2018 ESTATE AGENTS TRUST ACCOUNTS INFORMATION SESSION - FNB Learning Centre, Sandton 12 April 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2018 ESTATE AGENTS TRUST

ACCOUNTS INFORMATION

SESSION

FNB Learning Centre, Sandton

12 April 2018

1

2018 ESTATE AGENTS

TRUST ACCOUNTS

INFORMATION

SESSION

Presented by:

THOMAS MAKUPO CA(SA), RA

Audit Compliance Manager

Estate Agency Affairs Board

12 April 2018

WHAT WILL BE COVERED IN THIS INFORMATION SESSION Important definitions Scope of audits for estate agents Auditors reporting responsibilities Specific focus areas during an audit of estate agents MyEAAB Auditors Portal Consequences of late audit report submissions Consequences of audit findings in submitted audit reports Winding up of estate agency business IRBA inspection findings on audits of trust accounts Statistics on submitted audit reports and contraventions

IMPORTANT DEFINITIONS

Definition of estate agent

An estate agent means any person (or entity) who (which) for the acquisition of

gain carries the following business on the instructions of or on behalf of any

other person (or entity):

i. Sells or purchases or publicly exhibits for sale immovable property or

negotiates in connection therewith or canvasses or undertakes or offers to

canvass a seller or purchaser;

ii. Lets or hires or publicly exhibits for hire immovable property or negotiates

in connection therewith or canvasses or undertakes or offers to canvass a

lessee or lessor;

iii. Collects or receives any moneys payable on account of a lease of

immovable property

IMPORTANT DEFINITIONS Cont’d

Definition of an estate agent (Cont’d):

iv. Includes any person who is employed by an attorney;

v. But excludes an attorney who, on his own account or as a partner in a firm

of attorneys, (or an articled clerk) who performs estate agent activities

mentioned above:

a. In the course of; and

b. In the name of;

c. From the premises of such attorney.

Managing Agents and Independent contractors also falls within the definition.

NB: An estate agent also has to register with certain other organisations.

IMPORTANT DEFINITIONS Cont’d

Definition of trust money

Trust money means:

a. Money or other property entrusted to an estate agent in his or her capacity

as an estate agent;

b. Money collected or received by an estate agent and payable in respect of or

on account of estate agent activities as defined

c. Any other moneys, including insurance premiums, collected or received by

an estate agent and payable in respect of any immovable property.

SCOPE OF AUDITS FOR ESTATE AGENTS Section 29(a) of EAAA Every estate agent shall keep such accounting records as are necessary, fairly to reflect and explain the state of affairs: of all monies received or expended, including monies deposited to the trust account or interest-bearing account; of all assets and liabilities; and of all financial transactions and the financial position of the business. Section 29(b) of EAAA Such accounting records referred to in 29(a) must be audited by an auditor…. Section 32(5) of EAAA EAAB may, on good cause, at any time order any estate agent by notice in writing to submit to EAAB within a period stated in such notice, but not less than 30 days, an audited statement fully setting out the state of affairs in respect of the matters referred to in section 29(a)

AUDITORS REPORTING RESPONSIBILITIES Section 29(b) of EAAA …must be audited by an auditor within four months after the final date of the financial year of the estate agent. Section 32(4) of EAAA Any auditor who does an audit, shall forthwith after completing such audit, transmit to EAAB a report in the form from time to time determined by the EAAB, in regard to his findings, and a copy thereof to the relevant estate agent. The format of the auditor’s report is available on the IRBA website.

STRUCTURE OF THE AUDITOR’S REPORT

INTRODUCTION OF THE REPORT

The introduction includes the following information:

An engagement was completed on the trust accounting records; the

conclusion and any instances of non-compliance are reported under

section A of the report.

An audit of the financial statements was conducted in accordance with

ISAs. The following information relating to the audit is stated:

• The date of the auditor’s report.

• The type of audit opinion expressed.

• Financial reporting framework applied.

Auditor’s and estate agent’s responsibilities in terms of the trust

accounting records.

STRUCTURE OF THE AUDITOR’S REPORT Cont’d SECTION A Section A of the report includes: A summary of work performed by the auditor regarding sections 32(1), 32(2), 32(3)(a)-(c). A conclusion that the trust accounting records were maintained in compliance with above sections. If applicable, contraventions are described per section of the Act. SECTION B Section B of the report includes the auditor’s procedures and findings relating to additional compliance requirements applicable to the estate agent: Fidelity Fund Certificates (FFC) Registration with FIC and the requirements of section 28 of FICA It also includes a statement whether Reportable Irregularities have been reported.

STRUCTURE OF THE AUDITOR’S REPORT Cont’d SECTION C Section C of the report includes information extracted from accounting records: Disclosure of interest earned Interest received agreed to IT3b certificates

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS SECTION 32(1) Estate agents are obliged to open and keep at least one trust account, properly designated with the bank as a trust account opened in terms of section 32(1). Designation e.g.: ABC trust accounts in terms of section 32(1) of the EAA Act, 112 of 1976 SECTION 32(2) Estate agents are permitted to open separate savings or interest-bearing accounts when trust monies received will not immediately be required for any particular purpose. Such accounts must contain reference to S32(2). Designation e.g.: ABC trust accounts in terms of section 32(2) of the EAA Act, 112 of 1976

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS

SECTION 32(3)

Every estate agent shall -

a) keep separate accounting records of all monies

• deposited in the trust account

• Invested in any savings or other interest-bearing account

b) balance these books and records at intervals of not more than one

month, and cause them to be audited.

c) administer the accounts in the prescribed manner.SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS SECTION 32(2)(e) Estate agents must retain trust monies in the trust account until they either: become lawfully entitled to that money; or are lawfully instructed to release such trust money. Trust monies are sacrosanct as they are not the property of the estate agent but the property of another party. Trust monies must always be fully protected.

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS SECTION 26 To act as an estate agent a valid FFC is required. For estate agents registered as: a company this applies to every director. a close corporation this applies to every member who is competent and entitled to run the business and manage the corporation.

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS Sections 32(2)(c) and (d) In practice the estate agent must pay 50% of the interest earned on trust money to the Estate Agents Fidelity Fund (EAFF). • Unless an express written mandate indicates how the interest should be dealt with. Regulation 9.2 of the Code of Conduct for Estate Agents – require disclosure to the parties that the interest will accrue in favour of the EAFF in the absence of a express written mandate. A prior arrangement should always be made with the bank to debit bank charges in respect of the trust bank account directly to the business bank account and not to the trust account. (refer to case law)

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS Financial Intelligence Centre (FIC) Responsibilities Schedule I of the FIC Act (FICA) Estate agents are listed in as accountable institutions. Schedule II of the FICA The EAAB is a supervisory body who supervises estate agent’s compliance with the provisions of FICA. Duties of estate agents: Register as an accountable institution. Establish and verify the identity of clients, based on the risk-based approach. Report: cash transactions above prescribed limit; suspicious or unusual transactions; terrorist property reports

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS FIC Responsibilities Duties of estate agents cont’d: Keep record of clients and transactions. Develop, document, maintain and implement a Risk Management and Compliance Programme (RMCP). Train staff to enable them to comply with the FICA. Have a compliance function or appoint a person responsible for ensuring compliance with FICA and the RMCP. Duties of the auditor: As part of the auditor’s report submitted to the EAAB, confirm that: The estate agent is registered with the FIC as an accountable institution. The estate agent reported cash transactions above the prescribed limit to FIC.

SPECIFIC FOCUS AREAS DURING ESTATE AGENTS AUDITS Debt Collectors Act (DCA) Responsibilities The definition of a debt collector includes the functions of an estate agent when arrear rent or levies are collected. The Council for Debt Collectors (the Council) confirmed the following: a. The estate agent will be allowed to use their trust bank accounts opened in terms of the EAAA to register with the Council. b. The Council will accept the auditor’s report that is issued to the EAAB as compliance with section 20 of the DCA. c. The DCA requirement to pay over the interest earned on the trust bank account to the Council will not be enforced.

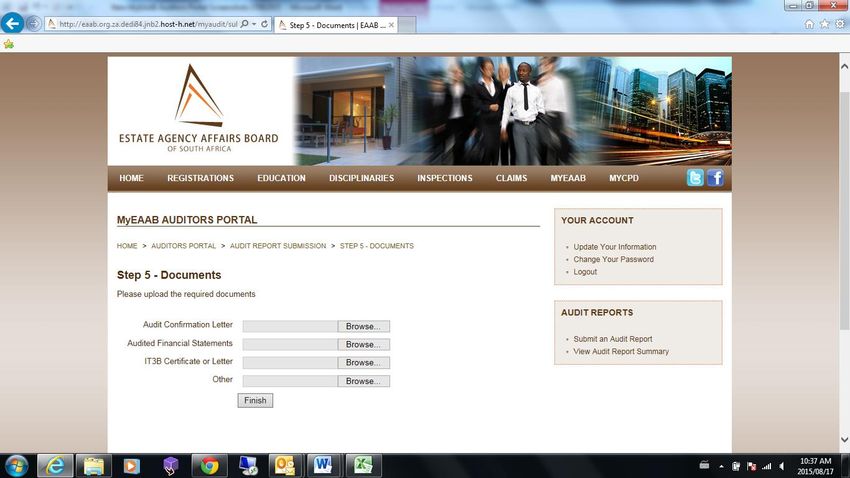

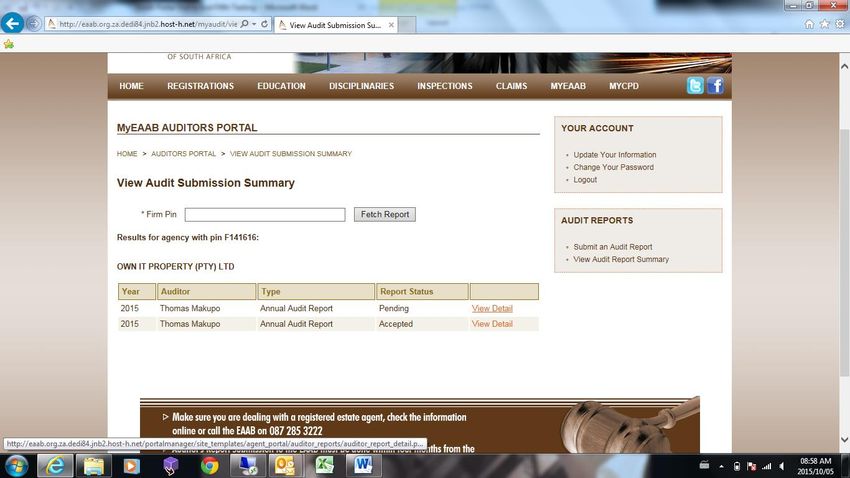

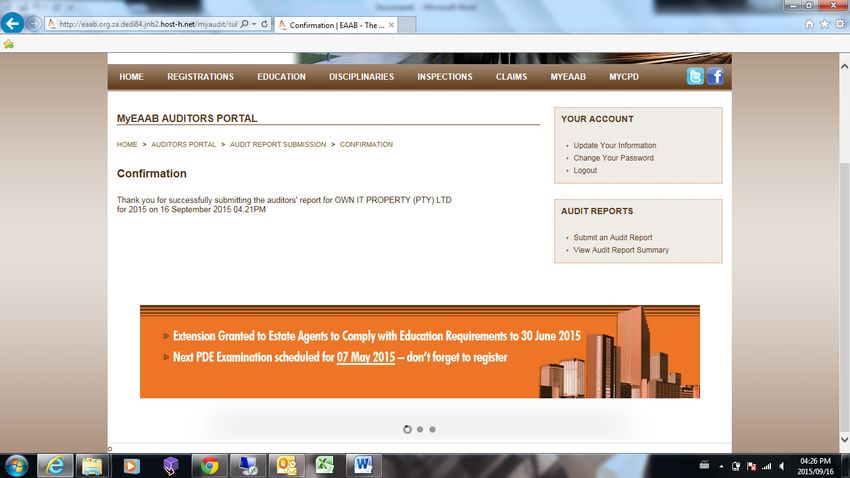

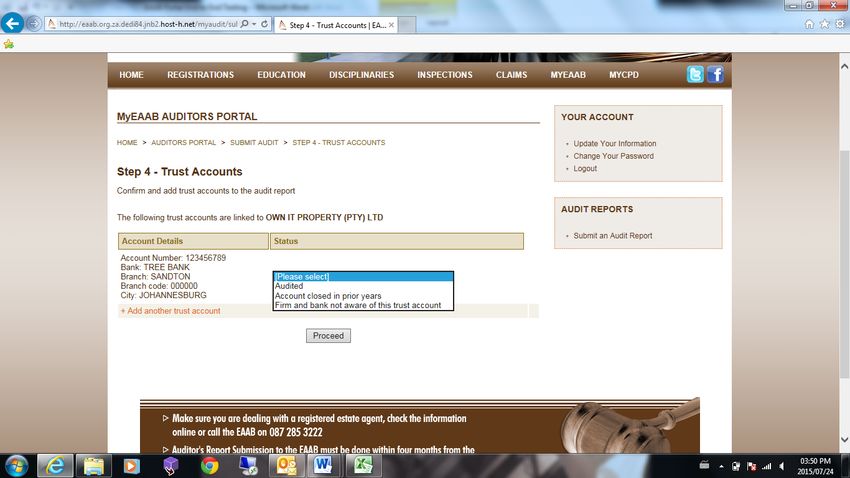

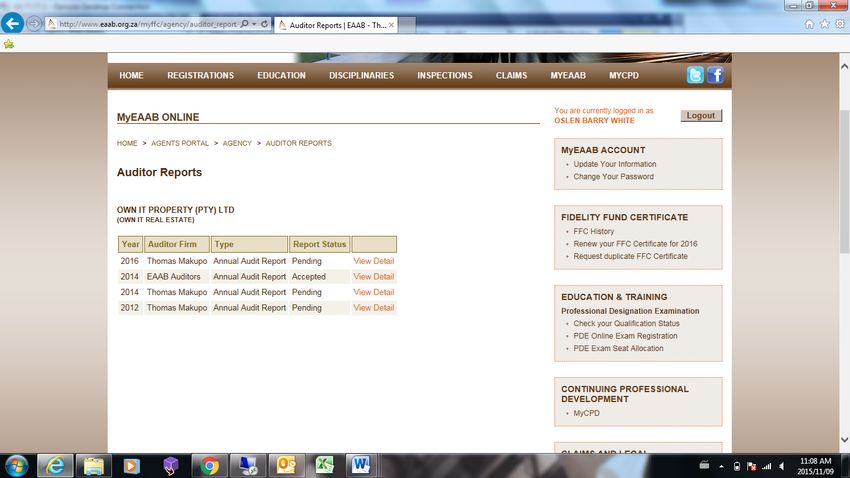

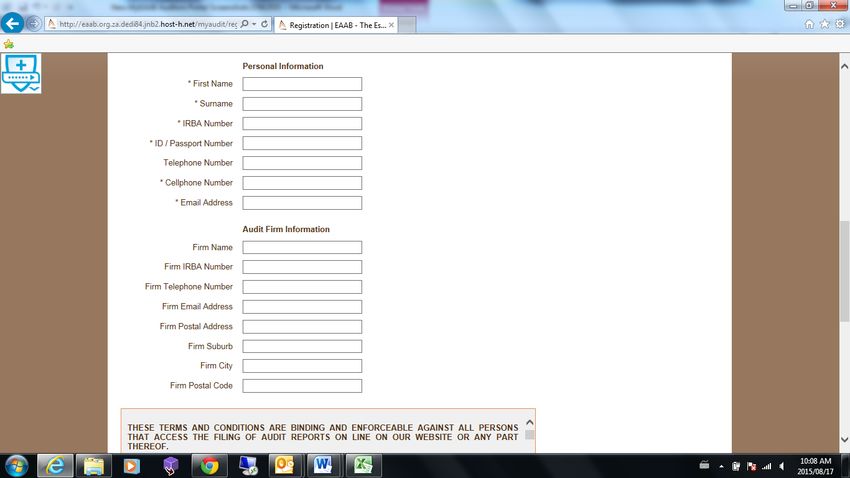

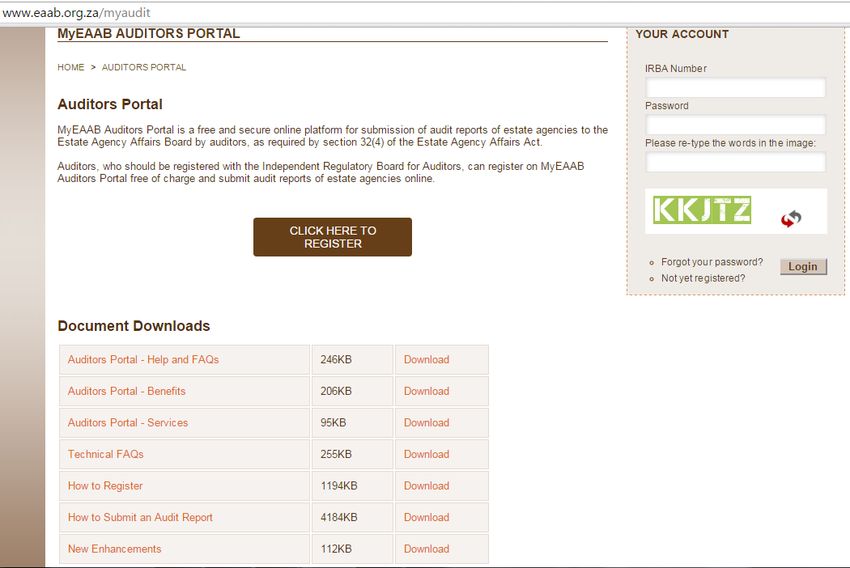

MYEAAB AUDITORS PORTAL

MYEAAB AUDITORS PORTAL Cont’d

Cont’dMYEAAB AUDITORS PORTAL Cont’d

MYEAAB AUDITORS PORTAL Cont’d

MYEAAB AUDITORS PORTAL Cont’d

MYEAAB AUDITORS PORTAL Cont’d

MYEAAB AUDITORS PORTAL Cont’d

MYEAAB AUDITORS PORTAL Cont’d

MYEAAB AUDITORS PORTAL Cont’d

CONSEQUENCES OF LATE AUDIT REPORT SUBMISSIONS

In terms of section 27 and section 16(4) the estate agent will automatically

be disqualified and the FFC will be withdrawn

Options available to the estate agent:

• Make a section 27 application for reinstatement by:

o Admitting non-compliance and indicating willingness to pay a

penalty/fine; or

o Contesting non-compliance and requesting to appear before a

Disciplinary Committee to make representations

• Deregister and wind up the estate agency businessCONSEQUENCES OF LATE AUDIT REPORT SUBMISSIONS

Documents required for reinstatement if set conditions are met:

• Submission of outstanding audit report

• Audited financial statements/ Confirmation of turnover

• Affidavit from principal:

Reasons for non-compliance;

Reasons why it should be considered in the interest of justice to

issue an FFC

History and experience in the estate agency industryCONSEQUENCES OF AUDIT FINDINGS IN SUBMITTED AUDIT REPORTS

Types of findings that are being reported:

Section 32 contraventions; FIC contraventions; modified opinions on the

financial statements; and other administrative findings

Consequences of Section 32 and FIC Contraventions

The estate agent’s principal will be requested to respond within 30 days.

A legal case is opened for each contravention.

After considering the response a decision is made whether to proceed with

a disciplinary hearing by an independent Disciplinary Committee.

Sanctions range from:

Withdrawal of FFC;

Fine of up to R25 000 per charge;

ReprimandCONSEQUENCES OF AUDIT FINDINGS IN SUBMITTED AUDIT REPORTS

Audit Opinions – Adverse, Qualified or Disclaimer

The principal of the estate agent is requested to provide the financial

statements within 30 days.

The basis for modified opinion is analysed in conjunction with auditors

comments.

If the basis for modified opinion indicates possible contravention of the

EAAA and FIC, particularly section 29(a); the matter will follow the same

process described on the previous slide.

Other administrative audit findings

Year-end selected by auditor does not match what is on EAAB’s records

New trust accounts audited but not on EAAB’s records

Trust accounts closed but EAAB not notified

Trust accounts on EAAB’s records not known by the bank or firm

Estate Agency type selected by auditor does not match what is on EAAB’s

recordsWINDING UP OF ESTATE AGENCY BUSINESS Section 32(7) Circumstances when winding up the estate agent's trust, savings or other interest-bearing accounts are required: The EAAB did not issue an FFC to the estate agent The EAAB withdrew an FFC issued to the estate agent The estate agent ceases to act as such The estate agent becomes subject to any disqualification referred to in section 27, The winding up of these accounts and paying out the amounts, should be done in the prescribed manner, described in the slide that follows.

WINDING UP OF ESTATE AGENCY BUSINESS Cont’d

Prescribed manner of winding up an estate agency business:

1. No moneys shall be withdrawn from, or paid out of the trust accounts without

EAAB’s consent in writing.

2. The estate agent concerned shall:

a. Notify EAAB immediately in writing.

b. Notify the bank immediately in writing that no moneys may be withdrawn

or paid out without EAAB’s written consent.

c. Furnish EAAB in writing with list of trust creditors, including amounts and

reasons.

d. Pay the trust creditors only with the written consent of EAAB.

e. Be entitled to any remaining balance, after the EAAB published a notice

inviting persons to lodge any claims within a 30 day period.

f. Close the trust account and notify the EAAB in writing.WINDING UP OF ESTATE AGENCY BUSINESS Cont’d Section 32(8) The effect of section 32(8) on an estate agent that is being liquidated, or is insolvent or deceased (in the case of a sole proprietor are as follows: Company or close corporation placed under liquidation The trust bank accounts and trust accounting records of the liquidated company or close corporation will not fall under the authority of the liquidator. Dissolution of a partnership The trust bank balances can not be distributed to the individual partners on dissolution of the partnership

WINDING UP OF ESTATE AGENCY BUSINESS Cont’d Section 32(8) Insolvent Sole Proprietor The trust bank accounts and trust accounting records of the liquidated company will not fall under the authority of the trustees. Deceased Sole Proprietor The trust bank accounts and trust accounting records of the liquidated company will not fall under the authority of the executor. The trust accounts have to be wound up in the prescribed manner as described in the previous slides.

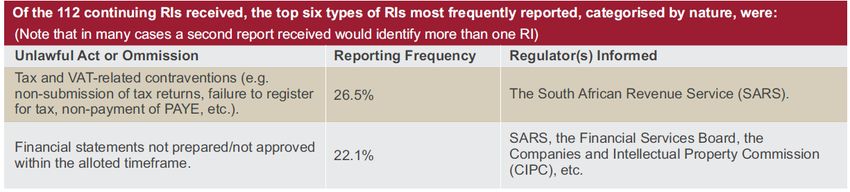

IRBA INESPECTION FINDINGS ON AUDITS OF TRUST ACCOUNTS Reportable Irregularities (Source: IRBA December 2017 Newsletter)

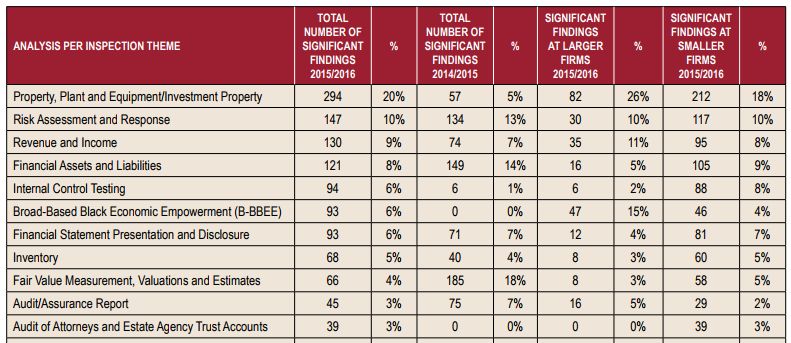

IRBA INESPECTION FINDINGS ON AUDITS OF TRUST ACCOUNTS Inspection findings (Source: IRBA 2016 Public Inspections Report )

IRBA INESPECTION FINDINGS ON AUDITS OF TRUST ACCOUNTS Inspection findings (Source: IRBA 2016 Public Inspections Report )

STATISTICS ON SUBMITTED AUDIT REPORTS AND CONTRAVENTIONS

STATISTICS ON SUBMITTED AUDIT REPORTS AND CONTRAVENTIONS

583 871

656

353 518

338

244 311 334

205 281

136

2015 2016 2017

2015 2016 2017

Section 32(1) Section 32(2) Section 32(3) Reportable Irregularities

3 426

1 895 1 896

132 87

9

2015 2016 2017

FIC registration Cash transactions reportingPROPERTY PRACTITIONERS BILL – STATUS UPDATE The Bill was published in the Government Gazette for public comment on 31 March 2017 The deadline for sending written comments to the Department of Human Settlements was on 18 May 2017 Public participation meetings were held in all provinces thereafter The changes were incorporated in July 2017 The Bill was approved by Cabinet in December 2017 for introduction in the National Assembly

ACCESS TO INFORMATION RELATING TO ESTATE AGENTS MyEAAB Auditors Portal https://www.eaab.org.za/myaudit IRBA Website https://www.irba.co.za/guidance-to-ras/industry- specific-guides-and-regulatory-reports/estate-agents- trust-account-report SAICA Website https://www.saica.co.za/Technical/Assurance/AuditofEst ateAgents/tabid/534/language/en-ZA/Default.aspx EAAB Audit Compliance Department audit@eaab.org.za

Thank you

You can also read