Why is the Euro Punching Below its Weight? - Banco de España

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Why is the Euro Punching Below its Weight? ETHAN ILZETZKI, LONDON SCHOOL OF ECONOMICS CARMEN M. REINHART, HARVARD UNIVERSITY KENNETH S. ROGOFF, HARVARD UNIVERSITY 3RD ANNUAL RESEARCH CONFERENCE OF THE BANCO DE ESPAÑA MADRID, SEPTEMBER 16, 2019

• The euro is the world’s second most important international currency…its creation consolidated the French franc and DM currency areas • But is a far second to the dollar by a Some broad variety of measures observations • Furthermore, after a promising start in its early years, it has lost ground in the global economy • We document these facts and delve into its plausible causes

Roadmap The international role of Why is the euro punching the Euro as an anchor Further research below its weight currency: Various metrics • IIR exchange rate • Illiquid euro debt • Measuring the liquidity regimes markets of debt markets • The geography of • The role of official • De facto versus dejure exchange rate regimes institutions capital controls • Central bank reserves • Post-crisis financial • China’s global footprint • The denomination of regulation and its implications EM external debt • The crisis and the “emergence” of a European periphery (evidence from ECB monetary policy) • EZ’s relative decline ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 3

The International Role of the Euro ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 4

Dollar and Euro as Anchor Currencies 80 Percent US Dollar 70 60 50 40 DM & FFR Euro 30 20 10 0 1975 1980 1985 1990 1995 2000 2005 2010 2015 Share of countries anchored to the dollar and euro by their share in world GDP, 1975-2015 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 5

Dollar and Euro as Anchor Currencies 60 Percent US Dollar 50 40 DM & FFR Euro 30 20 10 0 1975 1980 1985 1990 1995 2000 2005 2010 2015 Note: Share of countries anchored to the dollar and euro, 1975-2015 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 6

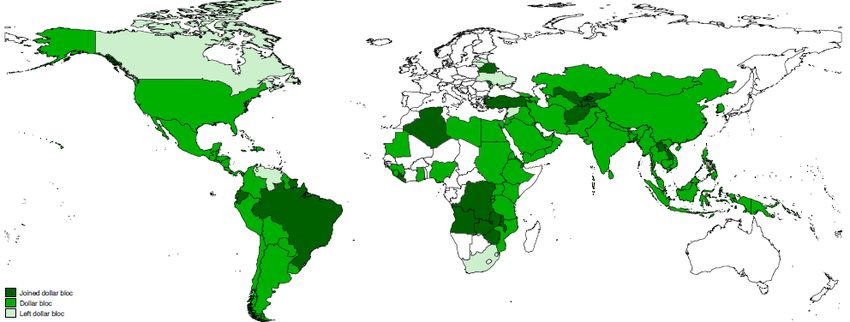

Countries with Euro Anchor ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 7

Countries with Dollar Anchor ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 8

Currency Composition of Central Bank Reserves: Dollar and Euro 100 Percent Billions USD 12.000 90 10.000 80 70 Total Reserves 8.000 60 50 6.000 40 US Dollar 4.000 30 20 2.000 Euro 10 Euro 0 0 1995 2000 2005 2010 2015 Note: Allocated central bank reserves denominated in euro (bottom, blue) and dollar (top, green), 1995- 2018.(Both left-hand axis.) The line (right-hand axis) shows total world central bank allocated reserves in billions of US dollars. The vertical line shows the date of euro adoption. ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 9

Foreign Exchange Turnover: Shares of Major Currencies 200 Percent 180 160 140 120 US Dollar 100 80 60 UK Pound Yen 40 Euro 20 0 1995 1998 2001 2004 2007 2010 2013 2016 Note: Share of foreign exchange transactions in which each of presented currencies was one side of the transaction, 1995-2016. ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 10

80 Percent Borrowing in 70 Euros and 60 US Dollar Dollars: Developing 50 Country 40 External Debt Not just what 30 you see but what DM & FFR Euro 20 you don’t see… 10 0 1975 1980 1985 1990 1995 2000 2005 2010 2015 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 11

The preceding chart (based on official World Bank data) seriously underestimates developing country exposure to US dollar debt. “Hidden Debts to China” are almost exclusively dollar- denominated (see Horn, Reinhart, and Trebesch, 2019). According to their estimates, the World Bank data incorporates about ½ of actual Chinese lending to EMs and developing countries--further widening the existing Euro-dollar gap in the past two decades. Ilzetzki, Reinhart and Rogoff: Euro Punching 12

China: Overseas lending boom, 1998-2018 Aggregate Data: PBOC Balance of Payments Statistics Loans: $590 bn Trade credits: $750 bn FDI debt: $160 bn Source: Horn, Reinhart, and Trebesch (2019) 13

Why is the Euro Punching Below its Weight? The role of increasingly illiquid debt markets ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 14

6.000 Billions USD Fed Dollar Liabilities to non-US residents 5.000 Global Demand for 4.000 Dollar and Euro Liquidity 3.000 of which to Europe 2.000 1.000 ECB Euro Liabilities to non-EZ r 0 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 15

16,000 Billions USD Bank dominance and bond 14,000 12,000 “scarcity”: Marketable Debt 10,000 Outstanding, 2018 8,000 US 6,000 4,000 Eurzone The top panel shows the marketable 2,000 France central government outstanding in 0 Germany billions of US dollars in 2018 for France and Germany, all Eurozone countries (including France and Germany) and the 40 Perecent of GDP Corporate Bonds Bank Lending US. 35 The bottom panel plots corporate bonds 30 outstanding and total corporate bank 25 lending as a percent of GDP in the 20 Eurozone and the US. 15 US Eurzone 10 5 Eurzone US 0 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 16

The post-crisis shift in EZ monetary policy (more to follow) has also contributed to the illiquidity of local bond markets… Ilzetzki, Reinhart and Rogoff: Euro Punching 17

% of total government debt 10 15 20 25 30 35 40 0 5 Austria Belgium Finland France Germany Greece Ireland Italy Netherlands EZ Portugal Slovenia 2004:Q1 Spain Australia Canada Czech Republic Select Advanced Economies: 2004 versus 2018 2018:Q4 Denmark Japan Korea New Zealand Norway Sweden Switzerland Domestic Central Bank Holdings as a Percent of Total Public Debt United Kingdom United States EZ avg Non EZ avg Non EZ ex Japan Sources: Authors' calculations based on Arsnalalp and Tsuda (2014 and 2019). 18

Other official institutions European Financial Stability Facility (EFSF) and European Stability Mechanism (ESM) also purchased Greek, Cypriot, Irish, Spanish, and Portuguese debt— shifting debt holdings into official hands and further reducing bond market liquidity. Ilzetzki, Reinhart and Rogoff: Euro Punching 19

Official Holdings as a Percent of Total Public Debt Select Advanced Economies: 2004 versus 2018 2004:Q1 2018:Q4 70.00 % of total government debt 60.00 EZ 50.00 40.00 30.00 20.00 10.00 0.00 Sweden United States Slovenia Portugal Non EZ avg New Zealand Canada Denmark Norway Switzerland Belgium Ireland Netherlands EZ avg Germany Korea United Kingdom Australia Finland Greece France Czech Republic Austria Italy Japan Spain Note scale Sources: Authors' calculations based on Arsnalalp and Tsuda (2014 and 2019). Ilzetzki, Reinhart and Rogoff 20

70 Percent 65 France 60 55 Germany 50 US 45 40 Foreign 35 30 Holdings as 25 a Share of 20 1999 2004 2009 2014 Marketable Percent share of marketable government that is held by foreign investors (private and Government official sectors). Debt Source: Merler and Pisani-Ferry (2012). ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 21

Post-crisis financial regulation (and more broadly financial repression) has meant that institutions are required to hold higher levels of government debt—further impacting market liquidity… Ilzetzki, Reinhart and Rogoff: Euro Punching 22

Ilzetzki, Reinhart and Rogoff: Euro Punching 23

Currency Home Bias in US and Eurozone Bank Holdings 100 Percent 95 90 US 85 80 75 70 Eurozone 65 60 55 50 1995 2000 2005 2010 Share US banks’ gross foreign assets denominated in dollars (top, green line) and of Eurozone banks gross foreign assets denominated in euro (post 1999) or ECU-lined currencies (pre 1999) (bottom, blue line). ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 24

As the next two charts highlight, Eurozone government debt markets became radically fragmented after the crisis. Ilzetzki, Reinhart and Rogoff: Euro Punching 25

Sovereign Spreads and Foreign Holdings as a Share of Marketable Government Debt Italy Spain 6 55 5 55 Sovereign Spread (Percent) Foreign Share (Percent) Sovereign Spread (Percent) Foreign Share (Percent) 5 50 4 50 4 45 3 45 3 40 2 40 2 35 1 35 1 30 0 30 0 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 25 -1 25 -1 -2 20 -2 20 14 Portugal 90 30 Greece Sovereign Spread (Percent) Foreign Share (Percent) Sovereign Spread (Percent) Foreign Share (Percent) 70 12 80 25 10 60 70 20 8 60 15 50 6 50 10 4 40 40 5 2 30 30 0 0 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 -2 20 -5 20 Percent share of marketable government that is held by foreign investors (private and official sectors, dashed lines, right-hand axis) and the spread of the 10-year bond of the country in question over Germany’s. ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 26

As foreign investors exit post-crisis, the reliance on domestic banks for funding government is greater. Home bias is not exclusively determined by currency denomination; within EZ national borders matter. The debt is 18 Percent 20 Percent Italy Greece transferred to 16 18 14 Official creditors 16 12 10 14 8 12 6 10 4 2 8 0 6 2004Jan 2006Jan 2008Jan 2010Jan 2012Jan 2014Jan 2016Jan 2004Jan 2006Jan 2008Jan 2010Jan 2012Jan 2014Jan 2016Jan 13 Percent Portugal 15 Percent Spain 11 13 9 11 7 9 5 7 3 5 1 3 2004Jan 2006Jan 2008Jan 2010Jan 2012Jan 2014Jan 2016Jan 2004Jan 2006Jan 2008Jan 2010Jan 2012Jan 2014Jan 2016Jan Share of domestic government debt in banks’ assets. 27

ECB policy before and after the financial crisis: I don’t think we’re in Kansas anymore ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 28

What we do: Estimate Taylor Rules for Eurozone Economies before and after the financial crisis • ECB’s main instrument: policy interest rate(s) • De jure mandate: target Eurozone inflation • Estimate Taylor rule of the form: ∗, , γ , , • With possible interest rate inertia: 1 ∗, • GMM instruments: 6 lags of inflation and output gap • Recall Taylor principle requires >1 i: policy interest rate , : inflation in country n in month t , : output gap measured as unemployment in country n relative to average unemployment 1992-2007. ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 29

What we do (cont.): Consider a Horse Race Regression • Test the hypothesis directly: can we reject that ECB is targeting German and not EZ inflation? ∗ , γ , , γ , , ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 30

• We document two phases in ECB policy: • “Bundesbank plus”: continuity with the EERM. • “Whatever it takes”: expansive credit policies with potentially new unintended consequences The Euro prior discussion). • On the ECB’s de jure inflation targeting we Anchor: ask: Whose inflation is targeted? • Germany wins the horserace (versus EZ and all Main • others) prior to the crisis. Cannot reject: ECB follows German Taylor principle takeaways • Reject: ECB follows EZ Taylor principle • Reject: ECB puts greater weight on EZ than German inflation • Cannot reject: ECB puts zero weight on EZ inflation once controlling for German inflation

-.5 0 .5 1 1.5 Austria Belgium Finland France Germany Greece Ireland Italy Luxembourg ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING Netherlands Inflation Coefficients Portugal Spain Euro 32

-1.5 -1 -.5 0 .5 1 Austria Belgium Finland France Germany Greece Ireland Italy Luxembourg ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING Netherlands Output Gap Coefficients Portugal Spain Euro 33

Horse Race Germany and EZ: Inflation Coefficients 1.5 1 .5 0 -.5 Euro Germany ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 34

We also consider counterfactual Taylor Rules What would ECB policy look like if it followed a Taylor rule for Germany? Eurozone? Southern Europe? Calculate the counterfactual Taylor rule for each country, using Taylor’s (1993) original values: • 1.5 • 0.5 ∗, , γ , , Takeaway: Any resemblance to a Taylor rule for the EZ is of recent vintage ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 35

Not surprisingly, in line with the view prior to the crisis in financial markets, ECB policy was not concerned with fragmentation of EZ financial markets or the distinction between core and periphery country debt. Of more note is that the sustained change in ECB policy did not immediately follow the financial (banking) crisis and that it is only after a debt crisis is underway in much of the south that changes become systematically discernable. Ilzetzki, Reinhart and Rogoff: Euro Punching 36

Taylor Rule vs. ECB Policy Germany 12% DM DM Regime € Regime 10% 8% 6% Rule 4% Policy 2% 0% 1992 1997 2002 2007 2012 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 37

Taylor Rule vs. ECB Policy France 12% DM DM Regime € Regime 10% 8% 6% Rule 4% 2% Policy 0% 1992 1997 2002 2007 2012 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 38

Taylor Rule vs. ECB Policy Portugal 12% DM DM Regime € Regime 10% 8% Rule 6% 4% 2% Policy 0% -2% -4% 1992 1997 2002 2007 2012 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 39

Taylor Rule vs. ECB Policy Eurozone 12% DM DM Regime € Regime 10% 8% Rule 6% 4% 2% Policy 0% 1992 1997 2002 2007 2012 -2% ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 40

Country ρ=0 ρ = 0.9 Austria 3.71 3.45 MSE Belgium 6.25 6.03 between Finland 7.14 6.71 ECB Policy France 3.45 3.55 and Taylor Germany Greece 2.30 10.91 2.14 11.40 Rules Ireland 33.58 33.34 Italy 6.06 6.04 Luxembourg 3.41 3.07 Netherlands 5.32 5.60 Portugal 6.18 6.36 Spain 19.11 19.03 Euro 4.02 4.03 ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 41

Lastly, the secular decline of the Eurozone economy ILZETZKI, REINHART AND ROGOFF: EURO PUNCHING 42

Eurozone's GDP in US Dollars, Actual and Projected: 1991‐2023 (as a share of world GDP and US GDP) 0.35 1.1 1 0.3 0.9 % of world 0.25 % of US 0.8 0.2 0.7 0.15 0.6 Recovery followed by crisis and stagnation 0.1 0.5 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 Eurozone/World US/World Eurozone/US right axis Sources: Authors' calculations based on World Economic Outlook, International Monetary Fund, April 2019. Ilzetzki, Reinhart and Rogoff: Euro Punching 43

• Euro is punching below its weight as international currency. • May be artefact of natural monopoly in international medium of exchange, store of value, unit of account • Scarcity of euro safe assets may be a key Summary contributor, as debt markets have become both fragmented within the EZ and other factors have and next impaired debt market liquidity, making Euro assets less globally attractive. steps • The nature and extent of market illiquidity merits closer scrutiny, as does the question of hysteresis. • The extent to which China’s role in global finance may be contributing to a mismeasurement of the global usage of the US dollar and the Euro also warrants further study.

You can also read