Airbnb Poised to Rally as Travel Bookings Accelerate in U.S. and U.K. in 2021 - Gary Scott

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ENR Advisory Extra Report April 2021 Recent Decline in Stock Price is a Buying Opportunity as Americans Travel Again Airbnb Poised to Rally as Travel Bookings Accelerate in U.S. and U.K. in 2021 In 2007, a cash-strapped Brian Chesky came up with a shrewd way to pay his $1,200 San Francisco apartment rent. He would offer “Air bed and breakfast”, which consisted of three airbeds, breakfast, WiFi and a desk to work, to attendees of the Industrial Design Conference, who needed a place to crash over the weekend. To fund this venture, the Mr. Chesky and his two co-founders created special presidential- themed breakfast cereals. They sold 800 of these boxes at $40 each in two months. Afterwards, they used their $30,000 in profits to start Airbnb, Inc. (NASDAQ-ABNB). After an initial period of uncertainty, the company received $20,000 in seed funding from Y Combinator and Sequoia Capital. The next year, it ran a Series A round which generated $7.2 million for the start-up. Well, the rest as they say, “is history.” The company continued to raise capital and its valuation soared. On December 9, 2020, Airbnb went public on the NASDAQ, surging 113% on the first day of trading and giving the company stock market valuation of $47 billion. The Airbnb website operates as an online marketplace for people who are looking for accommodations. Airbnb connects travelers with Airbnb hosts who want to rent out their homes or other property. For guests, Airbnb gives affordable temporary housing options and sometimes fun activities. For hosts, Airbnb is a way to earn extra money. I made my first Airbnb rental reservation last week for a trip to Miami next February; after a 13-month pandemic-induced hibernation at home in Montreal and a curfew since January, I needed to plan a long overdue holiday. I booked a beautiful downtown Miami apartment – far less expensive than a five-star hotel. I’ve already had numerous discussions with the host of the unit, and I’m pleased with the level of communication and price. ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

ENR ADVISORY EXTRA BULLETIN 2 Airbnb has grown at a remarkable compounded rate of 153% from 2009 to 2019. Airbnb makes money by acting as the middleman between renters and Airbnb guests. Every time an Airbnb guest books the host’s property, the Airbnb host pays Airbnb a fee. Airbnb also adds service fees depending on the total cost of the guest’s stay. Airbnb quickly attracted the attention of other companies, including investors. One year after its official launch, the San Francisco-based company had over 2,500 listings and 10,000 Airbnb users. The firm became instantly popular in Germany in 2011, serving as its launchpad for international users. In 2015, Airbnb was the official supplier for the alternative accommodation services for the Rio Olympic Games. For the past three years, Airbnb has consolidated its position in the market. It acquired Luxury Retreats in 2017 for $200 million, followed by a $400 million acquisition of Hotel Tonight in 2019. Even with these acquisitions, it is still considered a rather “light” asset company in comparison to its main rivals, Expedia (NASDAQ-EXPE) and Bookings.com. (NASDAQ-BKNG). As of March 29, 2021, the company fetches a $106.1 billion market capitalization. Though it lost money in 2020, management believes it will turn profitable in 2022 or sooner. Airbnb suffered a big hit after Covid-19 hit last year. At the pandemic peak, new bookings crashed 85%, although app usage has gradually increased as countries have relaxed travel restrictions. Despite a $4 billion loss in the fourth quarter, Airbnb posted revenue, bookings and room-night growth that beat expectations. Countries with the most listings in Airbnb include the United States (660,000), France (485,000), Italy (340,000), Spain (245,000) and the United Kingdom (175,000), according to iProperty Management. And according to Stratosjet.com, the most popular cities for Airbnb rentals are Kissimmee, Florida; New York City; Los Angeles; Davenport, Florida; San Diego; Atlanta; Miami; Panama Beach, Florida; Austin, Texas; and Las Vegas. The most popular international Airbnb city is Vancouver. Covid-19 Variant Risks Airbnb should lead the travel recovery theme in 2021. U.S. domestic air travel is already almost at a pre- pandemic peak as Americans hit the skies again with more than 1.5 million passengers clearing U.S. airports on March 28, according to TSA. But a surge in infections of new Covid-19 variants across Europe has resulted in renewed economic shutdowns. Markets worldwide have taken note; stocks and commodities are wobbling over the past week while bond yields have declined after a big spike this past winter. And the U.S. dollar, usually vulnerable amid a cyclical recovery, has rallied 4% off its multi-year low in January. As a result, the travel recovery theme has declined about 10% to 15% over the past three weeks; airlines, hotels and cruise lines are all off from post-March 2020 highs. I am hopeful the global economic recovery will not be derailed by Covid-19 variants. Thus far, there are no meaningful signs of spikes in infections in the United States, despite recent clusters of March break parties in South Texas and South Florida. Second, continental Europe has lagged far behind the United Kingdom and the United States in mass inoculations. Over 40 vaccines per 100 people have been administered in the U.K. and the U.S. In France and Italy, it is 14 while barely 10 in Canada. However, if ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

ENR ADVISORY EXTRA BULLETIN 3 we study the resultant reopening in Israel recently, there is certainly hope for an economic recovery for most advanced economies later in 2021 and 2022 once more vaccine supplies are delivered. Almost half of all Israelis have received their first shot of Pfizer-BioNTech; confirmed Covid-19 infections are literally falling to zero while very few cases of variants have surfaced. Let’s face it: People are fed up with Covid-19. We are all fatigued. I have been extolling the arrival of the biggest travel boom since 9-11. Travel focused investors have already missed the boat in the United States and the United Kingdom with huge gains recorded in MGM Resorts International (current open position in our portfolio since last November, +75%) and most other hotels, airlines, and cruise lines. But Airbnb is not priced for a massive travel recovery in the United States this summer and fall. Bookings are up, people are flocking to travel sites; Airbnb has said visits to its website have soared in recent weeks. And some 61% of 2,200 Americans surveyed by Expedia Group Inc. said they were likely to make a long-distance trip in the next year. Airbnb is poised to record big revenue gains as vacationer’s book longer stays after suffering from ‘cabin fever’ for the past year, mainly in the United States. Summer peak travel season is upon us. It is time to book a stay. BUY Airbnb, Inc. (NASDAQ-ABNB) at market up to $199. ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

ENR ADVISORY EXTRA BULLETIN 4 Inflation-Nation Ahead? Adjusted for inflation, average weekly earnings for production and nonsupervisory workers peaked in the early 1970s. But markets have grown increasingly obsessed with inflation as break-even rates on TIPS, commodities and massive U.S. fiscal deficits portend to a new secular period of rising prices. I am not convinced. At least not yet. We need to see a significant increase in wages first. There remains a lot of slack or unused capacity in the world economy. U.S. factory capacity utilization sits at just 71% -- significantly below the five-year average of 75.4% recorded from 2015 to 2019; the United States and the rest of the world have yet to replace the tens of millions of jobs lost after March 2020. It is hard to see a big spike in inflation without job gains, rising real wages and a concerted global economic recovery. Unlike the rampant inflation of the 1970s, there is one major critical difference today compared to the high inflation period more than forty years ago: China and other manufacturing countries. The rapid industrialization of China since 1978 and other emerging markets since the late 1980s have created a phenomenon in pricing called disinflation or in some cases, deflation. China was not a major economic powerhouse in the 1970s and certainly not a major exporter to the world. The advent and acceleration of Chinese exports has resulted in a deflationary environment for goods the last 20 years. You could say, for example, that technology is deflationary because it makes jobs increasingly redundant, lowers workers’ compensation and leads to more productivity. ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

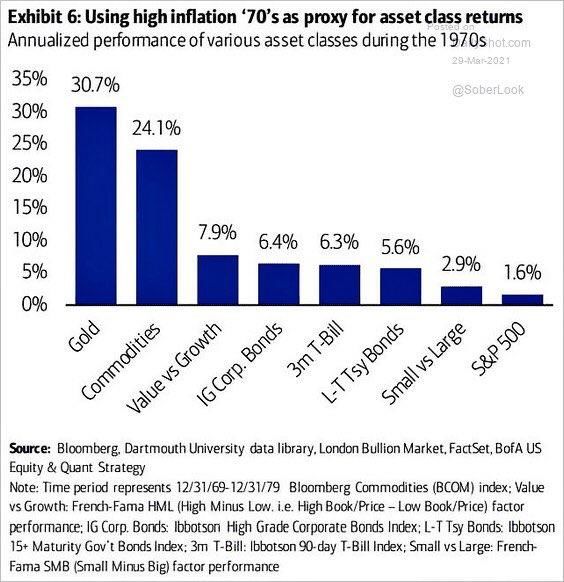

ENR ADVISORY EXTRA BULLETIN 5 Inflation, of course, is everywhere outside of the official government consumer price index (CPI). College tuition, healthcare costs, home construction and purchase prices, most services and big-ticket items are always rising. About the only things not increasing are consumer electronics. It makes you wonder what planet the government is living on when they report a CPI, excluding food and energy. How does someone live without food and energy? If inflation makes a big advance, we can look to the 1970s as a reference point for asset allocation. Please see chart on page 4, courtesy of Liz Ann Sonders at Charles Schwab. This capsule is a nominal return survey, not adjusted for inflation. The returns are much less after inflation. In the 1970s, U.S. annual inflation averaged 6.8%, double the long-term average. No surprise that gold and commodities dominated the performance in the ‘70s amid a plunging dollar following Nixon’s termination in 1971 of Bretton Woods (dollar convertibility to gold), soaring deficits largely due to the Vietnam War and LBJ’s Great Society programs. I did, however, find it interesting how value-based equities outpaced growth stocks that decade by a considerable margin. But after inflation of almost 7% per annum in 1970s, an investor lost real purchasing power in everything else, especially bonds, cash, the S&P 500 Index, and small stocks. One asset class not reviewed on page 4 is U.S. residential real estate, which surged a nominal 172% from Q4 1969 ($27,100 = average home price) to Q1 1980 ($73,600), according to the St. Louis Fed. Residential housing outpaced other major asset classes in the 1970s after inflation, except gold and commodities. As for an ideal inflation hedge, I stand by gold bullion. Gold’s recent price action amid rising fears of inflation this year remains an enigma; many inflation sensitive assets have rallied. Bullion is down a cumulative 19% since hitting an all-time high last summer. More than any single variable – outside of market manipulation – the gold price might be falling because the dollar has recovered sharply over the past six weeks. Rising rates do not necessarily hurt gold; I find that to be a poor excuse for declining gold ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

ENR ADVISORY EXTRA BULLETIN 6 prices. In the late 1970s, U.S. interest rates went through the roof before topping out above 20%, and yet gold blasted higher to $850 an ounce. Rates are simply too low to make a serious dent to gold prices. If we have a real acceleration in inflation, gold prices will skyrocket. Furthermore, the unprecedented size of U.S. fiscal deficits is a serious cause for concern. It is the same with the ECB, Bank of Canada, Bank of England, Bank of Japan etc. If you are a dollar-based investor, the threat of inflation is real because the Fed will continue to monetize a larger percentage of Treasury debt issuance. As deficits grow, the Fed will absorb what is necessary. The Biden administration is a strong proponent of Modern Monetary Theory (MMT), which advocates spend, tax, and borrow in a fiat currency controlled by the government, believing it is not financially constrained by money-printing limitations. I highly disagree. I think we have started a new chapter on government spending, and it will ultimately end badly with inflation and a devalued dollar. Buy gold as a hedge against government profligacy. ENR Advisory Portfolio Value Trounces Growth in 2021 As of March 30, the MSCI World Index has gained 4.5% in 2021 and the S&P 500 Index is up 5.7%. The first quarter will likely be a strong three-month period for most risk assets, except fixed-income securities, precious metals, foreign currencies, and growth stocks, including Big Tech. Value-based equities in the United States outpaced growth stocks by the widest margin in decades in the first quarter with the Vanguard Value ETF (NYSE-VTV) rising 11% compared to a 0.6% gain for the Vanguard Growth ETF (VUG). Market leaders Apple, Inc. (-10%), Amazon.com (-7%) and Tesla (-13%) have pulled back over the past 90 days. ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

ENR ADVISORY EXTRA BULLETIN 7 Market leadership continues to favor economic recovery stocks like cyclicals, industrials, financials, and materials. The energy sector, last year’s biggest loser, has surged 31% this year. Dow Theory has also turned bullish again. The Dow Jones Transportation Average has repeatedly hit fresh all-time high lately and is up over 16% in 2021 while the Dow Jones Industrials does the same. When both averages are hitting new highs, that is a positive sign for the economy and the market. In USD terms, the S&P 500 Index is dominant in 2021. Non-U.S. markets have retraced some of their gains over the past several weeks amid dollar strength. The MSCI EAFE Index (major markets, ex. USA) has rallied 3.3% this year and the MSCI Emerging Markets Index is up 1.5%. The top performing markets in dollar terms include Chile (+14%), South Africa (+11.4%), Taiwan (+10%), Singapore (+9.7%), and Canada (+8.5%). It is no surprise that most of this year’s leading bourses are natural resource-based economies. The ENR Advisory Extra Portfolio posted mixed results since our last update with most non-U.S. stock ETFs, financials and industrials posting gains but technology stocks correcting sharply, especially Chinese tech companies. In March, Chinese technology shares dropped sharply on growing concerns of possible de-listings from U.S. exchanges and reported plans by Beijing to take control of companies’ user data. The S&P/BNY Mellon China Select ADR Index that tracks 48 major U.S.-listed Chinese companies is 23% below its record on February 16. In addition to facing more scrutiny at home, investors have rotated out of growth stocks and into value shares in 2021. We hold two tech-focused Chinese securities in the model portfolio. The Invesco China Technology ETF plunged 17.5% since our last update and Alibaba Group Holdings has dropped 6%. Sell CQQQ or the Invesco China Technology ETF. Also this month, we are selling the CurrencyShares Japanese Yen ETF, down more than 6% this year as the dollar hits a 12-month high vis-à-vis the yen. In April, we are buying Airbnb, Inc. (NASDAQ-ABNB) up to $199. More Americans are traveling this spring whether by air or automobile. That trend will continue to gain traction as more people are vaccinated and warmer weather arrives. Airbnb is a great long-term growth story at this price following a correction in the IPO price last December. Other travel-related names have also pulled back, including Melia Hotels International (Madrid-MCE). Spain will recover and see a boom in travel later this year and into 2022. Melia is cheap. 2MX Organic SA, a SPAC traded in Paris and headed by three experienced French entrepreneurs, is down 10% from my first buy recommendation in February. The EUR has also declined. SPACs, in general, have consolidated heavily in the United States since early March amid a risk-off environment and rising bond yields. I remain bullish on 2MX because it is managed by successful French businessmen specializing in food and retail. Management seeks to buy and grow organic food distribution centers across Europe. This European SPAC has about €300 million in cash awaiting to make a deal with one or more companies in the European organic foods sector. BUY up to €11.25. ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.com

ENR ADVISORY EXTRA BULLETIN 8

The travel recovery theme has rallied hard over the past several weeks as more vaccines roll-out,

especially in the United States and UK. Airlines, cruise lines, hotels and restaurants have gained

considerably. In Europe, hotels and airlines have also posted big gains; our open position in Spain’s

Melia Hotels has rallied almost 25%. And Boeing Co., which I consider a ‘recovery play’ on travel, is up

almost 10% since January 5th. The best of the bunch is MGM Resorts International, up 77% since

November 3rd. I am placing this theme on HOLD until a new buying opportunity emerges.

What’s Included in This Service

As part of the ENR Advisory Extra package, you are entitled to the following services. We highly

recommend our clients take advantage of these services to better implement your long-term investment

goals and risk objectives:

• Quarterly portfolio/account review

• Portfolio planning and future projections

• Automatic portfolio rebalancing

• Tax-loss harvesting advice

Please call our office in Montreal and make an appointment with Eric. Telephone (Toll-Free) 1 877 989

8027 or email Dugald Malcolm at dugald@enrasset.com.

------------------------------------------------------------------------------------------------------------------------

Eric N Roseman

Montréal, Canada

March 30, 2021

ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada

Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.comENR ADVISORY EXTRA BULLETIN 9

Entry Current Current Gain/

Security Listed Symbol Date Advice

Price Yield Price Loss

Airbnb NASDAQ ABNB $174.40 Mar 26/21 0.00% $174.40 NEW BUY

Iberdrola Madrid IBE € 10.40 Mar 1/21 3.83% € 10.98 3.42% BUY

2MX Organic Paris 2MX € 10.70 Feb 8/21 0.00% € 9.90 -9.48% BUY

Meliá Hotels

MCE MEL € 5.57 Jan 5/21 0.00% € 6.34 9.24% BUY

International

WisdomTree

Chinese Yuan NYSE CYB $26.10 Oct 1/20 0.41% $27.20 4.64% BUY

Strategy Fund

Morgan Stanley

Global Franchise NASDAQ MSGFX $25.34 Jun 4/19 0.00% $30.33 19.69% BUY

Portfolio C*

Gold Bullion Unlisted N/A $1,492.47 Jan 4/16 0.00% $1,732.52 16.08% BUY

Invesco China

NYSE CQQQ $54.99 Mar 2/20 0.41% $81.25 48.46% SELL

Technology ETF

CurrencyShares

NYSE FXY $88.45 Sep 6/16 0.00% $86.00 -2.77% SELL

Japanese Yen ETF*

MercadoLibre NASDAQ MELI $297.43 Jul 4/18 0.00% $1,431.97 381.45% HOLD

Microsoft Corp. NASDAQ MSFT $101.27 Dec 21/18 0.90% $236.48 138.50% HOLD

Berkshire

NYSE BRK.B $125.79 Feb 9/16 0.00% $256.77 104.13% HOLD

Hathaway Class B*

Target Corp. NYSE TGT $107.91 May 1/20 1.34% $200.95 88.72% HOLD

MGM Resorts

NYSE MGM $21.52 Nov 3/20 0.03% $37.68 75.11% HOLD

International*

B2Gold Corp. NYSE BTG $2.73 May 30/18 3.07% $4.56 72.16% HOLD

iShares Currency

NYSE HEWJ $24.65 Sep 6/16 1.15% $39.46 69.02% HOLD

Hedged MSCI Japan

iShares MSCI South

NYSE EWY $59.31 Jul 2/19 0.71% $89.14 53.56% HOLD

Korea Capped ETF

Silver Bullion Unlisted N/A $16.46 Jul 30/19 0.00% $25.06 52.25% HOLD

Euronet

NASDAQ EEFT $94.20 Aug 3/20 0.00% $140.91 49.59% HOLD

Worldwide, Inc.

Vanguard FTSE

NYSE VWO $38.28 Dec 21/18 1.82% $51.90 42.69% HOLD

Emerging Markets

SPDR S&P Global

Natural Resources NYSE GNR $36.35 Jun 29/20 2.54% $50.93 42.21% HOLD

ETF

iShares MSCI

Global Gold Miners NASDAQ RING $22.01 Jul 30/19 0.95% $27.57 26.62% HOLD

ETF

Groupe Bruxelles

BSE GBLB € 77.04 Jun 4/20 2.83% € 88.20 19.87% HOLD

Lambert

Credit Suisse

NYSE CS $10.98 Sep 2/20 2.32% $12.87 18.60% HOLD

Group AG

The Boeing

NYSE BA $208.38 Jan 5/21 0.84% $244.87 17.51% HOLD

Company

Alibaba Group

NYSE BABA $194.57 May 1/20 0.00% $227.26 16.80% HOLD

Holdings*

ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada

Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.comENR ADVISORY EXTRA BULLETIN 10

Cambria Tail Risk CBOE

TAIL $20.66 Dec 4/20 0.37% $18.91 -8.41% HOLD

ETF BZX

Risk Disclaimer: The financial information provided in this Bulletin is accurate at the time of publication to the best of ENR’s knowledge. Recipients are advised that the

financial data provided is subject to constant change. Recipients are also made aware that investments in single stocks and bonds are a high-risk pursuit that could

result in a high or even total loss of invested capital. Investments in foreign currencies and securities should also be considered a high-risk venture, as the currency

might drop in value compared to the US dollar and political, or country-specific factors, might endanger the liquidity and/or value of the security. Investing in securities

has definite tax consequences, some of which may be dependent on a security’s type, its country of issue or the form of its income streams. ENR does not provide legal or

tax advice nor accepts any such liability. Clients should always consult a professional regarding specific legal or tax matters. *ENR or its employees or its access persons

own shares of Berkshire Hathaway Class B, MGM Resorts International, 2MX Organic SA, Boeing Co., and Morgan Stanley Global Franchise Portfolio C.

ENR Asset Management Inc. • 1 Westmount Square, Suite 380 • Westmount, Quebec • H3Z 2P9 Canada

Phone 1-514-989-8027 • Fax 1-514-989-7060 • Toll free 1-877-989-8027 • www.enrassetmanagement.comYou can also read