2017 Results and 2018 Operating Plan - FEBRUARY 21, 2018 PREMIER OPERATOR OF TOP TIER ASSETS - Criterion Research

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2017 Results and

2018 Operating Plan

FEBRUARY 21, 2018

PREMIER OPERATOR OF TOP TIER ASSETS

1

Please Read This presentation makes reference to:

Forward-looking statements

This presentation contains forward-looking statements within the meaning of securities laws. The words “anticipate,” “assume,” “believe,” “pending,” “budget,”

“estimate,” “expect,” “forecast,” “guidance,” “intend,” “plan,” “project,” “will” and similar expressions are intended to identify forward-looking statements. These

statements involve known and unknown risks, which may cause SM Energy's actual results to differ materially from results expressed or implied by the forward-

looking statements. Forward-looking statements in this presentation include, among other things, full year 2018 guidance, first quarter of 2018 guidance,

expectations concerning the planned closing of a previously announced divestiture, expectations about future cost inflation, and the expected benefits from

joint venture arrangements. General risk factors include the availability of and access to capital markets; the availability, proximity and capacity of gathering,

processing and transportation facilities; the volatility and level of oil, natural gas, and natural gas liquids prices, including any impact on the Company’s asset

carrying values or reserves arising from price declines; uncertainties inherent in projecting future rates of production or other results from drilling and

completion activities; the imprecise nature of estimating oil and natural gas reserves; uncertainties inherent in projecting future drilling and completion activities,

costs or results, including from pilot tests; the uncertainty of negotiations to result in an agreement or a completed transaction (including any delay in closing

our announced PRB divestiture as a result of litigation); uncertainties inherent in projecting the timing and ultimate outcome of litigation; the uncertain nature of

acquisition, divestiture, joint venture, farm down or similar efforts and the ability to complete any such transactions; the uncertain nature of expected benefits

from the actual or expected acquisition, divestiture, drilling carry, farm down or similar efforts; the availability of additional economically attractive exploration,

development, and acquisition opportunities for future growth and any necessary financings; unexpected drilling conditions and results; unsuccessful exploration

and development drilling results; the availability of drilling, completion, and operating equipment and services; the risks associated with the Company's

commodity price risk management strategy; uncertainty regarding the ultimate impact of potentially dilutive securities; and other such matters discussed in the

“Risk Factors” section of SM Energy's 2017 Annual Report on Form 10-K, as such risk factors may be updated from time to time in the Company's other

periodic reports filed with the Securities and Exchange Commission. The forward-looking statements contained herein speak as of the date of this

announcement. Although SM Energy may from time to time voluntarily update its prior forward-looking statements, it disclaims any commitment to do so except

as required by securities laws.

Non-GAAP financial measures: See Appendix for reconciliations

Reserves and resources: See Appendix for disclosure statement

Non-GAAP forward looking metrics: See Appendix for definitions

2

2017 – 2019 Driving Differential Value

Measuring returns: cash flow growth per debt adjusted share(1)

“Cash flow growth per debt adjusted share is the metric with the highest

correlation to intra sector relative performance”

– Credit Suisse 12/11/17(2)

Premier Operator

+ = ~35%

Top Tier assets Cash Flow Growth

per Debt Adjusted Share(1)

(1) See Appendix for Cash Flow per Debt Adjusted Share definition

(2) William Featherston/Betty Jiang, Credit Suisse 3

Premier Operator of Top Tier Assets

2017 marked by outstanding execution

“Top operator…SM ranks #1 in

“Key differentiator is

the Midland Basin on a

Howard County acreage”

revenues per lateral foot basis”

- Deutsche Bank(2)

- Baird(1)

Midland Basin Increased average Raised cash operating

production growth(3) lateral feet per well(4) margin(3)

165% ~1,200 48%

Increased proved Increased PV-10(6)

reserves(5)

47% 2.5x

(1) Baird 12/18/17 – Joseph Allman (4) 2017 average lateral feet compared to acquisition assumptions

(2) Deutsche Bank 2/1/18 – Nitin Kumar (5) 2017/2016; retained assets 4

(3) 4Q17/4Q16 (6) See Appendix for reconciliation of PV-10 (Non-GAAP) to Standardized Measure (GAAP)

2018-2019

Plan Overview

& Guidance

5

2018 – 2019 Plan Highlights

Big cash flow growth per debt adjusted share – near 35% projected CAGR

► Expected to nearly double cash flow per debt adjusted share in two years

► Expected to cut Net Debt : TTM EBITDAX by approximately 1.5 turns

$4.00 6

Net Debt : TTM EBITDAX

per Net Debt Adjusted Share

4

Cash Flow

$2.00

2

$0.00 0

2017 2018e 2019e

(1)

Cash Flow per Net Debt Adjusted Share Net Debt : TTM EBITDAX

(1) See Appendix for Cash Flow per Debt Adjusted Share definition

(2) Net Debt : TTM EBITDAX: see Appendix for definition. 6

2018 – 2019 Plan Highlights

Big Midland production growth driving expected margin expansion

► Midland projected production growth up ~135% 2017-2019

► Company projected cash operating margin up over 45% 2017-2019

60,000 $22

50,000

Cash Operating Margin

40,000

Production

(MBoe)

$/Boe

30,000 $16

20,000

10,000

0 $10

2017 2018e 2019e

(1)

Midland Basin Eagle Ford Rockies Sold/Pending Sale Operating Margin

(1) Realized price before the effect of hedges (2018e: current strip pricing through 1Q18 and $55/$3 for remainder of 2018;

price normalized for 2019e) less LOE, ad valorem, transportation, production taxes, and cash G&A.

7

SM Energy A Premier Operator of Top Tier Assets

Objective: to deliver long-term growth in cash flow per debt adjusted share

2 Year Plan Expected Outcomes:

Big growth in Cash flow Net

high-margin neutrality by Debt:EBITDAX

production MY 2019 ~2.5x YE 2019

2018 Priorities:

Operational Reduce debt / Focused

excellence / continue to capital program

capital core up to drive margin

efficiency portfolio expansion

8

2018 Capital Program

Aggressive growth expected in the Midland Basin

Total Capital Spend D&C Budget

~$1.27B ~$1.04B

Eagle Ford

14%

Facilities

10%

Drilling and Other(1)

Completion 8%

82%

Midland

Basin

86%

► Currently running 9 rigs in Midland Basin; expected to decline to 7 rigs by year-end (expected

average of 8 for full year); expected average 1 rig in Eagle Ford for full year

► Planning ~150 net wells drilled(2) and ~125 net completions(3)

► D&C budget assumes 10-15% cost inflation per lateral foot versus 2017 average

► Facilities expenditures include buildout of Midland water handling system for ~$70MM

(1) Other includes exploration, allocated overhead, and land. (3) Expect to complete ~100 net wells in Midland and ~25 net

(2) Expect to drill ~130 net wells in Midland and ~17 net wells in Eagle Ford wells in Eagle Ford

9

2018 Plan Guidance(1)

Capital & Production FY 2018

Total Capital Spend ($MM)(2) (before acquisitions) ~$1,270

2018 Production Guidance

Total Production (MMBoe) 42 - 46 by Quarter

150

Oil % ~41%

125

Costs

Production (Boe/d)

LOE ($/Boe) ~$5.00 100

Ad Valorem taxes ($/Boe) Operated Eagle $0.55 - $0.65 75

Transportation ($/Boe) Ford

~$4.50

20% 50

Production taxes ($/Boe) ~$1.55

25

G&A ($MM) $125 – 135

– includes ~$20MM non-cash compensation

0

Capitalized Overhead/Exploration ($MM) $70 - 75 86% 1Q18e 2Q18e 3Q18e 4Q18e

– before dry hole expense, all of which is 86% 8%

included in capital expenditure guidance Retained Assets Pending Sale

DD&A ($/Boe) $13.00 - $15.00

> 1Q18 production guidance 9.5 to 10.0 MMBoe

> LOE expected to exceed the average in 1H18 and be below the average in 2H18 as Permian costs are

reduced with completion of water handling systems

> Transportation expense expected to decline sequentially through the year as higher cost Eagle Ford

production is a reduced proportion of the commodity mix

(1) As of February 21, 2018

(2) Total Capital Spend is a non-GAAP financial measure. Please see the reconciliation of this measure in the Appendix. 102017

Reserves at Year-End

112017 Proved Reserves Additions and Revisions

► Proved reserves of retained assets up 47%

► Net proved reserve additions of 192MM Boe equaled 4.3 times production

► More than doubled proved reserve PV-10 to $3.1B(1)

500

7

450 23

14

Proved Reserves (MMBoe)

400

175

44

468

350

396

76

300

1

250

YE16 Production Divestitures Acquisitions Adds/ Aged Price Performance YE17

Proved Infills PUD's Revision Revision Proved

Reserves Reserves

192 MMBoe

► 46% Proved Developed

► 34% Oil, 46% Natural Gas, 20% NGLs

Note: Calculated in accordance with SEC Pricing at $51.34 per barrel of oil NYMEX, $3.00 per MMBtu of natural gas at Henry Hub and $27.69 per barrel of natural gas

liquids (“NGLs”) at Mt. Belvieu. 12

(1) See Appendix for reconciliation of PV-10 (Non-GAAP) to Standardized Measure (GAAP)2017 Proved Reserves By Region

Coring up the portfolio to top tier assets

YE 2016(1) (MMBoe) 228.9 53.0 36.3 318.2

Rocky

YE 2017 Eagle Ford Permian Total

Mountain

Oil (MMBbl) 13.3 117.5 27.4 158.2

Gas (Bcf) 998.1 252.8 29.2 1,280.1

NGL (MMBbl) 95.6 0.2 0.7 96.5

Total (MMBoe) 275.2 159.9 33.0 468.1

% Proved Developed 52% 34% 53% 46%

Reserve growth 20% 202% (9%) 47%

Permian proved reserves tripled to 160 MMBoe

Note: Proved reserves at year-end 2017 include approximately 4.2 MMBoe associated with the pending sale of certain Powder River Basin assets.

(1) Adjusted to show retained assets only 132018

Operations Plan

14Eagle Ford 2018 Plan Objectives

Value creation through better wells, longer laterals, and optimum number of wells per section

Eagle Ford

► Employ new technology and optimized spacing ~165,000 net acres

to drive improved well performance and cost

savings

Dimmit County

► Expect to drill ~17 net wells Webb County

> 2 rigs in 1Q18 to 1 in 2Q18

> Average lateral length increased to 9,300’ (from

6,500’ in 2017) North

Area

► Expect to complete ~25 net wells, optimize East

Area

completions

Mexico

> Average 1 completion crew

> Increase fracture injection points by decreasing South

Area

cluster spacing from 50 feet to 25 feet

► JV expected to drill and complete 16 North Area

wells testing new technology, improve capital

efficiency in the area, and increase asset value

► Test new intervals, including Austin Chalk

15Midland Basin 2018 Plan Objectives

Value creation through better wells, longer laterals, and increasing wells per section

Midland Basin

~88,000 net acres

► Initiate development stage in western

RockStar, continue delineation in RockStar

central Howard County

► Expect to drill ~130 net wells, optimize

landing zones

> 9 rigs in 1Q18 to 7 rigs at year-end

(average 8 for full year)

> 2 – 6 wells per pad

Sweetie

Peck

► Expect to complete ~100 net wells,

optimize completions

> Average 4 completion crews for full

year

Halff East

16Top Midland Basin Operator

SM Energy Ranks #1 in revenue per well and revenue per lateral foot

(1) Baird Equity Research 1/18/18 – Joseph Allman

17Premier Operator Permian

Top tier capital efficiency

Drilling Costs Completion Costs

800 12,000 1,200 3,000

Completion Cost Per Lateral Foot ($/ft)

Drilling Cost Per Lateral Foot ($/ft)

Proppant Per Lateral Foot (lb/ft)

700 10,500

1,000 2,500

Average Lateral Length (ft)

600 9,000

800 2,000

500 7,500

400 6,000 600 1,500

300 4,500

400 1,000

200 3,000

200 500

100 1,500

- - - -

2014 2015 2016 2017 2014 2015 2016 2017

Longer, faster and cheaper! Bigger, better and faster!

> Lateral lengths up 62% since 2014 > Stages per day up 71% since 2014

> Lateral Feet/Day up 171% since 2014 > Fluid per lateral foot up 55% since 2014

> $/Lateral Foot down 67% since 2014 > Sand per lateral foot up 24% since 2014

> Reduced stage spacing (200 to 167 ft/stage)

18Midland Basin Infrastructure Regional Sand Deal

Best in basin arrangement with US Silica and Sandbox Logistics

New sand mines

close to SM

locations ~55 miles(1)

~48 miles(1)

>$400K

expected capital Lamesa (3Q18)

savings per well Crane (1Q18)

(1) Road miles

19Midland Basin Infrastructure Water Management

Invest $70MM in fresh and produced water infrastructure

Expected cost

Accelerates System

savings

development control

(LOE + Capital)

20New Well Results

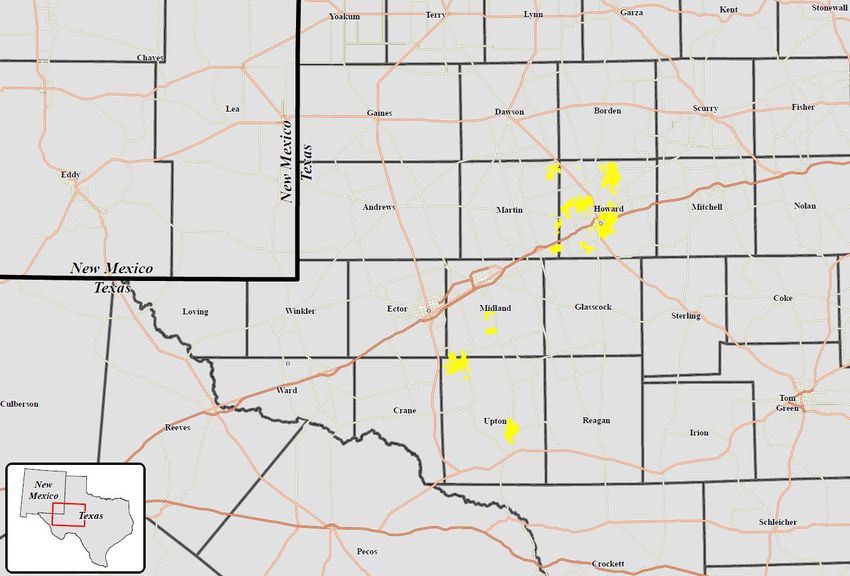

21New Well Results Howard County

Great results in multiple intervals across acreage position

Sundown 4566WB

Sundown 4524LS

Iceman 2-10A 1LS

Iceman 2-10A 2LS

Iceman 2-10A 3LS

Papagiorgio 33-40 B 1LS

Maverick 0341WA

Maverick 0361WB Fletch C 1352WA

Maverick 0342WA Fletch C 1368WB

Maverick 0321LS Fletch B 1351WA

Maverick 0322LS Fletch A 1350WA

Jester 2131LS

22Howard County New Well Results

Peak IP 24 Hour Clusters

Lateral IP per Proppant Oil

Well Name Interval Rate IP Days Peak IP Stages per

Length 1,000’ (lbs./ft) %

(BOE/d) Rate Stage

Maverick 0341WA(1) WCA 10,418 2,079 30-day 200 2,316 62 8 2,482 91

Maverick 0361WB(2) WCB 10,412 1,431 30-day 137 1,683 62 8 1,850 86

Maverick 0342WA(3) WCA 10,418 1,999 30-day 192 2,242 62 8 1,849 90

Fletch C 1352WA WCA 10,282 1,321 30-day 128 2,053 62 8 1,851 87

Fletch C 1368WB WCB 10,287 1,082 30-day 105 1,700 62 8 1,891 87

Fletch B 1351WA WCA 10,113 1,300 30-day 129 1,967 61 8 1,888 88

Fletch A 1350WA WCA 9,636 1,445 30-day 150 2,127 58 8 1,870 86

Sundown 4566WB WCB 10,336 1,035 30-day 100 1,435 83 8 1,966 91

Lower Spraberry

Iceman 2-10A 1LS LS 7,830 518 30-day 66 739 47 8 1,827 88

Iceman 2-10A 2LS LS 7,828 824 30-day 105 1,063 47 8 1,865 85

Iceman 2-10A 3LS LS 7,819 676 30-day 86 916 47 8 1,870 88

Papagiorgio 33-40 B 1LS LS 10,370 779 30-day 75 1,006 62 8 1,853 91

Jester 2131LS(4) LS 10,209 931 30-day 91 1,105 61 8 1,869 87

Maverick 0321LS(5) LS 10,419 1,048 30-day 101 1,194 62 8 1,849 88

Maverick 0322LS(6) LS 10,418 951 30-day 91 1,221 62 8 1,849 89

Sundown 4524LS LS 10,352 696 30-day 67 959 83 8 1,964 90

(1) Name changed from Maverick 09-03 A 1WA (4) Name changed from Jester 21-28 B 1LS

(2) Name changed from Maverick 09-03 A 1WB (5) Name changed from Maverick 09-03 A 1LS 23

(3) Name changed from Maverick 09-03 A 2WA (6) Name changed from Maverick 09-03 A 2LSHoward County Top Tier Well Performance Continues

New Wolfcamp wells continue outperformance trend

300,000

Gross Cumulative Production (BOE)

250,000

200,000

150,000

100,000

50,000

0

0 30 60 90 120 150 180 210 240 270 300 330 360

Days on Production

(1)

Previously Reported Well Avg New Well Avg(2) PEER 1MMBOE

Note: Monthly data normalized to days on production.

(1) Previously Reported Well Average includes all (19) previously reported SM operated wells on production since 11/3/2017.

(2) New Well Avg includes new Wolfcamp A and Wolfcamp B wells that have not been previously reported. 24Howard County Average Production by Formation

All intervals exceed peer 1 MMBoe type curve

300,000

Gross Cumulative Production (BOE)

250,000

200,000

150,000

100,000

50,000

0

0 50 100 150 200 250 300

Days on Production

WCA Average WCB Average LS Average PEER 1MMBOE

Note: Includes SM wells completed subsequent to 10/1/16.

25Differing Decline Characteristics of LS and WCA Wells

% of Peak Initial Production (IP) Rates vs Time, Jester and Papagiorgio Pads

Jester Pad Wells Papagiorgio Pad Wells

120% 120%

100% 100%

80% 80%

% of IP

% of IP

60% 60%

40% 40%

20% 20%

0% 0%

1

10

19

28

37

46

55

64

73

82

91

100

109

118

127

136

145

154

163

172

181

190

199

208

217

226

235

244

253

262

1

7

13

19

25

31

37

43

49

55

61

67

73

79

85

91

97

103

109

115

121

127

133

139

145

151

157

163

169

175

181

DAYS DAYS

JESTER WCA (BOPD/IP24HR) JESTER LS (BOPD/IP24HR) PAPAGIORGIO WCA (BOPD/IP24HR) PAPAGIORGIO LS (BOPD/IP24HR)

Lower Spraberry wells reach IP peak later but decline more slowly

26Inventory & Returns

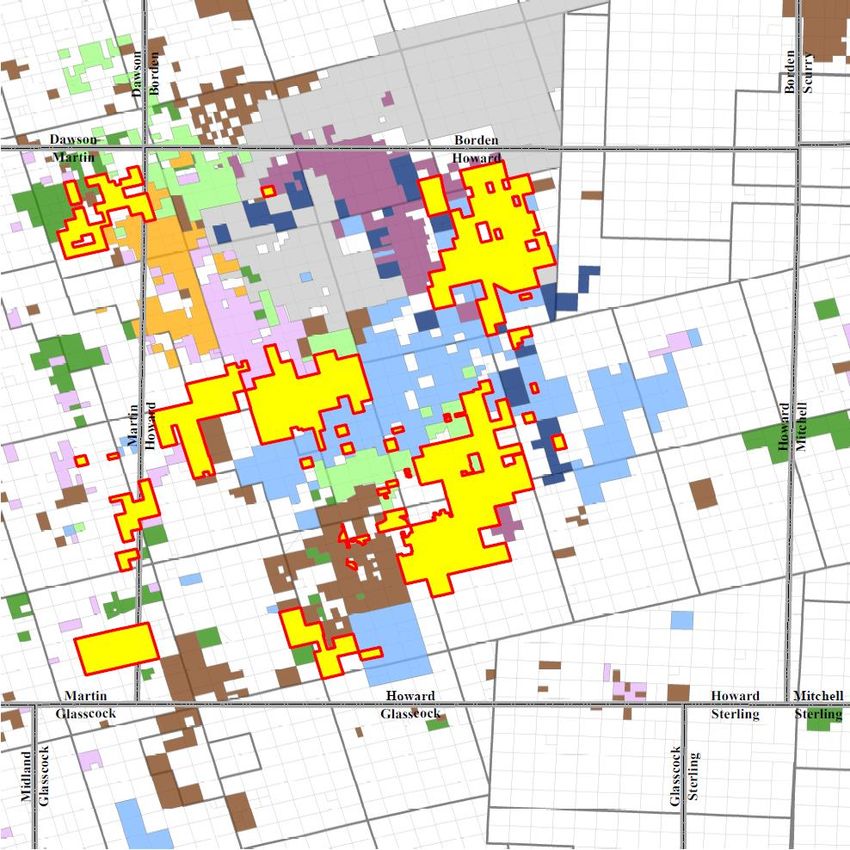

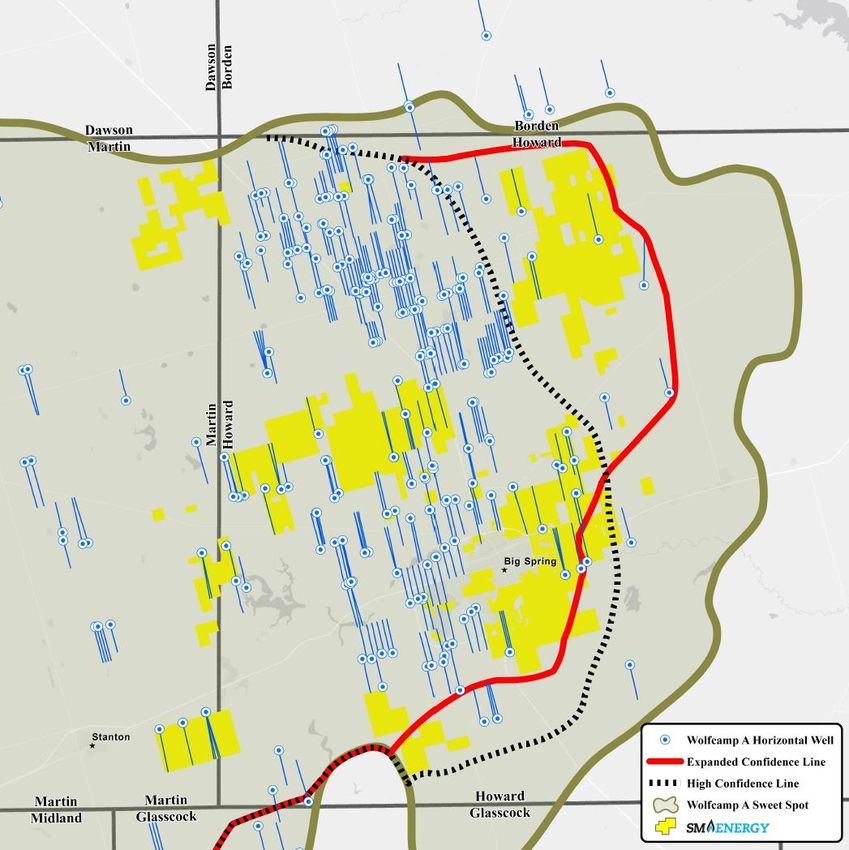

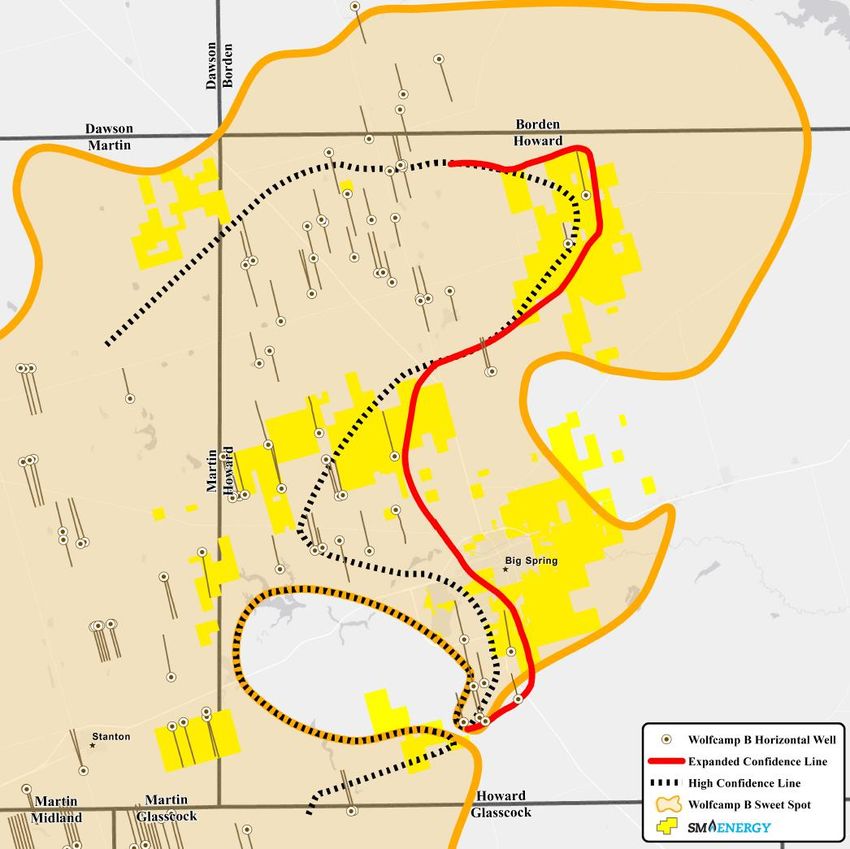

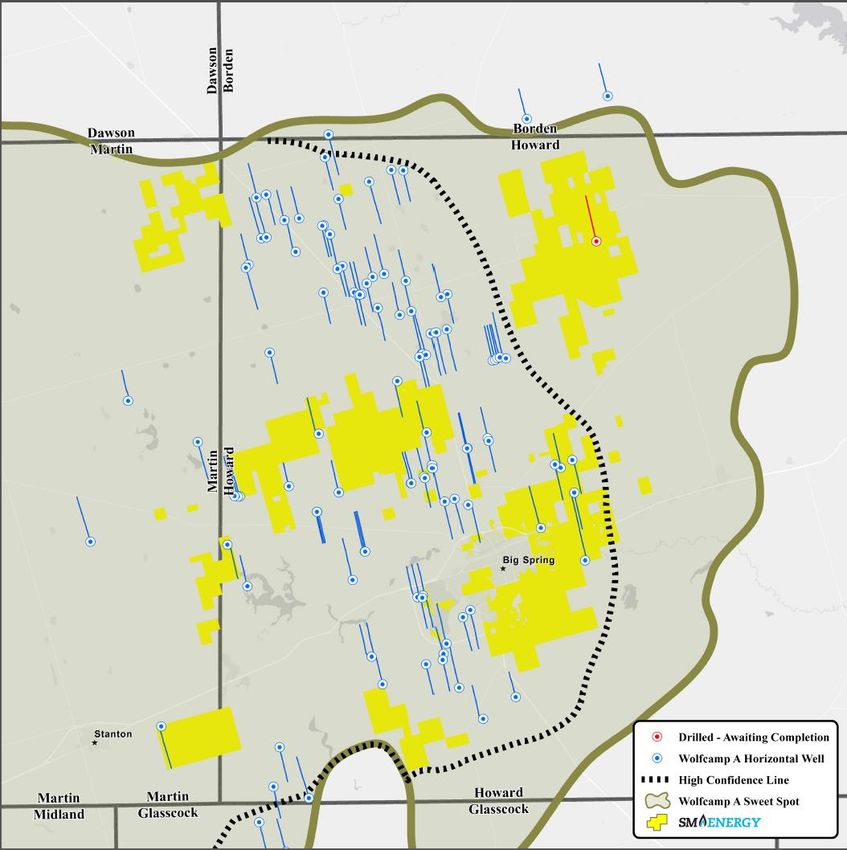

27Howard County Wolfcamp A Evolution of SM Sweet Spot Mapping

January 2017 February 2018

Higginbotham Unit B 30-19 1AH Cassidy 26-23 1H

Tall City – 6,397’ Tall City – 7,314’

Hyden 47-38 WA 1H 24hrIP = 403 BOEPD

24hrIP = 398 BOEPD

Grenadier – 9,639’

24hrIP = 848 BOEPD Viper 14-9 1WA

SM – 10,422’

24hrIP = 1,316 BOEPD

Oldham Trust 40-25 WA 1H

Grenadier – 10,426’

24hrIP = 1,274 BOEPD

Thumper 14-23 1AH

Sabalo – 10,105’

24hrIP = 1,357 BOEPD

Midland 15-10 1WA

Hannathon – 7,726’

24hrIP = 1,259 BOEPD

Broughton Wise 18-19 WA 1H

Grenadier – 7,012’

24hrIP = 875 BOEPD

Morgan Ranch 38-47 1WA

Hannathon – 7,727’

24hrIP = 713 BOEPD

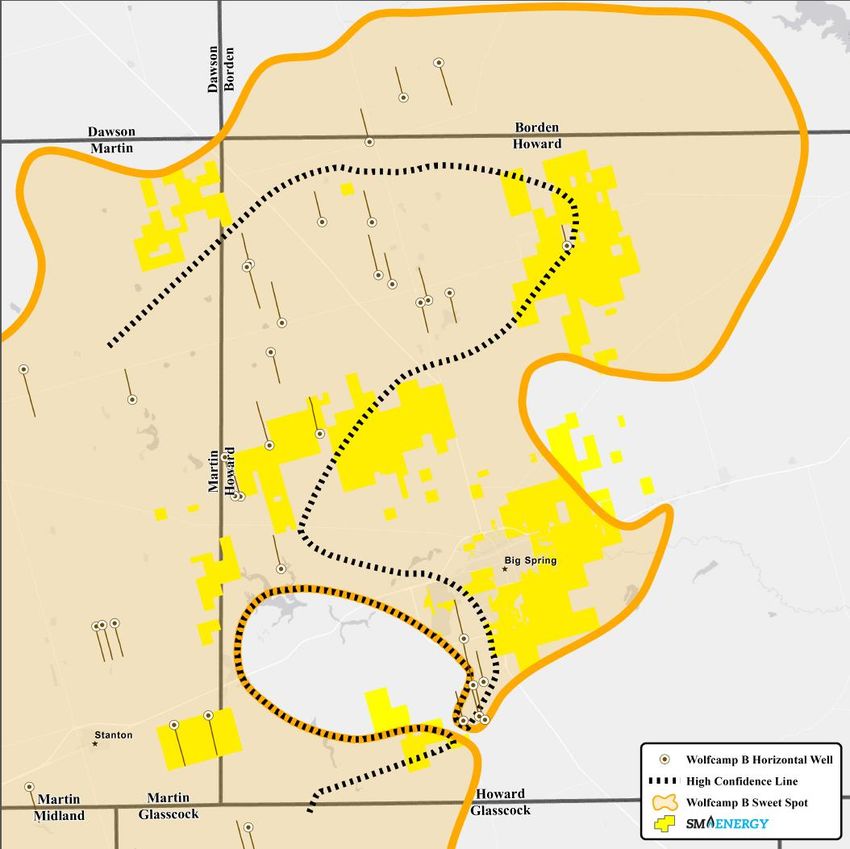

28Howard County Wolfcamp B Evolution of SM Sweet Spot Mapping

January 2017 February 2018

Sundown 4566WB

SM – 10,336’

24hrIP = 1,435 BOEPD

Prichard J 10BH

Legacy – 7,644’

24hrIP = 602 BOEPD

Maverick 0361WB

SM – 10,412’

24hrIP = 1,683 BOEPD Prichard J 9BH

Legacy – 7,641’

24hrIP = 655 BOEPD

International Unit 9H

Callon – 7,579’

24hrIP = 887 BOEPD

Fletch C 1368WB

SM – 10,287’

24hrIP = 1,700 BOEPD

Tubb 1WA

Crownquest – 9,873’

24hrIP = 1,178 BOEPD

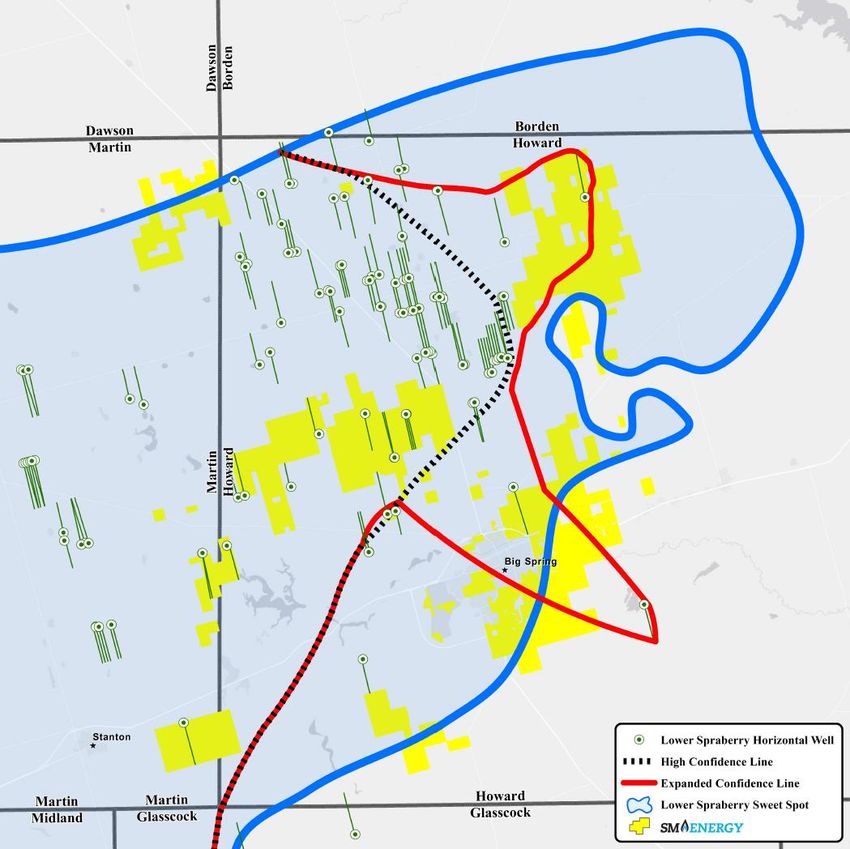

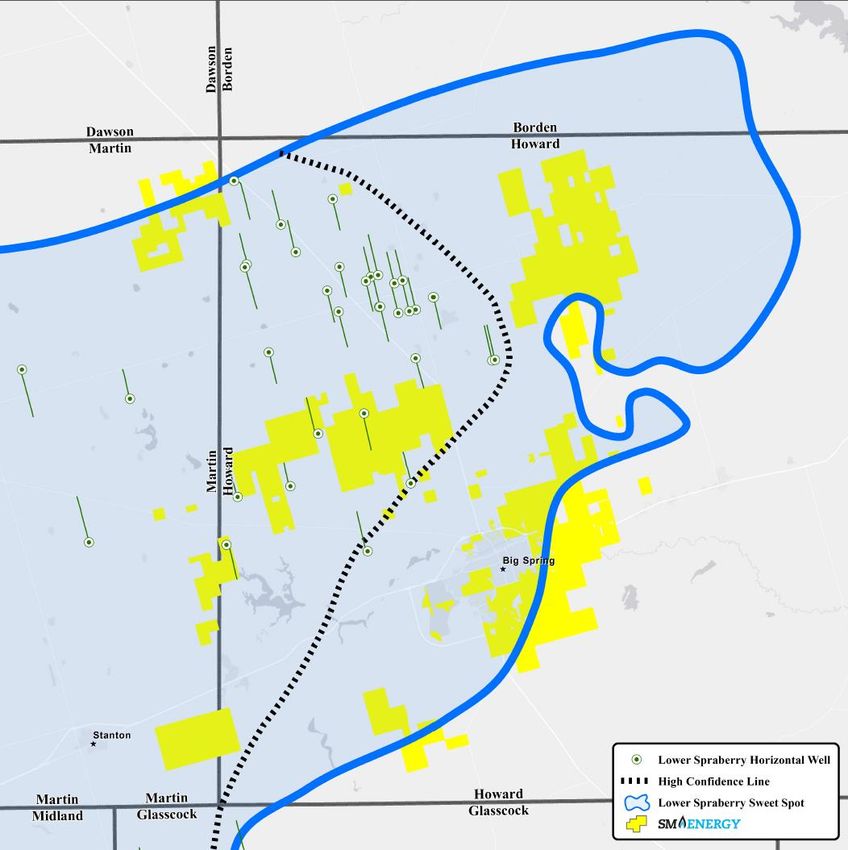

29Howard County Lower Spraberry Evolution of SM Sweet Spot Mapping

January 2017 February 2018

Sundown 4524 LS

Moby Dick 31-30 8SH

SM – 10,352’

Surge – 7,362’

24hrIP = 959 BOEPD

24hrIP = 319 BOEPD

Mr. Phillips 11-2 1SH

Sabalo – 10,047’

24hrIP = 1,032 BOEPD

Papagiorgio 33-40 B1LS

SM – 10,370’

24hrIP = 1,006 BOEPD

Allar LS

Hannathon – 7,580’

24hrIP = 1,135 BOEPD

30Drilling Inventory Midland Basin

Increasing inventory and NPV per section

4,000

3,500 Average Lateral Average Working

Length Interest

3,000

9,600’ 72%

Drilling Locations

(gross operated)

2,500

(up 13% from 2016) (up 10% from 2016)

2,000

Economic lateral feet 10% IRR threshold

1,500 increased economic locations:

17% 1,640(2)

1,000

~1,250 (from 2016) (comparable to peers)

500

0

(1)

Economic Resource Additional Resource

(1) Economic Resource represents 3P inventory within the confirmed contours and 20% IRR at $60/Bbl oil, $3/MMBtu natural gas, $30/Bbl NGLs

(2) 3P inventory inside and outside the confirmed contours; 10% IRR

31Drilling Inventory ~15 Years at Current Activity Level

Approximately 45 years including upside resources

Midland Basin and Eagle Ford

6,000

5,000

Drilling Locations

4,000

(gross operated)

3,000

2,000

1,000

0

Economic Resource(1) Additional Resource

Note: Eagle Ford 2017 average lateral length = 9,000’; up 18% from 2016

(1) Economic Resource represents 3P inventory within the confirmed contours for Howard and Martin Counties and 20% IRR at $60/Bbl oil,

$3/MMBtu natural gas, $30/Bbl NGLs

32Top-Tier Assets Regional Well Projected Economics

RockStar Sweetie Peck

Wells(1) across all intervals (WCA, WCB, LS) in the 2018 drilling program Wells(1) across all intervals (WCA, WCB, LS) in the 2018 drilling program

120% 100%

100%

80%

80%

60%

IRR

IRR

60%

40%

40%

20% 20%

0% 0%

$50 $55 $60 $65 $50 $55 $60 $65

NYMEX WTI NYMEX WTI

Well Cost: $8.3MM Well Spacing: 513’ – 660’ Well Cost: $7.5MM Well Spacing: 660’

Sand loading: 1,900 lbs/ft; Stage Spacing: 167’; Length: 10,000’ Sand loading: 1,900 lbs/ft; Stage Spacing: 167’; Length: 8,333’

Eagle Ford

Wells(1) across UEF/LEF in East, South and North Area in the 2018 drilling program

60%

50%

40%

IRR

30%

January 2018 Average

Mt. Belvieu ($/Gal)

20%

10%

0%

$0.60 $0.70 $0.80

Mt. Belvieu $/Gal

Well Cost: $6.8MM, Lateral Length: 8,800’, Well Spacing: 625’-900’, Sand Loading: 2,000 lbs/ft, Stage Spacing: 150’

Note: well costs include drill, complete, and equip; sensitivities at $3.00/MMBtu NYMEX; Eagle Ford oil flat at $60/Bbl WTI, excludes JV wells

(1) Weighted average by interval

332018 Planned Rig Activity and Completions By Month

2018: expected ~100 net completions Midland Basin; expected ~25 net completions Eagle Ford

14 120

12

100

Drilled But Uncompleted Wells

10

80

Operated Rigs

8

60

(1)

6

40

4

20

2

0 0

Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Midland Basin Eagle Ford Total Net DUCs

Note: The Company is currently operating one rig in the Powder River Basin, Wyoming, which is funded entirely through a carry arrangement with a third party

34SM Energy Premier Operator of Top Tier Assets

4 recent analyst initiation reports, 4 great recommendations

Value

proposition

“SM undervalued based on CF growth per debt adjusted share”

- Credit Suisse 12/11/17 - William Featherston

“Key differentiator is its Howard County acreage that has lived

up to management’s expectations and belied industry and

investor skepticism”

- Deutsche Bank 2/1/18 - Nitin Kumar

Drilling

“Top Midland Basin operator…SM ranks #1 in the Midland

catalysts Basin on a revenues per lateral foot basis”

- Baird 12/18/17 - Joseph Allman

“…growth asset base (Permian) sufficiently geologically de-

risked and SM now ideally positioned… From this point

forward should create a disproportionate amount of risk

adjusted equity value”

- FBR 2/5/18 - Rehan Rashid

“see upside to 2018 oil production given strong Howard County

well results and solid execution in 2017; less concerned about

2018 outspend given more constructive oil prices and visibility to

cash flow neutrality in 2019”

- Credit Suisse 12/11/17 - William Featherston

35Appendix

362017

Financial & Operating

Results

374th Quarter and FY 2017 Performance Solid Execution

Production 4Q17 FY 2017

Total Production (MMBoe) 10.4 44.5

Average Daily Production (MBoe/d) 112.6 121.8

Pre-Hedge Realized Price ($/Boe) $32.95 $28.20

Post-Hedge Realized Price ($/Boe) $32.16 $28.68

Costs $/Boe $/Boe

LOE $5.10 $4.43

Ad Valorem $0.33 $0.34

LOE including Ad Valorem $5.43 $4.77

Transportation $5.01 $5.48

Production Taxes (~4.0 – 4.5% of pre-derivative oil,

$1.41 $1.18

gas & NGL revenue)

Production Expenses $11.85 $11.43

Cash Production Margin (pre-hedge) $21.10 $16.77

G&A – Cash $2.69 $2.28

Cash Margin (pre-hedge) $18.41 $14.49

G&A – Non Cash $0.69 $0.43

DD&A $12.69 $12.53

38Well Hedged(1)

2018 percentage of expected production hedged

► ~85% of expected 1Q18 production

Production Hedged volumes hedged(2); ~65% of oil

volumes, ~85% of gas volumes (NGLs

hedged by product)

► ~75% of expected 2018 production95%

volumes hedged(2) : ~75% of oil

volumes, ~65% of gas volumes (NGLs

2018 75% hedged by product)

► Credit Agreement allows hedging of up

to 85% of projected production for the

first three years

► Significant hedge positions limit effect of

oil price changes when price is greater

than $57/Boe or less than $51/Boe

Note: The hedged volumes on this slide do not include any volumes related to basis swaps. See Appendix for details.

(1) Hedging data as of February 15, 2018 39

(2) At mid-point of guidanceBalance Sheet Solid Position Entering 2018

Liquidity of $1.2B, including $314MM cash on hand(1)

Balance Sheet offers financial flexibility

> No bond maturities until 2021

> Senior Secured Debt:TTM Adjusted EBITDAX at ~0.0 times; max ratio allowed 2.75 times

> TTM Adjusted EBITDAX:Interest at ~3.8 times; minimum ratio required 2.0 times

Debt Maturities(1)

(in millions)

$1,000

Facilities

Commitments and Borrowing Base: $925 million(3) 6%

Drilling and $750(1)

Completion Other

Corporate ratings: S&P BB-, Moody’s B1 8%

86% Other

$500

$172.5 86% 8%

$562 $500 $500 $500 $250

$345 $395

~$0 drawn

$0

2018 2019 2020 2021 2022 2023 2024 2025 2026

1.500%

Coupon 6.500%

6.125% 6.500% 5.000% 5.625% 6.750%

Yield to worst(2) 5.66% 5.64% 6.38% 6.13% 6.56% 6.59%

Initial call date 11/2016 11/2018 7/2017 7/2018 6/2020 9/2021

Initial call price 103.25% 103.06% 103.25% 102.50% 102.81% 103.38%

(1) As of December 31, 2017 (3) Reaffirmed November 2017

(2) As of February 15, 2018 404Q17 Regional Realizations

Benchmark Pricing

NYMEX WTI Oil ($/Bbl) $55.40

NYMEX LLS Oil ($/Bbl) $60.98

NYMEX Henry Hub Gas ($/MMBTU) $2.93

Hart Composite NGL ($/Bbl) $32.12

Production Volumes Eagle Ford(1) Permian Rocky Mountain SM Total

Oil (MBbls) 355 2,826 636 3,817

Gas (MMcf) 20,423 4,619 950 25,992

NGL (MBbls) 2,163 5 38 2,206

MBOE 5,922 3,601 833 10,356

Revenue (in thousands)

Oil $17,012 $152,432 $34,105 $203,549

Gas 56,750 21,501 2,003 80,254

NGL 56,093 142 1,149 57,384

Total $129,855 $174,075 $37,257 $341,188

Expenses (in thousands)

LOE $16,381 $25,383 $11,042 $52,807

Ad Valorem 2,469 940 35 3,444

Transportation 50,201 166 1,564 51,931

Production Taxes 2,421 8,637 3,592 14,650

Per Unit Metrics:

Realized Oil/Bbl $47.91 $53.94 $53.58 $53.32

% of Benchmark - WTI 86% 97% 97% 96%

Realized Gas/Mcf $2.78 $4.66 $2.11 $3.09

% of Benchmark – NYMEX HH 95% 159% 72% 105%

Realized NGL/Bbl $25.94 $26.36 $30.12 $26.01

% of Benchmark – HART 81% 82% 94% 81%

Realized BOE $21.93 $48.34 $44.73 $32.95

LOE/BOE $2.77 $7.05 $13.26 $5.10

Ad Val/BOE $0.42 $0.26 $0.04 $0.33

Transportation/BOE $8.48 $0.05 $1.88 $5.01

Production Tax- per BOE/% of Pre-Hedge $0.41/1.9% $2.40/5.0% $4.31/9.6% $1.41/4.3%

Revenue

Production Margin $9.86 $38.59 $25.24 $21.09

Note: Totals may not sum due to rounding and other classifications

(1) Includes nominal amounts of other production and expenses from the region. 412017 Activity Wells Drilled, Flowing Completions & DUC Count

Wells Drilled Flowing Completions DUC Count

4th Quarter 2017 2017 YTD 4th Quarter 2017 2017 YTD As of 12/31/17

Region Gross Net Gross Net Gross Net Gross Net Gross Net

Permian

Sweetie Peck 5 5 30 28 9 8 32 31 9 8

RockStar 27 22 74 66 15 14 40 39 40 33

Permian total 32 27 104 94 24 22 72 70 49 41

Eagle Ford 10 7 27 24 - - 38 35 33 30

Rocky Mountain

Divide County - - - - 2 2 2 2 18 15

Powder River Basin(1) 3 - 11 1 2 - 8 1 4 -

Rocky Mountain total 3 - 11 1 4 2 10 3 22 15

Subtotal Operated Wells 45 34 142 119 28 24 120 108 104 86

Non-operated Wells(2) n/a 1 n/a 4 n/a - n/a 3 n/a 1

Total n/a 35 n/a 123 n/a 24 n/a 111 n/a 87

As of December 31, 2017

(1) Activity in the Powder River Basin is provided by third party services and funding.

(2) Non-operated activity relates to wells located in the Permian Basin. 42Leasehold Summary

Pro-forma for pending transactions

Net Acres(1) Pro-forma

12/31/17 Pending Sales Net Acres

Midland Basin

RockStar 65,150 - 65,150

Sweetie Peck(2) 17,265 - 17,265

Halff East (Upton County) 5,420 - 5,420

Midland Basin Total 87,835 - 87,835

Eagle Ford 164,605 - 164,605

Rocky Mountain

Divide 119,415 - 119,415

Powder River Basin 138,545 (112,125) 26,420

Rocky Mountain Other(3) 186,845 - 186,845

Other Areas/Exploration 24,915 - 24,915

Total 722,160 (112,125) 610,035

(1) Includes developed and undeveloped oil and gas leasehold, fee properties, and mineral servitudes held as of December 31, 2017.

(2) Sweetie Peck acreage includes 2,450 net acres of drill-to-earn acreage.

(3) Rocky Mountain Other includes non-core Williston Basin, and other non-core acreage located in North Dakota, Montana, Wyoming, and Utah.

43Adjusted EBITDAX Reconciliation

Reconciliation of net loss (GAAP) to adjusted EBITDAX (non-GAAP) to Three Months Ended Twelve Months Ended

net cash provided by operating activities (GAAP): (in thousands) December 31, 2017 December 31, 2017

Net loss (GAAP) $(26,258) $(160,843)

Interest expense 43,618 179,257

Interest income (1,067) (3,968)

Income tax benefit (117,145) (182,970)

Depletion, depreciation, amortization, and asset retirement obligation liability accretion 131,393 557,036

Exploration(1) 14,484 49,879

Impairment of proved properties - 3,806

Abandonment and impairment of unproved properties 12,115 12,272

Stock-based compensation expense 6,540 22,700

Net derivative loss 115,778 26,414

Derivative settlement gain (loss) (8,168) 21,234

Net (gain) loss on divestiture activity (537) 131,028

Loss on extinguishment of debt - 35

Other, net 3,200 8,820

Adjusted EBITDAX (Non-GAAP) $173,953 $664,700

Interest expense (43,618) (179,257)

Interest income 1,067 3,968

Income tax benefit 117,145 182,970

Exploration(1) (14,484) (49,879)

Exploratory dry hole expense 2,381 2,381

Amortization of debt discount and deferred financing costs 3,798 16,276

Deferred income taxes (124,608) (192,066)

Plugging and abandonment (640) (2,735)

Other, net 326 (581)

Changes in current assets and liabilities 29,460 69,613

Net cash provided by operating activities (GAAP) $144,780 $515,390

Adjusted EBITDAX represents net income (loss) before interest expense, interest income, income taxes, depletion, depreciation, amortization and asset retirement obligation liability accretion expense, exploration expense, property abandonment and

impairment expense, non-cash stock-based compensation expense, derivative gains and losses net of settlements, gains and losses on divestitures, gains and losses on extinguishment of debt, and certain other items. Adjusted EBITDAX excludes

certain items that we believe affect the comparability of operating results and can exclude items that are generally one-time in nature or whose timing and/or amount cannot be reasonably estimated. Adjusted EBITDAX is a non-GAAP measure that we

present because we believe it provides useful additional information to investors and analysts, as a performance measure, for analysis of our ability to internally generate funds for exploration, development, acquisitions, and to service debt. We are also

subject to financial covenants under our Credit Agreement based on adjusted EBITDAX ratios. In addition, adjusted EBITDAX is widely used by professional research analysts and others in the valuation, comparison, and investment recommendations

of companies in the oil and gas exploration and production industry, and many investors use the published research of industry research analysts in making investment decisions. Adjusted EBITDAX should not be considered in isolation or as a

substitute for net income (loss), income (loss) from operations, net cash provided by operating activities, or other profitability or liquidity measures prepared under GAAP. Because adjusted EBITDAX excludes some, but not all items that affect net

income (loss) and may vary among companies, the adjusted EBITDAX amounts presented may not be comparable to similar metrics of other companies. Our credit facility provides a material source of liquidity for us. Under the terms of our Credit

Agreement, if we failed to comply with the covenants that establish a maximum permitted ratio of senior secured debt to adjusted EBITDAX and a minimum permitted ratio of adjusted EBITDAX to interest, we would be in default, an event that would

prevent us from borrowing under our credit facility and would therefore materially limit our sources of liquidity. In additi on, if we are in default under our credit facility and are unable to obtain a waiver of that default from our lenders, lenders under that

facility and under the indentures governing our outstanding Senior Notes and Senior Convertible Notes would be entitled to exercise all of their remedies for default.

(1) Stock-based compensation expense is a component of exploration expense and general and administrative expense on the statements of operations. Therefore, the exploration line

items shown in the reconciliation above will vary from the amount shown on the statements of operations for the component of stock-based compensation expense recorded to

exploration expense.

44Adjusted Net Loss Reconciliation

Reconciliation of net loss (GAAP) to adjusted net loss Three Months Ended Twelve Months Ended

(non-GAAP): (in thousands, except per share data) December 31, 2017 December 31, 2017

Net loss (GAAP) $(26,258) $(160,843)

Net derivative loss 115,778 26,414

Derivative settlement gain (loss) (8,168) 21,234

Net (gain) loss on divestiture activity (537) 131,028

Impairment of proved properties - 3,806

Abandonment and impairment of unproved properties 12,115 12,272

Loss on extinguishment of debt - 35

Other, net 8,200 13,820

Tax effect of adjustments(1) (45,987) (75,308)

US tax reform (63,675) (63,675)

Adjusted net loss (Non-GAAP) $(8,532) $(91,217)

Diluted net loss per common share (GAAP) $(0.24) $(1.44)

Net derivative loss 1.04 0.24

Derivative settlement gain (loss) (0.07) 0.19

Net (gain) loss on divestiture activity - 1.18

Impairment of proved properties - 0.03

Abandonment and impairment of unproved properties 0.11 0.11

Loss on extinguishment of debt - -

Other, net 0.07 0.12

Tax effect of adjustments(1) (0.42) (0.68)

US tax reform (0.57) (0.57)

Adjusted net loss per diluted common share (Non-GAAP) $(0.08) $(0.82)

Diluted weighted-average common shares outstanding (GAAP): 111,611 111,428

Adjusted net loss excludes certain items that the Company believes affect the comparability of operating results. Items excluded generally are non-recurring items or are items whose timing

and/or amount cannot be reasonably estimated. These items include non-cash and other adjustments, such as derivative gains and losses net of settlements, impairments, net (gain) loss on

divestiture activity, materials inventory loss, and gains or losses on extinguishment of debt. The non-GAAP measure of adjusted net income (loss) is presented because management believes

it provides useful additional information to investors for analysis of SM Energy's fundamental business on a recurring basis. In addition, management believes that adjusted net income (loss) is

widely used by professional research analysts and others in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and production industry,

and many investors use the published research of industry research analysts in making investment decisions. Adjusted net income (loss) should not be considered in isolation or as a

substitute for net income (loss), income (loss) from operations, cash provided by operating activities, or other income, profitability, cash flow, or liquidity measures prepared under GAAP.

Since adjusted net income (loss) excludes some, but not all, items that affect net income (loss) and may vary among companies, the adjusted net income (loss) amounts presented may not

be comparable to similarly titled measures of other companies.

(1) Income taxes are calculated using a tax rate of 36.1%, for the three and twelve-month periods ended December 31, 2017. These rates approximate

the Company's statutory tax rate adjusted for ordinary permanent differences. 45Total Capital Spend Reconciliation

Reconciliation of costs incurred in oil and gas

activities (GAAP) to Total capital spend Twelve Months Ended

(Non-GAAP)(1)(3) (in millions) December 31, 2017

Costs incurred in oil and gas activities (GAAP): $1,040.0

Asset retirement obligation (12.1)

Capitalized interest (12.6)

Proved property acquisitions(2) (1.6)

Unproved property acquisitions (78.6)

Other 1.3

Total capital spend (Non-GAAP): $936.4

(1) The non-GAAP measure of total capital spend is presented because management believes it provides useful information to investors for analysis of

SM Energy's fundamental business on a recurring basis. In addition, management believes that total capital spend is widely used by professional

research analysts and others in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and

production industry, and many investors use the published research of industry research analysts in making investment decisions. Total capital spend

should not be considered in isolation or as a substitute for Costs Incurred or other capital spending measures prepared under GAAP. The total capital

spend amounts presented may not be comparable to similarly titled measures of other companies.

(2) Includes approximately $1.4 million of ARO associated with proved property acquisitions for the year ended December 31, 2017.

(3) The Company completed several primarily non-monetary acreage trades in the Midland Basin during 2017 totaling $294.0 million of value attributed to

the properties surrendered. This non-monetary consideration is not reflected in the costs incurred or capital spend amounts presented above.

46PV-10 Reconciliation

Reconciliation of standardized measure (GAAP) to As of

PV-10 (Non-GAAP)(1) (in millions) December 31, 2017

Standardized measure of discounted future net cash flows (GAAP): $3,024.1

Add: 10 percent annual discount, net of income taxes 2,573.2

Add: future undiscounted income taxes 205.7

Undiscounted future net cash flows 5,803.0

Less: 10 percent annual discount without tax effect (2,746.5)

PV-10 (Non-GAAP): $3,056.5

(1) The non-GAAP measure of PV-10 is presented because management believes it provides useful information to investors for analysis of SM Energy's

fundamental business on a recurring basis. In addition, management believes that PV-10 is widely used by professional research analysts and others

in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and production industry, and many

investors use the published research of industry research analysts in making investment decisions. PV-10 should not be considered in isolation or as

a substitute for other measures prepared under GAAP.

47Oil and Gas Derivative Positions

By quarter through 2019

Fixed Swaps Oil Gas

Volume Volume

Period (MBbls) $/Bbl(1) (BBTU) $/MMBTU(1)

1Q’18 1,075 $50.16 20,788 $3.25

2Q’18 1,534 $49.57 15,712 $2.85

3Q’18 1,769 $49.77 17,147 $2.88

4Q’18 1,894 $49.87 18,646 $2.91

1Q’19 442 $50.70 16,979 $2.92

2Q’19 439 $50.70 - -

3Q’19 524 $50.70 - -

4Q’19 535 $50.70 - -

Collars Oil Midland – Cushing Oil Basis Swaps

Volume Ceiling Floor Volume Price Differential

Period (MBbls) $/Bbl(1) $/Bbl(1) Period (MBbls) $/Bbl(1)

1Q’18 1,445 $59.07 $50.00 1Q’18 2,113 ($1.15)

2Q’18 1,459 $59.03 $50.00 2Q’18 2,392 ($1.03)

3Q’18 1,948 $58.61 $50.00 3Q’18 3,018 ($1.06)

4Q’18 2,222 $58.44 $50.00 4Q’18 3,327 ($1.08)

1Q’19 1,445 $59.25 $47.75 1Q’19 1,366 ($1.07)

2Q’19 1,450 $59.23 $47.67 2Q’19 1,411 ($1.08)

3Q’19 1,501 $59.18 $47.59 3Q’19 1,497 ($1.09)

4Q’19 1,511 $59.12 $47.58 4Q’19 1,515 ($1.10)

Note: Includes all commodity derivative contracts for settlement at any time during the first quarter of 2018 and later periods through 2019, entered into as of 2/15/18.

(1) Prices are weighted averages; natural gas prices reflect the weighted average of regional contract positions and are no longer adjusted to a

NYMEX equivalent. 48NGL Derivative Position Detail(1)

NGL Swaps OPIS Eth Purity Mt Belv NGL Swaps OPIS Propane Mt Belv Non-TET NGL Swaps OPIS IsoButane Mt Belv Non TET

Volume Volume Volume

(2) (2) (2)

Period (MBbls) $/Bbl Period (MBbls) $/Bbl Period (MBbls) $/Bbl

1Q’18 923 $10.90 1Q’18 628 $25.39 1Q’18 167 $35.76

2Q’18 915 $10.87 2Q’18 554 $24.94 2Q’18 66 $35.07

3Q’18 1,033 $10.99 3Q’18 610 $24.27 3Q’18 70 $35.07

4Q’18 1,146 $11.18 4Q’18 671 $24.39 4Q’18 76 $35.07

2018 Total 4,017 2018 Total 2,463 2018 Total 379

1Q’19 853 $12.25 1Q’19 440 $26.13 1Q’19 29 $35.70

2Q’19 877 $12.29 2Q’19 348 $28.53 2Q’19 29 $35.70

3Q’19 907 $12.34 3Q’19 360 $28.53 3Q’19 30 $35.70

4Q’19 896 $12.36 4Q’19 355 $28.53 4Q’19 29 $35.70

2019 Total 3,533 2019 Total 1,503 2019 Total 117

1Q’20 275 $11.13

NGL Swaps Natural Gasoline Mt Belv Non TET NGL Swaps OPIS NButane Mt Belv Non TET

2Q’20 264 $11.13

Volume Volume

2020 Total 539 (2) (2)

Period (MBbls) $/Bbl Period (MBbls) $/Bbl

1Q’18 189 $49.40 1Q’18 206 $35.83

2Q’18 175 $50.99 2Q’18 84 $35.69

3Q’18 202 $51.13 3Q’18 93 $35.70

4Q’18 208 $50.99 4Q’18 102 $35.70

2018 Total 774 2018 Total 485

1Q’19 48 $50.93 1Q’19 37 $35.64

2Q’19 49 $50.93 2Q’19 38 $35.64

3Q’19 50 $50.93 3Q’19 39 $35.64

4Q’19 50 $50.93 4Q’19 39 $35.64

2019 Total 197 2019 Total 153

(1) Includes all commodity derivative contracts for settlement at any time during the first quarter of 2017 and later periods entered into as of February 15, 2018.

(2) Weighted-Average Contract Price 49NGL Realizations

• 30% increase in realized price (before hedges) from 4Q16 to 4Q17

• SM NGL price realizations are predominately tied to Mont Belvieu, fee

based contracts

• Differential reflects NGL barrel product mix and transportation and

fractionation fees

SM Typical NGL Bbl(1)

4Q16 1Q17 2Q17 3Q17 4Q17

13%

Mt. Belvieu ($/Bbl) $24.11 $26.74 $24.11 $27.55 $32.12

9%

42%

SM Realization $20.02 $22.06 $19.71 $22.40 $26.01 9%

($/Bbl)

27%

% Differential to 83% 82% 82% 81% 81%

Mt. Belvieu

Ethane Propane

Iso Butane Normal Butane

Natural Gasoline

(1) Includes the effects of ethane rejection

50Howard County Operators

SM Energy

Callon

Encana

Surge/Yantai Xinchao

Diamondback

Oxy

Energen

Breitburn

Sabalo

Grenadier

51Sweetie Peck Operators

SM Energy

Apache

Chevron

Concho

Devon

Diamondback

Discovery

Endeavor

Exxon

Legacy

Oxy

Pioneer

Summit

Miscellaneous

52Eagle Ford Operators

Dimmit

Maverick

Dimmit

Webb

Area

North

Fasken

Area

East

Area

South

53Divide County Operators

Canada

CPEG

RE

RE HES

CPEG RE

FAC

FAC

CLR

MRX HNT

NP

Divide

Williams

KKN CLR

HES

CPEG

54Reserves and Resources

Information about the terms “economic resources” and “economic inventory”

The Securities and Exchange Commission (“SEC”) requires oil and natural gas companies, in their filings with the SEC, to disclose proved

reserves, which are those quantities of oil, natural gas and NGLs, which, by analysis of geoscience and engineering data, can be estimated with

reasonable certainty to be economically producible—from a given date forward, from known reservoirs and under existing economic conditions

(using the trailing 12-month average first-day-of-the-month prices), operating methods and government regulations—prior to the time at which

contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic

or probabilistic methods are used for the estimation. The SEC also permits the disclosure of separate estimates of probable or possible

reserves that meet SEC definitions for such reserves; however, the Company currently does not disclose probable or possible reserves in its

SEC filings.

In this presentation, proved reserves attributable to the Company at December 31, 2017, are estimated utilizing SEC reserve recognition

standards and pricing assumptions based on the trailing 12-month average first-day-of-the-month prices of $51.34 per Bbl of oil, $3.00 per

MMBtu of natural gas, and $27.69 per Bbl of NGLs. At least 80% of the PV-10 of the Company’s estimate of its total proved reserves at

December 31, 2017, was audited by Ryder Scott Company, L.P. The Company may use the terms “economic resource,” “economic inventory,”

“additional resource” and similar phrases to describe estimates of gross drilling locations that the SEC rules may prohibit from being included in

filings with the SEC. These are the Company’s internal estimates of drilling locations. These quantities may not constitute “reserves” within the

meaning of the Society of Petroleum Engineer’s Petroleum Resource Management System or SEC rules. Such estimates and identified drilling

locations may not have been fully risked by Company management and are inherently more speculative than proved reserves estimates. Actual

locations drilled and quantities that may be ultimately recovered from the Company’s interests could differ substantially from these estimates.

There is no commitment by the Company to drill all of these drilling locations.

The calculation of economic resources is not necessarily calculated in accordance with SEC guidelines for proved reserves and is not reviewed

by third party engineers. Economic resources presented in this presentation are calculated using benchmark pricing and projected pricing,

which differs from the pricing used for proved reserves. Management believes the presentation of economic resources and economic drilling

inventory are useful to investors in the valuation of SM Energy; however, the calculations may not be consistent with similar metrics provided by

peers.

55Definitions of Non-GAAP, forward looking metrics

The following metrics are forward-looking non-GAAP financial measures. The Company believes these measures are commonly

used in the E&P industry, and other industries, by shareholders, professional research analysts and others in valuation,

comparison and investment recommendations. Certain forward-looking metrics cannot be presented in conjunction with a

reconciliation to the closest GAAP measure, because certain portions of the forecast calculation would are inherently

unpredictable. Accordingly, investors are cautioned not to place undue reliance on these numbers.

1) Projected cash flow per debt adjusted share:

For purposes of forward-looking cash flow from operations, it is not possible to project changes in working capital. The Company calculates

forward-looking cash flow as projected adjusted EBITDAX (reconciled above to GAAP Net Loss and GAAP Net cash provided by operating

activities for actual results) less projected cash interest expense and cash taxes.

The calculation of debt adjusted shares is the sum of average fully diluted common shares outstanding plus the quotient of total principal value

of long-term debt outstanding (including senior notes, convertible stock, credit facility) less cash and cash equivalents divided by the price of

common stock. In the case of the current 2-year plan, the price of common stock used is the closing price at year-end 2017.

2) Capital spend:

For purposes of forward-looking capital spend, it is the sum of projected capital expenditures for drilling and completion of wells, capitalized

geologic and geophysical work, exploration costs excluding dry hole expenses, facilities and infrastructure, allocated overhead and land costs

exclusive of acquisitions.

Capital spend as reported for actual results is reconciled above to GAAP costs incurred in oil and gas activities.

3) Net debt:EBITDAX:

Net debt is total principle value of long-term debt outstanding less cash and cash equivalents. Projected net debt:EBITDAX is projected net debt

divided by projected adjusted EBITDAX. Adjusted EBITDAX is reconciled above to GAAP Net Loss and GAAP Net cash provided by operating

activities for actual results.

56Contact Information

Jennifer Martin Samuels

Vice President - Investor Relations

303-864-2507

jsamuels@sm-energy.com

57You can also read