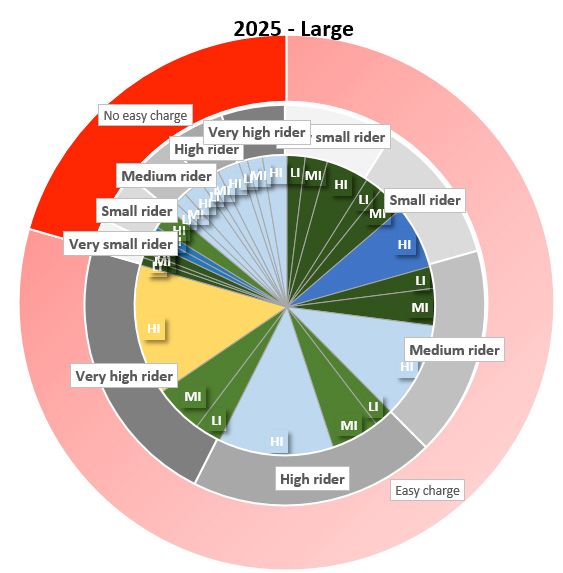

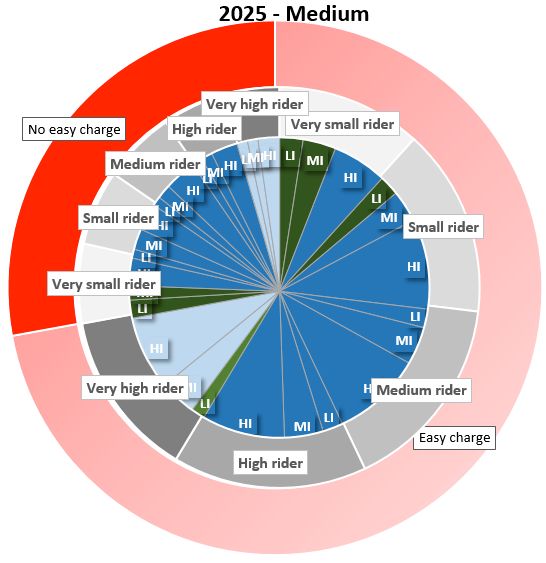

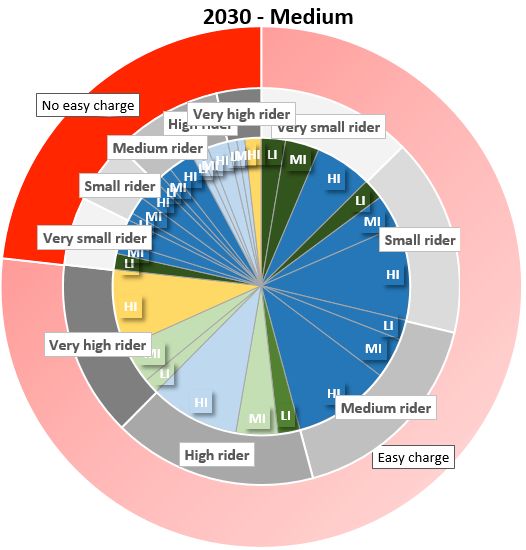

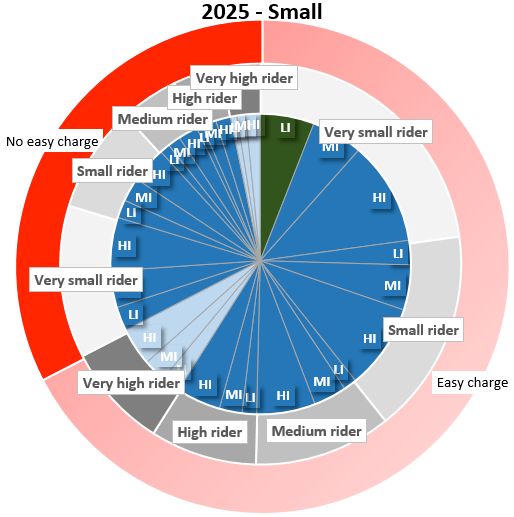

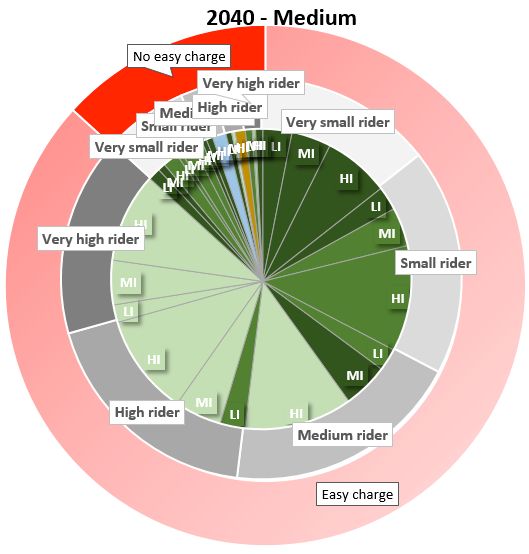

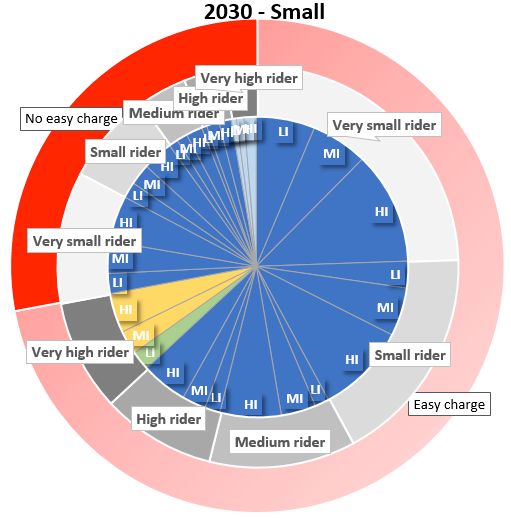

6-103-19 PERNOLLET ET AL 6. TRANSPORT AND MOBILITY Figure 8. Sales market share according to motorization in France for 2020, 2025, 2030, 2040 for different household segments. 1042 ECEEE 2019 SUMMER STUDY

6. TRANSPORT AND MOBILITY 6-103-19 PERNOLLET ET AL Figure 9. TCO/km in 2020 for very small riders with large car. Figure 10. TCO/km for high riders with high income with medium car. medium incomes. From 2020 to 2025, we can see that mon- fusion is very limited because of the importance of considering etary BEV TCO doesn’t decrease so much (Figure 10), even if non-monetary constraints. battery prices decrease a lot, and BEV car body price reduces In 2030, compared to 2025, BEV would take some market a bit, it just compensates bonus decrease. From 2020 to 2025, shares to ICV for medium and small vehicles for high riders. As BEV take market share from gasoline and hybrid gasoline on a matter of fact, from 2025 to 2030, for high riders, BEV with the large car segment, for medium, high and very high riders high autonomy (80 kWh) offers the cheaper generalized TCO (Figure 8) thanks to battery price decrease and ICV malus in- (Figure 11) thanks to battery price decrease. For medium riders, crease (Table 2). PHEV appear for very high range riders, with 80 kWh BEV are too expensive (investment on battery is amor- high income for large vehicles, since investment on PHEV is tized in fewer kilometers than for high riders), and 30–40 kWh more easily amortized due to the importance of annual kilome- BEV have not enough autonomy, so ICV are more likely to be tres driven, and WTPautonomy for this household segment is too chosen. For very small riders, as in 2025, since their needs for high in order BEV to be chosen. autonomy are low, 30–40 kWh BEV would be sufficient. In 2030, 30–40 kWh BEV monetary TCO in 2025 is lower than ICV for high income people, very high riders, people want to have a TCO for a majority of household segments; however BEV dif- high autonomy level, they are likely to choose PHEV. ECEEE SUMMER STUDY PROCEEDINGS 1043

6-103-19 PERNOLLET ET AL 6. TRANSPORT AND MOBILITY Figure 11. TCO/km in 2030 for medium car, and medium income, with easy charge at home. Figure 12. TCO/km in 2040 for medium income, with easy charge at home, small rider for small, medium, large car. In 2040, BEV is mainly spread in medium and large car mar- decrease in battery prices, BEV diffusion could not be as fast ket, even for people who may have some difficulties to charge as expected by analyses that only rely on monetary attributes. BEV at home. For very high or high riders or high income the New BEV buyers from 2020 to 2025 are likely to be households BEV autonomy is bigger. For small cars, for small or medium with either low income or with limited annual mileage. In 2025, riders, BEV monetary TCO is cheaper than gasoline TCO or these people are likely to buy 30 or 40 kWh BEV since BEV hybrid gasoline TCO but not enough to balance the autonomy TCO shall be cheaper and people are ready to have little range constraints (Figure 12). The gap between ICV and BEV TCO needs. Then, in 2030, high income and long distance drivers for small cars is smaller than for medium or large cars. That is are likely to buy PHEV in order to avoid autonomy constraints, why, in 2040, without ban, some people are likely to buy small and medium income and long distance drivers should prefer gasoline cars. From 2030 to 2040, 80–100 kWh BEV would take 80 kWh BEV. This study shows that BEV should spread faster market share from PHEV. In 2040, PHEV would be too expen- for large and medium vehicles than for small vehicles. In par- sive compared to high autonomy BEV. ticular, without ban, people having a small car, with medium or high revenue and small or average rider in 2040 are expected to buy small ICV. Finally, this paper highlights that people who Conclusions have no easy access to charge at their homes are more reluctant This paper shows that it is essential to take into account non- to buy BEV. This article highlights that to boost EV sales, it is monetary constraints to analyse the diffusion of EV. By tak- important to facilitate charge at home, to help people buying ing them into account, we can see that, even if there is a huge EV for example with bonus/malus differentiated by standard 1044 ECEEE 2019 SUMMER STUDY

6. TRANSPORT AND MOBILITY 6-103-19 PERNOLLET ET AL of living and develop solutions in order people reduce their IEA. “World Energy Outlook 2018.” 2018. autonomy willing and understand their real autonomy needs. It INSEE. “Enquête Budget des Familles 2011.” 2011. should be interesting to study how to develop second hand EV Kanninen B.J. “Valuing environmental amenties using stated market in particular for underprivileged rural people. shoice studies, a common sense approach to theory However, it is important to stress that the model has some lim- and practice,.” The economics of Non-market Goods and its. First, vehicle choice is not always rational and is not always Resources, 2007. guided by prices and constraints but sometimes by other social MTES. “Projet de Stratégie Nationale Bas-Carbone – La tran- factors (social rank given by the car, etc.) and it is only partially sition écologique et solidaire vers la neutralité carbone.” taken into account by the WTPmotorization. Secondly, it does not take 2018. into account some evolutions (household segments repartition, MTES 2. “Strategie Française pour l’énergie et le climat – bigger car arrival, annual kilometer, autonomous car arrival …). Présentation de la programmation pluriannuelle de l’éner- Third, it does not include some likely regulatory constraints (ICV gie et de la stratégie nationale bas carbone.” 2018. ban, city-center banned for ICV …). Then discount rate is not Pasaoglu G., et Al. “A system dynamics based market differentiated by income. And finally, it is quite sensitive to some agent model simulating future powertrain technology hypotheses that are calibrated by expert knowledge (evolution on transition: Scenarios in the EU light duty vehicle road autonomy will, global BEV appreciation …). transport sector.” Technological Forecasting & Social The model could be improved by discriminating household Change, 2016. segments by localization urban/rural/periurban, BEV experi- Pernollet F., Cayla J.M., Crocombette C., Willingness to pay ence, and multi-motorized households. It could also have been for electric vehicles and their attributes: the impact on interesting to expand the scope to company vehicles and fleet electric vehicles market diffusion in France, EVS32 Sym- vehicles. Since non-monetary criteria could have less importance posium, Lyon, France, May 19–22, 2019 (in press). and vehicle more luxurious, we may expect a faster diffusion. Pierre M., Jemelin C. et Louvet N. ‘‘Driving an electric vehicle. Another interesting work would have been to try and find how A sociological analysis on pioneer users”, revue Energy to set the right parameters combinations in the model in order to Efficiency, 2011. reach EV diffusion target fixed by the French public authorities. Pierre M., Fulda A.S.‘‘Driving an EV: a new practice? How electric vehicle private users overcome limited battery range through their mobility practice”, eceee summer study References proceedings, 2015. Ahkamiraad A., Wang Y. “An agent-based model for zip-code Pfahl S., Jochem P., Fichtner W. «When will electric vehicles level diffusion of electric vehicles and electricity con- capture the German market ? And Why ?» Electric sumption in New York city.” Energies, 2018. Vehicle Symposium and Exhibition (EVS27) World IEEE, Al-Alwi B.M., Bradley T.H. “Review of hybrid, plug-in hybrid, 2013. and electric vehicle market modeling studies.” Renewable Plötz P., Gnann T., Wietschel M. “Modelling market diffusion of and Sustainable Energy Reviews, 2013. electric vehicles with real world driving data – Part 1: Mod- Becker T.A., Sidhu I. “Electric vehicles in the Unites States A el structure and validation.” Ecological Economics, 2014. new model with forecasts to 2030, CET.” 2009. Pons D. “Mise en place d’enquêtes par préférences déclarées Briand, Y. Lefevre, J. Cayla JM. “Pathways to deep decar- dans le cadre de projets d’étude relatifs au secteur des bonization of the passenger transport sector in France” transports de personnes.” Economies et finances. Université IDDRI, UMR 8568 CIRED, EDF R&D, 2017. Lumière – Lyon II, 2011. Brooker A., et Al. “Adopt: a historically validated light duty Qian L., Soopramanien D. “Incorporating heterogeneity to vehicle consumer choice model.” SAE international, 2015. forcast the demand of new products in emerging markets: Brown M. “Catching the PHEVer: Simulating electric vehicle Green cars in China.” Technological Forecasting & Social diffusion with an Agent-Based Mixed Logit Model of Change, 2015. Vehicle Choice.” Journal of Artificial Societies and Social Tanaka M., et Al. “Consumers’ willingness to pay for alterna- Simulation, 2013. tive fuel vehicles: a comparative discrete choice analysis CGDD. “Les comptes des transports en 2017 – 55e rapport de between the US and Japan.” Transportation Research, 2014. la Commission des comptes des transports de la Nation.” United Nations. “Paris Agreement.” 2015. 2018. Varian Hal. R., Microeconomic Analysis, Vol 3. New York: WW Fernandez-Antolin A., de Lapparent M., Bierlaire M. “Model- Norton, 1992. ing purchases of new cars: an analysis of the 2014 French Wu G., Inderbitzin A., Bening C. “Total cost of ownership market.” Theory and Decision, 2018. of electric vehicles compared to conventional vehicles: a Gnann T., Et Al. “What drives the market for plug-in electric probabilistic analysis and projection across market seg- vehicles? A review of international PEV market diffusion ments.” Energy Policy, 2015. models.” Renewable and Sustainable Energy Reviews, 2018. Hackbarth A., Madlener R. “Willingness-to-pay for alterna- tive fuel vehicle characteristics: a stated choice study for Acknowledgements Germany.” Transportation Research, 2016. We are very thankful for the support of Magali Pierre from EDF Hidrue M.K., et Al. “Willingness to pay for electric vehicles and and Stéphane Dupré La Tour from EDF, who fruitfully helped their attributes.” Resource and Energy Economics, 2011. us carrying out this research. ECEEE SUMMER STUDY PROCEEDINGS 1045

You can also read